Former President Donald Trump entered pleas of not guilty Thursday at an arraignment in Washington, D.C., giving his formal response to his four-count indictment over his efforts to overturn the 2020 presidential election, including his role in the Jan. 6, 2021, attack on the U.S. Capitol.

Trump, the frontrunner in polls for the 2024 Republican presidential nomination, has denied wrongdoing, and earlier Thursday he continued to criticize the legal proceedings as largely about helping President Joe Biden, a Democrat, in next year’s election.

“The Dems don’t want to run against me or they would not be doing this unprecedented weaponization of ‘Justice.’ BUT SOON, IN 2024, IT WILL BE OUR TURN,” Trump said in a post on his Truth Social platform.

In Tuesday’s 45-page indictment, Trump was hit with charges that included conspiracy to defraud the U.S. and conspiracy to obstruct an official proceeding.

The former president’s appearance in Washington is just one step in a legal battle that will likely take months or even years to play out.

Special counsel Jack Smith on Tuesday said his office “will seek a speedy trial” in the Jan. 6 case, but Trump defense attorney John Lauro has pushed back repeatedly on Smith’s statement, telling NPR on Wednesday that his side wants “a just trial, not simply a speedy trial,” and that the trial itself “could last six months or nine months or even a year.”

Trump’s legal team looks likely to make change-of-venue requests, with the former president talking up West Virginia in a Truth Social post late Wednesday. He said the Jan. 6 case “will hopefully be moved to an impartial Venue, such as the politically unbiased nearby State of West Virginia! IMPOSSIBLE to get a fair trial in Washington, D.C., which is over 95% anti-Trump.”

The next hearing in the case was reportedly scheduled for Aug. 28, which would be five days after the first GOP presidential primary debate.

Biden told CNN Thursday that he was not planning to follow Trump’s arraignment, responding with an emphatic “no” when asked about it during a bike ride in Rehoboth Beach, Del., where he is vacationing this week.

I’ve lived in the city for the last four decades, but I’ve mostly been renting. My priorities are a three-bedroom apartment with easy access to grocery stores and the subway in a nice, quiet neighborhood.

But housing prices are insane in New York City. I want a house, but my partner is looking at a co-op. And for my price range of $700,000, the best options I can find are co-ops.

I plan to buy the home and live in it, and am not looking to rent it out in the foreseeable future. The home is for my family of four.

So my question is this: Is a co-op a good idea?

New York Native

‘The Big Move’ is a MarketWatch column looking at the ins and outs of real estate, from navigating the search for a new home to applying for a mortgage.

Do you have a question about buying or selling a home? Do you want to know where your next move should be? Email Aarthi Swaminathan at TheBigMove@marketwatch.com.

Dear New Yorker,

For those unfamiliar with what a co-op is, it’s short for housing cooperative. A cooperative is a legal group that owns one or more residential buildings, and the residents are members of it. The cooperative can comprise apartments, but it can also be made up of single-family homes. Residents who purchase a co-op unit don’t own the unit itself and have a share in the common areas. Instead, they’re purchasing a share of the overall property, and that share gives them the right to live in a specific unit.

When you look for homes, you may find that co-operative apartments are cheaper than comparable condominium units in the same city, or than single-family homes. And with the median home price in Manhattan being $1.2 million, according to Douglas Elliman, a co-op apartment for $700,000, if you find one, may sound like a good deal.

But, as you already know, for a three-bedroom, you’ll be quickly priced out of Manhattan. The real-estate brokerage said that a three-bedroom co-op apartment on the island would run about $2.23 million. And only 12% of co-op sales were three-bedroom apartments, versus 38% for one-bedrooms.

You will find deals further out. In Queens, Douglas Elliman said, the median price of a condo unit was about $720,000 in the second quarter of this year, and a co-op apartment cost roughly $310,000.

But there are drawbacks that you should consider, if you haven’t already.

First of all, you don’t technically own your co-op apartment as you would own an apartment in a condominium. Co-ops also charge you fees, which can run $4,000 a month, as Streeteasy observes, depending on the size of the unit, and so on. Applying for co-op ownership can be a painful process. Renting them out (if you can do that at all) will be hard, since the renter will have to go through the co-op board.

Selling is similarly tough, as the prospective buyer needs to be approved by the board. A board can require that a buyer put a lot of money up front, as Curbed explains. Ultimately, you may end up with less equity over time as experts say co-ops don’t typically appreciate at the same pace as condominium units or single-family houses or town houses.

Co-ops are also very “secretive,” as the Guardian put it, with little transparency into how boards make their decisions about potential buyers and renters. According to data from the New York City Department of Housing Preservation and Development, there were 3.6 million housing units as of 2021, out of which 832,000 were in a condominium or a co-op.

That being said, co-ops aren’t all that bad.

The important thing to remember is if you’re just looking for an affordable place to live with your family, the numbers may very well make sense.

Co-op apartments are priced lower than units in condominiums, as already mentioned, so you’re still able to find good options with easy access to the subway and other urban amenities. You can stop dealing with rent hikes from your landlord and have a property to call your own. And, ultimately, you also live in a building with many long-term tenants versus living among neighbors who change every year. There can also be a greater sense of community in a co-op vs. a condominium as co-op residents may tend to change less frequently.

So you have to weigh the pros and cons. If you’re looking for a more affordable entry into New York City real estate, and have the stomach to navigate the co-op process, then, by all means, apply for that apartment your wife liked.

Bottom line: Just be sure you won’t want to move in a couple of years from now because you likely won’t be able to rent it out for long, if at all.

By emailing your questions, you agree to having them published anonymously on MarketWatch. By submitting your story to Dow Jones & Co., the publisher of MarketWatch, you understand and agree that we may use your story, or versions of it, in all media and platforms, including via third parties.

The Big Number: Former President Donald Trump’s political action committee has spent $40.2 million on legal fees in this year’s first half, according to multiple published reports citing unnamed sources.

The PAC, called Save America, is expected to disclose the spending in a filing on Monday with the Federal Election Commission.

What it means: The outlays show the sizable legal challenges that Trump and his associates have been dealing with.

The 45th president, who has a big lead in polls for the 2024 Republican presidential primary, was indicted in March in a Manhattan case focused on hush-money payments, as well as indicted in June in a Miami case focused on classified documents. In addition, he could get indicted in Washington, D.C., in a case focused on the Jan. 6, 2021, attack on the U.S. Capitol and in a separate probe in Georgia’s Fulton County over election interference, and he was found liable in May for sexual abuse in a civil lawsuit.

What people are saying: Former New Jersey Gov. Chris Christie, an outspoken Trump critic who is seeking the 2024 GOP presidential nomination, criticized their race’s frontrunner for not using his own money for the legal expenses that he and his associates are incurring.

“He’s making regular Americans pay his legal fees. It’s outrageous,” Christie said over the weekend in a CNN interview.

But Trump campaign spokesman Steven Cheung told CNN that the spending is needed, saying that “to protect these innocent people from financial ruin and prevent their lives from being completely destroyed, the leadership PAC contributed to their legal fees to ensure they have representation against unlawful harassment.”

Trump’s team is now setting up a legal defense fund to help handle some of the legal fees, according to other published reports citing unnamed sources.

The numbers: Home sales inched up for the first time in four months, even as the U.S. housing market continues to deal with a dearth of listings.

Pending home sales rose by 0.3% in June from the previous month, according to the monthly index released Thursday by the National Association of Realtors.

The figure exceeded expectations on Wall Street. Economists were expecting pending home sales to fall 0.5% in June.

Transactions were still down 15.6% from last year.

Pending home sales reflect transactions where a contract has been signed for the sale of an existing home but the sale has not yet closed. Economists view it as an indicator of the direction of existing-home sales in subsequent months.

Big picture: Home sales rose as the housing market contends with excess buyer demand and a shortfall in the supply of homes for sale.

What the real-estate experts said: “The recovery has not taken place, but the housing recession is over,” NAR chief economist Lawrence Yun said. “The presence of multiple offers implies that housing demand is not being satisfied due to lack of supply.”

The NAR also said it expects rates for 30-year mortgages to average 6.4% this year and to fall to 6% in 2024.

The NAR also expects existing-home sales to fall 12.9% in 2023 from the previous year, to 4.38 million, before recovering in 2024 to a rate of 5.06 million.

The group also expects home prices to hold steady this year, falling only slightly by 0.4% to $384,900, before rising 2.6% next year to $395,000.

“The West — the country’s most expensive region — will see reduced prices, while the more affordable Midwest region is likely to see a small positive increase,” Yun added.

U.S. stocks finished higher on Wednesday as the Dow Jones Industrial Average clinched its eighth straight day in the green amid a flurry of corporate earnings reports. The blue-chip gauge DJIA, +0.31%

finished 108.88 points, or 0.3%, higher at 35,060.81, according to preliminary closing data from FactSet. It marked the first time that the Dow finished above 35,000 since April 20, 2022, and its longest winning streak since September 2019. The S&P 500 SPX, +0.24%

gained 10.72 points, or 0.2%, to 4,565.69. The Nasdaq Composite COMP, +0.03%

gained 4.38 points, or less than 0.1%, to finish at 14,358.02, preliminary data show.

U.S. stocks finished at new highs for the year on Monday to kick off a busy week for corporate earnings, with the Nasdaq leading the way up. The Dow Jones Industrial Average DJIA, +0.22%

rose about 76 points, or 0.2%, ending near 34,585, based on preliminary FactSet data. The S&P 500 index SPX, +0.39%

gained 0.4% and the Nasdaq Composite Index COMP, +0.93%

closed up 0.9%. That was the Dow’s sixth straight day of wins and marked the highest close since April 2022 for all three major stock indexes, according to Dow Jones Market Data. Equities have rallied as the U.S. economy remains resilient in the face of sharply higher interest rates, keeping investors hopeful about a soft landing, instead of a recession. Treasury Secretary Janet Yellen said on Monday that she doesn’t anticipate a U.S. recession, in an interview with Bloomberg television. After several big banks reported on Friday, second-quarter earnings results continue with Tesla, TSLA, +3.20%

Morgan Stanley MS, +0.69%,

Goldman Sachs GS, +0.31%,

Netflix NFLX, +1.84%

and more on deck.

The numbers: Commercial and industrial loans — a key economic driver — held roughly steady in the week ending July 5, the Federal Reserve said Friday. Loans rose $200 million to $2.754 trillion, the central bank said.

Bank lending has been slowly decelerating, falling for three straight months. C&I loans hit a peak of $2.82 trillion in mid-March, right before the collapse of Silicon Valley Bank.

Uncredited

Key details: Total bank deposits rose by $24.9 million to $17.367 trillion in the same week. Deposits have been shrinking slowly. They peaked at $18. 21 billion in mid-April.

Big picture: In the wake of the collapse of Silicon Valley Bank in March, economists have been watching the data carefully for signs of a credit crunch, as banks have weak balance sheets as a result of the Fed’s swift increases in interest rates since March 2022.

San Francisco Fed President Mary Daly said Monday she hadn’t seen credit tightening that is in excess of normal.

“I do think, from research literature, that this takes a while to show itself, and so I think we are still looking into the fall before we would have a declarative statement to make about the extent of credit tightening and the impact on the economy,” Daly said.

The housing market may feel out of whack to home buyers coping with fast-rising home prices and 7% mortgage rates. But like it or not, the housing market is in the pink of health.

Several economic indicators that measure housing activity — from home prices to sentiment surveys — show that home builders and sellers (the few that are out there) are finding strong demand from home buyers.

News of the housing market’s relative health may be welcome to some — like real-estate agents and investors — but it’s becoming a concern for economists. The more buoyant the housing market, economists say, the more likely the U.S. Federal Reserve will unveil another interest-rate hike, which further heightens the risk of a recession.

“‘The housing market has started to recover, and this is a problem for the Fed because more demand for housing will boost home prices and rents.’”

— Torsten Slok, chief economist at Apollo

“The housing market has started to recover, and this is a problem for the Fed because more demand for housing will boost home prices and rents,” Torsten Slok, chief economist at Apollo, wrote in a note in May. And housing is a big part of how the government measures inflation, he added. This will make it more difficult to reduce inflation from 5% to the Fed’s 2% inflation target, he said.

If the Fed launches another rate hike, it would push mortgage rates, which are already in the 7% range, to go even higher.

“The housing market is in a very — if fragile — recovery,” Mike Simonsen, founder and president of real-estate analytics firm Altos Research, told MarketWatch.

“There appears to be more demand than available supply for homes, especially in the real-estate market,” he explained, which is keeping home prices high, but that doesn’t mean demand could evaporate if the current situation changes. Recall when rates doubled from pandemic-era lows in 2021 to 7% last year, which zapped home-buying momentum.

House hunters have adjusted their expectations. But if rates were to jump from 7% today to even higher levels, “I would not be at all surprised if homebuyers stopped abruptly again,” Simonsen said, stating his thesis for the fragility of the sector. Americans broadly expect rates to go over 8%, according to a March survey by the New York Federal Reserve.

MarketWatch looked at three housing-market indicators — and the picture looks rosier than ever:

Active listings are down — blame interest rates

Redfin’s deputy chief economist, Taylor Marr, said his go-to indicator was active listings.

Active listings are down this spring, compared to the previous year, according to the company’s data. At the end of June, the number of homes listed for sale on the market was down 8.1% over the prior year.

“It really captures that supply is pulling back significantly relative to demand,” Marr said.

Redfin data says that active listings of homes are down.

As a result, the housing market is seeing an excess of demand and not enough supply, which has led to a resurgence of bidding wars in some parts of the U.S.

While this metric is showing signs of the housing market returning to life and heating up amid a shortage of houses for sale, Marr said he’s not yet ready to call it a recovery. “It’s hard to declare completely the bottom of the housing market,” he said.

Still battle-scarred by the housing crash of the Great Recession, Marr said economists “might be hesitant” to say that the housing market is in recovery mode. “We still have a lot of uncertainty with the economy ahead,” he added. “If the economy really takes a turn three or four months from now for whatever reason, it could certainly bring the housing market back lower than it was even last November,” he added.

The price gap between new and existing homes

With a major shortage of resale homes, new-home sales have been taking off.

Home builders, understandably, are thrilled about the inventory shortage.

The National Association of Home Builders measures builders’ sentiment in a monthly index, and that indicator has been very cheery of late. In June, the index turned positive for the first time in nearly a year. Builders were scaling back price reductions; they were happy about current sales conditions as well as sales over the next six months, the NAHB said.

“A bottom is forming for single-family home building as builder sentiment continues to gradually rise from the beginning of the year,” said Rob Dietz, chief economist of the NAHB.

One of the major U.S. home builders, Lennar, also offered some commentary on its second-quarter earnings call last month. The company’s executive chairman, Stuart Miller, said that “the market and the economy will remain constructive for home builders as pent-up demand continues to come to market and consume affordable offerings.”

Miller also doesn’t expect the supply issue to be fixed anytime soon: “We believe that the supply constraint will continue to limit available inventory and maintain supply-demand balance,” he said on the call. “The core elements of the supply shortage will not resolve in the near term as the almost 15-year production deficit will take years to resolve.”

Home-builder confidence, as a result, is signaling high optimism about the future of the housing market, and a return to normalcy.

Builders have ramped up building new single-family and multi-family homes.

Ali Wolf, chief economist at Zonda, looks at how prices of new homes trend relative to resale homes as a key indicator of the health of the housing market. Her conclusion? Housing industry professionals involved in the construction and sale of new homes are out of a recession, given the robust demand.

In fact, demand has been so strong that new homes — generally considered to be more expensive than resales — have become more affordable in home buyers’ eyes given the competition in the existing home space.

Typically, new homes are 20% more expensive than resales, Wolf said. And today? That spread has fallen to 4%.

So what’s going on? Builders are not necessarily slashing prices. Instead, existing home prices have risen as homeowners are reluctant to sell.

That’s a good deal for buyers. New homes, Wolf said, are traditionally considered a “luxury good.” They’re brand new, and buyers can often customize them. They also require less maintenance than older homes.

Sellers are holding out on cutting prices

Simonsen, who leads Altos Research, said price cuts were his go-to indicator to gauge the health of the real-estate market. Specifically, price cuts formed a proxy for demand, he explained.

“When the houses are on the market, if there are no buyers for the current houses that are listed, people start taking price cuts,” Simonsen said.

And to be clear, price cuts jumped last year, when rates jumped, he added.

But that dynamic has since changed, as seen in the chart below. “There are currently fewer price reductions now than in 2018 or 2019,” Simonsen said.

Data from Redfin says that homeowners aren’t cutting prices on their homes when selling, possibly due to strong interest from buyers.

And for those of you holding out for home prices to crash? Keep waiting, Simonsen said.

“There’s nothing in the data that shows prices crash,” he said. Even if a recession hits at the end of the year, which results in more job layoffs, demand for home-buying falling, and an increase in foreclosures and distress, that’s still a few years from now, he added.

“There’s no signal of home prices crashing anywhere,” Simonsen added.

If you’re a retiree and you’re trying to square the circle of rising costs, longer lifespans, more expensive medical care and turbulent markets, don’t be afraid to run the numbers on your biggest investment.

That would be your home — if you own it.

U.S. house prices are now so high that it is almost impossible for seniors not to ask themselves the obvious question: “Should we cash in, invest the money, and rent?”

Right now the average U.S. house price is nearly $360,000. That’s about a third higher than just a few years ago, before the COVID-19 pandemic. The lockdowns, the panic, the stimulus checks and 2.5% mortgage rates have all passed into history. But the sky-high prices remain — for now.

After several years of double-digit percentage increases, apartment-rent growth is falling for only the second time since the 2008 financial crisis. WSJ’s Will Parker joins host J.R. Whalen to discuss.

There is a similar story for seniors. Federal data show that the average U.S. house price is now nearly 17 times the average annual Social Security benefit — an even higher ratio than it was in August 2008, just before Lehman Brothers collapsed. At that juncture, the average house price was 15 times higher.

U.S. National Home Price Index vs. average rent of primary residence in U.S. city, according to the U.S. Bureau of Labor Statistics. Indexed: January 1987=100.

S&P/Case-Shiller

Our simple chart, above, compares average U.S. home prices with average U.S. rents, going back to 1987. (The chart simply shows the ratio, indexed to 100.) The bottom line? House prices are very high at the moment compared with rents — again, prices are about where they were in 2006-07.

And the two must run in tandem over the long term, because the economic value of owning a house is not having to pay rent to live there.

If there are times when, in general, it makes more financial sense for seniors to rent than to own, this has to be one of those.

Seniors who own their own homes may think high interest rates on new mortgages don’t affect them. They most likely either already have a mortgage at a lower, older rate or they’ve paid off their home loan. But if you want to sell, you’ll almost certainly be selling to someone who needs a mortgage.

If borrowing costs drive down real-estate prices, seniors who hold off on selling may miss out on gains they may never see again. After the last housing peak, in 2006, it took a full decade for prices to recover fully. Those who sold when the going was good had the chance to buy lifetime annuities at excellent rates or to invest in stocks and bonds that overall rose about 80% over the same period.

Incidentally, there is also an exchange-traded fund that invests in residential REITs, Armada’s Residential REIT ETF HAUS, -0.53%,

though in addition to single-family homes and apartment-complex operators, about 25% of the fund is invested in companies involved in manufactured-home parks and senior-living facilities.

For each person, the math will be different, and there are a number of questions you need to ask. Where do you want to live? How much would you get if you sold your house? How much would you pay in taxes? How much would it cost to rent the right place? Do you want to leave a property to your heirs? And what would be the costs of moving — both financial and emotional?

The conventional wisdom is that you should own your home in retirement.

“I would advise any and all retirees against renting if at all possible,” says Malcolm Ethridge, a financial planner at CIC Wealth in Rockville, Md. “You need your costs to be as fixed as possible during retirement, to match your income being fixed as well. If you choose to rent, you’re leaving it up to your landlord to determine whether and by how much your No. 1 expense will increase each year. And that makes it very tough to determine how much you are able to allocate toward everything else in your budget for the month.”

A key point here, from federal data, is that nationwide rents have risen year after year, almost without a break, at least since the early 1980s. They even rose during the global financial crisis, with just one 12-month period where they fell — and then by only 0.1%.

“My general advice for clients is that owning a home with no mortgage in retirement is the best scenario, as housing is typically the highest cost we pay monthly,” says Adam Wojtkowski, an adviser at Copper Beech Wealth Management in Mansfield, Mass. “It’s not always the case that it works out this way, but if you can enter retirement with no mortgage, it makes it a lot easier for everything to fall into place, so to speak, when it comes to retirement-income planning.”

“Renting comes with a lot of risk,” says Brian Schmehil, a planner with the Mather Group in Chicago. “If you rent, you are subject to the whims of your landlord, and a high inflationary environment could put pressure on your finances as you get older.”

But it’s not always that simple.

“With housing costs as high as they are now though, renting may be a viable solution, at least for the moment,” says Wojtkowski. “We don’t know what the housing-market trends will be going forward, but if someone is waiting for a housing-market crash before they move, they could very likely be waiting for a long time. We just don’t know.”

“Any decision comes with pros and cons,” says Schmehil. “Selling when your home values are historically high and renting allows you to capture the equity in your home, which is usually a retiree’s largest or second-largest financial asset. These extra funds allow you to spend more money on yourself in retirement without having to worry about doing a reverse mortgage or selling later in retirement, when it may be harder for you to do so.”

Renting also allows you to be more flexible about where you live, for example nearer your children or grandchildren, he adds.

And as any experienced property owner knows, renting also brings another benefit: You no longer have to do as much work around the house.

“Renting is great in that you don’t need to maintain a residence,” says Ann Covington Alsina, a financial planner running her own firm in Annapolis, Md. “If the dishwasher breaks or the roof leaks, the landlord is responsible.”

Wojtkowski agrees, noting that many people no longer want to spend time mowing the lawn or shoveling snow in retirement. “Ultimately, one of the things that I’ve seen most retirees most concerned with is eliminating the general upkeep [and] maintenance of homeownership in retirement,” he says.

Several planners — including Covington Alsina and Wojtkowski — note that one alternative to selling and renting is simply downsizing. This can free up capital, especially when home prices are high, like now, without leaving you exposed to rising rents.

Many baby boomers have been doing exactly that.

Meanwhile, I am reminded of my late friend Vincent Nobile, who — after a long and fruitful life owning homes and raising a family — found himself widowed and alone in his 80s. He rented a small cottage on a New England sound and said how glad he was that he never had to worry about maintaining the roof or the appliances, or fixing the plumbing or the heating, or any one of a thousand other irritations. Or paying property taxes — which go down even more rarely than rents.

When the regular drives to Boston got too onerous, he moved into the city and rented there. And he was glad to do it. The money he had made was all in investments — a lot less hassle both for him and his heirs.

I once asked him if he would prefer to own his own home. He shook his head and laughed.

The construction industry posted a slight gain in May as companies and the government increased spending on projects across the U.S.

Spending on construction projects rose 0.9% in May to $1.93 trillion, the Commerce Department reported Monday.

Wall Street was expecting construction spending to rise 0.5% in April.

Construction spending reveals how much the government and private companies spend on projects, from housing to highways. The more the U.S. spends on construction, the higher the level of economic activity.

The government revised spending on construction in April to 0.4% from an initial read of a 1.2% increase.

Over the past year, construction spending was up 2.4%.

In terms of residential real estate, private residential construction fell 11.6% in May as compared to the previous year. It was up 2.2% as compared to April.

Single-family construction rose on a month-over-month basis in May by 1.7%, but fell sharply by 25% from last year.

Multifamily construction fell by 0.1% in May, but increased by 20.4% from last year.

Spending on public residential construction rose by 0.1% from last month, and 12.3% from last year. The U.S. increased spending on public residential construction by 1.1% from last month, and 8.3% over the last year.

The increase in spending May overall was “strong,” Stephen Stanley, chief U.S. economist at Santander U.S. Capital Markets, wrote in a note.

“In particular, new residential activity jumped by 2.2%, reversing the cumulative declines recorded over the three prior months,” he added. “This lines up with the big increase in housing starts in May and adds to the growing body of evidence that the housing sector is bottoming out.”

Home-equity lines of credit (HELOCs) and second-lien mortgages have been staging a notable comeback as U.S. homeowners look for liquidity and ways to monetize the pandemic surge in home prices, according to BofA Global.

It used to be that borrowers sitting on an estimated $33 trillion pile of equity built up in their homes could simply refinance and pull out cash, until the Federal Reserve’s rapid rate hikes began squelching the option.

Now, with mortgage rates above 6%, and the Fed penciling in two more rate hikes in 2023, cash-strapped homeowners have been seeking out alternatives to extract cash from their properties.

While cash-out refinances tumbled 83% in the fourth quarter of 2022 from a year before, HELOCs rose 7% and home-equity loans grew 31%, according to the latest TransUnion data.

“Borrower demand remains high, particularly given household budgets have been pressured by rising food and energy costs,” a BofA Global credit strategy team led by Pratik Gupta’s, wrote in a weekly client note.

Risky loans to subprime borrowers and home equity products helped precipitate the 2007-2008 global financial crisis and the era’s wave of devastating home foreclosures.

At the time, households had more than $1.2 trillion of home equity revolving and available credit (see chart), whereas the figure was closer to $900 billion in the first quarter of this year.

Home equity products are making a big comeback as households seek liquidity

BofA Global, New York Fed Consumer Credit Panel/Equifax

The pandemic saw home prices surge, giving a big boost to home equity levels. The Urban Institute pegged home equity in the U.S. at $33 trillion as of May, up from a post-2008 peak of about $15 trillion.

BofA analysts argued this time home equity products look different, with roughly $17 trillion of tappable equity across 117 million U.S. homeowners, and most borrowers having high credit scores and low rates.

“The vast majority of that — $14 trillion — is from the cohort of homeowners who own their homes free & clear,” Gupta’s team wrote.

Another $1.6 trillion of equity could be available from Freddie Mac and Fannie Mae borrowers, according to his team, which pegged an estimated 94% of all outstanding U.S. first-lien home mortgages now below 4% rates.

Major banks own the bulk of home equity balances (see chart), led by Bank of America Corp. BAC, +1.23%,

PNC Bank PNC, +0.57%,

Wells Fargo, WFC, -0.05%,

JPMorgan Chase JPM, +0.24%

and Citizens CFG, +0.35%,

according to the team, which notes several other major banks appear to have hit pause on their programs.

A smaller portion of HELOCs and second-lien mortgages have been securitized, or packaged up and sold as bond deals, while nonbank lenders have been offering the products as well.

Stocks closed lower Monday, taking a pause from a recent rally, as investors monitored weekend tumult in Russia. The Dow Jones Industrial Average DJIA, -0.04%

was less than 0.1% lower, while the S&P 500 index SPX, -0.45%

was off 0.5% and the Nasdaq Composite COMP, -1.16%

fell 1.2%, according to FactSet.

Chicago, Philadelphia and Houston have some of the highest percentages of problem office loans when looking at delinquency rates and other early warnings signs of trouble, according to a new report by Barclays.

That might come as a surprise, given that San Francisco has been making headlines for its broader commercial real estate woes, technology sector layoffs and struggles getting workers back to the office.

But so far, it’s other cities like Philadelphia with a 14% rate of office loans at least 30 days delinquent (see chart), or Chicago where 21.2% of its office loans facing imminent default, triggering a transfer of their debt to a “special” loan servicer (Sp. Srv).

Chicago, Houston and Philadelphia are top cities for trouble office loans

Trepp, Barclays Research

Researchers at Barclays based their findings on the performance of commercial property debt in metro areas with at least $2 billion of loans that were packaged into bond deals. They found that, “although there has been much discussion linking issues in the office sector with the very slow pace of return-to-office policies, we see very little correlation between performance of office collateral within various MSAs and Kastle’s weekly occupancy report.”

Kastle’s most recent Back to Work Barometer showed Houston with a 61.6% rate of physical occupancy, above the 50% 10-city average. San Jose’s rate was pegged at below 39%, while the San Francisco metro area was near 45%, when looking at card swipes at more than 2,000 office buildings in 138 cities.

But San Jose and Seattle were outperforming, both with no office loan delinquencies, few specially serviced loans or those on a watchlist for potential problems, according to Barclays.

“Given that tech companies have pulled back from office occupancy and many have embraced remote work, we believe that office delinquencies will continue to rise,” wrote Lea Overby’s credit research team at Barclays, in a Tuesday client note.

While Wall Street’s bond machine, known as the “commercial mortgage-backed securities (CMBS)” market, isn’t the biggest lender on U.S. office buildings, it’s the most transparent place to track loan performance in commercial real estate, because of its monthly public reporting requirements.

Another caveat to the findings is that physical occupancy rates aren’t the same as in-place leases, which many companies continued to pay each month throughout the pandemic. Physical occupancy rates, however, can be a sign of tenant demand for future space.

Stocks were lower Tuesday, as investors awaited Chair Powell’s two days of testimony to Congress, with the Dow Jones Industrial Average DJIA, -0.72%

off 200 points, or 0.6%, the S&P 500 index SPX, -0.47%

off 0.4% and the Nasdaq Composite Index COMP, -0.16%

0.2% lower, according to FactSet.

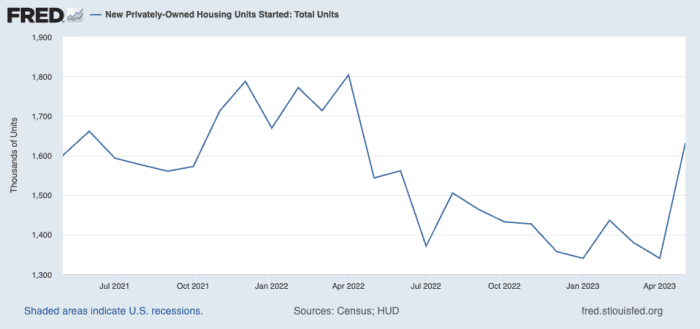

The numbers: Construction on new American homes jumped 21.7% in May, as homebuilders ramp up building single-family homes to meet strong demand from buyers.

Housing starts rose to a 1.63 million annual pace last month from 1.34 million in April, the government said Tuesday. That’s how many houses would be built over an entire year if construction took place at the same rate in every month as it did in May.

Economists were expecting a slight decline of about 0.8%. The numbers are seasonally adjusted.

This is the second month in a row that starts are up. The pace of construction was the highest since last April, when starts hit a 1.8 million pace.

The surge in construction this spring was led by the Midwest.

Both single and multi-family construction rose in May. Keen interest from would-be home buyers is creating strong demand for new homes. These buyers continue to face a lack of options in the resale market.

Building permits, a sign of future construction, rose 5.2% to a 1.49 million rate.

Key details: As the weather warms up, construction pace has picked up considerably.

The construction pace of single-family homes rose 18.5% in May while apartment building rose 28.1%.

Home builders were most active in the Midwest, where housing starts rose by 67% from the previous month. The Midwest also led the nation in terms of single-family construction.

Permits for single-family homes rose 5.2% in May while permits in buildings with at five units or more rose 7.8%.

Housing starts are up on an annual basis for the first time in nearly a year. The annual rate of total housing starts rose 5.7% from last May.

Big picture: New construction is a bright spot in an otherwise despondent housing market. For the buyers who brave 6% mortgage rates, there are few options in the resale market, which continues to funnel demand for new homes.

Builders also reported that they were feeling upbeat about the housing market for the first time in nearly a year.

What are they saying? “To say that we did not see this one coming would not even come close to capturing the degree to which the May residential construction data caught us off guard,” Richard Moody, senior vice president and chief economist at Regions Financial Corporation, wrote in a note.

“This is without question an exaggeration of the underlying reality and a reminder that the housing starts data are among the most volatile and random of the government’s major economic indicators,” Stephen Stanley, chief U.S. economist at Santander U.S. Capital Markets, wrote in a note.

“Having said that,” he added, “the housing sector broadly appears to be healing remarkably fast after enduring a historic shock in affordability last year, when 30-year mortgage rates more than doubled.”

The numbers: For the first time in nearly a year, home builders are upbeat about the housing market outlook.

The shortage of previously-owned sales is helping to buoy builders’ confidence.

With mortgage rates above 6%, many homeowners find little incentive to sell—nearly 92% have an outstanding mortgage with a rate below 6%, according to a recent survey conducted by Redfin RDFN, -0.37%,

a brokerage and real estate listings company. And 23.5% of homeowners have a mortgage rate of less than 3%. Consequently, the number of new home listings has dropped by 22%, as compared with the same period a year ago, according to a Realtor.com housing trends report.

In turn, home builders are feeling good about their business. The National Association of Home Builders’ (NAHB) monthly confidence index rose 5 points to 55 in June, the trade group said Monday.

This is the sixth month in a row that sentiment has improved among builders. It is also the first time in 11 months that builder confidence has moved into positive territory of above 50.

The June reading of 55 was the strongest since July 2022. A year ago, the index stood at 67.

Key details: Builders were starting to pull back on sales incentives. The share of builders cutting prices to boost sales has dropped to 25% in June, from a peak of 36% in November 2022.

The typical builder was cutting prices by 7% in June, the NAHB said.

The three gauges that underpin the overall builder-confidence index were up.

A reading on current sales conditions rose by 5 points.

A measure on future sales gained 6 points.

A gauge of traffic of prospective buyers rose by 4 points.

Big picture: Due to pandemic-era monetary policies that depressed mortgage rates, the home buyers, real-estate agents, mortgage brokers and the rest of the industry are stuck trying to find solutions to a major supply crunch of homes.

Builders seem to be one of the few participants who have benefited from the supply crunch, given the nature of their business of new construction. The homebuilder ETF, XHB, -0.38%,

is up 25% year-to-date.

What the NAHB said: “A bottom is forming for single-family home building as builder sentiment continues to gradually rise from the beginning of the year,” Robert Dietz, chief economist at the NAHB, wrote.

And with the “Federal Reserve nearing the end of its tightening cycle,” the statement read, it’s “good news for future market conditions in terms of mortgage rates and the cost of financing for builder and developer loans.”

U.S. stocks finished mostly higher on Wednesday in a choppy session that saw the Fed leave rates steady in June, while penciling in another 50 basis points of potential hikes later this year. The Dow Jones Industrial Average DJIA shed about 231 points, or 0.7%, ending near 33,980, according to preliminary FactSet data, or well off the session’s low of 33,783. The S&P 500 index SPX added about 3 points, or 0.1% and the Nasdaq Composite Index COMP closed 0.4% higher. “It’s just the idea that were are trying to get this right,” Fed Chairman Jerome Powell said about the potential mixed messaging of holding rates steady in…

Bidding wars are back, as limited housing-market inventory pits buyers against each other. To compete — and certainly to win — buyers need to come fully prepared, Barbara Corcoran says.

Despite a sharp rise in the 30-year mortgage rate to nearly 7%, buyers aren’t able to catch a break, due to a shortage of listings. Competition for homes…

U.S. stocks ended mostly lower on Thursday, with the Dow booking a fourth day in a row of losses, as selling pressures returned to shares of regional banks. The Dow Jones Industrial Average DJIA, -0.66%

shed about 221 points, or 0.7%, ending near 33,310, according to preliminary FactSet data. The S&P 500 index SPX, -0.17%

fell about 0.2%, while the Nasdaq Composite Index COMP, +0.18%

closed 0.2% higher. Disappointing earnings from Disney Co. DIS, -8.73% tied to its streaming business helped drag down the blue-chip Dow, while shares of PacWest Bancorp PACW, -22.70%

fell more than 20% after it disclosed a 9.5% decline in deposits in recent weeks. Short-term rates remained volatile on Thursday as investors hoped for progress on the debt-ceiling stalemate in Washington D.C. The 2-year Treasury TMUBMUSD02Y, 3.891%

was pegged at 3.906%, up four of the past five trading days, according to Dow Jones Market Data. The 6-month Treasury bill was at 5.11%.

U.S. stocks drifted, closing mostly lower on Tuesday, as investors waited for earnings season to gather more steam. The Dow Jones Industrial Average DJIA, -0.03%

ended down 10 points, or less than 0.1%, near 33,976, while the S&P 500 index SPX, +0.09%

gained 0.1%, according to preliminary figures from FactSet. The Nasdaq Composite Index COMP, -0.04%

fell less than 0.1%. Bank of America BAC, +0.63%

and Goldman Sachs GS, -1.70%

were among the major banks to report quarterly results, while streaming giant Netflix Inc. NFLX, +0.29%

was on deck after the bell. It is ending its red-envelope DVD rental service after 25 years. Investors also heard Tuesday from several more staffers at the Federal Reserve, with Atlanta Fed President Raphael Bostic telling Reuters that he expects one more rate hike, but for the Fed’s policy rate to stay higher for awhile. Continued gridlock in Washington on the debt-ceiling stalemate also has been coming into focus for markets. BlackRock also sold the first batch of seized assets from Silicon Valley Bank and Signature Bank, which fetched about 85 cents to 90 cents on the dollar.

The chief executive of the high-end office-furniture company MillerKnoll has gone viral. And probably not in a manner she would prefer.

In a leaked Zoom call of a MillerKnoll staff town hall last month, CEO Andi Owen addressed concerns from employees about the company’s decision to withhold bonuses. It quickly descended into her lambasting staff for complaining about the move.

“Questions came through about, ‘How can we stay motivated if we’re not going to get a bonus?‘ ” she says in the meeting recording. Owen — tapped in 2021 by Fast Company as one of the most creative people in business and celebrated that same year in the New York Times for her navigation of the coronavirus pandemic and swing-state sociopolitics — tells employees of the Zeeland, Mich., company to focus on things the company can control, such as customer service.

“Don’t ask about: What are we going to do if we don’t get a bonus?” she says, growing animated, even, apparently, agitated. “Get the damn $26 million. Spend your time and your effort thinking about the $26 million we need and not thinking about what you’re going to do if you don’t get a bonus. All right? Can I get some commitment for that? I would appreciate that.”

Though she didn’t specifically identify the significance of the $26 million figure, the company’s operating expenses rose by exactly that amount in its third quarter due to “voluntary and involuntary reductions in the company’s workforce and charges for the impairment of assets associated with the decision to cease operating fully as a stand-alone brand.”

MillerKnoll’s third-quarterly filing showed that the furniture maker — the product of a 2021 merger of the Herman Miller and Knoll brands, behind products such as the Eames lounge chair and the Saarinen Tulip table, respectively — expects lower sales in the fourth quarter after posting a decline in orders and sales margins in the three months ending March 4.

Owen recalls in the video that a past employer told her, “You can visit Pity City, but you can’t live there.”

“So, people, leave Pity City,” she continues, exclaiming: “Let’s get it done.”

“You have to be a psychopath to say this stuff to your employees when you are taking a massive bonus. Does she think they won’t find out?” asked one Twitter user.

“Plenty going on here but one of many things that leapt out to me was that mere moments after she went with the ‘be kind to people’ bit, she was yelling at workers,” another said.

The company said that the widely shared video clip had been taken out of context.

“Andi fiercely believes in this team and all we can accomplish together, and will not be dissuaded by a 90-second clip taken out of context and posted on social media,” a spokesman said in a statement.

Owen made $5 million last year. The company has yet to say how much she will make this year. The company this year has expensed $15.7 million in stock-based compensation.

MillerKnoll shares MLKN, -2.38%

have dropped 12% in 2023, compared with the 8% gain for the benchmark S&P 500 SPX, +0.02%.

Other MillerKnoll brands include Design Within Reach, acquired by Herman Miller a decade ago and recognized as having made the iconic midcentury designs of Charles and Ray Eames, Isamu Noguchi, George Nelson, and others available to a wider, if affluent, audience without engaging an interior designer; the Danish design brand Hay; and Holly Hunt.

Here’s a thought for investors: If the Federal Reserve raises interest rates to 5% or more would that wreck the economy and stock prices ?

The U.S. stock market has been rallying to start 2023, clawing back a big chunk of the painful losses from a year ago. The bullish tone has been linked to a view that the Federal Reserve will need to cut interest rates this year to prevent a recession, reversing one of its quickest rate-increasing campaigns in history.

Doomsday investors, including hedge-fund billionaire Paul Singer, have been warning against that outcome. Singer thinks a credit crunch and deep recession may be necessary to purge dangerous levels of froth in markets after an era of near-zero interest rates.

Another scenario might be that little changes: Credit markets could tolerate interest rates that prevailed before 2008. The Fed’s policy rate could increase a bit from its current 4.75%-5% range, and stay there for a while.

“A 5% interest rate is not going to break the market,” said Ben Snider, managing director, and U.S. portfolio strategist at Goldman Sachs Asset Management, in a phone interview with MarketWatch.

Snider pointed to many highly rated companies which, like the majority of U.S. homeowners, refinanced old debt during the pandemic, cutting their borrowing costs to near record lows. “They are continuing to enjoy the low rate environment,” he said.

“Our view is, yes, the Fed can hold rates here,” Snider said. “The economy can continue to grow.”

Profits margins in focus

The Fed and other global central banks have been dramatically increasing interest rates in the aftermath of the pandemic to fight inflation caused by supply chain disruptions, worker shortages and government spending policies.

Fed Governor Christopher Waller on Friday warned that interest rates might need to increase even more than markets currently anticipate to restrain the rise in the cost of living, reflected recently in the March consumer-price index at a 5% yearly rate, down to the central bank’s 2% annual target.

The sudden rise in interest rates led to bruising losses in stock and bond portfolios in 2022. Higher rates also played a role in last month’s collapse of Silicon Valley Bank after it sold “safe,” but rate-sensitive securities at a steep loss. That sparked concerns about risks in the U.S. banking system and fears of a potential credit crunch.

“Rates are certainly higher than they were a year ago, and higher than the last decade,” said David Del Vecchio, co-head of PGIM Fixed Income’s U.S. investment grade corporate bond team. “But if you look over longer periods of time, they are not that high.”

When investors buy corporate bonds they tend to focus on what could go wrong to prevent a full return of their investment, plus interest. To that end, Del Vecchio’s team sees corporate borrowing costs staying higher for longer, inflation remaining above target, but also hopeful signs that many highly rated companies would be starting off from a strong position if a recession still unfolds in the near future.

“Profit margins have been coming down (see chart), but they are coming off peak levels,” Del Vecchio said. “So they are still very, very strong and trending lower. Probably that continues to trend lower this quarter.”

Net profit margins for the S&P 500 are coming down, but off peak levels

Refinitiv, I/B/E/S

Rolling with it, including at banks

It isn’t hard to come up with reasons why stocks could still tank in 2023, painful layoffs might emerge, or trouble with a wall of maturing commercial real estate debt could throw the economy into a tailspin.

Snider’s team at Goldman Sachs Asset Management expects the S&P 500 index SPX, -0.21%

to end the year around 4,000, or roughly flat to it’s closing level on Friday of 4,137. “I wouldn’t call it bullish,” he said. “But it isn’t nearly as bad as many investors expect.”

“Some highly levered companies that have debt maturities in the near future will struggle and may even struggle to keep the lights on,” said Austin Graff, chief investment officer at Opal Capital.

Still, the economy isn’t likely to “enter a recession with a bang,” he said. “It will likely be a slow slide into a recession as companies tighten their belts and reduce spending, which will have a ripple effect across the economy.”

However, Graff also sees the benefit of higher rates at big banks that have better managed interest rate risks in their securities holdings. “Banks can be very profitable in the current rate environment,” he said, pointing to large banks that typically offer 0.25%-1% on customer deposits, but now can lend out money at rates around 4%-5% and higher.

“The spread the banks are earning in the current interest rate market is staggering,” he said, highlighting JP Morgan Chase & Co. JPM, +7.55%

providing guidance that included an estimated $81 billion net interest income for this year, up about $7 billion from last year.

Del Vecchio at PGIM said his team is still anticipating a relatively short and shallow recession, if one unfolds at all. “You can have a situation where it’s not a synchronized recession,” he said, adding that a downturn can “roll through” different parts of the economy instead of everywhere at once.

The U.S. housing market saw a sharp slowdown in the past year as mortgage rates jumped, but lately has been flashing positive signs while “travel, lodging and leisure all are still doing well,” he said.

U.S. stocks closed lower Friday, but booked a string of weekly gains. The S&P 500 index gained 0.8% over the past five days, the Dow Jones Industrial Average DJIA, -0.42%

advanced 1.2% and the Nasdaq Composite Index COMP, -0.35%

closed up 0.3% for the week, according to FactSet.

Investors will hear from more Fed speakers next week ahead of the central bank’s next policy meeting in early May. U.S. economic data releases will include housing-related data on Monday, Tuesday and Thursday, while the Fed’s Beige Book is due Wednesday.