On Wednesday, the U.S. Securities and Exchange Commission for the first time greenlighted several exchange-traded funds investing directly in bitcoin.

But the 24 hours leading up to that approval were chaotic, to say the least.

The SEC approved the launch of 11 bitcoin BTCUSD, +0.09%

ETFs, according to a filing posted on the regulatory agency’s website. The ETFs are due to start trading on Thursday.

On Tuesday, however, the SEC’s official account on X, formerly known as Twitter, published what the agency described as an “unauthorized” post indicating that it had approved the spot bitcoin ETFs. In reality, the regulator had not approved any such ETFs as of Tuesday and its X account had been “compromised,” SEC Chair Gary Gensler said on the social-media platform. The SEC subsequently deleted the unauthorized post.

The agency found “there was unauthorized access to and activity on” the its X account by “an unknown party,” an SEC spokesperson said on Tuesday, adding that the “unauthorized access has been terminated” and that the SEC would work with law enforcement to investigate the matter.

Bitcoin’s price briefly shot 2% higher after the unauthorized tweet went out on Tuesday before soon pulling back.

Then on Wednesday, shortly before the U.S. stock market closed for the day, the SEC posted an actual approval order of bitcoin ETFs on its website — but the link was soon broken, leading to an “error 404” page. The same filing was later reposted by the SEC.

It is unclear why the first link was broken. A SEC spokesperson did not respond to an email seeking comment on the matter.

The events of the past 24 hours have proven “a bit embarrassing” for the SEC, especially as the agency has stressed that cryptocurrencies are exceptionally risky and vulnerable to market manipulation, according to Greg Magadini, director of derivatives at Amberdata.

Despite those warnings, Magadini said he doesn’t expect investors to be deterred from investing in the bitcoin ETFs.

Bitcoin has actually seen lower volatility on Tuesday and Wednesday than options traders had priced in, Magadini said. The crypto was up about 0.4% over the past 24 hours to around $46,400 on Wednesday evening, according to CoinDesk data.

Steven Lubka, head of private clients and family offices at Swan Bitcoin, echoed Magadini’s point, noting that the hiccups on the way to SEC approval are unlikely to impact investor interest in the funds.

“Ultimately, the SEC is not the one that launches the ETFs,” Lubka said in a call. “If anything, it shows how much attention is on these ETF products.”

The U.S. Securities and Exchange Commission voted Wednesday to allow mainstream investors to buy and sell bitcoin as easily as stocks and mutual funds, a decision hailed by the industry as a game changer.

The SEC decision clears the way for the first U.S. exchange-traded funds that hold bitcoin to be sold to the public. Expectations of U.S. regulatory approval for such funds drove the price of bitcoin to the highest level in about two years. The digital currency fell to just below $46,000 late Wednesday, up from $17,000 in January 2023.

Stock futures traded flat Tuesday, a day after the S&P 500 finished up 0.5% and moved closer to its all-time. The broad market index stands just 1.2% below its record of 4,796.56 reached in early January 2022.

Continue reading this article with a Barron’s subscription.

Blockchain-based private credit is gaining traction in 2023 as companies seek financing in a high-interest-rate environment.

According to data from RWA.xyz, blockchain-powered private loans have surged by 55%, reaching approximately $581.6 million as of Dec. 18. While this figure is below the peak of nearly $1.5 billion in June 2022, it represents a noteworthy shift as the total loans value surpassed the $4.5 billion mark.

Active blockchain-based loans value by protocol | Source: rwa.xyz

As reported by Bloomberg, the traditional private credit market remains dominant with a value of $1.6 trillion, dwarfing the emerging blockchain-based private credit sector.

Among nine RWA protocols, only one extends its services beyond Ethereum to Solana, while another operates on Ethereum’s sidechain, Polygon. Currently, Centrifuge leads in active value, boasting over $255 million in active loans and a total loan value exceeding $492 million, according to RWA.xyz data.

RWA protocols ranged by active loans value | Source: rwa.xyz

Blockchain lending, leveraging increased transparency and smart contracts, is acknowledged for reducing risks and lowering borrowing rates compared to the slower and more opaque traditional private credit market. This evolving landscape is enticing for investors, with blockchain protocols charging borrowers less than 10% APR, a significant contrast to the 15% to 20% rates prevalent in traditional finance.

Crypto giants are also entering the blockchain-based private credit space with new developments, such as Project Diamond by Coinbase Asset Management. As crypto.news earlier reported, the new product leverages Ethereum’s layer-2 scaling network, Base, and integrates Coinbase’s components, including the exchange’s Prime’s services as well as web3 crypto wallet, and Circle’s USDC stablecoin.

Currently, Project Diamond is accessible to registered institutional users outside the U.S. The launch occurs amid intense competition to integrate traditional financial assets like bonds and credit into blockchain systems. This process, known as the tokenization of real-world assets, is believed to enhance settlement speeds, reduce operational costs, and increase transparency.

Yields on 3-month BX:TMUBMUSD03M

and 6-month BX:TMUBMUSD06M

Treasury bills have been seeing yields north of 5% since March when Silicon Valley Bank’s collapse ignited fears of a broader instability in the U.S. banking sector from rapid-fire Fed rate hikes.

Six months later, the Fed, in its final meeting of the year, opted to keep its policy rate unchanged at 5.25% to 5.5%, a 22-year high, but Powell also finally signaled that enough was likely enough, and that a policy pivot to interest rate cuts was likely next year.

Importantly, the central bank chair also said he doesn’t want to make the mistake of keeping borrowing costs too high for too long. Powell’s comments helped lift the Dow Jones Industrial Average DJIA

above 37,000 for the first time ever on Wednesday, while the blue-chip index on Friday scored a third record close in a row.

“People were really shocked by Powell’s comments,” said Robert Tipp, chief investment strategist, at PGIM Fixed Income. Rather than dampen rate-cut exuberance building in markets, Powell instead opened the door to rate cuts by midyear, he said.

“Eventually, you end up with a lower fed-funds rate,” Tipp said in an interview. The risk is that cuts come suddenly, and can erase 5% yields on T-bills, money-market funds and other “cash-like” investments in the blink of an eye.

Swift pace of Fed cuts

When the Fed cut rates in the past 30 years it has been swift about it, often bringing them down quickly.

Fed rate-cutting cycles since the ’90s trace the sharp pullback also seen in 3-month T-bill rates, as shown below. They fell to about 1% from 6.5% after the early 2000 dot-com stock bust. They also dropped to almost zero from 5% in the teeth of the global financial crisis in 2008, and raced back down to a bottom during the COVID crisis in 2020.

Rates on 3-month Treasury bills dropped suddenly in past Fed rate-cutting cycles

FRED data

“I don’t think we are moving, in any way, back to a zero interest-rate world,” said Tim Horan, chief investment officer fixed income at Chilton Trust. “We are going to still be in a world where real interest rates matter.”

Burt Horan also said the market has reacted to Powell’s pivot signal by “partying on,” pointing to stocks that were back to record territory and benchmark 10-year Treasury yield’s BX:TMUBMUSD10Y

that has dropped from a 5% peak in October to 3.927% Friday, the lowest yield in about five months.

“The question now, in my mind,” Horan said, is how does the Fed orchestrate a pivot to rate cuts if financial conditions continue to loosen meanwhile.

“When they begin, the are going to continue with rate cuts,” said Horan, a former Fed staffer. With that, he expects the Fed to remain very cautious before pulling the trigger on the first cut of the cycle.

“What we are witnessing,” he said, “is a repositioning for that.”

Pivoting on the pivot

The most recent data for money-market funds shows a shift, even if temporary, out of “cash-like” assets.

The rush into money-market funds, which continued to attract record levels of assets this year after the failure of Silicon Valley Bank, fell in the past week by about $11.6 billion to roughly $5.9 trillion through Dec. 13, according to the Investment Company Institute.

Investors also pulled about $2.6 billion out of short and intermediate government and Treasury fixed income exchange-traded funds in the past week, according to the latest LSEG Lipper data.

Tipp at PGIM Fixed Income said he expects to see another “ping pong” year in long-term yields, akin to the volatility of 2023, with the 10-year yield likely to hinge on economic data, and what it means for the Fed as it works on the last leg of getting inflation down to its 2% annual target.

“The big driver in bonds is going to be the yield,” Tipp said. “If you are extending duration in bonds, you have a lot more assurance of earning an income stream over people who stay in cash.”

Molly McGown, U.S. rates strategist at TD Securities, said that economic data will continue to be a driving force in signaling if the Fed’s first rate cut of this cycle happens sooner or later.

With that backdrop, she expects next Friday’s reading of the personal-consumption expenditures price index, or PCE, for November to be a focus for markets, especially with Wall Street likely to be more sparsely staffed in the final week before the Christmas holiday.

The PCE is the Fed’s preferred inflation gauge, and it eased to a 3% annual rate in October from 3.4% a month before, but still sits above the Fed’s 2% annual target.

“Our view is that the Fed will hold rates at these levels in first half of 2024, before starting cutting rates in second half and 2025,” said Sid Vaidya, U.S. Wealth Chief Investment Strategist at TD Wealth.

U.S. housing data due on Monday, Tuesday and Wednesday of next week also will be a focus for investors, particularly with 30-year fixed mortgage rate falling below 7% for the first time since August.

The major U.S. stock indexes logged a seventh straight week of gains. The Dow advanced 2.9% for the week, while the S&P 500 SPX

gained 2.5%, ending 1.6% away from its Jan. 3, 2022 record close, according to Dow Jones Market Data.

The Nasdaq Composite Index COMP

advanced 2.9% for the week and the small-cap Russell 2000 index RUT

outperformed, gaining 5.6% for the week.

Federal Reserve Chairman Jerome Powell startled economists with a press conference Wednesday that was viewed as much more dovish than expected.

It was “12 doves a-leaping,” said Michael Feroli, U.S. economist at JPMorgan Chase.

“The Fed can’t believe its luck. The data is going their way,” said Krishna Guha, vice chairman of Evercore ISI.

The first dovish signals came in the Fed’s statement and economic forecasts at 2 p.m. Eastern. First, the Fed penciled in three rate cuts in 2024 instead of two that were projected in September. The Fed also softened its tightening bias by saying they were mulling the need for “any” more hikes.

Then, half an hour later at his press conference, “Chair Powell did nothing to undo the impression of those signals,” said Feroli, in a note to clients. Powell said Fed officials were starting to discuss when to cut rates.

“The question of when it will be appropriate to begin dialing back the policy restraint” was clearly “a discussion for us at out meeting today,” Powell said. Fed officials think the Fed is “likely at or near the peak rate for this cycle.”

While Powell didn’t take rate cuts “off the table,” they are “collecting dust,” said Michael Gregory, deputy chief economist at BMO Capital Markets.

Markets reacted with the 10-year Treasury yield BX:TMUBMUSD10Y

falling to 4.025%.

Traders in derivative markets now see an 80% chance of the first rate cut in March, and now see five quarter-point cuts next year.

Matt Luzzetti, chief U.S. economist at Deutsche Bank, said the main thing learned from Wednesday’s press conference was that Fed Gov. Chris Waller’s dovish comments a few weeks ago were a reflection of the mainstream view at the central bank, rather than a dovish outsider.

Some economists think that March is too soon for a rate cut.

“We still judge rate cuts will commence later rather than sooner, still by the end of the third quarter of 2024,” Gregory of BMO Capital Markets said.

Feroli said he now sees the first rate cut in June, instead of his prior forecast of July, and predicted that the Fed will cut five times by the end of 2024.

Luzzetti of Deutsche Bank sees six rate cuts next year, but not beginning until June as the economy falls into a mild recession.

The Fed doesn’t forecast a recession. Its rate cuts are purely a story of weakening inflation. If there is a recession, the Fed will cut very fast, Luzzetti said.

Diane Swonk, chief economist at KPMG, said the odds of a recession are lower now that the Fed has signaled it will actively take steps to try to avoid one.

The Fed wants the economy to cruise at a lower altitude, and no longer wants a landing, Swonk said in an interview.

That is a 180-degree turn from Powell’s speech in Jackson Hole, Wyo., in the summer of 2022 when he spoke for less than 10 minutes but warned of “pain” and the unfortunate costs of fighting inflation. That speech, “a bucket of ice water,” Swonk said, sent the stock market reeling at the time.

A group of 51 stocks in the benchmark equity index swept to record finishes on Tuesday, the most since April 20, 2022, according to a tally from Dow Jones Market Data.

Equities have been in a year-end rally mode, driven higher by tumbling benchmark yields that finance much of the U.S. economy and expectations of coming interest-rate cuts.

The 10-year Treasury rate BX:TMUBMUSD10Y

fell to 4.2% on Tuesday from a high of about 5% in October.

The Dow Jones Industrial Average DJIA

on Tuesday ended at its third-highest level on record, while the S&P 500 index SPX

and Nasdaq Composite Index COMP

added to a string of new closing highs for 2023. The Dow finished 0.6% away from its record close logged almost two years ago, while the S&P 500 was only 3.2% below its close from the same period, according to Dow Jones Market Data.

The push higher for stocks followed inflation data for November that showed price pressures continued to ease from peak levels, but still were above the Fed’s 2% annual target.

The consumer-price index pegged the annual rate of inflation at 3.1%, down from 3.2% in October, with the “last mile” of inflation expected to be the hardest part to tame.

Investors now will be focused on Wednesday’s Federal Reserve decision. Short-term interest rates are expected to remain unchanged at a 22-year high, but the central bank is expected to update its “dot plot” forecast of rates over a longer time horizon.

“Although the market will focus on the timing of rate cuts, we suspect Chair Powell will be keen to strike notes of caution to avoid financial conditions easing too much further to ensure the Fed continues to see encouraging progress on inflation,” said Emin Hajiyev, senior economist at Insight Investment, in emailed comments.

The rally lifting U.S. stocks to fresh 2023 highs in the year’s home stretch could be at risk if the Federal Reserve on Wednesday crushes expectations for interest-rate cuts in 2024.

U.S. central bankers and investors haven’t exactly been seeing eye-to-eye about when the Fed will start easing its monetary policy, according to Melissa Brown, senior principal of applied research at Axioma.

Traders also have been flip-flopping on their forecasts for rate cuts over the past few months, based on fed-funds futures data.

Oxford Economics/Bloomberg

Given the whipsaw of recent volatility, it isn’t hard to imagine a jittery market backdrop as investors wait to hear from Fed Chairman Jerome Powell on Wednesday, even though the central bank isn’t expected to change its range for short-term interest rates. Since July, the Fed funds rate rate has been at a 22-year high in a 5.25% to 5.5% range.

U.S. stocks advanced this year after a bruising 2022, adding big gains in November, as benchmark 10-year Treasury yields BX:TMUBMUSD10Y

tumbled from a 16-year high of 5%. The Dow Jones Industrial Average DJIA

closed on Friday only 1.5% away from its record close nearly two years ago. The S&P 500 index SPX

booked its highest finish since March 2022, according to Dow Jones Market Data.

“I don’t see any report on the horizon that would really make them [the Fed] change their stance on where we are on monetary policy,” said Alex McGrath, chief investment officer at NorthEnd Private Wealth. It is mostly the expectation of Fed rate cuts next year that have supported stock and bond markets rallies recently, he said.

The Dow Jones closed 9.4% higher on the year through Friday, the S&P 500 was up 19.9% and the Nasdaq Composite advanced 37.6% for the same period, according to FactSet data.

“We have been a little skeptical of the market’s excitement over rate cuts early next year,” said Ed Clissold, chief U.S. strategist at Ned Davis Research.

It takes a gradual process for the Fed to move away from its monetary policy tightening, Clissold told MarketWatch. The Fed is likely to pivot its tone from being very hawkish to neutral, remove the tightening bias, and then talk about rate cuts, noted Clissold.

The bond market on Friday already was again flashing signs of a potential rethink by investors about the path of interest rates in 2024.

HYG,

often a canary in the coal mine for markets, hit pause on a rally that started in late October as benchmark borrowing costs fell, even though the sector has benefited from big inflows of funds in recent weeks.

Treasury yields for 10-year and 30-year BX:TMUBMUSD30Y

bonds also shot higher Friday, echoing volatility that took hold in mid-October.

Mike Sanders, head of fixed income at Madison Investments, has been similarly cautious. “I think the market is a little too aggressive in terms of thinking that cuts are going to occur in March,” Sanders said. It is more likely that the Fed will start cutting rates in the second half of next year, he said.

“I think the biggest thing is that the continued strength in the labor market continues to make the services inflation stickier,” Sanders said. “Right now we just don’t see the weakness that we need to get that down.”

Friday’s U.S. employment report adds to his concerns. About 199,000 new jobs were created in November, the government said Friday. Economists polled by the Wall Street Journal had forecast 190,000 jobs. The report also showed rising wages and a retreating unemployment rate to a four-month low of 3.7% from 3.9%.

The U.S. central bank will likely “try their best to push back on the narrative of cuts coming very soon,” Sanders said. That could be accomplished in its updated “dot plot” interest rate forecast, also due Wednesday, which will provide the Fed’s latest thinking on the likely path of monetary policy. The Fed’s update in September surprised some in the market as it bolstered the central bank’s stance of higher rates for longer.

There’s still a chance that inflation will reaccelerate, Sanders said. “The Fed is worried about the inflation side more than anything else. For them to take the foot off the brake sooner, it just doesn’t do them any good.”

Ahead of the Fed decision, an inflation update is due Tuesday in the November consumer-price index, while the producer-price index is due Wednesday.

Still, seasonality factors could aid the stock market in December. The Dow Jones Industrial Average in December rises about 70% of the time, regardless of whether it is in a bull or bear market, according to historical data.

“The overall market outlook remains constructive,” said Ned Davis’s Clissold. “A soft landing scenario could support the bull market continuing.”

Last week the Dow eked out a gain of less than 0.1%, the S&P 500 edged up 0.2% and the Nasdaq rose 0.7%. All three major indexes went up for a sixth straight week, with the Dow logging its longest weekly winning streak since February 2019, according to Dow Jones Market Data.

U.S. stocks closed higher on Friday, shaking off earlier weakness after a strong monthly jobs report, to clinch a sixth straight week in a row of gains. The Dow Jones Industrial Average DJIA, +0.36%

advanced about 130 points, or 0.4%, to end near 36,247, according to preliminary FactSet data. The S&P 500 index gained 0.4% Friday and the Nasdaq Composite finished 0.5% higher. A string of weekly gains propelled the S&P 500 index SPX, +0.41%

to a fresh 2023 closing high and left the Dow about 1.4% away from its record close set nearly two years ago, according to Dow Jones Market Data. Equities have benefitted from a risk-on tone going into year end, which has been driven by falling 10-year Treasury yields TMUBMUSD10Y, 4.230%

and optimism around the Federal Reserve potentially cutting interest rates in the year ahead. That hinges on if inflation continues to ease. November’s robust jobs report served as a reminder Friday of the tough path of the “last mile” in getting inflation down to the Fed’s 2% annual target. As part of this, the 10-year Treasury yield jumped about 11.5 basis points Friday to 4.244%, but still was about 74 basis points lower than its October high. For the week, the Dow was only fractionally higher, the S&P 500 gained 0.2% and the Nasdaq climbed 0.7%.

November’s sharp pullback in 30-year fixed mortgage rates may not last if the labor market remains strong, said Mark Palim, deputy chief economist at Fannie Mae.

Palim was speaking to the robust jobs report released on Friday, showing the U.S. added 199,000 jobs in November and that wages rose, albeit with the figures somewhat inflated by the return of striking workers from the auto industry and from Hollywood.

Homebuyers can benefit from a robust labor market and the near 80 basis point decline in mortgage rates since the end of October, Palim said. But if the “labor markets remain this strong, we believe the pace of mortgage rate declines will likely not continue in the near term or may partially reverse,” he said in a statement.

The benchmark 30-year fixed mortgage rate was edging down to 7.05% on Friday, after surging to nearly 8% in October, according to Mortgage Daily News.

Optimism around the potential for falling mortgage costs to thaw home sales helped lift shares of Toll Brothers Inc., TOL, +1.86%

and a slew of other homebuilders tracked by the SPDR S&P Homebuilders ETF, XH,

to record highs earlier this week, even while investors in some homebuilder bonds have been sellers in recent weeks.

Yields on 10-year BX:TMUBMUSD10Y

and 30-year Treasury notes BX:TMUBMUSD30Y

were up sharply Friday, to about 4.23% and 4.32%, respectively, but still below the highs of about 5% in October. The surge in long-term borrowing costs was stoked by tough talk by Federal Reserve officials about the need to keep rates higher for longer to bring inflation down to a 2% annual target.

U.S. stocks were up Friday afternoon, shaking off earlier weakness following the jobs report. The Dow Jones Industrial Average DJIA

was 0.2% higher, further narrowing the gap between its last record close set two years ago, the S&P 500 index SPX

and the Nasdaq Composite Index COMP

also were up 0.2%, according to FactSet data.

This is a developing story. Stay tuned for updates here.

The numbers: The University of Michigan’s gauge of consumer sentiment rose to a preliminary December reading of 69.4 from a six-month low of 61.3 in the prior month. This is the highest level since August.

Economists polled by the Wall Street Journal had expected a December reading of 62.4.

Expectations of inflation cooled in early December, according to the report.

Americans think inflation will average a 3.1% rate over the next year, down from 4.5% in the prior month. That’s the lowest level since March 2021.

Expectations for inflation over the next five years fell to 2.8% from 3.2% in November, which was the highest reading in over a decade.

Key details: According to the report, a gauge of consumers’ views on current conditions jumped to 74 in December from 68.3 in the prior month, while a barometer of their expectations of the future rose to 66.4 from 56.8.

Big picture: A lot of factors were behind the increase in confidence, with the solid job market and declining gasoline prices mentioned most often by economists. Stock prices have also been strong. Despite the gains, sentiment is still well below prepandemic levels.

SPX

were higher in early trading on Friday, while the 10-year Treasury yield BX:TMUBMUSD10Y

rose to 4.21% after the solid job report was released earlier in the morning.

Financial conditions are now looser than in September, says economist

Financial conditions in the U.S. are looser than in September, says economist.

Getty Images

The feel-good tone gripping markets in the home stretch of 2023 may not be what the Federal Reserve had penciled in for the holidays.

The stock market in December, once again, has been knocking on the door of record levels, driven by optimism about easing inflation and potential Fed rate cuts next year.

But while the prospect of double-digit equity gains this year would be a reprieve for investors after a brutal 2022, the latest rally also points to looser financial conditions.

Ultimately, the risk of looser financial conditions is that they could backfire, particularly if they rub against the Fed’s own goal of keeping credit restrictive until inflation has been decisively tamed.

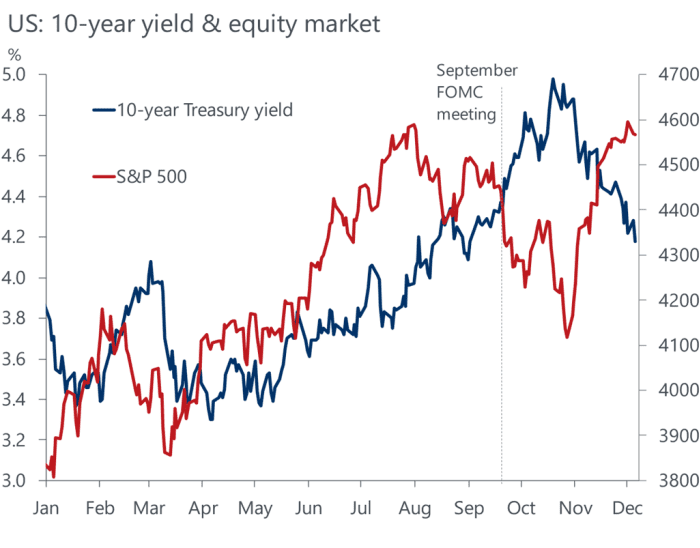

Specifically, the November rally for the S&P 500 index SPX

can be traced to the 10-year Treasury yield BX:TMUBMUSD10Y

dropping to 4.1% on Thursday from a 16-year peak of 5% in October.

Falling 10-year Treasury yields from a 5% peak in October coincides with a sharp rally in the S&P 500 at the tail end of 2023.

Oxford Economics

The Fed only exerts direct control over short-term rates, but 10-year and 30-year Treasury yields BX:TMUBMUSD30Y

are important because they are a peg for pricing auto loans, corporate debt and mortgages.

That makes long-term rates matter a lot to investors in stocks, bonds and other assets, since higher rates can lead to rising defaults, but also can crimp corporate earnings, growth and the U.S. economy.

Michael Pearce, lead U.S. economist at Oxford Economics, thinks the November rally may put Fed officials in a difficult spot ahead of next week’s Dec. 12 to 13 Federal Open Market Committee meeting — the eighth and final policy gathering of 2023.

“The decline in yields and surge in equity prices more than fully unwinds the tightening in conditions seen since the September FOMC meeting,” Pearce said in a Thursday client note.

The Fed next week isn’t expected to raise rates, but instead opt to keep its benchmark rate steady at a 22-year high in a 5.25% to 5.5% range, which was set in July. The hope is that higher rates will keep bringing inflation down to the central bank’s 2% annual target.

Ahead of the Fed’s July meeting, stocks were extending a spring rally into summer, largely driven by shares of six meg-cap technology companies and AI optimism.

Rates in September were kept unchanged, but central bankers also drove home a “higher for longer” message at that meeting, by penciling in only two rate cuts in 2024, instead of four earlier. That spooked markets and triggered a string of monthly losses in stocks.

Pearce said he expects the Fed next week to “push back against the idea that rate cuts could come onto the agenda anytime soon,” but also to “err on the side of leaving rates high for too long.”

That might mean the first rate cut comes in September, he said, later than market odds of a 52.8% chance of the first cut in March, as reflected by Thursday by the CME FedWatch Tool.

Stocks were higher Thursday, poised to snap a three-session drop. A day earlier, the S&P 500 closed 5.2% off its record high set nearly two years ago, the Dow Jones Industrial Average DJIA

was 2% away from its record close and the Nasdaq Composite Index COMP

was almost 12% below its November 2021 record, according to Dow Jones Market Data.

A rally in the U.S. stock and bond markets in the past week defied the bears and fueled hopes for more gains to come by year-end and in 2024 as Wall Street bought into the idea that the economy will pull off a “soft landing” after a run of interest-rate hikes by the Federal Reserve.

But market skeptics are putting investors on alert that the “soft-landing” scenario is still at risk with consumer spending and job growth slowing, along with corporate earnings.

“The equity market is misguided,” said Josh Schachter, senior portfolio manager at Easterly Investment Partners, in a phone interview with MarketWatch. “The markets are behaving in almost a bipolar fashion — some asset classes such as bonds BX:TMUBMUSD10Y,

oil BRN00, -0.29%,

and dollar DXY,

are being priced for a recession, while other assets such as equities and bitcoin BTCUSD, +2.16%,

are priced risk-on.”

U.S. stocks built on their November gains in the past week, with the S&P 500 index SPX

ending at new 2023 high on Friday and the Dow Jones Industrial Average DJIA

logging its fifth week in the green. The rebound in stocks was due in part to bond investors starting to believe the Fed is done raising interest rates and is likely to begin cutting them by the first quarter of 2024.

Meanwhile, the narrative that a resilient labor market and steadier-than-expected economic growth should keep a recession at bay has gained traction, bolstering the “goldilocks” scenario for the financial markets.

Joseph Quinlan, head of CIO market strategy for Merrill and Bank of America Private Bank, said the “softness” in the U.S. consumer sector is visible but not huge, referring to that as “a canary in a coal mine,” he told MarketWatch via phone on Thursday.

The pullback in consumer spending is welcome news for Fed officials, who have increased interest rates 11 times since March 2022 to get inflation back to its preferred target of 2%. However, some analysts are worried that high interest rates and a decline in pandemic savings could eventually translate to weaker consumers in 2024, potentially another sign of a long-predicted slowdown in the U.S. economy.

“One of the things I’m most concerned about is consumers’ ability to continue to pace the economy — you’ve got several headwinds that haven’t really borne completely out yet,” said Jason Heller, senior executive vice president at Coastal Wealth. “Does the consumer continue to behave the way they behaved the last 36 months? I think you will eventually see a slowdown in consumer spending which is going to mandate a slowdown in the labor market.”

Lauren Goodwin, economist and portfolio strategist at New York Life Investments, acknowledged that a modest slowdown in inflation and employment growth means that a “Fed relief rally” in stocks can be sustained, but her concern is this late-cycle limbo is no different than those of the past, which is a moment of “goldilocks” before the very reason that inflation is moderating — slowing economic growth and employment — becomes clear in the data.

That’s why the November employment report, which will be released by the Bureau of Labor Statistics next Friday at 8:30 a.m. Eastern, will be key for investors to watch. The U.S is expected to add 172,500 jobs in November after a 150,000 increase in the prior month, according to economists polled by Dow Jones. The percentage of jobless Americans seeking work is forecast to stay the same at 3.9%, leaving it at the highest level since the beginning of 2022.

In fact, nonfarm payroll report publication days have been among the most volatile for stocks in 2023, compared with the release of monthly consumer-price index readings, which sparked some of the biggest daily up and down moves for the S&P 500 and other major indexes in 2022.

This year, the S&P 500 saw an absolute average percentage change of 1.12% on employment situation release dates, compared with an average percentage move of 0.64% on CPI days, according to figures compiled by Dow Jones Market Data.

That said, analysts are skeptical if the employment data is able to tell “a radically different story” but suggest the labor market will remain relatively tight into 2024, said Quinlan and Lauren Sanfilippo at Merrill and Bank of America Private Bank, in a phone interview.

Corporate America and their shares are telling investors a different story about next year.

With an estimated average S&P 500 earnings growth of 11.7% next year, the U.S. stock market is nowhere near recessionary concerns, said Heller. “We’ve [the stocks] priced in pretty significant growth in 2024.”

Strategists at Merrill and Bank of America Private Bank are in the camp of expecting a “mid-single digit” earnings growth for the S&P 500 in 2024, as earnings have troughed and the economy will fall back to the 2%-level of real growth after high rates confine consumer spending and corporate profits, cooling a red-hot economy.

To be sure, Wall Street analysts tend to overestimate the earnings-per-share (EPS) for the S&P 500, said John Butters, senior earnings analyst at FactSet.

The current bottom-up EPS estimate for the S&P 500 in 2024 is $246.30. If that holds true, that would be the highest EPS number reported by the large-cap index since FactSet began tracking this metric in 1996.

However, over the past 25 years, the average difference between the EPS estimate at the beginning of the year and the actual EPS number has been 6.9%, meaning analysts on average have overestimated the earnings one year in advance, said Butters in a Friday note (see chart below).

Bitcoin has extended its rally on Friday, rising to the loftiest level since May 2022, pushing its yearly gain up to over 130%, on pace to be one of the best performing assets this year.

The crypto BTCUSD, +1.28%

rose about 2.5% over the past 24 hours to around $38,676 Friday afternoon, as excitement about the potential approval of bitcoin exchange-traded funds continues to build. Bitcoin is still 44% down from its all-time high in 2021.

Risk assets in general performed well in November, as concerns eased around several pressure points, including the surge in long-term Treasury yields and inflation, analysts at Grayscale Research wrote in a Friday note.

Despite outperforming many major assets year-to-date, bitcoin underperformed long-term Treasurys and the S&P 500 in November on a volatility-adjusted basis, gaining 9% for the month.

Bloomberg; Grayscale Investments

Sam Callahan, market analyst at Swan Bitcoin, said he expects bitcoin to trade between $36,000 and $40,000 by the end of the year, “provided that the macroeconomic environment doesn’t take a turn for the worse, and barring any significant positive development, such as the approval of a Spot Bitcoin ETF or the adoption of Bitcoin by a major corporation, sovereign-wealth fund, or nation-state.”

Despite bitcoin’s rally so far this year, December has historically been a particularly volatile month for the crypto, since it was created in 2009. It rose seven out of 13 times in December, according to Dow Jones Market Data.

In years when bitcoin gained more than 100% through November, the digital asset saw an average gain of 20% in December, rising four of the six times it occurred, according to Dow Jones Market Data.

To be sure, bitcoin has a relatively short history and was particularly volatile during its early years.

The Reserve Bank of India’s recent decision to hike risk weights on certain segments of consumer credit is a reflection that the central bank has “turned cautious from conscious”, India Ratings said.

While banks, with their strong capital buffers, should be able to largely absorb the incremental capital requirements, NBFCs will need to borrow more from the capital markets leading to an increase in lending rates amid robust demand.

“With sustained pressure on inflationary drivers coupled with strong credit growth, the lending rates could only go up in the near term. Believing the policy rate has peaked out, the RBI is expected to use an array of instruments and levers to nudge the lending rates towards the higher side,” said Soumyajit Niyogi, Director, Core Analytical Group.

The spread between MCLR and repo facility is at a six-year low, suggesting incomplete pass-through of the tightening credit cycle caused by the stiff competition among banks. Even as the repo rate stays at the current level of 6.5 per cent, MCLR could go up modestly, the rating agency said.

System liquidity

However, the key monitorable aspect will be system liquidity from the macro side and balance sheet liquidity from the micro side, it said, adding that high-rated borrowers will continue to benefit from the intense competition in terms of lending cost.

Overall, in its base case scenario, India Ratings does not envisage any large OMO sales, barring regular interventions by the RBI as excess liquidity is likely to correct in Q3 FY24.

“The sustained strong retail lending seems to have become one of the key monitoring factors for the regulator, which also necessitates close monitoring of short-term rates to ensure proper allocation of short-term capital without stoking inflation or financial stability risk,” it said, adding that the RBI wants to maintain system liquidity at an optimum level to avoid excess liquidity causing any risk to financial stability.

Some companies claim they can repair your credit and solve your debt problems quickly. However, you can only rebuild credit and there’s no quick fix to do so. We’ll walk you through why you should be skeptical of companies offering credit repair services and explore other ways to rebuild and maintain strong credit.

The importance of strong credit in Canada

It’s important to have a good credit score so you can get a loan, be approved for a credit card, buy a home and a car. And you want to get the best interest rates when doing so. A credit score may also determine whether a landlord approves your rental application, and employers might even consider credit histories in their hiring process. Having a strong credit score shows you are good at managing debt and credit. In contrast, bad credit suggests you are a risky bet to lenders because you may be having problems with money.

Why someone might reach out to a credit repair service

The average Canadian owes more than $21,000 in consumer debt. When you have a lot of debt and other monthly bills to take care of, it can become difficult to manage and make all of your payments on time, especially amid high inflation and rising costs of living. However, if you don’t manage your payments on time, your credit score will take a hit. Feeling desperate in a financial situation can cause anyone to make a bad decision. But many people run into further financial problems by trying to repair their credit with a quick fix.

How credit repair companies work

Credit repair companies say they will repair your credit by removing negative information from your credit report, thus boosting your credit score—for a costly, upfront fee. They may also offer to negotiate with credit reporting agencies to improve your credit score or encourage you to take out a high-interest loan to pay off your debts. Be aware that these credit repair companies make money from fees, set-up costs and interest, so you may be left with even more debt without any changes to your credit score.

These companies often take advantage of the fact that many Canadians don’t know you can’t remove accurate information from your credit report—even if it’s bad. You should be skeptical if a company says they can remove accurate, negative information from your history.

Pay attention to the warning signs

Many Canadians run into further financial problems as they attempt to “repair” their credit because they fall victim to credit repair scams. Credit repair services are different from not-for-profit credit counselling agencies. The latter are typically a free service offering non-profit financial education and advice. But back to the scams, here are the warning signs that a company offering credit repair services is likely a scam:

They request an “upfront” payment (this is illegal under Canadian consumer protection laws)

They offer instant approval for loans or other credit products without fully understanding your financial situation

They call themselves a “credit repair company”

They request payment by gift cards

They use high-pressure sales tactics

They say they “erase” your negative credit information

They don’t provide a transparent contract (or any contract at all)

They warn you against contacting a credit bureau

How to rebuild your credit in Canada

Accurate negative information on your credit report cannot magically go away; it’s there until it falls off your credit report, which takes about six years. If your credit report isn’t great, the only way you can go about “fixing” it is by rebuilding it with a positive credit history. You have to show your creditors that your financial habits have improved, which takes time. Here’s what you can do to get the ball rolling:

1. Review your credit

It is important to review your credit report regularly by getting a free copy of your credit history from both Equifax Canada and TransUnion. Look over the report to see what’s documented and if the information is correct. For no charge, you can remove incorrect information by filing a dispute with the credit reporting company.

Ever since the collapse of crypto currencies last year, the lawsuits have been flying.

But a series of class-action suits targeting celebrity endorsers of crypto exchanges like FTX and Binance have been piling up in federal court in Miami, all filed by the same group of south Florida lawyers.

The latest suit names global soccer superstar Cristiano Ronaldo for allegedly promoting “the mass solicitation of investments in unregistered securities” sold by Binance, the crypto exchange that was hit with a $4 billion fine last week after pleading guilty to violating the bank secrecy act.

The suit was filed in federal court in the southern district of Florida this week and centered around Ronaldo’s role in a global marketing campaign launched in 2022 for a series of Binance NFTs — or non-fungible tokens, a form of blockchain-backed art works that were, for a brief time, wildly popular.

A representative for Ronaldo didn’t immediately respond to a message seeking comment.

The filing against Ronaldo on Monday came alongside similar class action suits naming Major League Baseball, Formula 1 racing, Mercedes Benz and the advertising giants Dentsu and Wasserman, who created much of FTX’s global promotion campaign.

Messages left with representatives for MLB, Formula 1, Mercedes Benz, Dentsu and Wasserman weren’t immediately returned.

Those suits are the latest in a series of similar class action suits starting last year against celebrity endorsers of failed crypto exchanges such as Voyager and FTX, in which customers lost billions of dollars in deposits.

Over the past 18 months, a group of south Florida lawyers led by Adam Moskowitz have brought the suits on behalf of investors who lost money in last year’s crypto collapse, against paid celebrity endorsers including Shaquille O’Neal, Mark Cuban, Tom Brady, Gisele Bundchen, Shohei Ohtani, Larry David, Steph Curry and Naomi Osaka.

“All of these celebrities were paid hundreds of millions of dollars taken directly from customer deposits,” Moskowitz said in a statement. “Some of the most famous and wealthiest groups in the world may now be held responsible for the dramatic $20 billion dollar crypto collapse and biggest financial scandals in U.S. history.”

Moskowitz, who has been joined in the suits by lawyers with the firms Mark Migdal & Hayden and Boies Schiller and Flexner, headed by famed litigator David Boies, is seeking at least $5 billion in damages from those who helped promote the crypto exchanges.

The cases from last year are ongoing and each of the celebrities named have been fighting the suits in court.

Moskowitz, who specializes in class-action lawsuits, says issues revolving around crypto first got his attention more than two years ago, before the entire market crashed, when he came to believe that the special tokens each exchange was minting amounted to an unregistered security.

He first filed a lawsuit against Voyager early last year, before the exchange collapsed and the Securities and Exchange Commission began filing suits against many in the industry accusing them of dealing in unregistered securities.

“Right then what we were doing started to gain traction,” he said.

A series of favorable court rulings have allowed his cases to gain steam, he said, and has allowed to him to take the lead in such actions.

Apple Inc. AAPL is calling it quits on its credit-card partnership with Goldman Sachs Group Inc. GS, ending the Wall Street bank’s push into consumer lending, according to a Wall Street Journal report Tuesday. The iPhone maker sent a proposal to Goldman to leave the contract within 15 months, according to people briefed on the matter. The exit would cover the companies’ consumer partnership, which includes the credit card the companies launched in 2019 and the savings account rolled out in 2023. It is unclear if Apple has lined up a new issuer for the card.