[ad_1]

Former President Donald Trump unveiled Thursday a “limited edition collection” of NFT trading cards featuring cartoon-like images of himself depicted as a superhero, Hollywood actor and more.

[ad_2]

[ad_1]

Former President Donald Trump unveiled Thursday a “limited edition collection” of NFT trading cards featuring cartoon-like images of himself depicted as a superhero, Hollywood actor and more.

[ad_2]

[ad_1]

Sam Bankman-Fried has been remanded in Bahamian custody until February, a day after he was arrested at a luxury apartment in the Bahamas.

[ad_2]

[ad_1]

This is an opinion editorial by Pierre Rochard, the Vice President of Research at Riot.

Ben Sixsmith has published a thoughtful piece in The Spectator entitled “Saying Goodbye To The Crypto Nerd Utopia,” providing an outside perspective on the crisis facing the broader crypto economy.

While there’s a lot I agree and disagree with in his piece, I’ll focus on the primary line of reasoning: Bitcoin is one of many cryptocurrencies, cryptocurrencies have no intrinsic value, and cryptocurrencies are speculatively traded on exchanges like FTX; therefore, the scandalous collapse of FTX reveals that Bitcoin is no better than the status quo.

The first paragraph in Sixsmith’s piece establishes the conflation of Bitcoin and crypto: “The value of Bitcoin, Ethereum and Luna crashed in May.”

At first glance, this assertion may seem uncontroversial, all three of these assets rely on cryptography and varying degrees of decentralization, and all three of these assets experienced sharp declines in trading prices on exchanges. On the other hand, if we look at their underlying open-source software, we see radical differences:

Putting all three of these assets into a single “crypto” bucket is reductive — they are different technologies optimizing for different outcomes. Bitcoin has accomplished long-term network stability — you could have run the same node software continuously for the past decade without any problems. The same cannot be said for Ethereum node software, which completely changed its consensus mechanism in September 2022. This change was only able to occur because the Ethereum Foundation has a unique centralized role in designating the official staking contract. Ethereum has to be more centralized than Bitcoin to push through aggressive “upgrades” to its protocol. Bitcoin has no such centralized operator or authority, and its consensus rules are unofficial: a spontaneous, inter-subjective, network-wide agreement among the users.

To address the second element in Sixsmith’s line of reasoning: the intrinsic value of holding any form of money is that you are minimizing uncertainty by hedging against unpredictable future cash flows. In the fiat system, the least-uncertain assets are physical cash and government-insured bank accounts; however, even those are subject to the fiat power of the governments issuing such currencies and insuring those bank accounts — that is, your money is only as good as the applicable government’s promises.

Setting aside Bitcoin’s exchange rate, on a fundamental engineering level, holding BTC with your own private keys and verifying the ledger with your own node results in less uncertainty than holding even physical cash or an insured bank account. That is bitcoin’s intrinsic value. While the spot price/purchasing power of BTC can be subject to the whims of market forces, the uncertainty-minimizing principles of how to receive, hold and send BTC have not changed since its inception. Thus, you can be certain that the smart contracts locking your BTC will execute as written, so that only a signature from your private keys can move your money.

The third element addressed in Sixsmith’s piece relates to the speculative trading of cryptocurrencies on exchanges. Exchanges operating in the United States are legal entities subject to U.S. laws governing exchanges and are subject to compliance with both state and federal money transmitter, custodian and investor protection regulations. They are regulated federally by the Commodity Futures Trading Commission, the U.S. Securities and Exchange Commission and/or the Financial Crimes Enforcement Network, and they have clear terms of service and user agreements. Even an “offshore” exchange in the Bahamas is accountable to the English Common Law. To label these entities as “crypto” exchanges obfuscates their centralized fiat nature.

Sixsmith states, “…we knew that crypto-currencies were not a surefire route to freedom and independence when their value hinged on the good sense and morals of a bunch of weird nerds online.”

While humorous, this statement conflates Bitcoin’s value with the (mis-)management of fiat/crypto exchanges; akin to questioning the value of tomatoes because a supermarket went bankrupt. Furthermore, there’s nothing inherent about BTC that would necessitate leaving it at a fiat exchange, vulnerable to theft. It is harder and riskier to properly secure and use an exchange account’s password than it is to do so with BTC private keys. Furthermore, there are bitcoin-only brokerages that encourage or require the delivery of BTC directly to the client’s keys. Countless individuals and businesses receive BTC not as a trade for fiat, but as revenue for goods and services. The continued development of a circular economy will lessen the need to ever exchange for fiat.

In conclusion, despite adjacent cryptocurrencies and fiat exchanges that are centralized and unreliable, Bitcoin is a decentralized and reliable alternative monetary system. Bitcoin’s vision for the future is not utopian or idealistic, rather it is simply looking at the past decade of successful adoption, noting that Bitcoin’s fundamental properties have only improved, and projecting out continued growth. Perhaps the bottleneck in Bitcoin’s adoption is peoples’ understanding of what differentiates Bitcoin from fiat and crypto.

This is a guest post by Pierre Rochard. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

[ad_2]

Pierre Rochard

Source link

[ad_1]

Before he was arrested Monday in the Bahamas, disgraced FTX founder and former CEO Sam Bankman-Fried was planning to testify before Congress on Tuesday about the dramatic collapse of his cryptocurrency exchange.

[ad_2]

[ad_1]

Sam Bankman-Fried, the founder of the collapsed FTX cryptocurrency exchange, has been arrested in The Bahamas after being criminally charged by prosecutors in the United States.

The 30-year-old was taken into custody in the Caribbean nation after US prosecutors notified them they had filed charges and planned to seek his extradition, the Office of the Attorney General of the Bahamas said in a statement on Monday.

The US has not elaborated on the nature of the charges.

FTX filed for Chapter 11 bankruptcy protection in the US last month.

Here is a history of FTX since it was set up in 2019:

May: Former Wall Street trader Sam Bankman-Fried and ex-Google employee Gary Wang found FTX, the owner and operator of cryptocurrency exchange FTX.COM.

July: FTX concludes a $900m funding round, which values the exchange at $18bn.

September: FTX signs a sponsorship deal with the Mercedes Formula 1 team.

October: FTX raises capital at a valuation of $25bn from investors, including Singapore’s Temasek and Tiger Global.

January 27: FTX’s US arm puts its valuation at $8bn after raising $400m in its first funding round from investors, including SoftBank Group and Temasek.

January 31: FTX raises $400m from investors, including SoftBank, at a valuation of $32bn.

June 4: FTX signs for naming rights for the home arena of basketball’s Miami Heat in a deal reportedly worth $135m.

July 1: FTX signs a deal with an option to buy embattled crypto lender BlockFi for as much as $240m.

July 22: FTX offers a partial bailout of bankrupt crypto lender Voyager Digital. Voyager calls it a “low-ball bid”.

August 19: A US bank regulator orders FTX to halt “false and misleading” claims it has made about whether funds at the company are insured by the government.

November 2: Crypto news website CoinDesk reports a leaked balance sheet that shows Alameda Research, Bankman-Fried’s crypto trading firm, was heavily dependent on FTX’s native token, FTT. The Reuters news agency was unable to verify the report.

November 6: Binance CEO Changpeng Zhao says his firm plans to liquidate its holdings of FTT due to unspecified “recent revelations”.

November 7: Bankman-Fried says “FTX is fine. Assets are fine”.

November 8: Binance says it is planning a deal to acquire FTX.

November 9: Binance decides against pursuing a bailout of FTX.

November 10: FTX suspends onboarding of new clients as well as withdrawals until further notice. Bankman-Fried tells staff in a memo that he is scrambling to raise funds and has held talks with Justin Sun, founder of the crypto token Tron.

November 11: FTX starts voluntary Chapter 11 proceedings in the US, along with its US unit, crypto trading firm Alameda Research and nearly 130 other affiliates. Bankman-Fried resigns as CEO.

November 12: Reuters reports at least $1bn of customer funds have vanished from FTX. The exchange says it has detected unauthorised transactions. Blockchain analytics firms estimate outflows between $473m and $659m in “suspicious circumstances”.

November 13: Bahamas securities regulators launch a probe over the collapse of FTX, which has its base in the Caribbean nation.

November 15: Financial regulators in the Bahamas appoint liquidators to run FTX’s unit in the country.

November 16: FTX outlines a “severe liquidity crisis” in US bankruptcy filings, which show the group could have more than 1 million creditors.

A court filing shows FTX’s Bahamas unit, FTX Digital Markets, is seeking protection from creditors in the US under Chapter 15 of the US Bankruptcy Code.

Bankman-Fried is sued in a US court by investors alleging the company’s yield-bearing crypto accounts violated Florida law.

Liquidators for FTX Digital Markets “reject the validity” of FTX’s US bankruptcy proceedings.

Major crypto player Genesis Global Capital suspends customer redemptions in its lending business, citing the sudden failure of FTX.

November 17: The US House Financial Services Committee says it plans to hold a hearing in December to investigate the collapse of FTX.

November 30: Bankman-Fried says in an interview at the New York Times Dealbook Summit that “he didn’t ever try to commit fraud”.

December 12: Police arrest Bankman-Fried in the Bahamas, with the US expected to file for his extradition. US authorities decline to comment on potential charges, but the New York Times reports the charges include wire fraud, wire fraud conspiracy, securities fraud, securities fraud conspiracy and money laundering.

[ad_2]

[ad_1]

This is an opinion editorial by Jonathan Leger, a software developer and author of the Regarding Bitcoin newsletter. A version of this article was originally published on Substack.

I was raised in a doomsday cult that taught that God was getting ready to wage the war of Armageddon and bring about the end of the current world order. The governments, all ruled by the devil, would be replaced with the Kingdom of Heaven ruled by Jesus Christ. The cult discouraged any kind of real financial planning because of this worldview. After all, what was the point of investing in a system facing imminent destruction?

This extreme religious upbringing — and my eventual escape from it — helped me in my path to understanding Bitcoin Maximalism.

My Bitcoin experience began with a losing trade in the summer of 2014. After reading a few articles about this “magic internet money,” I bought my first whole coin for about $500. I wasn’t prepared for how volatile the price swings would be, though, and sold at a loss later that year. If only I had known…

The last five years have been an intense learning experience for me. At the end of 2017, I left the cult with my wife, who is currently shunned by her entire family (as required by cult doctrine). I lost all of my “friends” as well. We had to learn how the real world worked and how to build a social network outside of the ready-made set of “friends” handed to us by the church, as getting close to non-members was deeply discouraged. All non-members were going to die by God’s hand at Armageddon anyway, so there was no point in getting too familiar. Plus, their wicked ways might rub off on you, so it was best to keep your distance for fear that you might get hit by a stray fireball when the end came.

After leaving the cult, I embraced life with the fervor of a wrongly-jailed prisoner embracing freedom upon exoneration. I studied politics for the first time, since members didn’t vote or participate in any form of campaigning due to the belief that all earthly governments were Satanic. I read books on how far humanity had advanced and how much better off we all are than in centuries past, however imperfect the current world may be. I was excited and optimistic for the future.

In 2004, I had started and grew a successful business as a software developer and internet marketing coach. The tools our team developed helped people compete with larger companies for getting websites to the top of the search results in Google, as well as other related use cases. For many years, searching Google for “coolest guy on the planet” returned my website as the number one result, demonstrating the importance of the Bitcoiner mantra, “Don’t trust, verify.”

Despite making millions of dollars in successful software product launches, I lost most of it through poor financial decisions coupled with intensifying competition from much better capitalized companies. On top of that, I went through a very expensive, acrimonious divorce.

“Love is grand,” they say, “but divorce is a hundred grand.” I grew up poor and had little formal or personal education in how to properly manage money or what money even really was, so when I finally “made it” I didn’t know how to properly handle it.

As you might imagine, it wasn’t all bad. The money afforded me many incredible personal experiences. But my personal and home life were a mess, I was still a true believer in the doomsday cult praying for the end of the world, and on balance was very unhappy. I felt like the wealthy writer of Ecclesiastes, “I have seen all the works that are done under the sun; and, behold, all is vanity and vexation of spirit.”

In 2019, I was 42 years old, had escaped the cult and was remarried to a wonderful woman whom I adore. I spent much of my time studying markets to prevent repeating past mistakes and working to develop a retirement plan. I did well with stocks that year but kept hearing about Bitcoin and how it was like nothing else. After reading “The Bitcoin Standard,” I finally understood why sound money was important and why fiat was doomed to fail. I again bought into BTC, this time at around $9,000.

When COVID-19 first reared its ugly head in early 2020, I did what many people did: listen to the “experts.” But as the scenes of pandemic theater played out, I began to understand that politics exhibited many of the same attributes as the cult I came out of. There were leaders that could not be questioned and members who would shame and shun anyone who dared to speak up. Their god was “The Science,” their Pope, Anthony Fauci, their clergy, the CDC and politicians. Rights were eroded and small businesses shut down while big box chains and mega-corporations raked in record profits, including Big Pharma. Trillions of dollars were printed out of thin air, proving true the Cantillon effect that says the largest beneficiaries of changes in money supply are the people and corporations closest to the money printers.

Unlike many hardcore Bitcoiners, my investment goals were purely financial, not philosophical. Like so many others in the crypto casino, I was chasing gains. Because of this, I sold my bitcoin at $45,000 and jumped into altcoins with the belief that I could multiply my investment, which I did. In fact, I did well enough to be able to stop writing software for about a year and a half, which was a much-needed hiatus and gave me even more time for the research I was doing.

Then came the market crash of 2022. With inflation clearly not “transitory,” the money printer was halted, and the Federal Reserve began to raise rates at a historically-unprecedented pace. Markets reacted negatively, bringing all cryptocurrencies down with them. The price of bitcoin cratered along with everything else. Low prices exposed the weakness of overleveraged schemes like Celsius and Three Arrows Capital, sending them into bankruptcy. Terra collapsed along with a host of other smaller crypto operations.

The purportedly second-largest centralized crypto exchange in the world, FTX, stepped in with a promise to rescue the industry, only to turn out to be the largest fraud of them all when its own balance sheet was leaked. FTX’s founder, Sam Bankman-Fried (SBF), was accused of stealing investors’ and users’ money and sending it to its trading arm, Alameda, where it was gambled away on high-risk trades that spectacularly failed to the tune of $10 billion.

A massive “hack” of FTX followed shortly thereafter, the repercussions of which are still playing out. Evidence of political intrigue emerged, supported by the fact that most mainstream media coverage treated SBF with kid gloves, some even painting him as a victim rather than a predator. As of this writing, nobody has been arrested. By way of comparison, Bernie Madoff was in handcuffs the day after his fraud was uncovered.

Bitcoin began flying off exchanges while Bitcoiners shook their damn heads at how many people had again ignored one of their most basic truths, “Not your keys, not your coins.” While I was glad to see people finally listening, the damage done was tremendous, both in financial and reputational loss. Since my start with Bitcoin, I always self-custodied my bags and so was unaffected by any of the collapses, at least as far as losing any of my holdings.

Though I never lost my respect for Bitcoin or the principles of decentralization and sound money, these events returned them front and center to my consciousness. I resumed listening to Bitcoiner podcasts, reading long-form articles, watching videos and reminding myself just how badly off the current world financial system really is.

“It’s just math,” say the Bitcoiners, and I believe they are correct. There’s no stopping the debt spiral now. The end is indeed coming, just not in the way I had been taught growing up.

During the time I was trading and HODLing altcoins, I thought Bitcoin Maxis were too extreme. Even though I agreed with their views on sound money and decentralization and agreed that most cryptos were just vaporware rug pulls waiting to happen, I didn’t understand their disdain for every crypto that wasn’t bitcoin. This was especially true for projects that were actively being used in the real world to seemingly beneficial effect.

As a software developer myself, I am aware that there is no single tool that covers all use cases. There’s Windows, or MacOS X, or Linux for computers, Android or Apple’s iOS for phones, and countless different apps that run on all of those platforms that perform different functions, many of them competing for market share. This competition encourages innovation which ultimately makes all software better. That free-market principle is something Bitcoiners honor, so I didn’t understand why they jettisoned it when it came to cryptocurrencies. My assumption was they did so out of self-interest. If people invested in other projects, they wouldn’t put their money in bitcoin, which hurt the Bitcoiner’s own portfolio.

Then there was proof of work. It’s power intensive and comparatively slow, even if far superior to bank technologies like SWIFT in terms of speed and guaranteed settlement. Even if the “green” argument was just fear, uncertainty and doubt (FUD), why stick with proof of work when other tech had proven far faster and more efficient, making it much more viable for payments systems?

Today, at last, after everything that’s happened over the past three years, I finally get it.

“Don’t trust, verify.”

The whole Bitcoiner philosophy comes down to those three words. Trust has always been abused, even if only by a small minority. But all it takes is a minority of people abusing and misusing your trust to cause you, and everyone else who trusts them, grave harm. So don’t trust, verify.

How does this relate to Bitcoiner’s referring to all other cryptos as “shitcoins” and dismissing them outright? It’s simple. The entire fiat currency system is a Ponzi scheme. Fiat is “money by decree” — it’s not backed by any real asset and only has value because the government says it does. Governments use fiat to rob citizens by printing money without citizens’ consent. This is, in effect, a tax that has not been approved by or voted on by the people. It’s theft.

For example, prior to fiat, governments would need actual hard currency (usually gold) to fund the wars they wanted to fight. If they didn’t have the money, they couldn’t fight the wars without raising taxes, which is never a popular proposition. With fiat, however, the government can print as much money as they want, pulling the money to fund their self-serving conflicts out of the pockets of the people who use that fiat currency: no permission necessary, and without most people realizing what’s happening.

Fiat also keeps people on a perpetual hamster wheel through inflation. If you know the money you have in the bank will be worth less next year than it is this year, you must keep trying harder to earn more money, year after year, just to keep your head above water. This keeps the majority of people as perpetual wage slaves, never quite able to get ahead, at least not enough to stop and enjoy their lives.

Without inflation you could live below your means, save your extra money, and trust in the deflationary effects of technology to make your money stretch much further once you decide to retire. After all, with technology constantly making supply chains more efficient through improvements in transportation and automation, everything should cost less over time, not more. And yet prices keep rising. Why? Inflation.

So what does fiat have to do with cryptocurrencies other than bitcoin? All other cryptocurrencies are working within the current financial system trying to improve it, make it more efficient, provide better privacy, etc. This has some positive effects. For instance, stablecoins give access to the U.S. dollar to people in countries whose currency is undergoing severe inflation and whose banking systems are corrupt or unreliable. But it still requires the fiat Ponzi to function.

You can talk until you’re blue in the face about how a highly-efficient cryptocurrency could give access to the financial system to billions of unbanked individuals, improving their lives by helping them escape their own inflationary currencies and bypassing their corrupt governments. But it doesn’t matter because you’re only providing those people access to another fiat currency, and fiat is murdering the free market. You can talk about how issuing tokens give small businesses the ability to raise money without having to pay billions to big banks to IPO. Doesn’t matter. You’re still working within the fiat system, and the fiat system is the fundamental root of all the problems to begin with.

To the Bitcoiner, cryptocurrencies are decks being built onto the Titanic as it sinks, while Bitcoin is the life raft people need to get on to save themselves. The tech of some cryptos might be great, but it only delays the inevitable demise of the sinking ship. Maxis believe that bitcoin is destined to replace fiat, not shore it up, returning sound money to the world. As they often say, “Bitcoin fixes this.”

For Bitcoiners, this isn’t just about money. It’s a guidestone that influences every aspect of life. It’s a belief system, though I’ll stop short of calling it a religion, since people of every conceivable religion also subscribe to its tenants. To those who aren’t Bitcoiners, maxis can appear to be in some kind of cult, but it’s not a cult. Quite the opposite, in fact.

Bitcoiners are people who, like me, have escaped a cult: the cult of fiat. Once they were like everyone else, brainwashed into believing that the government could be trusted with control over the money printer, that the Fed was capable of central planning of the economy, and that inflation was necessary for economic growth.

Plato’s famous Allegory of the Cage describes a group of people who have lived chained to the wall of a cave for their entire lives. All they can see is a blank wall and the shadows cast upon it from a fire burning behind them. They give the shadows names, believing them to be actual representations of the real world. One of the prisoners escapes from the cave and, having experienced the actual world, realizes that the shadows are not true representations of it. He returns to the cave to try and convince the other prisoners, but they don’t believe him because the shadows are all they have ever known. Bitcoiners are the escaped man.

The Bitcoiner tribe can be rowdy and crass and harsh, but you must consider what they’re out to achieve and what they’re up against. Their endeavor is not for the faint of heart. It’s a real David and Goliath moment. The Bitcoiner stands, golden coins in hand, looking the giant in the eye with a defiance that onlookers usually perceive as madness. Maybe it is madness, but without that dauntless quality, Bitcoin wouldn’t have come as far as it has. And I, for one, will cheer them on as the giant collapses.

This is a guest post by Jonathan Leger. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

[ad_2]

Jonathan Leger

Source link

[ad_1]

FTX founder Sam Bankman-Fried went on an “I screwed up” media blitz this week, highlighted by his video appearance at the New York Times DealBook summit on Wednesday and continuing into the Sunday talk shows.

U.S. securities lawyer James Murphy, speaking to CNN’s Quest Means Business on Thursday, said Bankman-Fried “did a very good job of sticking to his talking points.”

Murphy said: “His talking points were, ‘I didn’t do anything wrong intentionally. I may have been negligent. I may have breached fiduciary obligations.’ But those two things get you sued, get you penalized. They don’t get you to jail. And so he steered clear of anything that sounded like intentional misconduct.”

FTX imploded in spectacular fashion last month, spurring calls for tighter regulation and shaking confidence in the crypto sector. The $32 billion cryptocurrency exchange had established itself as a leader in the field, enlisting star athletes like Stephen Curry and other celebrities to bolster its image.

A key accusation leveled against Bankman-Fried is that he used customer funds from his crypto exchange to fund risky bets at affiliate trading arm Alameda Research.

In the DealBook interview, Bankman-Fried peppered his statements with legalese, stating that he “did not ever try to commit fraud on anyone,” didn’t “know of times when I lied,” and “didn’t knowingly comingle funds.”

Said Murphy of Bankman-Fried sticking to the script: “He’s a very, very bright man and managed to do that for an hour.”

In a Financial Times interview published Sunday, Bankman-Fried stuck with the theme, saying, “I f****d up big and people got hurt.”

On ABC’s This Week on Sunday, Bankman-Fried said, “Look, I screwed up. Like I was CEO, I had a responsibility here and a responsibility to be on top of what was going on the exchange. I wish I had done much better at that.”

ABC legal analyst Dan Abrams said afterwards, “His basic defense, it sounds like, is, ‘I didn’t have the intent. I wasn’t trying to do it.’ That’s not enough in a lot of cases. That’s not going to protect him necessarily from getting indicted. But it is something we hear from CEOs who get tried, and it almost never works.”

Abrams added that Bankman-Fried could be facing a long time in jail.

“We’re talking about, by the way, the possibility of up to life in prison,” he said. “When you’re talking about this much money, in the federal sentencing guidelines, you’re talking about the possibility of enhancement after enhancement after enhancement based on the dollar amounts that could lead to something up to life.”

Earlier this week Coinbase CEO Brian Armstrong said of Bankman-Fried, “It’s “baffling to me why he’s not in custody already.”

Mark Cuban, billionaire owner of the Dallas Mavericks and a prominent crypto investor, recently told TMZ that Bankman-Fried should be worried about prison time.

Mike Novogratz, CEO of crypto firm Galaxy Digital Holdings, told Bloomberg TV on Thursday, “Sam and his cohorts perpetuated a fraud…He took our money. And so he needs to get prosecuted. People will go to jail, and should go to jail.”

Securities lawyer Murphy added that prosecutors don’t have to prove that there was securities fraud. “They can go with mail and wire fraud,” he said. “If the money of customers was misappropriated and given to this affiliated company Alameda, that is a fraud and should qualify under the statues. I sincerely hope our Department of Justice is looking at it very hard.”

Fortune reached out to Bankman-Fried for comments but did not receive an immediate reply.

Our new weekly Impact Report newsletter will examine how ESG news and trends are shaping the roles and responsibilities of today’s executives—and how they can best navigate those challenges. Subscribe here.

[ad_2]

Steve Mollman

Source link

[ad_1]

Bill Ackman said Saturday that his recent comments on Sam Bankman-Fried were misinterpreted.

Ackman, founder and chief executive officer of Pershing Square Capital Management LP, faced criticism after he tweeted on Nov. 30 that he believed SBF, as the founder of crypto exchange FTX is known, was telling the truth at the New York Times Dealbook Summit. Bankman-Fried denied trying to perpetrate a fraud, while acknowledging many errors at the helm of the company.

FTX imploded last month after the exchange revealed an $8 billion hole in its balance sheet, fueling questions about whether it mishandled customer funds. Since then Bankman-Fried has embarked on an apology tour, accepting that his company broke its own rules but denying fraud.

Ackman said Saturday that the collapse of FTX is “at a minimum, the most egregious, large-scale case of business gross negligence that I have observed in my career.” Still, the hedge fund manager said Bankman-Fried could have “civil rather than criminal liability” if he has told the truth.

Our new weekly Impact Report newsletter will examine how ESG news and trends are shaping the roles and responsibilities of today’s executives—and how they can best navigate those challenges. Subscribe here.

[ad_2]

Susanne Barton, Bloomberg

Source link

[ad_1]

FTX founder Sam Bankman-Fried should be in custody by now, as far as Brian Armstrong is concerned. The Coinbase CEO said this week it’s “baffling to me why he’s not in custody already.”

“The DOJ or somebody should be able to make—just based on his public statements, I think there’s a very open and shut case for fraud,” Armstrong said at the a16z crypto Founder Summit on Tuesday. He added, “I’m not an expert on this, but the people I talk to seem to agree on that.”

Armstrong also questioned why the media has refrained from calling Bankman-Fried a criminal.

“I think we were all pretty shocked to see the scope of the fraud that happened at FTX. And let’s call it a fraud. We have to call it what it actually is. It’s been pretty bizarre that mainstream media hasn’t really come out and said, ‘This guy’s a criminal.’ Maybe they want to wait until he’s actually indicted or something like that, and in custody. But it seems very clear at this point that that’s the case.”

FTX imploded in spectacular fashion last month, surprising many inside and outside the crypto sector. The $32 billion exchange had established itself as a leader in the field, having enlisted star athletes like Tom Brady and other celebrities to bolster its image. Its collapse shook confidence in the crypto sector and spurred calls for tighter regulation.

Bankman-Fried resigned as FTX CEO on Nov. 11, the same day that the company, along with affiliated trading arm Alameda Research, filed for bankruptcy. A key accusation leveled against Bankman-Fried is that he used customer funds from his crypto exchange to fund risky bets at Alameda Research.

Armstrong’s Coinbase, like FTX, is a cryptocurrency exchange. But whereas Bankman-Fried based FTX in the Bahamas—where he reportedly enjoyed an extravagant penthouse lifestyle—Coinbase is a public company in the U.S.

“You can to read our financial statements,” Armstrong said. “They’re audited by a third party, you don’t have to trust us. All the customer funds are segregated. We don’t invest any customer funds without their explicit direction.”

Armstrong was not the only crypto luminary sharing harsh views of Bankman-Fried this week. Mike Novogratz, CEO of crypto firm Galaxy Digital Holdings, told Bloomberg TV on Thursday, “Sam and his cohorts perpetuated a fraud. They used customer money to make bets that he ‘poorly risk managed’ after he made them.”

“The problem was, he took our money,” Novogratz added. “And so he needs to get prosecuted. People will go to jail, and should go to jail.”

Shares in Coinbase and Canada-listed Galaxy Digital both plunged more than 25% last month, exacerbating an already brutal “crypto winter.” Coinbase shares have fallen roughly 80% this year, erasing about $44 billion in value. BlackRock CEO Larry Fink said this week, “I actually believe most of the companies are not going to be around,” referring to the beleaguered crypto sector.

Last week Mark Cuban, billionaire owner of the Dallas Mavericks and a prominent crypto investor, told TMZ that Bankman-Fried should be worried about prison time.

“I don’t know all the details, but if I were him, I’d be afraid of going to jail for a long time,” he said. “It sure sounds bad. I’ve actually talked to the guy, and I thought he was smart, but boy, I had no idea he was going to, you know, take other people’s money and put it to his personal use. Yeah, that sure…seems like what happened.”

Armstrong lamented the fact that the crypto sector attracts an inordinate number of bad actors.

“We have to kind of come to terms as an industry with the fact that, I think our industry is attracting a disproportionate share of fraudsters and scammers. And that’s really unfortunate. That doesn’t mean it’s representative of the whole industry. ”

Our new weekly Impact Report newsletter will examine how ESG news and trends are shaping the roles and responsibilities of today’s executives—and how they can best navigate those challenges. Subscribe here.

[ad_2]

Steve Mollman

Source link

[ad_1]

The below is an excerpt from the Bitcoin Magazine Pro report on the rise and fall of FTX. To read and download the entire 30-page report, follow this link.

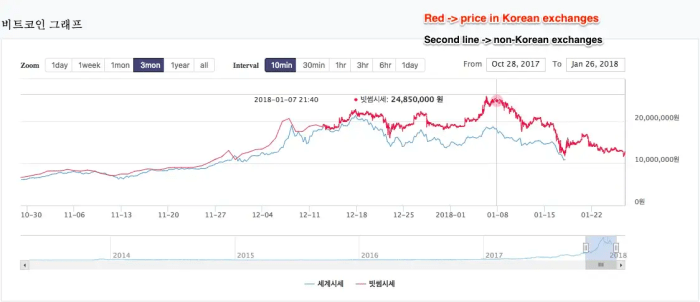

Where did it all start for Sam Bankman-Fried? As the story goes, Bankman-Fried, a former international ETF trader at Jane Street Capital, stumbled upon the nascent bitcoin/cryptocurrency markets in 2017 and was shocked at the amount of “risk-free” arbitrage opportunity that existed.

In particular, Bankman-Fried said the infamous Kimchi Premium, which is the large difference between the price of bitcoin in South Korea versus other global markets (due to capital controls), was a particular opportunity that he took advantage of to first start making his millions, and eventually billions …

At least that’s how the story goes.

The Kimchi Premium – Source: Santiment Content

The real story, while possibly similar to what SBF liked to tell to explain the meteoric rise of Alameda and subsequently FTX, looks to have been one riddled with deception and fraud, as the “smartest guy in the room” narrative, one that saw Bankman-Fried on the cover of Forbes and touted as the “modern day JP Morgan,” quickly changed to one of massive scandal in what looks to be the largest financial fraud in modern history.

As the story goes, Alameda Research was a high-flying proprietary trading fund that used quantitative strategies to achieve outsized returns in the cryptocurrency market. While the story was believable on the surface, due to the seemingly inefficient nature of the cryptocurrency market/industry, the red flags for Alameda were glaring from the start.

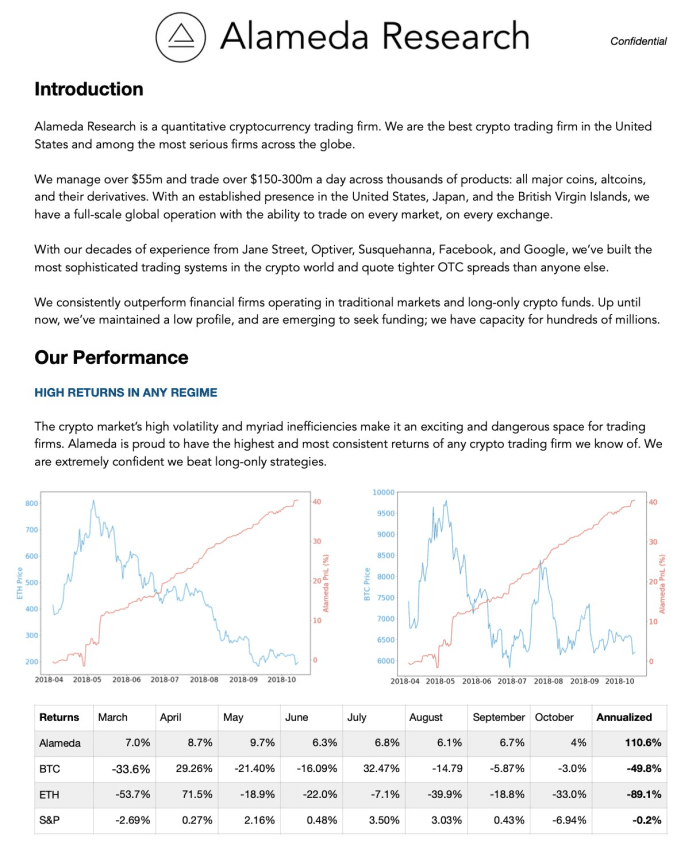

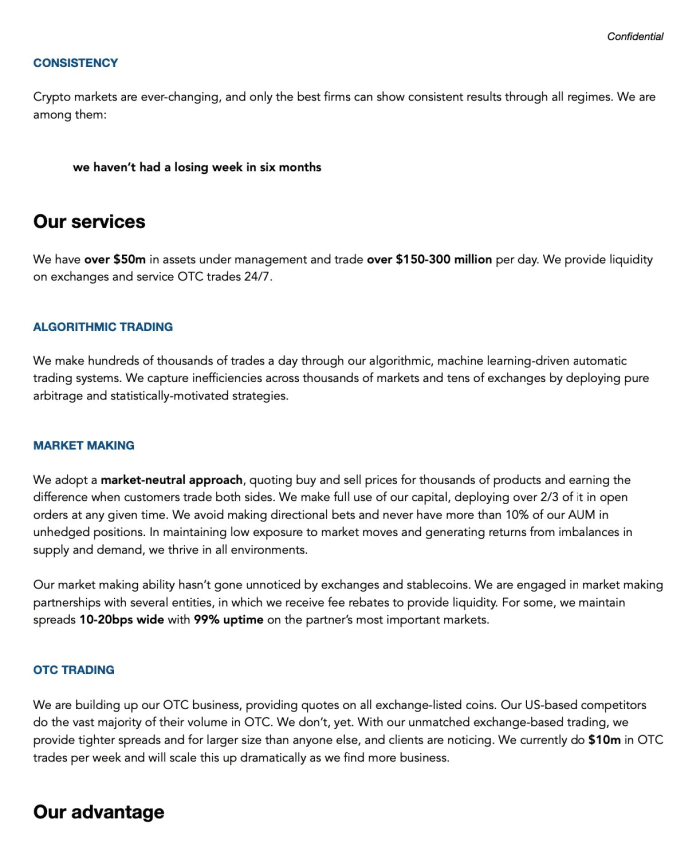

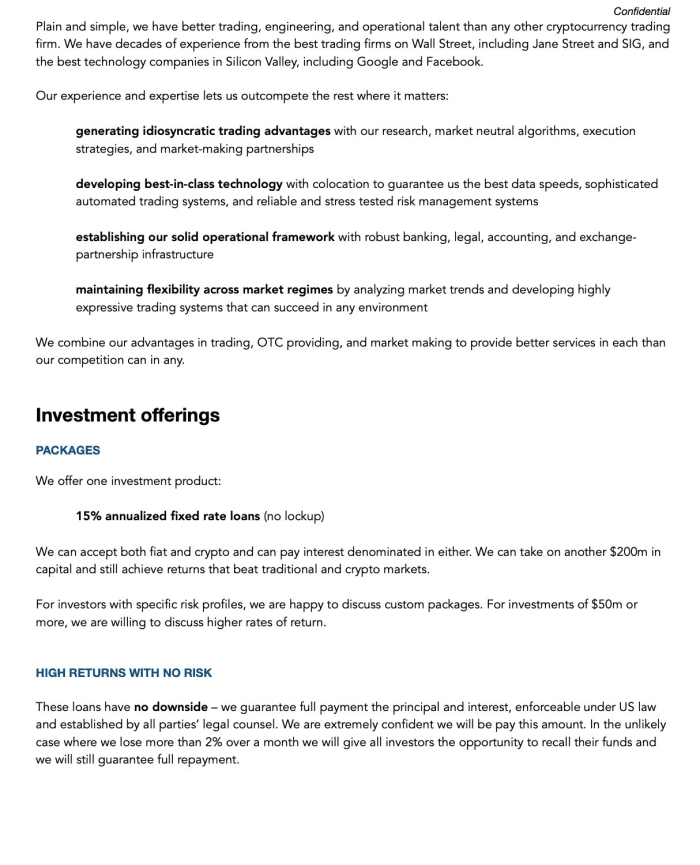

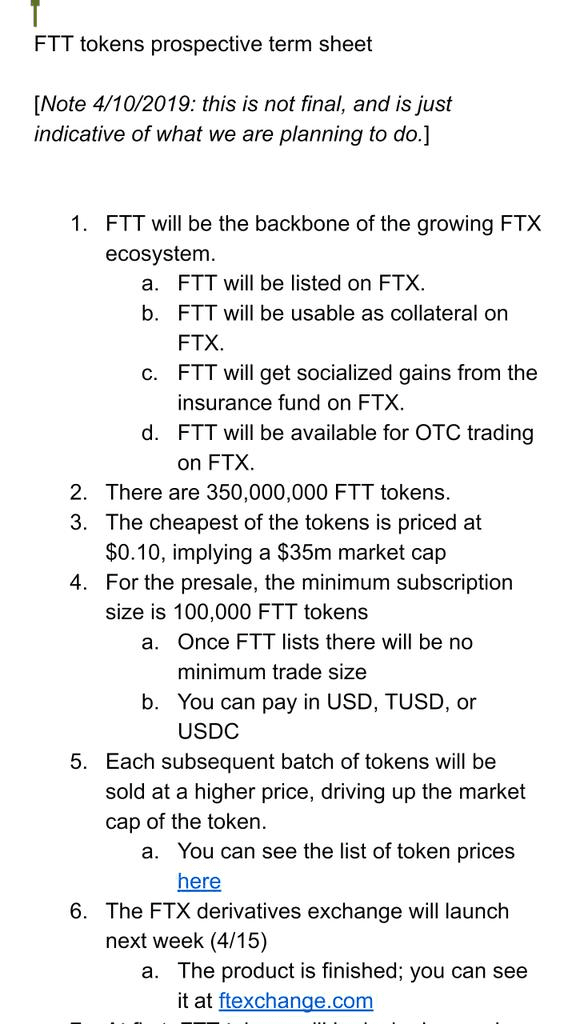

As the fallout of FTX unfolded, previous Alameda Research pitch decks from 2019 began to circulate, and for many the content was quite shocking. We will include the full deck below before diving into our analysis.

The deck contains many glaring red flags, including multiple grammatical errors, including the offering of only one investment product of “15% annualized fixed rate loans” that promise to have “no downside.”

All glaring red flags.

Similarly, the shape of the advertised Alameda equity curve (visualized in red), which seemingly was up and to the right with minimal volatility, while the broader cryptocurrency markets were in the midst of a violent bear market with vicious bear market rallies. While it is 100% possible for a firm to perform well in a bear market on the short side, the ability to generate consistent returns with near infinitesimal portfolio drawdowns is not a naturally occurring reality in financial markets. Actually, it is a tell-tale sign of a Ponzi scheme, of which we have seen before, throughout history.

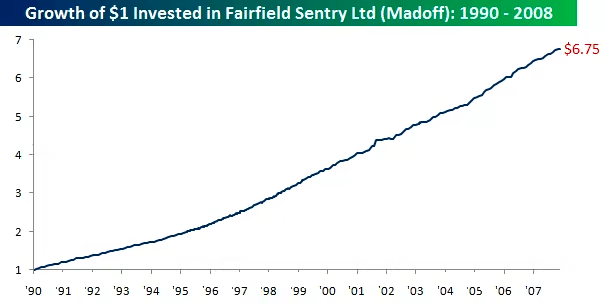

The performance of Bernie Madoff’s Fairfield Sentry Ltd for nearly two decades operated quite similarly to what Alameda was promoting via their pitch deck in 2019:

Stated returns by Bernie Madoff’s fund

It appears that Alameda’s scheme began to run out of steam in 2019, which is when the firm pivoted to creating an exchange with an ICO (initial coin offering) in the form of FTT to continue to source capital. Zhu Su, the co-founder of now-defunct hedge fund Three Arrows Capital, seemed skeptical.

Approximately three months later, Zhu took to Twitter again to express his skepticism about Alameda’s next venture, the launch of an ICO and a new crypto derivatives exchange.

“These same guys are now trying to launch a “bitmex competitor” and do an ICO for it. 🤔” – Tweet, 4/13/19

Beneath this tweet, Zhu said the following while posting a screenshot of the FTT white paper:

“Last time they pressured my biz partner to get me to delete the tweet. They started doing this ICO after they couldn’t find any more greater fools to borrow from even at 20%+. I get why nobody calls out scams early enough. Risk of exclusion higher than return from exposing.” – Tweet, 4/13/19

Additionally, FTT could be used as collateral in the FTX cross-collateralized liquidation engine. FTT received a collateral weighting of 0.95, whereas USDT & BTC received 0.975 and USD & USDC received a weighting of 1.00. This was true until the collapse of the exchange.

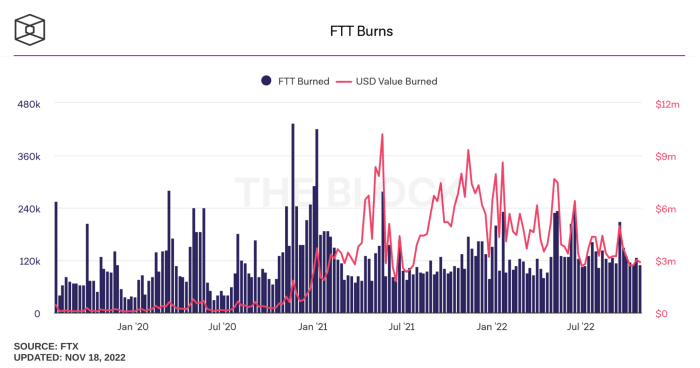

The FTT token was described as the “backbone” of the FTX exchange and was issued on Ethereum as a ERC20 token. In reality, it was mostly a rewards based marketing scheme to attract more users to the FTX platform and to prop up balance sheets. Most of the FTT supply was held by FTX and Alameda Research and Alameda was even in the initial seed round to fund the token. Out of the 350 million total supply of FTT, 280 million (80%) of it was controlled by FTX and 27.5 million made their way to an Alameda wallet.

FTT holders benefited from additional FTX perks such as lower trading fees, discounts, rebates and the ability to use FTT as collateral to trade derivatives. To support FTT’s value, FTX routinely purchased FTT tokens using a percentage of trading fee revenue generated on the platform. Tokens were purchased and then burned weekly to continue driving up the value of FTT.

FTX repurchased burned FTT tokens based on 33% of fees generated on FTX markets, 10% of net additions to a backstop liquidity fund and 5% of fees earned from other uses of the FTX platform. The FTT token does not entitle its holders to FTX revenue, shares in FTX nor governance decisions over FTX’s treasury.

Alameda’s balance sheet was first mentioned in this Coindesk article showing that the fund held $3.66 billion in FTT tokens while $2.16 billion of that was used as collateral. The game was to drive up the perceived market value of FTT then use the token as collateral to borrow against it. The rise of Alameda’s balance sheet rose with the value of FTT. As long as the market didn’t rush to sell and collapse the price of FTT then the game could continue on.

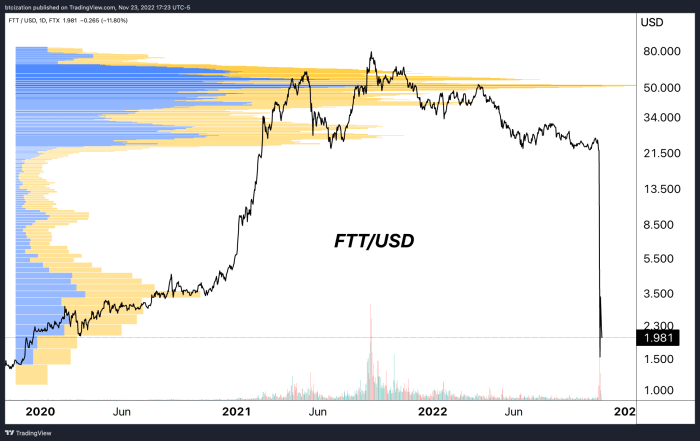

FTT rode on the backs of the FTX marketing push, rising to a peak market cap of $9.6 billion back in September 2021 (not including locked allocations, all the while Alameda leveraged against it behind the scenes. The Alameda assets of $3.66b FTT & $2.16b “FTT collateral” in June of this year, along with its OXY, MAPs, and SRM allocations, were combined worth tens of billions of dollars at the top of the market in 2021.

The price of FTT with a side profile showing FTT trading volume on FTX (logarithmic scale)

FTT Market Cap (logarithmic scale) – Source:CoinMarketCap

In one decision and tweet, CEO of Binance, CZ, kicked off the toppling of a house of cards that in hindsight, seems inevitable. Concerned that Binance would be left holding a worthless FTT token, the company aimed to sell $580 million of FTT at the time. That was bombshell news since Binance’s FTT holdings accounted for over 17% of the market cap value. This is the double edged sword of having the majority of FTT supply in the hands of a few and an illiquid FTT market that was used to drive and manipulate the price higher. When someone goes to sell something big, value collapses.

As a response to CZ’s announcement, Caroline of Alameda Research, made a critical mistake to announce their plans to buy all of Binance’s FTT at the current market price of $22. Doing that publicly sparked a wave of market open interest to place their bets on where FTT would go next. Short sellers piled in to drive the token price to zero with the thesis that something was off and the risk of insolvency was in play.

Ultimately, this scenario has been brewing since the Three Arrows Capital and Luna collapsed this past summer. It’s likely that Alameda had significant losses and exposure but were able to survive based on FTT token loans and leveraging FTX customer funds. It also makes sense now why FTX had an interest in bailing out companies like Voyager and BlockFi in the initial fallout. Those firms may have had large FTT holdings and it was necessary to keep them afloat to sustain the FTT market value. In the latest bankruptcy documents, it was revealed that $250 million in FTT was loaned to BlockFi.

With hindsight, now we know why Sam was buying up all of the FTT tokens he could get his hands on every week. No marginal buyers, lack of use cases and high risk loans with the FTT token were a ticking time bomb waiting to blow up.

After pulling back the curtain, we now know that all of this led FTX and Alameda straight into bankruptcy with the firms disclosing that their top 50 creditors are owed $3.1 billion with only a $1.24 cash balance to pay it. The company likely has over a million creditors that are due money.

The original bankruptcy document is riddled with glaring gaps, balance sheet holes and a lack of financial controls and structures that were worse than Enron. All it took was one tweet about selling a large amount of FTT tokens and a rush for customers to start withdrawing their funds overnight to expose the asset and liability mismatch FTX was facing. Customer deposits weren’t even listed as liabilities in the balance sheet documents provided in the bankruptcy court filing despite what we know to be around $8.9 billion now. Now we can see that FTX never had really backed or properly accounted for the bitcoin and other crypto assets that customers were holding on their platform.

It was all a web of misallocated capital, leverage and the moving of customer funds around to try and keep the confidence game going and the two entities afloat.

.

.

.

This concludes an excerpt from “The FTX Ponzi: Uncovering The Largest Fraud In Crypto History.” To read and download the full 30-page report, follow this link.

[ad_2]

Dylan LeClair And Sam Rule

Source link

[ad_1]

Sen. Sherrod Brown (D-Ohio) made a plea to the Treasury Department on Wednesday to draft legislation that would set up surveillance and regulatory measures over the crypto industry following the collapse of FTX.

[ad_2]

[ad_1]

Cryptocurrency exchange FTX US donated $1 million to a super PAC linked to Senate Minority Leader Mitch McConnell (R-Ky.) just weeks before the parent company declared bankruptcy early this month, shorting clients, creditors and investors out of billions of dollars, Bloomberg first reported Saturday.

The political contribution can be seen in the Senate Leadership Fund political action committee’s latest filing with the Federal Election Commission. The super PAC, which is aligned with McConnell and supports GOP Senate candidates, was the biggest spender ($239 million) in the midterm elections, according to OpenSecrets.

The payment was made Oct. 27 by West Realm Shires Services Inc., which does business as FTX US. Just weeks later, more than 100 FTX-related companies, including the U.S. operation — which had been one of the largest financial exchanges in the world — filed for bankruptcy.

The Washington Post called the implosion of FTX, which had been valued earlier this year at $32 billion, “one of the fastest meltdowns of wealth in modern history.” The $23 billion personal fortune of American CEO Sam Bankman-Fried, who founded FTX, reportedly evaporated in a week.

Lawyers have estimated that more than a million people or businesses have lost money. The top 50 creditors alone are facing more than $3 billion in losses.

FTX lawyer James Bromley said at a bankruptcy hearing last Tuesday that Bankman-Fried, who resigned earlier this month, had treated the company as his “personal fiefdom” before it fell apart, according to the Post. “The emperor had no clothes,” he said.

The FTX companies and executives reportedly had easy access to customer accounts. Only “a fraction” of clients’ money has been located and secured since the bankruptcy was declared, the Post noted.

“Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information,” FTX’s new chief, John Ray III, said in a bankruptcy filing. Ray once oversaw the liquidation of Enron, one of America’s most notorious corporate frauds.

Yet before the meltdown, Bankman-Fried, who founded FTX, donated close to $39 million to Democratic candidates in the midterm elections, according to FEC records. One of his top lieutenants, Ryan Salame, gave $23.6 million, mostly to Republicans, Bloomberg reported.

FTX US also gave $750,000 to the Congressional Leadership Fund, $150,000 to the American Patriots, and $100,000 to the Alabama Conservatives Fund, all of which supported Republican congressional races, according to Bloomberg.

It’s unclear whether any of the money could be clawed back as part of the bankruptcy court ruling.

[ad_2]

[ad_1]

The Golden State Warriors were named in a lawsuit Monday alleging the bankrupt cryptocurrency exchange FTX used the reigning NBA champions to fraudulently promote its platform.

[ad_2]

[ad_1]

Securities Commission of The Bahamas says it has taken control of FTX Digital Markets’ assets to protect investors.

The Bahamas unit of troubled cryptocurrency exchange FTX has had its digital assets seized by financial authorities in the Caribbean country.

The Securities Commission of The Bahamas said on Thursday it had transferred the digital assets of FTX Digital Markets (FDM) to a digital wallet under its control for “safekeeping”.

The regulator said it had taken the action on Saturday to protect the interests of clients and investors.

“Urgent interim regulatory action was necessary to protect the interests of clients and creditors of FDM,” the commission said in a statement.

“Under the Digital Assets and Registered Exchanges Act, 2020 (“DARE Act”), the Commission has the authority to apply for a judicial order to protect the interests of clients or customers of a registrant of the Commission under the DARE Act.”

The regulator said it was its understanding that FDM is not a party to bankruptcy proceedings in the United States involving parent company FTX.

“Over the coming days and weeks, the Commission will engage with other regulators and authorities, in multiple jurisdictions, to address matters affecting the creditors, clients and stakeholders of FDM globally to obtain the best possible outcome,” it said.

The announcement comes after a US court filing on Tuesday showed that FDM was seeking protection under Chapter 15 of the US Bankruptcy Code.

Non-US companies use the provision to protect themselves from creditors seeking to file lawsuits or tie up assets in the US.

FTX filed for bankruptcy last week after investors rushed to withdraw $6bn from the platform and a proposed rescue deal by its rival Binance fell through.

The collapse of FTX, the third-largest crypto exchange, has sent shockwaves through the crypto sector, prompting allegations of fraud and comparisons to the collapse of Lehman Brothers.

In a court filing on Thursday, new FTX CEO John Ray said he had never seen such a “complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here”.

Former CEO and founder Sam Bankman-Fried, who stepped down last week, said in an interview with Vox this week he regretted his decision to file for bankruptcy protection and that regulators “don’t protect customers at all”, before appearing to walk back some of his comments.

Bankman-Fried and several celebrities who promoted FTX are facing an $11bn class action lawsuit from investors, while the US Department of Justice and the Securities and Exchange Commission are investigating whether Bankman-Fried or his company violated securities law.

[ad_2]

[ad_1]

The tech industry is having a tough time. Only months ago, those who were bragging about their hot tech jobs and (seemingly) hyper-performing Crypto portfolios are probably screaming, crying, gnashing their teeth, and throwing up. And they may or may not be unemployed.

First, the recession is obliterating the stock market as we speak. Then, the summer Crypto proved the “decentralized marketplace” isn’t as impervious as Crypto nerds claimed. And now, the entire tech industry is facing a serious reckoning. It’s meltdown season — and Mercury isn’t even in retrograde.

First, Elon Musk bought Twitter. He subsequently fired a staggering number of employees. He then instituted Twitter Blue, a verification subscription which was a spectacular FAILURE. Most notably, causing the stock price of every significant insulin company to plummet by BILLIONS. It’s a long story, but the takeaway: the best $8 some random Twitter user ever spent.

Meanwhile, major tech companies like Meta, Salesforce, Redfin — and more — have been laying off thousands of employees. Wave after wave of layoffs are tearing through the entire tech sector, leaving thousands bamboozled and bereft. And this — alllll this — is happening while Jeff Bezos is giving away his money to Dolly Parton. I love her, but she has a theme park. These people don’t have jobs!

But this is nothing compared to the drama going on at former-Crypto giant FTX. And somehow, Tom Brady and Gisele are implicated!?! First, the divorce, now this.

Here’s a simplified version of events — and you don’t even need to understand crypto to follow along.

The Super Bowl: The true origins can be traced back to the Super Bowl, where much ad time was devoted to emergent crypto companies vying for the attention of potential investors. Among them: FTX.

January 2022: FTX was valued at an estimated $32 billion. They even had an NBA stadium named after them in Miami. But most prominently, their now infamous Super Bowl ad starring Larry David, who had never appeared in a commercial before. Just imagine that shoot. You should’ve stuck to your guns, Larry.

https://www.youtube.com/watch?v=BH5-rSxilxo

Don’t Miss Out on Crypto: Larry David FTX Commercial

Nov 2: The real drama started — as it always does — with some shady trades. CoinDesk published a report that exposed that Alameda Research – owned by the same people as FTX – had bought a ton of FTT … FTX’s cryptocurrency.

Nov 6: In a Tweet, the founder of Binance — one of FTX’s biggest competitors — said their company was going to dump their FTX tokens “due to recent revelations that have came to light.” Investors panicked and followed suit. And so began the FTT price plummet.

But with all their investors cashing in their coins, FTX was on the hook for all that money — which it could not afford to pay out. This is when things started to look really hairy.

Nov 8: With their tails between their legs, FTX went to Binance for an out. Binance agreed to acquire FTX.

Nov 9: Just kidding! Whatever was in those docs must have scared off Binance because they pulled out of the deal just a day later. Does this feel like an episode of Succession to you, too?

Nov. 11: FTX had no way to repay all this money. And any potential buys were not going anywhere near this dumpster fire. So FTX was forced to file for bankruptcy. 30-year-old CEO and founder Sam Bankman-Fried resigned.

He tweeted that he was “really sorry,” though! SO maybe that counts for something. Cue the world’s tiniest violin playing in the background.

But there’s more!

Later that day, reports emerged that FTX transferred $10 BILLION to Alameda — the same sister company mentioned above. That’s right, the one that started this mess — sparking controversy about how much access top leaders had to the company’s finances.

Nov 13: Where’s the money? New reports reveal that those BILLIONS of dollars had just … disappeared?

Nov 14: Now the cops are involved. Where the hell is the money, man? Regulators are trying to get to the bottom of this, while looking into criminal liabilities.

Nov 16: Here comes the class action. Defendants are suing FTX’s Bankman-Fried for misleading information. But the walls are now closing in on celebrities who appeared in FTX commercials, including Tom Brady, Gisele Bundchen, Stephen Curry, Larry David, and Shaquille O’Neal.

“FTX’s fraudulent scheme was designed to take advantage of unsophisticated investors from across the country, who utilize mobile apps to make their investments,” the lawsuit alleges. “As a result, American consumers collectively sustained over $11 billion dollars in damages.”

There you have it. But don’t hold your breath — there’s more to come, I’m sure. In fact, the documentary is already in the works

And if you still don’t follow, here are some TikToks tracking the drama:

@yourrichbff SBF bears a striking resemblance to Bernard Madoff. #money #crypto #ftx #finance #sbf #news #binance #alameda #bitcoin #ethereum #ftt #coin #cryptocurrency

[ad_2]

LKC

Source link

[ad_1]

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

We’re currently in the middle of the industry contagion and market panic taking shape. Although FTX and Alameda have fallen, many more players across funds, market makers, exchanges, miners and other businesses will follow suit. This is a similar playbook to what we’ve seen before in the previous crash sparked by Luna, except that this one will be more impactful to the market. This is the proper cleansing and washout from the misallocation of capital, speculation and excessive leverage that come with the global economic liquidity tide going back out.

That said, everyone is quick to jump on the next domino to fall. It’s natural. Most information surrounding balance sheets and hidden leverage in the system is unknown while new information and developments in real time are flowing out every half hour, it seems. Exchanges are under the spotlight right now and the market is watching their every move and transaction. There’s likely no exchange that is going to be as egregious with client funds as FTX and Alameda were, but we don’t know which exchanges can or cannot survive a bank run.

As shown by the market’s reaction, Crypto.com’s Cronos token (CRO), fell 55% in a week before getting some relief over the last day. There’s been a parabolic trend of withdrawals — a bank run — on the exchange over the last two days with the CEO doing the media rounds to assure everyone that withdrawals are processing fine and that they will survive.

The price of CRO fell 55% in a one-week period.

Huobi token (HT) follows the same path, down nearly 60% in the last two weeks. Huobi recently provided their list of assets on the platform, showing around $900 million in HT owned by both Huobi Global and Huobi users. It’s not clear what percentage of that $900 million is owned by Huobi Global, but it’s quite the haircut. Exchanges everywhere have been scrambling to provide some version of proof of reserves in attempting to calm the market.

The price of HT fell 60% in a two-week period.

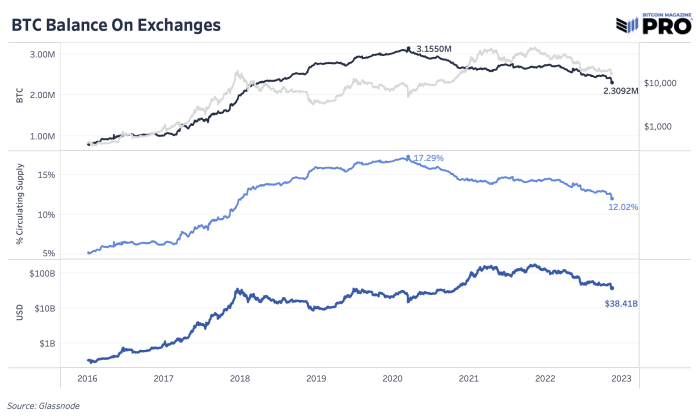

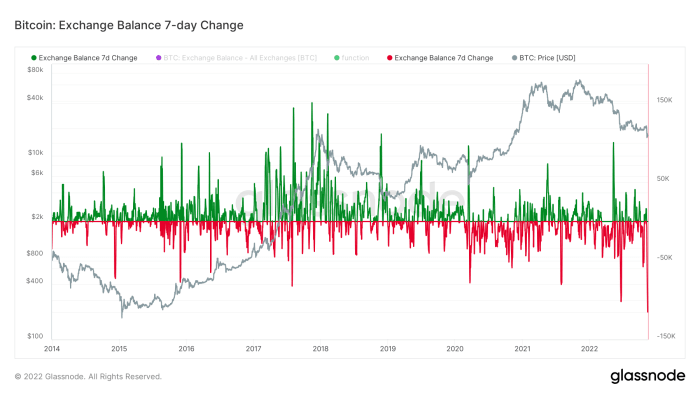

In terms of bitcoin leaving exchanges, it’s been a similar trend for the last three major market panic events: the March 2020 COVID crash, the Luna crash and now the FTX and Alameda crash. Bitcoin flies off exchanges as exchange and counterparty risk becomes priority No. 1 to mitigate. Overall, this is a welcome trend with over 122,000 bitcoin flowing out of exchanges over the last 30 days. It’s the lack of transparency, trust and excessive leverage in centralized institutions that have fueled the latest fall.

Having more of the bitcoin supply in self-custody is the way to counter this risk in the future. That said, assuming all of this bitcoin is going to self-custody and is intended to not come back to the market is a broad, unlikely assumption. Likely, market participants are taking whatever precaution they can regardless if their intent is to store this bitcoin long-term versus sending it back to an exchange later on.

In previous times, bitcoin flowing in and out of exchanges was more of a signal for price, but as more paper bitcoin, wrapped bitcoin on other chains and bitcoin financial products have grown, bitcoin exchange flows are more reflective of current user trends despite the last two major exchange outflows marking local price bottoms. Just 12.02% of bitcoin supply lives on exchanges today, down from its 2020 high of 17.29%. Although we’re only halfway through the month, November 2022 is shaping up to be the largest outflow month in history.

Bitcoin balances on exchanges continues to trend down since March 2020.

Bitcoin is leaving exchanges at a record pace.

The silver lining of the industry’s largest-ever exchange collapse is that a broad sense of distrust in counterparties and self-sovereign practices are set to increase among buyers of bitcoin going forward. While many have been speaking for over a decade on the importance of personal custody for the world’s first decentralized digital bearer asset, it often fell on deaf ears, as financial institutions like FTX seemed credible and trustworthy. Fraud assuredly can change that.

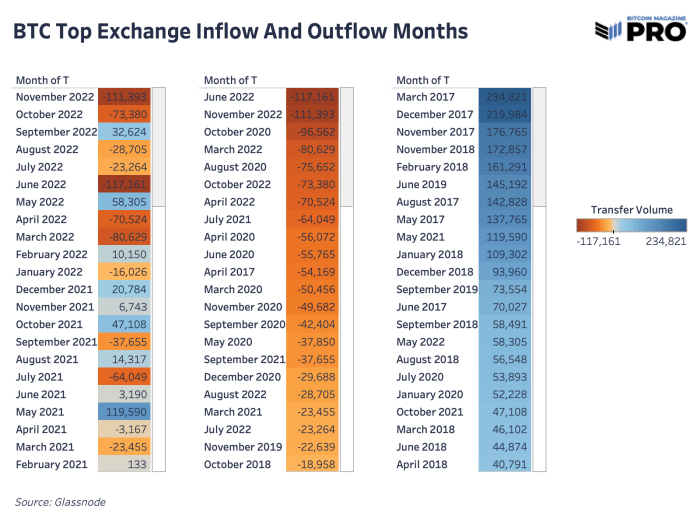

This dynamic, and the potential for greater amounts of contagion among the crypto space, has users fleeing to personal custody, with this past week bringing in the largest week-over-week decline in bitcoin on exchanges at -115,200 BTC.

This past week was the largest week-over-week decline in bitcoin on exchanges.

Interestingly enough, this sell-off was unique in the sense that unlike previous sell-offs in recent years, it wasn’t triggered by a flood of bitcoin being sent to exchanges, instead moreso by an implosion of illiquid crypto collateral without many (or in the case of FTT, any) natural buyers.

Given our immense focus on the risks of crypto-native contagion over the previous six months, we highly recommend our readers learn about and look into the prospects of self-custody; if nothing else, for the ease of mind.

[ad_2]

Dylan LeClair And Sam Rule

Source link

[ad_1]

As the autopsy of Sam Bankman-Fried’s crypto empire begins, it’s worth saying that there were red flags all over the place. We missed them.

[ad_2]

[ad_1]

At one point in the last several years, Sam Bankman-Fried, the cofounder of cryptocurrency exchange FTX, was reportedly worth an estimated $26 billion. At the beginning of last week, that number was a reported $16 billion. Now, it’s approximately zero dollars and zero cents. And that’s got to hurt, but probably of more concern to “SBF,” as he is known, is the prospect of potentially going to prison following the stunning, epic collapse of his company, which filed for bankruptcy on Friday, days after he assured customers that “FTX is fine.”

The Wall Street Journal reports that the Manhattan US attorney’s office has launched an investigation into FTX’s implosion, according to people familiar with the matter. At present, one thread prosecutors are likely focusing on, per the Journal, is that FTX reportedly lent billions in customer money to Alameda Research—a crypto trading firm that also happens to be owned by SBF—to fund risky trades. As the Journal notes, “Using customer funds for proprietary trading or lending them out—without an investor’s consent—is generally forbidden in the regulated securities and derivatives markets.” While such protections do not exist in the unregulated crypto market, as the Journal points out, FTX’s terms of service explicitly told users that they owned the cryptocurrencies in their accounts; the terms of service document reads: “None of the digital assets in your account are the property of, or shall or may be loaned to, FTX Trading.” As the Journal’s Gregory Zuckerman reported last week, revelations about the use of customer funds not only shocked Bankman-Fried’s “admirers” and employees, they “tore a hole in FTX’s finances” and “set the stage for the exchange’s swift implosion.”

FTX is also reportedly under investigation at the Securities and Exchange Commission and the Commodity Futures Trading Commission.

According to prosecutors, using customer money for a purpose that was not clearly communicated can be the basis for fraud or embezzlement charges. “What this will boil down to is, were there deliberate lies to convince depositors or investors to part with their assets?” Samson Enzer, a former Manhattan federal prosecutor, told the Journal. “Were there statements made that were false, and the maker of those statements knew they were false, and made with the intent to deceive the investor?” The Feds could also point to SBF’s tweets last week, just before the company collapsed, in which he wrote that FTX was “fine” and so were its assets, particularly in light of the fact that he later deleted such claims.

As the Journal notes, “Authorities would need to show Mr. Bankman-Fried intended to mislead customers when he wrote those tweets,” and while it can be difficult to prove intent, prosecutors could point to the allegedly secret efforts SBF undertook to prop up Alameda. “That is all potentially powerful circumstantial evidence of intent,” Aitan Goelman, a former federal prosecutor, told the Journal. Over the weekend, Reuters reported that of the roughly $10 billion in customer funds SBF moved from FTX to Alameda, at least $1 billion, and potentially up to $2 billion, had “vanished.” The outlet also wrote that Bankman-Fried has “secretly transferred” the money; in response, he texted Reuters to say he “disagreed with the characterization” of the transfer, writing, “We didn’t secretly transfer. We had confusing internal labeling and misread it.” Asked about the reportedly missing funds, he responded, “???”

Reuters also reported that:

In his texts to Reuters, Bankman-Fried denied implementing a “backdoor.” On Friday, he tweeted that he was “piecing together” what had happened at FTX, adding: “I was shocked to see things unravel the way they did earlier this week. I will, soon, write up a more complete post on the play by play.” At 10 p.m. on Sunday in the Bahamas, where SBF is based and FTX operated, he tweeted, “What.” Nearly an hour later, he tweeted the letter H. Over the course of Monday, he appeared to be spelling out Happened, though as of the late afternoon, he’d only gotten to the letter n.

[ad_2]

Bess Levin

Source link

[ad_1]

This is an opinion editorial by Tim Niemeyer, a Bitcoiner since circa-2018 and co-host of the Lincolnland Bitcoin Meetup in Springfield, Illinois.

Amidst the carnage of the FTX drama, a moment of clarity illuminated the Twittersphere. Michael Saylor’s words were the signal in the noise resulting from the dysfunctional trainwreck unaffectionately known as “crypto”. Before we can truly appreciate his insights, we should first meditate on what makes this relationship dysfunctional or, in the context of couples therapy, a toxic relationship.

While many in the cryptocurrency industry were happily going about their life viewing their relationship with money (trust, commitment, support, etc.) in a positive light, they were ignoring the warning signs that their relationship was anything but healthy. Sure, all good relationships have their ups and downs. Disagreements happen, but overall you share common goals and trust the other to have your best interests at heart. There’s a certain level of expectation that your partner will support you, communicate openly and honestly, and refrain from controlling behaviors. Life this way is freeing and you’re generally able to flourish.

But what if one side doesn’t have your best interests at heart? What if they are dishonest? What if there becomes a pattern of disrespect? What if they ignore your needs? Sure, you can hope for change, but you still feel drained, stressed, anxious, or depressed. Eventually, you want out. Your need for a positive, healthy relationship overwhelms the comfort of the known, current relationship. The first step is admitting there’s a problem. Acknowledging signs of a toxic relationship are necessary.

In regards to our relationship with money, support may be displayed in many ways. One way we support each other is through the ability to trust that our counterpart has our best interests at heart. The overwhelming problem with the cryptocurrency sphere (defined here as everything other than Bitcoin) is that it’s still largely based on an expectation of trust. Whether it’s FTX, Celsius, LUNA or the countless other scams and Ponzis that are sewn into the fabric of the cryptocurrency industry, it’s clear that having centralized entities controlling your value requires you trust the fallible seamstresses and their incentives. It’s like the trust fall; an exercise in which one person lets him- or herself fall without trying to stop it, relying on their friend(s) to catch them. How many times do you allow yourself to fall to the ground before you lose trust?

These recent fallouts in crypto continue to illuminate the inherent dishonesty in its DNA. Investors are deceived into a false sense of security in the relationship; it’s a form of dishonest communication based on non-transparency and the over-leveraged nature of exchanges. Allowing humans to control money allows controlling behaviors to be coded into the system, which leads to growing resentment in the relationship … The relationship is further strained when the toxic side puts their needs ahead of your own. The needs of some CEOs often incentivize them into leveraging the customers’ trust to benefit their gain. This display of negative financial behaviors is becoming all too common in the cryptocurrency industry (again, non-Bitcoin-only entities). At some point, as my father would say, we need to separate the wheat from the chaff.

The first step is to accept responsibility. Not that you caused the situation per se, but that you acknowledge the situation you’re in and begin advocating for yourself. This can be done by investing in yourself. In the context of this article, that investment is education in Bitcoin as well as understanding the unintended consequences of adopting a “digital fiat” mindset present throughout the altcoin and centralized exchange industries. Once we shift from blaming to understanding, we allow ourselves to begin healing. The pain resulting from the recent developments will linger for a while, but it is our responsibility to not dwell on the past but move forward with compassion. The next step in the journey to healing is allowing yourself to be vulnerable again. This can be attained by sharing your self-love with others; calmly and clearly explaining the benefits of Bitcoin, self-custody and proof of reserves to friends and family.

People recovering from a toxic relationship can benefit from finding support. It is the opinion of the author that Bitcoiners should be that support structure. It’s ironic that many Bitcoiners are known as the toxic ones when they are the ones trying to illuminate the toxicity inherent in the ecosystem. That being said, an “I told you so,” doesn’t assist in the healing process. This is the moment where we must rise above and lead with compassion. We should hold space in our heart and allow others the time to heal and change.

There will be many who do not recover from a toxic relationship of this magnitude. While we can continue to educate from a place of humility, we must remember that, “You can lead a horse to water, but you can’t make it drink.” Everyone will ultimately heal in their own way at their own pace. Some may never learn. We’ve probably all had a friend who’s jumped from one toxic relationship to another. As much as you may want to help, they need to first choose to help themselves. Even more, some people will continue to “Tinder around” with unhealthy cryptocurrency relationships. That’s their prerogative. If a friend of ours wants to be part of the hookup culture, that’s on them. They have to deal with the consequences of STDs and the like.

Regardless of the actions of certain exchanges or crypto in general, we must continue to espouse the benefits of Bitcoin in a positive light. Tell them how truth is born from trustlessness. Demonstrate how actual decentralization leads to pure democracy. Illuminate how immutability and permissionless systems allow for a free-flowing, cooperative society. Michael Saylor acutely recognized the toxicity we are allowing to proliferate through the perceived connection to crypto. We must choose to move forward towards a bitcoin standard for ourselves, our friends and family, and, ultimately, for society to flourish.

This is a guest post by Tim Niemeyer. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

[ad_2]

Tim Niemeyer

Source link

[ad_1]

Britain is taking the lead among major developed economies in moving away from cash in everyday payments, but more than two-thirds of people surveyed remain reluctant to go fully digital. That’s the conclusion of a survey by YouGov Plc for Bloomberg, which showed 57% of people in the UK rarely or never use cash in […]

[ad_2]

Bloomberg News

Source link