The Republican-run House of Representatives approved a debt-ceiling bill in a 217-215 vote on Wednesday evening, marking one step in a process that’s getting closely watched by traders worried about a possible U.S. default.

The bill, dubbed the Limit, Save, Grow Act, aims to raise the limit on federal borrowing for a year while also cutting spending. President Joe Biden and his fellow Democrats have said the lift should be made without spending cuts or other conditions, but House Speaker Kevin McCarthy and his fellow Republicans…

Seemingly every day, U.S. investors are being buffeted by a flurry of sometimes conflicting economic data.

Take this past week, for example: the U.S. leading economic index sank 1.2% in March, its biggest decline in three years. The indicator has now declined for 12 straight months.

Then, one day later on Friday, investors received readings…

Stocks ended a choppy session slightly higher Friday, with major indexes suffering small weekly declines as investors weighed corporate earnings and the economic outlook. The Dow Jones Industrial Average DJIA rose around 22 points, or 0.1%, to close near 33,809, according to preliminary figures. The S&P 500 SPX and Nasdaq Composite COMP each eked out a rise of 0.1%. That left the Dow down 0.2% for the week, while the S&P 500 lost 0.1% and the Nasdaq declined 0.4%.

U.S. stocks finished lower on Thursday as Tesla Inc.’s earnings report weighed on shares of the electric-vehicle giant. The S&P 500 SPX, -0.60%

fell by 24.64 points, or 0.6%, to 4,129.88, according to preliminary data from FactSet. The Dow Jones Industrial Average DJIA, -0.33%

declined by 110.13 points, or 0.3%, to 33,786.88. The Nasdaq Composite COMP, -0.80%

shed 97.67 points, or 0.8%, to 12,059.56.

Price wars have consequences, even for Tesla, the world’s most valuable car company.

Tesla‘s (ticker: TSLA) first-quarter earnings, reported Wednesday evening, met expectations, but its first-quarter automotive gross profit margins were bad. No matter how investors slice and dice the numbers, results will leave them with questions about EV demand and Tesla’s pricing strategy.

U.S. stocks drifted, closing mostly lower on Tuesday, as investors waited for earnings season to gather more steam. The Dow Jones Industrial Average DJIA, -0.03%

ended down 10 points, or less than 0.1%, near 33,976, while the S&P 500 index SPX, +0.09%

gained 0.1%, according to preliminary figures from FactSet. The Nasdaq Composite Index COMP, -0.04%

fell less than 0.1%. Bank of America BAC, +0.63%

and Goldman Sachs GS, -1.70%

were among the major banks to report quarterly results, while streaming giant Netflix Inc. NFLX, +0.29%

was on deck after the bell. It is ending its red-envelope DVD rental service after 25 years. Investors also heard Tuesday from several more staffers at the Federal Reserve, with Atlanta Fed President Raphael Bostic telling Reuters that he expects one more rate hike, but for the Fed’s policy rate to stay higher for awhile. Continued gridlock in Washington on the debt-ceiling stalemate also has been coming into focus for markets. BlackRock also sold the first batch of seized assets from Silicon Valley Bank and Signature Bank, which fetched about 85 cents to 90 cents on the dollar.

U.S. stocks finished higher on Monday after paring earlier losses during the final hour of trading as the first-quarter earnings season is poised to pick up the pace. The S&P 500 SPX, +0.33%

gained 13.69 points, or 0.3%, to 4,151.33, according to preliminary data from FactSet. The Dow Jones Industrial Average DJIA, +0.30%

gained 100.71 points, or 0.3%, to 33,987.18. The Nasdaq Composite COMP, +0.28%

rose by 34.26 points, or 0.3%, to 12,157.72. Investors are looking ahead to a batch of earnings from megacap technology names later in the week, including Netflix Inc., which reports on Tuesday.

U.S. stocks just touched their highest levels in two months. Yet, signs of a looming selloff are piling up, according to Jonathan Krinsky, chief technical strategist at BTIG.

The S&P 500 SPX, +0.33%

and Russell 3000 RUA, +0.40%

are both trading just shy of their highs from mid-February, but market breadth hasn’t recovered, as index gains over the past month have largely relied on megacap names like Microsoft Corp. MSFT, +0.93%

and Apple Inc. AAPL, +0.01%

helping to offset weakness in other areas of the market.

As of Friday, only 45% of Russell 3000 stocks were trading above their 200-day moving averages, according to data cited by Krinsky. By comparison, when the broad-market gauge was trading at its highest level of 2023 back in February, 70% of the individual stocks included in the index were trading above their 200-day moving average. Technical analysts use moving averages as a gauge of a stock or index’s momentum.

BTIG

Lackluster breath is looking like more of an issue analysts say, especially now that the Nasdaq’s outperformance appears to be fading after leading markets higher since the start of the year.

Over the last two weeks, the Dow Jones Industrial Average DJIA, +0.30%

has outperformed the Nasdaq Composite COMP, +0.28%

by the widest margin since the two-week period ending Dec 30, according to FactSet data.

Krinsky cited exchange-traded funds that feature megacap technology names, including the iShares Expanded Tech-Software ETF IGV, +0.45%,

the Communications Services Select Sector SPDR Fund ETF XLC, -0.57%

and Consumer Discretionary Select Sector SPDR Fund ETF XLY, +0.71%,

as examples of emerging weakness in this critical sector of the market. Meanwhile, regional bank stocks, small-cap stocks and shares of retailers, all of which have lagged behind the market this year, look weak.

Krinsky summed up this dynamic thus: “The weak parts of the market remain weak, while the strong parts now appear vulnerable,” the BTIG analyst said in a Sunday note to clients.

Furthermore, “[i]n absolute and relative terms, the tech sector looks like a poor risk/reward to us here,” Krinsky added.

Low implied volatility is another issue for markets, Krinsky said. That can mean investors have gotten too complacent and markets may be heading for a selloff, analysts say.

The Cboe Volatility Index VIX, -0.41%,

otherwise known as Wall Street’s “fear gauge,” finished Friday at its lowest end-of-day level since Jan. 4, according to Dow Jones Market Data. The Cboe S&P 500 9-Day Volatility Index, which tracks implied volatility over a shorter time horizon, has also fallen to January lows, FactSet data show.

Such low levels mean volatility could be poised to “mean revert,” Krinsky said, which may portend a selloff in the months ahead for the S&P 500, the most liquid and most closely watched gauge of U.S. stock-market performance.

Implied volatility gauges measure activity in option contracts linked to the S&P 500 to gauge how volatile traders expect markets to be over the coming days and weeks. Typically, implied volatility advances when U.S. stocks are falling.

The greenback has shown some signs of life in recent sessions, although the U.S. dollar remains well below the multi decade highs it reached back in September. That the buck bounced off its February lows late last week suggests that momentum could be skewed toward the upside for the dollar, Krinsky said, which could create more problems for stocks given the dollar’s tendency to weigh on markets during 2022.

The ICE U.S. Dollar Index DXY, -0.43%,

a gauge of the dollar’s strength measured against a basket of rivals, was up 0.7% in recent trade at 102.22.

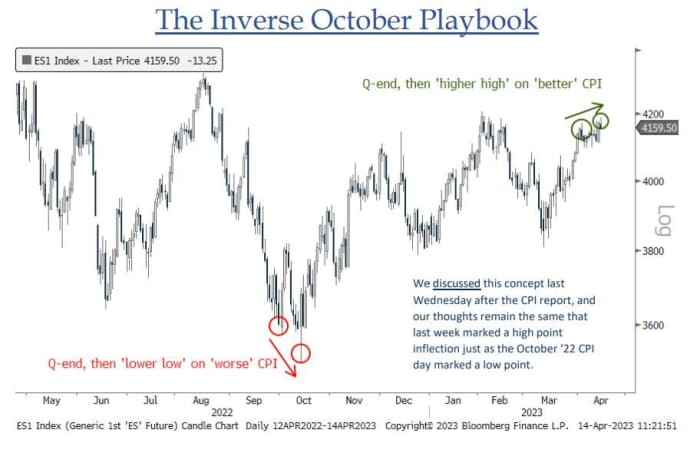

All of these factors support the notion that stocks could be headed for what Krinsky called the “reverse October playbook.”

BTIG

Just as the S&P 500 bottomed following the hotter-than-expected September report on consumer-price inflation, the market’s monthslong rebound rally may have peaked following last week’s CPI report for March, which showed consumer prices rose a scant 0.1% last month, less than the 0.2% increase that had been forecast by economists polled by MarketWatch.

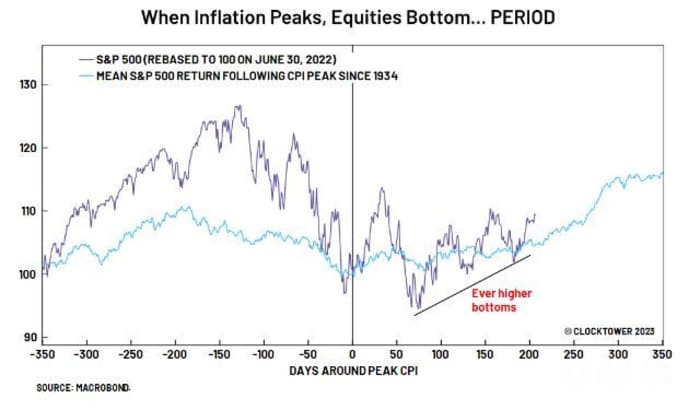

Not everybody agrees with this assessment. Marko Papic, chief strategist at Clocktower Group, cited market data going back to 1934 to show that U.S. stocks tend to rally after inflation peaks. Consumer-price inflation reached its highest level in more than four decades when the CPI headline number showed prices up 9.1% year-over-year in June.

CLOCKTOWER GROUP

U.S. stocks look set to decline for a second day in a row on Monday, with the S&P 500 off 0.3% at 4,126, while the Nasdaq Composite was down by 0.4% at 12,070, and the Dow Jones Industrial Average traded marginally lower at 33,881.

Here’s a thought for investors: If the Federal Reserve raises interest rates to 5% or more would that wreck the economy and stock prices ?

The U.S. stock market has been rallying to start 2023, clawing back a big chunk of the painful losses from a year ago. The bullish tone has been linked to a view that the Federal Reserve will need to cut interest rates this year to prevent a recession, reversing one of its quickest rate-increasing campaigns in history.

Doomsday investors, including hedge-fund billionaire Paul Singer, have been warning against that outcome. Singer thinks a credit crunch and deep recession may be necessary to purge dangerous levels of froth in markets after an era of near-zero interest rates.

Another scenario might be that little changes: Credit markets could tolerate interest rates that prevailed before 2008. The Fed’s policy rate could increase a bit from its current 4.75%-5% range, and stay there for a while.

“A 5% interest rate is not going to break the market,” said Ben Snider, managing director, and U.S. portfolio strategist at Goldman Sachs Asset Management, in a phone interview with MarketWatch.

Snider pointed to many highly rated companies which, like the majority of U.S. homeowners, refinanced old debt during the pandemic, cutting their borrowing costs to near record lows. “They are continuing to enjoy the low rate environment,” he said.

“Our view is, yes, the Fed can hold rates here,” Snider said. “The economy can continue to grow.”

Profits margins in focus

The Fed and other global central banks have been dramatically increasing interest rates in the aftermath of the pandemic to fight inflation caused by supply chain disruptions, worker shortages and government spending policies.

Fed Governor Christopher Waller on Friday warned that interest rates might need to increase even more than markets currently anticipate to restrain the rise in the cost of living, reflected recently in the March consumer-price index at a 5% yearly rate, down to the central bank’s 2% annual target.

The sudden rise in interest rates led to bruising losses in stock and bond portfolios in 2022. Higher rates also played a role in last month’s collapse of Silicon Valley Bank after it sold “safe,” but rate-sensitive securities at a steep loss. That sparked concerns about risks in the U.S. banking system and fears of a potential credit crunch.

“Rates are certainly higher than they were a year ago, and higher than the last decade,” said David Del Vecchio, co-head of PGIM Fixed Income’s U.S. investment grade corporate bond team. “But if you look over longer periods of time, they are not that high.”

When investors buy corporate bonds they tend to focus on what could go wrong to prevent a full return of their investment, plus interest. To that end, Del Vecchio’s team sees corporate borrowing costs staying higher for longer, inflation remaining above target, but also hopeful signs that many highly rated companies would be starting off from a strong position if a recession still unfolds in the near future.

“Profit margins have been coming down (see chart), but they are coming off peak levels,” Del Vecchio said. “So they are still very, very strong and trending lower. Probably that continues to trend lower this quarter.”

Net profit margins for the S&P 500 are coming down, but off peak levels

Refinitiv, I/B/E/S

Rolling with it, including at banks

It isn’t hard to come up with reasons why stocks could still tank in 2023, painful layoffs might emerge, or trouble with a wall of maturing commercial real estate debt could throw the economy into a tailspin.

Snider’s team at Goldman Sachs Asset Management expects the S&P 500 index SPX, -0.21%

to end the year around 4,000, or roughly flat to it’s closing level on Friday of 4,137. “I wouldn’t call it bullish,” he said. “But it isn’t nearly as bad as many investors expect.”

“Some highly levered companies that have debt maturities in the near future will struggle and may even struggle to keep the lights on,” said Austin Graff, chief investment officer at Opal Capital.

Still, the economy isn’t likely to “enter a recession with a bang,” he said. “It will likely be a slow slide into a recession as companies tighten their belts and reduce spending, which will have a ripple effect across the economy.”

However, Graff also sees the benefit of higher rates at big banks that have better managed interest rate risks in their securities holdings. “Banks can be very profitable in the current rate environment,” he said, pointing to large banks that typically offer 0.25%-1% on customer deposits, but now can lend out money at rates around 4%-5% and higher.

“The spread the banks are earning in the current interest rate market is staggering,” he said, highlighting JP Morgan Chase & Co. JPM, +7.55%

providing guidance that included an estimated $81 billion net interest income for this year, up about $7 billion from last year.

Del Vecchio at PGIM said his team is still anticipating a relatively short and shallow recession, if one unfolds at all. “You can have a situation where it’s not a synchronized recession,” he said, adding that a downturn can “roll through” different parts of the economy instead of everywhere at once.

The U.S. housing market saw a sharp slowdown in the past year as mortgage rates jumped, but lately has been flashing positive signs while “travel, lodging and leisure all are still doing well,” he said.

U.S. stocks closed lower Friday, but booked a string of weekly gains. The S&P 500 index gained 0.8% over the past five days, the Dow Jones Industrial Average DJIA, -0.42%

advanced 1.2% and the Nasdaq Composite Index COMP, -0.35%

closed up 0.3% for the week, according to FactSet.

Investors will hear from more Fed speakers next week ahead of the central bank’s next policy meeting in early May. U.S. economic data releases will include housing-related data on Monday, Tuesday and Thursday, while the Fed’s Beige Book is due Wednesday.

Investors are getting used to them. The bigger deal now is the electric-vehicle company’s first-quarter gross profit margins are due to be reported in just a few days.

Reuters reported Friday that Tesla cut prices for its electric vehicles in Europe and some other countries. The price of a Model 3 and Y in Germany were reduced about 5% and 10%, respectively.

U.S. stocks closed lower Friday as investors digested strong big bank earnings, weak retail sales, and hawkish comments from a Federal Reserve official, but all three major benchmarks booked weekly gains.

How did stocks trade?

The Dow Jones Industrial Average DJIA, -0.42%

shed 143.22 points, or 0.4%, to close at 33,886.47.

The S&P 500 SPX, -0.21%

fell 8.58 points, or 0.2%, to finish at 4,137.64.

Nasdaq Composite COMP, -0.35%

declined 42.81 points, or 0.4%, to end at 12,123.47.

For the week, Dow rose 1.2%, the S&P 500 gained 0.8% and the technology-heavy Nasdaq Composite edged up 0.3%. The Dow booked a fourth straight week of gains in its longest win streak since October, according to Dow Jones Market Data.

“Because financial conditions have not significantly tightened, the labor market continues to be strong and quite tight, and inflation is far above target, so monetary policy needs to be tightened further,” Waller said Friday during a speech in San Antonio, Texas.

Waller’s comments were “pretty hawkish,” said Jackie Rogowicz, an investment analyst at Penn Mutual Asset Management, in a phone interview. She said she’s expecting the Fed to raise its benchmark interest rate by a quarter percentage point in May, and at least at this stage, sees some potential for another rate hike in June.

Inflation data released earlier in the week showed a larger-than-expected slowdown in wholesale prices, while so-called core consumer-price inflation remained stubbornly high as it ticked higher to a rate of 5.6% year-over-year.

Marvin Loh, senior global strategist at State Street, said Waller’s comments were a departure from the more dovish tone evinced by other senior Fed officials since the Fed’s March policy meeting.

“This is one of the more hawkish comments over the past week. A lot of the Fed speak has leaned toward ‘one and done’ in terms of rate hikes,” Loh said during a phone call with MarketWatch.

Meanwhile, fresh economic data on Friday showed sales at retailers, a critical component of consumer spending, dropped 1% in March, declining for the fourth time in the past five months. The decline was sharper than the contraction that economists polled by the Wall Street Journal had anticipated.

A popular consumer-sentiment survey released Friday showed respondents’ outlook has risen slightly to 63.5 in April, rebounding from a four-month low, but also reflected slightly higher anxiety about inflation.

While consumer spending hasn’t fallen off a cliff, it has continued to weaken from the elevated levels seen in the aftermath of the COVID-19 pandemic, economists said.

“The cumulative effect of historically high inflation, rising interest rates, and reduced access to credit is already taking a toll on consumers’ ability and willingness to spend,” said Lydia Boussour, senior economist at EY Parthenon, in emailed commentary. “And the full effect of recent banking-sector turmoil and the associated tightening in credit conditions has yet to be felt.”

The first bank earnings reports since regional banks including Silicon Valley Bank failed last month offered some optimism though. Shares of JPMorgan Chase & Co. JPM, +7.55%,

the U.S.’s biggest bank, jumped after it reported earnings and revenue well above forecasts.

JPMorgan CEO Jamie Dimon said the U.S. economy looked “generally healthy,” but warned the coast was not completely clear. “The storm clouds that we have been monitoring for the past year remain on the horizon, and the banking industry turmoil adds to these risks,” he said.

The “big banks are well-capitalized,” said Anthony Saglimbene, chief market strategist at Ameriprise Financial in a phone interview. “They benefited from some deposit inflows in March.”

Investors have been anxious to see how the banks would perform as analysts have been cutting earnings estimates for both large and regional banks in the wake of the crisis.

“So far it seems the numbers are coming in pretty good,” said State Street’s Loh. However, “we have to wait for more smaller lenders to start reporting” to get a better picture of how banks are doing in the wake of last month’s turmoil.

Companies in focus

Shares of Boeing Co. BA, -5.56%

dropped 5.6% after the jet maker warned late Thursday that a manufacturing hang-up could cause problems for production and delivery of “a significant number” of 737 Max planes.

U.S.-listed shares of Curaleaf Holdings Inc. CURLF, -6.69%

Shares of General Electric Co. GE, +1.21%

rose 1.2% after bullish UBS analyst Chris Snyder raised his price target by 15%. The company’s shares have surged this year thanks to a planned spin off.

U.S. stock indexes traded mostly higher on Tuesday as investors cautiously looked ahead to March’s inflation data due Wednesday that could determine the Federal Reserve’s next interest-rate move, as well as to the start of the corporate earnings reporting season on Friday.

How are stock indexes trading

The S&P 500 SPX, -0.00%

rose 14 point, or 0.4%, to 4,123

Dow Jones Industrial Average DJIA, +0.29%

added 176 points, or 0.5%, to 33,763

Nasdaq Composite COMP, -0.43%

dropped 3 points, or less than 0.1%, to 12,081

On Monday, the Dow Jones Industrial Average rose 101 points, or 0.3%, to 33,587, the S&P 500 increased 4 points, or 0.1%, to 4,109, and the Nasdaq Composite dropped 4 points, or 0.03%, to 12,084.

What’s driving markets

Wall Street’s main stock indexes mostly advanced Tuesday afternoon, as investors awaited the release of March’s consumer price index and the start of the first-quarter earnings season, with the banking sector slated to report numbers later this week.

The S&P 500 index sits less than 0.5% off its best level since mid-February as investors have become more relaxed about prospects for the U.S. economy and more accepting of the path of Federal Reserve policy.

The March employment report released last Friday showed a steady pace of job creation but with no great sign of accelerating wage inflation, which helped calm fears of a sharp economic slowdown and faster Fed interest rate hikes.

But now attention turns to the March’s consumer price index report due Wednesday, which is seen as one of the last key data points before the Federal Reserve’s next interest-rate move.

The March CPI reading from the Bureau of Labor Statistics, which tracks changes in the prices paid by consumers for goods and services, is expected to show a 5.2% rise from a year earlier, slowing from a 6% year-over-year rise in the previous month, according to a survey of economists by Dow Jones.

Core CPI, which strips out volatile food and fuel costs, is expected to rise 0.4% from a month ago, or 5.6% year over year. The increase in the core rate over the 12-month period dipped to 5.5% in February.

Investors are wondering whether the Fed is satisfied with what it has done to fight inflation, and whether the central bank has done too much that it would drag the U.S. economy into a recession, according to Kristina Hooper, chief global market strategist at Invesco.

“Tomorrow’s data point will only help us answer that first question,” Hopper said. Meanwhile, “while CPI is important, it’s just one data point. Hopefully it will confirm what we’ve seen with other data points that there’s significant progress in fighting inflation, and hopefully that’s enough to satisfy the Fed,” Hooper said in a call.

Seema Shah, chief global strategist at Principal Asset Management, expects the decline in inflation in 2023 will likely be “incomplete with inflation remaining above central bank targets,” complicating its policy decisions.

“Global inflation is moderating, but so far this deceleration has been largely driven by last year’s energy price spike unwind. Core inflation remains uncomfortably high and, in some economies, continues to rise,” Shah said in emailed comments on Tuesday.

“Central banks have made less progress towards disinflation than they had hoped. Inflation is likely to remain sticky and will still sit above central bank targets at year-end,” Shah said.

The U.S. and global economies are likely to struggle to grow over the next few years as countries fight to reduce high inflation and cope with rising interest rates, the International Monetary Fund said Tuesday.

Meanwhile, the IMF said recent stress in the banking sector could reduce the ability of U.S. banks to lend over the next year, and materially lower U.S. economic growth.

The IMF estimated that lending capacity in the U.S. could fall by almost 1% in the coming year. That would reduce U.S. real gross domestic product by 44 basis points over that time frame, all else being equal, the IMF said.

Then, on Friday, the first-quarter corporate earnings season kicks into gear with the’ financial sector in the vanguard.

It’s particularly important to pay attention to earnings calls and guidance provided by companies’ management, noted Hooper. “That to me is where we’re likely to get the best insights or at least the most robust insights into current credit conditions, to understand what could happen to the economy,” Hooper said.

Philadelphia Fed President Harker will be speaking at 6:30 p.m. and Minneapolis Fed President Kashkari is due to speak at 7:30 p.m. Both times Eastern.

National CineMedia Inc. shares NCMI, +54.96%

shot up 58% after movie theater operator AMC Entertainment Holdings Inc. AMC, +3.63%

disclosed that it has taken a 9.1% stake in the cinema advertising platform. AMC shares jumped 5.9%.

Virgin Orbit Holdings Inc.’s stock VORB, -29.55%

plunged 32% premarket after announcing last Monday that the exchange would delist the space launch companies’ shares after it filed for Chapter 11 bankruptcy protection last week.

Bitcoin rallied Monday to its highest level in 10 months, as some industry proponents touted the asset as a potential “safe haven,” like gold, as recession fears return to the forefront, and after fears rose last month about potential instability in the banking system.

The world’s largest cryptocurrency topped $30,000 Monday night for the first since June 10, 2022, according to Dow Jones Market Data, peaking at $30,321 before pulling back. Bitcoin BTCUSD, +3.20%

has surged 81% year to date, though is still down over 57% from an all-time high in November 2021. Ethereum ETHUSD, +1.68%

also rallied Monday, and was closing in on the $2,000 level for the first time since last August.

“With the bank crisis, I think that the leading feature of bitcoin has changed from speculative tech to safety. A lot more like gold,” said David Tawil, president and co-founder at ProChain Capital. Some investors may have started to view the asset as a haven from the banking turmoil and a recession, instead of a speculative asset, Tawil said.

Still, bitcoin has been often trading in tandem with other risky assets, such as stocks, for the past few years.

“I also believe there will be an influx of liquidity from Asia, especially Asian tech companies who had accounts with Silicon Valley Bank who are now looking for places to put their money,” according to Stefan Rust, founder of Truflation.

The rally on Monday may be partially driven by “the growing influence on the crypto market led by Hong Kong,” while U.S. regulators increase their oversight over the industry, according to Rachel Lin, co-founder and chief-executive at Synfutures.

Hong Kong Financial Secretary Paul Chan said Sunday in a blog post that while crypto markets have been highly volatile, it’s the “right time” to push the adoption of Web3, or the so-called third generation of the internet, in the region.

Bitcoin had been attempting to break the $30,000 level, a psychological level, for three weeks, Rust noted.

Stocks were mixed Monday, with the Dow Jones Industrial Average DJIA, +0.30%

up 0.3% and the S&P 500 SPX, +0.10%

up 0.1%, while the Nasdaq Composite COMP, -0.03%

dipped 0.1%.

U.S. investors will hop right back to work on Easter Monday, after the confluence of Good Friday and “jobs day” required an abbreviated trading session for stock-index futures and Treasurys.

Because Good Friday isn’t a federal holiday, the U.S. Labor Department released the March jobs report at its usual time of 8:30 a.m. Eastern. U.S. stock exchanges and most markets were closed Friday, but U.S. stock-index futures on the CME remained open until 9:15 a.m., giving investors a 45-minute window to trade the employment data….

U.S. stock-index futures turned higher in a holiday-shortened session after a solid March jobs report, though investors won’t fully digest the data until next week with cash trading in equities closed due to the Good Friday holiday.

Trading in stock-index futures closed at 9:15 a.m. Eastern. Stock-index futures resume trading at their regular time, 6 p.m., on Sunday, as U.S. markets return to normal trading hours Monday.

The U.S. stock market is closed Friday, April 7, for the Good Friday holiday, but the bond market will be briefly open.

Friday morning has seen the release of the monthly jobs report for March, a key piece of economic data that households, investors and industry leaders will be following for clues to how much further progress the Federal Reserve has been making in its inflation fight.

U.S. stock-index futures turned higher in a holiday-shortened session after a solid March jobs report, though investors won’t fully digest the data until next week with cash trading in equities closed due to the Good Friday holiday.

Trading in stock-index futures closed at 9:15 a.m. Eastern. Stock-index futures resume trading at their regular time, 6 p.m., on Sunday, as U.S. markets return to normal trading hours Monday.

What stock-index futures are doing

Futures on the Dow Jones Industrial Average YM00, +0.19%

rose 64 points, or 0.2%, to 33,723.

S&P 500 futures ES00, +0.24%

gained 9.75 points, or 0.2%, to 4,141.75.

Nasdaq-100 futures NQ00, +0.10%

ticked up 13.50 points, or 0.1%, to 13,184.25.

With the exception of the Dow industrials, U.S. stocks finished the holiday-shortened week lower on Thursday after three consecutive weekly gains for the S&P 500 and the tech-heavy Nasdaq. The Dow DJIA, +0.01%

rose 0.6% for the week, while the S&P 500 SPX, +0.36%

shed 0.1% and the Nasdaq COMP, +0.76%

slumped 1.1%, after scoring its best quarter since 2020.

Market drivers

The U.S. added 236,000 new jobs in March, defying the Federal Reserve’s hopes for a big slowdown in hiring and possibly making it harder for the central bank to tame inflation. Economists polled by The Wall Street Journal had forecast 238,000 new jobs.

The unemployment rate, meanwhile, slipped to 3.5% from 3.6%. Wages rose 0.3% last month.

“This month’s report indicates that interest rate hikes have yet to impact tight unemployment conditions,” said Steve Rick, chief economist at CUNA Mutual Group, in emailed comments.

Treasury yields popped higher and the dollar rose, though traders noted conditions were thin due to the holiday. Fed-funds futures showed traders pricing in a nearly 70% chance the Federal Reserve will lift interest rates by a quarter-point in May and a roughly 30% chance policy makers will leave rates unchanged. Traders had seen a roughly 50-50 split on Thursday.

“Today’s jobs report is consistent with a slow-moving recession unfolding in the U.S. and one that does not point to immediate resolution of inflation concerns,” said Jason Pride, chief investment officer of private wealth at Glenmede, in a note. “As such, the odds of another quarter-point rate hike in May should go higher as the data does not appear to justify a Fed pause.”

That said, policy makers and investors will see a raft of data before the next Fed meeting, including next week’s consumer-price index reading, Pride noted.

Good Friday is a market holiday but not a U.S. federal holiday. That means the U.S. Labor Department released its March jobs report, as usual. Bond traders will see a half day of trading, with Sifma recommending a noon ET close to allow a reaction to the data.

Investors saw a stream of jobs-related data over the course of the past week. Data on Tuesday showed the number of U.S. job openings dropped below 10 million to a 21-month low, indicating a hot jobs market may be starting to lose some sizzle.

ADP on Wednesday said the private sector added 145,000 jobs in March, well below the 210,000 expected by economists. Weekly jobless claims data on Thursday morning showed first-time applications for benefits last week came in higher than expected.

U.S. stocks eked out modest gains on Thursday after a choppy session, helping the S&P 500 avoid a third day of losses as investors await Friday’s jobs report. The S&P 500 SPX gained 14.61 points, or 0.1%, to finish at 4,104.99, according to preliminary closing data from FactSet. The Nasdaq Composite COMP rose by 91.09 points, or 0.8%, to 12,087.96. The Dow Jones Industrial Average DJIA finished just 2.63 points, or less than 0.1%, higher at 33,485.35. Cash trading in stocks will be closed Friday when the March report from the Department of Labor is released. Economists polled by the Wall Street Journal have a median forecast…

U.S. stocks closed mixed on Wednesday as weaker economic data weighed on equities and focus among investors returned to recession concerns. The Dow Jones Industrial Average DJIA, +0.24%

gained about 80 points, or 0.2%, ending near 33,482, according to preliminary FactSet data, but the S&P 500 index SPX, -0.25%

and Nasdaq Composite Index COMP, -1.07%

fell 0.3% and 1.1%, respectively. That left the S&P 500 down for two straight days and the Nasdaq lower for a third day in a row. Investors were focused on an ADP report showing that private-sector employers added 145,000 jobs in March, well below the 210,000 expected by economists surveyed by The Wall Street Journal. Also, the bellwether Institute for Supply Management’s service sector activity index showed business conditions at U.S. companies fell to a three-month low of 51.2% in March.