[ad_1]

“‘You could ask who is really running the show? Jerome Powell or Jensen Huang? Amazingly, it may not be Powell, but Jensen Huang who is driving Fed expectations.’”

Those are the words of Ben Emons, a senior portfolio manager and the head of fixed income at NewEdge Wealth in New York, who identifies reasons why artificial-intelligence leader Nvidia Corp.

NVDA,

is demonstrating central-bank-like powers.

It starts with the idea that the Santa Clara, California-based chip designer — which reports fiscal second-quarter earnings on Wednesday — acts as a bellwether for AI-capital expenditures that are likely to boost productivity across the U.S. economy. And in the bond market, a surge of AI-related expectations is translating into higher real yields, which reflect inflation-adjusted growth in gross domestic product and productivity, he said.

Read: Nvidia’s stock snaps losing streak and sits 1% below record close as earnings optimism builds

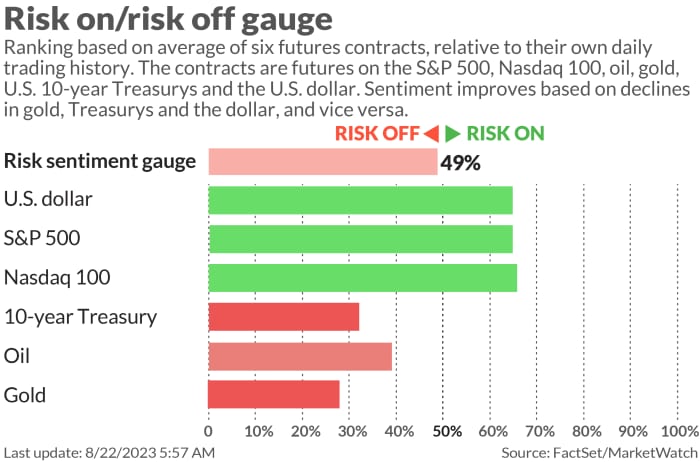

Higher real yields in the U.S. are a key reason why 10-

BX:TMUBMUSD10Y

and 30-year Treasury yields

BX:TMUBMUSD30Y

climbed to multi-year highs through Monday. Real yields, as measured by rates of Treasury inflation-protected securities, offer a glimpse of how the market expects the U.S. to perform when inflation isn’t a factor.

Read: Rise in Treasury yields is almost entirely due to one factor, strategist says

“The bigger macro story behind Nvidia as the bellwether of artificial intelligence is the role it plays in the economy, which is proving to be stronger than anyone thought it would be,” Emons said via phone on Tuesday. “People connect AI to productivity and productivity leads to growth, and to some extent this is impacting interest-rate expectations today.”

Amid growing anticipation over Nvidia’s upcoming earnings announcement and Friday’s speech by Federal Reserve Chairman Jerome Powell in Jackson Hole, Wyo., “the probability of a rate hike is creeping higher,” the senior portfolio manager wrote in a note this week. “With each additional dollar increase of NVDA EPS estimates, the probability of a hike by November goes up. NVDA is gaining Fed-like power.”

Need to Know: Nvidia may be the AI stock for now, but here are the picks for later, says Goldman Sachs

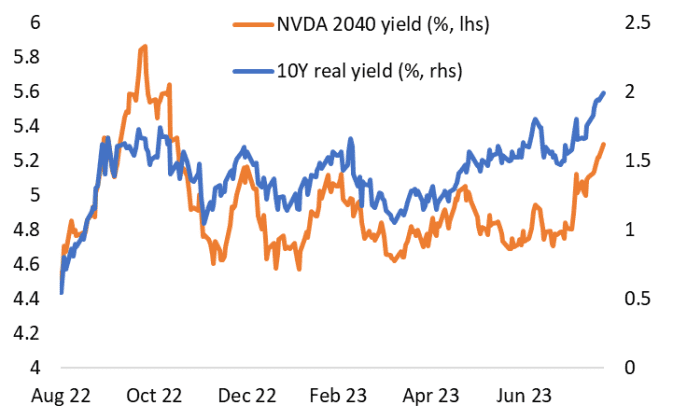

A chart provided by Emons shows how the median estimate of analysts for Nvidia’s earnings-per-share in the fiscal second quarter has been rising alongside the market-implied probabilities of a November Fed rate hike.

Source: Bloomberg, Nvidia

In addition, the yield on one of Nvidia’s own corporate bonds, issued in 2020 and maturing in April 2040, has been rising in relation to the 10-year TIPS or real yield “because of the company’s broader effect on the economy,” Emons said.

Source: Nvidia, U.S. Treasury

As University of Pennsylvania Wharton School finance professor Jeremy Siegel explained in a separate interview with MarketWatch, real interest rates track real growth. Improving productivity and stronger growth “mean the Fed won’t be able to cut rates as much as it would otherwise be able to.”

On Tuesday, Treasury yields finished mixed, while Nvidia’s shares closed down by 2.8%, as traders and investors await the company’s earnings report on Wednesday followed two days later by Powell’s remarks.

Analysts expect Powell to address what’s known as the real neutral rate of interest — or the inflation-adjusted level which is likely to prevail when the economy is operating at full strength and price gains are stable — as a way of justifying the higher-for-longer theme in U.S. interest rates.

See also: How higher-for-longer rates are playing out as 10-year yield hits 15-year high

[ad_2]