[ad_1]

It’s that time again: monthly stock-market options for August are set to expire on Friday, potentially spurring more volatility in stocks after a bruising three-week run.

U.S. stock option contracts with a notional value of $2.2 trillion are set to expire, according to Rocky Fishman, founder of newly formed strategy firm Asym 500 and a former head of index derivatives strategy at Goldman Sachs Group. Notional value measures the market value of the stocks, indexes and exchange-traded funds controlled by the options, although the premiums paid by holders of the options are worth much less.

ASYM 500

Fishman noted that the size of option-market open interest expiring on Friday is about average for an off-month expiration.

Monthly options expire every month, but once a quarter — in March, June, September and December — an event known as “Triple Witching” takes place, causing notional value of expiring options to swell as quarterly and sometimes calendar-year options expire along with monthlies and weeklies.

Sessions where monthly options expire often see higher-than-normal volatility, and options-market analysts warned that the same could happen on Friday.

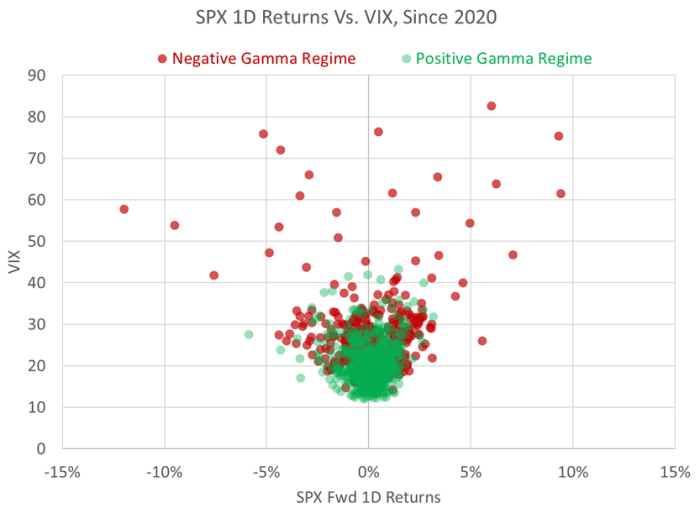

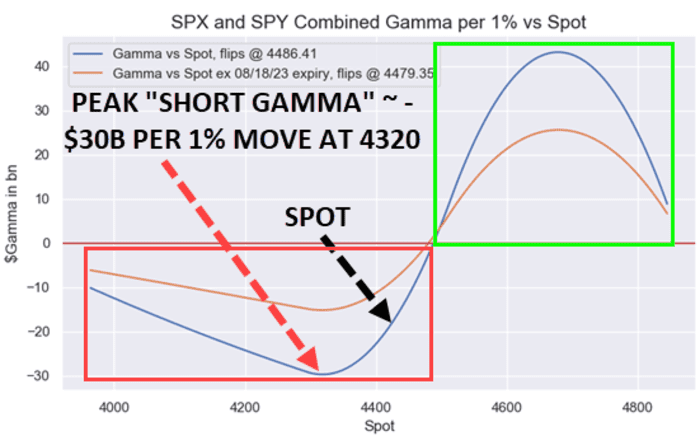

Charlie McElligott, a longtime derivatives strategist who publishes research on Nomura’s trading desk, warned clients that option dealers are “short gamma” heading into Friday’s expiration, increasing the potential for option dealers to exacerbate market volatility. McElligott illustrated this tendency in the chart below.

NOMURA

Why are dealers short gamma, and what does this mean? As stocks have stumbled, option traders have been buying put options and selling call options. As a result, dealers could be forced to hedge their positions by buying futures if stocks rise and their customers close out their short-call positions, or selling futures to hedge the risk of puts moving into the money.

This would serve to exaggerate the market’s move in either direction, driving a rising market higher and a falling market lower, McElligott said.

Dealers could hit “peak short gamma” if the S&P 500 falls to 4,320, sending a wave of puts into the money. If that happens, it’s possible dealers could slam stocks lower as they rush to avoid being on the hook for puts sold to customers. The S&P 500

SPX

finished Thursday at 4,370.36.

NOMURA

Gamma is used by options analysts to describe how quickly an option’s delta changes. Delta represents how sensitive the price of an option is to moves in the underlying asset. When options are about to expire, delta typically increases dramatically, since small moves that put it closer to being in or out of the money can have a dramatic impact on the option’s price.

Brent Kochuba, founder of SpotGamma, also cited risks tied to dealers’ short-gamma position in research shared with clients. SpotGamma shares data and analytics about the option market.

“We have been watching market gamma fall into negative gamma territory all month. Once it entered that range, price action became visibly choppier, as expected during these conditions,” he said in written commentary shared with MarketWatch and SpotGamma clients.

Option contracts give traders the right, but not the obligation, to buy or sell the underlying asset or currency. Often, options tied to stock-market indexes like the S&P 500 are settled in futures or cash. Options tied to exchange-traded funds like the SPDR S&P 500 ETF Trust

SPY,

which tracks the S&P 500 index, are settled in shares of the ETF.

A put option allows the buyer the right, but not the obligation, to sell shares at an agreed-upon price known as the “strike price.” A call option, conversely, gives the holder the right to buy shares. Put options tend to appreciate when the underlying stock or index falls, while the opposite is true for calls.

U.S. stocks finished lower on Thursday, with the S&P 500 and Nasdaq Composite poised to record a third straight weekly decline, what would be the longest such streak for the S&P 500 since February.

The S&P 500 was off by 0.8% on Thursday, while the Nasdaq Composite

COMP

fell by 1.2% to 13,316.93. The Dow Jones Industrial Average

DJIA

shed 290.91 points, or 0.8%, to 34,474.83.

In addition to monthly options expiring Friday, weekly options known as “zero days until expiration” or “0DTE” options could further complicate the market’s reaction. A veteran Goldman Sachs Group strategist warned earlier this week that 0DTE traders have been limiting upswings in stocks while piling on the pressure when markets sink.

[ad_2]