Zhejiang Leapmotor Technology’s shares were lower at the mid-day break after initially rising on news of a 1.5 billion euro ($1.58 billion) investment by Stellantis in the Chinese electric-vehicle maker.

Leapmotor shares ended the morning session down 9.4% at 33.40 Hong Kong dollars, reversing course from early gains of as much as 11.5%.

Some of the whipsawing into negative territory arose from early investors in the company seeking an exit point, said Ke Qu, an analyst at CCB International Securities.

“The stock price is under pressure due to selling pressure from pre-IPO investors,” Qu said in an email. “Most may think this partnership announcement creates [a] better exit window for their three-year or even longer investment.”

Qu added that Leapmotor is relatively short on cash compared with other listed startups in China, and can benefit from a partner to leverage its exposure and competitiveness in European or U.S. markets.

“Greater access to [the] EU means better profitability than elsewhere in the world,” she said.

Netherlands-based Stellantis said early Thursday that it is taking a roughly 20% stake in Leapmotor, with the companies planning to create a joint venture to sell Leapmotor products outside of China, starting with Europe.

Leapmotor debuted in Hong Kong in September 2022 after raising about HK$6.06 billion (US$774.8 million) in its initial public offering.

The Chinese company delivered 44,325 vehicles in the third quarter, up almost 25% from a year earlier. Revenue in the quarter rose 32% on the year to CNY5.66 billion.

The Nasdaq Composite Index fell into its 70th correction in history on Wednesday, as surging long-term Treasury yields increased borrowing costs and weighed on stocks.

The interest rate sensitive Nasdaq COMP

barreled higher in the year’s first half, in part on optimism about a potential Federal Reserve pivot away from rate hikes to fight inflation, but stocks have been under fire in recent months as the Fed dialed up its message that interest rates could will stay higher for longer.

The tech-heavy equity index fell 2.4% on Wednesday to close below the 12,922.216 threshold, marking a drop of a least 10% from its prior peak, which was set in mid-July at 14,358.02, according to Dow Jones Market Data.

That met the common definition for a correction in an asset’s value and is the Nasdaq’s 70th close in correction territory since the index’s inception in February 1971.

Robert Pavlik, senior portfolio manager at Dakota Wealth Management, said the sharp rise in long-term Treasury yields has spooked investors, especially those in highflying, high-growth technology stocks where rising rates can be particularly corrosive.

Pavlik likened the dynamic to the spending power of a lottery winner hitting a jackpot when rates are at 2% versus someone who wins when rates are closer to 10%.

He also expects the 10-year Treasury yield BX:TMUBMUSD10Y,

which rose to 4.952% Wednesday, to top out at 5.25% to 5.5% and likely complicate any recovery for the Nasdaq.

In the past 20 corrections for the Nasdaq, it took an average of three months for performance to improve, with index then gaining 14.4% on average a year later, according to Dow Jones Industrial Average.

Nasdaq corrections are usually followed by a bounce in a few months

“You’re feeling the pressure in some big-name stocks,” Pavlik said. “But this too will, at some point, end. But concerns about the Fed are still in the forefront of everybody’s minds.”

The Nasdaq was still up 22.5% on the year through Wednesday, while the Dow Jones Industrial Average DJIA

was down 0.3% and the S&P 500 index SPX

was up 9% in 2023, according to FactSet.

The U.S. economy has not only defied widespread predictions of a sharp slowdown. It’s grown even faster.

But that doesn’t mean a recession is far away. The U.S. has often experienced fast growth shortly before the bottom fell out.

Let’s start with the good news.

Gross domestic product, the official scorecard of the economy, looks likely to top 4% or even 5% annual growth in the third quarter. The government will release its preliminary estimate on Thursday morning.

Economists polled by The Wall Street Journal predict 4.7% GDP in the third quarter.

Other top forecasters see even faster growth. S&P Global estimates 5.6% GDP and the Atlanta Federal Reserve GDPNow forecast projects 5.4%.

How fast is that? GDP only topped 5% once from 2010 to the start of the pandemic in early 2020.

This is not what was supposed to happen.

After solid 2%-plus growth in the first and second quarters, the economy was widely expected to slow down in response to rapidly rising interest rates.

The Federal Reserve has jacked up borrowing costs in the past year and a half to try to tame inflation, a strategy that typical depresses consumer spending and business investment. Those are the dual engines of the economy.

To some extent the Fed has succeeded. Home sales and construction, for instance, have tumbled due to the highest mortgage rates in decades. And manufacturers have taken a hit as customers curtailed purchases of goods and big-ticket items.

The annual rate of inflation, meanwhile, has tapered to 3.7% as of September from a 40-year high of 9.1% in 2022.

Still, spending and investment have not dropped off nearly as much as expected. And there are two reasons for that.

The first is a strong and ultra-tight labor market, with unemployment hovering just below 4%. Most Americans who want a job have one, and as a result, they have been able to keep spending. Travel, recreation, leisure and hospitality have been the big winners.

S&P Global estimates a flush of consumer spending in the third quarter will account for just over half of the growth.

The industrial side of the economy, for its part, has been the beneficiary of tens of billions of dollars in subsidies from the Biden administration to support green energy and bring home more manufacturing.

The U.S. has also ramped up military aid to Ukraine and has to replace outgoing equipment, weapons and ammunition.

All the government money has helped to keep manufacturers from falling too far down the well. Government outlays could add as much as 0.6 percentage points to third-quarter GDP.

Making the third quarter look even better, the U.S. trade deficit fell sharply and is likely to add 1.0 percentage point or more to GDP.

A small rebound in the production of inventories, or unsold goods, would be the icing on the cake.

So the economy is doing great, right? Maybe not.

Consumers probably can’t keep spending at their current pace since their incomes are barely rising faster than inflation. Businesses are proceeding cautiously because of higher borrowing costs. And banks are more reluctance to lend.

Other restraints on the economy include higher gasoline prices and a surge in long-term interest rates that make it far more expensive to buy houses, cars, appliances and the like.

That’s why many forecasters believe the economy start to soften in final months of 2023. S&P Global, for instance, initially projects 1.7% growth in the fourth quarter.

Nor does the third quarter’s heady growth rate suggest there is no reason to worry about a recession. The economy has expanded rapidly just before the onset of prior recessions.

The economy grew at solid 2.5% pace right before the 2007-2009 Great Recession, for example. And GDP grew a frothy 4.4% in the first quarter of 1990 just several months before a recession started.

Many of the same economic headwinds, it turns out, are still in place that led to widespread Wall Street predictions of recession earlier in the year.

Indeed, some forecasters such as the Conference Board still insist a short recession is likely in 2024. Other economists are also on guard.

“I still believe a recession is coming — though far less severe than the 2008-2009 event,” said chief economist Steve Blitz of TS Lombard.

Bitcoin surged over 10% on Monday, briefly surpassing $34,500, on continued optimism that an exchange-traded fund investing directly in the cryptocurrency will soon be approved in the U.S.

The largest cryptocurrency BTCUSD, +6.59%

by market cap on Monday reached as high as $34,616, the loftiest level since May 2022, according to CoinDesk data, before falling to around $33,021 by Monday evening. Other major cryptocurrencies also rose, with ether up 5.8% over the past 24 hours to $1,763.

The U.S. Securities and Exchange Commission has repeatedly rejected bitcoin ETF applications in the past, citing risks of market manipulation. But crypto-industry participants are expecting that to change soon.

A U.S. Appeals court on Monday issued a mandate, putting into effect its ruling in August, which overturned the SEC’s rejection of Grayscale Investments’ application to convert its Bitcoin Trust product GBTC

into an ETF. The final ruling on Monday confirmed Grayscale’s win in court.

Meanwhile, BlackRock’s proposed bitcoin ETF has been listed on the Depository Trust & Clearing Corporation. While it doesn’t mean that the ETF is guaranteed to be approved, it shows another step closer for BlackRock to bring the fund to the market.

If bitcoin ETFs are approved, the crypto may see “historical price increases,” with a crypto bull market coming, according to Alex Adelman, chief executive and co-founder of Lolli. “Bitcoin ETFs will give institutional and retail investors new ways to gain exposure to bitcoin within established regulations,” Adelman said.

A Wall Street strategist who foresaw the U.S. stock-market rally in the first half of the year now sees stocks treading water through the end of 2023, unlikely to extend the previous momentum until at least April 2024.

Barry Bannister, chief equity strategist at Stifel, extended his 4,400 target for the S&P 500 SPX

to April 2024 from the end of this year, as higher interest rates could pressure corporate earnings, weighing on stock prices, he said.

“We believe the rally off the Oct. 2022 lows is over, and our view since summer 2023 has been a sideways trading range,” Bannister said in a Monday note. “The updated view is that we now believe our year-end 2023 target of 4,400 applies through Apr. 30, 2024.”

Bannister was one of the few Wall Street strategists who correctly anticipated the U.S. stock-market rally in the first half of 2023. He also said economic risk for equities will rise in late 2023 as stock gains would stall in the second half of the year. He set his 4,400 year-end target for the S&P 500 in May, a roughly 4.3% advance from Monday’s close of 4,217.04, according to FactSet data.

“We traded the relief rally [in early 2023], turned neutral in summer 2023 and discouraged bullishness before the third quarter of 2023,” Bannister said. He said he thinks a new record-high for the S&P 500 by year-end 2023, as some of the most bullish strategists on Wall Street have projected, is “exceptionally unlikely.”

Meanwhile, Bannister thinks the key 10-year U.S. Treasury yield BX:TMUBMUSD10Y

will peak around 5% in the current cycle, but he projects a “normalized” 10-year yield of 5% or 6% in the mid-2020s, which could put pressure on corporate earnings.

The 10-year Treasury yield flirted with 5% on Monday for the first time since 2007, touching an intraday high of 5.02% in the morning trading before retreating to finish the New York session at 4.836%, according to Dow Jones Market Data.

“It is not ‘Fed high for longer’ — the Fed has returned to ‘policy modulation at normalized rates,’” Bannister wrote.

Bannister also pointed to the health of the U.S. labor market as a source of economic resilience and a reason for “the Fed rate normalization,” which could tighten financial conditions and weigh on price-to-earnings ratios for stocks.

The price-to-earnings ratio, sometimes known as the price multiple, is a ratio of a stock price divided by a public company’s yearly earnings per share. It is a way to determine stock valuation.

That’s why the strategist sees the S&P 500 will remain flat or “range-bound” for the rest of the 2020s decade as price-to-earnings ratios across U.S. firms will be halved due to tightening financial conditions, but it could offset growth in earnings-per-share (EPS). Bannister forecasts the S&P 500 EPS will at least double from $156 in 2019 to a range of $300-325 in 2030.

EPS is a company’s net profit divided by the number of common shares it has outstanding, and it usually indicates how much money a company makes for each share of its stock.

U.S. stocks finished mostly lower on Monday, with the Dow Jones Industrial Average DJIA

down 190 points, or 0.6%, to end at 32,936, but the Nasdaq Composite COMP

edged up 0.3%, according to FactSet data.

Bill Gross, a co-founder of fixed-income investing giant Pacific Investment Management Co., said Monday in a post on social-media platform X that the U.S. economy is likely headed for a recession by year’s end.

“Regional bank carnage and recent rise in auto delinquencies to long-term historical highs indicate U.S. economy slowing significantly. Recession in 4th quarter,” Gross said.

Such an outcome would represent a remarkable turnaround, considering the Atlanta Federal Reserve’s GDP Now real-time indicator shows the U.S. economy expanding at a 5.4% annualized clip during the third quarter. Official GDP data is due Thursday, with economists polled by The Wall Street Journal looking, on average, for a 4.5% annualized growth figure.

Many Wall Street economists had anticipated that the U.S. recession would slide into recession earlier this year. However, strength in construction, consumer spending and other areas has helped it defy expectations, as data show it has instead continued to expand at a solid pace.

Revised data released last month by the Commerce Department showed the U.S. economy grew by 2.1% during the second quarter. Typically, investors only become aware of recessions in hindsight after they’ve been officially declared by the National Bureau of Economic Research.

Rising auto-loan delinquencies are an alarming portent of economic pain to come, Gross said, citing data from Fitch Ratings, reported by Bloomberg News on Friday, which showed the percentage of subprime auto loans more than 60 days delinquent surpassed 6% in September. At 6.1%, it’s the highest rate ever recorded by the data series going back to 1994.

As far as how investors might play this, Gross said he’s “seriously considering” investing in shares of regional banks, which have fallen substantially this year: the SPDR S&P Regional Banking ETF KRE,

one popular exchange-traded fund tracking regional players down more than 30% year-to-date. He also touted some merger-arbitrage plays, a strategy he endorsed in a recent investment outlook.

He also recommended betting that the Treasury curve will continue steepening as it looks to break out of negative territory for the first time in more than a year. Rising long-term rates have nearly caught up with short term rates, with the 10-year yield BX:TMUBMUSD10Y

within 30 basis points of the 2-year yield BX:TMUBMUSD02Y

on Monday.

10-year yields have been lower than 2-year yields for 327 days, according to Dow Jones Market Data. That’s the longest stretch since the 444-trading day streak that ended May 1, 1980.

Gross is using interest-rate futures for his steepening trade. He expects the curve will re-enter positive territory before the end of the year as a slowing economy forces investors to adjust their expectations regarding the timing of Federal Reserve interest-rate cuts.

“’Higher for longer’ is yesterday’s mantra,” Gross said.

Following a decadeslong career on Wall Street, Gross announced his retirement a few years back after a stint at Janus Capital Group. He joined Janus after a contentious exit from Pimco.

Nevertheless, Gross has continued to share his views on markets in posts on X, as well as in investing outlook letters published to his website, and during interviews with the financial press.

The S&P 500 index capped off a busy week for U.S. markets on Friday by breaking below its 200-day moving average for the first time in more than six months. It also erased the last of its gains from a summer advance that peaked in late July.

The index SPX

fell 53.84 points, or 1.26%, on Friday to finish the week at 4,224.16 after falling for a fourth straight day, marking the lowest closing level for the index since June 1, and also the first close below its 200-day moving average — which stood at 4,233.17 — since March 17. The S&P 500 fell 2.4% this week, its worst week in a month, and has now finished lower during five of the past seven weeks.

DOW JONES

The index has fallen 6.8% from its July 31 closing high, FactSet data show but remains up 10% year to date.

Although a break below the moving average is usually seen as a bearish signal, other indicators suggest that the S&P 500 has fallen into oversold territory which could portend a fresh turn higher beginning as soon as next week, technical analysts said.

“From my perspective, this market has gotten to be pretty oversold,” said Craig Johnson, chief market technician at Piper Sandler, during a phone interview with MarketWatch.

A proprietary Piper Sandler database of all U.S. traded stocks with a market capitalization greater than $25 million and a share price above $2 showed that just 18% of stocks were trading above a 40-week moving average, a level that’s only been reached 10 times since 1987, Johnson said. Often, when so many stocks are trading at such low levels relative to their recent performance, it signals that a turnaround could be near.

“It’s really rare to see readings this low,” Johnson added.

Furthermore, more than 65% of S&P 500 stocks were trading below their 200-day moving average as of Friday’s close, the highest reading in a year, FactSet data show. All of this is consistent with what Johnson and others have described as a “washout” for stocks.

Back in March, when the index last closed below its 200-day moving average, it only remained below it for six sessions. Dow Jones data showed that the S&P 500 closed below its 200-day moving average for five straight days from March 9 to March 15, then closed below the average again for a single day on March 17.

U.S. stocks are sliding this week, erasing October’s gains, as higher Treasury yields weigh on markets. The Dow Jones Industrial Average DJIA , S&P 500 SPX and Nasdaq Composite COMP were all down heading toward the closing bell on Friday, with each index on pace for a weekly loss. Investors saw this month’s gains evaporate on Thursday, as equities fell under pressure from rising interest rates in the bond market as investors weighed Federal Reserve Chair Jerome Powell’s remarks that another rate hike may be needed to slow the economy and bring down inflation. So far this month, the Dow has slumped 1%, the S&P 500 has…

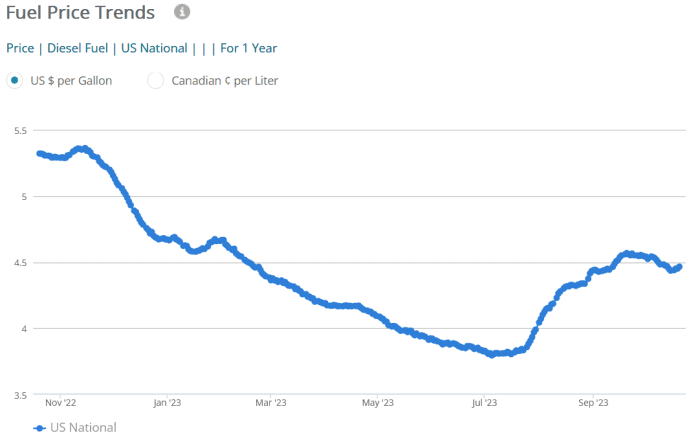

Fuel prices, with the cost of gasoline and diesel at the pump both down from a month ago, don’t appear to be fazed by the escalating risks to oil supplies in the Middle East from the Israel-Hamas war, but they are.

The decline in fuel prices seen nationally is actually a “bit above what would be ‘normal’ for this time of year,” said Patrick De Haan, head of petroleum analysis at GasBuddy. However, he believes “prices won’t fall as far as they would have had the attacks on Israel not happened.”

On Friday, the average retail price for a gallon of regular gasoline stood at $3.528, down 5.7 cents from a week ago, while the average retail diesel price was at $4.465 a gallon on Friday, down 7.8 cents from Sept. 30, according to data from GasBuddy.

U.S. retail gasoline prices have fallen so far this month.

GasBuddy

“Geopolitical risk is now heightened, changing the calculus” for the fuel market, said Brian Milne, product manager, editor and analyst at DTN.

‘Seasonal component’

In considering retail gasoline prices during the fourth quarter, the “seasonal component is less pronounced than in years past,” said Milne. Demand for gasoline tends to fall following the summer travel season. Combined with a “strong slate of refinery maintenance,” which led to less fuel supply on the market, the rise in crude oil prices has slowed the decline in fuel prices, said Milne.

If not for the heightened geopolitical risk in the Middle East, he said he might have expected to see gasoline prices decline by another 30 cents to 40 cents per gallon into late December because of lower demand.

Retail gas prices may fall another 20 cents a gallon or more, depending on the location within the U.S., if we avoid broader hostilities in the Middle East, said Milne.

However, if a conflict breaks out beyond Israel and the Gaza Strip, gasoline prices are likely to move sharply higher because of a spike in crude costs, he said.

For its part, oil has seen volatile trading following the Hamas attack on Israel on Oct. 7, with futures prices for U.S. benchmark West Texas Intermediate crude CLZ23, -0.42%

For now, California, which typically is among the states that pays the most per-gallon for gasoline partly due to taxes on the fuel, is seeing prices “plummet” — down nearly 60 cents in the last three weeks, said GasBuddy’s De Haan.

“The West Coast is certainly seeing a much larger decline than is ‘normal’ and it’s due to the refinery situation now improving drastically,” as well as California’s RVP waiver, he said.

The California Air Resources Board allowed gasoline sold or supplied for use in California that exceeds the RVP, or Reid Vapor Pressure, limits through the end of Oct. 31, marking an early transition for the state from the lower RVP gas used in the summer to help cut gasoline emissions to the higher RVP gas used in the winter.

On Friday, the average price for a gallon of regular gasoline in California sold for $5.476, GasBuddy data show. That’s down 16.7 cents in just the last week.

Gas price outlook

De Haan said he does not expect to see a spike in gas prices nationally at this point, and there’s still room for prices to fall — just not as much following the Hamas attack on Israel.

“If we get to November and Iran gets involved in the situation, then we certainly could see gas prices impacted in some way as the current drops will likely be fully passed on by then, giving stations no ‘room’ to absorb higher prices reflected by a potential rise in oil,” said De Haan.

Still, falling demand, as well as “seasonality in general,” are what are pushing prices down, “enhanced by refinery improvements in areas” that saw price surges, he said.

Prices may even fall further after refinery maintenance season wraps up in mid-November, and refiners have to find places to put even more gasoline output, said De Haan.

He’s comfortable with the gasoline price forecasts GasBuddy issued in December of last year, which predicted a monthly national average for the fuel of $3.53 for October — matching the current price. The forecast also called for an average of $3.36 a gallon for November and $3.17 for December.

GasBuddy doesn’t have a forecast for 2024 yet, but prices may look similar to this year, as long as the situation in the Middle East doesn’t further crumble,” said De Haan.

View on diesel

Diesel, however, is another story.

Price for that fuel have dropped by 85.5 cents a gallon from a year ago to Friday’s $4.465 level, GasBuddy data show.

U.S. retail diesel prices are sharply lower than a year ago.

GasBuddy

While down from a year ago, diesel prices are currently at a “very high level historically” because global supply is low, said DTN’s Milne.

At this time in 2022 diesel fuel inventory was even tighter than it is now, and Europe was heading into winter without Russian natural gas after it was cutoff following the invasion of Ukraine, he said.

That led to a spike in natural-gas prices and prices for gasoil, a European heating oil, also surged, lifting heating oil and diesel prices globally, explained Milne.

Like gasoline, diesel prices could move “sharply higher if the war in Israel expands, and oil flow is put at greater risk,” he said.

De Haan, meanwhile, said diesel prices could climb closer to $5 a gallon if there’s a “squeeze,” with relief then [coming] in the spring/summer” seasons.

The 10-year Treasury yield continued to pull back from 5% on Friday after moving tantalizingly close to surpassing that level in the previous session.

The yield touched 5% at 5:02 p.m. Eastern time on Thursday, only to drift back down, according to Tradeweb data. It ended Friday’s New York session down by 6.3 basis points at 4.924%.

Rising Middle East tensions gave way to renewed safe-haven demand in government debt on Friday that not only sent the 10-year yield BX:TMUBMUSD10Y

lower, but dragged down rates on everything from 3-month Treasury bills BX:TMUBMUSD03M

to the 30-year bond BX:TMUBMUSD30Y.

Investors were trying to catch the proverbial falling knife by taking advantage of a cheaper 10-year Treasury note, the product of recent selloffs. Analysts warn that it’s difficult to have much short-term conviction in catching that knife, however, given the likelihood that the selloff could return.

One big reason is the onslaught of new supply from the U.S. Treasury as the result of the government’s growing borrowing needs, which is raising the risk that investors will keep demanding more compensation to hold long-dated debt to maturity.

On Oct. 30 and Nov. 1, which is the same day as the Federal Reserve’s next policy decision, Treasury is expected to provide updated guidance on its borrowing needs and auction sizes. Treasury’s refunding announcement could even upstage the Federal Open Market Committee — creating “fertile ground for a continuation of the selloff in Treasuries,” said BMO Capital Markets rates strategists Ian Lyngen and Ben Jeffery.

Over the next several weeks, “it becomes much easier to envision a surge in Treasury yields in anticipation of the upcoming coupon supply,” they wrote in a note on Friday. While the 10-year yield has stopped shy of 5%, “we continue to expect this milestone will be reached shortly.”

Stock-market investors have been focused on the prospects of a 5% 10-year yield because such a level would dent the appeal of equities and make government debt a more attractive investment by comparison.

As of Friday, the 10-year yield, used as the benchmark on everything from mortgages to student and auto loans, has jumped 163.9 basis points from its 52-week low of almost 3.29% reached on April 5. The 10-year yield hasn’t ended the New York session above 5% since July 19, 2007.

COMP

ended the day lower as the prospects of a widening conflict in the Middle East triggered a flight-to-safety trade into Treasurys.

Taking a step back, a 5% 10-year yield would imply that a Goldilocks-scenario of a U.S. economy — one that’s neither too hot or too cold, and able to sustain moderate growth — “is here to stay for a decade,” or that the Fed’s main interest-rate target needs to be materially higher on average over the next decade, according to BMO’s Lyngen and Jeffery. One of the biggest questions facing policy makers is whether the economy might be moving into a new stage in which even higher interest rates down the road could be required to cool demand and activity.

Though BMO Capital Markets is biased toward lower yields into the weekend given the absence of major economic data on Friday, technical indicators “continue to favor higher rates in the near-term,” and “our conviction that 5% will ultimately be traded through has grown.”

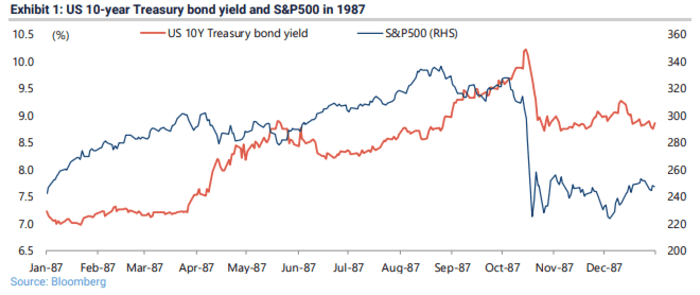

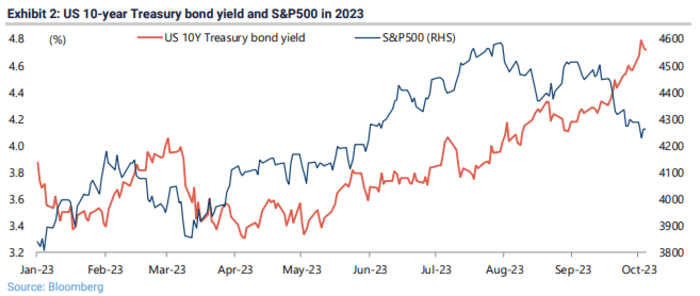

As the anniversary of “Black Monday” approaches, some on Wall Street are observing it by swapping ominous-looking charts and speculating that one of the most terrifying days in markets history might recur.

One could even go as far to say that on social media, some seem eager to relive it, evidenced by a proliferation of viral markets charts, some comparing the stock market’s recent trading action to 1987. Here’s one example from The Market Ear which adheres to a template that caught on following the publication of a column by Bloomberg’s John Authers.

THE MARKET EAR

Authers pointed out that the Nasdaq in 2023 has followed a similar pattern to the Dow in 1987, and that this pattern has also played out in Treasury yields.

To be sure, there are plenty of differences between markets today and in 1987. For one, stock exchanges have strengthened circuit-breaker mechanisms in order to prevent major indexes from crashing by double digits during a single session.

Here is another: While the S&P 500 SPX

has climbed this year in spite of rising yields, the index’s gains have been concentrated in a handful of stocks. Outside of these lucky few, much of the market has lagged or has continued to slide following losses in 2022.

Skeptics contend fretful investors are hearing echoes of 1987, while ignoring important differences.

“In 1987, the market was more overbought, the October decline before the crash was far more pronounced, interest rates were higher, economic growth and inflation were accelerating, and cyclical sectors were stronger” — all in contrast with the current setup, noted Ed Clissold and Thanh Nguyen, strategists at Ned Davis Research, in a note last week.

That hasn’t daunted doomsayers on social media, eager to augur a crash ahead of this year’s anniversary, which falls on Thursday.

On Oct. 19, 1987, the Dow Jones Industrial Average DJIA

plunged 508 points, a decline of almost 23%, in a daylong selling frenzy that ricocheted around the world and tested the limits of the financial system. The S&P 500 dropped more than 20%. At current levels, an equivalent percentage drop would translate into a one-day loss of over 7,700 points. Circuit breakers make a drop of similar magnitude nearly impossible.

Even on Wall Street, some are using the anniversary as an opportunity to take another look at Treasury yields and the dark cloud they’re casting over stocks.

Jefferies’ Global Head of Equity Strategy Christopher Wood recently shared a couple of charts comparing the relationship between stocks and bond yields in 2023 to 1987, driving home the point that stocks appeared resilient to higher yields in 1987 until they finally capitulated with an economy-shaking selloff.

JEFFERIES

JEFFERIES

“The potential similarity with what occurred in October 1987 is that the historic stock market crash was preceded by a big sell-off in the 10-year Treasury over the summer months,” Woods said in the report.

But suppose, for argument’s sake, that stocks did experience a 1987-style selloff. How then might the bond market react? Would yields tumble like they did in 1987, opening the door for stocks to bolt higher once again? Some on Wall Street have posited that a stock-market rout is necessary to stem the bleeding in bonds.

Woods delved into this line of thinking in his report.

“But the other salient point to note is that when the S&P 500 subsequently collapsed by 28.5% in four days, and by 20.5% on 19 October 1987 alone, the Treasury bond market staged a classic flight-to-safety rally in the context of a then dramatic decline in the 10-year Treasury bond yield,” Woods added.

Société Générale’s sharp-tongued strategist Albert Edwards has also warned about the possibility of a 1987-style crash.

But NDR’s Clissold and Nguyen argued that “while there are several high-level similarities, not enough line up to conclude that a crash-like event is likely.

I recently graduated with my master’s degree and am seeking full-time employment at age 53. I want to know what is the best way to invest some of my earnings when I begin receiving a paycheck. I expect to have an annual salary of between $80,000 and $90,000.

For religious reasons, I cannot invest to earn interest, but business-related ventures such as stocks are acceptable. I am planning to set aside up to $1,000 per month for investment purposes, so that I can build some retirement funds. What are my options?

“You have already made the best investment you can make — one in yourself, your education and your future.”

MarketWatch illustration

Dear First-Time,

Congratulations on your master’s degree. You have already made the best investment you can make — one in yourself, your education and your future. It takes patience, guts and stamina to go back to college in your 50s, and you should be very proud. You were one of about 505,000 students in college ages 50 and over, representing less than 4% of the student population.

Given your faith, CDs and high-yield savings accounts are ruled out. A letter writer recently asked me where he should start looking to invest his $50,000 life savings, and I pointed him in the “make interest off your cash” direction, particularly given the recent rise in interest rates. That won’t work for you, but the good news is that you do have many options.

There are investment vehicles for you. In fact, the Accounting and Auditing Organization for Islamic Financial Institutions sets guidelines for investing in accordance with the Sharia religious code, including rules around companies that derive a percentage of their profits from tobacco and alcohol products. And, yes, it also regards interest as unjust and exploitative.

Saturna Capital has mutual funds that follow Islamic principles. The Amana Income Fund AMANX, which focuses on current income and the preservation of capital, has had an average annual five-year return of 8.8% for investor shares, slightly lower than the 9.9% average return for the S&P 500 SPX

over the same period with dividends reinvested. I suggest this as a guidepost rather than a recommendation.

Similarly, the Knights of Columbus assets are managed by Knights of Columbus Asset Advisors in accordance with Catholic moral principles, which are distilled to six main tenets: “protecting human life, promoting human dignity, reducing arms production, pursuing economic justice, protecting the environment [and] encouraging corporate responsibility.”

Of course, investing along religious principles — similar to ESG investment, which takes environmental, social, and corporate-governance factors into account when deciding what to do with your money — is fraught with complications, contradictions and problems with transparency. Regulators are cracking down on vehicles that “greenwash” their ESG credentials.

A major report by the Organization for Economic Cooperation and Development, an intergovernmental organization with 38 member nations, found that ESG ratings vary strongly depending on the provider, as they commonly use different measures, indicators, metrics, data and qualitative judgments to make decisions about funds and companies.

“Moreover, returns have shown mixed results over the past decade, raising questions as to the true extent to which ESG drives performance,” the OECD said. “This lack of comparability of ESG metrics, ratings, and investing approaches makes it difficult for investors to draw the line between managing material ESG risks within their investment mandates.”

You have many funds to choose from. If you’re Catholic, you could look into the Global X S&P 500 Catholic Values ETF CATH

; the LKCM Aquinas Catholic Equity Fund AQEIX; or Ave Maria, which offers mutual funds for growth AVEGX, value AVEMX and bonds AVEFX AVEFX. You can read more here. Investing based on religious, moral or ethical principles doesn’t guarantee a satisfactory return.

It’s not too late to start investing at 53. With the advice of a financial adviser, your risk profile may need regular adjusting, based on your age and tolerance. But you may work into your 70s and may live into your 80s or 90s, and you will want to find myriad ways to build your wealth throughout your retirement. Cash-hoarding typically gets outdone by inflation.

You may find a job with a 401(k) and an employer match, meaning your employer will contribute an additional sum toward your retirement based on the amount you are contributing every month. You may also consider an IRA. Both account types have “catch-up” contributions for people who are over 50. Annual IRA contribution limits for 2023 are $6,500 for people under 50, but $7,500 for those 50 and older.

You can also use pretax dollars for health savings accounts, which are used to offset the burden of high-deductible healthcare plans. With the latter, you pay a lower premium, but you will be saddled with higher out-of-pocket expenses for medical services should you require them. You can contribute up to $4,150 to an HSA for 2024, up from $3,850 this year.

As for right now? Pay off your credit cards. Don’t let high-interest debt trap you. Warren Buffett said one of the best investments he ever made was buying his Omaha, Neb., home for $31,500 in 1958. It’s worth $1.4 million today. He has said he may have put that money to better use if he had rented instead, but owning your own home will solidify your financial position in retirement.

Investing $1,000 a month may be ambitious. But thinking in the medium to long term — and knowing this is a marathon rather than a sprint, even at 53 — is half the battle. With compounding, or making money off your principal and the increase in value of your initial investment, you could have more than $120,000 in 10 years, and over $600,000 in 30 years.

Bravo on this new chapter. Take it one day, one week and one month at a time, and enjoy your life.

You can email The Moneyist with any financial and ethical questions at qfottrell@marketwatch.com, and follow Quentin Fottrell on X, the platform formerly known as Twitter.

Check out the Moneyist private Facebookgroup, where we look for answers to life’s thorniest money issues. Post your questions, tell me what you want to know more about, or weigh in on the latest Moneyist columns.

The Moneyist regrets he cannot reply to questions individually.

Financial literacy peaks at age 54, according to a 2022 study. That’s around the time you’ve gained enough knowledge and experience to make sound money decisions — and before your cognitive ability might start to ebb.

“As we get older, we seem to rely more on past experience, rules of thumb, and intuitive knowledge about which products and strategies are better,” said Rafal Chomik, an economist in Australia who led the study.

If people in their mid-50s tend to make smart financial moves, where does that leave younger generations?

Advisers often educate clients at different stages of life to avoid money mistakes. While those in their 50s usually demonstrate optimal prudence in navigating investments and savings, advisers keep busy helping others — from twentysomethings to mid-career professionals — avoid costly financial blunders:

Navigate your 20s

Perhaps the biggest blunder for young earners is spending too much and saving too little. They may also lack the long-term perspective that encourages long-range planning.

“The mistake is not establishing the saving habit early, and not appreciating the power of compounding” over time, said Mark Kravietz, a certified financial planner in Melville, N.Y.

Similarly, it’s common for young workers to delay enrolling in an employer-sponsored retirement plan. Not participating from the get-go comes with a steep long-term cost.

“ Better to prioritize debt with the highest interest rate, which can result in paying less interest over the long run. ”

People in their 20s process incoming information quickly. But their high level of fluid intelligence can work against them. Cursory research into a consumer trend or hot sector of the stock market can spur them to make rash investments. Such impulsive moves might backfire.

“It’s important to resist the hype,” Kravietz said. “Don’t chase fads or try to make fast money” by timing the market.

Many young adults with student debt juggle multiple loans. Eager to chip away at their debt, they fall into the trap of choosing the wrong loan to tackle first, says Megan Kowalski, an adviser in Boca Raton, Fla.

Rather than pay off the highest-interest rate loan first (so-called avalanche debt), they mistakenly focus on the smallest loan (a.k.a. snowball debt). It’s better to prioritize debt with the highest interest rate, which can result in paying less interest over the long run.

Navigate your 30s

“ Resist the temptation to lower your 401(k) contribution to boost your take-home pay. ”

By your 30s, insurance grows in importance. You want to protect what you have — now and in the future. But many people in this age group neglect their insurance needs. Or they misunderstand which coverages matter most.

“If you have a life partner and kids, get the proper life insurance while in your 30s,” Kravietz said.

It’s easy to get caught up in your career and assume you can put off life insurance. But even low odds of your untimely death doesn’t mean you can ignore the risk of leaving your loved ones without a cash cushion.

Another common blunder involves disability insurance. If your employer offers short-term disability insurance as an employee perk, you may think you’re all set.

However, the real risk is how you’d earn income if you suffer a serious and lasting illness or injury. Don’t confuse short-term disability insurance (which might cover you for as long as one year) with long-term disability coverage that pays benefits for many years.

Assuming you were wise enough to enroll in your employer-sponsored retirement plan from the outset, don’t slough off in your 30s. Resist the temptation to lower your 401(k) contribution to boost your take-home pay.

“You want to give till it hurts,” Kravietz said. “Keep putting money away” in your 401(k) or other tax-advantaged plan until you feel a sting. Weigh the minor pain you feel now against the major relief of having a much bigger nest egg decades from now.

Navigate your 40s

“ ‘The 40s are often the most expensive in anyone’s life. Life is getting more complicated.’”

For Kravietz, the 40s represent a decade of heavy spending pressures. Mid-career professionals face a mortgage and mounting tuition bills for their children.

“The 40s are often the most expensive in anyone’s life,” he said. “Life is getting more complicated.”

As a result, it’s easy to overlook seemingly minor financial matters like updating beneficiaries on your 401(k) plan or completing all the appropriate estate documents such as a will.

“People in their 40s sometimes fail to update beneficiaries,” Kravietz said. For example, a new marriage might mean changing the beneficiary from a prior partner or current parent to the new spouse.

It’s also easy to get complacent about your investments, especially if you’re the conservative type who favors a set-it-and-forget-it strategy. Instead, think in terms of tax optimization.

“In your 40s, you want to take advantage of what the government gives you,” Kravietz said. “If you have a lot of money in a bank money market account and you’re in a top tax bracket, shifting some of that money into municipal bonds can make sense” depending on your state of residence and other factors.

If you’re saving for a child’s college tuition using a 529 plan — and you have parents who also want to chip in — work together to strategize. Don’t make assumptions about how much (or how little) your parents might contribute to your kid’s education.

“Rather than assume you’ll have to pay a certain amount for educational expenses, coordinate between generations of parents and grandparents” on how much they intend to give, Kowalski said. “That way, you’re not duplicating efforts and you won’t put extra funds in a 529 plan.”

But after results from a handful of companies soundly beat estimates in recent days, one analyst who tracks the ebbs and flows of earnings data says at least a slight profit gain for the quarter is more likely — with potentially double-digit percentage growth next year.

FactSet Senior Earnings Analyst John Butters, in a report out Friday, said that of the 32 companies in the S&P 500 Index SPX

that reported third-quarter results through Friday, 84% have reported per-share profits that were above Wall Street’s expectations, and he said they were beating those expectations by a greater degree than usual.

The index collectively, so far, was putting up a third-quarter earnings growth rate of 0.4% — compared to estimates on Oct. 6 for a 0.3% decline. Most companies, he said, tend to turn in earnings results that beat estimates.

“Based on the average improvement in the earnings growth rate during the earnings season, the index will likely report year-over-year growth in earnings or more than 0.4% for Q3,” he said.

That assessment follows quarterly results from big companies like JPMorgan Chase & Co. and Delta Air Lines, Inc.. Both the bank and the airline reported better-than-expected profits. JPMorgan JPM, +1.50%

Chief Executive Jamie Dimon said U.S. consumers and businesses “generally remain healthy,” despite thinning pandemic-era savings, while Delta DAL, -2.99%

pointed to enduring “robust” travel demand.

More broadly, the quarter will be a look at how customers are faring amid still-high prices, an approaching holiday season and borrowing costs that could stay higher for longer. Recession pessimism has shown signs of easing. But Citigroup Inc.’s chief financial officer, Mark Mason, said on Friday that the bank expected a soft economic landing with a “mild recession” in the first half of 2024. However, he said such an outcome was “hard to call,” amid a strong job market.

Financial forecasts tend to fluctuate as analysts digest real-life financial data. For now, they expect S&P 500 index earnings growth of 7.6% for the fourth quarter, and 0.9% for 2023 overall, according to FactSet. Next year, at the moment, looks better, with expected earnings growth of 12.2%.

This week in earnings

More names from the financial sector will report in the week ahead, following results from JPMorgan, Citigroup C, -0.24%

and Wells Fargo & Co. WFC, +3.07%.

Reports from Morgan Stanley MS, -0.03%

and Goldman Sachs Group Inc. GS, -0.18%

will offer more context on deal-making and market sentiment, while earnings from credit-card giants Discover Financial Services DFS, -1.47%

and American Express AXP, -0.12%

will get more granular on customer spending.

More airlines, like United Airlines Holdings Inc. UAL, -2.76%

and American Airlines Group Inc. AAL, -2.82%,

will also report, providing more detail on whether revenge travel still has any life left. Earnings are also due from Johnson & Johnson JNJ, +0.33%

and AT&T Inc. T, -0.62%.

In total 55 S&P 500 companies total will report quarterly results this week, including five from the Dow, according to FactSet.

The call to put on your calendar

Has Netflix become a utility? Hollywood’s writers will start returning to work, while talks with actors and studios have stalled. But the TV-and-film production limbo hasn’t been the only headache for streaming platform Netflix Inc., which reports quarterly results on Wednesday. The company will report amid greater pressure to boost profits, as the entertainment industry tries to find its footing in the streaming era. Ahead of the results, Wolfe Research analyst Peter Supino recently expressed concern that Netflix’s NFLX, -1.53%

ad-supported plan was slow to catch on with viewers. Bernstein analysts likened the company to a mature, durable “utility.” But they also compared the stock to a long-running TV show that, while still good, might be starting to bore its audience. Executives will be hoping for better a better reception from investors.

The number to watch

Tesla margins: When EV maker Tesla Inc. reports results on Wednesday, it will be “all about margins,” Deepwater Asset Management’s Gene Munster said in note recently. Those results, and the focus on margins, will follow price cuts, and questions over profit growth and enthusiasm for Tesla’s TSLA, -2.99%

new Cybertruck. And Morgan Stanley analyst Adam Jonas, in a research note, said the year ahead could be “volatile.”

The volatility in the world’s biggest bond market in recent weeks has been too much for U.S. stocks to handle as investors come to terms with the likelihood that interest rates will remain high deep into 2024 until underlying inflationary pressures ease.

The U.S. Treasury market, the bedrock of the global financial system, has been hammered by repeated selling since late September, sending the yields on the 10-year and 30-year Treasurys to levels last seen when the economy was moving toward the financial crisis in 200, before yields fell again in the past week.

Back in September a bond market selloff was fueled by a hawkish outlook from the Federal Reserve, along with mounting concern about the U.S. fiscal deficit and federal debt amid the potential for a government shutdown if a budget for the 2024 fiscal year is not settled by mid-November.

Earlier this week though, increased uncertainty about the conflict in the Middle East propelled demand for safer assets and caused longer-term bond prices to jump and their yields to fall.

Investors are now wondering what it will take for interest rates and bond yields to fall in the months ahead and whether a retreat in yields could eventually push stocks higher to rally into the year-end.

Tim Hayes, chief global investment strategist at Ned Davis Research, said “excessive pessimism” in the bond market is setting up for a relief rally both in stock and bond prices as “there’s not as much inflationary pressures as the market has been pricing in,” he told MarketWatch in a phone interview on Thursday.

Hayes said his team found the bond sentiment data has started to reflect a “decisive reversal” away from too much pessimism in the Treasury market which could send bond yields lower and boost equities given the inverse correlations between the S&P 500 SPX

and the 10-year Treasury note yield BX:TMUBMUSD10Y.

Meanwhile, some analysts said disinflation may not be enough for the Federal Reserve to drop its “higher-for-longer” interest rate narrative which was primarily responsible for the big spike in yields since September.

The economy needs a slowdown in the consumer sector for some relaxation in the Fed’s “higher-for-longer” narrative and to maybe push policymakers to adopt a more flexible outlook for its long-term guidance, said Thierry Wizman, global FX and interest rates strategist at Macquarie.

“Of course, the Fed right now is certainly not saying anything that’s remotely suggestive of ‘high-for-long’ being taken away or being removed or negated, so I don’t expect yields to fall a lot unless we start to get reasons to believe the Fed is going to remove that narrative based on the economic data,” Wizman told MarketWatch via phone.

However, Wizman said he is confident that the U.S. consumption data will weaken over the next few months when major consumer-product and -service companies start to provide guidance for the fourth quarter, and when U.S. consumers, which have been trapped in a web of conflicting signals on the health of the economy, open their wallet for the holiday shopping season.

“This will produce some weakness on the consumer side of the market and there’s no doubt the slowdown will be more pronounced than most people expect in the economy, [but] that will be the positive scenario for bonds,” said Marco Pirondini, head of U.S. equities at Amundi U.S., in an interview with MarketWatch.

However, that also means investors should not be “too anxious to buy dips in the stock market” because it would be very unusual if the stock market doesn’t see “multiple compression” with Treasury yields at 16-year highs, Wizman said. “Stocks would still look too rich even if the Fed drops the ‘higher-for-longer’ narrative in the first quarter of 2024.”

The “higher-for-longer” mantra is an idea Fed officials have tried to get the market to absorb in recent months, with Fed Chair Powell hardening his rhetoric at the September FOMC meeting, pointing potentially to more rate hikes or, more importantly, interest rates that stay higher for longer.

Fed officials saw interest rates coming down to 5.1% in 2024, higher than June’s outlook for rates to finish next year at 4.6%, according to the latest Summary of Economic Projections at the September policy meeting.

However, Wizman characterized the “higher-than-longer” narrative as a “publicity stunt,” as he thought Fed officials simply wanted to signal to the market that they were frustrated that financial conditions hadn’t measurably tightened enough in 2023, so they utilized the narrative to get rising Treasury yields to do some of the “heavy lifting.”

“… Fed officials are not really serious about ‘higher-for-longer’ – they just did it to drive long-term yields higher for now,” he added.

If a slowdown in the consumer sector of the economy and ongoing disinflation are powerful enough to sap Fed’s rate expectations, Treasury yields could continue to decline without having to have a calamity or big recession in the U.S. economy to drive investors back to the safe-haven assets like Treasurys, strategists said.

Meanwhile, stock-market seasonality may also help lift sentiment. Historically, the fourth quarter has been the best quarter for the U.S. stock market, with the large-cap S&P 500 index up nearly 80% of the time dating back to 1950 and gaining more than 4% on average.

The S&P 500 has risen 0.9% so far in the fourth quarter, while the Dow Jones Industrial Average DJIA

is up 0.5% and the Nasdaq Composite COMP

has advanced 1.4% in October, according to FactSet data.

“So you have this situation where sentiment got stretched and now sentiment is reversing with more confidence that bond yields have reached their peak, so equities can rally moving into the end of the year, and that should start to become increasingly evident,” said Hayes.

The yield on the 10-year Treasury note dropped 8.2 basis points to 4.628% on Friday, while the yield on the 30-year Treasury BX:TMUBMUSD30Y

declined by 9.2 basis points to 4.777%. The 30-year yield fell 16.4 basis points this week, its largest weekly drop since the period that ended March 10, according to Dow Jones Market Data.

Financial literacy peaks at age 54, according to a 2022 study. That’s around the time you’ve gained enough knowledge and experience to make sound money decisions — and before your cognitive ability might start to ebb.

“As we get older, we seem to rely more on past experience, rules of thumb, and intuitive knowledge about which products and strategies are better,” said Rafal Chomik, an economist in Australia who led the study.

If people in their mid-50s tend to make smart financial moves, where does that leave younger generations?

Advisers often educate clients at different stages of life to avoid money mistakes. While those in their 50s usually demonstrate optimal prudence in navigating investments and savings, advisers keep busy helping others — from twentysomethings to mid-career professionals — avoid costly financial blunders:

Navigate your 20s

Perhaps the biggest blunder for young earners is spending too much and saving too little. They may also lack the long-term perspective that encourages long-range planning.

“The mistake is not establishing the saving habit early, and not appreciating the power of compounding” over time, said Mark Kravietz, a certified financial planner in Melville, N.Y.

Similarly, it’s common for young workers to delay enrolling in an employer-sponsored retirement plan. Not participating from the get-go comes with a steep long-term cost.

“ Better to prioritize debt with the highest interest rate, which can result in paying less interest over the long run. ”

People in their 20s process incoming information quickly. But their high level of fluid intelligence can work against them. Cursory research into a consumer trend or hot sector of the stock market can spur them to make rash investments. Such impulsive moves might backfire.

“It’s important to resist the hype,” Kravietz said. “Don’t chase fads or try to make fast money” by timing the market.

Many young adults with student debt juggle multiple loans. Eager to chip away at their debt, they fall into the trap of choosing the wrong loan to tackle first, says Megan Kowalski, an adviser in Boca Raton, Fla.

Rather than pay off the highest-interest rate loan first (so-called avalanche debt), they mistakenly focus on the smallest loan (a.k.a. snowball debt). It’s better to prioritize debt with the highest interest rate, which can result in paying less interest over the long run.

Navigate your 30s

“ Resist the temptation to lower your 401(k) contribution to boost your take-home pay. ”

By your 30s, insurance grows in importance. You want to protect what you have — now and in the future. But many people in this age group neglect their insurance needs. Or they misunderstand which coverages matter most.

“If you have a life partner and kids, get the proper life insurance while in your 30s,” Kravietz said.

It’s easy to get caught up in your career and assume you can put off life insurance. But even low odds of your untimely death doesn’t mean you can ignore the risk of leaving your loved ones without a cash cushion.

Another common blunder involves disability insurance. If your employer offers short-term disability insurance as an employee perk, you may think you’re all set.

However, the real risk is how you’d earn income if you suffer a serious and lasting illness or injury. Don’t confuse short-term disability insurance (which might cover you for as long as one year) with long-term disability coverage that pays benefits for many years.

Assuming you were wise enough to enroll in your employer-sponsored retirement plan from the outset, don’t slough off in your 30s. Resist the temptation to lower your 401(k) contribution to boost your take-home pay.

“You want to give till it hurts,” Kravietz said. “Keep putting money away” in your 401(k) or other tax-advantaged plan until you feel a sting. Weigh the minor pain you feel now against the major relief of having a much bigger nest egg decades from now.

Navigate your 40s

“ ‘The 40s are often the most expensive in anyone’s life. Life is getting more complicated.’”

For Kravietz, the 40s represent a decade of heavy spending pressures. Mid-career professionals face a mortgage and mounting tuition bills for their children.

“The 40s are often the most expensive in anyone’s life,” he said. “Life is getting more complicated.”

As a result, it’s easy to overlook seemingly minor financial matters like updating beneficiaries on your 401(k) plan or completing all the appropriate estate documents such as a will.

“People in their 40s sometimes fail to update beneficiaries,” Kravietz said. For example, a new marriage might mean changing the beneficiary from a prior partner or current parent to the new spouse.

It’s also easy to get complacent about your investments, especially if you’re the conservative type who favors a set-it-and-forget-it strategy. Instead, think in terms of tax optimization.

“In your 40s, you want to take advantage of what the government gives you,” Kravietz said. “If you have a lot of money in a bank money market account and you’re in a top tax bracket, shifting some of that money into municipal bonds can make sense” depending on your state of residence and other factors.

If you’re saving for a child’s college tuition using a 529 plan — and you have parents who also want to chip in — work together to strategize. Don’t make assumptions about how much (or how little) your parents might contribute to your kid’s education.

“Rather than assume you’ll have to pay a certain amount for educational expenses, coordinate between generations of parents and grandparents” on how much they intend to give, Kowalski said. “That way, you’re not duplicating efforts and you won’t put extra funds in a 529 plan.”

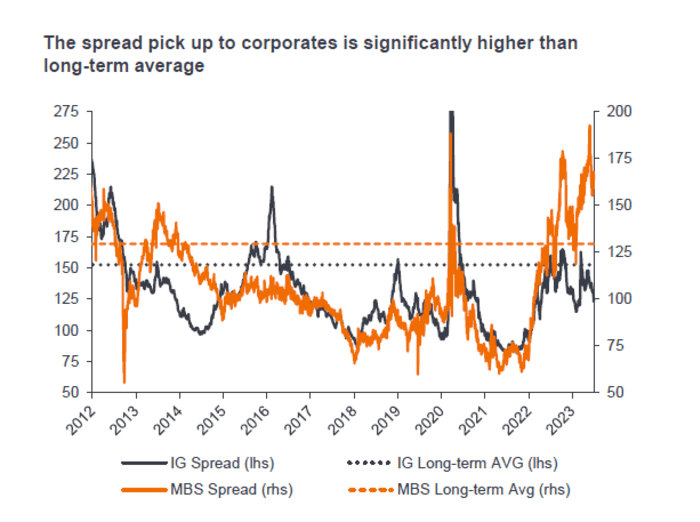

U.S. homes may be wildly unaffordable for first-time buyers, but mortgage bonds backed by those same properties could be dirt cheap.

Shocks from the Federal Reserve’s dramatic rate increases have walloped the $8.9 trillion agency mortgage-bond market, the main artery of U.S. housing finance for almost the past two decades.

Spreads, or compensation for investors, have hit historically wide levels, even through the sector is underpinned by home loans that adhere to the stricter government standards set in the wake of the subprime-mortgage crisis.

Bond prices also have tumbled, sinking from a peak above 106 cents on the dollar to below 98, despite guarantees that mean investors will be fully repaid at 100 cents on the dollar.

From $106 to $98 cents, agency mortgage-bond prices are falling.

Bloomberg, Goldman Sachs Global Investment Research

“It’s really, really struggled,” Nick Childs, portfolio manager at Janus Henderson Investors, said of the agency mortgage-bond market during a Thursday talk on the firm’s fixed-income outlook.

Yet Childs and other investors also see big opportunities brewing. While mortgage bonds have gotten cheaper with the sector’s two anchor investors on the sidelines, the stalled housing market should breed scarcity in the bonds, which could help lift the sector out of a roughly two-year slump.

Prices have tumbled since rate shocks hit, but also since the Fed continued winding down its large footprint in the sector by letting bonds it accumulated to help shore up the economy roll off its balance sheet.

“Banks have been not only absent, but selling,” said Childs, who helps oversee the Janus Henderson Mortgage-Backed Securities exchange-traded fund JMBS,

an actively managed $2 billion fund focused on highly rated securities with minimal credit risk.

“But we’re moving into an environment where supply continues to dwindle,” he said, given anemic refinancing activity and the dearth of new home loans being originated since 30-year fixed mortgage rates topped 7%.

The bulk of all U.S. mortgage bonds created in the past two decades have come from housing giants Freddie Mac FMCC, +0.66%,

Fannie Mae FNMA, +1.09%

and Ginnie Mae, with government guarantees, making the sector akin to the $25 trillion Treasury market. But unlike investors in Treasurys, investors in mortgage bonds also earn a spread, or extra compensation above the risk-free rate, to help offset its biggest risk: early repayments.

While homeowners typically take out 30-year loans, most also refinanced during the pandemic rush to lock in ultralow rates, instead of continuing to make three decades of payments on more expensive mortgages. If someone refinances, sells or defaults on a home, it leads to repayment uncertainty for bond investors.

“To put this another way, the biggest risk to mortgages is now off the table, yet spreads are at or near historic wides,” said Sam Dunlap, chief investment officer, Angel Oak Capital Advisors, in a new client note.

That spread is now far above the long-term average, topping levels offered by relatively low-risk investment-grade corporate bonds.

Agency mortgage bonds are offering far more spread that investment-grade corporate bonds. But these mortgage bonds will fully repay if borrowers default.

Janus Henderson Investors

Agency mortgage bonds typically are included in low-risk bond funds and can be found in exchange-traded funds. While they have been hard hit by the sharp selloff in long-dated Treasury bonds BX:TMUBMUSD10Y

BX:TMUBMUSD30Y,

there has also been hope that the worst of the storm could be nearly over.

Goldman Sachs credit analysts recently said they favored the sector but warned in a weekly client note that it still faces “high rate volatility and a dearth of institutional demand.”

As evidence of the U.S. bond selloff, the popular iShares 20+ Year Treasury Bond ETF TLT

recently sank to its lowest level in more than a decade. It also was on pace for a negative 10% total return on the year so far, according to FactSet. Janus Henderson’s JMBS ETF was on pace for a negative 2.7% total return on the year through Friday.

“Frankly, why they fit portfolios so well is that because the government backs agency mortgages, there is no credit risk,” Childs said. “So if a borrower defaults, you get par back on that. It just comes through as a typical payment.”