[ad_1]

U.S. Stocks Wobble Ahead of Fed Minutes

[ad_2]

[ad_1]

The numbers: Business conditions at U.S. companies deteriorated again in November and pointed to a slowing economy.

The “flash” U.S. services sector index drop to a three-month low of 46.1 this month from 47.8 in October, keeping it near the lowest level of the pandemic era. The service side of the economy employs most Americans.

The S&P Global U.S. manufacturing sector index, meanwhile, slid to a 2 1/2-year low of 47.6 from 50.4.

Any number below 50 reflects a contracting economy.

Key details: New orders, a sign of future sales, fell in November at the fastest pace since early in the pandemic in 2020, S&P Global found. Exports also declined.

The cost of supplies, a measure of inflation, eased again in a sign that intense inflationary pressures are on the wane. Companies also raised prices at the slowest rate in more than two years.

Shortages of supplies, a big problem during the pandemic, also continued to diminish.

These shortages were one of the biggest contributors to the U.S. and global surge in inflation. While they are fading, they remain a big problem.

Big picture: Businesses are still expanding by some measures, but they are also preparing for slower economic growth.

Rising interest rates orchestrated by the Federal Reserve have dampened sales in the U.S. while a strong dollar has hurt exports by making American products more expensive.

Looking ahead: “Inflationary pressures should continue to cool in the months ahead, potentially markedly, but the economy meanwhile continues to head deeper into a likely recession,” said Chris Williamson, chief business economist at S&P Global Market Intelligence.

Market reaction: The Dow Jones Industrial Average

DJIA,

and S&P 500

SPX,

rose in Wednesday trades.

[ad_2]

[ad_1]

The numbers: Orders at American factories for long-lasting goods such as autos and computers jumped 1% in October, marking a strong showing that probably isn’t sustainable because of a slowing U.S. economy.

Economists polled by the Wall Street Journal had forecast a 0.5% increase. Durable goods are items such as autos, appliances and computers meant to last at least three years.

A key measure of business spending, meanwhile, also rose a solid 0.7% last month.

Orders tend to rise steadily in an expanding economy and shrink when it weakens. Yet the results in October don’t look quite as strong after inflation is taken into account. The consumer price index rose 0.4% last month.

Big picture: Manufacturers are able to produce more of what their customers want after two years of chronic shortages, but mostly because demand has softened. Rising U.S. interest rates have curbed sales at home while a strong dollar has dented exports.

The situation could get worse. The Federal Reserve is jacking up interest rates to bring down high inflation, but higher borrowing costs are expected to slow the economy even further.

Key details: Orders for new cars climbed 0.6% in October. Orders for aircraft rose a sharper 7.4%. The transportation segment is a large and volatile category that often exaggerates the swings in industrial production.

Outside of transportation, new orders rose a still-decent 0.5%. Bookings increased in every major category except for primary metals.

The rate of growth in business investment, or core orders, has slowed considerably. however. The figure excludes military spending and the auto and aerospace industries.

Looking ahead: “Business equipment investment continues to hold up reasonably well in the face of higher borrowing costs,” said senior U.S. economist Andrew Hunter of Capital Economics, but “we doubt that resilience will continue indefinitely.”

Market reaction: The Dow Jones Industrial Average

DJIA,

and S&P 500

SPX,

were set to open slightly higher in Wednesday trades.

[ad_2]

[ad_1]

Tesla Inc. shares on Monday were poised to end at a fresh two-year low, with shares of other electric-vehicle makers also underperforming the broader equity market as worries about China’s COVID-19 lockdowns re-emerged and oil futures prices dropped to their lowest level since January.

Shares of Tesla

TSLA,

extended their losing streak to a fourth session and were on track for their lowest close since Nov. 20, 2020, when they closed at $163.20. The stock was the 10th worst performer in the S&P 500 index

SPX,

and fourth worst in the Nasdaq 100

COMP,

— and the most active stock on both exchanges.

American depositary shares of several China-based EV makers, including Nio Inc.

NIO,

and XPeng Inc.

XPEV,

also underperformed the broader market. In contrast, shares of General Motors Co.

GM,

and Ford Motor Co.

F,

merely edged lower.

The energy sector was taking a broad beating as well, with the SPDR Energy Select Sector ETF

XLE,

looking at a four-week low.

Related: GM’s EV roadmap is ‘ambitious,’ but Wall Street doesn’t give it full credit just yet

Tesla’s underperformance as compared with the broader indexes holds on a monthly and yearly basis as well. The stock is down more than 25% so far in November and 52% this year.

If the trend continues, this would be the worst yearly performance for the stock on record.

The S&P has lost about 17% year to date and has clawed back to a 2% gain so far in November.

[ad_2]

[ad_1]

For the first time ever, rich nations, including a top-polluting U.S., will pay for the climate-change damage inflicted upon poorer nations.

These smaller economies are often the source of the fossil fuels

CL00,

minerals

PICK,

and other raw materials behind the developed world’s modern conveniences and technologicial advancement, including many practices responsible for the Earth-warming emisisons. And yet the developing world shoulders the worst of the droughts, deadly heat, ruined crops and eroding coastlines that take lives and eat into economic growth.

The deal, called “loss and damage” in summit shorthand, was struck as the U.N.’s Conference of Parties, or COP27, gaveled to a close near dawn Sunday in Egypt. Official talks ended Friday, but negotiations extended into the weekend.

Read: Historic compensation fund approved at U.N. climate talks

It was a big win for poorer nations which have long sought money — sometimes viewed as reparations — because they are often the victims of climate-worsened floods, famines and storms despite contributing little directly to the pollution that heats up the globe. It took last-minute, pre-summit negotiations to even get the topic on the official agenda.

“Three long decades and we have finally delivered climate justice,” said Seve Paeniu, the finance minister of island nation Tuvalu, according to the Associated Press. “We have finally responded to the call of hundreds of millions of people across the world to help them address loss and damage.”

“ ‘Three long decades and we have finally delivered climate justice.’ ”

Pakistan’s environment minister, Sherry Rehman, said the establishment of the fund “is not about dispensing charity.” Pakistan, hit by devastating drought and more, dominated climate-change headlines this year.

“It is clearly a down payment on the longer investment in our joint futures,” she said, speaking for a coalition of the world’s poorest nations.

According to many conference participants, the U.S. was a late-stage roadblock to establishing this official payout language, though it signed off in the end. U.S. participation was also impacted once chief climate negotiator John Kerry tested positive for COVID-19, although he continued to work from his hotel.

According to the agreement, the fund would initially draw on contributions from developed countries and other private and public sources such as international financial institutions, including the World Bank and the International Monetary Fund.

While major emerging economies such as China wouldn’t automatically have to contribute, that option remains on the table. This is a key demand by the European Union and the U.S., who argue that China and other large polluters currently classified as “developing” countries have the financial clout and responsibility to pay their way.

The fund would be largely aimed at the most vulnerable nations, though there would be room for middle-income countries that are severely battered by climate disasters to get aid.

Attention on methane, a more-potent but shorter-lasting greenhouse gas than carbon, was considered a major win at the summit. Some 150 countries have now signed on to the voluntary Global Methane Pledge, an official effort to cap the release of the GHG whose reduction presents perhaps the easiest way to reduce the global warming.

Read more: Natural gas-focused methane pact expands at climate summit, minus China

With the pledge, countries representing 45% of global methane emissions have vowed to reduce their emissions by 30% by 2030. If methane-reduction pledges are met, the result would be equivalent to eliminating the GHG emissions from all of the world’s cars, trucks, buses and all two- and three-wheeled vehicles, according to the International Energy Agency.

China, the world’s largest polluter by some measures, has not signed the deadline-based pledge, but has agreed to reduce methane emissions.

COP27 talks wrapped without concrete progress on the contentious issue of shifting an overall 1.5 degrees Celsius temperature limit from a voluntary marker to an established requirement of nations. Most voluntary pacts among nations and private entities, including a vow by Amazon.com

AMZN,

Ford Motor

F,

Apple

AAPL,

and others signing on to a “First Movers” pledge, loosly use the 1.5-degree limit set in 2015 when talks took place in Paris.

Private banks, insurers and institutional investors representing $130 trillion said they would align their investments with the goal of keeping global warming to 1.5 degrees Celsius, toward a pledge to net-zero emissions economy-wide by 2050. Advocacy groups cheer the pledge and its expanding roster but are also keeping up pressure on the signatories to speed up progress toward this goal and to stop undermining the pledge with fossil-fuel investment.

Read: Here’s where the big U.S. banks stand up and fall down on climate change

The Egypt pact was also void of firmer language on emissions cutting and the desire by some officials to target all fossil fuels

NG00,

for a phase-down.

Natural gas, which is relatively cheaper to produce than other fossil fuels, has been the major alternative to more-polluting coal in electricity generation. Still, it has its own emissions risk.

In the U.S., for example, electricity is the most common energy source used for cooking — electricity often powered by gas. Still, about 38% of U.S. households use natural gas directly for cooking, according to the U.S. Energy Information Administration.

Natural gas providers also own an established pipeline infrastructure that may serve alternative energy, and is pushed by the industry as a viable alternative alongside solar, wind

ICLN,

and other means. The industry also promotes its efforts to cap methane leaks.

Related: World’s richest nations stick to 1.5-degree climate pledge despite energy crunch

“ ‘It is more than frustrating to see overdue steps on mitigation and the phase-out of fossil energies being stonewalled by a number of large emitters and oil producers.’”

With fossil fuels in their sight, the European Union and other nations fought back at what they considered backsliding in the Egyptian presidency’s overarching cover agreement and threatened to scuttle the rest of the process, while advancing their own draft. The package was revised again, removing most of the elements Europeans had objected to but adding none of the heightened ambition they were hoping for, the AP said.

Egypt has played a unique role as host, representative of Africa, which sits at the front lines of those hurt by climate change and yet, remaining loyal to its own fossil-fuel ambitions and those of OPEC nations.

Germany’s Foreign Minister Annalena Baerbock voiced frustration.

“It is more than frustrating to see overdue steps on mitigation and the phase-out of fossil energies being stonewalled by a number of large emitters and oil producers

XOM,

BP,

” she said.

The agreement includes a veiled reference to the benefits of natural gas as low- emission energy, despite many nations calling for a phase down of natural gas, which does contribute to climate change.

At least 636 representatives of the fossil fuel industry registered to attend the summit, a 25% increase over the industry’s presence last year, according to an analysis released by three advocacy groups.

More fossil fuel lobbyists are on the roster than any single national delegation, besides the UAE who has registered 1,070 delegates compared to 176 last year, according to a report from Corporate Accountability, Corporate Europe Observatory (CEO) and Global Witness (GW).

Frances Colón, senior director for International Climate Policy at the Center for American Progress, found plenty of fault with this round of talks.

“The final text reflects the outsized and corrupting presence of fossil fuel and big agricultural lobbyists at COP27, compounded by a lack of ambition from key, high-emitting countries,” she said, in a statement. “The agreement makes only a passing reference to the 1.5-degree Celsius warming goal and does not include any new language on phasing down or phasing out all fossil fuels

RB00,

— the only way to reach emissions reduction goals and secure a livable future.”

Colón also worried that the official statement did not adequately advance efforts. World leaders failed to reference the twin, interlocking crises of nature loss and climate change, and declined to link COP27 to next month’s U.N. biodiversity summit in Montreal.

“ ‘The agreement makes only a passing reference to the 1.5-degree Celsius warming goal and does not include any new language on phasing down or phasing out all fossil fuels — the only way to reach emissions reduction goals and secure a livable future.’”

While the new agreement doesn’t ratchet up calls for reducing emissions, it does retain language to keep alive the voluntary global goal of limiting warming to 1.5 degrees Celsius (2.7 degrees Fahrenheit). The Egyptian presidency kept offering proposals that harkened back to 2015 Paris language which also mentioned a looser goal of 2 degrees.

This year’s pact also neglected to toughen the main sticking point from the previous COP, in Glasgow last year. At that time, China and India united to dig in unless coal language was softened. Nations this year did not expand on last year’s call to phase down global use of “unabated coal” even though India and other countries pushed to include oil and natural gas in language from Glasgow.

“We joined with many parties to propose a number of measures that would have contributed to this emissions peaking before 2025, as the science tells us is necessary. Not in this text,” the United Kingdom’s Alok Sharma said.

Climate campaigners are concerned that pushing for strong action to end fossil fuel use will be even harder at next year’s meeting, which will be hosted in Dubai, located in the oil-rich United Arab Emirates.

The Associated Press contributed.

[ad_2]

[ad_1]

The U.S. leading economic index fell 0.8% in October, the Conference Board said Friday.

Economists polled by The Wall Street Journal had expected a 0.4% fall.

This is the eighth straight decline in the leading index.

The long period of declines suggests “the economy is possibly in a recession,” said Ataman Ozyildirim, senior director of economic research at the Conference Board. He said the data show a recession is likely to start around the end of the year and last through mid-2023.

The coincident index, which measures current conditions, rose 0.2% in October after a 0.1% gain in the prior month. The lagging index increased by 0.1%, matching the September gain.

The LEI is a weighted gauge of 10 indicators designed to signal business-cycle peaks and valleys.

Stocks

DJIA,

SPX,

were trading higher on Friday morning and the yield on the 10-year Treasury note

TMUBMUSD10Y,

rose to 3.8%.

[ad_2]

[ad_1]

The numbers: Existing-home sales fell 5.9% to a seasonally adjusted annual rate of 4.43 million in October, the National Association of Realtors said Friday. Compared with October 2021, home sales were down 28.4%.

Economists polled by the Wall Street Journal had expected an decrease to 4.37 million units.

The level of sales is the lowest since December 2011 excluding the 2020 pandemic.

This is also the ninth straight monthly decline in sales, the longest streak on record.

Key details: The median price for an existing home was $379,100 up 6.6% from October 2021.

But price gains are decelerating. Prices were up over 20% on a year-on-year basis earlier this year.

Housing inventory fell 0.8% to 1.22 million units in October. Unsold inventory sits at a 3.3-month supply at the current sales pace, up from 3.1 months in September and 2.4 months a year ago.

A 6-month supply of homes is generally viewed as indicative of a balanced market.

Sales declined in all regions of the country.

Big picture: Home sales have dropped as mortgage rates have risen sharply and affordability has dropped.

Softer inflation data in October have led to a drop in mortgage rates, which could lead for a floor on sales.

At the same time, Federal Reserve officials may pencil in a “peak” interest rate above 5% at the policy meeting next month.

Economists see home prices have further to fall in this market.

What the NAR is saying: Home sales have been very low and the softness could continue for a few months. But sales could pick up early next year if the mortgage rate has peaked, said Lawrence Yun, chief economist at the NAR.

Market reaction: Stocks

DJIA,

SPX,

opened lower on Friday. The yield on the 10-year Treasury note

TMUBMUSD10Y,

rose to 3.79%.

[ad_2]

[ad_1]

The numbers: Construction on new houses fell 4.2% in October as high mortgage rates put off buyers and forced builders to scale back, a situation that’s likely to continue through 2023.

U.S. housing starts slowed to an annual pace of 1.43 million last month from 1.49 million in September. That figure reflects how many homes would be built in 2022 if construction took place at same rate over the entire year as it did in October.

Economists polled by MarketWatch had expected housing starts to register a rate of 1.41 million after adjusting for the typical seasonal swings in demand.

New construction hit a record 1.8 million in April before tapering off.

The number of permits, meanwhile, slipped 2.4% to a rate of 1.53 million, down sharply from a record 1.9 million last December.

Permits foreshadow how many houses are likely to be built in the months ahead, assuming a stable real estate market. But a major increase in mortgage rates this year has depressed demand and forced builders to scale back plans.

Key details: Single-family home construction fell 6.1% to an annual rate of 855,000 in October. Projects with five units or more registered a 556,000 rate, little changed from the prior month.

Housing starts are down 9% from a year ago, when mortgage rates briefly dipped below 3%.

Permits have fallen 10% from a year earlier.

Big picture: The highest mortgage rates in several decades have stifled new construction and are likely to do so through the next year or longer. The rate on a 30-year fixed mortgage recently topped 7%, more than double the rate a year ago.

While the U.S. has an acute need for more housing, fewer people can now afford to buy a home. Home prices are starting to come off record highs, but not by much.

Looking ahead: “Higher mortgage rates continue to exact a heavy toll on new construction,” said Richard Moody, chief economist of Regions Financial.

Market reaction: The Dow Jones Industrial Average

DJIA,

and S&P 500

SPX,

fell in Thursday trades.

Related: Home prices will fall in 2023, but affordability will be at its worst since 1985, research firm says

[ad_2]

[ad_1]

The European Union’s ban on seaborne imports of Russian oil, along with the Group of Seven’s plan to cap prices of oil from Russia early next month won’t guarantee that prices for the commodity will see a lasting rally, or that supplies will tighten further in the days ahead.

“In isolation, the sanctions on Russia should be bullish for prices,” says Matt Smith, lead oil analyst, Americas, at Kpler. However, they may have a limited effect, as Russian barrels get “rerouted and not taken off the market,” while a price cap still has so much uncertainty surrounding it that its impact may be “muted due to workarounds or may simply be ineffective.”

[ad_2]

[ad_1]

Republicans will take over the U.S. House of Representatives two years into President Joe Biden’s term, though their narrow majority looks set to cause headaches for GOP leaders.

Republican hopes for a strong red wave have been dashed, but the Associated Press said Wednesday that the party won enough House seats — 218 — to control that chamber of Congress, as results from the midterm elections continue to be tabulated.

The battle for the U.S. Senate went to the Democrats late Saturday. Democrats will retain their hold on the Senate after winning a key race in Nevada, giving Biden’s party control of at least one chamber of Congress for the next two years.

“Republicans have officially flipped the People’s House!” Rep. Kevin McCarthy, R-Calif., the front-runner to become House Speaker, tweeted late Wednesday. “Americans are ready for a new direction, and House Republicans are ready to deliver.”

While Republicans will control just one chamber of Congress, they now are expected to deliver a check on Biden’s policy priorities, such as by potentially using a debt-ceiling showdown to force spending cuts.

In a statement late Wednesday, President Joe Biden called for bipartisanship: “The American people want us to get things done for them. They want us to focus on the issues that matter to them and on making their lives better. And I will work with anyone — Republican or Democrat — willing to work with me to deliver results.”

Related: Democrats weigh end run around Republicans to raise debt limit

And see: Republican lawmakers likely to target ‘woke capitalism’ after the midterm elections, analysts say

The Republican House majority has yet to be finalized but could be the narrowest of the 21st century, even less than in 2001, when the GOP had a nine-seat majority with two independents.

Washington is likely to face new periods of gridlock, with Democrats also keeping their hold on the White House since Biden still has two years to serve before the 2024 presidential election. That’s after Democrats in the past two years used party-line votes to push through measures such as March 2021’s stimulus law and this past summer’s package targeting healthcare, climate change and taxes.

The House switching to red from blue fits the historical pattern in which a first-term president’s party tends to lose congressional ground in the midterms. The GOP highlighted raging inflation in its effort to win over American voters.

The House seats to flip to the GOP included one held by Democratic Rep. Elaine Luria of Virginia, who lost to Republican challenger Jen Kiggans, as well as two seats in Florida. But Democrats also flipped House seats and won re-elections in bellwether races, with Virginia Rep. Abigail Spanberger and Indiana Rep. Frank Mrvan notching victories.

Read more: Here are the congressional seats that have flipped in the midterm elections

Democrats have had a grip on the House since the 2018 midterms. They’ve run the Senate for two years, controlling the 50-50 chamber only because Vice President Kamala Harris can cast tiebreaking votes.

Among the competitive Senate races, Democrats kept their hold on seats in Arizona, Colorado and New Hampshire, while scoring a pick-up in Pennsylvania. Republicans maintained their control of seats in North Carolina, Ohio and Wisconsin.

Georgia’s Senate contest is headed to a Dec. 6 runoff, but its outcome has become less significant.

Betting markets since late on Election Day have been seeing Democrats staying in charge of the Senate and Republicans winning the House. Ahead of last Tuesday’s voting, betting markets had signaled confidence in GOP prospects for taking over both the Senate and House.

Analysts had said voters last month appeared increasingly focused on Republican issues such as high prices for gasoline

RB00,

and other essentials, at the expense of Democrats’ agenda items such as climate change and abortion rights.

But exit polls suggested that Republicans performed worse than expected because many Democrats and independents voted partly to show their disapproval of former President Donald Trump — and those voters were energized by the Supreme Court’s Dobbs decision that overturned Roe.

See: Anti-Trump vote and Dobbs abortion ruling boost Democrats in 2022 election

The former president announced his 2024 White House run late Tuesday. Earlier Tuesday, House Republicans chose Rep. Kevin McCarthy of California, the current minority leader, as their candidate for speaker. Thirty-one Republicans voted against McCarthy, signaling that he must shore up his support before the vote on the speakership takes place in January. It’s an early sign of how Republicans’ narrow majority is creating turbulence for the House GOP leadership.

Plus: Senate Republicans pick Mitch McConnell as their leader, as Rick Scott’s challenge flops

[ad_2]

[ad_1]

U.S. stocks closed higher Tuesday, but off the session’s best levels, after more data suggested inflation may be slowing and mega-retailer Walmart offered a rosier annual forecast.

The Dow turned negative earlier in the session after the Associated Press reported that Russian missiles crossed into Poland and killed two people, ratcheting up geopolitical tension given Poland is a NATO country.

On Monday, U.S. stocks finished near session lows after early gains evaporated. The Dow Jones Industrial Average fell 211 points, or 0.6%, while the S&P 500 declined 36 points, or 0.9% and the Nasdaq Composite dropped 226 points, or 2%.

U.S. stocks closed higher Tuesday, after another batch of inflation data showed that whole prices rises were slowing in October for the second straight month.

The Dow’s brief negative turn came after reports that Russian military bombarded Ukraine Tuesday. In the attack, missiles reportedly crossed into Poland, a member of NATO, the Associated Press said, citing a senior U.S. intelligence official.

“Geopolitical concerns obviously are never positive for the market,” said Peter Cardillo, chief market economist at Spartan Capital Securities.

On Tuesday, oil futures settled higher. West Texas Intermediate crude for December delivery rose to $1.05, or 1.2%, reaching $86.92 a barrel.

While markets had started to price in the toll of Russian’s nearly nine-month invasion of Ukraine, it had not priced in an potential escalation of the war, said Kent Engelke, chief economic strategist at Capitol Securities Management.

“Talk about geopolitical angst returning,” Engelke said, later adding, “If there were really missiles shot to Poland and that was really not an accident, wow, that is really increasing the scope of the war.”

A U.S. National Security Council spokesperson said the agency was aware of the news reports out of Poland, but that it cannot confirm the reports or any details at this time.

While international worries clouded the session, there was also encouraging domestic news.

The U.S. producer-price index climbed 8% over the 12 months through October, the Labor Department said Tuesday, easing from September’s revised 8.4% increase. Last week, stocks surged after the October consumer-price index rose more slowly than expected.

See: Wholesale prices rise slowly again and point to softening U.S. inflation

Tuesday’s PPI report helped support the notion that inflation has peaked, at least for now.

“Today, it’s really about the PPI and the market reaction to it,” Steve Sosnick, chief strategist at Interactive Brokers

IBKR,

said in a Tuesday morning interview before the reports of missiles crossing into Poland.

Markets ripped higher last Thursday after October’s consumer-price index showed signs of easing. The same dynamic was playing out Tuesday, but the response now has been “a bit more muted” because it’s an iteration on inflation data that investors already had been starting to see, Sosnick said.

So, is the economy really at peak inflation? It’s too early to say for sure, according to Sosnick. Still, the PPI numbers, paired with last week’s CPI reading “does add evidence to that narrative,” he added.

Walmart’s third quarter earnings also were buoying markets, Sosnick said. The massive retailer’s beat on earnings offers a glimpse at the minds and wallets of many American consumers. For anyone who worries about consumers “getting highly defensive” and not spending, Walmart’s numbers are “counter evidence.”

In other news, the first face-to-face meeting between President Joe Biden and President Xi Jinping helped support stocks listed in China and Hong Kong, as some of the tensions between the world’s two largest economies were seen to be easing.

The upbeat tone from Asia, which included Taiwan Semiconductor Manufacturing Company

TSM,

jumping 7.7% on news Warren Buffett had bought a $5 billion stake, underpinned European bourses, which closed higher for a fourth session in a row.

Analysts increasingly expect stocks to enjoy a positive end to the year. “The near-term picture still looks positive for U.S. benchmark indices and while momentum has reached intra-day overbought levels, this doesn’t imply a selloff has to happen right away,” said Mark Newton, head of technical strategy at Fundstrat.

Philadelphia Federal Reserve President Patrick Harker said Tuesday that he favored a 50 basis-point hike to the Fed’s benchmark rate in December. Atlanta Fed President Raphael Bostic said more rate hikes will be needed, even through there have been “glimmers of hope” on inflation.

Fed Vice Chairman for Supervision Michael Barr said Tuesday that the U.S. economy is likely to slow in coming months, and more workers will lose their jobs, in Senate testimony. The Fed is working with regulators to assess risks tied to cryptocurrency markets, following the collapse of FTX and its associated companies.

In other U.S. economic data, the New York Empire State manufacturing index for November showed a gauge of manufacturing activity in the state rose 13.6 points to 4.5 this month.

The yield on the 10-year Treasury note

TMUBMUSD10Y,

was down 6.7 basis points at 3.798%. Bond yields move inversely to prices.

—Jamie Chisholm contributed reporting to this article

[ad_2]

[ad_1]

Home Depot

third-quarter earnings results beat expectations, giving the stock a boost on Tuesday.

The home-improvement retailer reported third-quarter earnings of $4.24 a share, topping analysts’ projections of $4.12 a share. Revenue came in at $38.9 billion, up 5.6% from a year earlier and topping estimates for $38 billion. Same-store sales rose 4.3%, ahead of estimates for 3.1%. U.S. same-store sales rose 4.5%.

[ad_2]

[ad_1]

More than 1 million barrels a day of Russian oil exports are set to be upended by Western sanctions expected to come into force within weeks, shipments Moscow will struggle to redirect elsewhere which threatens to further tighten global energy markets, the International Energy Agency said Tuesday.

Russian crude oil exports, including to the European Union, were largely unchanged last month, despite the prospect of an imminent EU ban on Russian crude oil imports and a separate plan to cap prices for Russian crude oil sales, the Paris-based agency said in a monthly report.

Russian exports to the EU were 1.5 million barrels a day in October, of which 1.1 million barrels a day will be halted when the bloc’s ban comes into effect on December 5, the IEA said.

It was unclear how much of those supplies Russia would be able to redirect to customers elsewhere in the world, the IEA said. India, China and Turkey have snapped up discounted Russian crude shipments, but buying from those nations has stabilized in recent months, the IEA said. Meanwhile, the volume would be too large for the remaining nations to absorb, the agency said.

The warning comes as the IEA predicted additional demand this year and next would come from China as the nation slowly eases its Covid-19 lockdown measures–though global demand growth will be sluggish as economies are expected to struggle.

The agency upped its 2022 global oil demand forecasts by 170,000 barrels a day to 99.8 million barrels a day. For 2023, the IEA raised its oil demand forecasts by 130,000 barrels a day to 101.4 million barrels a day.

Russia’s declining oil output will drag on global supplies which will grow at an anemic rate next year, failing to keep pace with growing oil demand. The IEA said global oil supplies would rise to 100.7 million barrels a day in 2023, 100,000 barrels a day more than it was forecasting last month, but still 700,000 barrels a day short of the world’s expected appetite for oil

CL.1,

Write to Will Horner at william.horner@wsj.com

[ad_2]

[ad_1]

The latest message from former FTX chief executive Sam Bankman-Fried left onlookers puzzled and alarmed after the swift decline into bankruptcy for the cryptocurrency exchange he founded.

In successive tweets, Bankman-Fried’s twitter account merely stated, “What,” followed by capital letters H.A.P.P.E.N., unfurled slowly over the span of about 19 hours.

Bankman-Fried has been an active tweeter throughout FTX’s demise, earlier having written that he was “shocked to see things unravel the way they did.”

Twitter and Tesla

TSLA,

CEO Elon Musk, who’s also having some difficulties, tweeted with fire emojis to an attempt at a translation of the cryptic tweet.

Musk also tweeted his amusement at the claim that Bankman-Fried played a “League of Legends” game — the same game the executive infamously was playing when the venture-capital firm Sequoia invested in FTX. Court filings from Musk’s failed attempt to get out of his Twitter purchase show that he doubted that Bankman-Fried ever had $3 billion liquid to co-invest in Twitter.

While the broader social-media sentiment was a wish for Bankman-Fried to be jailed, there also was concern for his health.

FTX has filed for Chapter 11 bankruptcy protection, and over the weekend there also seems to have been a hack of customer funds. The securities regulator in FTX’s headquarters of the Bahamas meanwhile said it had not requested the prioritization for withdrawals of funds for Bahamian clients.

Reuters reported the allegation Bankman-Fried had a “back door” that allowed him to mask the transfer of customer funds to his Alameda hedge fund, which Bankman-Fried told the news agency was just “confusing internal labeling.”

The former FTX CEO couldn’t be reached for comment.

[ad_2]

[ad_1]

Federal Reserve Gov. Christopher Waller said Sunday that financial markets seem to have overreacted to the softer-than-expected October consumer price inflation data last week.

“It was just one data point,” Waller said, in a conversation in Sydney, Australia, sponsored by UBS.

“The market seems to have gotten way out in front over this one CPI report. Everybody should just take a deep breath, calm down. We’ve got a ways to go ” Waller said.

Investors cheered the soft CPI print, released Thursday, driving stocks up to their best week since June. The S&P 500 index

SPX,

closed 5.9% higher for the week.

The data showed that the yearly rate of consumer inflation fell to 7.7% from 8.2%, marking the lowest level since January. Inflation had peaked at a nearly 41-year high of 9.1% in June.

Waller said it was good there was some evidence that inflation was coming down, but noted that there were other times over the past year where it looked like inflation was turning lower.

“We’re going to see a continued run of this kind of behavior and inflation slowly starting to come down, before we really start thinking about taking our foot off the brakes here,” Waller said.

“We’ve got a long, long way to go to get inflation down. Rates are going keep going up and they are going to stay high for awhile until we see this inflation get down closer to our target,” he added.

The Fed is focused on how high rates need to get to bring inflation down, and that will depend solely on inflation, he said.

Waller said “the worst thing” the Fed could do was stop raising rates only to have inflation explode.

The 7.7% inflation rate seen in October “is enormous,” he added.

The Fed signaled at its last meeting earlier this month that it might slow down the pace of its rate hikes in coming meetings.

The central bank has boosted rates by almost 400 basis points since March, including four straight 0.75-percentage-point hikes that had been almost unheard of prior to this year.

“We’re looking at moving in paces of potentially 50 [basis points] at the next meeting or the next meeting after that,” Waller said.

The Fed will hold its next meeting on Dec. 13-14, and then again on Jan. 31-Feb. 1.

At the same time, Powell said the Fed was likely to raise rates above the 4.5%-4.75% terminal rate that they had previously expected.

“The signal was ‘quit paying attention to the pace and start paying attention to where the endpoint is going to be,’” Waller said.

In the wake of the CPI report, investors who trade fed funds futures contracts see the Fed’s terminal rate at 5%-5.25% next spring and then quickly falling back to 4.25%-4.5% by November. That’s well below the levels prior to the CPI data.

[ad_2]

[ad_1]

Investors finally got the inflation reading they were looking for, and are likely to get a split government for the next two years. That combination propelled stocks to their best weekly showing since June. On Friday, the

S&P 500

even briefly crossed the 4,000 threshold, a level it hadn’t breached in two months.

The S&P ended the week 5.9% higher, closing just below 4,000. The

Dow Jones Industrial Average

rose 4.1%, and the

Nasdaq Composite

jumped 8.1%. It was the best weekly showing for the Nasdaq since March, and it came during a week when tech news seemed largely negative. Facebook parent

Meta Platforms

(ticker: META) announced that it will cut 11,000 jobs, the latest in a wave of Silicon Valley layoffs. The best thing Facebook can say for itself now is that it isn’t Twitter.

[ad_2]

[ad_1]

Billionaire Dallas Maverick’s owner Mark Cuban recently offered his perspective on the implosion of crypto platform FTX late this week.

“‘That’s somebody running a company that’s just dumb-as-fucking greedy.’”

Cuban, speaking on Friday at a conference in Washington, D.C. hosted by Sports Business Journal, shared the view that avarice was at the root of the downfall of one-time crypto darling Sam Bankman-Fried, whose firm FTX Group just filed for chapter 11 bankruptcy.

“So what does Sam Bankman [Fried] do, he’s just–‘gimme more, gimme more, gimme more.’ So I’m gonna borrow money, loan it to an affiliated company and hope and pretend to myself that the FTT tokens that are in there on my balance sheet are gonna to sustain their value.”

Check out: Mark Cuban says buying metaverse real estate is ‘the dumbest shit ever

FTX’s collapse marks a stunning turnabout for a company, which was once valued at $26 billion, and whose founder, Bankman-Fried was viewed by many in the crypto industry as a venerable actor in the Wild West of digital exchanges.

On Thursday, the 30-year-old entrepreneur tweeted: “I f—ked up, and should have done better,” referencing the collapse of his exchange.

Embattled FTX, short billions of dollars, sought bankruptcy protection after the exchange experienced the crypto equivalent of a bank run. FTX, an affiliated hedge fund Alameda Research, and dozens of other related companies also filed a bankruptcy petition in Delaware on Friday morning. Boasting a nearly $16 billion fortune recently, Sam Bankman Fried’s net worth had all but evaporated in the wake of the FTX implosion, according to the Bloomberg Billionaires Index.

The price of FTX’s native token FTT went down about 88.8% over the past seven days to around $2.74, according to CoinMarketCap data.

The U.S. Justice Department and the Securities and Exchange Commission are looking into the crypto exchange to determine whether any criminal activity or securities offenses were committed.

Regulators and are examining whether FTX used customer deposits to fund bets at Alameda Research, a no-no in traditional markets, according to reports.

Cuban, who is one of the stars of the investing show “Shark Tank” and owns the NBA’s Dallas Mavericks, is a big investor in crypto and blockchain-related platforms. According to a CNBC report, he has said that 80% of his investments that aren’t on Shark Tank are crypto-centric.

See: Tom Brady, Steph Curry and Kevin O’Leary set to lose big from FTX bankruptcy filing

For his part, Cuban is part of a class-action lawsuit accused of misleading investors into signing up for accounts with crypto platform Voyager Digital, which filed for bankruptcy in July. The suit alleges that Cuban touted his support for Voyager and referred to it “as close to risk-free as you’re gonna get in the crypto universe.”

Cuban mentioned Voyager in his Friday interview. Representatives for the billionaire investor didn’t immediately respond to a request for comment.

The Mavericks owner took to Twitter on Saturday to say that the crypto implosions “have been banking blowups. Lending to the wrong entity, misvaluations of collateral, arrogant arbs, followed by depositor runs.”

Cuban’s net worth is $4.6 billion, according to Forbes.

[ad_2]

[ad_1]

Investors feeling giddy about last week’s sharp rally for stocks might want to give a listen to Tom Waits’ song, “Whistlin’ Past the Graveyard” from 1978, to sober up for the dangers that still lurk ahead.

The surge in stocks catapulted the S&P 500 index

SPX,

almost back to the 4,000 mark on Friday, also lifting it to the biggest weekly gain in roughly five months, according to Dow Jones Market Data.

Investors showed courage on signs of a slight slowing of inflation, but the fortitude also comes as a drearier backdrop for investors has been unfolding in plain sight. Massive layoffs at big technology companies, the dramatic implosion of crypto-exchange FTX, and the day-to-day pain of high inflation and skyrocketing borrowing on businesses and households are all taking a toll.

“We are not convinced this is the beginning of a new bull market,” said Sam Stovall, chief investment strategist at CRFA Research. “We believe that we are headed for recession. That has not been factored into earnings estimates and, therefore, share prices.”

Stovall also said the stock market has yet to see the “traditional shakeout of confidence capitulation that we typically see that marks the end of the bear markets.”

From Meta Platforms Inc.

META,

to Lyft Inc.

LYFT,

to Netflix Inc.

NFLX,

there is a wave of major technology companies resorting to layoffs this fall, a threat that could sweep other sectors of the economy if a recession materializes.

Yet, information technology stocks in the S&P 500 jumped 10% for the week, while financials, which stand to benefit from higher interest rates, rose 5.7%, according to FactSet.

That could reflect optimism about the odds of a slower pace of Federal Reserve rate hikes in the months ahead, after sharp rate rises helped to undermine valuations and pull tech stocks dramatically lower in the past year. However, Loretta Mester, president of the Cleveland Fed, and other Fed officials since the October inflation reading on Thursday have reiterated the need to keep rates high, until 7.7% annual rate finds a clearer path to the central bank’s 2% target.

The stock-market rally also might suggest that investors view continued mayhem in the crypto sector as contained, despite bitcoin

BTCUSD,

trading near its lowest level in two years and the shocking collapse in recent days of FTX, once the world’s third-largest cryptocurrency exchange.

Read: FTX’s fall: ‘This is the worst’ moment for crypto this year. Here’s what you should know.

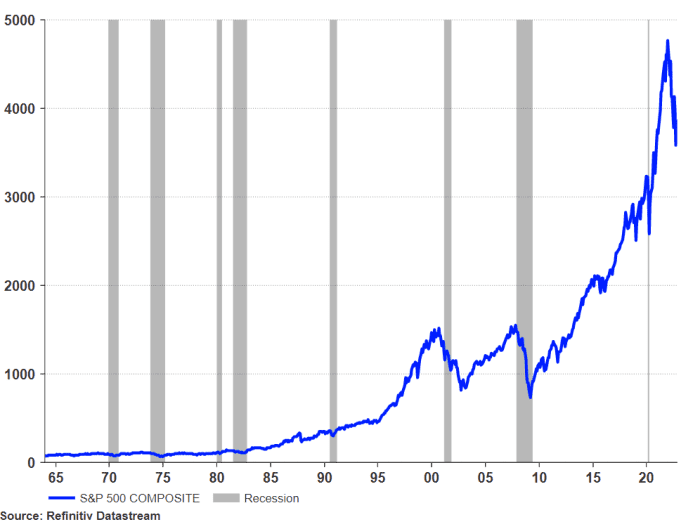

Blows to the American economy rarely have been good for stocks. A look at seven past recessions, starting in 1969, shows declines for the S&P 500 as more typical than gains, with its most violent drop occurring in the 2007-2009 recession.

Refinitiv data, London Stock Exchange Group

While a looming U.S. recession isn’t a foregone conclusion, CEOs of America’s biggest banks have been warning about the risks for months. JP Morgan Chase’s Jamie Dimon said in October that a “tough recession” could drag the S&P 500 down another 20%, even though he also said consumers were doing fine, for now.

Still, the steady stream of warnings about the recession odds have left many Americans confused and wondering if one can even happen without an increase in job losses.

Big moves lately in stocks also have been hard to decode, given the economy was shocked back to life in the pandemic by trillions of dollars in fiscal stimulus and easy-money policies from the Fed that are now being reversed.

“What I think goes unnoticed, certainly by the average person, is that these moves are not normal,” said Thomas Martin, senior portfolio manager at Globalt Investments, about stock swings this week.

“It’s all about who is positioned how — and for what — and how much leverage they’re employing,” Martin told MarketWatch. “You get these outsized moves when people are offside.”

Here’s a view of the sharp trajectory upward of the S&P 500 since 2010, but also its dramatic drop this year.

Refinitiv Datastream

While Martin isn’t ruling out the potential for a seasonal “Santa Claus” rally heading into year-end, he worries about a potential leg lower for stocks next year, particularly with the Fed likely to keep interest rates high.

“Certainly what’s being priced in now is either no recession or a very, very mild recession,” he said .

However, Kristina Hooper, Invesco’s chief global market strategist, said the overarching story might be one of stocks sniffing out the first steps in a path to economic recovery, and the Fed potentially stopping its rate hikes at a lower “terminal” rate than expected.

The Fed increased its benchmark interest rate to a 3.75% to 4% range in November, the highest in 15 years, but also has signaled it could top out near 4.5% to 4.75%.

“If often happens that you can see stocks do well, in a less-than-good economic environment,” she said.

The S&P 500 rose 4.2% for the week, while the Dow Jones Industrial Average

DJIA,

gained 5.9%, posting its best weekly gain since late June, according to Dow Jones Market Data. The Nasdaq Composite Index shot up 8.1% for the week, its best weekly stretch in seven months.

In U.S. economic data, investors will get an update on household debt on Tuesday, retail sales and homebuilder data on Wednesday, followed by jobless claims and housing starts data Thursday. Friday brings existing home sales.

[ad_2]

[ad_1]

Sam Bankman-Fried, co-founder at crypto exchange FTX, tweeted Friday that he was “shocked to see things unravel the way they did,” after he quit as chief executive and the company and its related entities filed for bankruptcy.

The bankruptcy “doesn’t necessarily have to mean the end for the companies or their ability to provide value and funds to their customers chiefly, and can be consistent with other routes,” Bankman-Fried tweeted Friday.

Bankman-Fried has seen his net worth plunge to almost zero from $16 billion in less than a week, according to Bloomberg Billionaires index.

FTX was once the third largest cryptocurrency exchange by trading volume. Bitcoin

BTCUSD,

fell 3.4% Friday to around $16,838, hovering at around a two-year low, according to the CoinDesk data.

A representative at FTX didn’t respond to a request seeking comment.

[ad_2]

[ad_1]

FTX, the crypto exchange, filed for voluntary Chapter 11 bankruptcy in a Delaware court on Friday, and chief executive Sam Bankman-Fried has resigned.

Following the news, here is how prices are doing for major cryptocurrencies, according to CoinDesk data.

Bitcoin BTCUSD, -4.92% The price for Bitcoin was around $19,350 before the announcement of the potential FTX/Binance deal on Tuesday. The price jumped to $20,590 in less than an hour after the announcement. But dropped to a 2-year low of $17,484. Currently, the Bitcoin price is $16,907.19, a change of -5.04% over the past 24 hours.

Ethereum ETHE, -9.66% Currently, the Ethereum price is $1,252.60, a change of -6.60% over the last 24 hours. The price of Ethereum was around $1,438 before the announcement, and peaked at $1,562 under an hour after. Later on Nov 8, the price dropped to $1,289.

FTT: Today the price of FTT, which is the FTX token, is $2.74, down 20.37% in the last 24 hours, according to CoinMarketCap data. At the beginning of the week, on Nov 7, the price was around $22.06.

Solana: Currently, the price is $17.34, a change of 2.91% over the past 24 hours. The price of Solana before the announcement was around $27.69, and peaked at $31.29 shortly after the announcement.

Binance Coin: The Binance Coin price is $285.74, a change of -7.02% over the past 24 hours. The Binance Coin price was around $322 before the announcement that Binance might acquire FTX on Nov 8.

[ad_2]