Just in time to create a new Super Bowl ad, Crypto.com founder Kris Marszalek has made the priciest domain purchase in history, buying AI.com for $70 million, according to the Financial Times. The deal, paid entirely in cryptocurrency to an unknown seller, shatters previous records. (Broker Larry Fischer, who facilitated the sale, is presumably celebrating his good fortune.)

Marszalek plans to debut the site during Sunday’s big game, offering consumers a personal AI agent for messaging, app usage, and stock trading. “If you take a long-term view — 10 to 20 years – [AI] is going to be one of the greatest technological waves of our lifetime,” he told the FT.

The purchase rewrites the domain record books — not that crypto industry itself is known for its restraint when it comes to spending. Previously, CarInsurance.com held the crown at $49.7 million (2010), followed by VacationRentals.com ($35 million in 2007) and Voice.com ($30 million in 2019). Other eye-popping sales include PrivateJet.com ($30 million), 360.com ($17 million), and Sex.com, which has sold twice for over $13 million each time, though its second owner went bankrupt trying to monetize it.

“With assets like AI.com, there are no substitutes,” Fischer told the FT. “When one becomes available, the opportunity may never present itself again.”

Whether these mega-dollar domains actually deliver returns remains an open question. But for Marszalek, who already owns Crypto.com and dropped $700 million on stadium naming rights, owning two category-defining domains is apparently worth the outlay.

The founder of Crypto.com is tackling AI next, and he spared no expense.

Crypto.com co-founder and CEO Kris Marszalek has launched a new AI agent platform under the brand AI.com, a domain he reportedly purchased for $70 million.

The new company claims this transaction is “believed to be the single largest domain purchase in history.” There’s a chance there have been even larger deals that have not been disclosed. Historically, Cars.com has been cited as the most valuable domain name ever after financial statements tied to its acquisition in 2014 revealed the site was listed as an intangible asset worth $872.3 million.

According to a press release, the platform will allow users to generate a private, personal AI agent that operates on the user’s behalf. The company says the AI agent will be able to send messages, build projects, trade stocks, and even update a dating profile.

The company said that all user agents will operate in a dedicated secure environment with data encryption using user-specific keys.

“We are at a fundamental shift in AI’s evolution as we rapidly move beyond basic chats to AI agents actually getting things done for humans,” said Marszalek, in the press release. “Our vision is a decentralized network of billions of agents who self-improve and share these improvements with each other, vastly and rapidly expanding agentic capabilities and accelerating the advent of AGI.”

The website’s landing page currently features a countdown clock for Sunday, when the platform is set to officially launch following a Super Bowl commercial.

Marszalek is set to serve as CEO for both Crypto.com and AI.com.

Marszalek launched Crypto.com in 2016, formerly known as Monaco. The company eventually acquired the Crypto.com domain, when it was reportedly worth $5 to 10 million. It has since grown into one of the world’s largest crypto exchanges, with more than 150 million retail users. Now Marszalek appears to be betting he can do the same in the AI space.

“When we started Crypto.com there were around a thousand different exchanges, and we somehow managed to make it work,” Marszalek told The Financial Times. “We will make this [AI.com] work one way or another.”

He added, “I thought it was quite interesting that one person can own two domains that stand for such important categories.”

He has reportedly already received interest from buyers for the domain, but believes AI.com will help the company build brand awareness and trust with customers.

Cyrpto.com is no stranger to big, splashy marketing schemes. In 2021, it reached a $700 million multi-decade deal to rename Staples Center to the “Crypto.com Arena.”

According to a September 7 report by Bloomberg, Premier League (PL) clubs have secured a record-breaking $170 million in sponsorship deals from crypto companies for the 2024/25 season.

This uptick comes as league participants face tightening restrictions on gambling sponsorships, which have traditionally been a major source of revenue for them.

Crypto Sponsorships on the Rise

Per the report, several top clubs have already signed major crypto deals. For instance, leading crypto exchange Kraken is sponsoring Tottenham Hotspur, La Liga’s Atlético Madrid, as well as RB Leipzig from the German Bundesliga.

Meanwhile, in June 2023, reigning Premier League champions Manchester City extended their partnership with OKX for three years in a deal that will cost the platform $70 million.

Another crypto exchange, Crypto.com, is also heavily involved in football. The company, which owns the naming rights to the former Staples Center, hosting the Los Angeles Lakers and Los Angeles Clippers, among others, announced in August that it will sponsor UEFA’s Champions League until 2027.

The crypto sponsorship influx isn’t limited to just the biggest names in the biggest leagues; Turkish side Galatasaray recently signed a two-season deal with blockchain analytics firm Arkham Intelligence, worth about $4 million, to have its logo featured on the team’s shirt sleeves.

Gambling Out, Crypto In

For PL clubs, these partnerships mark a major shift in the sponsorship landscape, especially with a looming proscription on front-of-shirt gambling ads by mid-2026. This is in addition to a 2019 “whistle-to-whistle” ban on gambling ads during live matches.

During the 2023/24 season, eight teams had front-of-shirt gambling sponsors, collectively earning them nearly $80 million per year.

However, according to Daniel McDonagh, an associate at UK law firm Charles Russell Speechlys, who was quoted in the Bloomberg report, crypto firms are now stepping in to fill the vacuum caused by the limitations on gambling sponsorship.

Some feel the move is part of efforts to clean up the image of the digital asset industry following the bad press that came with the collapses of several high-profile enterprises, including Three Arrows Capital (3AC), Voyager Digital, and FTX.

SPECIAL OFFER (Sponsored)

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER 2024 at BYDFi Exchange: Up to $2,888 welcome reward, use this link to register and open a 100 USDT-M position for free!

Several crypto exchanges are taking steps to adhere to recently imposed regulations by the UK government. These regulations require crypto entities to inform users about the risks associated with trading digital assets and to promote their services responsibly.

These measures have been implemented as part of the Financial Services and Markets Act in the UK, which has expanded its scope to include firms dealing with crypto and stablecoins, subjecting them to the same regulatory standards as traditional financial services.

Adapting to UK Regulations

In the case of Coinbase’s UK users, compliance involves disclosing their investor type and completing a form confirming their understanding of the high-risk nature of crypto investments, aligning with guidelines from the UK Financial Conduct Authority (FCA). In an email to its UK users, Coinbase has made it clear that both tasks must be completed to retain access to their accounts.

@coinbaseuk so you are telling us to complete the UK FCA declarations, Task 1 & 2 but they are no where to be found on the app or logging in on a computer, what a joke! I didn’t have this problem with other exchanges. pic.twitter.com/pwLOem6Yls

A similar approach was taken by the Seychelles-based OKX, which issued a statement on January 2 stating its intention to implement new requirements in compliance with rules set by the UK’s regulator. Starting from January 8, UK users on OKX will be required to complete two questionnaires.

The first questionnaire aims to ensure users are informed about the risks associated with crypto investments and will categorize users based on their investor profiles. The second questionnaire will inquire about users’ knowledge and experience in crypto investing to assess their understanding of certain topics and associated risks.

Users failing to complete these tasks risk losing access to their accounts.

Besides Coinbase and OKX, Crypto.com and Gemini have also expressed their commitment to meeting UK investor protection standards and ensuring that customers understand the risks involved in investing in crypto, the report said. They are actively working with local regulators to provide the necessary knowledge for users to make informed investment decisions.

Significance of January 8

The significance of January 8 lies in the fact that individuals using these platforms are obligated to complete a declaration detailing their investor profile and participate in a questionnaire focusing on financial services and regulations. This declaration requires users to identify themselves as either high-net-worth individuals or restricted investors, depending on specific criteria.

The ultimate objective of these procedures is to promote responsible trading and protect investors. As such, crypto firms are required to secure authorization or registration from the Financial Conduct Authority (FCA) to promote cryptoassets to retail customers.

SPECIAL OFFER (Sponsored)

Binance Free $100 (Exclusive): Use this link to register and receive $100 free and 10% off fees on Binance Futures first month (terms).

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

We’re currently in the middle of the industry contagion and market panic taking shape. Although FTX and Alameda have fallen, many more players across funds, market makers, exchanges, miners and other businesses will follow suit. This is a similar playbook to what we’ve seen before in the previous crash sparked by Luna, except that this one will be more impactful to the market. This is the proper cleansing and washout from the misallocation of capital, speculation and excessive leverage that come with the global economic liquidity tide going back out.

That said, everyone is quick to jump on the next domino to fall. It’s natural. Most information surrounding balance sheets and hidden leverage in the system is unknown while new information and developments in real time are flowing out every half hour, it seems. Exchanges are under the spotlight right now and the market is watching their every move and transaction. There’s likely no exchange that is going to be as egregious with client funds as FTX and Alameda were, but we don’t know which exchanges can or cannot survive a bank run.

As shown by the market’s reaction, Crypto.com’s Cronos token (CRO), fell 55% in a week before getting some relief over the last day. There’s been a parabolic trend of withdrawals — a bank run — on the exchange over the last two days with the CEO doing the media rounds to assure everyone that withdrawals are processing fine and that they will survive.

Huobi token (HT) follows the same path, down nearly 60% in the last two weeks. Huobi recently provided their list of assets on the platform, showing around $900 million in HT owned by both Huobi Global and Huobi users. It’s not clear what percentage of that $900 million is owned by Huobi Global, but it’s quite the haircut. Exchanges everywhere have been scrambling to provide some version of proof of reserves in attempting to calm the market.

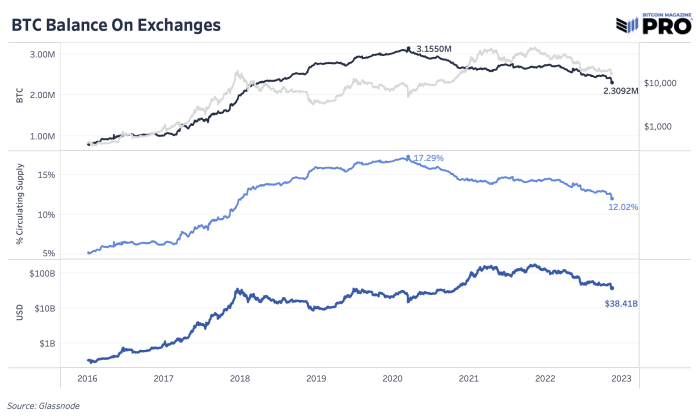

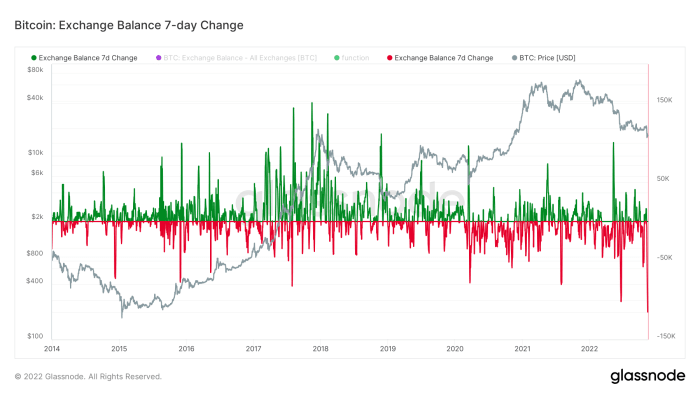

In terms of bitcoin leaving exchanges, it’s been a similar trend for the last three major market panic events: the March 2020 COVID crash, the Luna crash and now the FTX and Alameda crash. Bitcoin flies off exchanges as exchange and counterparty risk becomes priority No. 1 to mitigate. Overall, this is a welcome trend with over 122,000 bitcoin flowing out of exchanges over the last 30 days. It’s the lack of transparency, trust and excessive leverage in centralized institutions that have fueled the latest fall.

Having more of the bitcoin supply in self-custody is the way to counter this risk in the future. That said, assuming all of this bitcoin is going to self-custody and is intended to not come back to the market is a broad, unlikely assumption. Likely, market participants are taking whatever precaution they can regardless if their intent is to store this bitcoin long-term versus sending it back to an exchange later on.

In previous times, bitcoin flowing in and out of exchanges was more of a signal for price, but as more paper bitcoin, wrapped bitcoin on other chains and bitcoin financial products have grown, bitcoin exchange flows are more reflective of current user trends despite the last two major exchange outflows marking local price bottoms. Just 12.02% of bitcoin supply lives on exchanges today, down from its 2020 high of 17.29%. Although we’re only halfway through the month, November 2022 is shaping up to be the largest outflow month in history.

Bitcoin balances on exchanges continues to trend down since March 2020.

Bitcoin is leaving exchanges at a record pace.

The silver lining of the industry’s largest-ever exchange collapse is that a broad sense of distrust in counterparties and self-sovereign practices are set to increase among buyers of bitcoin going forward. While many have been speaking for over a decade on the importance of personal custody for the world’s first decentralized digital bearer asset, it often fell on deaf ears, as financial institutions like FTX seemed credible and trustworthy. Fraud assuredly can change that.

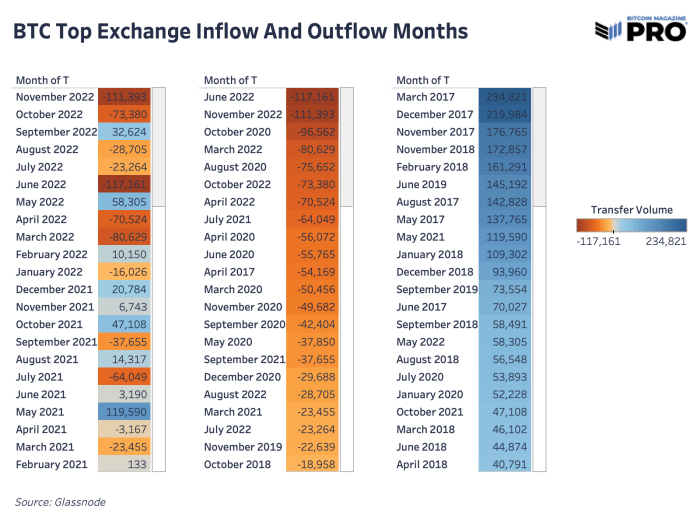

This dynamic, and the potential for greater amounts of contagion among the crypto space, has users fleeing to personal custody, with this past week bringing in the largest week-over-week decline in bitcoin on exchanges at -115,200 BTC.

This past week was the largest week-over-week decline in bitcoin on exchanges.

Interestingly enough, this sell-off was unique in the sense that unlike previous sell-offs in recent years, it wasn’t triggered by a flood of bitcoin being sent to exchanges, instead moreso by an implosion of illiquid crypto collateral without many (or in the case of FTT, any) natural buyers.

Given our immense focus on the risks of crypto-native contagion over the previous six months, we highly recommend our readers learn about and look into the prospects of self-custody; if nothing else, for the ease of mind.

Crypto.com announces multiple updates following a hack that resulted in millions in total losses, … [+] though the exchange said all affected individuals were reimbursed. (Photo illustration by Jakub Porzycki/NurPhoto via Getty Images)

NurPhoto via Getty Images

Crypto.com, one of the biggest and best known cryptocurrency exchanges in the world now backed by superstar actor Matt Damon, has admitted that 483 of its users were hit in a hack earlier this month, leading to unauthorized withdrawals of bitcoin and Ether worth $35 million. The company had initially said $15 million was taken in the heist.

“On 17 January 2022, Crypto.com learned that a small number of users had unauthorized crypto withdrawals on their accounts,” Cyrpto.com wrote in a post on Thursday. “Crypto.com promptly suspended withdrawals for all tokens to initiate an investigation and worked around the clock to address the issue. No customers experienced a loss of funds. In the majority of cases we prevented the unauthorized withdrawal, and in all other cases customers were fully reimbursed.”

The company said that on Monday it saw that for a handful of accounts, transactions were being approved without the second-factor of authentication (the additional one-time code beyond the password allowing access to an account) being entered by a user. As it investigated, all withdrawals across Crypto.com were put on hold, lasting 14 hours. It then required all customers to login again and go through a new two-factor authentication process.

As an additional measure, Crypto.com introduced a feature that means when a new address is added as a payee on an account, the user will get notifications and have 24 hours to cancel any payment if they didn’t authorize it.

Finally, it’s announced the Worldwide Account Protection Program (WAPP), promising to restore funds up to $250,000 for users who qualify. To qualify, users have to be using multi-factor authentication and have filed a police report that it can show Crypto.com. “While we are reminded of the existence of bad actors intent on committing fraud, this new Worldwide Account Protection Program, along with our new MFA [multi-factor authentication] infrastructure, gives our users unprecedented protection of their funds, and hopefully, peace of mind,” said Kris Marszalek, cofounder and CEO of Crypto.com.

There remains little in the way of an explanation of how the attack actually occurred, however. The internal investigation continues.