Shares of electric-vehicle startup VinFast Auto Ltd. have surged since the company went public through a special-purpose acquisition company deal last week, taking its market capitalization to levels well beyond established automakers such as Ford Motor Co. and General Motors Co.

Shares of low-float company VinFast VFS, +40.35%

rose 16.1% Friday, after ending Thursday’s session up 32.3%, sending the company’s market cap to $231.3 billion. In comparison, Ford’s F, +1.36%

market cap is $47 billion and GM’s GM, +0.21%

is $45.2 billion, according to FactSet data. Rival EV maker Rivian Automotive Inc. RIVN, +2.19%

has a market cap of $18.6 billion. However, all of these are dwarfed by Tesla Inc.’s TSLA, +3.72%

$730.2 billion market cap.

In roughly a week, the VinFast stream on Stocktwits, a social platform for investors and traders, has racked up about 3,000 watchers, and message volume is “pretty consistent” throughout the day, Tommy Tranfo, Stocktwits’ head of community, and Tom Bruni, a senior writer for the platform, told MarketWatch Thursday.

“What everyone is discussing is whether or not the current hype in the stock is warranted given where the business is,” Tranfo and Bruni said in a statement emailed to MarketWatch Thursday, noting the company’s soaring market cap. “That’s despite the underlying business doing less than $1 billion in revenue, having negative cash flow from operations of $1.5 to $2 billion.”

Uncredited

In the short term, the stock is trading on momentum and hype, according to Tranfo and Bruni. “But eventually, its business results have to justify the valuation. And as we’ve seen with other startups in the space, it’s easy to say they’re going to accomplish XYZ, but harder to actually execute and produce results,” they said.

“From the community side: [We] think what we’re paying attention to the most right now is if this hype sticks,” they added.

The EV maker is a majority-owned affiliate of Vietnamese conglomerate Vingroup, one of the largest publicly traded companies in Vietnam. VinFast said that as of June 30, 2023, the company has delivered close to 19,000 EVs.

About 99% of VinFast’s shares are controlled by Vingroup chair and VinFast founder Pham Nhat Vuon, making only a small portion available to investors.

Stocktwits’ Tranfo and Bruni noted that EVs have a good track record of growing strong retail community support. “So there is reason to believe that this momentum could continue, but it may be too early to tell for sure,” they added. “Retail loves the electric-vehicle industry, so the interest is likely to continue regardless of how well the company (and stock) actually perform.”

VinFast is importing its vehicles into the U.S. and is also ramping up its North American presence. In July, the company broke ground on an electric-vehicle manufacturing site within the Triangle Innovation Point in Chatham County, N.C. The EV startup says the plant will eventually have the capacity to make 150,000 EVs a year.

Credit Suisse said it has abandoned its plan to launch an initial public offering for its Credit Suisse 1a Immo PK real-estate fund due to low trading volumes for listed Swiss real-estate funds.

The Swiss bank–now part of UBS Group–said Thursday that Credit Suisse Funds decided not to carry out the IPO, which had been planned for the fourth quarter of 2023, and that this will allow the newly formed real-estate unit within UBS Asset Management to coordinate its offer of real-estate investment services.

A fall in trading volumes on the market for listed Swiss real-estate funds would likely have meant higher volatility in the event of a listing, Credit Suisse said.

The bank last year postponed the IPO of the fund, citing market conditions and the high volatility.

Write to Adria Calatayud at adria.calatayud@dowjones.com

stock plunged on Wednesday as investors kicked around a bevy of bad news. The shoe and sportswear retailer missed expectations for second-quarter sales, slashed its full-year outlook again, and paused its dividend.

UPS employees approved a new five-year union contract with the delivery giant Tuesday, about a month after reaching a tentative deal that averted a strike of 340,000 United Parcel Services workers.

The Teamsters said 86.3% of members voted for the “historic” deal, saying it was “the highest vote for a contract in the history of the Teamsters at UPS.” UPS, -0.97%

“Teamsters have set a new standard and raised the bar for pay, benefits and working conditions in the package-delivery industry,” Teamsters General President Sean O’Brien said in a statement. “This is the template for how workers should be paid and protected nationwide, and nonunion companies like Amazon AMZN, -0.32%

better pay attention.”

Among the parts of the contract the union highlighted were $2.75-an-hour raises for existing full- and part-time union members this year, and a total of a $7.50-an-hour raise over five years. All existing part-timers will earn at least $21 an hour starting immediately per the contract, according to the Teamsters.

The union also noted that the pay increases for full-timers will keep UPS Teamsters as the highest-paid delivery drivers in the country, with the average top rate rising to $49 an hour. In addition, the Teamsters said the new contract ends what it called the two-tier wage system at the company, with all UPS Teamster drivers currently classified as “22.4s” — or hybrid drivers and warehouse workers who were paid less than full-time drivers — to be reclassified immediately as RPCDs, or regular package car drivers.

A UPS spokesperson sent the following statement from the company: “Our Teamsters-represented employees have voted to overwhelmingly ratify a new five-year National Master Agreement that covers more than 300,000 full- and part-time UPS employees in the U.S.”

Amazon did not immediately respond to a request for comment.

One local supplemental agreement that affects 174 workers in Florida will be renegotiated, the union said. The national master agreement will go into effect as soon as that supplement, which is one of 44 local supplements, has been renegotiated and ratified, the union said.

U.S. banks and regional banks fell across the board on Tuesday, after S&P Global Ratings downgraded five smaller players after a review of risk related to funding, liquidity and asset quality with a focus on office commercial real estate.

Adding to the gloom, Republic First Bancorp. Inc.’s stock FRBK, -41.90%

tanked by 39%, after Nasdaq told the company that its stock would be delisted on Wednesday, after it failed to file its annual report in time.

S&P’s move comes just days after Fitch Ratings analyst Christopher Wolfe reduced his operating environment score for U.S. banks to aa- from aa due to the unknown path of interest rate hikes and regulatory changes facing the sector.

And Moody’s Investors Service just two weeks ago upset investors when it downgraded some lenders and said it was reviewing ratings on bigger banks, including Bank of New York Mellon BK, -1.71%,

State Street STT, -1.59%

and Northern Trust NTRS, -1.73%.

The S&P 500 Financials Sector has fallen for seven consecutive days, and is on pace for its longest losing streak since April 7, 2022, when it also fell for seven straight trading days.

Individual bank names are also performing poorly, with Goldman Sachs Group Inc. GS, -0.94%

and Citigroup Inc. C, -1.68%

down for 10 of the past 11 days and Charles Schwab Corp. SCHW, -4.84%

down 11 straight days.

Goldman alone has fallen for seven straight days for a total loss of 6.3%. It’s the longest losing streak since Feb. 28, 2020, when it also fell for seven straight days as the pandemic was taking hold.

The KBW Nasdaq Regional Banking Index KBWR

is down for 11 straight days. and the KBW Nasdaq Bank Index BKX

is down for seven straight days.

S&P downgraded Associated Banc. Corp. ASB, -4.20%,

Comerica Inc. CMA, -3.82%,

KeyCorp KEY, -3.58%,

UMB Financial Corp. UMBF, -2.42% % and Valley National Bancorp. VLY, -4.19%

by one notch and said the outlook on all five is stable.

The rating agency affirmed ratings on Zions Bancorp ZION, -4.17%

and maintained a negative outlook, meaning it could downgrade them again in the near-term. And it affirmed ratings and a stable outlook on Synovus Financial Corp. SNV, -3.37%

and Truist Financial Corp. TFC, -1.36%

“We reviewed these 10 banks because we identified them as having potential risks in multiple areas that could make them less resilient than similarly rated peers ,” S&P said in a statement.

“For instance, some that have seen greater deterioration in funding—-as indicated by sharply higher costs or substantial dependence on wholesale funding and brokered deposits—-may also have below-peer profitability, high unrealized losses on their assets, or meaningful exposure to CRE.”

The steep rise in interest rates orchestrated by the Federal Reserve over the past year has raised deposit costs as banks are now competing for savers seeking higher returns and that’s forced some to pay up on deposits and discourage their clients from heading to other institutions and instruments.

However, S&P said about 90% of the banks it rates have stable outlooks and just 10% have negative ones. None have positive outlooks.

The widespread stable outlooks shows that stability in the U.S. banking sector has improved significantly in recent months.

S&P is expecting FDIC-backed banks in aggregate to earn a relatively healthy ROE of about 11% in 2023.

KeyCorp. and Comerica both fell more than 3% on the news. Of the two, KeyCorp. has more outstanding debt and its 10-year bonds widened by about 5 to 10 basis points, according to data solutions provider BondCliq Media Services.

As the following chart shows, the bonds have seen better selling on Wednesday with buyers emerging around midmorning.

KeyBank net customer flow (intraday). Source: BondCliQ Media Services

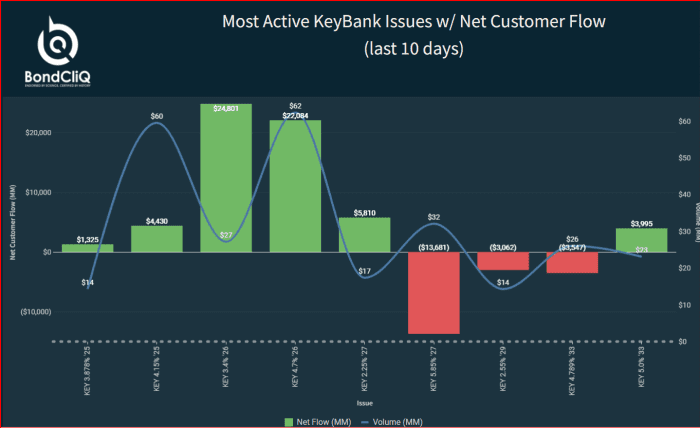

The next chart shows customer flow over the last 10 days.

Most active KeyBank issues with net customer flow (last 10 days). Source: BondCliQ Media Services

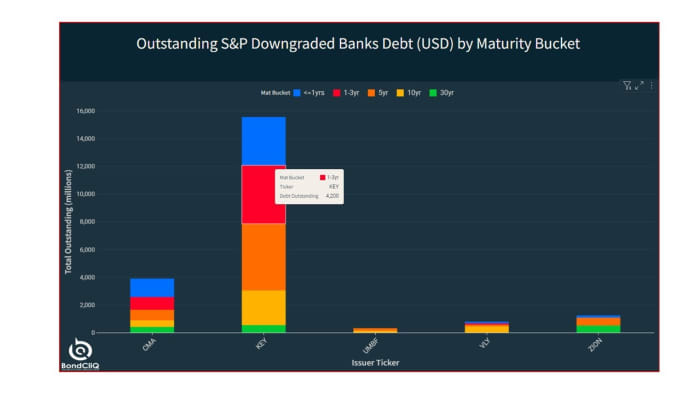

The next chart shows the outstanding debt of the downgraded banks, with KeyCorp. clearly the leader with almost $16 billion of bonds.

Outstanding S&P downgraded banks debt USD by maturity bucket. Source: BondCliQ Media Services

Arm Holdings Ltd. filed its long-awaited initial public offering late Monday, following last year’s failed bid by Nvidia Corp. to acquire the U.K.-based chip architecture company.

Arm has reportedly been seeking to raise $8 billion to $10 billion at a valuation of $60 billion to $70 billion, making its IPO the biggest of the year so far, and a number of large tech companies, including Amazon.com Inc. AMZN, +1.10%, Intel Corp. INTC, +1.19%

and Nvidia NVDA, +8.47%,

are reportedly in the mix to be anchor investors.

At the time of the breakup, chips sales had hit record highs in 2021, surging 26.2% to a record $555.9 billion, fueled by pandemic-triggered shortages. But the chip industry has since swung to a glut.

Arm listed Barclays, Goldman Sachs, JP Morgan, Mizuho, BofA Securities, Citigroup, and Deutsche Bank Securities among the IPO’s underwriters.

Recent reports said SoftBank was in discussions to purchase the 25% stake in Arm that it does not outright own, which is held by its Vision Fund 1, ahead of the IPO.

Arm reported net income of $524 million, or 51 cents a share, on revenue of $2.68 billion for fiscal 2023, which ended March 31, compared with net income of $549 million, or 54 cents a share, on revenue of $2.7 billion, in fiscal 2022, and $388 million, or 38 cents a share, on revenue of $2.03 billion in fiscal 2021.

Arm uses an architecture that is different from the once-standard x86 one built by Intel in the early days of computing.

The company said it has shipped more than 250 billion Arm-based chips since its started in 1990 as a joint venture between Acorn Computers, Apple AAPL, +0.77%

and VLSI Technology. In fiscal 2023, Arm said it shipped 30.6 billion chips.

The company said it is going public as the “resources required to develop leading-edge products are significant and continue to increase exponentially as manufacturing process nodes shrink.” Transistors are expressed in scales of nanometers, with design costs running about $249 million for a 7-nanometer chip and about $725 million for a 2-nm chip.

“As the world moves increasingly towards AI- and [machine language]-enabled computing, Arm will be central to this transition,” the company said in the filing. “Arm CPUs already run AI and ML workloads in billions of devices, including smartphones, cameras, digital TVs, cars and cloud data centers.”

Arm said it is working with Alphabet Inc. GOOG, +0.64%

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

Novartis said the planned spinoff of its Sandoz generic pharmaceuticals and biosimilars business is expected to occur on or around Oct. 4.

The Swiss pharmaceutical giant said Friday that the separation will take place through a proposed distribution of Sandoz shares to its existing shareholders. Novartis shareholders will get one Sandoz shares for every five Novartis shares held and one Sandoz American depositary receipts–or ADRs–for every five Novartis ADRs, the company said.

Novartis had previously said it expected the spinoff to happen early in the fourth quarter.

The Sandoz spinoff remains subject to approval by Novartis’s shareholders. Novartis has scheduled an extraordinary general meeting for Sept. 15 to vote on the proposed distribution of Sandoz shares and a reduction in its own share capital in connection with the spinoff, it said.

Following the separation, Sandoz would be listed in SIX Swiss Exchange, with an ADR program in the U.S., Novartis said.

Write to Adria Calatayud at adria.calatayud@dowjones.com

Heavily-indebted Evergrande, which has symbolized China’s property crisis, made its filing amid growing fears that the sector’s troubles will spread to other parts of the country’s economy.

Since mid-2021, companies accounting for 40% of Chinese home sales have defaulted, stoking fears about the resilience of the world’s second-largest economy.

A Chapter 15 bankruptcy is a way for foreign companies with U.S. assets to get access to domestic courts.

Spillover from Evergrande’s 2021 debt woes rattled investors in stocks and spurred a flight to safety in U.S. government bonds. Investors this week have been closely monitoring developments in China’s property markets.

Stocks were headed for another week of losses on Thursday, with the Dow Jones Industrial Average DJIA

off 2.3% so for the week, the S&P 500 index SPX

2.1% lower and the Nasdaq Composite Index off 2.4%, according to FactSet. Dow YM00, -0.08%

and S&P 500 ES00, -0.15%

futures fell slightly late Thursday.

Chris Low, FHN Financial’s chief economist, said the “mess in China” was resulting in a flight-to-quality bid for 10-year Treasurys, in a Wednesday note to clients. The 10-year yield BX:TMUBMUSD10Y

shot up to 4.307% on Thursday, the highest since November 2007, according to FactSet.

Adyen shares fell as much as 22% on Thursday as the fast-growing Dutch payment company’s first-half results lagged estimates.

Adyen’s ADYEN, -25.02%

first-half profit was virtually flat at €282.2 million ($307 million), while net revenue rose 21% to €739.1 million, missing the consensus of €777 million.

Its earnings before interest, tax, depreciation and amortization fell 10% to €320 million, lagging the consensus of €379 million.

Adyen has previously lamented not being able to grow its team in North America, which it said is impacting now. “We now see the impact of a sales team size that did not match our ambitions, particularly in North America,” the company said in its shareholder letter. In the first half, it added 551 full-time employees, three-quarters in tech roles. The company blamed the adjusted profit decline on increased wages and salaries.

Inflation was a problem for its customers, too. “As a natural consequence of the shifting economic climate – driven by higher inflation and interest rates – profit outweighed growth for many North American digital businesses in the first half. Enterprise businesses prioritized cost optimization, while competition for digital volumes in the region provided savings over functionality,” the company said.

The company reiterated its longer-term revenue and margin goals, including for revenue growth between the mid-twenties and low-thirties. “We know that growth is not always linear, and reiterate our financial objectives,” the company said.

Hawaiian Electric Industries Inc.’s stock added to losses Tuesday, tumbling 26% after S&P Global Ratings downgraded its rating on the utility company to junk.

S&P Global Ratings cut its rating on the company HE to BB- and placed it on CreditWatch negative, meaning the rating agency could downgrade it again in the near term.

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

SoftBank Group Corp. is reportedly in discussions to purchase the 25% stake in chip designer Arm Ltd. that is held by its Vision Fund 1, ahead of a highly anticipated IPO.

Reuters reported Sunday that Japan’s SoftBank 9984, +0.37%

— which owns 75% of Arm — is negotiating a deal with VF1, the $100 billion investment fund it created in 2017, and noted that a deal could give VF1 investors a big boost after years of meager returns. Saudi Arabia’s Public Investment Fund and Abu Dhabi’s Mubadala Investment Co. are among VF1’s largest investors.

SoftBank is planning to launch a long-awaited initial public offering for British chip designer Arm as soon as September. That will likely be the biggest IPO of the year on Wall Street, aiming to raise $8 billion to $10 billion at a valuation around $60 billion to $70 billion.

The thing that will make companies lower prices is if consumers stop complaining about paying more for the things they need and want, and actually start refusing to buy them.

As the U.S. corporate earnings-reporting season progresses, with earnings from major retailers Walmart Inc. WMT, +0.59%,

Target Corp. TGT, +0.10%

and Home Depot Inc. HD, +0.52%

on tap next week, investors can get a ground-floor view of how consumer demand may have been hurt, or not, by higher prices, and what the companies plan to do, or not do, about it.

This dynamic of how consumers adjust their spending habits when prices change is referred to by economists as the price elasticity of demand.

“ For companies to cut prices, ‘you have to have the consumer go on strike, and they’re not there yet.’”

— Jamie Cox, Harris Financial Group

Those who trust companies will choose to ratchet down prices on their own, or at least not raise them because the rise in input costs has been slowing, haven’t been listening to what the many companies have told analysts on their post-earnings-report conference calls.

Kraft Heinz Co. KHC, +0.47%

acknowledged after its second-quarter report that its relatively higher prices have hurt demand, but not by enough for the food and condiments company to consider cutting prices.

Colgate-Palmolive Co. CL, +0.81%

said it will continue to raise prices, even as inflation slows and selling volume declines, as the consumer-products company continues to be laser focused on boosting margins and profits.

And while PepsiCo Inc. PEP, +0.16%

was worried that elasticities would increase, given how its lower-income customers were being particularly pressured by inflation, the beverage and snack giant reported strong results as it witnessed “better elasticities” in most of the markets in which it operated.

“Obviously, there is still carryover pricing, and I don’t think we’ll do anything different than our normal cycles on pricing in the balance of the year,” PepsiCo Chief Financial Officer Hugh Johnston told analysts, according to an AlphaSense transcript.

Basically, as MarketWatch has reported, so-called greedflation is alive and well.

Jamie Cox, managing partner for Harris Financial Group, said as long as the job market stays strong, as it is now, corporate greed will continue to pay off.

“If something is more expensive, and you have a job, you’ll complain about it, but you won’t substitute it for something cheaper,” Cox said. For companies to cut prices, “you have to have the consumer go on strike, and they’re not there yet,” Cox added.

“ ‘At some point, people are going to say, “All right — enough.” ’ ”

— Paul Nolte, Murphy & Sylvest Wealth Management

The reason elasticity is so important in the current environment is that, as long as consumers continue to pay the higher prices companies are charging, inflation will remain stubbornly high, making it, in turn, more likely that the Federal Reserve will continue to raise interest rates or, at the very least, not lower them.

But the longer interest rates stay high enough to crimp economic growth, the more likely the stock market will reverse lower as recession fears rise.

“At some point, people are going to say, ‘All right — enough,’ ” said Paul Nolte, senior wealth manager and market strategist at Murphy & Sylvest Wealth Management. “But we just haven’t seen that yet.”

What is elasticity?

Economists use the term “price elasticity of demand” to refer to the way in which consumers adjust their spending habits when prices change.

“Elasticity tries to measure how much more producers will want to produce if prices rise, and how much more consumers will want to buy if prices fall,” explained Bill Adams, chief economist at Comerica.

Elasticity often depends on the type of product a company sells.

For example, consumer-discretionary-goods companies that sell products and services that people want will often experience greater price elasticity than consumer-staples companies that sell things that people need, such as groceries and prescription drugs.

But even for needs, consumers often still have a choice, as less expensive generic, or private-label, alternatives may be available.

Andre Schulten, chief financial officer of consumer-staples maker Procter & Gamble Co. PG, +0.58%,

which recently beat earnings expectations as it continued to raise prices, telling analysts that, while there was “some trading into private label,” the overall market share of private-label products was unchanged for the year.

As Harris Financial’s Cox said, consumers may be complaining about higher prices, but they aren’t yet desperate enough to stop buying.

The Federal Reserve’s latest Beige Book economic survey stated that business contacts in some districts had observed a “reluctance” to raise prices as consumers appeared to have grown more sensitive to prices, but other districts reported “solid demand” allowed companies to maintain prices and profitability.

That’s likely why companies and analysts have become less concerned about price elasticity. Based on a FactSet analysis, mentions of the word “elasticity” in press releases and conference calls of S&P 500 companies SPX

increased as inflation and interest rates started surging in early 2022 through the end of the year.

Mentions of the word elasticity in earnings press releases and conference-call transcripts of S&P 500 companies.

FactSet

As the chart shows, “elasticity” popped up in more than 55% of earnings releases and conference calls in mid-2022, but with the second-quarter 2023 earnings-reporting season more than half over, mentions had dropped to about 20%.

Perhaps that will pick up, as retailers, especially those catering to lower-income customers — recall the PepsiCo comment — assess the demand impact of continued price increases.

Meanwhile, the branded-foods company Conagra Brands Inc. CAG, +0.71%,

whose wide-ranging food brands including Birds Eye, Duncan Hines, Hunt’s, Orville Redenbacher’s and Slim Jim, were starting to see the emergence of a different dynamic.

Chief Executive Sean Connolly said consumers were shifting behavior in some categories as prices remained high. Rather than trade down to lower-priced alternatives, he noticed some consumers buying fewer items overall, “more of a hunkering down than a trading down.”

That’s exactly the kind of consumer behavior that is needed, if companies are to stop feeding into the greedflation phenomenon and to start pulling back on prices.

Analysts got to the point early and often during a conference call late Wednesday: What are Disney Chief Executive Robert Iger’s M&A plans, particularly following reports that former Disney executives Kevin Mayer and Tom Staggs, now co-CEOs of Blackstone-backed Candle Media, have been retained in a “consulting capacity” to decide ESPN’s fate?

The prospect of an Apple-Disney combo seems far-fetched in a heated regulatory climate, where the Federal Trade Commission is attempting to crack down on Big Tech acquisitions, but it could happen should Disney sell off assets and Apple gobbles up Disney’s direct-to-consumer business that includes streaming service Disney+, some media analysts speculate. Apple could conceivably even buy ABC, which reportedly is on the block. But the path is long and circuitous.

Yet the rumors persist, dating back to Apple co-founder Steve Jobs’ reverence for the Disney brand, and the increasingly overlapping businesses of both companies over the years.

When pressed by analysts during a conference call late Wednesday, Iger declined to discuss the future of Disney’s structure or possible asset sales. When asked if Disney might “plausibly” be snapped up by one company — read Apple — an exasperated Iger said he would not “speculate” on the sale of Disney to a technology company or anyone else, given the current global stance of regulators. The FTC has aggressively challenged mergers from the likes of Microsoft Corp. MSFT, -1.17%

and Facebook parent Meta Platforms Inc. META, -2.38%,

with limited success.

Since Iger hinted at the potential sale of Disney’s assets in an interview with CNBC last month, rumors have swirled around ESPN.

ESPN and related properties likely could command at least one-third of Disney’s current depressed market cap of about $150 billion, say some media watchers, though Iger has denied ESPN is for sale. He has acknowledged “the sports leader” is seeking “strategic partners” — possibly with the NFL, MLB, NBA and NHL — to generate revenue. Late Tuesday, ESPN stuck up a deal with Penn Entertainment Inc. PENN, +9.10%

to create ESPN Bet, a digital sportsbook to launch in the fall in 16 states.

Another possible property being dangled is ABC. But with rights to the NBA Finals and two Super Bowls in the next eight years, it is unclear who would acquire the network and how Disney would replace lucrative sports revenue.

Other properties on the block include cable channels Freeform and Disney Channel, according to a report by the Wall Street Journal.

“If an asset sale happens, will the proceeds be deployed into fortifying its balance sheet or beefing up its remaining operations?” Rick Munarriz, senior media analyst at The Motley Fool, said in an email.

Disney, which is in the midst of a $5.5 billion cost-cutting campaign, is exploring several avenues to prop up sales as linear TV ads shrink, Disney+ subscriptions decline and attendance at Walt Disney World wanes.

Shares of Disney are trading at half their highs from a few years ago, in large part because of dwindling sales and profits at ESPN and Disney’s other cable networks.

Enter Mayer, who previously ran Disney’s strategic planning group for years and engineered a trifecta of mega deals: The acquisition of the aforementioned Pixar Animation Studios from Steve Jobs for $7.4 billion in 2006, the purchase of Marvel Entertainment for $4 billion in 2009, and the acquisition of Lucasfilm for $4.05 billion in 2012. Mayer also led the $71.3 billion acquisition of 20th Century Fox’s entertainment assets in 2019, which has drawn mixed reviews.

Online sports-betting company Penn Entertainment Inc. sealed a $1.5 billion deal with Walt Disney Co.’s DIS, +1.50%

ESPN to launch ESPN Bet, a branded sportsbook for fans in the U.S., and pivoted away from Barstool Sports on Tuesday, selling the platform back to founder Dave Portnoy.

Penn Entertainment PENN, -0.68%

will rebrand its current sportsbook and relaunch as ESPN Bet in the fall in 16 legalized-betting states where Penn is licensed.

The rebrand — which includes the mobile app, website, and mobile website — sent Penn’s stock soaring 13% in after-hours trading Tuesday. ESPN Bet will benefit from exclusive promotional services across ESPN’s platforms, including access to ESPN talent, the companies said.

Penn will pay ESPN $1.5 billion over 10 years as part of the strategic partnership, and will grant ESPN $500 million of warrants to purchase about 31.8 million Penn common shares, with additional bonus warrants possible.

“Together, we can utilize each other’s strengths to create the type of experience that existing and new bettors will expect from both companies, and we can’t wait to get started,” Penn Entertainment Chief Executive Jay Snowden said in a release.

Penn also said it has divested 100% of its stake in Barstool Sports to Portnoy, allowing the sports media platform “to return to its roots of providing unique and authentic content to its loyal audience without the restrictions associated with a publicly traded, licensed gaming company.”

For Penn, the ESPN partnership represents “a clear step up from Barstool in terms of mass appeal…and minimal regulatory risk,” according to Wells Fargo analyst Daniel Politzer, who said it was a “nearly impossible challenge for a publicly traded, licensed gaming company” to own “a media platform that thrived on viral/provocative content.”

Still, he said in a note to clients that “it’s premature to conclude this is a game change” since past partnerships between online sports-betting companies and media players have come up short of what initial fanfare would’ve suggested.

The news sent rival DraftKings Inc. shares DKNG, +0.25%

sinking about 5% in after-hours trading.

The decline in DraftKings shares comes as they’ve advanced 178% so far in 2023, through Tuesday’s close. Two analysts upgraded DraftKings’ stock just this week.

Palantir Technologies Inc. matched expectations with its latest quarterly results Monday while announcing a new $1 billion buyback authorization.

The software company posted its third quarter in a row of GAAP profitability, recording second-quarter net income of $28 million, or 1 cent a share, whereas Palantir PLTR, -1.15%

racked up a net loss of $179.3 million, or 9 cents a share, in the year-earlier period. Analysts tracked by FactSet were modeling GAAP earnings per share of 1 cent.

Palantir logged adjusted earnings per share of 5 cents, in line with the FactSet consensus.

Revenue rose to $533 million from $473 million and also met the FactSet consensus. The company notched $232 million in commercial revenue, up 10% from a year before, along with $302 million of government revenue, up 15%.

After initially falling following the report, Palantir shares rose 2.6% in after-hours trading.

“We continue to see unprecedented demand,” Chief Revenue Officer Ryan Taylor told MarketWatch. That includes both “top-of-funnel” conversations with new customers and others expanding their use of Palantir software, as momentum builds for the company’s artificial-intelligence offerings.

Taylor added that Palantir’s U.S. government work has “never been stronger.”

Palantir also announced that its board of directors has approved a stock-buyback program of up to $1 billion. The move comes as the company posted $285 million in adjusted free cash flow during the first half of the year and finished the second quarter with $3.1 billion in cash and equivalents on its balance sheet.

“Our cash flow, balance sheet and the authorization of a billion-dollar buyback show what we believe in for the future of this company,” Chief Financial Officer David Glazer told MarketWatch. The belief is that “AI is a massive opportunity.”

Added Chief Executive Alex Karp in a shareholder letter: “The scale of the opportunity that lies ahead has increased significantly in recent months. And we intend to capture it.”

He noted that the company is in talks with more than 300 additional enterprises about using Palantir’s AI platform, “all of which are searching for an effective and secure means of adapting the latest large language models for use on their internal systems and proprietary data.”

For the third quarter, Palantir expects $553 million to $557 million in revenue, along with GAAP profitability. Analysts tracked by FactSet were modeling $553 million,

Palantir also expects to report GAAP net income for its fourth quarter. It further models upwards of $2.212 billion in full-year revenue, while analysts were looking for $2.210 billion.

Palantir Technologies Inc. matched expectations with its latest quarterly results Monday while announcing a new $1 billion buyback authorization.

The software company posted its third quarter in a row of GAAP profitability, recording second-quarter net income of $28 million, or 1 cent a share, whereas Palantir PLTR, -1.15%

racked up a net loss of $179.3 million, or 9 cents a share, in the year-earlier period. Analysts tracked by FactSet were modeling GAAP earnings per share of 1 cent.

Palantir logged adjusted earnings per share of 5 cents, in line with the FactSet consensus.

Revenue rose to $533 million from $473 million and also met the FactSet consensus. The company notched $232 million in commercial revenue, up 10% from a year before, along with $302 million of government revenue, up 15%.

After initially falling following the report, Palantir shares rose 2.6% in after-hours trading.

“We continue to see unprecedented demand,” Chief Revenue Officer Ryan Taylor told MarketWatch. That includes both “top-of-funnel” conversations with new customers and others expanding their use of Palantir software, as momentum builds for the company’s artificial-intelligence offerings.

Taylor added that Palantir’s U.S. government work has “never been stronger.”

Palantir also announced that its board of directors has approved a stock-buyback program of up to $1 billion. The move comes as the company posted $285 million in adjusted free cash flow during the first half of the year and finished the second quarter with $3.1 billion in cash and equivalents on its balance sheet.

“Our cash flow, balance sheet and the authorization of a billion-dollar buyback show what we believe in for the future of this company,” Chief Financial Officer David Glazer told MarketWatch. The belief is that “AI is a massive opportunity.”

Added Chief Executive Alex Karp in a shareholder letter: “The scale of the opportunity that lies ahead has increased significantly in recent months. And we intend to capture it.”

He noted that the company is in talks with more than 300 additional enterprises about using Palantir’s AI platform, “all of which are searching for an effective and secure means of adapting the latest large language models for use on their internal systems and proprietary data.”

For the third quarter, Palantir expects $553 million to $557 million in revenue, along with GAAP profitability. Analysts tracked by FactSet were modeling $553 million,

Palantir also expects to report GAAP net income for its fourth quarter. It further models upwards of $2.212 billion in full-year revenue, while analysts were looking for $2.210 billion.