Shares of Alibaba Group Holding Ltd. were rallying more than 2% in Thursday’s premarket trading after the Chinese e-commerce giant topped expectations with its latest revenue and earnings.

The company notched fiscal first-quarter net income of RMB34.3 billion ($4.6 billion), or RMB13.30 per American depositary share, compared with net income of RMB22.7 billion, or RMB8.51 per ADS, in the year-before period.

On an adjusted basis, Alibaba BABA, +0.67%

earned RMB17.37 per ADS, while the FactSet consensus was RMB14.59 per share. Revenue rose to RMB234.2 billion from RMB205.6 billion, where analysts had been modeling RMB224.7 billion.

Chief Executive Daniel Zhang said the company’s reorganization was “beginning to unleash new energy across our businesses.” Alibaba recently realigned into six units with their own CEOs and boards of directors, and the ability to pursue independent fundraising.

“Through this self-driven transformation, we aim to catalyze innovation, promote vitality in our organization and enable businesses to focus on long-term growth,” Zhang continued. “We look forward to positive impacts on our business, including strengthening competitiveness, sustainable growth and shareholder value creation.”

Overall revenue for the company’s Taobao and Tmall Group, which represents the company’s core e-commerce marketplaces in China, rose to RMB115.0 billion from RMB102.5 billion.

Within that group, customer management revenue was up 10% to RMB79.7 billion, “primarily due to the increase in merchant’s willingness to invest in advertising” and an increase in the volume of online physical goods generated on the platforms.

Alibaba bought back $3.1 billion worth of ADRs during the June quarter, “which is supported by our continuous generation of strong free cash flow,” Chief Financial Officer Toby Xu said in the release. Free cash flow was RMB39.1 billion in the quarter, up 76% from a year earlier.

U.S.-listed shares of Alibaba are up about 8% so far this year.

Investors should think twice before picking an actively managed mutual fund according to its style category. By “style category,” I’m referring to the widely used method of grouping mutual funds according to the market-cap of the stocks they invest in and where those stocks stand on the spectrum of growth-to-value.

This matrix traces to groundbreaking research in 1992 by University of Chicago professor Eugene Fama and Dartmouth College professor Ken French, and has since been popularized by investment researcher Morningstar in the form of its well-known style box.

In urging you to think twice before picking a fund based on this matrix, I’m not questioning the existence of important distinctions between the various styles. Fama and French’s research convincingly showed that there are systematic differences between them. My point is that there also are huge differences within each style as well. You can pick a style that outperforms all others on Wall Street and still lose a lot of money, just as you can pick the worst-performing style and turn a huge profit.

This points to the two types of risk you face when picking an actively managed fund. You have the risk associated with the fund’s style (category risk) and you also have the risk associated with the particular stocks that the fund’s manager selects (so-called idiosyncratic risk). Idiosyncratic risk often overwhelms category risk, especially over shorter periods.

To illustrate, consider the midcap-growth style. As judged by the Vanguard Mid-Cap Growth ETF VOT,

this style produced a 28.8% loss in 2022. Yet, according to Morningstar Direct, the best-performing actively managed midcap-growth fund last year produced a gain of 39.5%, while the worst performer lost 67.0%.

This best-versus-worst performance spread of over 100 percentage points is illustrated in the accompanying chart. Notice that the comparable spread was almost as wide for many of the other styles as well. Though I haven’t done the research to compare 2022’s spreads with those of other calendar years, I have no reason to expect that they on average were any lower.

“ The only way to eliminate idiosyncratic risk when investing in particular styles is to invest in an index fund.”

The only way to eliminate idiosyncratic risk when investing in particular styles is to invest in an index fund benchmarked to the style in question. If you are enamored of a particular fund manager and willing to bet he will significantly outperform the category average, just know that you also incur the not-significant idiosyncratic risk that the fund will lag by a large amount.

The bottom line? By investing in an actively managed fund in a style category, you will be incurring the risk not only of that category itself but also the not-insignificant idiosyncratic risk of that particular fund. Fasten your seatbelt if that’s the path you take.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

My colleagues JP Aubry and Yimeng Yin just released an update on state and local pension plans. Their analysis compared 2023 to 2019 – the year before all the craziness began. Think of the unusual events that have occurred in the last few years: 1) the onset of COVID; 2) the subsequent COVID stimulus; 3) declining interest rates; 4) rising inflation; and then 5) rising interest rates.

Despite the volatility of asset values over this period, the 2023 funded status of state and local pension plans is about 78%, which is 5 percentage points higher than in 2019 (see Figure 1). Of course, the numbers for 2023 are estimates based on plan-by-plan projections, but these projections have an excellent track record.

While the aggregate funded ratio provides a useful measure of the public pension landscape at large, it also can obscure variations in funding at the plan level. Figure 2 separates the plans into thirds based on their current actuarial funded status. The average 2023 funded ratio for each group was 57.6% for the bottom third, 79.5% for the middle third, and 91.1% for the top third.

The major reason for the improvement in plans’ funded status is that, despite the turbulence in the economy, total annualized returns, which include interest and dividends, have risen noticeably for almost all major asset class indexes over the 2019-2023 period (see Figure 3). The exception over this short and volatile period is fixed-income assets, which have declined in value.

The effect of fixed income’s decline on overall portfolio performance has been modest because, since 2019, fixed income has averaged only about 20% of pension fund assets (see Figure 4).

So, things are looking a little better for state and local pensions. Yes, the funded ratios are biased upward because plans use the assumed return on their portfolios – roughly 7% – to discount promised benefits. That said, trends are important, and the trend is good.

Moreover, annual state and local benefit payments as a share of the economy are approaching their peak for two reasons. First, most pension plans do not fully index retiree benefits for inflation, which lowers the real value of benefits over time. Second, the benefit reductions for new hires – introduced in the wake of the Great Recession – have started to have an impact.

With liabilities in check and solid asset performance, maybe we can all relax a bit about the future of the state and local pension system.

U.S. stocks would be in much worse shape in 2023 if it wasn’t for “excessive” fiscal policy from the government and explosive money-supply growth in recent years.

That’s the latest take from Morgan Stanley’s Mike Wilson, the bank’s chief investment strategist who, as MarketWatch’s Steve Goldstein pointed out earlier, seems to never miss an opportunity to recall how wrong his market calls have been this year.

In his latest note, Wilson told clients and the financial press that excessive government spending has helped prop up the U.S. economy and markets to a degree that Wilson and his team failed to anticipate.

“Part of the reason we’ve found ourselves offside this year is that the fiscal impulse returned with a vengeance and remained quite strong in 2023 — something we didn’t factor into our forecasts,” Wilson said in the note.

In an accompanying chart, Wilson noted that fiscal spending looks particularly excessive when compared with the U.S. unemployment rate, which fell to 3.5% in July, according to data from the Department of Labor released on Friday.

MORGAN STANLEY

To be sure, Wilson was one of a select few on Wall Street to correctly anticipating last year’s inflation-driven selloff.

But heading into the New Year, he expected stocks would tumble to new lows during the first half of 2023.

And after hanging on to his bearish view for months in spite of a powerful rally in equities driven by the artificial intelligence craze and a surprisingly resilient U.S. economy, he’s recently taken the opportunity to reflect on why he got it wrong, while acknowledging the possibility that the rally could continue.

It’s possible, even likely, that the government’s excessive spending could continue, at least until it comes time to raise the debt ceiling again in 2025.

Fitch Ratings last week cited projections for ballooning budget deficits for helping to inspire its decision to strip the U.S. of its AAA credit rating.

“The main takeaway for the equity market this year is that fiscal policy has allowed the economy to grow faster than forecast, giving rise to the consensus view that the risk of a recession has faded considerably. Furthermore, with the recent lifting of the debt ceiling until 2025, this aggressive fiscal spending could continue,” Wilson said.

The biggest problem with spending so much during good economic times, however, is that it limits Congress’s ability to act when another recession inevitably arrives.

That could create problems for corporate earnings and, by extension, stocks, down the road, Wilson said.

“If fiscal policy is showing such little constraint in good times, what happens to the deficit when the next recession arrives?”

U.S. stocks were trading higher early Monday after the S&P 500 SPX

logged its fourth straight day in the red on Friday, capping off the worst week for stocks since March. The index was up 0.5% in recent trade near 4,500, while the Nasdaq Composite COMP

was 0.2% lower at 13,881.

The Dow Jones Industrial Average DJIA,

which has surged higher over the past month as traders have favored some of this year’s market laggards, was up 300 points, or 0.9%, at 35,362.

The U.S. stock market has been conspicuously calm for most of 2023, prompting some analysts to question whether investors might be overdue for a powerful jolt of volatility.

It’s been 113 trading sessions since the S&P 500 has seen a daily drop of 2% or more, the longest such stretch since Feb. 21, 2020, according to Dow Jones Market Data.

The last time the large-cap index fell by 2% or more through the close was Feb. 21, 2023, when the index dropped by 2% exactly. That was nearly six months ago.

Such subdued volatility is perhaps the most pertinent indication of just how much has changed for markets since 2022.

When measured by the total number of 2% swings in either direction, last year was the most volatile for U.S. stocks since 2009. The S&P 500 recorded 46 daily swings of 2% or more in either direction last year, compared with 55 in 2009, Dow Jones data show. Of those, roughly half were down days.

This quiet streak has been good for stocks: Since Feb. 21, the S&P 500 has gained nearly 13%, according to FactSet data. And as of Thursday, it was up more than 18% for the year.

But as August has gotten off to a rocky start, with the S&P 500 and Nasdaq Composite on track to finish lower for the first week of the month following a three-day streak of losses, some are wondering if the market might be overdue for a larger and perhaps more aggressive drop.

To the extent that the market’s past performance can tell investors anything useful about the future, historical data compiled by Dow Jones Market Data show that streaks of relative calm have endured for much longer in the not-too-distant past.

However, investors have often paid the price eventually.

The longest streak in recent memory without a 2% drop for the S&P 500 ended on Feb. 1, 2018 after 351 trading days — nearly 18 months. It encompassed all of 2017, a memorably tranquil year for markets that saw the Cboe Volatility Index fall to an all-time low in single-digit territory.

A few days later, stocks would see one of their biggest daily routs in years during the now-infamous “Volmageddon” episode on Feb. 5, 2018 when the Dow Jones Industrial Average fell by 1,175 points while the Cboe Volatility Index, otherwise known as the VIX, doubled, jumped by a record 20 points from 18.44 to a high of 38.40, FactSet data show.

At the time, it was the biggest daily point decline on record for the Dow. Data also show that the index has traded lower one year after the end of such streaks two out of five times.

Date Streak Ended

Length of Streak

6-Month Performance

1-Year Performance

10/08/2014

125

5.74%

2.26%

6/26/2015

179

-1.93%

-3.05%

02/01/2018

351

-0.31

-4.09%

10/09/2018

129

-0.07%

1.36%

02/21/2020

124

1.78%

17.05%

SOURCE: DOW JONES MARKET DATA

Ryan Detrick, chief market strategist at Carson Group, said stocks might be ripe for a larger pullback in August, although he acknowledged that streaks of low volatility have often persisted for much longer.

“While these periods of low volatility can increase the odds of some type of near-term pull back, these trends can last a while,” Detrick said during a phone interview with MarketWatch.

“We might be overdue for a modest 4% to 6% pullback here, but it makes sense that this low-volatility world we’ve been living in could have legs.”

Detrick noted that 2022 saw the biggest pullback for the S&P 500 since 2008 as the index fell 19.4%, according to FactSet data.

To be sure, the selloff in the bond market was even more intense, with many analysts describing it as the worst year for bonds in decades, if not in the history of modern financial markets.

“The whole apple cart got rocked last year,” he said.

Detrick also noted that August and September tend to be more volatile months for stocks.

“The odds are higher that we could see some seasonal volatility here,” he said. “August isn’t a great month for stocks, but it’s even worse when you’ve had a good year going into it,” he said.

U.S. stocks rebounded on Friday following the release of the Labor Department’s July jobs report. The S&P 500 SPX

was up 0.8% in recent trade, while the Nasdaq Composite COMP

rose by 1%. The Dow DJIA

was trading 256 points, or 0.7%, higher at 35,474.

A worsening U.S. fiscal situation caught stock and bond investors off guard in the past week and now a round of approaching government auctions is about to provide a crucial test for Treasurys.

The question in the days ahead is whether risks to the demand for U.S. government debt are growing. If so, that could put upward pressure on Treasury yields, which would undermine the performance of stocks. However, if investors end up caring less about the fiscal situation than they do about the possibility of slowing economic growth and decelerating inflation, government debt’s safe-haven appeal could be reinforced, putting a limit on how high yields might go.

Concern about the deteriorating fiscal outlook was a factor behind the past week’s rise in long-term Treasury yields. Ten- BX:TMUBMUSD10Y

and 30-year yields BX:TMUBMUSD30Y

respectively jumped to 4.188% and 4.304% on Thursday, the highest levels since early November, as investors sold off long-term government debt — which took the shine off U.S. stocks. By Friday, though, a moderating pace of U.S. job creation for July sent yields into reverse, giving equities a temporary lift during the final trading session of the week.

At issue is the extent to which potential buyers of Treasurys may be deterred by Fitch Ratings’ Aug. 1 decision to cut the U.S. government’s top AAA rating, at a time when the government is about to unleash what Barclays rates strategists describe as a “tsunami” of supply. A total of $103 billion in 3-, 10-and 30-year Treasurys come up for sale between Tuesday and Thursday. In addition, a spate of Treasury bills are scheduled to be auctioned starting on Monday.

Gene Tannuzzo, global head of fixed income at Boston-based Columbia Threadneedle Investments, said that while he and his team still have room to add T-bills to the government money-market funds they oversee during the week ahead, they haven’t made up their minds about whether to buy more longer-dated maturities for their bond funds.

“While we are comfortable that the Fed is at or near the end of its rate hikes, there are a lot more questions about the durability of the economic recovery, the degree that inflation will remain low, and the risk premium that needs to be put in at the long end,” Tannuzzo said via phone.

Treasury’s $1 trillion third-quarter borrowing plans, along with some technical issues and the Bank of Japan’s decision to switch to a more flexible yield-curve control approach, might reduce demand for U.S. government debt, he said. Columbia Threadneedle managed $617 billion as of June.

“One can’t ignore the risk of an unruly rise in yields, but our view is that this is a low risk and what the Treasury auctions may produce instead is ‘indigestion,’ driven by poor technicals and low liquidity, Fitch’s downgrade, and the Bank of Japan action — and by the end of August, we should be past much of this,” he told MarketWatch.

Risks to the demand for Treasurys may become obvious soon, given Tuesday-Thursday’s $103 billion in total sales of 3-, 10- and 30-year securities, according to analyst John Canavan of U.K.-based Oxford Economics. The main “question mark” for the market’s ability to absorb the increased Treasury issuance will be whether or not domestic investment funds continue to show interest, Canavan wrote in a note distributed on Friday.

Source: Oxford Economics.

“ ‘My suspicion is that with higher rates comes equally solid demand’ at upcoming auctions.”

— John Flahive, head of fixed income at BNY Mellon Wealth Management

Market players have had little difficulty absorbing Treasury coupon issuances in recent years because of flight-to-safety trades made after the U.S. onset of the Covid-19 pandemic in 2020. Now, however, increased auction sizes are being accompanied by still-elevated inflation, better-than-expected economic growth, and the possibility of more rate hikes by the Federal Reserve — which is likely to complicate the market’s ability to absorb the increased supply “without hiccups,” Canavan said.

On the flip side of the debate is John Flahive, head of fixed income at BNY Mellon Wealth Management in Boston, which managed $286 billion in assets as of June. He said equity markets will continue to be much more focused on economic developments and earnings. And as long as the latter of the two remains robust, stocks “can grind higher in a low-volatility environment,” Flahive said via phone.

Saying he does not expect his team to be a major participant in the Treasury auctions, Flahive said that the bond market’s reaction in the past week was “a little overdone” and “we always felt that there was a limited to how much yields could go up to reflect more government debt.”

“My suspicion is that with higher rates comes equally solid demand” at upcoming auctions, he said. “I’m still optimistic about rates going back down over time as the result of a slowing economy and decelerating inflation. We continue to like the bond market and see a better-than-even chance that yields go down as the economy continues to weaken in the quarters ahead.”

Friday’s reaction to July’s official jobs report, which showed the U.S. added a modest 187,000 new jobs, provided a breather from the past week’s run-up in Treasury yields.

On Friday, the 30-year Treasury yield fell 9 basis points to 4.214%, yet still ended with its biggest weekly gain since early February. The 10-year rate, which dropped 12.8 basis points to 4.06%, finished with a third straight week of advances.

Stocks fell Friday, leaving major indexes with weekly declines. The Dow Jones Industrial Average DJIA

posted a 1.1% weekly fall, while the S&P 500 SPX

shed 2.3% and the Nasdaq Composite COMP

retreated 2.9%. The soft start to August comes after a run of sharp gains for equities. The S&P 500 remains up 16.6% for the year to date.

The economic calendar for the week ahead includes U.S. inflation updates.

On Monday, June consumer-credit data is set to be released. Tuesday brings the NFIB’s small business optimism index, plus data on the U.S. trade balance and wholesale inventories. Then on Thursday, weekly initial jobless claims and the July consumer-price index are released. That’s followed on Friday by the producer-price index for last month and an August consumer-sentiment reading.

Meanwhile, portfolio manager and fixed-income analyst John Luke Tyner at Alabama-based Aptus Capital Advisors, which manages roughly $5 billion in assets, said he plans to follow the Treasury auctions, but doesn’t usually participate in them.

“One of the biggest trends we’ve seen is the continued increase in the issuance amounts from Treasury. Whatever we are budgeting for is never enough, which justifies the Fitch downgrade,” Tyner said via phone. “It’s tough to say people aren’t going to buy U.S. debt, but you’ve got to entice them to buy duration and take the risk.

“The U.S. is not an emerging market, but ultimately we are going to see the market rate that participants require be higher, with a notable uptick in term premia,” he said. “What we could see in the face of all this issuance is a grind up in yields on an auction-by-auction basis. If I look at the technicals, a 4.9%-5% yield on the 10-year note seems in the cards,” and “it will be difficult for stocks to hold or expand from full valuations as rates run up.”

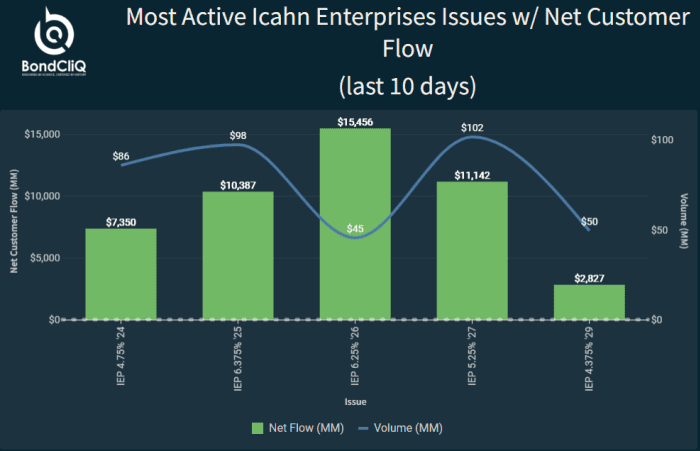

Icahn Enterprises Inc.’s bonds saw better buying on Friday, after Carl Icahn’s investing arm announced it was halving its quarterly distribution, a move that disappointed unit holders but is positive for its bonds.

Bondholders are typically focused on making sure a company can make its interest payments and repay the principal when a bond matures.

The company said it would now make a distribution of $1, down from $2 previously. The news came as the company posted a surprise loss for the second quarter and a $1 billion decline in revenue.

Icahn placed the blame for the fund’s poor performance on Hindenburg Research, the short seller that published a report about IEP on May 2, accusing it of overstating asset values. Hindenburg also revealed that Icahn himself had borrowed from the company, among other issues.

The stock promptly tumbled and was last down 24%, putting it on track for its biggest one-day selloff since it went public 36 years ago. The next biggest drop was 20.0% on May 2, when the Hindenburg Research report was released.

As the chart below from data-as-a-service provider BondCliQ Media Services shows buyers emerging after 8:00 a.m. Eastern, immediately after the news was announced. By midmorning, some sellers had emerged.

Icahn Enterprises net customer flow (intraday). Source: BondCliQ Media Services

The following table shows there was net buying over the last 10 days, focused on the 6.35% notes that mature in 2026.

Most active Icahn Enterprises issues with net customer flow (last 10 days). Source: BondCliQ Media Services

In a letter to unit holders accompanying the results, Icahn acknowledged missteps in the past several years as the company has shifted away from its core activist strategy and shorted far more than was necessary.

“While we made money on the long side through our activism efforts, our returns have been overwhelmed by our overly bearish view of the market and related oversized short (hedge) positions,” Icahn wrote. “Over the past six months, we have significantly reduced our hedges. Going forward, we intend to stick to our knitting and focus on our activist strategy while remaining appropriately hedged.”

Activism is the best investment paradigm because “there is no accountability in Corporate America,” he wrote.

With many exceptions, “most CEOs are incapable of creating great businesses (or even improving them) and the desire to empire build is rampant. “

Many are not the best person for the job or even the most talented individual in the organization, he continued. Far too often, they have climbed through the ranks by being agreeable and presenting no threat to their superiors.

“Those CEOs are generally too busy playing at the proverbial country club to realize what improvements can be made or what hidden jewels can be unlocked,” he said.

CEOs are hard to unseat, as they can pack a board with loyal cronies and use company funds to defend against an activist campaign by hiring expensive legal and financial experts, further depleting the coffers.

Icahn has himself waged endless activist campaigns against companies and their management teams, and most recently succeeded in his effort to shake up management at gene sequencing test maker Illumina Inc. ILMN, +1.85%, as the Associated Press reported.

Past activist campaigns by Icahn’s company have generated billions of dollars for shareholders and helped boards and CEOs capture untapped value, Icahn has argued, citing Reynolds, Netflix NFLX, +0.66%,

Forest Labs, Apple AAPL, -3.72%,

CVR Energy CVI, -0.40%,

Herbalife HLF, -0.32%

eBay EBAY, -0.73%,

Tropicana, Cheniere LNG, +0.27%

and Occidental OXY, +3.14%

as examples.

Blackstone chief executive officer Steve Schwarzman said Fitch Ratings’ recent downgrade to long-term U.S. debt was justified, and it is a “shot across the bow” after repeated debt-ceiling standoffs over the borrowing limit make the U.S. government less trustworthy than before.

“We’ve had an explosion of debt since the global financial crisis and we don’t appear to have a lot of discipline going forward,” Schwarzman said in a CNBC interview on Friday. “We’re running huge deficits now.”

Fitch Ratings late Tuesday lowered its rating on the U.S.’ long-term foreign currency issuer default rating to AA+ from AAA, saying that it reflects “expected fiscal deterioration,” a “high and growing” government debt burden and an “erosion of governance” in face of multiple debt-limit standoffs.

Fitch’s ratings downgrade was the first for the U.S. sovereign debt since Standard & Poor Global Ratings took the same step in 2011, cutting the nation’s credit rating to AA+ from AAA also after a debt-ceiling standoff in Congress. Moody’s Investors Service has kept its U.S. credit rating at Aaa, its highest, and remains the last of the three major credit credit-rating firms to maintain a top rating for the country.

Treasury Secretary Janet Yellen on Wednesday slammed the move by Fitch Ratings, calling it “arbitrary and based on outdated data” as it came two months after a debt-ceiling agreement that averted a U.S. default. She said the decision “does not change what Americans, investors, and people all around the world already know: that Treasury securities remain the world’s pre-eminent safe and liquid asset, and that the American economy is fundamentally strong.”

Schwarzman said regardless of the rating, the U.S. dollar is the world’s reserve currency. “We do defend a large part of the world including people who have triple As, and when there’s a crisis in the world, they buy our securities,” he said on Friday.

“Now that doesn’t last forever if you don’t keep some discipline. And so in a way, it’s a bit of a shot across the bow,” Schwarzman said.

U.S. stocks were holding gains Friday following the July jobs report, with the Dow Jones Industrial Average DJIA

up 170 points, or 0.5%, while the S&P 500 SPX

also advanced 0.5%.

Tupperware Brands Corp.’s stock climbed more than 90% in extended trading Thursday after the beleaguered maker of iconic food containers announced a debt restructuring agreement.

The surge sent the stock hurtling toward a nine-month high. In a statement released after market close, Tupperware TUP, -4.09%

said that it has finalized an agreement with its lenders to restructure its existing debt obligations. The agreement will improve the company’s overall financial position by amending certain credit obligations and extending the maturity of certain debt facilities to allow it to continue with its turnaround efforts, Tupperware said.

The agreement provides for the reduction/reallocation of $150 million in interest and fees, and an extension of the stated maturity of approximately $348 million of principal and reallocated interest and fees to fiscal year 2027 with payment-in-kind, or PIK, interest.

Tupperware also announced the reduction of amortization payments required to be paid through fiscal year 2025 by approximately $55 million, and immediate access to a revolving borrowing capacity of approximately $21 million.

“I am confident that this agreement provides us with the financial flexibility to continue executing on our near-term turnaround efforts as well as our long-term strategy to create a global omni-channel consumer brand,” Tupperware CFO Mariela Matute said in the statement. “We are committed to making ongoing progress in improving liquidity and strengthening our capital structure. We appreciate the support of our lenders, who share in our strategy, as we move forward.”

In April, Tupperware issued a going-concern warning, essentially cautioning that it could go bust. The beleaguered company also announced the hiring of financial advisers to help it navigate its near-term challenges. On July 7, Tupperware said that it had entered a waiver agreement with some of its creditors.

Also on Thursday, Tupperware said that its second-quarter earnings report will be filed late. In an SEC filing, Tupperware explained that it is unable to file its report for the quarter ended July 1 by the prescribed due date. Tupperware cited “the time and effort” required to complete its consolidated financial statements for its Form 10-K annual report for the fiscal year ended Dec. 31, 2022 and the Form 10-Q for the quarter ended April 1, 2023. “The company will be unable, without unreasonable effort or expense, to complete and file the Q2 Form 10-Q within the prescribed time period,” it said. “As previously disclosed on its Form 8-K on April 7, 2023, the Company is continuing its restatement of previously issued financial statements and the financial statement close process for the year ended December 31, 2022.”

Since the 8-K filing, Tupperware has “identified additional prior period misstatements and additional material weaknesses in internal control over financial reporting,” the company said. The April 7 8-K filing also disclosed the company’s “substantial doubt” about Tupperware’s ability to continue as a going concern. “While the Company is still completing its second-quarter 2023 financial close process, it expects that its Q2 Form 10-Q will reflect a material decline in revenues for the quarter ended July 1, 2023 as compared to the quarter ended June 25, 2022,” Tupperware said in the filing. “The Company believes that its preliminary estimated revenue results for the quarter ended July 1, 2023 will be within the range of $260-$270 million.”

Tupperware’s stock has skyrocketed recently, despite a dearth of fresh news. Nonetheless, Tupperware should not be confused with a meme stock, according to Samantha LaDuc, founder of LaDucTrading.com. Tupperware’s recent trading activity is also reminiscent of spikes in other names also recently seen as “left for dead,” as LaDuc put it to MarketWatch last week.

As you’ve probably heard by now, Fitch Ratings late Tuesday cut the U.S. federal government’s credit rating to AA+ from AAA.

Here’s a look at what it means for investors and markets:

What’s a credit rating?

A credit rating is an independent assessment of the ability of an organization, including corporations and governments, ranging from school boards to cities, counties, states and countries, that have issued debt to meet their obligations. Fitch — alongside S&P Global and Moody’s Investors Service — is one of the world’s big three ratings firms.

The ratings firms use scales that employ letters, and in Moody’s case also include numbers, to provide a guide to creditworthiness. At the top of the list is the AAA rating from S&P and Fitch, or Aaa, in the case of Moody’s. AA+ is the second-highest rating.

Ratings that employ Cs are at the bottom of the scales, with Fitch and S&P using D ratings in cases of default or bankruptcy.

Any rating below BBB- from Fitch and S&P, or Baa from Moody’s, is considered below “investment grade.” Such debt is often termed “junk.”

Why did the U.S. rating get cut

Fitch had warned in May that a cut was possible, with the ratings firm expressing dismay over what it termed another round of “brinkmanship” around the U.S. government’s debt ceiling. The warning came amid a battle between congressional Republicans and the Biden administration over lifting or suspending the federal government’s debt ceiling.

The limit has been a frequent source of political squabbling. While the showdown was resolved with a two-year suspension of the limit, the battle underlined the high stakes. Failure to reach a deal could have led to a default. In Tuesday’s decision, Fitch said that the past two decades have seen “a steady deterioration in standards of governance” in the U.S., the debt-ceiling agreement notwithstanding.

How does the U.S. rating stack up to other countries

Fitch isn’t the first of the big three ratings firms to strip the U.S. of its AAA rating. S&P did so in 2011, amid an earlier debt-limit battle. That leaves Moody’s as the only firm to still assign the U.S. its top rating.

The pool of triple-A sovereign ratings, meanwhile, continues to dwindle. Only a handful of countries carry triple-A ratings across the board from all three ratings firms.

The cut isn’t seen having much lasting effect on investor demand for U.S. Treasurys. The market for Treasurys is the largest and most liquid debt market in the world. Despite the lack of triple-A ratings, Treasurys are viewed and treated by investors as being virtually “risk-free,” or equivalent to cash. Other types of debt are often quoted in terms of the yield premium, or spread, demanded by investors to hold them over Treasurys.

That isn’t going to change overnight. Analysts have emphasized that investors don’t buy Treasurys based on the credit rating. And any outflows from funds that are required to hold only triple-A rated bonds are expected to be limited.

“Many major Treasury holders, such as funds and index trackers, have already prepared for the move by changing mandates to specifically refer to Treasurys rather than AAA credit, and are unlikely to be forced into selling given the importance of the asset class,” said Solita Marcelli, chief investment officer for the Americas at UBS Global Wealth Management, in a Wednesday note.

How are markets reacting?

The downgrade was blamed for a weak tone across global equity markets, with U.S. stocks following suit. The Dow Jones Industrial Average DJIA

dropped around 315 points, or 0.9%, while the S&P 500 SPX

shed 1.3%. The moves come after a strong run of gains, however.

Treasury yields, which move opposite to price, were higher. The selling, however, took hold only after data from ADP that showed a stronger-than-expected rise in private-sector payrolls. Treasurys took the downgrade in stride in earlier trading, with yields moving lower.

The yield on the 10-year Treasury note BX:TMUBMUSD10Y

was up around 2 basis points near 4.02%.

Marcelli recalled that in 2011 the yield on the 10-year U.S. Treasury fell around 50 basis points, or half a percentage point, in the three days after the S&P downgrade to 2.6% on Aug. 5. Even 15 trading days later, yields were still down 40 basis points from the day of the downgrade, and around 80 basis points lower compared with where they were 15 trading days before the move.

U.S. stock futures stumbled Wednesday after markets were rattled by a downgrade to the U.S. government’s credit rating.

How are stock-index futures trading

S&P 500 futures ES00, -0.73%

dipped 42 points, or 0.9%, to 4559

Dow Jones Industrial Average futures YM00, -0.51%

fell 257 points, or 0.7%, to 35500

Nasdaq 100 futures NQ00, -1.04%

lost 204 points, or 1.3%, to 15613

On Tuesday, the Dow Jones Industrial Average DJIA

rose 71 points, or 0.2%, to 35631, the S&P 500 SPX

declined 12 points, or 0.27%, to 4577, and the Nasdaq Composite COMP

dropped 62 points, or 0.43%, to 14284.

Fitch’s move follows a similar downgrade by S&P more than a decade ago. The U.S. Treasury market acts as a global benchmark upon which many financial products are based and so uncertainty about its stability can cause anxiety for investors.

The news found a stock market arguably vulnerable to unwelcome surprises, with the S&P 500 having already gained 19.2% this year and the tech-heavy Nasdaq Composite up 36.5%.

The CBOE VIX Index , an option-based gauge of expected S&P 500 volatility, jumped 16% to 16.2, its highest in nearly four weeks.

Traditional perceived havens saw demand, with the Japanese yen USDJPY, -0.41%

gaining 0.7%, gold GC00, +0.34%

nudging up to $1,950 an ounce, and benchmark German government bond yields BX:TMBMKDE-10Y

moving lower. U.S. 10-year Treasury yields BX:TMUBMUSD10Y

were little changed at 4.03%.

However, most analysts did not see the downgrade causing the stock market much long term damage.

“While debt downgrades seldom, if ever, have long legs, investors may pause and let the dust settle before re-entering risk markets. However, within this super market-friendly environment of stable growth and a Fed close to the end of its hiking cycle creating fertile ground for stock gains, its unlikely risk sentiment will wander too far off the soft landing path,” said Stephen Innes, managing partner of SPI Asset Management.

Sophie Lund-Yates, lead equity analyst at Hargreaves Lansdown, said “the market remains sensitive as the final throes of earnings season rumble on, but 82% of S&P 500 companies that have reported results so far have surprised to the upside, offering a bit of a sentiment buffer.”

It’s become a common refrain among those who believe the 2023 stock-market rally seems too good to last: by almost any measure one chooses, equity valuations in the U.S. are looking stretched.

While this point is generally conceded by equity analysts, it glosses over another debate of potentially greater import. What impact, if any, do so-called fundamental factors like valuation have on stock-market performance, and could we really see them put the breaks on a momentum-driven rally?

At least for now, the answer may be that valuation is taking a back seat to hopes tied to artificial-intelligence and the strength of the U.S. economy fuel optimism that could continue to push the market higher.

“Every investors should explore fundamentals, but you have periods of momentum where fundamentals take a back seat,” said Liz Young, head of investment strategy at SoFi, during a phone interview with MarketWatch.

Valuations are looking stretched

Investors buying stocks today are paying more per unit of expected earnings than at any point since April of 2022, when interest rates were much lower than were they are now. The forward price-to-earnings ratio for the S&P 500 SPX, -0.23%

currently stands at 19.7, according to FactSet data.

That is higher than the five-year average of 18.6, and the 10-year average of 17.4, FactSet data show.

To be sure, the P/E for S&P 500 index companies masks a remarkably wide dispersion internally. An analysis by Goldman Sachs analysts found that the so called “magnificent seven” technology stocks are currently sporting a P/E of 31, while the remaining 493 companies in the index are being valued at 17.

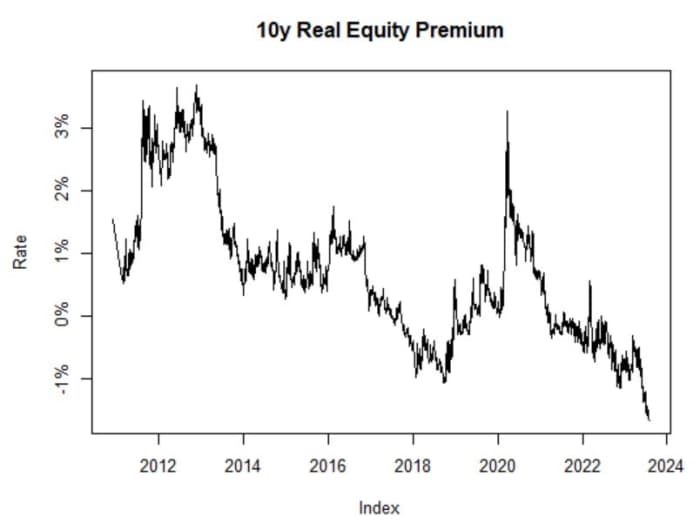

Another closely watched valuation metric that compares the value investors could reap from owning stocks with that of owning comparatively safer Treasury bonds is looking even more extreme.

The equity risk premium (ERP) has fallen to its lowest level since mid-2002, according to data analysis conducted by MarketWatch and Sierra Investment Management CIO James St. Aubin.

JAMES ST. AUBIN

According to Aubin, the reason investors are willing to accept such a low equity risk premium instead of parking their money in short-term Treasury bills yielding more than 5% is that corporate earnings growth is expected to accelerate markedly starting in 2024.

In the past, investors have been willing to accept a low or even negative ERP if they believed they would be well-compensated for it by explosive earnings growth further out in the future. And the AI craze is bolstering expectations that some of the largest U.S. technology firms could reap windfall profits while boosting productivity across the U.S. economy.

“You’re willing to accept a low ERP, or in the case of the 1990s, even a negative ERP, if you think you’re going to have strong earnings growth,” St. Aubin said during a phone interview with MarketWatch.

Great expectations

Right now, Wall Street analysts expect to see earnings growth rise next year following several consecutive quarters of declines in late 2022 and the first half of 2023.

Although many S&P 500 firms have yet to report earnings for the quarter ended in June, the index is on track to see earnings shrink by more than 7% year-over-year, according to FactSet data. Assuming this comes to pass, it would mark the third straight quarter of year-over-year declines.

If earnings growth ticks higher during the second half of the year, analysts expect 2023 will ultimately yield earnings growth of roughly 1% for the calendar year.

But in 2024, analysts are already penciling in profit expansion of more than 12%, according to FactSet.

A lot of things need to go right for companies to meet this lofty benchmark, St. Aubin said. For example, companies will need to show that they can continue to raise prices even as inflation levels off, while the U.S. economy will need to avoid the recession that many economists still expect will eventually arrive.

Even if everything goes right and U.S. companies beat Wall Street’s expectations, an analysis of historical data suggests investors buying at today’s prices could experience smaller returns over the long term.

What does history tell us?

A regression analysis performed for MarketWatch by St. Aubin using data going back to 1991 found that when stocks are valued north of 20 on a forward price-to-earnings basis, annualized returns over the following decade tend to shrink to less than 5%.

Even if lofty valuations don’t put the breaks on the market rally, their influence could be felt by investors in other ways. For example, given the dispersion between valuations for the market leaders and everybody else, value-conscious investors might start to view small-cap stocks and other underappreciated cyclical sectors as a better buy.

“As valuations reach extremes in some of the sectors, I think it’s natural for people to move away from them. If investors aren’t going to rotate their money out of the equity market, maybe they move into other areas like small-caps that look more attractive,” Young said.

That is already starting to happen, to a degree. The Russell 2000 RUT, -0.51%,

an index of small-cap stocks, has outperformed even the highflying Nasdaq Composite COMP, -0.35%

over the past month, rising 5% to the Nasdaq’s 3.6%, according to FactSet data. Although the Nasdaq is still sitting on a year-to-date gain of 36.5%, compared with the 12.7% for the Russell.

However, July was a good month for U.S. stocks, broadly speaking. Whether August portends the same is unclear. At least one prominent stock-market bull, Fundstrat’s Tom Lee, has advised clients to expect a shallow pullback in August. So far, the main U.S. equity indexes are starting the month in the red, with the S&P 500 and Nasdaq down 0.3% at 4,575 and 14,295 in recent trade.

Just a day after the Treasury Department released a $1 trillion borrowing estimate for the third quarter, questions are being raised about the extent to which foreign and domestic buyers can continue to keep up their demand for U.S. government debt.

Further details about Treasury’s financing need will be released at 8:30 a.m. on Wednesday. For now, the $1 trillion estimate, the largest ever for the July-September period, has analysts concluding that the U.S. is facing a deteriorating fiscal deficit outlook and continuing pressure to borrow.

At stake for the broader fixed-income market is whether the presence of large ongoing auctions over the coming quarter and beyond will lead to a prolonged period where demand from potential buyers might begin to dry up, Treasury yields edge higher, and the government-debt market returns to some form of illiquidity.

“You can make the argument that since 2020, with the onset of Covid, that Treasury issuances have been met with reasonably good demand,” said Thomas Simons, an economist at Jefferies JEF, -1.75%.

“But as we go forward and further away from that period of time, it’s hard to see where that same flow of dollars can come from. We may be looking at recent history and drawing too much of a conclusion that this borrowing need will be easily met.”

Simons said in a phone interview Tuesday that “the risk is that you don’t get continued demand from foreign or domestic buyers of fixed income.” The result could be “six to nine months where the market is fatigued by bigger auction sizes, Treasurys become more and more difficult to trade, there’s a grind higher in yields, and there may be issues with liquidity where markets may not be so deep.” Still, he expects such a period, if there is one, to be less acute than what was seen in the 2013 taper tantrum or last year’s volatility in the U.K. bond market.

On Monday, the Treasury revealed a $1.007 trillion third-quarter borrowing estimate that was $274 billion higher than what it had expected in May. The estimate — which Simons calls “eye-popping” — assumes an end-of-September cash balance of $650 billion, and has gone up partly because of projections for lower receipts and higher outlays, according to Treasury officials.

Monday’s estimate is the largest ever for the third quarter, though not relative to other parts of the year. In May 2020, a few months after the onset of the COVID-19 pandemic in the U.S., Treasury gave an almost $3 trillion borrowing estimate for the April-June quarter of that year.

For the upcoming fourth quarter, Treasury is now expecting to borrow $852 billion in privately-held net marketable debt, assuming an end-of-December cash balance of $750 billion. According to strategist Jay Barry and others at JPMorgan Chase & Co. JPM, -1.05%,

the third- and fourth-quarter estimates “suggest that, at face value, Treasury continues to expect a wider budget deficit” for the 2023 fiscal year.

As of Tuesday, investors appeared to be less focused on the Treasury’s borrowing needs than on signs of continued strength in the U.S. labor market, which raises the prospect of higher-for-longer interest rates. One- TMUBMUSD01Y, 5.400%

through 30-year Treasury yields TMUBMUSD30Y, 4.100%

were all higher as data showed demand for workers is still strong. Meanwhile, all three major U.S. stock indexes DJIA, +0.05%

COMP, -0.41%

were mostly lower in morning trading.

According to Simons, who the most likely buyers will be at Treasury’s upcoming auctions will depend on where the department decides to focus its issuances. If the focus is on bills, then money-market mutual funds could “move some cash over,” he said. And if it’s on long-duration coupons, it would be “real money” players such as insurers, pension funds, hedge funds and bond funds — though much will rely on inflows from clients “before demand would pick up.”

The Institute for Supply Management’s manufacturing index is due for release Tuesday, which outside of inflationary periods (i.e., now), tends to be one of the more important economic indicators for financial markets, given its record as a bellwether.

ISM manufacturing data during the current rate-hike cycle (in red) has lagged other periods.

Even compared to other rate-hike cycles, the ISM manufacturing series has been one of the worst in history, points out Jason Daw, head of North America rates strategy at RBC Dominion Securities. Daw makes the case that the U.S. economy overall is not very strong for this period of the cycle, and the manufacturing data, not just ISM but also industrial production, has been particularly feeble.

But the call of the day comes from JPMorgan’s economic team. They note that while global manufacturing stalled in the first half, the non-manufacturing components rose at a 3.2% annualized rate, allowing the global economy to grow at an above trend 2.7% rate.

The team led by Bruce Kasman say that the typical channels through which weak manufacturing would bring down the broader economy haven’t materialized. “A major channel by which weakness in goods sectors broadens out is through depressing corporate income and pricing power. While our start-of-year outlook anticipated elevated wage gains to pressure corporate profits, the surprising strength in [first-half] global GDP was accompanied by upside surprises to inflation,” they say. In turn, there have been solid gains in both labor income and profits, and while margins have come off their peaks, they are well above pre-pandemic levels.

Business hiring, they add, is the ultimate signal of confidence, and employment growth has continued even though expectations have soured.

Now, say the JPMorgan team, the stage is set for a goods sector recovery. Labor income, when adjusted for inflation, is rising, while finished goods inflation is falling sharply.

Also, business capital spending continues to expand, particularly in emerging economies outside of China. And importantly, inventories are swinging from a drag to a lift. In the first half, the step down in the pace of stock building depressed global industrial production by 3.4 percentage points.

“Even if the pace of stockbuilding was only to level off, the impulse to global industry would be material. Add to that a potential desire to align the pace to firming demand growth and the boost could generate a jump in factory output in the coming months,” they say.

Finally, they note, the tech spending decline after the 2020 to 2021 surge looks to be ending, and global motor vehicle production is picking up as supply-chain bottlenecks ease.

The markets

After an okay finish for the S&P 500 SPX, -0.29%

to a strong July, U.S. stock futures ES00, -0.36%

NQ00, -0.42%

were a bit lower as the seasonally weak month of August commenced. Gold futures GC00, -1.28%

were trading below $2,000 an ounce. The dollar DXY, +0.42%

rose.

The ISM report is due out at 10 a.m. Eastern, when the job openings and construction spending reports also come out. Monthly auto sales also will be released throughout the day.

The inflation-adjusted equity premium is looking pretty bleak. That’s calculated by taking the expected return to the S&P 500 and subtracting 10-year TIPS yields. “While admittedly this graphic is skewed by the few megacaps trading at huge multiples, it’s sobering nonetheless,” says Michael Ashton, better known as the Inflation Guy.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Listen to the Best New Ideas in Money podcast with MarketWatch financial columnist James Rogers and economist Stephanie Kelton.

Tupperware Brands Corp.’s stock skyrocketed Monday, and has more than tripled amid a four-day win streak, as the shares of the beleaguered maker of iconic food-storage containers continued their meteoric rally.

The stock soared 44.5% in midday trading, to put it on track for the highest close since Feb. 3, 2023, and has rocketed 234.6% amid a four-day win streak.

Monday’s rally adds to the stock’s 242.2% rally last week, which was the biggest one-week gain since it went public in May 1996.

So far in July, it has blasted 456.4% higher, which would also be a monthly record. The previous record was the 224.8% gain seen in July 2020.

The stock’s historic rally kicked off after closing at a record low of 62 cents on July 18. The daily gains have been highlighted by the record 75.6% jump on July 24, despite no news being reported.

Since the record low close, the stock has soared more than 7-fold (up 617.7%).

Amid its surging share price, the company’s market capitalization has reached $196.96 million. On July 7, when Tupperware said that it had entered a waiver agreement with some of its creditors, the company’s market cap hovered around $33 million.

Tupperware’s recent trading activity is reminiscent of spikes in other names also recently seen as “left for dead,” as Samantha LaDuc, founder of LaDucTrading.com, put it to MarketWatch last week.

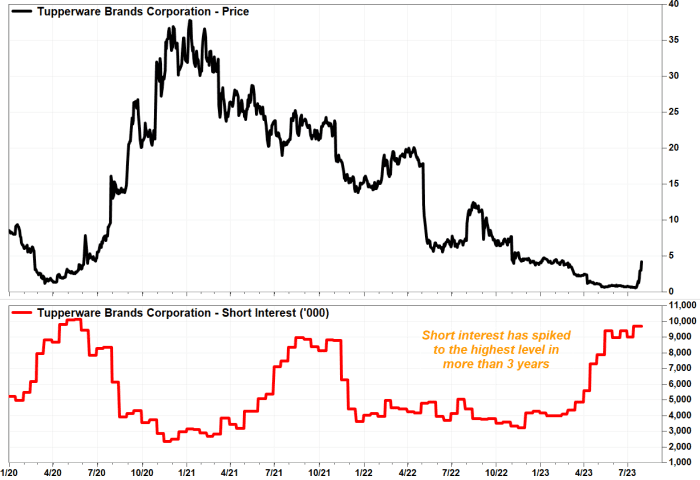

The latest exchange data showed that short interest in Tupperware’s stock, or bearish bets made, had climbed to a three-year high of 9.69 million shares, which 27% of the public float, or shares readily available for the public to trade. Read more about short selling and how it works.

In its preliminary full-year results reported in March, Tupperware sported an 18% sales decline compared with the prior year. Back then, Tupperware Chief Financial Officer Mariela Matute said in a statement that 2023 was expected to be a transition year for the company as it worked to stabilize its business and get on better financial footing.

The following month, Tupperware issued a going-concern warning, essentially cautioning that it could go bust. Tupperware also announced the hiring of financial advisers to help it navigate its near-term challenges.

The company is projected to release its next quarterly report later this week, according to FactSet.

Emily Bary, Claudia Assis and Tomi Kilgore contributed.

The bond market is expressing confidence in company cash flows, flashing a sign of support for the stock market’s rally, according to DataTrek Research.

“U.S. corporate bond spreads continue to tighten and are now essentially the same as 2017–2019,” said Nicholas Colas, co-founder of DataTrek Research, in a note emailed Monday. “That is a green light for further stock market gains.”

Declining corporate bond spreads over comparable Treaurys signal rising confidence in future cash flows and earnings, said Colas. Both investment-grade and high-yield bonds have broadly seen their spreads tighten over the past few weeks to average levels seen in 2017–2019, when conditions in the economy were generally good, his note shows.

Investment-grade spreads averaged 1.19 percentage points over Treasurys over that stretch, while junk bonds averaged 3.82 percentage points, according to Colas’s research.

“This was a period of generally good economic conditions and just one hiccup in capital markets, namely when the Fed briefly overreached on rate policy in late 2018,” he said.

This year, investment-grade bond spreads have recently declined to around 1.22 percentage points and those for high-yield debt have narrowed to 3.78%, the DataTrek note said.

“Corporate bond markets continue to mirror equity market confidence” in stable and strengthening company cash flows, Colas said. “This is not only supporting the ongoing rally in large caps, but also helping small caps outperform in July.”

The Russell 2000 index RUT, +1.09%,

which tracks small-cap stocks in the U.S., has climbed 4.9% so far this month, exceeding the S&P 500’s 3% gains over the same period, according to FactSet data. The Russell 2000 has been trailing the S&P 500 in 2023, though, with 12.5% gains so far this year.

Earlier this month, Bespoke Investment Group also pointed to high-yield bonds as the latest indicator confirming the equity market’s rally. The S&P 500, a gauge of U.S. large-cap stocks, has jumped 19.3% this year through Friday.

Citigroup analysts said in a research note on Friday that they raised their 2023 target for the S&P 500 by 600 points to 4,600, while revising up their mid-2024 target to 5,000, from 4,400.

The popular stock-market index SPX, +0.15%

closed Friday at 4,582.23.

A wider swath of stocks have joined the S&P 500 SPX, +0.15%’s

upswing after the so-called Magnificent Seven — Apple AAPL, +0.32%,

Amazon AMZN, +1.11%,

Alphabet GOOG, +0.08%,

Microsoft MSFT, -0.72%,

Meta META, -2.11%,

Nvidia NVDA, -0.04%

and Tesla TSLA, +0.37%

— single-handedly propelled the large-cap index into a bull market in early June, with the gauge now up more than 28% from its low notched last October and rising to new highs since April 2022, according to Dow Jones Market Data.

Hopes that the U.S. economy could pull off a soft landing and avoid a recession despite the Federal Reserve’s aggressive interest-rate hikes, as well as receding inflation pressures and expectations for the end of the Fed’s monetary tightening campaign, have underpinned a notable expansion in market breadth over the past two months, according Adam Turnquist, chief technical strategist at LPL Financial.

The S&P 500 Equal Weighted Index SP500EW, +0.27%,

which lagged behind the market-cap-weighted S&P 500 index for most of the year, has now kicked back into gear and staged an impressive comeback in July. The equal-weighted index and the S&P 500 each advanced 3.1% this month, according to FactSet data.

The equal weighting eliminates the distortion of the megacap components and significantly changes several sector weightings in the S&P 500, including technology, which drops from around 29% on the SPX to only 13% on the equal-weighted index, said Turnquist in a Friday note. Meanwhile, the industrials sector has the biggest increase in weight, jumping from 9% on the SPX to 16% on the equal-weighted index.

Another way to quantify and compare market breadth is to look at the percentage of stocks on an index trading above their longer-term 200-day moving average (dma), Turnquist said. In general, if a stock is trading above its 200 dma, it is considered to be in an uptrend, and if the price is below the 200 dma, it is considered in a downtrend. Furthermore, a higher percentage of stocks above their 200 dma implies buying pressure is more widespread — suggesting the market’s advance is likely sustainable.

The chart below shows that 73% of stocks within the S&P 500 are trading above their 200 dma as of July 27, which compares to only 48% at the end of 2022. Moreover, the composition of breadth leadership has turned increasingly bullish. The highest sector readings include technology, industrials, energy, and consumer discretionary.

“So not only is breadth on the index robust, but cyclical stocks are also leading,” said Turnquist.

SOURCE: LPL RESEARCH, BLOOMBERG

Wall Street often views broadening participation in the stock-market rally as a measure of health and a constructive sign of the sustainability of the bull market.

Jimmy Lee, founder and chief executive officer of The Wealth Consulting Group said he is seeing “a lot of money” flowing into areas that are not the Magnificent Seven such as stocks in the industrials, financials, materials, energy and even real-estate sectors.

The S&P 500’s industrials sector SP500.20, +0.23%

climbed 2.9% in July, while the financials sector SP500.40, +0.44%

advanced over 4.7% this month. The S&P 500’s energy sector SP500.10, +2.00%,

which had been the biggest laggard when the rest of the markets exited the bear market in June, jumped 7.3% month to date after the U.S. oil benchmark CL.1, -0.20%

Meanwhile, the tech-heavy S&P 500’s communication-services sector SP500.50, -0.03%

rose 6.7% in July, while the consumer-discretionary sector SP500.25, +0.56%

gained 2.4% and the information-technology sector SP500.45, +0.13%

was up 2.6%, according to FactSet data.

Stephen Hoedt, managing director of equity and fixed income research at Key Private Bank, told MarketWatch in an interview that he doesn’t see “any reason to get bearish here with the fundamentals that are underlying,” which gives investors reason to rotate toward the more cyclical areas such as energy, financials and industrials, while broadening the market away from just being concentrated in the megacap technology names.

“The growth has been a surprise this year for everyone, so that’s what the market got wrong coming into this year. When I look at growth, nominal GDP growth translates directly into earnings and we’ve seen earnings continue to surprise on the upside,” Hoedt said.

Hoedt pointed to the direction of the 12-month forward earnings estimate for the S&P 500 as an important indicator. “As long as the direction of the 12-month forward earnings number for the S&P 500 is going up, it’s really, really difficult to be bearish on the stock market,” he said. “It seems to me that we may start to see another inflection higher in forward earnings revisions that take into account this stronger growth environment that we’re in.”

However, the broadening of the stock-market rally and the bullish sentiment were also driving some on Wall Street to believe stocks are overbought and due for a correction.

Lee said there’s still too much pessimism out there and too much concern that some investors haven’t chased the market yet. “In the second half of this year, when the Fed does stop raising rates and if the economy stays out of recession, you can see major money — trillions of dollars moving from the money market into equities and other risk assets,” he told MarketWatch in a phone interview on Friday.

“When that happens, it’s probably going to push valuations even further. So I would imagine when that happens is when you can expect more of a correction to occur, but I think that we still have more room to go before that happens.”

U.S. stocks ended higher on Monday, finishing up July on a positive note. Three major stock indexes rallied this month, with the S&P 500 up 3.1% and booking its fifth monthly gain. The tech-heavy Nasdaq Composite COMP, +0.21%

gained 4.1% month to date, while the Dow Jones Industrial Average DJIA, +0.28%

advanced 3.4%, according to Dow Jones Market Data.

The S&P 500 index is on the verge of a fifth straight monthly gain in July. It’s a reality that few on Wall Street expected just eight months ago.

As a result, it seems that one by one, equity analysts at the big banks are issuing mea culpas or tweaking their S&P 500 targets.

With so many reconsidering their assumptions about markets and the economy, one analyst who has been bullish for months sees an opportunity to reflect on what Wall Street got wrong in 2023 — and by doing so, pinpoint potential existential threats to the rally that may lie ahead.

Jawad Mian, a longtime financial markets professional and the founder of Stray Reflections, said professional investors and economists generally underestimated just how resilient U.S. corporations, and U.S. consumers, and the broader U.S. economy would be to higher interest rates. At the same time, they failed to fully appreciate inflation’s ability to boost corporate profits over the long term.

So far, stocks have proved resilient to higher bond yields in 2023, but that doesn’t mean they always will be. Mian believes that rising real yields could eventually push past a “tipping point” that would send U.S. equity valuations sharply lower.

“I think what’s happening is we are collectively discovering how high interest rates can go before the economy breaks,” he said.

“I think the 10-year yield is heading toward 5%. But the nuanced take here is the path higher is not troublesome…however, at some point, we’ll reach a level that’s too much,” Mian added during a phone interview with MarketWatch.

The yield on the 10-year Treasury note TMUBMUSD10Y, 3.962%

stood at 3.955% on Friday.

Past the point of no return

The Federal Reserve pushed its policy interest-rate to its highest level in 22 years earlier this week, and further hikes certainly could push long-dated bond yields higher, Mian said. But the blow that drives markets over the cliff could easily come from somewhere else as well.

For example: Foreign investors, particularly those in Japan, could choose to dump U.S. Treasurys now that they’re being enticed by more attractive yields back home.

Investors received a small taste of what this might look like on Thursday afternoon when a headline about the Bank of Japan’s plans to loosen its grip on its government bond market sent the yield on the 30-year Treasury bond TMUBMUSD30Y, 4.021%

north of 4%, sparking a selloff in stocks that led to the Dow Jones Industrial Average snapping a 13-day winning streak.

Yields on the 10-year Japanese government bond hit their highest levels since 2014 on Friday after the BOJ confirmed those reports during its July policy meeting.

While it’s important for investors to monitor bond-market threats like this, yields don’t exist in a vacuum. Corporate earnings are another important piece of the puzzle.

Higher yields make bonds more attractive to investors, helping to dim the appeal of stocks, but they also increase borrowing costs for corporations, potentially cutting into profits and pushing companies to lay off employees or enact other belt-tightening measures.

The more pressure companies face from rising borrowing costs, they more likely they’ll need to take more cost-cutting measures like laying off employees.

“Generally speaking, if yields move higher that should put downward pressure on multiples. That’s a risk to the stock market for sure,” said James St. Aubin, chief investment officer for Sierra Investment Management, during a phone interview with MarketWatch.

For now at least, it looks like stocks could continue to ride this wave of momentum higher, even if valuations are looking somewhat stretched relative to recent history already, St. Aubin said. For this to continue though, corporate earnings will need to keep pace with increasingly optimistic expectations.

Already, stock valuations are looking lofty based on the price-to-earnings ratio, one of Wall Street’s favorite metrics for determining how expensive or cheap the market looks.

The forward 12-month price-to-earnings ratio for the S&P 500 index currently stands at 19.4. That’s already higher than the five-year average of 18.6, and the 10-year average of 17.4, according to FactSet data.

Right now, investors are willing to tolerate this because they expect corporate profits to grow substantially in the years ahead, even though profits are expected to contract by 7% in the quarter ended in June, bringing the stretch of negative earnings growth to a third straight quarter.

But in 2024, year-over-year earnings growth is expected to swell to 12.6%. If companies meet, or surpass, these expectations, stocks will likely hold on to their gains, if not continue to climb, St. Aubin said.

However, should earnings growth disappoint, a painful market reckoning might follow.

Since the start of 2023, U.S. stocks have nearly erased all of their losses from 2022, which was the worst year for stock-market performance since 2008, while bonds saw their biggest declines in decades as yields soared driven by inflation and the Federal Reserve’s aggressive interest-rate hikes. Since Jan. 1, the S&P 500 SPX, +0.99%

has risen 19.3% to 4,582.23, according to FactSet.

The Nasdaq Composite COMP, +1.90%

has risen 36.8% to 14,316, while the Dow Jones Industrial Average DJIA, +0.50%

is up 7%.