The numbers: Consumer sentiment soured in November, hitting its lowest level since July as Americans contended with continued inflation and a worsening economic outlook.

The University of Michigan’s gauge of the U.S. consumer’s outlook fell 5.2 index points from 59.9 in October.

Economists were expecting a reading of 59.5, according to a Wall Street Journal poll.

Inflation expectations for the next year rose to 5.1% from 5% in the prior month, while five-year inflation expectations rose to 3% from 2.9% in October.

Big picture: Inflation eased somewhat in October, but prices for a typical basket of consumer goods are still rising a historically rapid pace even as rising interests rates are weighing on many sectors of the economy.

Fears of a coming recession also weighed on Americans’ confidence about the economy.

“Declines in sentiment were observed across the distribution of age, education, income, geography, and political affiliation, showing that the recent improvements in sentiment were tentative,” wrote Joanne Hsu, director of the survey, in a statement. “Instability in sentiment is likely to continue, a reflection of uncertainty over both global factors and the eventual outcomes of the election.”

Key details: A gauge of consumer’s views of current conditions fell in November to 57.8 from 65.6 in October, while an indicator of expectations for the next six months fell to 52.7 from 56.2 last month.

Market reaction: U.S. stocks were trading mixed Friday morning, with the S&P 500 SPX, +0.92%

posting gains and the Dow Jones Industrial Average DJIA, +0.10%

edging lower.

That means a full day of trading for stocks, which appear poised to book a robust week of gains, despite continued fears of a potential U.S. economic recession as the Federal Reserve works to tame stubbornly high costs of living.

While Friday marks the start of a three-day weekend for the bond market, Treasury yields already have climbed dramatically this year with the Fed’s sharp rate hikes. The central bank aims to temper demand for goods and services by making borrowing costs more restrictive.

Consumers may feel certain effects of inflation in their everyday lives, like when they go to the grocery store. But it can also impact our savings and investments. Here’s what to know.

The benchmark 10-year Treasury rate TMUBMUSD10Y, 3.819%

fell to about 3.8% on Thursday, but was up from a 1.3% low last December. Bond yields move in the opposite direction of prices.

The fresh rally on Wall Street followed the consumer-price index reading for October showing a 7.7% annual rate, down from a 9.1% high in June. The Dow remains down more than 8% from its January peak, the S&P 500 is 17.5% lower and the Nasdaq is 31% below its last record close, according to Dow Jones Market Data.

Shares of Chinese travel and consumer companies gained ground in Hong Kong after Beijing eased some Covid-19 restrictions, improving the outlook for sectors directly hit by the pandemic and the broader economic recovery.

In Friday afternoon trade, the Hang Seng China Enterprises Index 160462, +7.98%

advanced 7.6%, while the city’s benchmark Hang Seng Index HSI, +7.51%

jumped 7.1% to 17221.43, recovering to levels last seen a month ago. The benchmark index would mark its largest one-day gain since mid-March if it closes at current levels.

China’s three major airlines, Air China Ltd. 601111, -3.11%,

China Southern Airlines Co. 600029, +0.13%

and China Eastern Airlines Corp. 600115, +1.14%,

added between 2.2% and 5.1%, while travel retailer China Tourism Group Duty Free Corp. 601888, +3.65%

climbed 7.1%.

Broader consumer-related sectors also strengthened, amid hopes that less stringent rules could help revive consumption. E-commerce platforms Alibaba Group Holding Ltd. BABA, +7.60%

9618, +16.22%

jumped 11% and 16%, respectively, while restaurant operator Haidilao International Holding Ltd. 6862, +5.21%

climbed 4.7%.

China said Friday that it will shorten the quarantine period for close contacts of COVID cases and travelers to the country, among other policy tweaks. But the government also said it will stick to its zero-COVID policy.

Friday’s market upturn came on the back of U.S. stocks’ biggest rally in two years, after October inflation data was weaker than expected, lifting expectations of less aggressive interest-rate increases by the Federal Reserve.

Crypto lending platform BlockFi announced it was halting withdrawals Thursday night in the wake of the collapse of crypto exchange FTX.

“We are shocked and dismayed by the news regarding FTX and Alameda,” BlockFi said in a tweet. “We, like the rest of the world, found out about this situation through Twitter.”

BlockFi said that due to the “lack of clarity” regarding FTX and Alameda, “we are not able to operate business as usual,” and that until there is “further clarity, we are limiting platform activity, including pausing client withdrawals.”

The company asked clients not to deposit into BlockFi Wallet or Interest Accounts at this time, and said it will share more specifics “as soon as possible,” though it warned it likely would communicate “less frequently” than what its clients and stakeholders are used to.

FTX founder and CEO Sam Bankman-Fried reportedly extended about $10 billion in loans to its affiliated trading firm Alameda Research — amounting to about half of FTX’s customer assets of $16 billion, according to the Wall Street Journal.

“I fucked up, and should have done better,” Bankman-Fried said in a tweet Thursday, saying he had, among other things, misread the use of margin on the platform.

The FTX fiasco has spread fear of a “contagion” across the broader crypto industry, and sent the price of bitcoin BTCUSD, -3.87%

at one point to its lowest level since November 2020.

Just six months ago, CEOs, celebs and world leaders like Bill Clinton and Tony Blair flocked to him, gathering at a Davos-like conference he hosted in the Bahamas where he lives as one of the most outspoken evangelists for the power of the blockchain.

Fast forward to Sunday and Bankman-Fried’s crypto empire came crashing down, the victim of an old-fashioned bank run that quickly exposed the weaknesses of the new finance system he had championed.

Almost overnight, Bankman-Fried’s cryptocurrency exchange, FTX, had gone from being valued at $32 billion to worthless, leaving scores of investors scrambling to get their deposits back and triggering probes in the U.S. by the Securities and Exchange Commission, the Commodities Futures Trading Commission and the Department of Justice, according to reports.

On Thursday, the 30-year-old Bankman-Fried took to Twitter to level with his clients.

“I fucked up, and should have done better,” he wrote.

A very rapid rise

It took less than five years for Bankman-Fried to build a personal fortune that was estimated at its highest point to be more than $26 billion, making him among the richest people in the world.

His schlubby, boyish appearance — ill-fitting t-shirts, gym shorts and a mop of curly hair — made him look more like a college student ripping bong hits in the basement of a frat house than a finance guru, but fit nicely with the anti-establishment ethos that appealed to crypto enthusiasts.

The son of law professors at Stanford University, Bankman-Fried was a wunderkind from an early age. He studied physics and mathematics at the Massachusetts Institute of Technology.

After a stint as an ETF trader for Jane Street Capital, a highly respected Wall Street firm that is known for attracting genius quantitative traders, Bankman-Fried became interested in the concept of effective altruism, a philosophy that focuses on using reason and evidence to find solutions that benefit the most people possible. In 2017, he launched Alameda Research, a quantitative trading firm focused on digital currencies.

Over the next year, he began building his fortune through arbitrage trading of Bitcoin BTCUSD, +11.10%

between exchanges in the U.S. and Japan, where prices were often slightly higher. In 2019, Bankman-Fried launched the crypto exchange FTX.

The timing was fortuitous: as the COVID-19 pandemic spread across the globe the following year, interest in cryptocurrencies among people exploded. FTX took off and brought in the big-name celebrity endorsers and partners, like professional athletes Tom Brady and Steph Curry.

Bankman-Fried soon found himself feted by some of the biggest institutions in finance, attracting investment from the biggest names on Wall Street and beyond like Softbank 9984, -2.65%

Group, Sequoia Capital, Blackrock BLK, +13.26%.

Tiger Global Management and Thoma Bravo. He even raised money from billionaire hedge fund legends Paul Tudor Jones and Israel Englander.

Soon, FTX was among the biggest players in the industry.

The face of crypto

Despite his ballooning wealth, Bankman-Fried maintained the appearance and lifestyle of a teenage gamer. He moved to the Bahamas, where he reportedly lived in a penthouse apartment with 10 roommates.

On Zoom calls, he would often play video games while talking — his favorite game being League of Legends. Profiles of him often noted that he kept a bean bag just feet from his desk to sleep on.

What set Bankman-Fried apart from other crypto tycoons, was his professed interest in working with regulators to create a more robust framework around the nascent industry and treat it more like a traditional finance network.

To that end, Bankman-Fried appeared before Congress to try to explain to skeptical U.S. lawmakers how the crypto industry worked. He also said he welcomed regulation, not always a popular position in the crypto world.

“FTX believes [government agencies] could play an even more prominent role in the digital-asset ecosystem and bring greater investor protections by closing some regulatory gaps,” he said before a senate panel in February. “FTX believes that such efforts would combine the best aspects of traditional finance and digital-asset innovations.”

Bankman-Fried even put his great wealth to play in politics, becoming a major campaign donor for the Democratic party. In 2020, he was one of President Joe Biden’s largest single donors and spent nearly $40 million on political campaigns this year for the midterm elections, according to campaign filings.

As cryptocurrencies have experienced significant declines in prices this year, triggering the collapse of several operations, Bankman-Fried arose as a savior, buying up several failing partners as positioning himself as a kind of Robin Hood for the industry.

A swift collapse

For as fast a rise to the top of the world that Bankman-Fried enjoyed, the fall was just as rapid.

On Sunday, Changpeng Zhao, the CEO of FTX’s competitor, Binance, and an archrival of Bankman-Fried’s, announced on Twitter that his firm, the world’s biggest cryptocurrency exchange, was liquidating its sizable holdings of FTT, the coin issued by FTX, “due to recent revelations that have come to light.”

Bankman-Fried accused Zhao of spreading false rumors. But the damage was done.

Binance’s move triggered a massive selloff with customers seeking to redeem some $5 billion in deposits. FTX didn’t have it and redemptions froze up.

On Tuesday, Bankman-Fried announced that FTX had reached a tentative agreement to be acquired by Binance, due to a “significant liquidity crunch.” The turmoil set off broad declines among several of the most popular cryptocurrencies and even spilled into the world of traditional finance, sending markets tumbling.

The next day, the chaos increased, with reports that FTX and Bankman-Fried were under investigation by several U.S. agencies. By the end of the day, Binance said it was walking away from the deal because due diligence had revealed that “the issues are beyond our control or ability to help.”

Binance’s deal seemed like the only thing preventing FTX from potentially collapsing. “At some point I might have more to say about a particular sparring partner,” Bankman-Fried tweeted on Thursday. “For now, all I’ll say is: well played; you won.”

Also on Thursday, the Wall Street Journal reported that Bankman-Fried had been using some customer deposits to fund risky bets by his Alameda Research firm, setting FTX up for collapse.

With the Binance lifeline gone and with few options available, Bankman-Fried told investors he needed $8 billion or more to plug the hole in FTX’s books, according to reports.

On Twitter, Bankman-Fried said he would focus all his efforts on making sure depositors got their money back. He also tried to explain FTX’s collapse, saying “a poor internal labeling of bank-related accounts meant that I was substantially off on my sense of users’ margin. I thought it was way lower.”

Said Bankman-Fried: “My #1 priority–by far–is doing right by users,” he wrote. “Right now, we’re spending the week doing everything we can to raise liquidity. I can’t make any promises about that.”

Binance, the world’s largest crypto exchange, is abandoning its proposed acquisition of the non-U.S. assets of rival FTX, amid the latter’s liquidity crunch.

“As a result of corporate due diligence, as well as the latest news reports regarding mishandled customer funds and alleged US agency investigations, we have decided that we will not pursue the potential acquisition of FTX.com,” according to a tweet by Binance’s official account Wednesday.

“Our hope was to be able to support FTX’s customers to provide liquidity, but the issues are beyond our control or ability to help,” Binance wrote.

Executives at Binance have found a gap, likely in billions and possibly more than $6 billion, between the liabilities and assets of FTX, Bloomberg reported Wednesday, citing an anonymous source familiar with the matter.

Representatives at Binance and FTX didn’t immediately respond to a request seeking comments.

On Tuesday, Changpeng Zhao, Binance’s chief executive, said the exchange had signed a letter of intent to acquire FTX.com, a separate entity from FTX.US, after FTX “asked for help.”

Investors are worried about any contagion, as concerns over FTX’s solvency spilled over to the already battered crypto market. BitcoinBTCUSD plunged Wednesday to as low as $16,863, the lowest level since November 2020.

FTX is the third largest crypto exchange by trading volume, according to CoinMarketCap.

Oil hasn’t yet climbed back to $100 per barrel, but options traders are increasingly setting their sights on another target—$200. The most actively traded

Brent crude

options contract on Thursday was an option to buy Brent at $200 in March 2023.

About half of the contracts to buy oil at that price appeared to be placed by one buyer who spent about $810,000 on the options, according to Robert Yawger, the director of energy futures at Mizuho Securities USA. But that buyer isn’t the only person making a bet that oil prices will hit $200, along with other bullish bets on where oil goes in 2023. “There have been people dipping their toes into those higher [options strike prices] over the last couple of days,” Yawger said.

Shares of Apple Inc. and Alphabet Inc. both suffered their largest weekly declines since the beginning days of the pandemic this week, as Big Tech companies continued to draw closer scrutiny from Wall Street.

Apple’s stock AAPL, -0.19%

finished down 11.2% on the week, its worst weekly performance since the week that ended March 20, 2020, according to Dow Jones Market Data. The stock declined 17.5% during that early-pandemic stretch.

Shares of Apple fell during all five sessions this week.

GOOGL, +3.78%

declined 10.1% during the week, their worst one-day percentage drop since that same March 20, 2020 week, when they fell 12.03%. The stock’s biggest weekly tumble in more than two years came even as Alphabet snapped a four-session losing streak in Friday trading.

While Apple’s stock has fared better than that of Alphabet and other Big Tech peers, the company faces potential pandemic-related challenges owing to new COVID-19 setbacks at manufacturer Foxconn’s major facility. In addition, the realities of the current economic climate may be catching up to Apple, as Bloomberg News reported Thursday that the company had paused hiring in several areas unrelated to research and development.

Though there didn’t seem to be any major news developments pegged to Alphabet specifically in the past week, investors are putting more pressure on big internet companies, according to Bernstein analyst Mark Shmulik. He recently conducted a Big Tech “autopsy” of results from Alphabet, Amazon.com Inc. AMZN, +1.88%,

and Meta Platforms Inc. META, +2.11%,

concluding that “perfection is required from here” for the three tech giants since Wall Street has less patience for weak performance in any one of their many business areas.

All three names suffered negative stock reactions in the wake of their latest earnings reports, which indicated challenges in the ad market due to economic pressures. At Alphabet specifically, “Search was more or less in-line with the buy-side bogey and the Cloud beat, but disappointing YouTube results combined with margin contraction drove a ~10% fall after-hours,” Shmulik wrote.

Alphabet’s stock has declined 40% so far in 2022, while Apple’s is off 22% over the same span. The S&P 500 SPX, +1.36%

is down 21% on the year while the Dow Jones Industrial Average DJIA, +1.26%

is off 11%.

The numbers: The economy gained surprisingly strong 261,000 new jobs in October, underscoring the persistent strength of a labor market that the Federal Reserve worries will exacerbate high inflation.

Economists polled by The Wall Street Journal had forecast 205,000 new jobs.

The unemployment rate, meanwhile, rose to 3.7% from 3.5%, the government said Friday, as more people lost jobs and the size of the labor force shrank a little bit.

Fed Chairman Jerome Powell said on Wednesday the labor market is “out of balance” because there’s too many job openings and too few people to fill them.

Fed officials worry the labor shortage is driving up wages and making it harder for them to reduce inflation back to precrisis levels of 2% or so. The cost of living has risen 8.2% in the past year, one of the highest increases since the early 1980s.

Layoffs and unemployment are likely to increase, however, if the Fed keeps raising U.S. interest rates as expected. The central bank could push a key short-term rate to as high as 5% by next year from near zero just nine months ago.

Rising interest rates slow the economy and sometimes trigger recessions. Many economists predict a downturn is likely by next year. Powell himself admitted the odds of avoiding a recession have fallen due to persistently high inflation.

In October, wages grew 0.4%. Average hourly pay rose slightly in September to $32.58, lowering the increase over the past year to 4.7% from 5%.

It’s the first time in almost a year that the rate of wage growth has dropped below 5%. Before the pandemic, they were rising around 3% a year.

Another potential pressure valve for the economy showed little progress, however. The so-called participation rate — or share of working-age people in the labor force — dipped to 62.2% from 62.3%.

Big picture: The economy is slowing — almost every major indicator is much softer compared to earlier in the year.

The labor market is one of the few exceptions.

Normally that’s a good thing, but the Fed thinks the the labor market is too strong for its own good. The series of rate hikes undertaken by the central bank is bound to slow hiring even further and cause unemployment to rise in the months ahead.

The potential saving grace, Powell and some other economists say? Businesses have struggled so hard to hire people amid a labor shortage that they might not lay off as many people as they usually do when the economy goes sour.

Market reaction: The Dow Jones Industrial Average DJIA, -0.46%

and S&P 500 SPX, -1.06%

were set to open lower in Friday trades. The yield on the 10-year Treasury note TMUBMUSD10Y, 4.158%

rose to 4.19%.

Coinbase Global Inc. late Thursday reported a wider quarterly loss and a 54% drop in revenue, saying the headwinds for its business will continue and likely intensify next year.

Coinbase COIN, -8.09%

said it lost $545 million, or $2.43 a share, in the quarter, swinging from earnings of $406 million, or $1.62 a share, in the year-ago period.

Revenue dropped to $576 million from $1.24 billion a year ago.

Analysts surveyed by FactSet expected the crypto exchange to report a loss of $2.38 a share on revenue of $641 million.

Shares traded lower immediately after the report, but at last check were rising more than 8% in the extended session.

The quarter was “mixed” for Coinbase, the company said in a letter to shareholders. “Transaction revenue was significantly impacted by stronger macroeconomic and crypto market headwinds, as well as trading volume moving offshore.”

On the plus side, Coinbase saw “strong growth in our subscription and services revenue,” it said.

Those headwinds, however, continued to impact transaction revenue, which was down 44% quarter on quarter, Coinbase said in the letter.

Trading volume dropped to $159 billion in the quarter from $217 billion in the second quarter.

“For 2022, we remain cautiously optimistic that we will operate within the $500 million adjusted EBITDA loss guardrail that we previously communicated,” the company said. That assumes that the crypto market does not deteriorate further, it said.

For next year, however, Coinbase is “preparing with a conservative bias and assuming that the current macroeconomic headwinds will persist and possibly intensify,” the company said.

How good is a company’s chief executive officer at investing your money most efficiently? This is an important question for long-term investors. It may underline the difference between a steady long-term performer and a flash in the pan.

And Apple Inc. AAPL, -4.24%

now makes up 7% of the SPDR S&P 500 ETF Trust SPY, -1.03%,

the first and largest exchange-traded fund (with $360 billion in assets), which tracks the benchmark S&P 500 SPX, -1.06%.

That’s close to an all-time record, and the iPhone maker has a whopping 14.1% position in the Invesco QQQ Trust QQQ, -1.95%,

which tracks the Nasdaq-100 Index NDX, -1.98%.

Looking at the full Nasdaq Index COMP, -1.73%,

which has 3,747 stocks, Apple takes a 13.5% position.

Apple now makes up 7.3% of the S&P 500 by market capitalization, close to the 8% record it set late in September.

FactSet

This is very much an Apple stock market, with the company topping the broad indexes that are weighted by market capitalization. You are likely to be invested in the company indirectly. You also might be feeling Apple’s impact in other ways. Apple’s App Store ecosystem drives more than $600 billion in annual revenue for developers.

Tim Cook’s tenure as Apple’s CEO has been nothing short of breathtaking when measured by the company’s financial performance. Apple is not one of the fastest-growing companies when measured by sales or earnings — it is too big for that. But its excellent stock performance has reflected Cook’s ability to deploy invested capital with improving efficiency. Cook has also been a market trendsetter in other important ways. He has Apple repurchasing $90 billion of its shares annually, setting the pace for stock buybacks in the market. Cook’s steady hand has also helped Apple withstand the market’s tech wreck and remain a stable pillar for the teetering Nasdaq Composite index generally. For all these reasons, Cook has earned a spot on the MarketWatch 50 list of the most influential people in markets.

Apple keeps improving by this important measure

Investors in the stock market are looking for growth over the long term. The best measure of that is whether or not a company’s share price goes up or down. But Cook isn’t just managing Apple’s stock. Digging a bit deeper into the company’s actual operating performance can provide some insight into what a good job Cook has done.

What should a corporate manager focus on? The stock price? How about the most efficient and most profitable way to provide goods and services? There are different ways to do this, and Apple has focused on quality, reliability and excellent service to build customer loyalty.

Apple’s commitment can be experienced by anyone who calls the company for customer service. It is easy to get through to a well-trained representative who will solve your problem. How many companies can say that at a time when it seems many companies cannot even handle answering the phone?

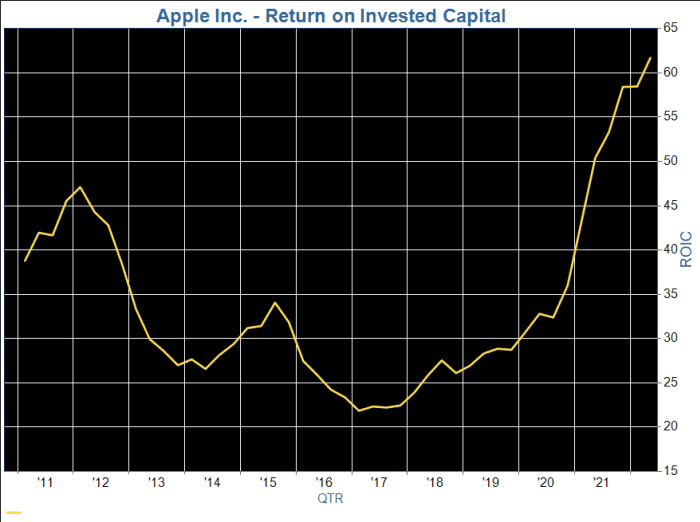

Apple’s returns on invested capital have increased markedly over the past six years.

FactSet

A company’s return on invested capital (ROIC) is its profit divided by the sum of the carrying value of its common stock, preferred stock, long-term debt and capitalized lease obligations. ROIC indicates how well a company has made use of the money it has raised to run its business. It is an annualized figure, but available quarterly, as used in the chart above.

The carrying value of a company’s stock may be a lot lower than its current market capitalization. The company may have issued most of its shares long ago at a much lower share price than the current one. If a company has issued shares recently or at relatively high prices, its ROIC will be lower.

A company with a high ROIC is likely either to have a relatively low level of long-term debt or to have made efficient use of the borrowed money.

Among companies in the S&P 500 that have been around for at least 10 years, Apple placed within the top 20 for average ROIC for the previous 40 reported fiscal quarters as of Sept. 1.

As you can see on the chart, Apple’s ROIC has improved dramatically over the past five years, even as the wide adoption of the company’s products and services has led to an overall slowdown in sales growth.

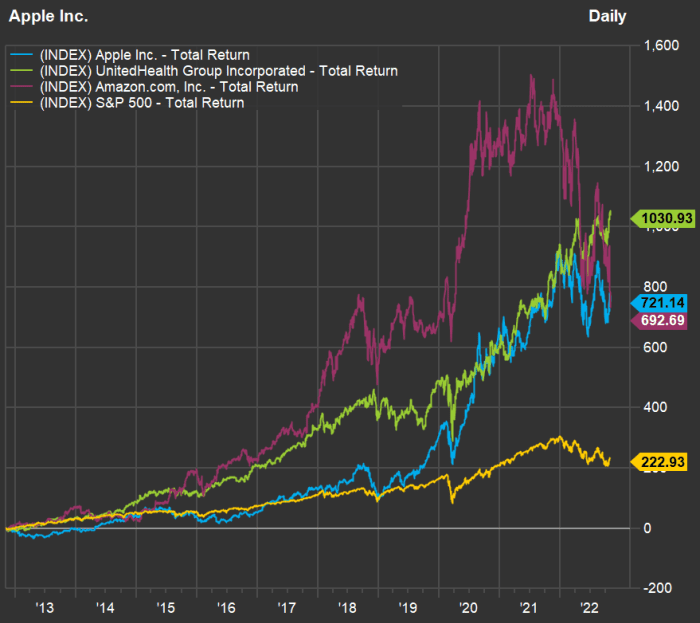

A quick comparison with other giants in the benchmark index

It might be interesting to see how Apple stacks up among other large companies, in part because some businesses are more capital-intensive than others. For example, over the past four quarters, Apple’s ROIC has averaged 52.9%, while the average for the S&P 500 has been a weighted 12.1%, by FactSet’s estimate.

Here are the 10 companies in the S&P 500 reporting the highest annual sales for their most recent full fiscal years, with a comparison of average ROIC over the past 40 reported quarters:

Among the largest 10 companies in the S&P 500 by annual sales, Apple takes the top ranking for average ROIC over the past 10 years, while ranking second for total return behind UnitedHealth Group Inc. UNH, +0.03%

and ahead of Amazon.com Inc. AMZN, -3.06%.

UnitedHealth has been able to remain at the forefront of managed care during the period of transition for healthcare in the U.S., in the wake of President Barack Obama’s signing of the Affordable Care Act into law in 2010.

Here’s a chart showing 10-year total returns for Apple, UnitedHealth Group, Amazon and the S&P 500:

FactSet

Apple is only slightly ahead of Amazon’s 10-year total return. But what is so striking about this chart is the volatility. Apple has had a smoother ride. During the bear market of 2022, Apple’s stock has declined 18%, while the S&P 500 has gone down 20%, the Nasdaq has fallen 32% (all with dividends reinvested) and Amazon has dropped 45%.

The broad indexes would have fared even worse so far this year without Apple.

Vicki Hollub’s Occidental Petroleum controls the biggest piece of the most important area for oil production in the United States. Not so long ago, an oilman in a position like that—and it would’ve been a man, before Hollub came along—would have gone for broke, turning up production to its physical limits.

Not Hollub. Occidental produces on average the equivalent of about 1.15 million barrels of oil a day, and that’s more than enough to turn a profit. The company can make money as long as oil prices are above $40 a barrel. They’ve been above $80 for almost all of this year, as the war in Ukraine takes a toll on global markets and the Saudi-led oil cartel OPEC now slashes production.

“We don’t feel like we’re in a national crisis right now,” Hollub told MarketWatch in an interview. And that means Hollub can keep executing on her plans: making shareholders happy by paying down debt and buying back shares. “When you have such a low break-even, to me there’s no pressure to increase production right now, when we have these other two ways that we can increase shareholder value,” Hollub said.

That market-focused logic puts her at odds with President Biden, who is acting like there is a national energy crisis ongoingprecisely because of what oil CEOs like Hollub are doing. The size of oil companies’ profits is outrageous, Biden said Monday. They’re raking in cash not because of innovation or investment but as a windfall from the war in Ukraine, Biden said. “Rather than increasing their investments in America or giving American consumers a break, their excess profits are going back to their shareholders and to buying back their stock, so the executive pay is — are going to skyrocket,” Biden said. He has ordered releases from the Strategic Petroleum Reserve to keep down gas prices and asked Congress to tax oil-company profits.

But Hollub is single-mindedly focused on seizing the moment to improve the company’s financial position. Occidental still has significant debt left over from a challenging acquisition Hollub spearheaded before the pandemic. In the second quarter alone, the company used its windfall to repay $4.8 billion in debt. If Biden called, she’d listen, but she hasn’t spoken to him one-on-one. Hollub said she’d spoken to the administration through Energy Secretary Jennifer Granholm. (“She doesn’t know the industry very well right now, but it’s because she hasn’t been in her job very long,” Hollub said.) The White House and the Department of Energy did not return requests for comment.

Hollub says she’s just following the market. “If demand goes down, we reduce production, if it goes up, we increase.” Oil prices have fluctuated rapidly over the year, and with a recession widely anticipated in the near future, demand could drop, Hollub said. Biden’s releases of oil from the SPR, she added, may have reduced gasoline prices, but at a cost to national security. “The SPR should be reserved for emergency situations, and you never know when those might come,” Hollub said.

Hollub’s message may not be politically convenient, but it’s exactly what her shareholders want to hear. Occidental OXY, -2.29%

is America’s hottest stock and has returned 150% this year, making it the top-performing company in the S&P 500 SPX, -0.65%.

Investors who bought shares of Occidental in January and held them through today would have more than doubled their money, even as the broader market has crashed. Warren Buffett’s Berkshire Hathaway has gone on a buying spree this year, and now owns more than 20% of Occidental’s shares. How Hollub got here constitutes America’s greatest corporate saga in recent years, from her 2019 debt-fueled decision to buy bigger rival Anadarko Petroleum over the vocal objections of activist investor Carl Icahn, to the pandemic-induced collapse in oil prices that almost bankrupted Occidental, and Buffett’s extension, removal, and re-extension of support.

With Occidental now on solid financial footing, Hollub is continuing to leave a mark on the oil industry and the world, landing her on the MarketWatch 50 list of the most influential people in markets. Hollub’s tangles with the wise men of Wall Street have left her savvier about how to manage her business. Stung by previous boom-and-bust cycles, Hollub has helped lead America’s oil frackers away from being “swing producers” that could counter the war-driven increase in energy prices, as she paid down debt and returned cash to shareholders through dividends and stock buybacks instead of plowing some of that money into shale oil fields. She is also pushing investment into Occidental’s massive new carbon-capture effort.

More than anything, Hollub is focused on guys like Bill Smead, founder of Smead Capital Management, who is a long-term investor in Occidental and a Hollub fan. “She’s somebody that we have a great deal of respect for and appreciate all the money she’s making us,” he said.

With that kind of backing, Hollub is planning to put Occidental in the driver’s seat of the massive national economic transition induced by climate change. She is positioning Occidental to be the company of the energy transition, one geared not to the free-for-all economy of the last century or some carbonless vision of the next, but the oil company for right now. She might even stop drilling new oil wells entirely.

“Now we feel like we control our own destiny,” Hollub said.

For the chief executive of a company that’s having a banner year on Wall Street while investors choke down generational losses, Hollub seems to constantly be on the alert for threats. Talking through the company’s prospects, she repeats a certain phrase: “I know that this will ultimately get me in trouble, but…”

Trouble? Hollub and Occidental have known their share.

The drama surrounding Occidental’s 2019 acquisition of Anadarko would make for a good boardroom thriller—or at least a lively business-school case study. Anadarko had big assets in the crucial Permian Basin region of Texas and New Mexico, where horizontal drilling in shale rock had reinvigorated an aging oil field into the nation’s biggest production zone.

Hollub and her team made an offer to buy Anadarko after months of research. She thought she had a deal locked, only to hear on the radio that Anadarko had announced plans to combine with Chevron. She nearly drove off the road, Texas Monthly recounts.

Hollub turned to Buffett for help. He agreed to what was effectively a $10 billion loan at 8% interest, in the form of preferred shares, along with warrants that allow Berkshire Hathaway, Buffett’s company, to buy more common stock. That got Hollub what she wanted, but many on Wall Street hated it. “The Buffett deal was like taking candy from a baby and amazingly she even thanked him publicly for it!” Icahn wrote in a letter to his fellow shareholders. Icahn had bought a slug of Occidental’s shares and, in the ensuing months, the billionaire investor led a shareholder campaign against Hollub, insisting that she needed stronger board oversight. Icahn allies were made Occidental directors.

In 2020, as COVID-19 flattened the global economy, deeply indebted Occidental was forced to cut its dividend for the first time in decades. Buffett sold his stock. At Icahn’s urging, the company issued 113 million warrants to its shareholders, allowing them to buy shares at $22, at a time when the stock was trading at $17. Gary Hu, one of the Icahn directors on Occidental’s board, pointed to those warrants as evidence of their success. “Our involvement in Occidental represented activism at its finest,” said Hu.

Hollub flatly disagrees. Icahn saw an opportunity to make an easy profit in derailing the Anadarko deal, Hollub said. “And what he expected is that we would lose and he would benefit from that. Since that didn’t happen, he managed to maneuver his way onto the board.” Icahn’s representatives on the board came to Hollub with a number of plans, including the warrants. She felt that one wouldn’t do any harm. “So that’s what we agreed to, but yeah, the other 10 or so weird things, we didn’t do.”

““She’s somebody that we have a great deal of respect for and appreciate all the money she’s making us.””

— Bill Smead, founder of Smead Capital Management

Former Occidental CEO Stephen Chazen returned to chair the board at Icahn’s insistence. Icahn and Occidental ultimately reached a settlement. His board members left, and the activist sold his common shares earlier this year. Chazen passed away in September. The experience embittered both sides, but there is one point of agreement: Hollub will do as she sees fit. “We were clearly wrong about the board’s ability to restrain Vicki’s ambitions,” Hu said.

Icahn made a $1.5 billion profit. At a MarketWatch event in September, Icahn said he still holds the warrants. But he hasn’t let go of the issues that motivated him to push into Occidental in the first place, though he insists he has no problem with Hollub personally. He likened her to a kid who got lucky gambling in Vegas. “The system allowed her to do it. And she’s just one small example of what is wrong with corporate governance.”

But as Icahn has himself shown, the system of corporate money in America is malleable. Its players can learn the rules of the game and adapt. Quarter after quarter since the dark days of the pandemic, Hollub turned up on corporate earnings calls pledging to keep cash flows strong, to invest in the highest-returning assets, and not to fall into the trap of overinvesting in debt-fueled or expensive production capacity, as so many failed shale producers have done in the past. She’s driven the company’s debt from nearly $40 billion following the Anadarko acquisition to less than $20 billion today. She increased the company’s dividend earlier this year. Along the way she transformed from market pariah to textbook CEO.

Hollub and other CEOs who run America’s biggest shale-oil producers have learned from the industry’s past mistakes. After proving a decade ago they could successfully extract shale oil, many U.S. oil producers were cheered on by growth and momentum stock investors as they borrowed billions to ramp up production, only to have those same investors abandon them after Saudi Arabia induced a plunge in oil prices. In the years that followed, U.S. shale-oil producers cultivated a new set of more value-oriented shareholders by promising they would share in profits through dividends and stock buybacks. Hollub and many of those other CEOs are not interested in chasing unrestrained growth again.

The world’s most famous value investor is now also on board. For Buffett, an earnings call Hollub led in February was the turning point. “I read every word, and said this is exactly what I would be doing. She’s running the company the right way,” Buffett told CNBC. Berkshire Hathaway BRK.A, +0.15%

started buying Occidental stock soon after. In August, federal regulators gave Buffett’s company permission to buy up to half of the company. (Asked for comment, a representative of Berkshire Hathaway asked for questions by email but did not respond to them.)

The markets are rife with speculation that Buffett will go all the way and purchase the entire company, though neither Hollub nor Berkshire have said as much. Hollub said simply that Buffett is bullish on oil, so she expects him to invest for the long haul. A Buffett buyout wouldn’t necessarily be a win for the investors who’ve hung on as Occidental’s stock price has recovered. “I’d probably make more money if he doesn’t buy it,” said Smead.

Warren Buffett is back to betting on Hollub and bought 20% of Occidental’s stock this year.

Johannes Eisele/Agence France-Presse/Getty Images

Where Hollub might cause real trouble is in the fight to keep carbon dioxide out of the earth’s atmosphere. That’s not because she’s a climate-denier. Far from it. Like many of her fellow oil-and-gas CEOs in recent years, Hollub has come to see climate change not as a threat to the business, but as an opportunity to be managed.

“I know some people don’t want oil to be produced for very long, but it’s going to be,” Hollub said. For that to change, people have to start using less oil. “It’s not that the more supply we generate, then the more that people are gonna use. It’s all driven by demand,” she said. And even with an electric vehicle in every driveway, we’d still need to extract oil to produce plastics and to create airplane fuel, among other projects that fall under the category of hard-to-abate emissions.

Hollub’s plan for Occidental is to wrap the company around that lingering stream of demand for hydrocarbons. She says Occidental is now in the business of carbon management, a euphemism that glides over the messiness of the climate transition and companies’ role in it. Companies need to show anxious shareholders that they’re serious about reducing their carbon emissions, but they also need to keep operating in an economy that is still seriously short on meaningful alternatives to fossil fuels. Occidental is here to help, spurred along by a series of state and federal incentives that the company lobbied for over years, culminating in the passage this year of the Inflation Reduction Act.

Climate advocates have for years tried to make the use of fossil fuels reflect their full cost on the environment. That has put them deeply at odds with oil-and-gas executives like Hollub, who opposes carbon taxes. It’s also left U.S. climate policy stalled as the planet warms. But the IRA tries something else. “I do not see the IRA as a handout to the energy industry,” said Sasha Mackler, executive director of the energy program at the Bipartisan Policy Center, a D.C. think tank. Rather than making dirty energy more expensive, the IRA tries to make clean energy cheaper, Mackler said. And that’s something Hollub can get on board with. She’s selling the idea that a barrel of oil can be clean.

Getting to a net-zero barrel of oil, as Hollub calls it, involves literally rerouting the route carbon dioxide takes through the world. For companies like Occidental, CO2 isn’t just a planet-destroying waste product. It’s a critical input to the process of oil production. Engineers can use CO2 to essentially juice aging oil wells by pumping it underground to displace hydrocarbons. The process is called enhanced oil recovery, or EOR. Occidental is the industry leader, producing the equivalent of 130,000 barrels per day of EOR oil and gas as of 2020. And that oil can, in theory, be less impactful on the climate. “We have it documented that it takes more CO2 injected into the reservoir than what the incremental barrels from that CO2 that are produced will emit when they’re used,” she said.

The trick is where that injected CO2 comes from. The Permian is crisscrossed with thousands of miles of pipelines that bring CO2 to oil fields from as far away as Colorado. At the moment, the vast majority comes from naturally occurring reservoirs or as a byproduct of the production of methane. One of the strangest ironies of modern oil production is that companies like Occidental don’t actually have enough CO2. “There’s two billion barrels of resources remaining to be developed in our conventional reservoirs using CO2,” Hollub said.

So she and her team went out looking for more. Eventually they hit on the idea that’s encapsulated in the IRA. Instead of pulling CO2 out of the ground only to put it back, Occidental could divert some of the CO2 that’s being produced by so-called industrial sources, companies that would otherwise be dumping it into the atmosphere because, of course, there’s no business reason not to.

Finding companies that wanted to do the right thing with their waste CO2 turned out to be harder than Hollub thought. “We knocked on the doors of a lot of emitters,” Hollub said. They found one taker—a Texas ethanol producer that was willing to try a pilot. It was a decent start but not enough to unlock all those buried barrels.

That may soon change, driven by the IRA. The law puts new financial incentives behind those conversations Occidental was having with CO2 emitters. The IRA significantly beefed up the so-called 45Q tax incentive for companies to put CO2 permanently in the ground. Occidental can get $60 a ton in tax credits if the CO2 is stored in the process of pumping more oil for EOR, or $85 if the company just buries it.

There’s also a higher tier of incentives if companies obtain that CO2 using an experimental technology called direct air capture. Occidental is spending $1 billion to build what would be the world’s largest direct-air-capture facility in Texas, which you can loosely think of as a giant fan to suck ambient CO2 directly out of the atmosphere. Hollub plans to build as many as 70 by 2035.

The problem some see with this plan, and with Hollub and others’ efforts to shape legislation around it, is it tightens the economy’s dependence on fossil fuels rather than loosening it. Americans will now effectively pay Occidental to pursue more enhanced oil recovery. Those net-zero barrels of oil—should they materialize—might be better in climate terms than a traditional barrel. But that’s not the only alternative. Dollar for dollar, public money would be better spent on solar energy and other low-carbon options than on EOR, said Kurt House, who knows as much because he’s tried it. House got a Ph.D. at Harvard in the science of carbon capture and storage more than a decade ago and co-founded a company to put the idea into practice. “It is bad, bad economics,” he said. “If you pay people a million dollars a ton of CO2 sequestering, they will sequester a lot of CO2. But it’ll cost us. It’ll make solving global warming much, much, much, much, much more expensive.”

But Hollub isn’t likely to change course. “I would say to those who don’t like what we’re doing, who do they want to do this? Tell me who have they gotten to, that will commit to take CO2 out of the atmosphere?” she said. “This climate transition cannot happen as fast as some people want it to happen because the world can’t afford it,” Hollub said. “We’re looking at, you know, $100 to $200 trillion for this climate transition. We cannot spend that kind of money to make this transition happen without help from diverting some of the CO2 to enhanced oil recovery, which enables then the technology to be developed and to be built at a faster pace.” And in the meantime, Occidental can sell carbon offsets to companies like United Airlines, which is supporting the direct-air-capture facility.

Those companies can choose whether they want the CO2 Occidental is capturing to be buried, full stop, or used for more oil production. But it’s clear Hollub thinks EOR is a big part of the future for Occidental. She has often said that the last barrel of oil should come from EOR. “I think there could be a world where we do stop drilling new wells,” she said. “To increase recovery from the remaining conventional reservoirs is something that’s kind of like a best kept secret for the United States. Nobody very much realizes that, but that is there. And that gives us that longevity beyond what some people are forecasting,” Hollub said.

Hollub is well-aware of her critics. Perhaps that’s why she keeps looking around for signs of trouble. But even if it finds her, she doesn’t plan to change much. “I have no regrets,” she said.

The swift recent decline in Amazon.com Inc.’s stock has brought the company’s closing market value below $1 trillion for the first time in more than two years.

Amazon shares AMZN, -0.82%

fell 5.5% in Tuesday action, finishing with a market value of $987 billion. This marked the first time since April 6, 2020 that Amazon closed out of trillion-dollar territory, according to Dow Jones Market Data.

Amazon’s valuation fell below the trillion-dollar milestone Tuesday.

Dow Jones Market Data

Amazon shares have tumbled 19.74% over the most recent five-session stretch. That five-day decline was the worst five-day loss for Amazon since its 22.03% plunge during the period that ended Nov. 20, 2008.

The e-commerce giant has come under recent pressure after the company’s latest earnings report highlighted a slowdown in AWS cloud-computing revenue growth. Additionally, Amazon disappointed with the forecast it offered for the holiday quarter.

“Combined with wobbles on revenue momentum for both AWS and retail, and suddenly the Amazon hiding place doesn’t look good,” Bernstein analyst Mark Shmulik wrote following Amazon’s earnings report last Thursday. “The good news here is that the story isn’t broken, it’s just pushed out into 2023, while Q4 may get worse before it gets better.”

When looking at companies worth more than $200 billion, Amazon is currently closest to seeing its stock hit its pandemic-era low, according to Dow Jones Market Data. Amazon shares closed Thursday at $96.79, 15.5% above their pandemic low of $83.83. Only shares of Meta Platforms Inc. META, -2.30%

have actually plunged below their pandemic low, among this grouping of the largest U.S. companies.

Investors cheered when a report last week showed the economy expanded in the third quarter after back-to-back contractions.

But it’s too early to get excited, because the Federal Reserve hasn’t given any sign yet that it is about to stop raising interest rates at the fastest pace in decades.

Below is a list of dividend stocks that have had low price volatility over the past 12 months, culled from three large exchange traded funds that screen for high yields and quality in different ways.

In a year when the S&P 500 SPX, -0.40%

is down 18%, the three ETFs have widely outperformed, with the best of the group falling only 1%.

That said, last week was a very good one for U.S. stocks, with the S&P 500 returning 4% and the Dow Jones Industrial Average DJIA, -0.32%

having its best October ever.

This week, investors’ eyes turn back to the Federal Reserve. Following a two-day policy meeting, the Federal Open Market Committee is expected to make its fourth consecutive increase of 0.75% to the federal funds rate on Wednesday.

The inverted yield curve, with yields on two-year U.S. Treasury notes TMUBMUSD02Y, 4.540%

exceeding yields on 10-year notes TMUBMUSD10Y, 4.064%,

indicates investors in the bond market expect a recession. Meanwhile, this has been a difficult earnings season for many companies and analysts have reacted by lowering their earnings estimates.

The weighted rolling consensus 12-month earning estimate for the S&P 500, based on estimates of analysts polled by FactSet, has declined 2% over the past month to $230.60. In a healthy economy, investors expect this number to rise every quarter, at least slightly.

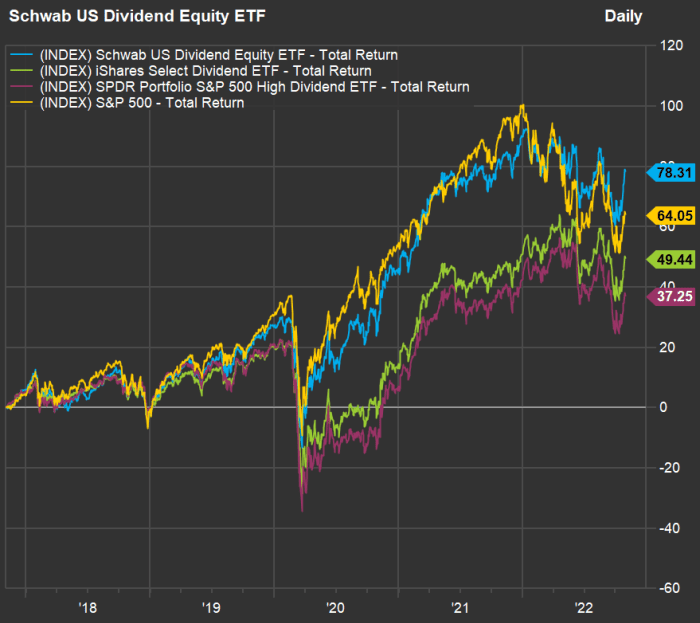

Low-volatility stocks are working in 2022

Take a look at this chart, showing year-to-date total returns for the three ETFs against the S&P 500 through October:

FactSet

The three dividend-stock ETFs take different approaches:

The $40.6 billion Schwab U.S. Dividend Equity ETF SCHD, +0.15%

tracks the Dow Jones U.S. Dividend 100 Indexed quarterly. This approach incorporates 10-year screens for cash flow, debt, return on equity and dividend growth for quality and safety. It excludes real estate investment trusts (REITs). The ETF’s 30-day SEC yield was 3.79% as of Sept. 30.

The iShares Select Dividend ETF DVY, +0.45%

has $21.7 billion in assets. It tracks the Dow Jones U.S. Select Dividend Index, which is weighted by dividend yield and “skews toward smaller firms paying consistent dividends,” according to FactSet. It holds about 100 stocks, includes REITs and looks back five years for dividend growth and payout ratios. The ETF’s 30-day yield was 4.07% as of Sept. 30.

The SPDR Portfolio S&P 500 High Dividend ETF SPYD, +0.60%

has $7.8 billion in assets and holds 80 stocks, taking an equal-weighted approach to investing in the top-yielding stocks among the S&P 500. It’s 30-day yield was 4.07% as of Sept. 30.

All three ETFs have fared well this year relative to the S&P 500. The funds’ beta — a measure of price volatility against that of the S&P 500 (in this case) — have ranged this year from 0.75 to 0.76, according to FactSet. A beta of 1 would indicate volatility matching that of the index, while a beta above 1 would indicate higher volatility.

Now look at this five-year total return chart showing the three ETFs against the S&P 500 over the past five years:

FactSet

The Schwab U.S. Dividend Equity ETF ranks highest for five-year total return with dividends reinvested — it is the only one of the three to beat the index for this period.

Screening for the least volatile dividend stocks

Together, the three ETFs hold 194 stocks. Here are the 20 with the lowest 12-month beta. The list is sorted by beta, ascending, and dividend yields range from 2.45% to 8.13%:

Any list of stocks will have its dogs, but 16 of these 20 have outperformed the S&P 500 so far in 2022, and 14 have had positive total returns.

You can click on the tickers for more about each company. Click here for Tomi Kilgore’s detailed guide to the wealth of information available free on the MarketWatch quote page.

The numbers: A closely-watched index that measures U.S. manufacturing activity fell 0.7 percentage points to 50.2 in October, according to the Institute for Supply Management on Tuesday.

Economists surveyed by the Wall Street Journal had forecast the index to inch down to 50. Any number below 50% reflects a shrinking economy.

It is the lowest level since May 2020.

Key details: The index for new orders remained in contraction territory, rising 2.1 points to 47.1. The production index rose 1.7 points to 52.3.

The employment index rose 1.3 points to 50 in October.

Supplier deliveries fell 5.6 points to 46.8 in October. This is the first time that deliveries were in a “faster” territory since February 2016.

The price index dropped 5.1 points to 46.6., also the lowest reading since the pandemic. Pricing power is shifting back to the buyer, the ISM said.

Only 8 of the 18 manufacturing industries reported growth in October.

Big picture: Manufacturing has been slowing recently led by softening business spending and fading demand for consumer goods. Economists think it is inevitable the index slips below the 50 threshold.

In a separate data, the S&P global U.S. manufacturing PMI inched up to 50.4 in its “final” reading in October from the “flash” reading of 49.9. This is down from a reading of 52 in September.

What ISM said: Manufacturing is slowing down and could soon enter contraction territory, but that doesn’t mean there will be a recession in the U.S., said Timothy Fiore, chair of the ISM factory business survey.

“I don’t see a collapse of new orders. I don’t see a collapse of the PMI,” Fiore said.

Looking ahead: “Recession jitters among manufacturers won’t disappear any time soon…manufacturing will endure more pain as demand weakens at home and abroad while prices stay high and interest rates remain fairly elevated,” said Oren Klachkin, economist at Oxford Economics.

The Chicago Business Barometer, also known as the Chicago PMI, dropped to 45.2 in October from 45.7 in the prior month, according to data released Monday.

Economists polled by the Wall Street Journal forecast a 47 reading.

Readings below 50 indicate contraction territory.

The index is produced by the ISM-Chicago with MNI. It is released to subscribers three minutes before its release to the public at 9:45 am Eastern.

The Chicago PMI is the last of the regional manufacturing indices before the national factory data for October is released on Tuesday.

Economist polled by the Wall Street Journal expect the closely-watched Institute for Supply Management’s factory index to barely remain above the 50 breakeven level in October.

Economists widely expect Federal Reserve monetary-policy makers to approve a fourth straight jumbo interest-rate rise at its meeting this week. A hike of three-quarters of a percentage point would bring the central bank’s benchmark rate to a level of 3.75%- 4%.

“The November decision is a lock. Well, I would be floored if they didn’t go 75 basis points,” said Jonathan Pingle, chief U.S. economist at UBS.

The Fed decision will come at 2 p.m. on Wednesday after two days of talks among members of the Federal Open Market Committee.

What happens at Fed Chairman Jerome Powell’s press conference a half-hour later will be more fraught.

The focus will be on whether Powell gives a signal to the market about plans for a smaller rise in its benchmark interest rate in December.

The Fed’s “dot plot” projection of interest rates, released in September, already penciled in a slowdown to a half-point rate hike in December, followed by a quarter-point hike early in 2023.

The market is expecting signals about a change in policy, and many think Powell will use his press conference to hint that a slower pace of interest-rate rises is indeed coming.

A Wall Street Journal story last week reported that some Fed officials are not keen to keep hiking rates by 75 basis points per meeting. That, alongside San Francisco Fed President Mary Daly’s comment that the Fed needs to start talking about slowing down the pace of hikes, were taken as a sign of a slowdown to come by the stock and bond markets.

“No one wants to be late for the pivot party, so the hint was enough,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Luke Tilley, chief economist at Wilmington Trust, said he thinks Powell will signal a smaller rate hike in December by focusing on some of the good wage-inflation news that was published earlier Friday.

There was a clear slowdown in private-sector wage growth, Tilley said.

But the problem with Powell signaling he has found an exit ramp from the jumbo rate hikes this year is that his committee members might not be ready to signal a downshift, Pingle of UBS said. He argued that the inflation data writ large in September won’t give Fed officials any confidence that a cooling in price pressures is in the offing.

Another worry for Powell is that future data might not cooperate.

There are two employment reports and two consumer-price-inflation reports before the next Fed policy meeting on Dec. 13–14.

So Powell might have to reverse course.

“If you pre-commit and the data slaps you in the head — then you can’t follow through,” said Stephen Stanley, chief economist at Amherst Pierpont Securities.

This has been the Fed’s pattern all year, Stanley noted. It was only in March that the Fed thought its terminal rate, or the peak benchmark rate, wouldn’t rise above 3%.

While the Fed may want to slow down the pace of rate hikes, it doesn’t want the market to take a downshift in the size of rate rises as a signal that a rate cut is in the offing. But some analysts believe that the first cut in fact will come soon after the Fed reduces the size of its rate rises.

In general terms, the Fed wants financial conditions to stay restrictive in order to squeeze the life out of inflation.

Pingle said he expects Kansas City Fed President Esther George to formally dissent in favor of a slower pace of rate hikes.

There is growing disagreement among economists about the “peak” or “terminal rate” of this hiking cycle. The Fed has penciled in a terminal rate in the range of 4.5%–4.75%. Some economists think the terminal rate could be lower than that. Others think that rates will go above 5%.

Those who think the Fed will stop short of 5% tend to talk about a recession, with the fast pace of Fed hikes “breaking something.” Those who see rates above 5% think that inflation will be much more persistent.

Ultimately, Amherst Pierpont’s Stanley is of the view that the data aren’t going to be the deciding factor. “The answer to the question of what either forces or allows the Fed to stop is probably not going to come from the data. The answer is going to be that the Fed has a number in mind to pause,” he said.

The Fed “is careening toward this moment of truth where it has very tight labor markets and very high inflation, and the Fed is going to come out and say, ‘OK, we’re ready to pause here.’ “

“That strikes me that is going to be a very volatile period for the market,” he added.

Fed fund futures markets are already volatile, with traders penciling in a terminal rate above 5% two weeks ago and now seeing a 4.85% terminal rate.

Over the month of October, the yield on the 10-year Treasury note TMUBMUSD10Y, 4.046%

rose steadily above 4.2% before softening to 4% in recent days.

“When you get close to the end, every move really counts,” Stanley said.

The Dow Jones Industrial Average has been criticized by some market watchers for being a poor barometer of equity-market performance given its relatively small sample size of just 30 stocks.

But this quality, along with the paucity of megacap technology names, has helped shepherd the index toward what’s expected to be its biggest October gain in its 126-year history.

With a month-to-date gain of 14.40% through Friday, the Dow DJIA, +2.59%

is on track for its best monthly performance since January 1976, when it rose 14.41%, according to Dow Jones Market Data. To clinch its best October ever, it only needs to hang on to a month-to-date gain of 10.65% by the time the U.S. market closes on Monday.

The Dow is still in a bear market, but is now down less than 10% for the year to date. That compares, however, with year-to-date losses of 18.2% for the S&P 500 SPX, +2.46%

and 29% for the Nasdaq Composite COMP, -8.39%.

What exactly has made the Dow’s October performance so stellar?

The blue-chip gauge is packed with energy and industrials stocks, which have been among the best performing sectors for the stock market since the start of the year, noted Art Hogan, chief market strategist at B. Riley Wealth Management.

These stocks have performed particularly well since the start of the latest quarterly earnings season, while megacap technology names like Meta Platforms Inc. META, +1.29%,

Amazon.com Inc. AMZN, -6.80%

and Alphabet Inc. GOOG, +4.30%

have sputtered after delivering results and guidance that disappointed Wall Street this week.

“It’s very tech-light, and it’s very heavy in energy and industrials, and those have been the winners,” Hogan said. “The Dow just has more of the winners embedded in it and that has been the secret to its success.”

The Dow is on track to log its highest close in at least two months on Friday as it outperforms both the S&P 500 SPX, +2.46%

and Nasdaq Composite COMP, -8.39%.

Furthermore, it’s on track to climb for a sixth straight session, what would be its longest winning streak since May 27, according to DJMD.

Adding to the list of notable factoids, the average is also on track to log a fourth straight weekly gain, which would cement its longest winning streak since Nov. 5, 2021, when the index rose for five straight weeks.

Caterpillar Inc. CAT, +3.39%,

Chevron Corp. CVX, +1.17%

And Amgen Inc. AMGN, +2.46%

are the top-performing Dow stocks so far this month, having gained 29.3%, 21.2% and 18.3%, respectively, as of Friday.

In recent trade, the blue-chip average was up around 700 points, or 2.2%, on track for its biggest daily point and percentage gain in exactly one week.

Economists widely expect Federal Reserve monetary-policy makers to approve a fourth straight jumbo interest-rate rise at its meeting this week. A hike of three-quarters of a percentage point would bring the central bank’s benchmark rate to a level of 3.75%- 4%.

“The November decision is a lock. Well, I would be floored if they didn’t go 75 basis points,” said Jonathan Pingle, chief U.S. economist at UBS.

The Fed decision will come at 2 p.m. on Wednesday after two days of talks among members of the Federal Open Market Committee.

What happens at Fed Chairman Jerome Powell’s press conference a half-hour later will be more fraught.

The focus will be on whether Powell gives a signal to the market about plans for a smaller rise in its benchmark interest rate in December.

The Fed’s “dot plot” projection of interest rates, released in September, already penciled in a slowdown to a half-point rate hike in December, followed by a quarter-point hike early in 2023.

The market is expecting signals about a change in policy, and many think Powell will use his press conference to hint that a slower pace of interest-rate rises is indeed coming.

A Wall Street Journal story last week reported that some Fed officials are not keen to keep hiking rates by 75 basis points per meeting. That, alongside San Francisco Fed President Mary Daly’s comment that the Fed needs to start talking about slowing down the pace of hikes, were taken as a sign of a slowdown to come by the stock and bond markets.

“No one wants to be late for the pivot party, so the hint was enough,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

Luke Tilley, chief economist at Wilmington Trust, said he thinks Powell will signal a smaller rate hike in December by focusing on some of the good wage-inflation news that was published earlier Friday.

There was a clear slowdown in private-sector wage growth, Tilley said.

But the problem with Powell signaling he has found an exit ramp from the jumbo rate hikes this year is that his committee members might not be ready to signal a downshift, Pingle of UBS said. He argued that the inflation data writ large in September won’t give Fed officials any confidence that a cooling in price pressures is in the offing.

Another worry for Powell is that future data might not cooperate.

There are two employment reports and two consumer-price-inflation reports before the next Fed policy meeting on Dec. 13–14.

So Powell might have to reverse course.

“If you pre-commit and the data slaps you in the head — then you can’t follow through,” said Stephen Stanley, chief economist at Amherst Pierpont Securities.

This has been the Fed’s pattern all year, Stanley noted. It was only in March that the Fed thought its terminal rate, or the peak benchmark rate, wouldn’t rise above 3%.

While the Fed may want to slow down the pace of rate hikes, it doesn’t want the market to take a downshift in the size of rate rises as a signal that a rate cut is in the offing. But some analysts believe that the first cut in fact will come soon after the Fed reduces the size of its rate rises.

In general terms, the Fed wants financial conditions to stay restrictive in order to squeeze the life out of inflation.

Pingle said he expects Kansas City Fed President Esther George to formally dissent in favor of a slower pace of rate hikes.

There is growing disagreement among economists about the “peak” or “terminal rate” of this hiking cycle. The Fed has penciled in a terminal rate in the range of 4.5%–4.75%. Some economists think the terminal rate could be lower than that. Others think that rates will go above 5%.

Those who think the Fed will stop short of 5% tend to talk about a recession, with the fast pace of Fed hikes “breaking something.” Those who see rates above 5% think that inflation will be much more persistent.

Ultimately, Amherst Pierpont’s Stanley is of the view that the data aren’t going to be the deciding factor. “The answer to the question of what either forces or allows the Fed to stop is probably not going to come from the data. The answer is going to be that the Fed has a number in mind to pause,” he said.

The Fed “is careening toward this moment of truth where it has very tight labor markets and very high inflation, and the Fed is going to come out and say, ‘OK, we’re ready to pause here.’ “

“That strikes me that is going to be a very volatile period for the market,” he added.

Fed fund futures markets are already volatile, with traders penciling in a terminal rate above 5% two weeks ago and now seeing a 4.85% terminal rate.

Over the month of October, the yield on the 10-year Treasury note TMUBMUSD10Y, 4.030%

rose steadily above 4.2% before softening to 4% in recent days.

“When you get close to the end, every move really counts,” Stanley said.