[ad_1]

Bank of America Reports Earnings Monday. What Wall Street Is Watching.

[ad_2]

[ad_1]

I’ll be 57 next month and am divorced with three kids living with me. One is 28, she’s working, another is 21 and a senior in college (with a full scholarship) and the youngest is 15 (a sophomore in high school with a full scholarship).

I plan to retire at the end of next year with $25,000 in credit card debt and 15 more years to pay my mortgage. The credit cards have 0% interest. I have a good medical benefit when I retire and it will cover my two sons under 26 years old. My monthly expenses are $2,000, including life insurance, utilities, and a car payment.

My mortgage is around $4,000 monthly impounded. The interest rate is 2% until January 2022, then 3% until January 2023 and the remaining loan is 4.5%. Is it worth it to refinance to a lower rate? I also plan to just pay the principal and pay interest in December and April. I have two credit cards: one that totals $20,000, where the 0% promo ends in April 2021, and another with $4,500 where the 0% interest promo ends this December.

I work for the state and have a pension and 401(k) and 457 investments that total $110,000. I also have one month’s worth of expenses in an emergency fund. I can only apply for a loan to the retirement accounts while employed.

I would like to ask if retiring will be a good idea. If so, is it appropriate to take a loan with my investment to pay off the credit card debt before retiring? Based on our benefit, I don’t have to repay the debt (to the 401(k)) after my retirement unless I win the lottery or something. There won’t be a penalty. My annual gross income is $96,000.

I’m a cohabitant with my ex on the house but get no contribution from him at all. I am working with my lawyer to see if I have the right to kick him out of the house.

Please help.

Thank you.

CDT

Dear CDT,

You have a lot to juggle, so the fact that you’re reaching out to someone for some financial guidance should be deemed an accomplishment all its own!

The truth is, you may want to hold off on retiring if you can. Having $110,000 in retirement accounts is great, and you don’t want to have to start dwindling that down while also trying to manage a way to effectively pay down credit card debt and a mortgage. Should an emergency arise, taking a big chunk out of that nest egg could end up hurting you significantly in the long run.

“I think she needs to take a hard look at her income and expenses,” said Tammy Wener, a financial adviser and co-founder of RW Financial Planning. “When it comes to retirement, so many things are out of your control, like inflation and investment return. The one thing you do have control over is expenses.” Furthermore, your pension may be enough to maintain your lifestyle — though advisers wondered what exactly you would be getting from that pension every month — but you would still be better off with a larger nest egg to fall back on.

Say you retire next year after all, but you still have credit card debt and hefty bills to pay. Any retirement income you have with and outside of your current funds may not be sufficient for your current living expenses, and if in a few years you realize this, you could end up back in the workforce — though it may be hard to get the same or a similar job you already have.

Let’s look at your 401(k) and 457 plans for a moment. You said you could take a loan and based on your benefit you don’t need to pay it back, but you should be extremely cautious about this. With 401(k) loans, employees may be required to repay that loan if they’re separated from their employers, so this is a stipulation you should absolutely verify. If there was any misunderstanding as to how a loan is treated, that remaining loan would be treated as taxable income when you left your job, Wener said.

Financial advisers usually caution investors not to take loans and withdrawals from retirement accounts if they can avoid it, and in your case, this may be especially true as you plan to retire in the next year. When you take a loan, you may be paying yourself and your account back, but your balance is reduced by the amount of the loan, which means you could lose out on investment returns. In the midst of this pandemic, many of the Americans who took a loan or withdrawal regret it now, a recent survey found. “I would not recommend ‘swapping debt’ by taking a loan from her investments,” said Hank Fox, a financial planner. “Instead, she should pay whatever amount is due each month to avoid the finance charges and continue to pay-down the balances.”

Don’t miss: 5 ways to find free financial advice

Also, consider what would happen if you continued to work: you’d still be able to contribute to a retirement account, boost your savings and, if applicable, reap the rewards with an employer match. You’d also narrow the amount of time you have between retirement and when you can claim Social Security benefits, Fox said.

Outside of the retirement accounts, you should try to build a “sizable” emergency fund, Wener said. Financial advisers typically suggest three to six months’ worth of living expenses, though you might want to strive for closer to six to offset any undesirable scenarios.

I’m not sure what the motivation was to retire next year, but if you can delay it, this may be the best solution. “The first thing I would recommend is that she reconsider retiring next year,” Fox said. “Since she will be 57 in November and assuming she is in good health, she should expect to be in retirement for 30 years or more.”

If postponing retirement is not an option, and it isn’t always, he suggests reducing or eliminating your mortgage, since it’s your largest expense by far. You could refinance, Wener said. Interest rates are very low these days, and while you may end up paying a little more every month for the next two years compared with that 2% rate you currently have, you’d end up paying the same and then less from February 2022 and on.

As for your credit cards, having a 0% interest rate is such a huge help in paying off debts faster, so you should try to extend that benefit, either by calling and asking about your options with your current credit card company or looking at alternative 0% interest cards.

A financial adviser — specifically, a Certified Financial Planner — could really help you crunch the numbers and find meaningful ways to make the most of the money you have now and will be getting in retirement, said Vince Clanton, principal and investment adviser representative at Chancellor Wealth Management.

An adviser can gather information on your current earnings and expenses, retirement savings, potential Social Security benefits and pension and create a financial plan to help you navigate retirement. “Voluntary retirement, and particularly early retirement, are very big decisions,” Clanton said. “It’s extremely important to know and understand all of the variables.”

Letters are edited for clarity.

Have a question about your own retirement savings? Email us at HelpMeRetire@marketwatch.com

[ad_2]

[ad_1]

Opinions expressed by Entrepreneur contributors are their own.

The path to success as an entrepreneur can take many different forms, and no matter what path you choose, difficulties will always exist. It’s easy to become a bit of a skeptic when it comes to doing business. The truth is, it’s not easy — and it’s not for everyone. It takes hard work and determination to succeed, no matter how cliché it sounds.

You also have to recognize challenges as bottlenecks — not as signs of failure, but as obstacles to be overcome. To prepare yourself for any difficulties you might encounter along your entrepreneurial journey, here are some of the most common challenges you should expect to face, along with tips on how to overcome them:

Related: Entrepreneurship Is All About Overcoming Obstacles

Cash is one of the most challenging elements of running a business. You have to ensure enough cash is coming in to keep everything and everyone up and running. Companies often go through periods of low cash flow, during which they may have to delay or cancel projects, hire less staff or even shut down entirely.

Why do entrepreneurs end up low on cash? Well, most of the time, it is a result of a slowing economy, but it can also occur due to a client going bankrupt or because marketing efforts aren’t working as well as initially anticipated. It could also be that they might not have predicted the amount of money they would need for various aspects of their business.

When you find yourself in any of these scenarios, managing your cash flow should be your top priority. You can always get a line of credit from another bank or finance company that charges very low-interest rates. Managing your credit, however, is a different topic we’ll get into later.

Try to be on the right side of your own decisions. If you are doing something that you’re passionate about, then it’s easy to convince yourself that people will want what you have to offer. You need to make sure that every decision you make is made with confidence and conviction.

It’s also important to understand that it’s normal for people to be indifferent toward a certain idea or person. Perhaps they have a preexisting opinion about you or your business that prevents them from considering it fully.

Besides preconceived notions, consider that naysayers’ lack of interest might also be caused by familiarity, ignorance and fear. You must uncover what causes them and provide a solution.

Having doubters doesn’t mean your idea or business isn’t good — it could mean that it just needs more work! DOUBTS ARE GOOD! They mean that something is missing from what would be perfect.

Related: How to Maintain Motivation When Surrounded by Naysayers

In the world of entrepreneurship, there are many ways clients can influence your business. They can be a great source of knowledge, especially if they’re interested in what you’re doing and how you do it. In this way, clients can be valuable resources for your company.

However, it’s important to remember that they are also customers who will want things from you. So, while they may share information and provide valuable feedback, they may also expect different things from you than they did before.

The difficulty here is that it’s up to you as an entrepreneur to make sure that their expectations are met and that they feel satisfied with their experience with your business. As an entrepreneur, having strong relationships with your clients is the key to remaining competitive while growing your business.

Entrepreneurship is a risky endeavor, and credit can be a big problem. But it won’t be a big problem if you know what you’re doing.

The credit system is a lot like a double-edged sword. On one side, it can help entrepreneurs get the resources they need to start and grow their businesses. On the other side, it can be a hindrance when it comes to keeping your business afloat.

For example, if you have a loan or line of credit with a bank, your business will have to pay interest on that loan every month. This means that if you don’t pay your bills on time, the bank will take more money out of your account than they’re supposed to — and then charge you more in interest for the money they took out of your account. This can lead to serious financial problems for you and your business.

To overcome problems with credit and keep your business running smoothly, you’ll need to have an understanding of all the options available to you and then make sure you take advantage of them.

Related: 3 Tips for Young Entrepreneurs on the Power of Credit

Having a lot of cash on hand might seem like a good sign, but you must also strike a balance between having an excessive amount out of precaution and not having enough. When you have too much cash, you may be missing out on investment opportunities that could increase your profits.

Instead of letting naysayers scare you away from making progress, focus on finding out where the holes are and filling them in before moving forward.

Give your clients a sense of ownership, and acknowledge the importance of the role they play in your company’s success.

Be smart when it comes to credit, and be aware of all the options available to you.

[ad_2]

Roy Dekel

Source link

[ad_1]

The U.S. stock market benchmark rebounded from a steep loss on the day when the government published hot inflation numbers.

The S&P 500 Index ended Thursday with a 2.6% gain after investors took a closer look and saw a significant improvement from July through September, as Rex Nutting explained.

The whipsaw action wasn’t limited to stocks, and was described by Rick Rieder, the chief investment officer for global fixed income at BlackRock, as “one of the craziest days” of his career.

Some investors who focus on stocks might not realize that the bond market is much larger, and that its movements can cause government and central-bank policies to shift. Larry McDonald, founder of The Bear Traps Report and author of “A Colossal Failure of Common Sense,” which described the 2008 failure of Lehman Brothers, explained just how bad the action was in the U.K. bond market over the past few weeks, when 30-year government bonds issued in December traded as low as 24 cents on the dollar. He also predicted what will happen if the Federal Reserve continues on its current course of interest-rate increases.

Related outlooks for interest rates:

Michael Brush argues the Federal Reserve is moving too quickly to raise interest rates and cool the U.S. economy. He expects a rapid decline in inflation and a new bull market for stocks. In a column, he shares five sentiment indicators that suggest it is time to buy stocks — especially this group of companies.

Beth Pinsker explains how to make sure your investments are best diversified to fit your needs during time of uncertainty in all financial markets.

The Social Security Administration has announced that its cost-of-living adjustment (COLA) for 2023 will be 8.7%, the largest increase in four decades. There is more to the story, including tax implications and changes to Medicare, as Jessica Hall and Alessandra Malito explain.

Related: Can I stop and restart Social Security benefits?

Medicare’s annual open enrollment season runs from Oct. 15 to Dec. 7. The majority of Medicare recipients don’t review their plans each year, which can cost them a lot of money. Here’s how to approach Medicare’s 2023 enrollment period.

Stefani Reynolds/Agence France-Presse/Getty Images

Freddie Mac said interest rates on 30-year mortgage loans averaged 6.92% on Oct. 13, up from 3.05% a year earlier. Mortgage Daily said rates had hit 7.10% — the highest in 20 years — and economists are warning these levels could be a “new normal.”

A homeowner locked-in with a low interest rate on their mortgage loan will be reluctant to sell. And some would-be buyers may now be priced out of the market because of much higher loan payments. Here’s what economists expect for home prices in 2023.

More housing coverage from Aarthi Swaminathan: ‘No housing market is immune to home-price declines’: Home values are already falling in these pandemic boomtowns.

When you fill out the Free Application for Federal Student Aid, or FAFSA, to help pay for your child’s college education, there may be a problem — old news. The form reflects your financial situation up to two years ago, and things may have worsened recently. Here’s how to make sure schools have the most recent information to help you get as much financial aid as possible.

Joe Raedle/Getty Images

Hurricanes are nothing new to Floridians, but insurers in the state are losing money even though premiums have doubled over the past five years. Shahid S. Hamid, the director of the Laboratory for Insurance at Florida International University, explains why the Florida insurance market is so distorted.

istock

Home swapping can give you an opportunity to live as a local in a faraway place while spending much less than you would as a tourist. Here’s how it works.

Want more from MarketWatch? Sign up for this and other newsletters, and get the latest news, personal finance and investing advice.

[ad_2]

[ad_1]

JPMorgan Chase & Co. shares rose Friday after the megabank beat analyst targets for third-quarter profit and revenue and said it would top forecasts for its net interest in come in the coming quarter.

In a busy day for bank earnings, Wells Fargo & Co.

WFC,

fell short of earnings target but its stock rose in premarket trades as it beat revenue estimates.

Morgan Stanley

MS,

shares fell after it missed Wall Street’s targets for earnings and revenue.

Citigroup Inc.

C,

shares rose after beating its profit mark, although revenue fell 1% after breaking out the impact of divestitures.

Overall, banks benefited from higher interest rates and strong trading volumes, but investment banking deal activity fell sharply. Banks also channeled more capital into reserves and away from their collective bottom lines to prepare for a potential economic downturn.

As the largest bank in the U.S. and a bellwether for the sector, JPMorgan Chase

JPM,

turned in a “solid performance” in the latest quarter, in the words of Chief Executive Jamie Dimon.

The bank said it expects to meet its capital requirements under the international Basel III banking guidelines and resume stock buybacks early in 2023.

“In the U.S., consumers continue to spend with solid balance sheets, job openings are plentiful and businesses remain healthy,” Dimon said. “However, there are significant headwinds immediately in front of us – stubbornly high inflation leading to higher global interest rates, the uncertain impacts of quantitative tightening, the war in Ukraine, which is increasing all geopolitical risks, and the fragile state of oil supply and prices.”

Dimon said the bank remains “prepared for bad outcomes” so it can continue to operate even in the most challenging times.

Dimon’s prepared statement comes a day after the oft-quoted CEO said the U.S. consumer sector remains strong currently, but inflation will start weighing on people by 2023.

Also Read: JPMorgan CEO Dimon says inflation hasn’t dampened consumer spending yet but give it time

JPMorgan Chase’s stock rose 2.4% ahead of Friday’s open after it said its third-quarter net income fell 16.7% to $9.74 billion, or $3.12 a share, from $11.69 billion, or $3.74 a share, in the year-ago quarter.

Third-quarter revenue at the megabank rose to $32.72 billion from $29.65 billion in the year-ago quarter.

Wall Street analysts expected JPMorgan Chase to earn $2.90 a share on revenue of $32.12 billion, according to estimated compiled by FactSet. T

The bank said a net credit reserve build of $808 million ate into its net income for the latest quarter, compared with a net reserve release of $2.1 billion in the prior year.

Net interest income climbed 34% to $17.6 billion and net interest income excluding its Markets unit rose 51% to $16.9 billion on higher interest rates.

JPMorgan Chase’s total assets under management fell 13% to $2.6 trillion in the face of losses in the equities market and difficult conditions in the bond market.

Looking ahead, JPMorgan Chase said it expects fourth-quarter net interest income of about $19 billion, ahead of the $18.2 billion analyst estimate.

Octavio Marenzi, CEO of management consultant company Opimas said the bank’s results were “surprisingly solid” and if you strip away its payments for loan reserves, its profit is basically unchanged.

“Individual lines of business, such as investment banking and mortgages did predictably badly, but this was more than compensated for by strength in other areas of lending and in trading,” Marenzi said.

Shares of JPMorgan Chase have lost 30.9% in 2022 compared with a 17.3% drop by the Dow Jones Industrial Average

DJIA,

and a 23.0% loss by the S&P 500

SPX,

Wells Fargo misses profit target but share rise

Wells Fargo & Co. shares advanced 2% in Friday’s premarket after the bank posted net income of $3.528 billion, or 85 cents a share, for the quarter to end September, down from $5.122 billion, or $1.17 a share, in the year-earlier quarter.

The megabank fell short of the earnings-per-share target of $1.09 a share.

Wells Fargo’s revenue rose to $19.505 billion from $18.834 billion a year ago, ahead of the $18.775 billion FactSet consensus.

Chief Executive Charlie Scharf said performance was “significantly impacted” by $2 billion, or 45 cents a share, in operating losses “related to litigation, customer remediation, and regulatory matters primarily related to a variety of historical matters.”

However, the bank is seeing historically low delinquencies and high payment rates, and the “timing of deterioration in those measures due to high inflation remains unclear. “

The bank set aside $784 million in provisions for loan losses, after reducing them by $1.395 billion a year ago.

Net interest income rose 36%, while noninterest income fell 25%, as mortgage banking income declined.

Citi analyst Keith Horowitz said Wells Fargo turned in a “good” quarter overall, although larger-than-expected one-time charges and a reserve build reduced profits. But Wells Fargo also raised its outlook for net interest income “and we still see upside to 2023 consensus,” Horowitz said.

Shares of Wells Fargo have declined 12% in the year to date.

Morgan Stanley shares fall on results

Morgan Stanley fell 2.6% in premarket trades after the investment bank missed Wall Street’s targets for earnings and revenue amid a drop in deal activity.

Morgan Stanley said its third-quarter net income fell to $2.49 billion, or $1.47 per share, from net income of $3.7 billion, or $1.98 per share in the year-ago quarter.

Third-quarter revenue dropped to $12.99 billion from $14.75 billion.

Wall Street analysts were looking for earnings of $1.52 a share and revenue of $13.29 billion, according to FactSet data.

“Firm performance was resilient and balanced in an uncertain and difficult environment, delivering a 15% return on tangible common equity,” said CEO James Gorman. “Wealth Management added an additional $65 billion in net new assets and produced a pre-tax margin of 28%, excluding integration-related expenses, demonstrating scale and stability despite declining asset values.”

Morgan Stanley shares have lost 19.2% in 2022.

Citi beats targets but shares lose ground

Citigroup shares fell 1.3% in premarket trades Friday after the bank posted stronger-than-expected profit, but revenue fell 1% after breaking out divestiture-related impacts, as growth in net interest income was more than offset by lower non-interest revenue.

Citi said its third-quarter net income dropped to $3.5 billion, or $1.63 per share, from $4.6 billion, or $2.15 a share, in the year-ago quarter.

Excluding divestiture-related impacts, earnings were $1.50 a share.

Total revenue increased to $18.5 billion from $17.4 billion.

Analysts were looking for earnings of $1.42 a share and revenue of $18.26 billion for Citigroup, according to a FactSet survey.

Citi said it continues to shrink its operations in Russia, and expects to end nearly all of the institutional banking services offered in the country next quarter. “To be clear, our intention is to wind down our presence in this country,” Chief Executive Jane Fraser said.

Shares of Citigroup have dropped 28.9% in 2022.

[ad_2]

[ad_1]

TOKYO (AP) — Asian shares were mostly lower on Wednesday following another volatile day on Wall Street, as traders braced for updates on inflation and corporate earnings.

Benchmarks fell in Tokyo

NIY00,

Shanghai

SHCOMP,

and Hong Kong

HSI00,

but rose in Sydney.

South Korea’s Kospi

180721,

lost 0.1% to 2,189.86 after the Bank of Korea raised its key rate by 0.5 percentage point, amid the backdrop of Fed rate hikes in the U.S. and growing inflation risks from the weak won and rebounding global oil prices.

In currency trading the Japanese yen declined to a 24-year low against the U.S. dollar

JPYUSD,

at 146 yen-levels, raising expectations of another intervention by Tokyo to prop up the yen. By midday the dollar

USDJPY,

was at 146.17 yen, up from 145.80 late Tuesday. The euro

EURUSD,

cost 96.96 cents, inching down from 97.07 yen.

The weaker yen raises costs for both consumers and businesses who rely on imports of food, fuel and other needs, but the bigger purchasing power for foreign currencies is expected to boost tourism. Japan reopened fully to individual tourist travel this week after being closed for more than two years because of the pandemic.

Japan’s benchmark Nikkei 225 lost 0.2% to 26,348.73 in morning trading. Australia’s S&P/ASX 200

ASX10000,

gained nearly 0.2% to 6,656.00. Hong Kong’s Hang Seng slipped 2% to 16,491.39, while the Shanghai Composite shed 1.2% to 2,943.24.

On Tuesday, the S&P 500

SPX,

fell 0.7%, marking its fifth straight loss, closing at 3,588.84. The Nasdaq

COMP,

dropped 1.1% to 10,426.19. The Dow Jones Industrial Average

DJIA,

added 0.1% to 29,239.19, while the Russell 2000 index

RUT,

rose 1 point, or about 0.1%, to 1,692.92.

Recession fears have been weighing heavily on markets as stubbornly hot inflation burns businesses and consumers. Economic growth has been slowing as consumers temper spending and the Federal Reserve and other central banks raise interest rates.

The International Monetary Fund on Tuesday cut its forecast for global economic growth in 2023 to 2.7%, down from the 2.9% it had estimated in July. The cut comes as Europe faces a particularly high risk of a recession with energy costs soaring amid Russia’s invasion of Ukraine.

Wall Street is closely watching the Federal Reserve as it continues to aggressively raise its benchmark interest rate to make borrowing more expensive and slow economic growth. The goal is to cool inflation, but the strategy carries the risk of slowing the economy too much and pushing it into a recession.

“The market desperately wants a reason for the Fed to be able to stop tightening and the data recently hasn’t given them that opening with respect to inflation,” said Willie Delwiche, investment strategist at All Star Charts.

Computer-chip manufacturers continued slipping in the wake of the U.S. government’s decision to tighten export controls on semiconductors and chip manufacturing equipment to China. Qualcomm

QCOM,

fell 4%.

Uber

UBER,

fell 10.4% and Lyft

LYFT,

slumped 12% following a proposal by the U.S. government that could give contract workers at ride-hailing and other gig economy companies full status as employees.

The Fed will release minutes from its last meeting on Wednesday, possibly giving Wall Street more insight into its views on inflation and next steps.

Investors still expect the Fed to raise its overnight rate by three-quarters of a percentage point next month, the fourth such increase. That’s triple the usual amount, and would bring the rate up to a range of 3.75% to 4%. It started the year at virtually zero.

Rex Nutting: Leading indicators show inflation is slowing, but Fed policy makers are too busy looking in rearview mirror to notice

The government will also release its report on wholesale prices Wednesday, providing an update on how inflation is hitting businesses. The closely watched report on consumer prices will be released on Thursday, and a report on retail sales is due Friday.

“Everyone is still hoping that every inflation report will be the one that shows that pressure is alleviating,” Delwiche said.

Wall Street is also gearing up for the start of the latest corporate earnings reporting season, which could provide a clearer picture of inflation’s impact.

Among the companies reporting quarterly results this week: PepsiCo

PEP,

Delta Air Lines

DAL,

and Domino’s Pizza

DPZ,

Banks including Citigroup

C,

and JPMorgan Chase

JPM,

will also report results.

In energy trading, benchmark U.S. crude

CL00,

lost 82 cents to $88.53 a barrel in electronic trading on the New York Mercantile Exchange. U.S. crude-oil prices fell 2% Tuesday. Brent crude

BRN00,

the international pricing standard, fell 62 cents to $93.67 a barrel.

[ad_2]

[ad_1]

John Foley, the co-founder and former chief executive of Peloton Interactive faced repeated margin calls on money he borrowed against his Peloton holdings before he left the fitness company’s board last month, according to people familiar with the situation.

As Peloton’s shares slumped over the past year, Goldman Sachs Group asked Mr. Foley several times to provide fresh funds or additional collateral for personal loans the bank had extended to him, the people said. The company’s share price has fallen nearly 95% from its $160 peak in December 2020.

[ad_2]

[ad_1]

With four weeks until Election Day, congressional candidates are on track to break midterm fundraising records, having raised nearly $2.5 billion so far this cycle. That’s already 70% more than what was raised during the 2014 cycle and just $200 million shy of the total raised during the full 2018 cycle.

This cycle has also seen record-shattering outside spending, topping $1 billion through the beginning of October, according to an OpenSecrets estimate.

The increase in spending and fundraising is due in large part to the involvement of millionaire and billionaire megadonors who have sought to influence the outcome of an election in which both chambers of Congress are in play.

“When megadonors pump millions of dollars into super PACs, they get to help call the shots,” said Michael Beckel, research director at Issue One, a nonpartisan political reform organization. “Massive spending from a megadonor can influence what issues are talked about on the campaign trail and in Congress.”

Super PACs are independent political action committees that can raise unlimited sums of money but are not allowed to coordinate with a candidate or campaign. Due to contribution limits, such as those restricting individuals’ candidate contributions to $2,900 per election per candidate, most megadonor spending goes to super PACs.

More context: These are the basics of campaign finance in 2020 — in two handy charts

A MarketWatch analysis of Federal Election Commission data through the end of September shows that these 10 business moguls and philanthropists are the biggest federal-level donors this cycle.

Read: These 3 races could determine whether Democrats or Republicans control the Senate in 2023

And see: If this seat flips red, Republicans will have ‘probably won a relatively comfortable House majority’

| Rank | Contributor | Total Contributions | For Republicans | For Democrats | Nonpartisan/Bipartisan |

| 1 | George Soros | $128,782,000 | $0 | $128,782,000 | $0 |

| 2 | Ken Griffin | $50,955,800 | $50,955,800 | $0 | $0 |

| 3 | Richard Uihlein | $49,117,000 | $49,117,000 | $0 | $0 |

| 4 | Sam Bankman-Fried | $39,931,000 | $201,000 | $37,725,000 | $2,005,000 |

| 5 | Jeff Yass | $32,754,000 | $32,754,000 | $0 | $0 |

| 6 | Peter Thiel | $30,189,000 | $30,189,000 | $0 | $0 |

| 7 | Fred Eychaner | $22,343,000 | $0 | $22,343,000 | $0 |

| 8 | Stephen Schwarzman | $21,870,000 | $21,865,000 | $0 | $5,000 |

| 9 | Larry Ellison | $21,003,000 | $21,003,000 | $0 | $0 |

| 10 | Ryan Salame | $18,932,000 | $17,432,000 | $0 | $1,500,000 |

| Totals: | $415,877,000 | $223,517,000 | $188,850,000 | $3,510,000 |

Source: MarketWatch analysis of FEC data as of Sept. 30, 2022

Note: Partisan breakdown includes non-party affiliated PACs with over 95% of their spending benefitting one party, data has been rounded to the nearest thousand

Big spending by itself doesn’t automatically mean winning. There have been notable instances of the financially strongest candidates losing (such as crypto-backed House candidate Carrick Flynn earlier this year and billionaire Michael Bloomberg’s self-financed presidential bid) — but money can certainly help put a candidate on the right track.

“Money alone doesn’t guarantee electoral success, but every candidate prefers to be the one with more money to spend,” Beckel said. He added: “Outside spending on behalf of a candidate isn’t a silver bullet that’s going to guarantee electoral success. But it goes a long way to boosting somebody’s name recognition, and to presenting them as a viable candidate — somebody who has the resources to run a competitive campaign.”

Information about the spending by the top 10 donors this cycle has been compiled from MarketWatch’s analysis of FEC data and filings, super PAC websites and previously reported comments. Read on to find out who are the top 10 biggest donors this cycle.

Ryan Salame, the co-CEO of FTX Digital Markets, a subsidiary of cryptocurrency exchange FTX, founded a hybrid PAC earlier this year called American Dream Federal Action. The vast majority ($15 million) of the $19 million Salame has spent this cycle has gone into bankrolling the PAC, which has spent $2.4 million in independent expenditures supporting Illinois Republican Rep. Rodney Davis, $2 million supporting Republican Senate candidate Katie Britt from Alabama, and $1.2 million each supporting Arkansas GOP Sen. John Boozman and Brad Finstad, a GOP congressional candidate in Minnesota.

On its website, the PAC describes itself as “organization dedicated to electing forward-looking candidates — those who want to protect America’s long term economic and national security by advancing smart policy decisions now.” A representative for Salame didn’t respond to a request for comment.

The co-founder of Oracle

ORCL,

has similarly bankrolled a PAC this election cycle — giving a total $20 million to Opportunity Matters Fund Inc. The super PAC has largely held onto its funds so far, recent FEC records show, having $17 million cash on hand as of the end of August. Of the independent expenditures it has made this cycle, it spent the most on Georgia Republican Senate candidate Herschel Walker ($1.3 million), Wisconsin Republican Sen. Ron Johnson ($1.3 million) and North Carolina Senate candidate and current Republican Rep. Ted Budd ($1.1 million). A representative for Ellison didn’t respond to a request for comment.

Billionaire Stephen Schwarzman, the CEO of private-equity giant Blackstone

BX,

is the eighth biggest donor at the federal level this cycle. In March, Schwarzman gave $10 million to both the Senate Leadership Fund and Congressional Leadership Fund, super PACs aimed at obtaining a Republican majority in the Senate and House, respectively. A representative for Schwarzman didn’t respond to a request for comment.

Fred Eychaner has also contributed $22 million so far this cycle, but unlike most of the spending on this list, his has been directed toward Democratic causes. The chairman of Chicago-based Newsweb Corporation has given $9 million to the House Majority PAC and $8 million to the Senate Majority PAC, as well as just under $1.5 million to the Democratic National Committee and several hundred thousands to the Democratic Congressional Campaign Committee and Democratic Senatorial Campaign Committee. A representative for Eychaner didn’t respond to a request for comment.

Venture capitalist Peter Thiel was heavily involved in backing Ohio Republican J.D. Vance’s primary bid, giving $15 million in the spring to the Vance-aligned Protect Ohio Values PAC.

The massive primary investment was “historic” and record-setting, according to Beckel, who added that Thiel’s involvement in the Ohio Senate primary could mark “a new chapter of how mega donors are choosing to play in politics.”

“I think it’s become clear for a lot of megadonors that there are high stakes to a lot of primaries, and by spending in the primary, where there is typically lower turnout than in say, a statewide general election, they can get a lot of bang for their buck by investing in a primary election,” Beckel added.

Thiel has indicated that he doesn’t intend to put any more money toward Vance’s bid as he reportedly believes the Ohio candidate is on track to win, and instead will focus his funding on Arizona Republican Blake Masters’ bid to oust Democratic Sen. Mark Kelly in the final weeks leading up to the midterm election.

Thiel, known for his roles in PayPal

PYPL,

Palantir

PLTR,

and Facebook

META,

has also given a total $15 million to the Masters-aligned PAC, Saving Arizona, with his most recent contribution in July. Both Vance and Masters are venture capitalists, but Masters has worked with Thiel. He served as chief operating officer of Thiel Capital and president of the Thiel Foundation, and he co-authored a book on startups with Thiel in 2014. A representative for Thiel didn’t respond to a request for comment.

Options trader Jeff Yass, who founded trading firm Susquehanna International Group, has contributed about $33 million on a federal level this cycle. Yass has given $15 million to the School Freedom Fund, or the equivalent of 97% of the PAC’s total fundraising. The group focuses on the issue of school choice, and its website states that some bureaucrats “hindered the development and education of our youth through school closures, mask mandates, critical race theory, and more.”

Aside from the School Freedom Fund, Yass’ other biggest contributions are to the conservative Club for Action ($6.5 million), Kentucky Freedom ($5 million), Protect Freedom ($2 million) and Crypto Freedom ($1.9 million). A representative for Yass didn’t respond to a request for comment.

Sam Bankman-Fried, the founder and CEO of FTX, is the main funder behind Protect Our Future PAC, giving it $27 million of the $28 million it raised this cycle.

The organization says on its website that it focuses on promoting Democratic candidates championing pandemic preparedness and prevention “so this is the last time in our lifetime, and our children’s lifetimes, that we will face the devastation that has gripped communities across the U.S. since 2020.”

The group spent more than $10 million supporting Democrat Carrick Flynn’s House bid in Oregon. Flynn lost his primary in May by 18 points despite his massive outside spending advantage. In addition to Flynn, the group has made over $1 million in independent expenditures each supporting Democratic congressional candidates Lucy McBath, a current representative from Georgia; Jasmine Crockett of Texas, Adam Hollier of Michigan, Valerie Foushee of North Carolina and Shontel Brown, a current representative from Ohio.

Most of the other $10 million Bankman-Fried spent this cycle has gone to the House Majority PAC ($6 million) and the crypto PAC GMI ($2 million).

While the vast majority of his spending has supported Democratic candidates and causes, Bankman-Fried does not classify himself as an exclusively Democratic donor — for instance he gave $105,000 to the Alabama Conservatives Fund in June and $45,000 to the NRCC in July.

He told Politico in August that he is “legitimately worried about doing things that will make people view me as partisan when it’s not how I feel … because I think it both misses what I’m trying to do and makes it harder for me to act constructively.” A representative for the FTX boss didn’t respond to a request for comment.

Richard Uihlein is the founder of the shipping and business supply company Uline, and is a longtime conservative donor. This cycle has seen nearly $50 million in political spending by him, with just over half of it going to Club for Growth Action. Uihlein has also given about $14 million to Restoration PAC, an organization that says it is “dedicated to strengthening the foundations that made America the greatest nation in the world: God, family, education, and community.”

Uihlein’s next largest contributions are to the conservative Team PAC ($2.5 million) and the Arkansas Patriots Fund ($2.2 million), which earlier this year made ad buys favoring Republican Sen. John Boozman’s primary opponent. A representative for Uihlein didn’t respond to a request for comment.

With $51 million in federal-level political spending, Ken Griffin, CEO of hedge fund Citadel, is the second most prolific donor this cycle.

The biggest beneficiaries are the Republican-aligned Congressional Leadership Fund with $18.5 million in contributions, the Senate Leadership Fund with $10 million and Honor Pennsylvania, a super PAC that backed Republican Dave McCormick’s Senate bid. McCormick lost in the primary to Mehmet Oz by less than a thousand votes.

While Griffin spent about $64 million during the last cycle, his $51 million figure this year marks by far the most he has spent during a midterm cycle. During the 2018 cycle, his contributions totaled less than $8 million.

A spokesperson for Griffin told MarketWatch that Griffin “supports leaders who are committed to protecting the American Dream and pursuing policies that will create a better future for the United States.”

“The right policies will focus on creating rewarding jobs, prioritizing public safety, and investing in a strong national defense,” his spokesperson said. “Preserving the American Dream will require that every child is well educated, can access great healthcare, and has the opportunity to succeed.”

Not one donor comes close to matching the sum that billionaire philanthropist George Soros has contributed this cycle: $129 million. However, much of that money hasn’t actually been put to work this cycle.

The majority of those on this list have focused their funding on Republican causes, but Soros’ money has gone to Democratic groups — specifically Democracy PAC II, whose $125 million in contributions comprises 99% of its fundraising. The super PAC spent more than $80 million on Democratic groups and candidates during the 2020 election.

A representative for Soros pointed MarketWatch to a Politico article from January, in which Soros said the $125 million is aimed at supporting pro-democracy “causes and candidates, regardless of political party” who are invested in “strengthening the infrastructure of American democracy: voting rights and civic participation, civil rights and liberties, and the rule of law” and called his contribution a “long-term investment” that will support political work beyond this year.

So far this cycle, Democracy PAC has spent very little and holds $113 million in available cash. Contributions the PAC has made this cycle include $5 million to the Senate Majority PAC, $2.5 million to One Georgia and $1 million to both Care in Action and House Majority PAC.

[ad_2]

[ad_1]

Don’t assume the worst is over, says investor Larry McDonald.

There’s talk of a policy pivot by the Federal Reserve as interest rates rise quickly and stocks keep falling. Both may continue.

McDonald, founder of The Bear Traps Report and author of “A Colossal Failure of Common Sense,” which described the 2008 failure of Lehman Brothers, expects more turmoil in the bond market, in part, because “there is $50 trillion more in world debt today than there was in 2018.” And that will hurt equities.

The bond market dwarfs the stock market — both have fallen this year, although the rise in interest rates has been worse for bond investors because of the inverse relationship between rates (yields) and bond prices.

About 600 institutional investors from 23 countries participate in chats on the Bear Traps site. During an interview, McDonald said the consensus among these money managers is “things are breaking,” and that the Federal Reserve will have to make a policy change fairly soon.

Pointing to the bond-market turmoil in the U.K., McDonald said government bonds that mature in 2061 were trading at 97 cents to the dollar in December, 58 cents in August and as low as 24 cents over recent weeks.

When asked if institutional investors could simply hold on to those bonds to avoid booking losses, he said that because of margin calls on derivative contracts, some institutional investors were forced to sell and take massive losses.

Read: British bond market turmoil is sign of sickness growing in markets

And investors haven’t yet seen the financial statements reflecting those losses — they happened too recently. Write-downs of bond valuations and the booking of losses on some of those will hurt bottom-line results for banks and other institutional money managers.

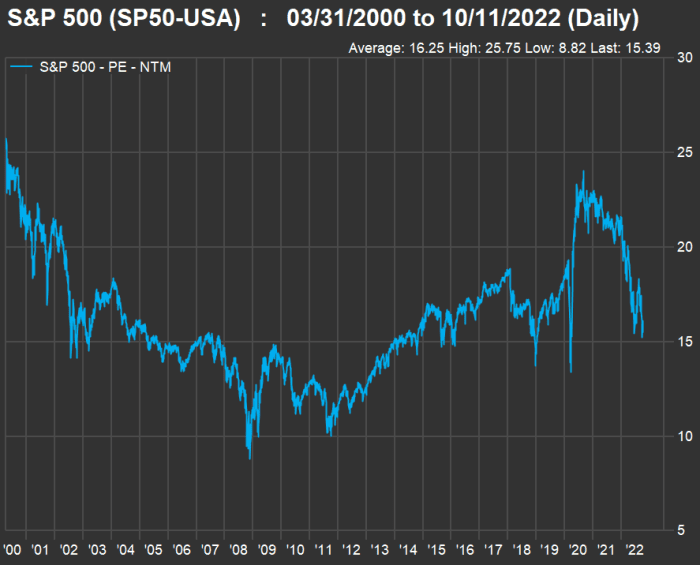

Now, in case you think interest rates have already gone through the roof, check out this chart, showing yields for 10-year U.S. Treasury notes

TMUBMUSD10Y,

over the past 30 years:

FactSet

The 10-year yield is right in line with its 30-year average. Now look at the movement of forward price-to-earnings ratios for S&P 500

SPX,

since March 31, 2000, which is as far back as FactSet can go for this metric:

The index’s weighted forward price-to-earnings (P/E) ratio of 15.4 is way down from its level two years ago. However, it is not very low when compared to the average of 16.3 since March 2000 or to the 2008 crisis-bottom valuation of 8.8.

McDonald said that interest rates didn’t need to get anywhere near as high as they were in 1994 or 1995 — as you can see in the first chart — to cause havoc, because “today there is a lot of low-coupon paper in the world.”

“So when yields go up, there is a lot more destruction” than in previous central-bank tightening cycles, he said.

It may seem the worst of the damage has been done, but bond yields can still move higher.

Heading into the next Consumer Price Index report on Oct. 13, strategists at Goldman Sachs warned clients not to expect a change in Federal Reserve policy, which has included three consecutive 0.75% increases in the federal funds rate to its current target range of 3.00% to 3.25%.

The Federal Open Market Committee has also been pushing long-term interest rates higher through reductions in its portfolio of U.S. Treasury securities. After reducing these holdings by $30 billion a month in June, July and August, the Federal Reserve began reducing them by $60 billion a month in September. And after reducing its holdings of federal agency debt and agency mortgage-backed securities at a pace of $17.5 billion a month for three months, the Fed began reducing these holdings by $35 billion a month in September.

Bond-market analysts at BCA Research led by Ryan Swift wrote in a client note on Oct. 11 that they continued to expect the Fed not to pause its tightening cycle until the first or second quarter of 2023. They also expect the default rate on high-yield (or junk) bonds to increase to 5% from the current rate of 1.5%. The next FOMC meeting will be held Nov. 1-2, with a policy announcement on Nov. 2.

McDonald said that if the Federal Reserve raises the federal funds rate by another 100 basis points and continues its balance-sheet reductions at current levels, “they will crash the market.”

McDonald expects the Federal Reserve to become concerned enough about the market’s reaction to its monetary tightening to “back away over the next three weeks,” announce a smaller federal funds rate increase of 0.50% in November “and then stop.”

He also said that there will be less pressure on the Fed following the U.S. midterm elections on Nov. 8.

Don’t miss: Dividend yields on preferred stocks have soared. This is how to pick the best ones for your portfolio.

[ad_2]

[ad_1]

The Bank of England said Tuesday that it will expand its daily U.K. bond purchase operations to include index-linked gilts, the second move this week aimed at trying to calm market volatility.

“These additional operations will act as a further backstop to restore orderly market conditions by temporarily absorbing selling of index-linked gilts in excess of market intermediation capacity,” the BoE said in a statement on Tuesday, adding that it has also consulted with the Debt Management Office.

The inclusion of those index-linked bonds will run from Oct. 11 to 14, alongside its existing daily conventional gilt purchase auctions, the BoE said.

But it remained to be seen if a second-day move by the central bank to calm markets will be effective.

Investors are anxiously looking ahead to Friday, when the central bank’s emergency bond-buying program announced last month are scheduled to end. The BoE announced additional measures on Monday to smooth that path, but the yield on the 30-year gilt

TMBMKGB-30Y,

jumped 29 basis points to 4.68% on Monday.

While that’s still below the 5.17% peak, it indicates concerns about the imminent end to the central bank’s program were causing fear in the market. The yield on the 10-year gilt

TMBMKGB-10Y,

which the central bank has not been buying, rose 24 basis points to 4.47%

On Monday, the BoE said it would boost the size of its daily gilt purchases and implement extra measures “to support an orderly end” to its emergency bond-buying plans.

It now will buy up to £10 billion ($11 billion) in bonds, up from a previous auction limit of £5 billion ($5.5 billion), though sticking with its pricing policy that has seen the central bank refuse many of the bonds put up for auction.

The BoE also said Monday that it plans to to launch a temporary expanded collateral repo operation for liability-driven investment funds through liquidity insurance operations, which will run beyond the end of this week.

LDI funds are a popular product sold by asset managers like BlackRock

BLK,

Legal & General

LGEN,

and Schroders

SDR,

to pension funds, using derivatives to help them match assets and liabilities so there is no risk of shortfall in money to pay pensioners.

But those measures failed to stop bond yields from surging, amid market fears that the pension fund market is not yet ready for that temporary debt purchase program to end.

[ad_2]

[ad_1]

U.S. stocks finished with losses on Monday, sending the Nasdaq Composite to its lowest close in more than two years, after investors failed to shake off worries about further Federal Reserve rate hikes and JPMorgan Chase & Co.’s Jamie Dimon warned of a potential 20% decline in the S&P 500.

Monday’s declines exacerbated losses which occurred at the end of last week. On Friday, the Dow fell 630 points, or 2.1%, the S&P 500 declined 2.8%, and the Nasdaq Composite dropped 3.8%. The Nasdaq Composite was down 31.9% for the year to date through Friday.

Major indexes finished lower for a fourth consecutive session on Monday as concerns about additional rate hikes by the Fed continued to damp sentiment. Dow industrials, the S&P 500 and the Nasdaq all fell to session lows after a CNBC interview with Dimon, chief executive of JPMorgan

JPM,

who said the S&P 500 could fall by “another easy 20%” from current levels.

Read: Here are the 5 times traders and stock-market investors got fooled by Fed ‘pivot’ hopes in past year

Soft data a week ago had raised hopes that the Fed would soon pause its monetary tightening cycle in its battle to suppress multidecade high inflation, and the market subsequently rebounded off its near two-year lows. But a strong jobs report on Friday crushed that Fed “pivot” narrative and stocks plunged again.

On Monday, the CBOE Vix index

VIX,

a gauge of expected S&P 500 volatility, sat at 32.15, well above its long-term average of 20.

“The low interest-rate environment forced investors to chase yield and bid up the asset prices too high. Eventually the market is fair and asset values have to achieve some sense of common ground or base level valuation. So it was inevitable that this valuation correction would happen,” said Siddharth Singhai, chief investment officer for New York-based hedge fund IronHold Capital.

“Panic will swing the market towards excessive pessimism and then the valuations will be too cheap. That hasn’t happened yet. Upcoming rate hikes will most likely be a catalyst for panic, however,” he wrote in an email to MarketWatch on Monday.

Coming into Monday’s session, trading had been expected to be somewhat thinned by the Columbus Day and Indigenous People’s Day holiday, which closed the Treasury market.

Now, traders are looking toward more data later in the week for further guidance on Fed thinking and equity valuations. The U.S. producer price numbers will be released on Wednesday and the consumer prices report on Thursday, the last of their kind before the Fed’s policy decision on Nov. 2.

Then on Friday, third-quarter corporate earnings season really kicks into gear when big banks like JPMorgan

JPM,

and Citigroup

C,

present their numbers.

Read: JPMorgan, Citi, Morgan Stanley and Wells Fargo kick off bank earnings season in choppy waters and S&P 500 would be in an ‘earnings recession’ if not for this one booming sector — but that may not last long

Investors were also keeping an eye on the strong U.S. dollar, which is considered a drag on the earnings of U.S. multinationals. The dollar index

DXY,

rose 0.3% to 113.12 as the euro intermittently broke below $0.97 after Russia sent missiles into cities across Ukraine.

See: A rampaging U.S. dollar is wreaking havoc in financial markets. Here’s why it’s so hard to stop it.

“We expect a lot more volatility in markets for the remainder of the year as the inevitability of higher rates sinks in and the economic consequences become more pronounced,” said Arthur Laffer Jr., president of Nashville-based Laffer Tengler Investments. Fed Chairman Jerome Powell “will not be a very popular person but it seems his legacy is focused on fighting any resurgence of 1970s inflation in the U.S. at all costs.”

–— Jamie Chisholm contributed to this article.

[ad_2]

[ad_1]

It’s a regular day of business for the U.S. stock market on Monday, October 10, as equity exchanges stay open for Columbus Day, a federal holiday that also has been recognized as Indigenous Peoples’ Day.

Bond markets, however, take the day off, which means a long weekend for the Treasury market, corporate bonds and other forms of tradable debt, starting after the close of business on Friday.

Stocks have endured a brutal selloff in the first nine months of the year as the Federal Reserve has worked to fight inflation that’s been stuck near it highest levels since the early 1980s.

The central bank’s main tool to battle inflation has been to dramatically increase interest rates, while also shrinking its balance sheet, in an effort to tighten financial conditions and squelch demand for goods and services, while also bringing down stubbornly high costs of living, including food, shelter and energy prices.

The Fed’s focus in recent months also has been on cooling the roaring labor market, with strong wage gains in the past year viewed as one of several culprits behind elevated inflation.

Friday’s jobs report for September pegged the unemployment rate as matching a prepandemic low of 3.5%, dashing hopes for now of a significant trend toward a pullback in the labor market.

The S&P 500 index

SPX,

tumbled 2.8% on Friday, the Dow Jones Industrial Average

DJIA,

fell 630.15 points, or 2.1%, and the Nasdaq Composite Index

COMP,

dropped 3.8%. An early October rally had offered some hope for a bounce for stocks, after a brutal first nine months for investors.

Bonds also have undergone a painful repricing this year as volatility tied to the Fed’s monetary tightening campaign has eroded the value of bonds issued in the past decade of low rates.

Read: Bond markets facing historic losses grow anxious about Fed that ‘isn’t blinking yet’

The S&P 500 is down about 24% for the year, while the Dow is off 19% and the Nasdaq nearly 32%.The 10-year Treasury rate

TMUBMUSD10Y,

was near 3.9% Friday, after recently touching 4%, it’s highest since 2010

[ad_2]

[ad_1]

U.S. stocks finished sharply lower Friday, but still booked their best weekly gains in a month, after September jobs data showed an unexpected fall in the unemployment rate that’s anticipated to reinforce the Federal Reserve’s resolve to keep tightening monetary policy.

Investors also weighed a profit warning at a leading microchip maker ahead of next week’s increase in quarterly earnings results.

Stocks posted back-to-back losses, trimming weekly gains, but recorded their best weekly gains since Sept. 9, according to Dow Jones Market Data.

Read: Will the stock market be open on Columbus Day?

Stocks recorded sharp losses Friday after the Labor Department said the U.S. economy added 263,000 jobs in September, while the unemployment rate declined to 3.5% from an August reading of 3.7%. Average hourly earnings rose 0.3%.

Still, a powerful rally earlier in the week boosted all three major stock indexes to weekly gains, a departure from three straight weekly losses, according to Dow Jones Market Data.

“It’s manic. We are all on edge,” said Kent Engelke, chief economic strategist at Capitol Securities Management, of the sharp market swings.

“Any piece of good news is a cause for an explosive rally,” Engelke said by phone. On the flip side, he pegged technology-based trading “in an illiquid and emotional market” as exacerbating Friday’s selloff.

“It’s a reflection that people have re-entered the mind-set that the Fed is going to be raising rates at a rapid clip, probably for longer than what they might have suspected at the start of the week,” said Robert Pavlik, a senior portfolio manager at Dakota Wealth Management, by phone.

Pavlik expects the Fed to keep tightening financial conditions to try to head off inflation. “But once we turn the corner, and the economy slows down, the Fed probably will be more aggressive in cutting rates on the way down.”

In addition, the Fed has been “draining liquidity from the system at a remarkable pace,” wrote Rick Rieder, BlackRock’s chief investment officer of global fixed income, in a Friday client note, while pointing to an astounding $1.3 trillion decline in the central bank’s balance sheet since the December 2021 peak.

Pavlik at Dakota Wealth said he anticipates the Fed will start slowing interest rate hikes by mid-next year, which likely means continued pressure for the stock market, particularly with a backdrop of big oil-price

CL00,

gains this week after global crude producers voted to cut monthly production and with the U.S. dollar’s

DXY,

surge this year against a basket of rival currencies.

U.S. crude oil prices climbed for a fifth day in a row on Friday to settle at $92.64 a barrel, while booking at 16.5% weekly gain.

New York Fed President John Williams said Friday that benchmark interest rates likely need to hit 4.5% over time. The Fed’s policy rate now sits in a 3%-3.25% range, up from a zero-0.25% range a year ago.

The benchmark 10-year Treasury rate

TMUBMUSD10Y,

climbed to 3.883% Friday, as the key metric used to gauge the affordability of credit for businesses, household and the economy posted 10 straight weeks of gains, according to Dow Jones Market Data.

Read: Bond markets facing historic losses grow anxious of Fed that ‘isn’t blinking yet’

Investors continued to hope for relief on the inflation front and will be monitoring next week’s release of the September consumer-price index, as well as corporate earnings season as it picks up.

—Steven Goldstein contributed reporting to this article

[ad_2]

[ad_1]

It’s a regular day of business for the U.S. stock market on Monday, October 10, as equity exchanges stay open for Columbus Day, a federal holiday that also has been recognized as Indigenous Peoples’ Day.

Bond markets, however, take the day off, which means a long weekend for the Treasury market, corporate bonds and other forms of tradable debt, starting after the close of business on Friday.

Stocks have endured a brutal selloff in the first nine months of the year as the Federal Reserve has worked to fight inflation that’s been stuck near it highest levels since the early 1980s.

The central bank’s main tool to battle inflation has been to dramatically increase interest rates, while also shrinking its balance sheet, in an effort to tighten financial conditions and squelch demand for goods and services, while also bringing down stubbornly high costs of living, including food, shelter and energy prices.

The Fed’s focus in recent months also has been on cooling the roaring labor market, with strong wage gains in the past year viewed as one of several culprits behind elevated inflation.

Friday’s jobs report for September pegged the unemployment rate as matching a prepandemic low of 3.5%, dashing hopes for now of a significant trend toward a pullback in the labor market.

The S&P 500 index

SPX,

tumbled 1.9% on Friday, the Dow Jones Industrial Average

DJIA,

was down 1.5% and the Nasdaq Composite Index

COMP,

was off 2.6%. And early October rally had offered some hope for a bounce for stocks, after a brutal first nine months for investors.

Bonds also have undergone a painful repricing this year as volatility tied to the Fed’s monetary tightening campaign has eroded the value of bonds issued in the past decade of low rates.

The S&P 500 is down about 23% for the year, the Dow off 19% and the Nasdaq off 31% since January. The 10-year Treasury rate

TMUBMUSD10Y,

was near 3.9% Friday, after recently touching 4%, it’s highest since 2010

[ad_2]

[ad_1]

Credit Suisse Group AG said Friday that it is offering to repurchase debt securities for a total of close to $3 billion as the troubled lender looks to manage its liabilities ahead of a touted restructuring.

The Swiss bank

CS,

CSGN,

is offering to buy back eight euro- or pound sterling-denominated senior debt securities for a total of up to 1 billion euros ($979.2 million,) it said.

It is also offering to buy back 12 U.S. dollar-denominated securities for up to $2 billion. Both offers are subject to various conditions and will expire on Nov. 3 and Nov. 10, respectively, Credit Suisse said.

The value of some Credit Suisse bonds fell at the beginning of this week alongside shares in the lender amid speculation over its financial health. The bank has moved to reassure investors ahead of a planned strategy update due on Oct. 27 alongside quarterly results.

Write to Joshua Kirby at joshua.kirby@wsj.com; @joshualeokirby

[ad_2]

[ad_1]

A strong fall COVID booster campaign could save about 90,000 people living in the U.S. from dying of the virus and avoid more than 936,000 hospitalizations, according to a new study by the Commonwealth Fund.

As immunity wanes and new variants that can evade protection from early vaccines emerge, surges in hospitalizations and deaths are increasingly likely this fall and winter, the authors wrote. That makes it important that people get the bivalent boosters recently authorized by the Food and Drug Administration and help stop transmission, they wrote.

Researchers analyzed three scenarios to evaluate the impact of vaccination on reducing fatalities, hospitalizations and medical costs to both the Medicare and Medicaid programs.

The first measured the outcome if daily vaccination rates remain unchanged from current levels; they have gradually declined since the first wave of the omicron variant. Federal financial support has also not been replenished, amid a perception among many Americans that the pandemic is over and as congressional Republicans oppose legislative efforts to continue the pandemic fight.

As of Oct. 3, some 68% of the U.S. population has had primary shots, but fewer than half of those have received a booster dose, and only 36% of those aged 50 and older have had a second booster.

The second and third Commonwealth Fund scenarios looked at outcomes if rates increased by the end of 2022.

In one scenario, researchers imagined booster uptake would track flu-shot coverage in 2020 to 2021. The other scenario assumed 80% of eligible individuals 5 and older get a booster by the end of 2022.

The data found that more than 75,000 deaths could be prevented along with more than 745,000 hospitalizations if coverage reaches similar levels to 2021 to 2022 flu vaccination. The best scenario would save $56 billion in direct medical costs over the course of the next six months.

“Stratifying by insurance type, we found direct medical costs would be reduced by $11 billion for Medicare alone under scenario 1 and $13 billion under scenario 2,” the authors wrote. “An additional $3.5 to $4.5 billion in savings would accrue to Medicaid. Even if the federal government paid all vaccination costs, accelerated campaigns would generate more than $10 billion in net savings from federal programs like Medicare and Medicaid.”

The study comes as U.S. known cases of COVID are continuing to ease and now stand at their lowest level since late April, although the true tally is likely higher given how many people are testing at home, with data not being collected.

The daily average for new cases stood at 44,484 on Tuesday, according to a New York Times tracker, down 22% from two weeks ago. Cases are rising in most northeastern states by 10% of more, while cases in the are rising in the western states Montana, Washington and Oregon.

The daily average for hospitalizations was down 12% at 27,334, while the daily average for deaths is down 8% to 393.

Coronavirus Update: MarketWatch’s daily roundup has been curating and reporting all the latest developments every weekday since the coronavirus pandemic began

Other COVID-19 news you should know about:

• Long COVID, a condition that can encompass symptoms such as respiratory distress, cough, “brain fog,” fatigue and malaise that last 12 weeks or longer after initial infection, is becoming a long-term challenge as both employers and workers navigate an ever-mutating virus, according to Liz Seegert, writing for NextAvenue.org. The Centers for Disease Control and Prevention found that one in five COVID survivors younger than 65 experienced at least one incident that might be related to previous COVID-19 infection. Among those 65 and older, the rate was one in four. Their data also show that nearly three times as many people age 50 to 59 currently have long COVID than those 80 or older.

• A retired judge opened a public inquiry on Tuesday into how Britain handled the coronavirus pandemic, saying bereaved families and those who suffered would be at the heart of the proceedings, the Associated Press reported. Former Court of Appeal judge Heather Hallett said the inquiry would investigate the U.K.’s preparedness for a pandemic, how the government responded, and whether the “level of loss was inevitable or whether things could have been done better.”

• Health experts are keeping an eye on new versions of the BA.5 omicron subvariant amid concerns those virus versions can evade the drugs developed to fight COVID, Salon reported. Of particular concern are two named BQ.1 and BQ.1.1, along with BA.2.75.2, which is spreading in Singapore, India and parts of Europe. Then there’s XBB, which some research suggest is the most antibody-evasive strain tested so far. The World Health Organization said in its weekly update on the virus that BA.5 descendent lineages continued to be dominant in the latest week, accounting for 80.8% of sequences shared through a global database. It also noted “increased diversity” within omicron and its lineages.

• Eiger BioPharmaecuticals Inc.

EIGR,

said Wednesday it will not pursue emergency authorization of its experimental treatment for mild and moderate COVID-19 infections. It had asked the Food and Drug Administration to consider an EUA application based on data from the Together trial, a Phase 3 study that has assessed 11 possible treatments for COVID-19 that is being conducted in Brazil and Canada. Eiger said the FDA instead recommended the company consider running its own pivotal trial for peginterferon lambda that would support full approval of the drug.

Here’s what the numbers say:

The global tally of confirmed cases of COVID-19 topped 619.2 million on Wednesday, while the death toll rose above 6.55 million, according to data aggregated by Johns Hopkins University.

The U.S. leads the world with 96.5 million cases and 1,060,446 fatalities.

The Centers for Disease Control and Prevention’s tracker shows that 225.3 million people living in the U.S., equal to 67.9% of the total population, are fully vaccinated, meaning they have had their primary shots. Just 109.9 million have had a booster, equal to 48.8% of the vaccinated population, and 23.9 million of those who are eligible for a second booster have had one, equal to 36.6% of those who received a first booster.

Some 7.6 million people have had a shot of the new bivalent booster that targets the new omicron subvariants that have become dominant around the world.

[ad_2]

[ad_1]

Elon Musk sent a letter to Twitter

TWTR,

indicating he intends to move forward with his original proposal that he acquire the company for $54.20 a share, according to a filing from the Securities and Exchange Commission.

The Tesla Inc.

TSLA,

CEO agreed to buy the social media company back in April for $44 billion, but in recent months said he wanted to terminate the deal, publicly citing concerns about bots on the platform. The two sides had been entrenched in a legal battle over the past few months, and a Delaware Chancery Court judge was scheduled to hear arguments on the case in October, a case Wedbush analyst Daniel Ives said Musk was “highly unlikely” to win.

Twitter users reacted to the news on Tuesday afternoon, many of them joking about a potential resolution to the seemingly never-ending Elon Musk Twitter saga.

One Twitter user said she believes Musk will look to reinstate the account of former President Donald Trump, which was banned shortly after the attack on the Capitol on Jan. 6, 2021. Trump has claimed he won’t return to Twitter even if the Musk deal is executed, and he’ll continue to post on his platform, Truth Social.

See also: Trump’s Facebook ban may end as soon as January 2023, Meta executive says

“We’re doing a big platform right now, so I probably wouldn’t have any interest,” the former president said.

Another user tweeted that supporters of the meme crypto dogecoin

DOGEUSD,

are excited by Musk’s move to proceed with the deal. Musk has touted dogecoin on several occasions in the past few years.

Similar to bitcoin, dogecoin is a peer-to-peer, open-source cryptocurrency. It trades under the ticker symbol “DOGE” and features the face of the shiba inu from the popular Doge meme as its logo. Dogecoin was up as much as 9.16% after the Bloomberg news was published.

Musk has not publicly commented on the report, but one Twitter user pointed out that he tweeted about his satellite internet project Starlink after the news broke, but did not mention Twitter in any way.

A report from The Wall Street Journal stated Musk’s legal team relayed the proposal to Twitter’s team “overnight Monday.”

Shares of Tesla Inc. dipped after the news, and are now up just 1.31% during Tuesday’s trading. Shares of the EV maker were up as much as 5.65% on the day before the Musk news.

The news comes a few days after hundreds of text messages from Musk’s phone were made public as evidence in Twitter’s lawsuit.

[ad_2]

[ad_1]

When the stock market has jumped two days in a row, as it has now, it is easy to become complacent.

But the Federal Reserve isn’t finished raising interest rates, and recession talk abounds. Stock investors aren’t out of the woods yet. That can make dividend stocks attractive if the yields are high and the companies produce more cash flow than they need to cover the payouts.

Below is a list of 21 stocks drawn from the S&P Composite 1500 Index

SP1500,

that appear to fit the bill. The S&P Composite 1500 is made up of the S&P 500

SPX,

the S&P 400 Mid Cap Index

MID,

and the S&P Small Cap 600 Index

SML,

The purpose of the list is to provide a starting point for further research. These stocks may be appropriate for you if you are looking for income, but you should do your own assessment to form your own opinion about a company’s ability to remain competitive over the next decade.

One way to measure a company’s ability to pay dividends is to look at its free cash flow yield. Free cash flow is remaining cash flow after planned capital expenditures. This money can be used to pay for dividends, buy back shares (which can raise earnings and cash flow per share), or fund acquisitions, organic expansion or for other corporate purposes.

If we divide a company’s estimated annual free cash flow per share by its current share price, we have its estimated free cash flow yield. If we compare the free cash flow yield to the current dividend yield, we may see “headroom” for cash to be deployed in ways that can benefit shareholders.

For this screen, we began with the S&P Composite 1500, then narrowed the list as follows:

For real-estate investment trusts, dividend-paying ability is measured by funds from operations (FFO), a non-GAAP figure that adds depreciation and amortization back to earnings. Adjusted funds from operations (AFFO) takes this a step further, subtracting cash expected to be used to maintain properties. So for the two REITs on the list, the FCF yield column makes use of AFFO.

For many companies in the financial sector, especially banks and insurers, free cash flow figures aren’t available, so the screen made use of earnings-per-share estimates. These are generally considered to run close to actual cash flow for these heavily regulated industries.

Here are the 21 companies that passed the screen, with dividend yields of at least 5% and estimated 2023 FCF yields at least twice the current payout. They are sorted by dividend yield:

| Company | Ticker | Type | Dividend yield | Estimated 2023 FCF yield | Estimated “headroom” |

| Uniti Group Inc. |

UNIT, |

Real-Estate Investment Trusts | 8.33% | 25.25% | 16.92% |

| Hanesbrands Inc. |

HBI, |

Apparel/ Footwear | 8.33% | 17.29% | 8.96% |

| Kohl’s Corp. |

KSS, |

Department Stores | 7.68% | 16.72% | 9.04% |

| Rent-A-Center Inc. |

RCII, |

Finance/ Rental/ Leasing | 7.52% | 17.26% | 9.73% |

| Macerich Co. |

MAC, |

Real-Estate Investment Trusts | 7.43% | 18.04% | 10.60% |

| Devon Energy Corp. |

DVN, |

Oil & Gas Production | 7.13% | 14.47% | 7.33% |

| AT&T Inc. |

T, |

Major Telecommunications | 6.98% | 14.82% | 7.84% |

| Newell Brands Inc. |

NWL, |

Industrial Conglomerates | 6.59% | 17.42% | 10.82% |

| Dow Inc. |

DOW, |

Chemicals | 6.18% | 15.63% | 9.45% |

| LyondellBasell Industries NV |

LYB, |

Chemicals | 6.09% | 16.07% | 9.99% |

| Scotts Miracle-Gro Co. Class A |

SMG, |

Chemicals | 6.04% | 12.68% | 6.65% |

| Diamondback Energy Inc. |

FANG, |

Oil & Gas Production | 5.56% | 13.63% | 8.08% |

| Best Buy Co. Inc. |

BBY, |

Electronics/ Appliance Stores | 5.53% | 14.08% | 8.55% |

| Viatris Inc. |

VTRS, |

Pharmaceuticals | 5.50% | 28.95% | 23.45% |

| Prudential Financial Inc. |

PRU, |

Life/ Health Insurance | 5.38% | 13.30% | 7.91% |

| Ford Motor Co. |

F, |

Motor Vehicles | 5.23% | 15.95% | 10.72% |

| Invesco Ltd. |

IVZ, |

Investment Managers | 5.23% | 14.95% | 9.73% |

| Franklin Resources Inc. |

BEN, |

Investment Managers | 5.17% | 13.21% | 8.04% |

| Kontoor Brands Inc. |

KTB, |

Apparel/ Footwear | 5.17% | 14.15% | 8.98% |

| Seagate Technology Holdings PLC |

STX, |

Computer Peripherals | 5.11% | 13.19% | 8.07% |

| Foot Locker Inc. |

FL, |

Apparel/ Footwear Retail | 5.03% | 15.52% | 10.49% |

| Source: FactSet | |||||

Any stock screen has its limitations. If you are interested in stocks listed here, it is best to do your own research, and it is easy to get started by clicking the tickers in the table for more information about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information for free on the MarketWatch quote page.

For the “estimated FCF yields,” consensus free cash flow estimates for calendar 2023 were used for all companies except the following:

Don’t miss: Dividend yields on preferred stocks have soared. This is how to pick the best ones for your portfolio.

[ad_2]

[ad_1]

This week Freddie Mac said the average interest rate on a 30-year mortgage loan in the U.S. had climbed to 6.70% from 6.29% the week before and 6.02% two weeks ago. The average rate a year ago was 3.01%.

Would-be sellers who have low-rate mortgage loans are reluctant if it means they need to take out a new loan to fund their next home. Would-be buyers are forced out of the market, as the monthly principal and interest payment for a new 30-year loan, based on Freddie Mac’s figures, has increased 53% from a year ago.

Home-sale contracts are being canceled at a record pace in some areas.

But these factors could lead to a buyer’s market in 2023 if prices plunge. Here are the areas economists expect to see the largest home price declines.

The dollar has strengthened as the Federal Reserve has taken the lead among central banks in raising interest rates. This is reverberating across the world, making it more costly for countries to make interest payments on dollar-denominated debt and increasing the cost of any commodity traded in dollars.