[ad_1]

Housing market has hit ‘rock bottom,’ says Redfin CEO

[ad_2]

[ad_1]

U.S. stocks closed sharply lower Tuesday as investors monitored signs of China’s darkening economic backdrop and gauged if a robust U.S. consumer could spell more Federal Reserve rate hikes. The Dow Jones Industrial Average DJIA fell about 360 points, or 1%, to about 34,946, according to preliminary FactSet data. The S&P 500 index SPX dropped 1.2% to about 4,437, its lowest close since mid-July, according to FactSet. The Nasdaq Composite Index COMP ended 1.1% lower. Chinese retail sales and industrial production in the world’s second biggest economy grew less than expected in July. Its growing property woes also contributed…

[ad_2]

[ad_1]

The numbers: Builder confidence waned in August as the 30-year mortgage rate surged, dampening U.S. home-buying interest.

Despite a persistent shortage of homes on the market for resale, builders have lost confidence in the late summer amid declining customer traffic from higher mortgage rates, as well as challenges in the construction process.

Mortgage…

[ad_2]

[ad_1]

U.S. stocks closed higher on Monday, with the Dow flipping positive near the closing bell, as technology stocks bounced back. The Dow Jones Industrial Average DJIA rose about 26 points, or 0.1%, ending near 35,308, according to preliminary FactSet data. The S&P 500 index SPX scored a 0.6% gain and the Nasdaq Composite Index COMP closed up 1.1%, booking its best daily percentage climb since July 28, according to FactSet data. The S&P 500’s information technology sector outperformed with a 1.9% gain, while the communication services segment rose 1%. The rally saw shares of Meta Platforms META, Apple Inc. AAPL, Alphabet…

[ad_2]

[ad_1]

Barry DiRaimondo, chief of SteelWave, a West Coast property developer that in the past half-century has partnering with many of the biggest names in commercial real estate, is looking for diamonds in the rough, distressed office properties located in the American city that many have given up on.

Others may be shunning San Francisco while it’s down on its luck, but DiRaimondo sees better days ahead, despite the city’s threat of a growing deficit, its fentanyl crisis, homelessness and a reluctant return of office workers to its financial core.

“Not much is coming up right now,” DiRaimondo said of buying opportunities, while speaking from his office in the heart of San Francisco’s financial district. But he was eager to point out several nearby buildings that could be candidates to buy, at the right price.

“I think over the next 12 to 18 months, you’re going to see a tsunami,” of distressed office properties, DiRaimondo said.

Like in many big cities, a wave of office buildings bought at peak prices before the pandemic now have a pile of debt coming due, at much higher rates. But San Francisco’s financial core only recently has begun to show flickers of hope in its weak recovery post-COVID.

“Whether it’s San Francisco, Oakland or anywhere here, and your debt is rolling, you’re having a conversation with your lender,” DiRaimondo said. “There’s either a restructuring going on or a foreclosure going on.”

A number of high-profile property owners this year surrendered local properties to lenders, including Westfield’s namesake shopping center downtown and a string of well-known hotels, a blow to the city’s comeback efforts.

Still, DiRaimondo expects the bulk of property ownership transfers in this boom-and-bust cycle to take place quietly, behind the scenes, often through a building’s debt changing hands. It’s a familiar playbook for veteran real-estate developers like SteelWave and its partners, especially when San Francisco office property values tumble and new loans remains expensive and hard to come by.

“Office is a nasty word, right now. Especially tech office,” he said. “We are doing something that’s a bit different.”

San Francisco’s history as a boom-and-bust town perhaps is best suited for real-estate developers able to take a bunch of lemons and make lemonade.

That has been SteelWave’s signature move in the notoriously rough-and-tumble commercial real-estate industry, through its ups and downs. It has bought over $17.5 billion in properties and developments in the past five decades, first under the Legacy Partners Commercial brand before it was renamed in 2015.

It has partnered with some of the biggest names in commercial real estate, including with Angelo Gordon & Co. in 2021 on two Silicon Valley office buildings, but also distressed debt titans that include Rialto Capital, and with Chenco, one of the largest Chinese-owned U.S. real-estate investment firms.

Its stronghold is the Bay Area and DiRaimondo is now looking to raise a $500 million fund to buy distressed buildings, including in downtown San Francisco, a place major Wall Street lenders have been backing away from for months.

“It’s hard to raise equity to buy this stuff right now,” he said, but argues his strategy, which includes expanding its reach to potential investors in the U.A.E., Israel and parts of Europe, will pan out.

SteelWave’s model of buying a property includes a final tally of costs often three to four times the initial purchase price, due to extensive overhauls.

“Typically, what we do is buy something, tear it apart, put it back together, lease it, sell it,” DiRaimondo said.

It’s niche in the distressed world that’s already produced overhauls of buildings from Seattle to Colorado to Los Angeles, places the tech industry wants to lease.

In the southern California town of Costa Mesa, that meant partnering with Invesco to turn an old newsroom and printing press for the Los Angeles Times into a creative work campus. An opinion piece in 2022 from the newspaper described the revamp as turning, “the glum newspaper architecture into something inviting.”

“In New York, people rushed back and refilled the apartments, streets, and subways. Restaurants and stores flooded with customers again,” a team from Moody’s analytics wrote in a recent “tale of two cities” report. “San Francisco, on the other end, battled safety concerns, homelessness, and population exodus which existed before but only became more obvious with barren neighborhoods.”

SteelWave thinks the old days of landlords raking in top-dollar commercial rents in San Francisco, while adding little back to office buildings, are a thing of the past.

“You have to have owners who want to create cool work environments to attract people back into the city,” DiRaimondo said of downtown San Francisco’s long slog back from the brink.

That means buying properties at low prices, but also risking putting money down for major improvements. He isn’t a distressed investors looking to become a “rent bandit,” he says, because the strategy will fail to get quality tenants.

Like the Moody’s team, DiRaimondo thinks San Francisco eventually will bounce back, but he thinks not before reality hits older office properties.

Take a “commodity” building downtown, often older and midblock with generic features, that previously might have been worth $750 to $800 a square foot. It now looks worth less than $300 a square foot, he said.

The early stages of fire-sales have begun already, with the 22-story tower at 350 California, nearby to DiRaimondo’s office, reportedly fetching $200 to $225 a square foot.

“San Francisco is not dead,” DiRaimondo said. “I think there are opportunities in San Francisco.”

See: San Francisco’s office market erases all gains since 2017 as prices sag nationally

[ad_2]

[ad_1]

Barry DiRaimondo, chief of SteelWave, a West Coast property developer that in the past half-century has partnering with many of the biggest names in commercial real estate, is looking for diamonds in the rough, distressed office properties located in the American city that many have given up on.

Others may be shunning San Francisco while it’s down on its luck, but DiRaimondo sees better days ahead, despite the city’s threat of a growing deficit, its fentanyl crisis, homelessness and a reluctant return of office workers to its financial core.

“Not much is coming up right now,” DiRaimondo said of buying opportunities, while speaking from his office in the heart of San Francisco’s financial district. But he was eager to point out several nearby buildings that could be candidates to buy, at the right price.

“I think over the next 12 to 18 months, you’re going to see a tsunami,” of distressed office properties, DiRaimondo said.

Like in many big cities, a wave of office buildings bought at peak prices before the pandemic now have a pile of debt coming due, at much higher rates. But San Francisco’s financial core only recently has begun to show flickers of hope in its weak recovery post-COVID.

“Whether it’s San Francisco, Oakland or anywhere here, and your debt is rolling, you’re having a conversation with your lender,” DiRaimondo said. “There’s either a restructuring going on or a foreclosure going on.”

A number of high-profile property owners this year surrendered local properties to lenders, including Westfield’s namesake shopping center downtown and a string of well-known hotels, a blow to the city’s comeback efforts.

Still, DiRaimondo expects the bulk of property ownership transfers in this boom-and-bust cycle to take place quietly, behind the scenes, often through a building’s debt changing hands. It’s a familiar playbook for veteran real-estate developers like SteelWave and its partners, especially when San Francisco office property values tumble and new loans remains expensive and hard to come by.

“Office is a nasty word, right now. Especially tech office,” he said. “We are doing something that’s a bit different.”

San Francisco’s history as a boom-and-bust town perhaps is best suited for real-estate developers able to take a bunch of lemons and make lemonade.

That has been SteelWave’s signature move in the notoriously rough-and-tumble commercial real-estate industry, through its ups and downs. It has bought over $17.5 billion in properties and developments in the past five decades, first under the Legacy Partners Commercial brand before it was renamed in 2015.

It has partnered with some of the biggest names in commercial real estate, including with Angelo Gordon & Co. in 2021 on two Silicon Valley office buildings, but also distressed debt titans that include Rialto Capital, and with Chenco, one of the largest Chinese-owned U.S. real-estate investment firms.

Its stronghold is the Bay Area and DiRaimondo is now looking to raise a $500 million fund to buy distressed buildings, including in downtown San Francisco, a place major Wall Street lenders have been backing away from for months.

“It’s hard to raise equity to buy this stuff right now,” he said, but argues his strategy, which includes expanding its reach to potential investors in the U.A.E., Israel and parts of Europe, will pan out.

SteelWave’s model of buying a property includes a final tally of costs often three to four times the initial purchase price, due to extensive overhauls.

“Typically, what we do is buy something, tear it apart, put it back together, lease it, sell it,” DiRaimondo said.

It’s niche in the distressed world that’s already produced overhauls of buildings from Seattle to Colorado to Los Angeles, places the tech industry wants to lease.

In the southern California town of Costa Mesa, that meant partnering with Invesco to turn an old newsroom and printing press for the Los Angeles Times into a creative work campus. An opinion piece in 2022 from the newspaper described the revamp as turning, “the glum newspaper architecture into something inviting.”

“In New York, people rushed back and refilled the apartments, streets, and subways. Restaurants and stores flooded with customers again,” a team from Moody’s analytics wrote in a recent “tale of two cities” report. “San Francisco, on the other end, battled safety concerns, homelessness, and population exodus which existed before but only became more obvious with barren neighborhoods.”

SteelWave thinks the old days of landlords raking in top-dollar commercial rents in San Francisco, while adding little back to office buildings, are a thing of the past.

“You have to have owners who want to create cool work environments to attract people back into the city,” DiRaimondo said of downtown San Francisco’s long slog back from the brink.

That means buying properties at low prices, but also risking putting money down for major improvements. He isn’t a distressed investors looking to become a “rent bandit,” he says, because the strategy will fail to get quality tenants.

Like the Moody’s team, DiRaimondo thinks San Francisco eventually will bounce back, but he thinks not before reality hits older office properties.

Take a “commodity” building downtown, often older and midblock with generic features, that previously might have been worth $750 to $800 a square foot. It now looks worth less than $300 a square foot, he said.

The early stages of fire-sales have begun already, with the 22-story tower at 350 California, nearby to DiRaimondo’s office, reportedly fetching $200 to $225 a square foot.

“San Francisco is not dead,” DiRaimondo said. “I think there are opportunities in San Francisco.”

See: San Francisco’s office market erases all gains since 2017 as prices sag nationally

[ad_2]

[ad_1]

Home Depot, Target, Cisco, Deere, Walmart, and More Stocks to Watch This Week

[ad_2]

[ad_1]

The thing that will make companies lower prices is if consumers stop complaining about paying more for the things they need and want, and actually start refusing to buy them.

As the U.S. corporate earnings-reporting season progresses, with earnings from major retailers Walmart Inc.

WMT,

Target Corp.

TGT,

and Home Depot Inc.

HD,

on tap next week, investors can get a ground-floor view of how consumer demand may have been hurt, or not, by higher prices, and what the companies plan to do, or not do, about it.

This dynamic of how consumers adjust their spending habits when prices change is referred to by economists as the price elasticity of demand.

“ For companies to cut prices, ‘you have to have the consumer go on strike, and they’re not there yet.’”

Those who trust companies will choose to ratchet down prices on their own, or at least not raise them because the rise in input costs has been slowing, haven’t been listening to what the many companies have told analysts on their post-earnings-report conference calls.

Read: U.S. inflation eases again, PCE shows. Prices rise at slowest pace in almost two years.

Kraft Heinz Co.

KHC,

acknowledged after its second-quarter report that its relatively higher prices have hurt demand, but not by enough for the food and condiments company to consider cutting prices.

Colgate-Palmolive Co.

CL,

said it will continue to raise prices, even as inflation slows and selling volume declines, as the consumer-products company continues to be laser focused on boosting margins and profits.

And while PepsiCo Inc.

PEP,

was worried that elasticities would increase, given how its lower-income customers were being particularly pressured by inflation, the beverage and snack giant reported strong results as it witnessed “better elasticities” in most of the markets in which it operated.

“Obviously, there is still carryover pricing, and I don’t think we’ll do anything different than our normal cycles on pricing in the balance of the year,” PepsiCo Chief Financial Officer Hugh Johnston told analysts, according to an AlphaSense transcript.

Basically, as MarketWatch has reported, so-called greedflation is alive and well.

Jamie Cox, managing partner for Harris Financial Group, said as long as the job market stays strong, as it is now, corporate greed will continue to pay off.

“If something is more expensive, and you have a job, you’ll complain about it, but you won’t substitute it for something cheaper,” Cox said. For companies to cut prices, “you have to have the consumer go on strike, and they’re not there yet,” Cox added.

“ ‘At some point, people are going to say, “All right — enough.” ’ ”

The reason elasticity is so important in the current environment is that, as long as consumers continue to pay the higher prices companies are charging, inflation will remain stubbornly high, making it, in turn, more likely that the Federal Reserve will continue to raise interest rates or, at the very least, not lower them.

But the longer interest rates stay high enough to crimp economic growth, the more likely the stock market will reverse lower as recession fears rise.

“At some point, people are going to say, ‘All right — enough,’ ” said Paul Nolte, senior wealth manager and market strategist at Murphy & Sylvest Wealth Management. “But we just haven’t seen that yet.”

What is elasticity?

Economists use the term “price elasticity of demand” to refer to the way in which consumers adjust their spending habits when prices change.

“Elasticity tries to measure how much more producers will want to produce if prices rise, and how much more consumers will want to buy if prices fall,” explained Bill Adams, chief economist at Comerica.

Elasticity often depends on the type of product a company sells.

For example, consumer-discretionary-goods companies that sell products and services that people want will often experience greater price elasticity than consumer-staples companies that sell things that people need, such as groceries and prescription drugs.

But even for needs, consumers often still have a choice, as less expensive generic, or private-label, alternatives may be available.

Andre Schulten, chief financial officer of consumer-staples maker Procter & Gamble Co.

PG,

which recently beat earnings expectations as it continued to raise prices, telling analysts that, while there was “some trading into private label,” the overall market share of private-label products was unchanged for the year.

As Harris Financial’s Cox said, consumers may be complaining about higher prices, but they aren’t yet desperate enough to stop buying.

The Federal Reserve’s latest Beige Book economic survey stated that business contacts in some districts had observed a “reluctance” to raise prices as consumers appeared to have grown more sensitive to prices, but other districts reported “solid demand” allowed companies to maintain prices and profitability.

That’s likely why companies and analysts have become less concerned about price elasticity. Based on a FactSet analysis, mentions of the word “elasticity” in press releases and conference calls of S&P 500 companies

SPX

increased as inflation and interest rates started surging in early 2022 through the end of the year.

With inflation trends softening this year, the Fed took a brief pause in raising rates in June, helping fuel further stock-market gains, before raising rates again in July.

FactSet

As the chart shows, “elasticity” popped up in more than 55% of earnings releases and conference calls in mid-2022, but with the second-quarter 2023 earnings-reporting season more than half over, mentions had dropped to about 20%.

Perhaps that will pick up, as retailers, especially those catering to lower-income customers — recall the PepsiCo comment — assess the demand impact of continued price increases.

Meanwhile, the branded-foods company Conagra Brands Inc.

CAG,

whose wide-ranging food brands including Birds Eye, Duncan Hines, Hunt’s, Orville Redenbacher’s and Slim Jim, were starting to see the emergence of a different dynamic.

Chief Executive Sean Connolly said consumers were shifting behavior in some categories as prices remained high. Rather than trade down to lower-priced alternatives, he noticed some consumers buying fewer items overall, “more of a hunkering down than a trading down.”

That’s exactly the kind of consumer behavior that is needed, if companies are to stop feeding into the greedflation phenomenon and to start pulling back on prices.

[ad_2]

[ad_1]

WeWork Inc. disclosed Tuesday that there’s “substantial doubt” about its ability to continue operating, as the company seeks to improve its financial positioning.

Shares of the company, which provides co-working spaces, were down 33% in Tuesday’s after-hours trading.

WeWork

WE,

lost $397 million in the second quarter and has $680 million of liquidity. In light of its losses and expected cash needs, “substantial doubt exists about the company’s ability to continue as a going concern,” WeWork said in its second-quarter earnings release.

Its ability to continue “is contingent upon successful execution of management’s plan to improve liquidity and profitability over the next 12 months.”

See also: Proterra stock craters as electric-bus maker files for Chapter 11 bankruptcy

As part of that liquidity planning, WeWork will aim to cut its rent and tenancy costs through restructuring as a renegotiation of lease terms. The company is also looking to boost revenue by lowering member churn, and it will try to rein in expenses and capital expenditures. Finally, WeWork is seeking additional capital through the issuance of debt or equity, or via asset divestitures.

The company was a hot technology player before the pandemic, enabling businesses to obtain flexible arrangements for workspaces, but it’s struggled to find its footing again now that companies and employees have become more comfortable with remote work.

WeWork’s losses narrowed in the latest quarter, though they were still sizable, as the company logged a net loss of $397 million, or 21 cents a share, compared with a loss of $635 million, or 76 cents a share, in the year-prior period. The FactSet consensus was for a 12-cent loss per share, based on three estimates.

The company also managed to grow revenue in its latest quarter, bringing in an $844 million haul on the top line, up from $815 million a year earlier, though analysts had been looking for $850 million.

“The company’s transformation continues at pace, with a laser focus on member retention and growth, doubling down on our real-estate portfolio optimization efforts, and maintaining a disciplined approach to reducing operating costs,” Interim Chief Executive David Tolley said in a release.

The company’s prior CEO stepped down in May.

See more: WeWork bonds sink after top executives resign from cash-burning company

[ad_2]

[ad_1]

Warren Buffett’s Berkshire Hathaway swung to a profit in the second quarter owed to its investment portfolio and insurance holdings, according to a release out Saturday.

The holding company with businesses that range from insurer Geico and railroad BNSF Railway to Dairy Queen restaurants and its own energy division posted net income of $35.9 billion, or $24,775 a class A share equivalent. That compared with a loss of $43.8 billion, or $29,754 a class A share equivalent, a year earlier.

Berkshire’s

BRK.A,

BRK.B,

after-tax operating earnings, a figure Warren Buffett wants shareholders to and which excludes some investment results, rose 6% to just over $10 billion from $9.3 billion a year earlier. Regulations do require Berkshire to include unrealized gains and losses from its investment portfolio when it reports its net income.

Berkshire’s stock repurchases totaled $1.4 billion in the second quarter, compared with $4.4 billion in the first quarter and $1 billion for the year-earlier period. The Q2 repurchases were below an estimate of $2.2 billion from UBS analyst Brian Meredith.

Reduced buybacks did come alongside appreciation in Berkshire stock, which was up 10% in the second quarter.

Berkshire ended the second quarter with $147.4 billion in cash and cash equivalents, compared with $105.4 billion in the same period a year ago.

Berkshire’s Class A shares have been hovering near all-time highs, up 21% over the past year and bringing the company’s market value to roughly $780 billion.

[ad_2]

[ad_1]

Icahn Enterprises Inc.’s bonds saw better buying on Friday, after Carl Icahn’s investing arm announced it was halving its quarterly distribution, a move that disappointed unit holders but is positive for its bonds.

Bondholders are typically focused on making sure a company can make its interest payments and repay the principal when a bond matures.

The company said it would now make a distribution of $1, down from $2 previously. The news came as the company posted a surprise loss for the second quarter and a $1 billion decline in revenue.

Icahn placed the blame for the fund’s poor performance on Hindenburg Research, the short seller that published a report about IEP on May 2, accusing it of overstating asset values. Hindenburg also revealed that Icahn himself had borrowed from the company, among other issues.

For more, see: Icahn Enterprises’ stock slides 30% after company halves quarterly distribution to $1 per unit

The stock promptly tumbled and was last down 24%, putting it on track for its biggest one-day selloff since it went public 36 years ago. The next biggest drop was 20.0% on May 2, when the Hindenburg Research report was released.

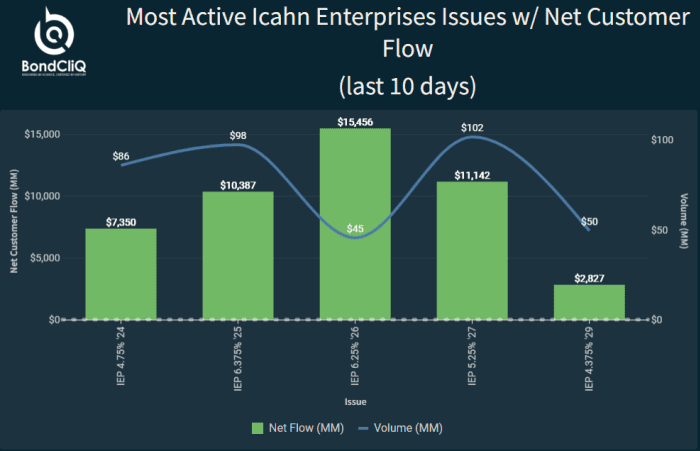

As the chart below from data-as-a-service provider BondCliQ Media Services shows buyers emerging after 8:00 a.m. Eastern, immediately after the news was announced. By midmorning, some sellers had emerged.

The following table shows there was net buying over the last 10 days, focused on the 6.35% notes that mature in 2026.

In a letter to unit holders accompanying the results, Icahn acknowledged missteps in the past several years as the company has shifted away from its core activist strategy and shorted far more than was necessary.

“While we made money on the long side through our activism efforts, our returns have been overwhelmed by our overly bearish view of the market and related oversized short (hedge) positions,” Icahn wrote. “Over the past six months, we have significantly reduced our hedges. Going forward, we intend to stick to our knitting and focus on our activist strategy while remaining appropriately hedged.”

For more, see: Carl Icahn admits he was wrong to take a huge short position on the market that lost $9 billion

Activism is the best investment paradigm because “there is no accountability in Corporate America,” he wrote.

With many exceptions, “most CEOs are incapable of creating great businesses (or even improving them) and the desire to empire build is rampant. “

Many are not the best person for the job or even the most talented individual in the organization, he continued. Far too often, they have climbed through the ranks by being agreeable and presenting no threat to their superiors.

“Those CEOs are generally too busy playing at the proverbial country club to realize what improvements can be made or what hidden jewels can be unlocked,” he said.

CEOs are hard to unseat, as they can pack a board with loyal cronies and use company funds to defend against an activist campaign by hiring expensive legal and financial experts, further depleting the coffers.

Icahn has himself waged endless activist campaigns against companies and their management teams, and most recently succeeded in his effort to shake up management at gene sequencing test maker Illumina Inc.

ILMN,

as the Associated Press reported.

Past activist campaigns by Icahn’s company have generated billions of dollars for shareholders and helped boards and CEOs capture untapped value, Icahn has argued, citing Reynolds, Netflix

NFLX,

Forest Labs, Apple

AAPL,

CVR Energy

CVI,

Herbalife

HLF,

eBay

EBAY,

Tropicana, Cheniere

LNG,

and Occidental

OXY,

as examples.

[ad_2]

[ad_1]

The second-quarter earnings season so far is showing that one trend that featured in the first quarter has not gone away.

“Greedflation,” or the practice of companies raising prices to protect their profit margins, is alive and well, based on the number of companies that have so far acknowledged raising prices yet again, even as inflation readings have come down and as some acknowledge that their input costs are falling.

At the same time, companies continue to emphasize on earnings calls that their customers are showing signs they are weary of higher prices and are shopping more frequently at more stores, while spending less per trip.

See: Consumers are shopping in more stores than ever before to save money

“Across industries, we’ve seen the same story over and over the last two years,” said Liz Zelnick, director of economic security and corporate power at Accountable.US, a liberal-leaning consumer-advocacy group.

“CEOs claim outside forces made them gouge consumers, then turn around and give themselves raises and boast of record profits and billions in new investor handouts,” she said, referring to the billions of stock buybacks and dividend payouts the same companies have made.

See: U.S. inflation slows again, CPI shows, as Fed weighs another rate hike

Also read: U.S. wholesale inflation slows to a crawl, PPI shows

Procter & Gamble Co.

PG,

for example, said it raised prices by up to 9% in its latest quarter, after raising them up to 10% the previous quarter and up to 10% in the same quarter in 2022.

On a call with analysts, Chief Executive Jon Moeller signaled more price increases to come, which he attributed to the company’s innovation pipeline, which is creating must-have products.

“If you look back historically, pricing has been a positive contributor to our top-line growth for something like 48 out of the 51 last quarters and again as we strengthen our innovation program even further, that will provide opportunities to continue to benefit from modest pricing,” said Moeller, according to a FactSet transcript.

See also: Colgate to keep raising prices as inflation slows to boost margins and profit

The company blew past earnings estimates with adjusted per-share earnings of $1.37, ahead of the $1.32 FactSet consensus, and sales of $20.6 billion, versus the $20 billion FactSet consensus.

Gross margin increased 380 basis points from a year ago, driven by 340 basis points of pricing benefit and 290 basis points of productivity savings.

Coca-Cola Co.

KO,

also swept past estimates and raised guidance after the drinks and snacks giant increased prices by 10%. The company’s adjusted operating margin rose to 31.6% from 30.6% a year ago.

Conagra Brands Inc.

CAG,

raised prices by up to 17%, which Chief Executive Sean Connolly described as “inflation-justified.” The parent of brands such as Birds Eye, Duncan Hines, Hunt’s, Orville Redenbacher’s and Slim Jim also reported that its customers are buying less food to stretch their budgets.

For more, see: Consumers are now ‘hunkering down’ rather than ‘trading down’ on groceries, Conagra says

Oreo cookie maker Mondelez International Inc.

MDLZ,

raised prices in North America by 10.4 percentage points in the second quarter and raised prices for all developed markets by 12.4 percentage points. That’s after raising North America prices by 15 percentage points and prices in developed markets by 13.4 percentage points in the first quarter.

The company’s second-quarter gross margins expanded by 3.1 percentage points to 39.4%. Revenues rose 17%, while volumes were flat.

At Campbell Soup Co.

CPB,

sales for its fiscal third quarter were up 5%, led by “favorable net price realization,” as the company disclosed as the very first bullet point in its release. Campbell raised prices of meals and beverages by 9% and if snacks by 15%, after raising them by 15% and 13%, respectively, in the second quarter.

However, volumes were down in the third quarter as shoppers proved sensitive to higher prices.

Kraft Heinz Co.

KHC,

on Tuesday said it too has lost business because it raised prices more than its competitors, but it’s not planning to cut prices to try to get those customers back anytime soon.

“[W]hile we did lose share in the quarter, as price gaps have stayed wider for longer than we would have liked, we are managing the business for the long term and still generated mid-single-digit top-line growth within the range of what we expected,” Chief Executive Miguel Patricio said.

The company, parent to brands including Kraft Mac and Cheese, Heinz Ketchup, Jell-O and Lunchables, indicated on the post-earnings conference call with analysts that rather than increasing discounting, or just cutting prices, it will remain focused on protecting margins, which has been allowing it to accelerate investment in the business, particularly in marketing, research and development and technology.

Besides, as Chief Financial Officer Andre Maciel said, the gaps between Kraft’s prices and those of competitors are not getting worse. “If anything, they are slightly getting better,” Maciel said, according to an AlphaSense transcript.

Considering the market-share losses and with inflation coming down, “do you think you took too much price, given you said you took price ahead of competitors, and they have not followed?” UBS analyst Cody Ross asked on the conference call.

CEO Miguel Patricio’s answer was simple: “No.”

“I mean, we had very high inflation. And we are leaders in the vast majority of categories where we play. And it’s our role as leader to try to compensate … this inflation with price increases,” Patricio said. “So I would do everything again. I mean we can always go back on price if we think we have to or when we have to. But we had to lead price increases.”

All of that leaves families to foot the bill for higher food prices, said Accountable.US’s Zelnick.

The Consumer Staples Select Sector SPDR exchange-traded fund

XLP

has gained 1.2% in the year to date, while the SPDR S&P Retail ETF

XRT

has gained 10.3%. The S&P 500

XRT

has gained 17%.

Tomi Kilgore contributed.

[ad_2]

[ad_1]

Icahn Enterprises L.P.’s stock tumbled 30% on Friday, after the company said it’s cutting its quarterly distribution to $1 from $2 previously.

The company

IEP,

made the announcement as it reported a surprise quarterly loss with Chairman Carl Icahn, the billionaire activist investor, blaming the news squarely on one thing.

“I believe the second quarter partially reflected the impact of short selling on companies we control or invest in, which I attribute to the misleading and self-serving Hindenburg report concerning our company, “Icahn said in a statement.

“It also reflected the size of the hedge book relative to our activist strategy.”

Icahn was referring to a report by short seller Hindenburg Research published on May 2 that accused IEP, Icahn’s publicly traded investing arm, of overstating asset values. Hindenburg also revealed that Icahn himself had borrowed from the company, among other issues.

That had been disclosed in a footnote to financials that Wall Street had overlooked.

Read: What we know about Carl Icahn’s margin loan

The report shaved billions off IEP’s market cap and was firmly rebutted by Icahn, who recently said he has finalized amended loan agreements with banks that untie his personal loans from the trading price of his company’s shares.

Icahn said IEP has paid out distributions for 73 continuous quarters and does not intend for a “misleading” report to interfere with that practice.

“The payment of future distributions will be determined by the board of directors quarterly, based upon current economic conditions and business performance and other factors that it deems relevant at the time that declaration of a distribution is considered,” said Icahn.

On a call with analysts, IEP’s Chief Executive David Willetts highlighted the long-term “lumpiness” of the business, given its many moving parts.

“We have large wins at times and we have volatility, we’re not a company that necessarily has predictable cash flow, there are no guarantees,” he told analysts.

But IEP is not changing its strategy on distributions, he added.

The stock was headed for the biggest one-day selloff since it went public 36 years ago. The next biggest drop was 20.0% on May 2, when the Hindenburg Research report was released.

The company, which is 84% owned by Icahn and his son, Brett, offers exposure to Icahn’s personal portfolio of public and private companies, including petroleum refineries, car-parts makers, food-packaging companies and real estate. Its unit holders are mostly retail investors.

The fund has performed poorly in the past decade. For many years Icahn has publicly expressed suspicion of the bull market that raged around him. He shorted the stock market in a big way as a hedge against his long activist positions. Going into 2021, for example, Icahn’s investment fund had a short exposure of 142%, SEC filings show.

For more, see: Carl Icahn admits he was wrong to take a huge short position on the market that lost $9 billion

Hindenburg, the short selling firm founded by Nate Anderson, took a victory lap on Elon Musk’s X platform, the renamed Twitter, noting that it had predicted that IEP’s poor investment performance would eventually force it to cut the distribution.

Icahn has himself waged endless activist campaigns against companies and their management teams, and most recently succeeded in his effort to shake up management at gene sequencing test maker Illumina Inc.

ILMN,

In June, that company accepted the resignation of its Chief Executive and director, Francis DeSouza, ending a monthslong heated battle over its $7.1 billion acquisition of cancer test maker Grail that has faced regulatory hurdles, as the Associated Press reported.

Icahn had urged shareholders to vote out its chairman, John Thompson, and DeSouza. Company shareholders voted out Thompson in late May.

Past activist campaigns by Icahn’s company have generated billions of dollars for shareholders and helped boards and CEOs capture untapped value, Icahn has argued, citing Reynolds, Netflix

NFLX,

Forest Labs, Apple

AAPL,

CVR Energy

CVI,

Herbalife

HLF,

eBay

EBAY,

Tropicana, Cheniere

LNG,

and Occidental

OXY,

as examples.

IEP said it had a loss of $269 million, or 72 cents per depositary unit, for the second quarter, wider than the loss of $128 million, or 41 cents per depositary unit, posted in the year-earlier period.

Revenue fell to $2.684 billion from $3.796 billion.

The FactSet consensus was for income of 25 cents per depositary unit and revenue of $2.657 billion.

Meanwhile, investors are waiting to see the outcome of a federal probe of IEP’s corporate governance and other issues, which was disclosed along with first-quarter earnings.

IEP’s stock is down 35% in the year to date, while the S&P 500

SPX

has gained 18%.

[ad_2]

[ad_1]

Former President Donald Trump entered pleas of not guilty Thursday at an arraignment in Washington, D.C., giving his formal response to his four-count indictment over his efforts to overturn the 2020 presidential election, including his role in the Jan. 6, 2021, attack on the U.S. Capitol.

Trump, the frontrunner in polls for the 2024 Republican presidential nomination, has denied wrongdoing, and earlier Thursday he continued to criticize the legal proceedings as largely about helping President Joe Biden, a Democrat, in next year’s election.

“The Dems don’t want to run against me or they would not be doing this unprecedented weaponization of ‘Justice.’ BUT SOON, IN 2024, IT WILL BE OUR TURN,” Trump said in a post on his Truth Social platform.

In Tuesday’s 45-page indictment, Trump was hit with charges that included conspiracy to defraud the U.S. and conspiracy to obstruct an official proceeding.

Related: Bill Barr says Jan. 6 indictment is ‘legitimate’ and that Trump knew he lost the election

The former president’s appearance in Washington is just one step in a legal battle that will likely take months or even years to play out.

Special counsel Jack Smith on Tuesday said his office “will seek a speedy trial” in the Jan. 6 case, but Trump defense attorney John Lauro has pushed back repeatedly on Smith’s statement, telling NPR on Wednesday that his side wants “a just trial, not simply a speedy trial,” and that the trial itself “could last six months or nine months or even a year.”

Trump’s legal team looks likely to make change-of-venue requests, with the former president talking up West Virginia in a Truth Social post late Wednesday. He said the Jan. 6 case “will hopefully be moved to an impartial Venue, such as the politically unbiased nearby State of West Virginia! IMPOSSIBLE to get a fair trial in Washington, D.C., which is over 95% anti-Trump.”

The next hearing in the case was reportedly scheduled for Aug. 28, which would be five days after the first GOP presidential primary debate.

Trump also entered pleas of not guilty earlier this year in a Manhattan case over hush-money payments and in a Miami case over classified documents. Another investigation, in Georgia’s Fulton County, centers on efforts by Trump and his allies to undo that state’s 2020 election result. The county prosecutor said over the weekend that she will announce charging decisions by Sept. 1 in that probe.

Biden told CNN Thursday that he was not planning to follow Trump’s arraignment, responding with an emphatic “no” when asked about it during a bike ride in Rehoboth Beach, Del., where he is vacationing this week.

Now read: ‘You’re too honest’: Donald Trump’s alleged Jan. 6 conspiracies, explained

And see: Trump indictment: What does arraignment mean, and what happens next?

Plus: How DeSantis is leading Trump in cash on hand, even as the former president dominates in polls

[ad_2]

[ad_1]

The second-quarter earnings season so far is showing that one trend that featured in the first quarter has not gone away.

“Greedflation,” or the practice of companies raising prices to protect their profit margins, is alive and well, based on the number of companies that have so far acknowledged raising prices yet again, even as inflation readings have come down and as some acknowledge that their input costs are falling.

At the same time, companies continue to emphasize on earnings calls that their customers are showing signs they are weary of higher prices and are shopping more frequently at more stores, while spending less per trip.

See: Consumers are shopping in more stores than ever before to save money

“Across industries, we’ve seen the same story over and over the last two years,” said Liz Zelnick, director of economic security and corporate power at Accountable.US, a liberal-leaning consumer-advocacy group.

“CEOs claim outside forces made them gouge consumers, then turn around and give themselves raises and boast of record profits and billions in new investor handouts,” she said, referring to the billions of stock buybacks and dividend payouts the same companies have made.

See: U.S. inflation slows again, CPI shows, as Fed weighs another rate hike

Also read: U.S. wholesale inflation slows to a crawl, PPI shows

Procter & Gamble Co.

PG,

for example, said it raised prices by up to 9% in its latest quarter, after raising them up to 10% the previous quarter and up to 10% in the same quarter in 2022.

On a call with analysts, Chief Executive Jon Moeller signaled more price increases to come, which he attributed to the company’s innovation pipeline, which is creating must-have products.

“If you look back historically, pricing has been a positive contributor to our top-line growth for something like 48 out of the 51 last quarters and again as we strengthen our innovation program even further, that will provide opportunities to continue to benefit from modest pricing,” said Moeller, according to a FactSet transcript.

See also: Colgate to keep raising prices as inflation slows to boost margins and profit

The company blew past earnings estimates with adjusted per-share earnings of $1.37, ahead of the $1.32 FactSet consensus, and sales of $20.6 billion, versus the $20 billion FactSet consensus.

Gross margin increased 380 basis points from a year ago, driven by 340 basis points of pricing benefit and 290 basis points of productivity savings.

Coca-Cola Co.

KO,

also swept past estimates and raised guidance after the drinks and snacks giant increased prices by 10%. The company’s adjusted operating margin rose to 31.6% from 30.6% a year ago.

Conagra Brands Inc.

CAG,

raised prices by up to 17%, which Chief Executive Sean Connolly described as “inflation-justified.” The parent of brands such as Birds Eye, Duncan Hines, Hunt’s, Orville Redenbacher’s and Slim Jim also reported that its customers are buying less food to stretch their budgets.

For more, see: Consumers are now ‘hunkering down’ rather than ‘trading down’ on groceries, Conagra says

Oreo cookie maker Mondelez International Inc.

MDLZ,

raised prices in North America by 10.4 percentage points in the second quarter and raised prices for all developed markets by 12.4 percentage points. That’s after raising North America prices by 15 percentage points and prices in developed markets by 13.4 percentage points in the first quarter.

The company’s second-quarter gross margins expanded by 3.1 percentage points to 39.4%. Revenues rose 17%, while volumes were flat.

At Campbell Soup Co.

CPB,

sales for its fiscal third quarter were up 5%, led by “favorable net price realization,” as the company disclosed as the very first bullet point in its release. Campbell raised prices of meals and beverages by 9% and if snacks by 15%, after raising them by 15% and 13%, respectively, in the second quarter.

However, volumes were down in the third quarter as shoppers proved sensitive to higher prices.

Kraft Heinz Co.

KHC,

on Tuesday said it too has lost business because it raised prices more than its competitors, but it’s not planning to cut prices to try to get those customers back anytime soon.

“[W]hile we did lose share in the quarter, as price gaps have stayed wider for longer than we would have liked, we are managing the business for the long term and still generated mid-single-digit top-line growth within the range of what we expected,” Chief Executive Miguel Patricio said.

The company, parent to brands including Kraft Mac and Cheese, Heinz Ketchup, Jell-O and Lunchables, indicated on the post-earnings conference call with analysts that rather than increasing discounting, or just cutting prices, it will remain focused on protecting margins, which has been allowing it to accelerate investment in the business, particularly in marketing, research and development and technology.

Besides, as Chief Financial Officer Andre Maciel said, the gaps between Kraft’s prices and those of competitors are not getting worse. “If anything, they are slightly getting better,” Maciel said, according to an AlphaSense transcript.

Considering the market-share losses and with inflation coming down, “do you think you took too much price, given you said you took price ahead of competitors, and they have not followed?” UBS analyst Cody Ross asked on the conference call.

CEO Miguel Patricio’s answer was simple: “No.”

“I mean, we had very high inflation. And we are leaders in the vast majority of categories where we play. And it’s our role as leader to try to compensate … this inflation with price increases,” Patricio said. “So I would do everything again. I mean we can always go back on price if we think we have to or when we have to. But we had to lead price increases.”

All of that leaves families to foot the bill for higher food prices, said Accountable.US’s Zelnick.

The Consumer Staples Select Sector SPDR exchange-traded fund

XLP

has gained 1.2% in the year to date, while the SPDR S&P Retail ETF

XRT

has gained 10.3%. The S&P 500

XRT

has gained 17%.

Tomi Kilgore contributed.

[ad_2]

[ad_1]

U.S. stock futures stumbled Wednesday after markets were rattled by a downgrade to the U.S. government’s credit rating.

On Tuesday, the Dow Jones Industrial Average

DJIA

rose 71 points, or 0.2%, to 35631, the S&P 500

SPX

declined 12 points, or 0.27%, to 4577, and the Nasdaq Composite

COMP

dropped 62 points, or 0.43%, to 14284.

Equity-index futures are succumbing to a broad risk off tone across markets after rating agency Fitch downgraded the U.S.’s credit rating from AAA to AA+, citing “expected fiscal deterioration” and an “erosion of governance”.

Fitch’s move follows a similar downgrade by S&P more than a decade ago. The U.S. Treasury market acts as a global benchmark upon which many financial products are based and so uncertainty about its stability can cause anxiety for investors.

The news found a stock market arguably vulnerable to unwelcome surprises, with the S&P 500 having already gained 19.2% this year and the tech-heavy Nasdaq Composite up 36.5%.

The CBOE VIX Index , an option-based gauge of expected S&P 500 volatility, jumped 16% to 16.2, its highest in nearly four weeks.

Traditional perceived havens saw demand, with the Japanese yen

USDJPY,

gaining 0.7%, gold

GC00,

nudging up to $1,950 an ounce, and benchmark German government bond yields

BX:TMBMKDE-10Y

moving lower. U.S. 10-year Treasury yields

BX:TMUBMUSD10Y

were little changed at 4.03%.

However, most analysts did not see the downgrade causing the stock market much long term damage.

“While debt downgrades seldom, if ever, have long legs, investors may pause and let the dust settle before re-entering risk markets. However, within this super market-friendly environment of stable growth and a Fed close to the end of its hiking cycle creating fertile ground for stock gains, its unlikely risk sentiment will wander too far off the soft landing path,” said Stephen Innes, managing partner of SPI Asset Management.

Sophie Lund-Yates, lead equity analyst at Hargreaves Lansdown, said “the market remains sensitive as the final throes of earnings season rumble on, but 82% of S&P 500 companies that have reported results so far have surprised to the upside, offering a bit of a sentiment buffer.”

Earnings results due Wednesday include CVS Health

CVS,

Humana

HUM,

and Carlyle Group

CG,

before the opening bell, followed after the close by PayPal

PYPL,

Shopify

SHOP,

and Qualcomm

QCOM,

U.S. economic updates set for release on Wednesday include the ADP employment report at 8:15 a.m. Eastern.

[ad_2]

[ad_1]

I’ve lived in the city for the last four decades, but I’ve mostly been renting. My priorities are a three-bedroom apartment with easy access to grocery stores and the subway in a nice, quiet neighborhood.

But housing prices are insane in New York City. I want a house, but my partner is looking at a co-op. And for my price range of $700,000, the best options I can find are co-ops.

I plan to buy the home and live in it, and am not looking to rent it out in the foreseeable future. The home is for my family of four.

So my question is this: Is a co-op a good idea?

New York Native

‘The Big Move’ is a MarketWatch column looking at the ins and outs of real estate, from navigating the search for a new home to applying for a mortgage.

Do you have a question about buying or selling a home? Do you want to know where your next move should be? Email Aarthi Swaminathan at TheBigMove@marketwatch.com.

For those unfamiliar with what a co-op is, it’s short for housing cooperative. A cooperative is a legal group that owns one or more residential buildings, and the residents are members of it. The cooperative can comprise apartments, but it can also be made up of single-family homes. Residents who purchase a co-op unit don’t own the unit itself and have a share in the common areas. Instead, they’re purchasing a share of the overall property, and that share gives them the right to live in a specific unit.

When you look for homes, you may find that co-operative apartments are cheaper than comparable condominium units in the same city, or than single-family homes. And with the median home price in Manhattan being $1.2 million, according to Douglas Elliman, a co-op apartment for $700,000, if you find one, may sound like a good deal.

But, as you already know, for a three-bedroom, you’ll be quickly priced out of Manhattan. The real-estate brokerage said that a three-bedroom co-op apartment on the island would run about $2.23 million. And only 12% of co-op sales were three-bedroom apartments, versus 38% for one-bedrooms.

You will find deals further out. In Queens, Douglas Elliman said, the median price of a condo unit was about $720,000 in the second quarter of this year, and a co-op apartment cost roughly $310,000.

But there are drawbacks that you should consider, if you haven’t already.

First of all, you don’t technically own your co-op apartment as you would own an apartment in a condominium. Co-ops also charge you fees, which can run $4,000 a month, as Streeteasy observes, depending on the size of the unit, and so on. Applying for co-op ownership can be a painful process. Renting them out (if you can do that at all) will be hard, since the renter will have to go through the co-op board.

Selling is similarly tough, as the prospective buyer needs to be approved by the board. A board can require that a buyer put a lot of money up front, as Curbed explains. Ultimately, you may end up with less equity over time as experts say co-ops don’t typically appreciate at the same pace as condominium units or single-family houses or town houses.

Co-ops are also very “secretive,” as the Guardian put it, with little transparency into how boards make their decisions about potential buyers and renters. According to data from the New York City Department of Housing Preservation and Development, there were 3.6 million housing units as of 2021, out of which 832,000 were in a condominium or a co-op.

That being said, co-ops aren’t all that bad.

The important thing to remember is if you’re just looking for an affordable place to live with your family, the numbers may very well make sense.

Co-op apartments are priced lower than units in condominiums, as already mentioned, so you’re still able to find good options with easy access to the subway and other urban amenities. You can stop dealing with rent hikes from your landlord and have a property to call your own. And, ultimately, you also live in a building with many long-term tenants versus living among neighbors who change every year. There can also be a greater sense of community in a co-op vs. a condominium as co-op residents may tend to change less frequently.

So you have to weigh the pros and cons. If you’re looking for a more affordable entry into New York City real estate, and have the stomach to navigate the co-op process, then, by all means, apply for that apartment your wife liked.

Bottom line: Just be sure you won’t want to move in a couple of years from now because you likely won’t be able to rent it out for long, if at all.

By emailing your questions, you agree to having them published anonymously on MarketWatch. By submitting your story to Dow Jones & Co., the publisher of MarketWatch, you understand and agree that we may use your story, or versions of it, in all media and platforms, including via third parties.

[ad_2]

[ad_1]

The Big Number: Former President Donald Trump’s political action committee has spent $40.2 million on legal fees in this year’s first half, according to multiple published reports citing unnamed sources.

The PAC, called Save America, is expected to disclose the spending in a filing on Monday with the Federal Election Commission.

What it means: The outlays show the sizable legal challenges that Trump and his associates have been dealing with.

The 45th president, who has a big lead in polls for the 2024 Republican presidential primary, was indicted in March in a Manhattan case focused on hush-money payments, as well as indicted in June in a Miami case focused on classified documents. In addition, he could get indicted in Washington, D.C., in a case focused on the Jan. 6, 2021, attack on the U.S. Capitol and in a separate probe in Georgia’s Fulton County over election interference, and he was found liable in May for sexual abuse in a civil lawsuit.

What people are saying: Former New Jersey Gov. Chris Christie, an outspoken Trump critic who is seeking the 2024 GOP presidential nomination, criticized their race’s frontrunner for not using his own money for the legal expenses that he and his associates are incurring.

“He’s making regular Americans pay his legal fees. It’s outrageous,” Christie said over the weekend in a CNN interview.

But Trump campaign spokesman Steven Cheung told CNN that the spending is needed, saying that “to protect these innocent people from financial ruin and prevent their lives from being completely destroyed, the leadership PAC contributed to their legal fees to ensure they have representation against unlawful harassment.”

Trump’s team is now setting up a legal defense fund to help handle some of the legal fees, according to other published reports citing unnamed sources.

[ad_2]

[ad_1]

When Amazon.com Inc. and Apple Inc. report quarterly results on Thursday, we’ll get a look at two big companies, with big expectations, trying to do smaller things — or at least less exciting things, or things that might be more inconveniencing to customers — to stay bigger.

For Apple

AAPL,

D.A. Davidson analyst Tom Forte said, the focus will be on the iPhone, as always, as well as demand abroad and a new VR headset, as its stock hovers near record highs and its market value holds above $3 trillion. And he said that Amazon

AMZN,

meanwhile, could face questions about the impact of cost cuts on e-commerce growth, and what AI could do to boost slower growth in its cloud business.

The results from those companies, which are big enough to make or break a single quarter’s worth for the S&P 500 Index

SPX,

will follow those from the other tech giants like Microsoft Corp.

MSFT,

and Facebook parent Meta Platforms Inc.

META,

And they’ll arrive as Wall Street starts to get a tad more realistic about AI: Microsoft shares fell after management said the expansion of its AI capabilities would be “gradual” — and gradually more expensive.

D.A. Davidson analyst Tom Forte, in a research note this month, said Amazon, like other big tech companies, was taking more steps to control its costs. That might help margins, he said. But he said he’d be watching for any impact to e-commerce sales growth, following thousands of layoffs and pulling back on its expansion of Amazon Fresh.

Amazon began tacking on servicing fees onto some Amazon Fresh delivery orders this year. And Forte noted what he said were other tweaks to service: Charging for a home pickup of a defective smoke alarm that used to be free, and incentives to wait longer during Prime Day.

“In our view, Amazon is playing a ‘game of chicken’ and banking on other e-commerce companies not to offer a superior service, instead of its historical approach of working backwards with a customer-obsessed approach,” D.A. Davidson analyst Tom Forte said in a research note.

He added later: “We believe there is something to be said about the experience of having an Amazon-branded delivery vehicle show up at your house EVERY day. Having one show up once a week or twice is not the same.”

At Apple, Forte said in a separate note, the iPhone, whose sales were still solid, had turned into more of a consumer staple than a discretionary buy. He also said he’d be looking for more detail about the upcoming iPhone 15 — likely to be modestly fancier than previous iPhones — the recovery in China and growth in India. Apple last month also unveiled its Vision Pro VR headset — for $3,499. Forte said he had his doubts.

“We believe Apple will have to overcome a number of structural challenges to achieve mass adoption for its AR/VR headset,” he said.

Apple and Amazon will report as more companies than normal report quarterly profit ahead of estimates, according to a FactSet report on Friday. For the week ahead, 170 S&P 500 companies report results, with four from the Dow, the repot said.

Results from Uber Technologies Inc.

UBER,

and DoorDash Inc.

DASH,

will offer an update on the gig economy and how far app-based deliveries can go, while results from Kraft Heinz Inc.

KHC,

will offer an update on food prices and how much they might ease from the highs seen in recent months.

With the “Barbie” movie lifting rival Mattel Inc.

MAT,

results from Hasbro Inc

HAS,

during the week will offer a glance at the rest of the toy industry, where demand hasn’t exactly been great, and what entertainment options Hasbro has up its sleeve to keep apace with its archrival. Drug maker Pfizer Inc.

PFE,

reports, as does video-game maker Electronic Arts Inc.

EA,

Starbucks Corp.

SBUX,

reports as well.

“Barbie,” the Hollywood strike and Warner Bros. Discovery: Mattel has said it wants to turn “Barbie” into a content franchise. Now we’ll hear what Warner Bros. Discovery Inc.

WBD,

the media conglomerate that produced the film, thinks about the film’s results and its prospects, as studios increasingly pump out sequels or offshoots of well-known, established character universes like “Star Wars,” Marvel and DC. The company — which reports oversees Warner Bros. CNN, TNT and the streaming service Max — reports quarterly results on Thursday. But even as “Barbie” and “Oppenheimer” carry the parts of the entertainment industry that are still functioning through the Hollywood strike, Wall Street will likely be focused on contingency plans, and any sense of whether more viewers are turning to streaming with productions on pause.

Payments and crypto volumes: Results this week from trading app Robinhood Markets Inc.

HOOD,

and crypto exchange Coinbase Global Inc.

COIN,

along with PayPal Holdings Inc.

PYPL,

and Block

SQ,

will land at the intersection of rebounding markets and job-market concerns.

UBS analysts predicted solid growth and cost control for Block, and “steady” e-commerce trends for PayPal. But BofA analysts said PayPal’s search for a new chief executive, following the announcement of Dan Schulman’s retirement at the end of the year, would become more important, adding that “we think investors should rightfully expect the CEO search to conclude in the near-term.” While Bitcoin’s rebound helped Coinbase, the company and others in the industry face the prospect of tougher regulations. Robinhood and PayPal report on Wednesday. Coinbase and Block report on Thursday.

[ad_2]