U.S. stocks closed lower for a fourth session in a row on Thursday as pressure on shares of banking stocks continued to weigh on equities. The Dow Jones Industrial Average DJIA fell about 286 points, or 0.9%, ending near 33,127, according to preliminary FactSet figures. The S&P 500 index SPX fell 0.7% and the Nasdaq Composite Index COMP slumped 0.5%. That marked the S&P 500’s longest losing streak since since Feb. 22, according to Dow Jones Market Data, and the longest losing stretch since Dec. 19 for the Nasdaq. Pressure in the U.S. banking sector has been a key focus for investors, with shares of the SPDR S&P Regional…

The Federal Reserve’s interest-rate increases have been propping open a window for people to get tempting yields in turbulent times from savings accounts, certificates of deposit and other low-risk cash investments.

Now the Fed increased its benchmark rate again Wednesday. The 25-basis point increase is the central bank’s tenth straight rate hike since March 2022. The increase, which brings the rate to a range of 5%-5.25%, could also be the final increase too, some Fed watchers say.

So if the window for high yields on low-risk cash investments is at its highest point for now, there’s likely only one direction they’ll go next, observers say.

“In our view, we are now at the peak or very near the peak in the federal funds rate. If you look at the market signals, they indicate exactly that,” said Angelo Kourkafas, investment strategist at Edward Jones.

What that means for rate-sensitive cash investments — like bank accounts, CDs, money-market funds and short-term Treasury debt maturing within one year — “is an opportunity to take advantage of these high yields that are not going to last forever,” he said.

The largest money-market funds currently offer an average 4.64% seven-day yield as of Monday, according to Crane Data. Meanwhile, the yields on Treasury bills are also ranging around 4% to 5%, according to data.

The annual percentage yields on high-yield savings accounts and one-year online bank CDs can now reach 4% and 5%, according to DepostAccounts.com.

But some of the longest maturity CDs “may have already peaked,” according to Ken Tumin, the site’s founder and senior industry analyst at LendingTree.

Long-term CD rates are less influenced by the federal funds rate moves and “are the first ones to react,” he said. The APY on a five-year CD averaged 3.95% in April, down from 4.04% in January, he noted.

Rate retreats show elsewhere. I-bonds, the fixed-income investments pegged to inflation that caught wide attention, now offer a 4.3% rate. That’s down from 6.89% in the previous six months, and off their recent peak of 9.62%.

“It’s not imminent that we see lower [Federal Reserve] rates down the road, but we could potentially by the end of the year,” said Kourkafas. “From an investor standpoint, locking in some of these high yields makes sense,” he later added.

“This could be ‘last call’ for savers,” said Greg McBride, Bankrate chief financial analyst. “CD yields on maturities of one year and longer have peaked, and now is the time to lock in. A slowing economy coupled with the Fed moving to the sidelines mean CD yields will start pulling back soon.”

Are we at the top?

It’s tough to say for sure whether the Fed has reached the top of this particular interest-rate cycle, but it’s a key question for Wednesday’s Fed meeting. Another question is when the central bank starts considering rate decreases.

With its latest rate increase Wednesday, the central bank said, looking ahead, it will weigh a range of factors to decide the extent that “additional policy firming may be appropriate.”

There’s been no decision on a pause, Federal Reserve Chair Jerome Powell told reporters Wednesday. But the central bank had a tone shift in its latest statement, discarding a line that said “some” extra increases “may” be necessary.

It was “a meaningful change that we’re no longer saying we anticipate. So we’ll be driven by incoming data meeting by meeting, and we’ll approach that question at the June meeting,” Powell said.

For around a year, “retail investors — as they do in every tightening cycle — they’ve been gradually moving their deposits into higher yielding places, such as CDs and other things, including money market funds,” Powell noted.

“That’s a gradual process that is quite natural and happens during a tightening cycle,” he said.

If the Fed keeps its rate higher for longer, the window for higher yields will likely stay at its peak for a while, said Tumin. “Deposit rates might not fall quickly, so people might have time to take advantage of higher deposit rates.”

Federal Deposit Insurance Corporation data showed banks paying $78.7 billion in interest on domestic deposit accounts last year, according to DepositAccounts.com research. That’s more than triple the $24.3 billion that banks paid for deposit interest in 2021.

“If things turn for the worse,” Tumin said, “deposit rates could fall quickly, before the first Fed rate cut.” If banks tone down their personal and business lending portfolios, they wouldn’t need to entice as many depositors with higher rates, he explained.

Economists say credit is already tightening as banks mull their next move after the failures of Silicon Valley Bank and Signature Bank last month. This week, JPMorgan Chase & Co. JPM, -2.12% acquired First Republic Bank after the troubled lender closed its doors.

Ever since the Fed started tightening, consumers have become “increasingly rate-conscious,” said Jennifer White, senior director of banking and payments intelligence at JD Power.

“What goes along with rate chasing is all the other behavior that consumers learned during this process,” she said. That includes a heightened focus on the customer services a bank offers, and the costs it charges for those services, she said.

If and/or when interest rates decline, “I don’t think that’s going to be lost on customers,” White said.

Don’t get carried away

“With cash rates where they are right now, you can get meaningful yield,” said Mike Loewengart, head of model portfolio construction at Morgan Stanley’s MS, -1.78%

Global Investment Office. “It can make sense to hold a larger portion of cash, and cash-like investments.”

Just how much cash you decide to hold onto depends on your own risk tolerance, and the amount of time before you need to tap your portfolio, he said. Just don’t go overboard, he said.

There are many convenient trade-offs, like the lock-up period for money in a CD, or the fact that returns on cash ultimately cannot outrun inflation. “If you’re holding excess cash in your portfolio, you run the risk of not maintaining purchasing power over time,” Loewengart added.

Suppose investors pulled all their money from stocks and bonds, and put it all into Treasury bills that matured in three months’ time?

That cash-focused investor would have a 74% chance of underperforming a 60/40 portfolio, according to Vanguard’s number crunch on four decades of data. The person’s returns would be around 4% lower, researchers said.

If the investor stayed in three-month Treasury bills for a year, Vanguard’s analysts said they faced an 87% chance of underperforming a 60/40 portfolio. Here, the T-bill investor underperformed the 60/40 portfolio by an average 13.5% underperformance, Vanguard said.

Joe Davis, Vanguard’s chief global economist, said does not expect a rate cut this year.

Vanguard sees inflation cooling, but it also predicts a recession in the second half of the year that entails less bank lending, more job losses, and more bankruptcy cases, he said.

Financial advisers always emphasize the importance of keeping the long view, and avoiding knee-jerk investment decisions that attempt to time the market.

Markets and investors have experienced “the most aggressive Fed rate-hiking campaign” in decades, said Kourkafas. “It’s a big milestone, but now we have to think about what’s next.”

It’s been “painful for everything — except cash — last year,” Kourkafas said. “But now, as we make that turning point, there’s an opportunity with cash, but also investors shouldn’t forgo other parts of their portfolio.”

U.S. stocks closed lower on Tuesday, but were well off the session’s lows, a day before the Federal Reserve could be poised to fire off its last interest rate hike of this cycle. The Dow Jones Industrial Average DJIA shed about 367 points, or 1.1%, ending near 33,684, according to preliminary FactSet figures. The S&P 500 index SPX shed 1.2%, while the Nasdaq Composite Index COMP closed 1.1% lower. Regional bank stocks were hammered on Tuesday, a day after JPMorgan Chase & Co. won an auction for the assets of the failed First Republic Bank. The SPDR S&P Regional Bank ETF KRE closed down 6.4% on Tuesday. U.S. crude oil…

Some clarity is emerging regarding statements from Biden administration officials that no one making less than $400,000 will see higher audit rates by the Internal Revenue Service, which is about to step up its scrutiny of wealthy taxpayers.

The Inflation Reduction Act — the tax and climate package enacted last summer — earmarked $80 billion for the IRS over the next decade and a half. The money is intended in part to facilitate more audits of corporations and wealthier individuals.

Ahead of the bill’s passage, Treasury Secretary Janet Yellen pledged that there would be no increase in the audit rate for households and small businesses with annual incomes below $400,000 “relative to historical levels.”

But Republican critics and other observers have asked what “historical levels” might actually mean.

The audit rate on returns for tax year 2018 is the reference point to keep in mind, IRS Commissioner Danny Werfel told senators on Wednesday. He emphasized that “there’s no surge coming for workers, retirees and others.”

The IRS audited fewer than 1% of 2018 returns with total positive incomes — the sum of all positive amounts shown for various sources of income reported on an individual income-tax return, which excludes losses — of between $1 and $500,000, according to statistics that the tax agency released last week.

The agency has three years to start an audit from the time it receives a return.

The numbers show that 0.4% of returns for taxpayers earning up to $25,000 were audited. That figure was 0.3% for returns between $200,000 and $500,000 and more than 9% for returns over $10 million, the IRS data show. Six years earlier, more than 13% of returns over $10 million were scrutinized, according to the IRS.

“Help us with understanding what the words ‘historic level’ means,” Sen. James Lankford, a Republican from Oklahoma, asked Werfel during a Wednesday budget hearing.

“We will take the most recent final audit rate, and it’s historically low … and we allow that to be the marker for least several years, and then we’re revisit it,” Werfel said. The 2018 audit rates were the newest final rates, he added.

“So the 2018 number is what it’s going to be?” Lankford asked.

“Yes,” Werfel replied.

“Werfel’s explanation that 2018 audit levels will be the reference point is the most detail I’ve heard so far,” Erica York, s senior economist at the Tax Foundation, told MarketWatch. “He did seem to leave open the possibility of revisiting the reference year for ‘historical’ in the future,” she added.

Another open question has been how the $400,000 income threshold will be determined. Months after the Inflation Reduction Act passed, IRS and Treasury officials still hadn’t finalized what counted as $400,000 in income, according to a January Treasury Department watchdog report.

“How are you arriving at this number?” asked Sen. Marsha Blackburn, a Republican from Tennessee. Blackburn’s state has many self-employed entrepreneurs who might appear richer on paper than they actually are, she said. “While they may have a higher gross, their net is very low,” she added.

“We’re going to look at total positive income as our metric,” Werfel said. He later added that “there would be no increased likelihood of an audit if they have less than $400,000 in total positive income.”

The IRS description of total positive income as “the sum of all positive amounts shown for the various sources of income reported on an individual income tax return and, thus, excludes losses” represents, effectively, a tally of income before taxpayers subtract their losses.

Total positive income is a metric the IRS usually applies to categorize audits, the Tax Foundation’s York noted. But one challenge of strict thresholds for more audits, she said, “is that it creates incentives for underreporting income” to stay under the line.

Compared with recent years, there are now more specifics about how the IRS will implement additional audits of higher-income taxpayers, said Janet Holtzblatt, a senior fellow at the Tax Policy Center.

“But still there are questions,” she noted, about how the agency will treat situations when taxpayers don’t provide full picture of their income.

Here’s a thought for investors: If the Federal Reserve raises interest rates to 5% or more would that wreck the economy and stock prices ?

The U.S. stock market has been rallying to start 2023, clawing back a big chunk of the painful losses from a year ago. The bullish tone has been linked to a view that the Federal Reserve will need to cut interest rates this year to prevent a recession, reversing one of its quickest rate-increasing campaigns in history.

Doomsday investors, including hedge-fund billionaire Paul Singer, have been warning against that outcome. Singer thinks a credit crunch and deep recession may be necessary to purge dangerous levels of froth in markets after an era of near-zero interest rates.

Another scenario might be that little changes: Credit markets could tolerate interest rates that prevailed before 2008. The Fed’s policy rate could increase a bit from its current 4.75%-5% range, and stay there for a while.

“A 5% interest rate is not going to break the market,” said Ben Snider, managing director, and U.S. portfolio strategist at Goldman Sachs Asset Management, in a phone interview with MarketWatch.

Snider pointed to many highly rated companies which, like the majority of U.S. homeowners, refinanced old debt during the pandemic, cutting their borrowing costs to near record lows. “They are continuing to enjoy the low rate environment,” he said.

“Our view is, yes, the Fed can hold rates here,” Snider said. “The economy can continue to grow.”

Profits margins in focus

The Fed and other global central banks have been dramatically increasing interest rates in the aftermath of the pandemic to fight inflation caused by supply chain disruptions, worker shortages and government spending policies.

Fed Governor Christopher Waller on Friday warned that interest rates might need to increase even more than markets currently anticipate to restrain the rise in the cost of living, reflected recently in the March consumer-price index at a 5% yearly rate, down to the central bank’s 2% annual target.

The sudden rise in interest rates led to bruising losses in stock and bond portfolios in 2022. Higher rates also played a role in last month’s collapse of Silicon Valley Bank after it sold “safe,” but rate-sensitive securities at a steep loss. That sparked concerns about risks in the U.S. banking system and fears of a potential credit crunch.

“Rates are certainly higher than they were a year ago, and higher than the last decade,” said David Del Vecchio, co-head of PGIM Fixed Income’s U.S. investment grade corporate bond team. “But if you look over longer periods of time, they are not that high.”

When investors buy corporate bonds they tend to focus on what could go wrong to prevent a full return of their investment, plus interest. To that end, Del Vecchio’s team sees corporate borrowing costs staying higher for longer, inflation remaining above target, but also hopeful signs that many highly rated companies would be starting off from a strong position if a recession still unfolds in the near future.

“Profit margins have been coming down (see chart), but they are coming off peak levels,” Del Vecchio said. “So they are still very, very strong and trending lower. Probably that continues to trend lower this quarter.”

Net profit margins for the S&P 500 are coming down, but off peak levels

Refinitiv, I/B/E/S

Rolling with it, including at banks

It isn’t hard to come up with reasons why stocks could still tank in 2023, painful layoffs might emerge, or trouble with a wall of maturing commercial real estate debt could throw the economy into a tailspin.

Snider’s team at Goldman Sachs Asset Management expects the S&P 500 index SPX, -0.21%

to end the year around 4,000, or roughly flat to it’s closing level on Friday of 4,137. “I wouldn’t call it bullish,” he said. “But it isn’t nearly as bad as many investors expect.”

“Some highly levered companies that have debt maturities in the near future will struggle and may even struggle to keep the lights on,” said Austin Graff, chief investment officer at Opal Capital.

Still, the economy isn’t likely to “enter a recession with a bang,” he said. “It will likely be a slow slide into a recession as companies tighten their belts and reduce spending, which will have a ripple effect across the economy.”

However, Graff also sees the benefit of higher rates at big banks that have better managed interest rate risks in their securities holdings. “Banks can be very profitable in the current rate environment,” he said, pointing to large banks that typically offer 0.25%-1% on customer deposits, but now can lend out money at rates around 4%-5% and higher.

“The spread the banks are earning in the current interest rate market is staggering,” he said, highlighting JP Morgan Chase & Co. JPM, +7.55%

providing guidance that included an estimated $81 billion net interest income for this year, up about $7 billion from last year.

Del Vecchio at PGIM said his team is still anticipating a relatively short and shallow recession, if one unfolds at all. “You can have a situation where it’s not a synchronized recession,” he said, adding that a downturn can “roll through” different parts of the economy instead of everywhere at once.

The U.S. housing market saw a sharp slowdown in the past year as mortgage rates jumped, but lately has been flashing positive signs while “travel, lodging and leisure all are still doing well,” he said.

U.S. stocks closed lower Friday, but booked a string of weekly gains. The S&P 500 index gained 0.8% over the past five days, the Dow Jones Industrial Average DJIA, -0.42%

advanced 1.2% and the Nasdaq Composite Index COMP, -0.35%

closed up 0.3% for the week, according to FactSet.

Investors will hear from more Fed speakers next week ahead of the central bank’s next policy meeting in early May. U.S. economic data releases will include housing-related data on Monday, Tuesday and Thursday, while the Fed’s Beige Book is due Wednesday.

The U.S. economy added 236,000 jobs in March, just shy of the 238,000 forecast by economists polled by the Wall Street Journal. The unemployment rate declined to 3.5% in March from 3.6% in February.

The latest data was calculated before the collapse of Silicon Valley Bank and Signature Bank last month, an event that…

April is National Financial Literacy Month. To mark the occasion, MarketWatch will publish a series of “Financial Fitness” articles to help readers improve their fiscal health, and offer advice on how to save, invest and spend their money wisely. Read more here.

Do you know the difference between a stock and a bond, or a mutual fund and an exchange-traded fund? MarketWatch put together a meat and potatoes — although that’s always relative — quiz for our savvy readers. We’ve stuck to some familiar topics — taxes, stocks, interest rates, savings and inflation. There are 10 questions — with one bonus question thrown in for good measure.

You don’t know what you don’t know until you get an incorrect answer in a financial literacy quiz. Some of the questions are tricky, but we hope they are fun and that — most importantly — readers learn something new. Financial literacy helps us to plan for the future, gives us peace of mind and brings more understanding and less fear about the complex world of investing and retirement.

Our aim is to raise awareness of Financial Literacy Month. If you get 10/10, including the bonus question, buy yourself (and a friend) a popsicle. If you didn’t answer all the questions correctly, buy yourself a popsicle anyway. We, at MarketWatch, aim to democratize and demystify financial news, and make this sometimes intimidating subject as accessible as possible.

If you found it useful and/or entertaining, share it with a friend.

–Quentin Fottrell

Question 1: What is the difference between a tax deduction and a tax credit?

(a) A tax deduction reduces your income taxes directly. A tax credit reduces your taxable income.

(b) A tax deduction reduces your taxable income. A tax credit reduces your income taxes directly.

(c) Both reduce your income taxes directly.

Question 2: Which way do bond prices move when interest rates rise?

(a) Bond-market prices fall as interest rates rise. Bond prices rise when interest rates decline.

(b) Bond-market prices rise as interest rates rise. Bond prices fall when interest rates decline.

(c) Bond-market prices fall as interest rates rise, but bond prices also fall when interest rates decline.

Question 3: What has been the average annual total return, with dividends reinvested, for the S&P 500 over the past 30 years?

(a) 9.7%, according to FactSet.

(b) 3%, according to FactSet.

(c) 6.5%, according to FactSet.

Question 4: What is compound interest and how does it work?

(a) Compound interest reflects the linear gain that comes from all the reinvested interest of your savings and investments, which allows your initial investment/deposit to gain value regardless of the amount of interest you pay.

(b) Compound interest reflects the exponential gain that comes from all the reinvested interest of your savings and investments, which allows your initial investment/deposit and the additional interest to increase in value.

(c) Compound interest reflects the amount of interest you pay every month on a loan, and the total amount of interest you have paid over the lifetime of that loan.

Question 5: What is APR and how is it different from a regular interest rate?

(a) APR is the annual interest on a loan calculated on the initial loan, including additional costs and fees, but not on the accumulated interest incurred on the loan.

(b) APR is the annual interest on a loan calculated on the initial loan and the accumulated interest over the first year.

(c) APR is the annual interest on a loan calculated on the initial loan, including additional costs and fees, and the accumulated interest over the lifetime of the loan loan.

Question 6: What percentage of your income should you spend on rent?

(a) Most real-estate experts say you should spend no more than 20% of your income on housing costs, which is considered to be a tipping point for becoming “cost-burdened.”

(b) Most real-estate experts say you should spend no more than 50% of your income on housing costs, which is considered to be a tipping point for becoming “cost-burdened.”

(c) Most real-estate experts say you should spend no more than 30% of your income on housing costs, which is considered to be a tipping point for becoming “cost-burdened.”

Question 7: What’s an ETF?

(a) ETFs, or Exchange-Traded Funds, are baskets of investments — stocks, bonds, or commodities — that investors can buy throughout the trading day like stocks.

(b) ETFs, or Exchange-Traded Funds, are baskets of investments — stocks, bonds, or commodities — that investors can only buy at the end of the trading day.

(c) ETFs, or Exchange-Traded Funds, are baskets of investments — stocks, bonds, or commodities — that investors can only buy during or at the end of the trading day.

Question 8: What is the difference between a stock and a bond?

(a) A stock is a temporary investment in a company, while a bond is issued by a company to reward shareholders.

(b) A stock is a share in the ownership of a company, while a bond is issued by a company to finance a loan.

(c) A stock is a share in the ownership of a company, while a bond is issued by a company to finance the stock.

Question 9: If you were born in 1960 or later, at what age can you receive your full Social Security in the U.S.? Bonus question: At what age can you receive your maximum Social Security benefit?

(a) Full retirement age in the U.S. is 65 for those born in 1960 and after. While you can start collecting your Social Security retirement benefits as early as 62, your benefits are permanently reduced. Your Social Security benefits max out at age 70. By delaying until 70, your benefit is 76% higher than if you had claimed at the earliest possible age (62).

(b) Full retirement age in the U.S. is 65 for those born in 1960 and after. While you can start collecting your Social Security retirement benefits as early as 62, your benefits are permanently reduced. Your Social Security benefits max out at age 67. By delaying until 67, your benefit is 76% higher than if you had claimed at the earliest possible age (62).

(c) Full retirement age in the U.S. is 67 for those born in 1960 and after. While you can start collecting your Social Security retirement benefits as early as 62, your benefits are permanently reduced by a small percentage each month until you reach 67. Your Social Security benefits max out at age 70. By delaying until 70, your benefit is 76% higher than if you had claimed at the earliest possible age (62).

Question 10: What is the Federal Reserve’s desired rate of inflation?

(a) 2%

(b) 3%

(c) 2.5%

Bonus question! What is considered a good credit score?

(a) 560

(b) 680

(c) 800

If you get 10/10, including the bonus question, buy yourself a popsicle.

Getty Images/iStockphoto

Answer 1:

(b) A tax deduction reduces your taxable income. A tax credit reduces your income taxes directly.

Answer 2:

(a) Bond-market prices fall as interest rates rise. Bond prices rise when interest rates decline.

Answer 3:

(a) 9.7%, according to FactSet.

Answer 4:

(b) Compound interest reflects the exponential gain that comes from all the reinvested interest of your savings and investments, which allows your initial investment/deposit and the additional interest to increase in value.

Answer 5:

(c) APR is the annual interest on a loan calculated on the initial loan, including additional costs and fees, and the accumulated interest over the lifetime of the loan.

Answer 6:

(c) Most real-estate experts say you should spend no more than 30% of your income on housing, which is considered to be a tipping point for becoming “cost-burdened.”

Answer 7:

(a) ETFs are Exchange-Traded Funds. These are baskets of investments — stocks, bonds, or commodities — that investors can buy or sell throughout the trading day.

Answer 8:

(b) A stock is a share in the ownership of a company, while a bond is issued by a company to finance a loan.

Answer 9:

(c) Full retirement age in the U.S. is 67 for those born in 1960 and after. While you can start collecting your Social Security retirement benefits as early as 62, your benefits are permanently reduced. Your Social Security benefits max out at age 70. By delaying until 70, your benefit is 76% higher than if you had claimed at the earliest possible age (62).

Answer 10:

(a) 2%

Answer for bonus question!

(b) 680. Although credit scores vary depending on the model, according to Experian, credit scores between 580 and 669 are considered “fair,” scores between 670 and 739 are regarded as “good”; 740 to 799 are considered “very good”; and scores of 800 and above are considered “excellent.”

Details about the Internal Revenue Service’s spending plans for a major cash influx are about to come to light, Treasury Secretary Janet Yellen said Tuesday.

More than half a year after Congress authorized $80 billion in new funding for the tax-collection agency over the next decade, Yellen said details are coming this week on how the IRS will put the money to use in improving customer service, upgrading internal technology and making sure the richest taxpayers are paying their fair share.

The $80 billion infusion is part of the Inflation Reduction Act, which passed Congress last summer without Republican support and plenty of GOP skepticism that the additional funding would be used appropriately, depicting it instead as engendering a sort of tax-collection police state in which middle-income individuals could find themselves targeted by armed IRS agents.

Yellen spoke Tuesday at the swearing-in ceremony for Danny Werfel, the newly confirmed IRS commissioner. Werfel “will lead the IRS through an important transition” after a period during which the agency “suffered from chronic underinvestment,” Yellen said in prepared remarks.

During Werfel’s confirmation hearing in February, senators from both parties pressed him about how he would oversee the new money’s use.

The U. S. House of Representatives is under Republican control, and observers expect lawmakers to give hard looks at the funding of the IRS. The House, in fact, voted in January to repeal the $80 billion. The measure isn’t expected to go further, with Democrats retaining control in the Senate and President Joe Biden, a Democrat, in the White House.

Some of the money will go toward modernizing the taxation experience. Within the first five years of the decade-long plan, taxpayers should be able to file all of their tax documents and respond to all IRS notices online, according to a Treasury official.

There are a handful of IRS notices for which taxpayers currently have that capacity. By the end of fiscal 2024, another 72 notices, which include Spanish-language notices, will add online capacity, the official said.

By the end of fiscal 2025, taxpayers, along with accountants and other professional tax preparers, should be able to peruse their accounts and view and download information, including payments and notices, the official said.

The IRS has already been hiring more staff, including 5,000 customer-service representatives to improve phone service, which has fallen off during the pandemic.

Tax Day is weeks away, on April 18. As of late March, income-tax refunds are 11% lower than they were last year. They are averaging $2,903 versus $3,263 at the same point last year. It’s an outcome many tax-code watchers predicted after pandemic-era boosts to certain tax credits went away.

The same day Yellen spoke, a new watchdog report said the IRS still has plenty of work to do processing the backlog of tax returns that built up during the pandemic.

During last year’s tax-filing season, the IRS hired 9,000 employees and shifted more than 2,400 workers from other areas to cut the backlog, according to Treasury’s inspector general for tax administration.

By last July the IRS had transcribed all tax-year 2020 paper returns but still had 9.5 million unprocessed 2021 paper returns. “The inability to timely process tax returns and address tax account work continues to have a significant impact on the associated taxpayers,” the report said.

At this point, the IRS says it has processed all paper and electronically filed returns that it received before this January. The agency said it still has 2.17 million unprocessed tax returns from the 2022 tax year and 2021 returns that needed fixes and corrections.

Surprise crude oil production cuts from Saudi Arabia and other oil-rich countries shouldn’t produce worries of skyrocketing gas costs for U.S. drivers still smarting from last year’s pump price shocks, according to fuel industry experts.

At a time when gas prices are already increasing because of rising seasonal demand, the slashed crude oil output that Saudi Arabia announced Sunday will translate into higher prices, they say. But compared to last year — when energy markets were absorbing the initial impact of Russia’s invasion of Ukraine — the altitude on those gas price increases may not feel so steep.

On Monday, the national average for a gallon of gas was $3.50, according to AAA. That’s around 10 cents more than a month ago, but almost 70 cents less than the $4.19 average cost one year ago.

The effects of decreased oil production could translate into initial price increases of up to 15 cents per gallon, according to two different energy sector watchers.

There’s Patrick De Haan, head of petroleum analysis at GasBuddy.

At OPIS, an outlet focused on energy sector news and analytics, Chief Oil Analyst Denton Cinquegrana said he was previously expecting summer gas prices to average around $3.60.

“This move probably boosts that by about 10 – 15 cents to about $3.70-3.75/gal.” Cinquegrana told MarketWatch.

OPIS is owned by Dow Jones, which also owns MarketWatch.

It’s possible for gas price averages to hit around $3.60 in the next week or so, he said. The other 10 to 15 cents might filter into retail pump prices later this month or in early May, according to Cinquegrana.

The surprise move came from Saudi Arabia and other members of OPEC+, the Organization of the Petroleum Exporting Countries and allies, including Russia. In Saudi Arabia, officials were reportedly “irritated” by recent remarks from U.S. Energy Secretary Jennifer Granholm.

After the Biden administration tapped the country’s strategic petroleum reserve to combat last year’s high gas costs, Granholm said it will difficult to restock the reserve.

By May, more than 1 million barrels of oil a day will be slashed from output in the global energy markets. That’s in addition to OPEC+ production cuts announced last fall.

In cost breakdowns for a gallon of gas, the price of crude oil is responsible for more than half the price tag, according to the U.S. Energy Information Administration.

In Monday morning trading, the price of West Texas Intermediate crude for May delivery jumped 6% to just over $80 on the New York Mercantile Exchange.

For context, when gas prices were breaking records last year, the costs of West Texas Intermediate crude were in the triple digits. While retail prices surged in early March 2022, West Texas Intermediate crude briefly traded for more than $130 during the trading day on March 7, 2022.

The national average for a gallon of gas hit a record $5.01 in mid-June, according to AAA. In the current context, Cinquegrana doesn’t see a return to $5 gas averages, he said. Gas prices vary across the nation. California drivers are paying $4.80 on average while Mississippi drivers are paying $3.02 per gallon.

Even if price increases are not as sharp as last year, hot inflation is retreating slowly. So any extra costs are unwelcome to millions of American drivers who are living their lives and more frequently commuting to the office.

Like last year, oil prices are poised to increase, said AAA spokesman Devin Gladden.

But the economy’s background noise right now could dampen the impact as downturn worries keep sticking around, he added. Furthermore, there can be discrepancies in the announced production reductions and the amounts that are actually reduced, Gladden said.

“If recessionary concerns persist in the market, oil price increases may be limited due to the market believing lower oil demand will lead to lower prices this year,” he said.

On Monday, energy sector stocks and related exchange traded funds were climbing after the production cut news. In early afternoon trading, the Dow Jones Industrial Average DJIA, +0.81%

was up more than 200 points, or 0.7%, while the S&P 500 SPX, -0.03%

is little changed and the Nasdaq Composite COMP, -0.98%

dropped 100 points, or 0.8%.

The collapse of Silicon Valley Bank sent shockwaves through the global economy and had the makings of another crisis. Depositors raced to withdraw money. Banks worried about the risk of contagion. I spent that weekend on the phone with small business owners in Ohio who didn’t know whether they’d be able to make payroll the next week. One woman was in tears, worried about whether she’d be able to pay her workers.

The Federal Deposit Insurance Corporation (FDIC) and the Federal Reserve responded quickly, took control of the bank, and contained the fallout. Consumers’ and small businesses’ money was safe. That Ohio small business was able to get paychecks out.

The regulators were able to protect Americans’ money from incompetent bank executives because when Congress created the Federal Reserve in 1913 and the FDIC in 1933, it ensured that their funding structures would remain independent from politicians in Congress and free from political whims.

But now, as the U.S. Supreme Court considers the case of Community Financial Services Association v. CFPB, these independent watchdogs’ ability to keep our financial system stable faces an existential threat.

The Consumer Financial Protection Bureau is the only agency solely dedicated to protecting the paychecks and savings of ordinary Americans, not Wall Street executives or venture capitalists. Corporate interests have armies of lobbyists fighting for every tax break, every exemption, every opportunity to be let off the hook for scamming customers and preying on families.

“ The CFPB’s funding structure is designed to be independent, just like the Fed and the FDIC. ”

Ordinary Americans don’t have those lobbyists. They don’t have that kind of power. The CFPB is supposed to be their voice — to fight for them. The CFPB’s funding structure is designed to be independent, just like the Fed and the FDIC. Otherwise, its ability to do the job would be subject to political whims and special interests — interests that we know are far too often at odds with what’s best for consumers.

Since its creation, the CFPB has returned $16 billion to more than 192 million consumers. It’s held Wall Street and big banks accountable for breaking the law and wronging their customers. It’s given working families more power to fight back when banks and shady lenders scam them out of their hard-earned money.

The CFPB can do this good work because it’s funded independently and protected from partisan attacks, just as the Fed and the FDIC are. So why, then, does Wall Street claim that only the CFPB’s funding structure is unconstitutional?

Make no mistake — the only reason that Wall Street, its Republican allies in Congress, and overreaching courts have singled out the CFPB is because the agency doesn’t do their bidding. The CFPB doesn’t help Wall Street executives when they fail. It doesn’t extend them credit in favorable terms or offer them deposit insurance like the other regulators do. The CFPB’s funding structure isn’t unconstitutional — it just doesn’t work in Wall Street’s favor.

If the Supreme Court rules against the CFPB, the $16 billion returned to consumers could be clawed back. What would happen then — will America’s banks really go back to the customers they’ve wronged with a collection tin?

“ Invalidating the CFPB and its work would also put the U.S. economy — and especially the housing market — at risk. ”

Invalidating the CFPB and its work would also put the U.S. economy — and especially the housing market — at risk. For more than a decade, the CFPB has set rules of the road for mortgages and credit cards and so much else, and given tools to help industry follow them. If these rules and the regulator that interprets them disappear, markets will come to a standstill.

By attacking the CFPB’s funding structure and putting consumers’ money at risk, Wall Street is putting the other financial regulators in danger, too.

The Fifth Circuit’s faulty ruling against the CFPB is astounding in its absurdity — the court ruled that the authorities that other financial agencies, like the Federal Reserve and the FDIC, have over the economy do not compare to the CFPB’s authorities. In other words, the court is claiming that the CFPB supposedly has more power in the economy than the Fed.

That’s ridiculous. Look at the extraordinary steps taken to contain the failures of Silicon Valley Bank and Signature Bank — the idea that the CFPB could take action even close to as sweeping is laughable.

But we know why the Fifth Circuit put that absurd assertion in there — they recognize the damage this case could do to these other vital agencies, and to our whole economy.

“ Imagine what might happen if another series of banks failed and the FDIC did not have the funds to stop the crisis from spreading.”

The FDIC’s own Inspector General has stated that the Fifth Circuit ruling could be applied to their agency. If that happens, the FDIC and other regulators could be subject to congressional budget deliberations, which we all know are far too partisan and have resulted in shutdowns. Imagine what might happen if another series of banks failed and the FDIC did not have the funds to stop the crisis from spreading, or the Deposit Insurance Fund to protect depositors’ money. Imagine if politicians caused a shutdown, and we were without a Federal Reserve.

U.S. financial regulators are independently funded so that they can respond quickly when crises happen. It’s telling, though, that plenty of people in Washington don’t seem to consider the CFPB’s issues in the same category. Washington and Wall Street expect the government to spring into action when businesses’ money is put at risk. But when workers are scammed out of their paychecks, that’s not an emergency — it’s business as usual.

When Wall Street’s abusive practices put consumers in crisis, the CFPB must have the funding and strength it needs to carry out its mission — to protect consumers’ hard-earned money.

U.S. Sen. Sherrod Brown (D-OH) is chairman of the U.S. Senate Committee on Banking, Housing, and Urban Affairs.

Regional banks shouldn’t be the only source of worry for potential fallout from the Federal Reserve’s rapid pace of interest-rate hikes in the past year, said a former top banking regulator.

“I don’t see regional banks as having any particular problem,” said Sheila Bair, who ran the Federal Deposit Insurance Corp. from 2006 to 2011, in an interview with MarketWatch on Thursday. “We need to be mindful of all unmarked securities at banks — small, medium and large.”

Bair called the hyperfocus on regional banks and interest-rate risks “counter productive” in the wake of the collapse earlier in March of Silicon Valley Bank and Signature Bank SBNY, -22.87%

of New York.

“This is a risk confronting all banks,” she said. “All examiners need to be on alert for how interest-rate risk is being managed. If there is a run, they will need to sell these securities. Those are the kinds of things all-size banks, and all examiners should be worried about.”

The FDIC estimated that U.S. banks had some $620 billion of unrealized losses from securities on their books as of the end of 2022, including longer-duration Treasurys and mortgage securities that have become worth less than their face value.

“Unrealized losses on securities have meaningfully reduced the reported equity capital of the banking industry,” FDIC Chairman Martin Gruenberg said on March 6, in a speech at the Institute of International Bankers.

Days after that gathering, Silicon Valley Bank and Signature Bank both collapsed, prompting regulators to roll out a new emergency bank funding program to help head off any liquidity strains at other U.S. lenders. Regulators also backstopped all deposits at the two failed lenders.

Treasury Secretary Janet Yellen said Wednesday that blanket deposit insurance protection isn’t something her department is considering, but added that the appropriate level of protection could be debated in the future.

Bair has been calling for a pause on Fed rate hikes since December. She said that instead of raising rates by another 25 basis points on Wednesday, Fed Chair Powell should have hit pause and said the central bank needs time to assess.

“If we have a financial crisis, we won’t have a soft landing,” Bair said. “We have to avoid that at all costs.”

Stocks closed modestly higher Thursday in choppy trade, with the Dow Jones Industrial Average DJIA, +0.23%

up 0.2% and S&P 500 index SPX, +0.30%

advancing 0.3%, while the Nasdaq Composite Index COMP, +1.01%

gained 1%.

U.S. stocks closed sharply lower on Wednesday, giving up earlier gains, after the Federal Reserve raises interest rates by 25 basis points as expected, but talked down the possibility of cuts to rates this year. The Dow Jones Industrial Average DJIA, -1.63%

tumbled 531 points, or 1.6%, ending near 32,028, while the S&P 500 index SPX, -1.65%

shed 1.7% and the Nasdaq Composite Index COMP, -1.60%

closed down 1.6%, according to preliminary FactSet figures. Fed Chairman Jerome Powell said the U.S. banking system remained resilient after it and regulators rolled out liquidity measures to help shore up confidence in the banking system after the collapse of Silicon Valley Bank and Signature Bank earlier in March. Powell also said that tighter credit conditions for consumers, following the bank failures, would likely work like rate hikes in terms of lowering inflation. It will be a key area of focus for the Fed in the coming weeks and months, he said. The 10-year Treasury rate TMUBMUSD10Y, 3.444%

fell Wednesday to 3.46%, a sign that investors in the bond market think growth will be slower.

U.S. stocks turned higher, shaking off earlier weakness, after the Federal Reserve on Wednesday raised its policy rate as expected by 25 basis points to help fight inflation. The increase in interest rates comes despite recent weakness in the banking system after the collapse earlier in March of Silicon Valley Bank. The S&P 500 index SPX, -0.55%

was up 14 points, or 0.4%, to about 4,016, at last check, while the Dow Jones Industrial Average DJIA, -0.68%

was up 0.2% near 32,609 and the Nasdaq Composite Index was 0.7% higher. The Fed also said the U.S. banking system remains resilient, in its policy statement. The 10-year Treasury rate TMUBMUSD10Y, 3.507%

was lower at 3.52%.

The S&P 500 on Tuesday posted its highest close since the collapse of Silicon Valley Bank earlier this month, which sent shockwaves through financial markets and raised concerns about the stability of the U.S. banking system. The S&P 500 index SPX, +1.30%

closed up about 51 points, or 1.3%, ending near 4,003, according to preliminary data from FactSet. That was its highest close since May 6, four days before the failure of Silicon Valley, the biggest bank collapse since the 2008 global financial crisis. The Dow Jones Industrial Average DJIA, +0.98%

rose 1% Tuesday, while the Nasdaq Composite Index COMP, +1.58%

swept to a 1.6% gain. Banks and companies with heavy exposure to rate-sensitive assets, including property loans, have been under pressure since Silicon Valley Bank’s implosion. It drew attention to some $600 billion in paper losses at banks from their holdings of “safe” but low-coupon securities that have fallen in value in the year since the Federal Reserve began rapidly increasing interest rates to combat high inflation. Those older bonds end up worth less when investors have access to new securities with higher yields, with a similar low-risk profile in terms of credit risks. The failure of several regional banks in March, plus the sale of Credit Suisse CS, +2.46%

to rival bank UBS UBS, +11.97%

over the weekend, has reawakened fears of potentially broader problems in the banking system as central bank have increased rates and ended an era of easy money. Even so, stocks were rallying as the Federal Reserve at the conclusion of its 2-day policy meeting on Wednesday is expected to raise its policy rate by another 25 basis points.

Heavy trading in SVB Financial Group’s SIVB,

debt pulled its BBB-rated 10-year bonds as low as 31 cents on the dollar on Friday after subsidiary Silicon Valley Bank was closed by regulators, marking the biggest bank failure since the financial crisis.

The Santa Clara, Calif.–based financial-services company has been reeling in recent days, with both its stock and bond prices hit hard, after it on Thursday disclosed a $1.8 billion loss from a sale of about $21 billion in securities.

Its bond prices lost further ground Friday after the California Department of Financial Protection and Innovation closed Silicon Valley Bank, placing the Federal Deposit Insurance Corp. in control of its assets.

Silicon Valley Bank had an estimated $209 billion in total assets and about $175.4 billion in deposits as of Dec. 31, according to the FDIC.

SVB Financial’s 4.57% bonds due April 2023 traded as low as 31 cents on the dollar on Friday in heavy trading, according to BondCliq. Since the low, the debt traded up to 38.50 cents. A week ago it was fetching 90 cents. Prices on U.S. corporate bonds below 70 cents on the dollar are broadly considered distressed.

Worries about distress at Silicon Valley Bank, and potential risks in the broader distress in the banking system, have weighed on shares and the debt of financial companies.

Bonds in the financial sector were broadly under pressure Friday, including debt issued by Bank of America Corp. BAC, -0.97%,

JPMorgan Chase and Co. JPM, +2.70%,

Goldman Sachs Group Inc. GS, -3.69%,

Morgan Stanley MS, -1.56%

and other major banks, according to BondCliq.

Shares of the Invesco KBW Bank ETF KBWB, -3.26%

were down 16% on the week through midday Friday, with some investors expressing concern about potential cracks in the financial system following a year of aggressive interest-rate hikes by the Federal Reserve.

Barclays analysts said Friday that they viewed the collapse of Silicon Valley Bank as an “isolated event, but that it still “raises risks of broader distress within the banking system” that could throw cold water on talk of a Fed interest-rate hike in March of 50 basis points vs. 25 basis points.

“Indeed, the possibility of capital losses at other institutions cannot be completely dismissed, with rising policy rates raising banks’ funding costs, more elevated longer-term rates exerting pressure on asset valuations, and potential loan losses related to idiosyncratic credit exposures.”

Shares of SBV Financial were halted Friday, but they are down about 54% on the year, according to FactSet. The S&P 500 index SPX, -1.11%

was down about 1.2% Friday afternoon, while the Dow Jones Industrial Average DJIA, -0.82%

fell 0.8% and the Nasdaq Composite COMP, -1.47%

was 1.7% lower.

There’s a very real possibility the government will stop issuing Social Security payments after the debt limit is hit.

Scary as that prospect is, however, the alternative might be even worse: A little-known provision of a 1996 law could be interpreted to allow the Social Security trust fund to be used not only to pay Social Security’s monthly checks but also to circumvent the debt limit and pay all the government’s otherwise overdue bills.

If that happens, any short-term relief to Social Security recipients would come with a potentially huge long-term price tag: The Social Security trust fund could be exhausted much sooner than currently projected—in just a couple of years, in fact.

These dire possibilities emerge from an analysis conducted by Steve Robinson, the chief economist for The Concord Coalition, a group that describes itself as “a nonpartisan organization dedicated to educating the public and finding common sense solutions to our nation’s fiscal policy challenges.”

An issue brief he wrote, entitled “Social Security’s Debt Limit Escape Clause,” is available on the group’s website.

Let me hasten to add that Robinson is not advocating that the Social Security trust fund be used in this way. In an interview, he instead stressed that he wrote his issue brief because we need to be aware not only that this “escape clause” exists but that its use could have unintended consequences. Though hardly anyone outside Washington knows that it even exists, and relatively few on Capitol Hill, the Treasury Department and the Social Security Administration are very much aware of it.

Before reviewing the details of this escape clause, it’s worth focusing on the political dynamics that surround it. Because the escape clause lessens the pressure on Congress and the president to come up with a solution to the debt crisis, neither side has an incentive to publicize its existence. But if the government is otherwise pushed to the edge of the fiscal cliff, and it’s facing the potentially huge consequences of an outright default (including the nonpayment of monthly Social Security checks), the political pressure to use the escape clause could be intense.

The 1996 law that creates the escape clause was passed in the wake of the government hitting its debt limit in 1995 and 1996. Ironically, the intent of that law was to prevent the Social Security trust fund from being used for anything other than paying Social Security benefits. But, Robinson explains, that’s unworkable in the real world. That’s because Social Security checks are sent out by the Treasury’s general account, and if that account is in default the checks would bounce.

If and when the debt limit is hit, therefore, the only way—in practice—for Social Security checks to continue being issued and cleared through the banking system would be for the Social Security trust fund to “lend” the Treasury sufficient funds that it could pay all the government’s unmet obligations. (I put “lend” in quotes because that’s not exactly how it works; the key is that the “loan” can be structured in ways that don’t count against the debt limit. If you’re interested in reading more about the complex logistics involved, you should read Robinson’s issue brief.)

Therefore, if the debt limit is hit, which it is projected to do perhaps as early as June, Congress and the president will be on the horns of a huge dilemma:

Do they allow Social Security checks to continue getting paid, risking the political fallout of being accused of “raiding” the Social Security trust fund?

Or do they stop issuing Social Security payments, risking the political fallout of not issuing Social Security payments, on whom the very livelihoods of many elderly currently depend?

You can appreciate why Congress and the president don’t want us to know that this escape clause exists. Once we are aware of it, they are put in a no-win situation.

So fasten your seat belts for a wild ride in coming months as both parties play political brinkmanship over the debt limit and, by extension, Social Security. With both sides by the day hardening their stances, there’s a very real possibility that the debt limit will be hit.

If that happens, we’ll be hearing a lot more about the little-known provision of a nearly 30-year-old law.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com.

What advice would you give to a widow and widower considering marriage on how to manage finances — and deal with adult children?

We are both 60 years old and plan to work a few more years, mostly for health insurance. We both have about $1.5 million in retirement savings accounts. Our spouses’ 401(k)s and IRAs rolled into our accounts.

I have another $500,000 in a brokerage and he has almost another $1 million. We both own homes with $300,000 mortgages. Mine is worth $500,000, Paul’s (not his real name) home is worth $1 million. We have no other debt.

We both have one married, and one unmarried child that we help. We both have two grandchildren.

We should be set up very well. Here’s the concern: His married, well-off daughter is very aggressive about inheritance. She wants the family home retitled in a trust. She wants all life insurance and brokerage beneficiaries in her name. Her brother has had drug-addiction problems, so she’s cutting him out even though it seems he’s the one who will need help.

“‘She wants the family home retitled in a trust. She wants all life insurance and brokerage beneficiaries in her name.’”

The daughter isn’t thrilled about our relationship and suggests we just live together. For religious reasons, I would never do this. Grandma shacking up? What example would I set for my grandchildren?

As a widowed couple, we are realistic enough to plan for the time one of us is left alone. Paul has diabetes, high blood pressure and already sees a cardiologist. What if he has a heart attack? Stroke? Or if he dies?

What’s a fair way to mingle finances and allow security for me should he predecease me while allowing Paul’s daughter to ultimately inherit?

By the way, my children have never raised money as an issue. After we both cared for spouses through cancer, they know life is short and just want us to be happy.

Happy to Have Found Love Again

Dear Happy,

She is overstepping the line, and overplaying her hand.

The first rule of inheritance is that it’s not yours until the decedent’s money is sitting in your bank account. Your fiancé’s daughter can make all the demands she likes, but the only thing your fiancé has to do is say, “You don’t need to be concerned. My affairs are all in order. I’ve always taken care of my own affairs, and I am not changing now.”

How your fiancé decides to split his estate is entirely up to him, and can be done in consultation with a financial adviser and attorney, taking into account each of his children’s individual needs. For instance, if you move in together, he could give you a life estate, allowing you to live in the home for the rest of your life, and dividing the property between his two children thereafter.

Given that you have your own home, however, you may decide to rent it out, and move back there in the event that he predeceases you. There are so many ways to split an inheritance. You could look at the intestate laws of your state, and follow them. In New York, the spouse inherits the first $50,000 of intestate property, plus half of the balance, and the kids inherit the rest.

“Paul” may decide to set up a trust for his son, so he can provide an income for him over the course of his life. If he has or had issues with addiction, this will help him while not putting temptation in his way with a lump sum of money. The best kind of trust is the one that deals with any recurring issues directly, and takes into account the person’s circumstances.

Martin Hagan, a Pennsylvania-based estate-planning attorney who has practiced for four decades, writes: “First, it would authorize distributions only if the beneficiary is actively pursuing treatment and recovery. Second, it would limit distributions to paying only for the expenses incurred in carrying out the treatment plan that will have been developed for the beneficiary.”

You have $2 million collectively in a retirement and brokerage account and $200,000 equity in his home, and you can use these next seven years or so to pay off your mortgage, while your fiancé has $2.5 million and $700,000 in equity on his home. You are both well set up for retirement, and let’s hope you have many years to spend together.

The financial services industry has many opinions. You should, advisers say, have 10 times your salary saved by the time you’re 65 years old. You don’t mention your salary, but I would be surprised if many people in America had that much money saved, especially given all of the unexpected events — divorce, illness, job loss — that can occur in the intervening years.

You also have other priorities than dealing with an aggressive daughter/daughter-in-law. AARP suggests that most people should look into long-term care insurance between the ages of 60 and 65, around the time most people are eligible to qualify for Medicare. If you do it earlier, it can serve as a savings account in the event that you never need long-term care, AARP says.

As retirement columnist Richard Quinn recently wrote on MarketWatch, everybody’s circumstances are different. “Living in retirement isn’t about averages. It isn’t about what other people do or the opinions of experts, especially online instant experts who don’t know anything about you and have yet to experience many years of retirement themselves.”

Don’t give too much oxygen or power to your future daughter-in-law. Her father should give her a stock answer, and be firm. If she persists, he can say, “The subject is closed. I need you to respect the decisions I make about my own life, respect my privacy on these matters, and it would be nice if you would be happy for us, and support us in our marriage together.”

You can’t change people. But you can change wills.

You can email The Moneyist with any financial and ethical questions related to coronavirus at qfottrell@marketwatch.com, and follow Quentin Fottrell on Twitter.

Check out the Moneyist private Facebookgroup, where we look for answers to life’s thorniest money issues. Readers write in to me with all sorts of dilemmas. Post your questions, tell me what you want to know more about, or weigh in on the latest Moneyist columns.

The Moneyist regrets he cannot reply to questions individually.

We want to hear from readers who have stories to share about the effects of increasing costs and a changing economy. If you’d like to share your experience, write to readerstories@marketwatch.com. Please include your name and the best way to reach you. A reporter may be in touch.

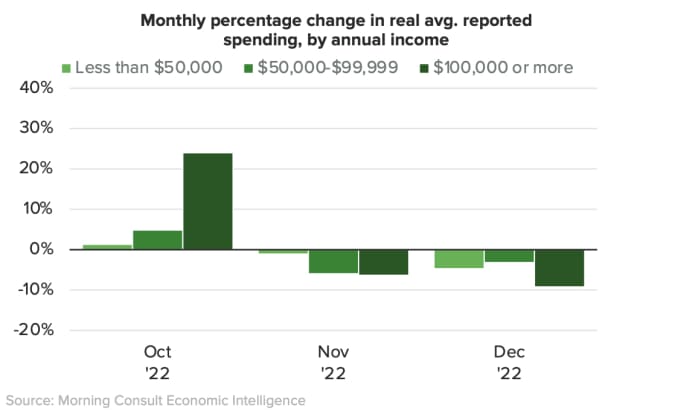

Higher-earning households are feeling the inflationary pinch.

Consumer spending slowed and household finances weakened across all income levels last month. But households earning $100,000 a year or more reported shaving more off their spending than less well-off households did, according to a report released this week by Morning Consult, a decision intelligence company.

The report also found that real monthly spending among U.S. adults fell by 4.3% from November to December.Even so, 21.3% of U.S. adults said their monthly expenses exceeded their monthly income in December, up from 19.2% in November.

On average, households earning $100,000 a year or more said they spent about 10% less in real terms in December than they did the previous month. Households earning $50,000 to $99,999 and those earning less than $50,000 a year, meanwhile, reported that they cut their monthly spending bills by no more than 5% on average.

Across the board, households are cutting back on recreation, alcohol, vehicle insurance, and other services in December, while spending more on hotels, gas and airfares, the report found.

One theory on the spending cutbacks: Higher earners typically have more discretionary income, and likely have decided to exercise more fiscal caution after seven interest-rate hikes by the Federal Reserve last year. (On Wednesday, St. Louis Fed President James Bullard told The Wall Street Journal in a live-streamed interview that the Federal Reserve should not “stall” on raising its benchmark rates until they are above 5%.)

The Morning Consult report did cite inflationary pressures. “Heightened budgetary pressures brought on by persistently high inflation are forcing trade-offs for consumers, leading to reallocation across categories,” it said. “For instance, as food grew more expensive over the past year, U.S. households accommodated an increase in grocery purchases by spending less at restaurants.”

Earlier last year, higher-income households led consumer spending in the face of rising prices, said Kayla Bruun, an economic analyst with Morning Consult and co-author of the report. But household income, even for those earning six-figure incomes, has not been growing fast enough to keep up with inflation, she said.

“They probably started to realize, ‘Hey, I can’t keep buying the same basket of goods each month and expect to continue adding to my savings,’” Bruun told MarketWatch.

At the same time, recent layoffs in the higher-earning tech and financial sectors may also have affected sentiment among wealthier households, Bruun said.

The tech and financial sectors felt the impact of rising interest rates and economic headwinds, she added. Goldman Sachs GS, -0.25%

and BlackRock BLK, -1.53%

said earlier this month they were cutting jobs. Microsoft Corp. MSFT, -2.14%

confirmed plans on Wednesday to lay off some 10,000 workers, equivalent to around 5% of the company’s global workforce.

Before Microsoft’s announcement, data compiled by the Layoffs.fyi website estimated that more than 25,000 global tech-sector employees have been laid off in the first few weeks of 2023. Last year, approximately 60,000 people in the tech industry were laid off, according to Challenger, Gray & Christmas.

Still, there has been some good news: Inflation eased in December for the sixth consecutive month: The annual rate of inflation fell to 6.5% from 7.1% in November after reaching a four-decade-high of 9.1% last summer.