Enjoy complimentary access to top ideas and insights — selected by our editors.

Bank of America said Monday that it will need to “de-designate” interest-rate swaps and reclassify how it accounts for them. Though the bank will take a noncash, pretax charge of $1.6 billion in the fourth quarter, it expects to regain that money as interest income over time.

Christopher Goodney/Bloomberg

Bank of America’s support for a short-lived interest rate index from Bloomberg L.P. will lead the bank to take a $1.6 billion hit in its earnings report on Friday, though it will earn that money back over time.

BofA was perhaps the leading backer of Bloomberg’s Short Term Bank Yield Index, or BSBY, rate, which was designed to play a major role in replacing the once-ubiquitous London Interbank Offered Rate. Libor was used in loans across the world before a rate-rigging scandal caused its demise. Bloomberg had foreseen a window in which it could come up with its own benchmark for banks to use in loans.

But regulators were either skeptical of BSBY or openly combative about its adoption. After the rate failed to gain much traction in the banking industry, Bloomberg said in November that it would permanently discontinue BSBY this year.

The rate’s demise is triggering an accounting shift at Charlotte, North Carolina-based BofA, since derivatives transactions the bank entered to hedge its exposure to BSBY no longer qualify for special treatment under accounting rules.

In a securities filing Monday, the $3.15 trillion-asset bank said it will need to “de-designate” those interest-rate swaps and reclassify how it accounts for them. BofA is taking a noncash, pretax charge of $1.6 billion in the fourth quarter due to that change. But the bank also said it expects to regain that $1.6 billion as interest income over time, with much of that occurring by the end of 2026.

The one-time charge will also cause a decline of eight basis points in the company’s common equity tier 1 ratio, Bank of America said.

Analysts described the change as a nonissue, even if it makes the bank’s quarterly earnings somewhat noisier than BofA might like. The bank reported $7.8 billion in earnings during the third quarter, so a $1.6 billion hit in the fourth quarter is not insignificant.

Jason Goldberg, a bank analyst at Barclays, said in an email that the change is “much more of an accounting nuisance” than anything. He noted that BofA will earn $1.6 billion over the next few years as it makes up the one-time charge.

Piper Sandler analyst Scott Siefers wrote in a note to clients that the “one-time accounting change” will “introduce some noise” into Bank of America’s quarterly earnings but will not have much impact beyond that.

Other banks that used BSBY in loans may also have to make moves to clean up from the index’s discontinuation. But few, if any, banks likely used BSBY as much as Bank of America, which made loans to several publicly traded companies that referred to the benchmark, according to securities filings that provide details of those loans.

The key feature that made BSBY attractive was that it was credit-sensitive. Like Libor, it moved up when financing conditions were tighter, which meant the interest payments banks received from borrowers reflected any stresses in real time.

By contrast, the Secured Overnight Financing Rate, which has replaced Libor in the United States, is seen as “risk-free” since it’s based on some of the safest transactions in the world. SOFR moves very little in times of financial stress, which bankers say does not reflect the fact that it’s more expensive for them to fund their operations when markets are tighter.

Bank of America, along with several regional banks, had participated in a series of virtual workshops in 2020 and 2021 that regulators set up to discuss the role of credit-sensitive rate options.

After those meetings, banking regulators said they were open to banks using non-SOFR rates as long as they understood and planned for any risks. But Securities and Exchange Commission Chairman Gary Gensler was openly critical of BSBY, which observers say contributed to its demise.

The developers of Ameribor, another credit-sensitive rate that some community banks have favored, said after Bloomberg decided to shut BSBY that their plans haven’t changed.

North Carolina banker Ed Crutchfield pioneered interstate banking as the head of First Union Corp., leading the Charlotte-based bank through more than 80 acquisitions to become a $253 billion-asset company. He retired in 2000, shortly before the banking heavyweight merged with Wachovia.

Ed Crutchfield, a deal-hungry banker who catapulted his relatively small North Carolina bank into a regional powerhouse during the 1980s and 1990s, died Tuesday at 82.

Crutchfield struck more than 80 deals as CEO of Charlotte-based First Union Bank, buying banks up and down the East Coast at a time when loosened interstate banking laws fueled a major wave of consolidation. First Union, which later became part of Wells Fargo, swelled from just $7 billion of assets when Crutchfield took over in 1984 to $253 billion when he retired in 2000. It had become the sixth biggest bank in the country.

Much like today, the vision driving the deals was get-big-or-get-bought. But First Union, along with cross-town rival NationsBank (now Bank of America), also sought to become a diversified bank that could help middle-market businesses in the South get the types of services typically offered only by big New York firms.

In the process, Crutchfield and his chief business rival, former BofA CEO Hugh McColl, turned Charlotte into the banking hub it is today.

“They viewed that they could have Wall Street in the South, and to a certain extent, that was created,” said Christopher Marinac, an analyst at Janney Montgomery Scott, who recalled Crutchfield laying out his vision at analyst meetings while chain-smoking. “I think they were largely successful.”

Crutchfield grew up in Albemarle, near Charlotte, and started working as a bond analyst at the bank in 1965. He’d become First Union’s president some eight years later and its CEO in 1984.

At the time, states were starting to ease restrictions on interstate branch footprints. A wave of financial industry deregulation under President Ronald Reagan continued under George H.W. Bush and then Bill Clinton, and the number of banks in the country would shrink from 14,000 in the early 1980s to 8,000 in 2000.

First Union was small at the time, making it a seeming candidate to be snapped up by a larger competitor. But Crutchfield was a buyer, not a seller, earning the nickname “Fast Eddie” as he scooped up lenders along the Eastern seaboard.

“He had a terrific way about him when he sat down with other CEOs,” said Rodgin Cohen, one of the country’s top banking lawyers and senior chair at the law firm Sullivan & Cromwell.

Cohen, who worked with Crutchfield on several deals, said he “disarmed people” with his down-to-earth-nature and humor.

“He could be convincing. He was seen as the type of person that you were glad to sell your bank to,” Cohen said.

Elliott Crutchfield, Ed’s son, said his father was a “builder” who took the lowest-paying job from his post-business school job offers because “he saw the most opportunity” to become a leader at First Union.

“He got a lot more satisfaction of catching Citigroup from nowhere than he would have working his way up through Citigroup,” his son said.

The First Union brand went away soon after Crutchfield left the bank. His successor as CEO, G. Kennedy Thompson, announced a merger with rival Wachovia in 2001, and First Union took on Wachovia’s brand. Wachovia, too, went away in 2008, two years after buying a mortgage lender that ran into trouble in the housing bust. Wells Fargo absorbed Wachovia at the height of the financial crisis.

The deals Crutchfield struck were not always pretty. Bringing together two regional banks’ systems and staffers is no easy task. Even today, Charlotte-based Truist Financial faces customer backlash following the merger that created it.

After First Union’s 1998 purchase of CoreStates Financial Corp. of Philadelphia, the integration went so poorly that the bank lost 19% of CoreStates’ customers.

Bankers have “learned a lot about how to do these integrations by virtue of some of the mistakes that occurred” in the 1990s consolidation wave, Marinac said. Analysts “cut less slack today” when messy integrations happen “because we know better,” he added.

“That’s not to knock it at all,” Marinac said, explaining that the banking industry learned lessons about the importance of back-end work after the “big and bold” deals of the 1990s.

Purchase prices were another source of controversy for Crutchfield. He faced skepticism from investors who thought First Union overpaid in certain deals, with some analysts arguing that the money the bank spent on M&A could have been used more productively elsewhere.

Crutchfield was a staunch defender of his bank’s strategy. At an American Banker conference in 1995, he said that “you need the scope and size” to compete with nonbank financial institutions, such as the mutual funds that were proliferating at the time.

“I don’t apologize for our acquisitions,” Crutchfield said. “It is a poor strategy to do no acquisitions and say, ‘We’ll just sit around for four or five years and wait for someone to buy us.’”

Crutchfield’s biggest critic was banking analyst Thomas Brown, who’s now CEO of the investment firm Second Curve Capital. Crutchfield once called Brown a “little red-haired boy” and banned him from coming into First Union’s main office, according to The Wall Street Journal.

In an email on Friday, Brown called Crutchfield “a good man with a down home spirit and honesty” who believed both in “making First Union a survivor in a consolidating industry” and in making Charlotte a thriving city.

“We strongly disagreed but there aren’t many bank CEOs that I enjoyed a drink with more than Ed Crutchfield,” Brown wrote.

Crutchfield retired as First Union’s CEO in 2000 after getting lymphoma, though he subsequently remained active in civic and business circles. Years later, he’d fight back a more severe bout of cancer.

Stock futures traded flat Tuesday, a day after the S&P 500 finished up 0.5% and moved closer to its all-time. The broad market index stands just 1.2% below its record of 4,796.56 reached in early January 2022.

Continue reading this article with a Barron’s subscription.

The U.S. economy continues to grow despite the 5.5% benchmark federal funds interest rate set by the Federal Reserve in 2023.

The Fed’s leaders expect their interest rate decisions to eventually slow that growth.

The increase in borrowing costs that stems from Fed decisions does not affect all consumers immediately. It typically affects people who need to take new loans — first-time homebuyers, for example. Other dynamics, such as the use of contracts in business, can slow the ripple of Fed decisions through an economy.

“It might not all hit at once, but the longer rates stay elevated, the more you’re going to feel those effects,” said Sarah House, managing director and senior economist at Wells Fargo.

“Consumers did have additional savings that we wouldn’t have expected if they had continued to save at the same pre-Covid rate. And so that’s giving some more insulation in terms of their need to borrow,” said House. “That’s an example of why this cycle might be different in terms of when those lags hit, versus compared to prior cycles.”

A 1% interest rate increase can reduce gross domestic product by 5% for 12 years after an unexpected hike, according to a research paper from the Federal Reserve Bank of San Francisco.

“It’s bad in the short term because we worry about unemployment, we worry about recessions,” said Douglas Holtz-Eakin, president of the American Action Forum, referring to the paper’s implications for central bank policymakers. “It’s bad in the long term because that’s where increases in your wages come from; we want to be more productive.”

Some economists say that financial markets may be responding to Federal Reserve policy more quickly, if not instantaneously. “Policy tightening occurs with the announcement of policy tightening, not when the rate change actually happens,” said Federal Reserve Governor Christopher Waller in remarks July 13 at an event in New York.

“We’ve seen this cycle where the stock market moved more quickly in some cases, more slowly in other cases,” said Roger Ferguson, former vice chair of the Federal Reserve. “So, you know, this question of variability comes into play, as in how long it’s going to take. We think it’s a long time, but sometimes it can be faster.”

Watch the video above to see why the Fed’s interest rate hikes take time to affect the economy.

Metallurgical coal is dumped onto a pile in Ceredo, West Virginia, in 2017. Climate groups are pressuring banks to stop financing the energy source, which is used to heat blast furnaces in the steelmaking process.

Luke Sharrett/Bloomberg

Sustainable finance advocates are pressuring five of the six largest U.S. banks to stop financing metallurgical coal, an emissions-heavy energy source used to heat blast furnaces in the steelmaking process.

In a letter to the banks on Thursday, climate groups called for commitments to “end all dedicated financial services” for the development and expansion of metallurgical coal projects and related infrastructure.

Metallurgical coal contains a higher amount of carbon, as well as ash and moisture, than thermal coal, which is more commonly used to generate power.

The climate groups argue that banks should include metallurgical coal in their phase-out plans and increase lending to “key enabling sectors” for the steel industry’s “transition.”

“It is essential that other energy sources are identified for both steelmaking and power generation, and that all coal remains in the ground,” the letter states.

The letter was signed by 67 climate organizations globally, including BankTrack, the Rainforest Action Network and the Sierra Club, and sent to 50 large financial institutions around the world.

The U.S.-based recipients were Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase and Morgan Stanley. Those five banks provided a combined $29.6 billion to finance metallurgical coal projects since 2016, according to the letters.

BofA, Citigroup and Morgan Stanley declined to comment. Goldman Sachs and JPMorgan did not respond to requests for comment.

In a March report, Citi committed to reducing the carbon exposure of its loan portfolio by 2030 in four sectors: steel, auto manufacturing, commercial real estate and thermal coal mining.

For the steel industry, Citi committed to reaching a score of zero, which is the best possible score under the Sustainable STEEL Principles, a reporting framework developed by the Rocky Mountain Institute, a nonprofit organization focused on decarbonization efforts.

Citi had previously committed to reducing 90% of emissions from thermal coal mining by 2030, based on a 2021 baseline.

JPMorgan Chase has set a 2030 target to reduce 30% of its emissions tied to the steel industry based on a 2019 baseline. BofA, Goldman Sachs and Morgan Stanley did not set 2030 targets to reduce their portfolio emissions from the steel industry.

Ariana Criste, who leads the steel campaign at Industrious Labs, one of the sustainable finance groups that signed the letter, said that metallurgical coal continues to be a “blind spot” for the financial industry.

“If the U.S. banking industry and the global banking industry continue to underwrite and enable the steel industry to rely on this outdated fossil fuel,” Criste said in an interview, “the green steel future is going to continue to remain out of reach.”

The activists are targeting not only banks, but also the steel industry, saying that steel production should be decarbonized or phased out to help meet commitments to prevent the worst effects of climate change.

Over the last decade, climate activists have pressured banks and other companies to stop funding greenhouse gas-emitting industries, and also to provide more transparency about their carbon footprints.

JPMorgan Chase has been searching for third-party capital to supplement the more than $10 billion of balance sheet cash that it has already set aside for its private credit strategy.

Michael Nagle/Bloomberg

JPMorgan Chase is running into some pushback over fees and control as it aims to pull together a group of lenders to help fund private credit deals it originates, an effort that has the potential to reshape the burgeoning market.

The biggest U.S. bank has held talks with several private credit firms about creating what would amount to a syndication group where members would take a slice of each loan, according to people with direct knowledge of the discussions. JPMorgan would select the loans, and others in the syndicate would have no or limited ability to veto deals they don’t want to fund, the people said.

Banks have been searching for the best way to carve out their own piece of the $1.6 trillion private credit market as higher rates spark a flood of investor interest and increasingly stringent capital rules make them more wary of keeping loans on their balance sheet. Private credit has already been eating into Wall Street banks’ share of the leveraged loan and high-yield bond markets, a key fee generator. Several lenders have announced private credit partnerships, and others are looking at options.

JPMorgan is in ongoing discussions with potential partners, and in some meetings has floated charging fees that amount to about 2.5%, said some of the people, who asked not to be identified describing private talks. The fees and lack of veto power pitched in some of the conversations have made some firms reluctant to join the effort, they said.

A spokeswoman for JPMorgan declined to comment.

JPMorgan has been searching for third-party capital to supplement the more than $10 billion of balance sheet cash that it has already set aside for its private credit strategy, which it began rolling out in the last year, Bloomberg reported last month. In addition to alternative asset managers, it’s also pursuing discussions with sovereign wealth funds, pension funds and endowments.

The firm is one of the largest underwriters of leveraged loans and high yield bonds, and the private credit effort may help it protect a crucial business. The structure it’s pitching would allow it to maintain control of client relationships and provide a level of certainty to borrowers that agreed loans would be funded, some of the people said.

Private credit specialists have gathered more money to deploy based on the pitch of higher returns and lower volatility than the public loan market. But now they face questions over how they’ll accomplish the unglamorous tasks of finding, underwriting and servicing a broader swath of loans.

While the largest credit firms and alternative asset managers have spent years building out origination platforms, many smaller or midsize rivals may struggle to replicate that in short order. Some traditional banks see that as their opening to get a steady stream of fees by leaning on their underwriting and servicing experience and existing relationships.

Huntington Bancshares’ entry into Native American financial services is an outgrowth of its 2021 acquisition of TCF Financial, which expanded the bank’s footprint into Minnesota and Colorado.

Emily Elconin/Bloomberg

Huntington Bancshares isn’t about to let a potential economic slowdown go to waste.

Huntington plans to expand commercial banking into North Carolina and South Carolina, and to create a unit that specializes in medical asset-based lending. The company also said it recently added a Native American financial services group.

“The ability at this stage — when other banks may be doing cost programs or reductions, or have a limited appetite for risk-weighted asset growth for capital or other reasons — this is a window,” said Huntington Chairman, President and CEO Steve Steinour. “We’ve been gearing the company for outperformance during a recession … and we’re going to deliver that.”

“It’s a bit of a contrarian play,” added Steinour, who was speaking at the Goldman Sachs U.S. Financial Services Conference in New York City. “With strong capital, excellent liquidity, the capabilities of the team, the credit performance, this is our time to move. We intend to do it throughout 2024, as well.”

In October, on a conference call to discuss third-quarter earnings, Steinour said that Huntington’s noninterest expenses, which totaled $1.1 billion for the three months ending Sept. 30, would increase by 4%-5% in the fourth quarter. He also said that the spending growth would carry over into 2024.

Huntington’s Carolinas expansion will be led by commercial banking, according to Steinour. The Columbus, Ohio-based bank plans to offer middle-market corporate specialty banking capabilities, along with treasury management and capital markets services, he said.

Banking teams in the Carolinas will be located in five regions: Charlotte; Raleigh-Durham; the Triad region of Greensboro, Winston-Salem and High Point; Upstate South Carolina; and Coastal South Carolina.

Huntington has already hired many of the bankers it needs to staff its teams, Steinour said, though he stopped short of disclosing precisely how many individuals it has recruited.

“We were able to be opportunistic in identifying teams of experienced bankers who know these markets well,” Steinour said. “I’m very enthusiastic about the teams who have recently joined the bank.”

While several Huntington specialty lending units, including Small Business Administration lending, have pursued nationwide expansions, commercial banking has heretofore been restricted largely to the company’s 10-state footprint in the Midwest and the West.

Huntington’s plans for a medical asset-based lending unit should dovetail with an existing health care specialty banking group, Steinour said. The new effort offers the opportunity to “extend the menu” with existing relationships and bring new ones into the company, he said: “It’s a natural fit, hand in glove.”

The entry into Native American financial services is an outgrowth of Huntington’s June 2021 acquisition of TCF Financial, which expanded the bank’s footprint into Minnesota and Colorado, according to Steinour.

“We’ve got a half dozen very experienced bankers [with] great reputations, and we’re prepared to invest,” he said.

Huntington joins a small group of companies, including Wells Fargo and the neobank Totem, that are seeking to expand the financial services options available to Native Americans. The move could have a positive impact on deposits, since loans to Native Americans are often part of relationships that feature high deposit-to-loan ratios, in many cases 100%, Steinour said.

“Done well, it’s a really good business, and it serves an underserved community. It’s in line with our purpose,” Steinour said.

Though he provided no details, Chief Financial Officer Zach Wasserman said the moves announced Wednesday will begin to have a positive impact on Huntington’s results in the second half of 2024 and into 2025.

“These are really exciting,” Wasserman said. “Each in and of themselves is additive and helpful. Cumulatively, they’ll be powerful. … We’re seeing the highest-caliber talent come to us. That’s what enables the fast payback.”

Big bank CEOs will likely convey deposits and earnings are stable to lawmakers on Wednesday, according to a major financial services executive. Thomas Michaud, CEO of Stifel company Keefe, Bruyette & Woods, thinks the hearing before the Senate Banking Committee will successfully provide assurance to Washington and Wall Street. Banking chiefs slated to speak at the “Annual Oversight of Wall Street Firms” hearing include JPMorgan CEO Jamie Dimon and Goldman Sachs CEO David Solomon. “The crisis of the spring where we had three of the four largest failures in history is behind us,” Michaud said on CNBC’s ” Fast Money ” on Tuesday. He’s referring to Silicon Valley Bank , Signature Bank and First Republic — the latter of which was the nation’s biggest bank failure since the 2008 financial crisis. Michaud, who testified before Congress in May on the bank failures, hopes Wednesday’s hearing re-addresses the call for changes to prevent bank runs from pushing other financial institutions over the edge. “One way to fix it is deposit insurance reform,” he said. “The targeted approach to change deposit insurance to reduce the ‘too big to fail’ thinking, so depositors don’t run like that. That is what we need, and that effort has stalled in Congress.” He thinks action is needed to keep mid-sized banks competitive with the big banks — starting with lifting Federal Deposit Insurance Corp coverage limits for small businesses. Currently, the FDIC covers $250,000 per depositor, per insured bank, per ownership category — an amount that is likely inadequate for small businesses . “If deposit insurance reform in my opinion doesn’t happen, there’s going to be tremendous pressure on those [mid-size] banks to consolidate,” Michaud said. Disclaimer

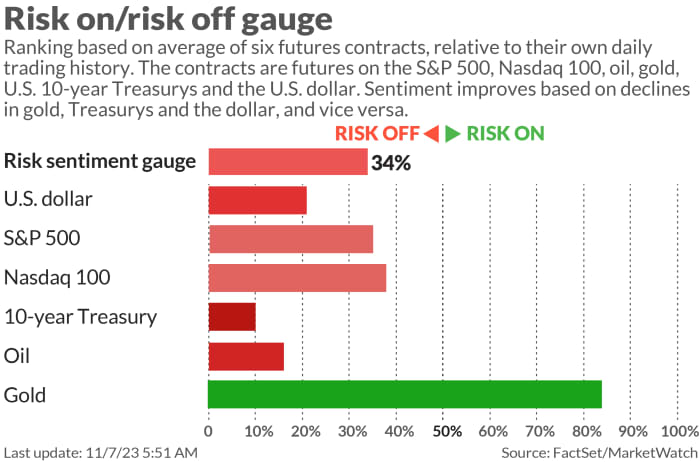

A rally in the U.S. stock and bond markets in the past week defied the bears and fueled hopes for more gains to come by year-end and in 2024 as Wall Street bought into the idea that the economy will pull off a “soft landing” after a run of interest-rate hikes by the Federal Reserve.

But market skeptics are putting investors on alert that the “soft-landing” scenario is still at risk with consumer spending and job growth slowing, along with corporate earnings.

“The equity market is misguided,” said Josh Schachter, senior portfolio manager at Easterly Investment Partners, in a phone interview with MarketWatch. “The markets are behaving in almost a bipolar fashion — some asset classes such as bonds BX:TMUBMUSD10Y,

oil BRN00, -0.29%,

and dollar DXY,

are being priced for a recession, while other assets such as equities and bitcoin BTCUSD, +2.16%,

are priced risk-on.”

U.S. stocks built on their November gains in the past week, with the S&P 500 index SPX

ending at new 2023 high on Friday and the Dow Jones Industrial Average DJIA

logging its fifth week in the green. The rebound in stocks was due in part to bond investors starting to believe the Fed is done raising interest rates and is likely to begin cutting them by the first quarter of 2024.

Meanwhile, the narrative that a resilient labor market and steadier-than-expected economic growth should keep a recession at bay has gained traction, bolstering the “goldilocks” scenario for the financial markets.

Joseph Quinlan, head of CIO market strategy for Merrill and Bank of America Private Bank, said the “softness” in the U.S. consumer sector is visible but not huge, referring to that as “a canary in a coal mine,” he told MarketWatch via phone on Thursday.

The pullback in consumer spending is welcome news for Fed officials, who have increased interest rates 11 times since March 2022 to get inflation back to its preferred target of 2%. However, some analysts are worried that high interest rates and a decline in pandemic savings could eventually translate to weaker consumers in 2024, potentially another sign of a long-predicted slowdown in the U.S. economy.

“One of the things I’m most concerned about is consumers’ ability to continue to pace the economy — you’ve got several headwinds that haven’t really borne completely out yet,” said Jason Heller, senior executive vice president at Coastal Wealth. “Does the consumer continue to behave the way they behaved the last 36 months? I think you will eventually see a slowdown in consumer spending which is going to mandate a slowdown in the labor market.”

Lauren Goodwin, economist and portfolio strategist at New York Life Investments, acknowledged that a modest slowdown in inflation and employment growth means that a “Fed relief rally” in stocks can be sustained, but her concern is this late-cycle limbo is no different than those of the past, which is a moment of “goldilocks” before the very reason that inflation is moderating — slowing economic growth and employment — becomes clear in the data.

That’s why the November employment report, which will be released by the Bureau of Labor Statistics next Friday at 8:30 a.m. Eastern, will be key for investors to watch. The U.S is expected to add 172,500 jobs in November after a 150,000 increase in the prior month, according to economists polled by Dow Jones. The percentage of jobless Americans seeking work is forecast to stay the same at 3.9%, leaving it at the highest level since the beginning of 2022.

In fact, nonfarm payroll report publication days have been among the most volatile for stocks in 2023, compared with the release of monthly consumer-price index readings, which sparked some of the biggest daily up and down moves for the S&P 500 and other major indexes in 2022.

This year, the S&P 500 saw an absolute average percentage change of 1.12% on employment situation release dates, compared with an average percentage move of 0.64% on CPI days, according to figures compiled by Dow Jones Market Data.

That said, analysts are skeptical if the employment data is able to tell “a radically different story” but suggest the labor market will remain relatively tight into 2024, said Quinlan and Lauren Sanfilippo at Merrill and Bank of America Private Bank, in a phone interview.

Corporate America and their shares are telling investors a different story about next year.

With an estimated average S&P 500 earnings growth of 11.7% next year, the U.S. stock market is nowhere near recessionary concerns, said Heller. “We’ve [the stocks] priced in pretty significant growth in 2024.”

Strategists at Merrill and Bank of America Private Bank are in the camp of expecting a “mid-single digit” earnings growth for the S&P 500 in 2024, as earnings have troughed and the economy will fall back to the 2%-level of real growth after high rates confine consumer spending and corporate profits, cooling a red-hot economy.

To be sure, Wall Street analysts tend to overestimate the earnings-per-share (EPS) for the S&P 500, said John Butters, senior earnings analyst at FactSet.

The current bottom-up EPS estimate for the S&P 500 in 2024 is $246.30. If that holds true, that would be the highest EPS number reported by the large-cap index since FactSet began tracking this metric in 1996.

However, over the past 25 years, the average difference between the EPS estimate at the beginning of the year and the actual EPS number has been 6.9%, meaning analysts on average have overestimated the earnings one year in advance, said Butters in a Friday note (see chart below).

ConnectOne Bank Senior Vice President and Chief Brand and Innovation Officer Siya Vansia is focused on aligning the bank’s digital and business strategies.

Siya Vansia, senior vice president and chief brand and innovation officer, ConnectOne Bank

During the third quarter, the Englewood Cliffs, N.J.-based, $9.7 billion bank invested in its people and technology, Chief Executive Frank Sorrentino said during the bank’s October Q3 earnings call.

In an interview with Bank Automation News, Vansia discussed how ConnectOne approaches innovation, how to prioritize projects and how to determine when to buy and when to build. What follows is an edited version of that conversation:

Bank Automation News: How does ConnectOne Bank prioritize its digital strategy?

Siya Vansia: Our investments in tech and digital are all an effort to support ConnectOne’s core business. We were founded to be a leading commercial bank built around the needs of entrepreneurs and business leaders and solve for the ecosystem of their banking needs. For example, we understand that business owners want a balance of self-serve solutions coupled with a people-first client experience. To that end, some of our investments have been on the client-facing side, and the others on the employee-facing side.

BAN: How does the bank decide on an innovation project to pursue?

SV: My North Star in innovation is that my effort should support the bank’s value proposition. We are a high-performing, growth-oriented commercial bank. My efforts should always be in alignment with that, while also supporting the company’s scale and our world’s evolving trends.

Additionally, there’s a lot of opportunity with legacy technology. I typically try to find opportunities to utilize modern tools to reimagine processes. There’s a lot we unpack before pursuing an opportunity — alignment with the business, business case, efficiency creation and scalability, for example.

BAN: What is the bank’s approach to innovation when balancing third-party vendors and in-house projects?

SV: Two years ago, we were much more dependent on third-party vendors. Today, we’ve brought on incredible tech talent, which presents new opportunities to us. Really, the build-versus-buy conversation comes down to whether there is a company on the market that we could partner with and, if we choose to build, whether we have the subject matter expertise in the business unit. We’ve also taken the hybrid approach, where we‘ve partnered with a vendor to build together.

BAN: What recent tech-forward projects have you been working on?

SV: We’re in the final phases of a deposit origination project with our partner MANTL. This wasn’t just a new system. We are overhauling our deposit onboarding infrastructure and building an omnichannel approach that connects digital and in-branch experience.

We’ve also been members of the USDF Consortium, where we work alongside about a dozen other banks to explore opportunities to bring blockchain technology into the regulatory perimeter.

BAN: How would you describe your leadership style?

SV: I like to take a collaborative, open and communicative approach to leadership. Much of the work we are trying to do is fairly new, and I believe strongly that bringing different perspectives to the table is key to success. I also believe that change is iterative, so I try to move quickly to meet incremental goals so that we can continuously improve as we go. I am personally not a fan of overengineered processes or project plans, but rather playbooks that give teams flexibility.

Get ready for the Bank Automation Summit U.S. 2024 in Nashville on March 18-19! Discover the latest advancements in AI and automation in banking. Register now.

During the third quarter, net charge-offs rose to 0.11% of average loans at the regional and community banks that Stephens Inc. covers, up from 0.04% a year earlier. Those numbers include both consumer and commercial charge-offs.

Adobe Stock

Move over, deposit costs. The health of commercial borrowers is now a major source of hand-wringing among bank investors.

Problems in business loans have risen in recent months as companies that were in a weak financial position have started closing up shop. The environment remains relatively benign, and few analysts expect the credit worsening to get nearly as dire as it did after the 2008 financial crisis.

But it’s clear that the starting gun has gone off in what analysts call “credit normalization.” Bank loans were unusually healthy during the pandemic, but now more commercial borrowers are running into trouble, and bankers are starting to write off soured loans.

Some bankers have described the issues as “one-off” problems with specific borrowers, rather than anything indicating broader stresses in their loan portfolios. But investors worry those isolated events will start piling up next year. The difficulty in gauging which banks will face more trouble is prompting many stock buyers to stay away from the sector as a whole.

“The problem that a lot of these investors are facing right now is that it’s hard to get your arms around credit quality and how the banks are going to perform in a worse credit environment,” said Andrew Terrell, a bank analyst at Stephens.

During this year’s third quarter, net charge-offs rose to 0.11% of average loans at the regional and community banks that Stephens covers, up from 0.04% a year earlier. Those numbers include both commercial and consumer charge-offs.

U.S. consumers experienced stress earlier than businesses, as inflation, high interest rates and depleted savings caused some to fall behind on their credit card payments. At many credit card issuers, charge-offs are nearing or have already surpassed pre-pandemic levels.

Regional banks have been relatively insulated from consumer pressures since many of them have smaller consumer books. But worries over their commercial real estate portfolios persist, and their non-real-estate loans to commercial borrowers are starting to turn, even if problem loans remain at mild levels.

One recent corporate bankruptcy caused some tremors. Mountain Express Oil, a Georgia-based company that distributed oil to hundreds of gas stations, had gotten a $218.5 million loan from a group of banks. But the oil distributor filed for liquidation, and the banks involved in the loan now say they’re unlikely to recover any of the money they lent. That’s a tougher pill to swallow than a reorganization bankruptcy, where some recovery is likely.

The 100% loss rate was unexpected and added to investors’ usual wariness of banks’ participation in syndicated loans, said Chris McGratty, an analyst at Keefe, Bruyette & Woods. Unlike loans directly to businesses, syndicated loans leave banks at a distance from the borrower, which means they have less control when things go south. Losses tend to be larger and less predictable.

In their third-quarter earnings calls, the CEOs of affected banks said the Mountain Express Oil issue was a one-time event. And they expressed confidence in the rest of their syndicated loan exposures.

Other than that one loan, the balance sheet at First Horizon “continues to perform very well,” CEO Bryan Jordan told analysts last month. The Memphis, Tennessee-based bank led the Mountain Express Oil syndicated loan.

Concerns over the oil distributor’s bankruptcy were understandably “magnified,” since it followed a long period where investors didn’t have to worry much about the health of bank loans, KBW’s McGratty said.

“There’s going to be a normalization process — it’s well underway,” he said. “It’s still fairly good, but the trend is moving against us.”

Nowhere is that trendline clearer than in the trucking sector, which is in dire financial straits after booming during 2020. Consumers spent big on furniture, electronics and appliances as they stayed home during the pandemic. But they rapidly shifted toward travel, entertainment and restaurants as the world reopened, causing a crisis for trucking companies that suddenly had less inventory to ship.

The trucking giant Yellow Corp. filed for bankruptcy in August, part of a bloodbath that’s taken down decades-old companies.

A large concentration in trucking loans appears to have been behind the failure of a small community bank in Sac City, Iowa — the fifth bank failure this year. The bank was tiny, with just $66 million of assets, but regulators had previously dinged it for being too exposed to trucking and shut it down because of “significant loan losses.”

Trucking loans likely make up a far smaller share of total loans at many other banks, which can get in trouble with regulators for being too exposed to any one sector. But any loan losses in one area lower the cushion they’ve built up to absorb troubles elsewhere.

Other commercial sectors don’t appear to be undergoing that kind of pain, said Stephens’ Terrell. But within various industries, some companies that were already struggling are suffering as high interest rates take a toll.

“When times are really good, you’ve got air cover to restructure anything you want,” Terrell said. But as the cycle turns, the “weakest operators go first.”

Bankers say they’re keeping a close eye on their commercial real estate portfolios, particularly office loans. Occupancy rates in office buildings have fallen amid the rise of remote and hybrid work. Banks are stashing away reserves in case those loans go bad and are marking more CRE loans as “nonaccrual” credits, according to the ratings firm Fitch Ratings.

Any problems will likely “disproportionately weigh on regional banks, which have relatively higher CRE exposure,” Fitch analysts wrote in a note this week.

“However, banks are generally well positioned to absorb further ‘normalization,’” they wrote.

Bill Demchak, chairman, president and CEO of PNC Financial Services Group.

Gettyimages/Drew Angerer

PNC Financial Services Group is far from the flashiest bank around. The Pittsburgh-based bank isn’t a megabank like JPMorgan Chase or Bank of America, nor is it engaged in the massive deals that those two arrange on Wall Street. It’s no laggard in technology, but it’s not the first bank that comes to mind in that regard either.

In fact, one could even say PNC is boring. But in a year of turmoil for the banking industry — which claimed the tech-obsessed Silicon Valley Bank and wealth-obsessed First Republic Bank — perhaps boring is a solid strategy.

PNC, which at $557 billion in assets is the eighth largest U.S. bank, calls itself a national Main Street bank. It focuses on middle-market businesses, ones that aren’t household names but still play a critical role in the U.S. economy. Its roots are in Pittsburgh, but it’s steadily expanded and now has a national, coast-to-coast footprint.

Leading the charge is Bill Demchak, who’s been PNC’s CEO since 2013 and has spent two decades at the bank.

Demchak, whom American Banker is naming Banker of the Year for 2023, declined an interview request. But analysts credit his steady hand for growing PNC into a strong national franchise — one that isn’t immune to industrywide pressures but often finds a way to the top of the pack.

“The investment community is willing to bet on Bill Demchak and bet on PNC, because of the track record that he and the company has had throughout multiple cycles,” said Terry McEvoy, an analyst at Stephens. “That reflects a high level of credibility. That doesn’t happen overnight within the banking sector.”

Few investors are buying bank stocks this year, but those who are often think PNC would be more resilient if a recession hits.

“Investors are looking for high-quality, defensive names … sleep-at-night stocks,” said Ebrahim Poonawala, an analyst at Bank of America. “PNC is one of those that comes up often.”

This year, as worries over regional banks popped up, PNC found itself in a stronger position than some competitors.

Dozens of banks reported deposit outflows after Silicon Valley Bank’s failure in March, but PNC registered a tiny increase as its depositors stuck with it. Its balance sheet was in decent shape too, even if its bond portfolio fell in value when a sharp rise in interest rates eroded the prices of low-yielding bonds. Critically, PNC made itself less vulnerable by buying securities with shorter durations than certain competitors — thus ensuring any pain was shorter-term — and it avoided putting too much cash into low-yielding assets.

To be sure, PNC isn’t impervious to the struggles facing the banking industry. Its profitability is down as depositors seek higher interest rates, prompting PNC to lay off 4% of its staff. Its stock price has fallen roughly 30% this year. Its capital markets business has underperformed. The regulators under the Biden administration are toughening up rules for PNC and other regional banks.

But other regional banks are facing bigger earnings pressures, or they’re needing to readjust more as regulations get tougher. PNC, in contrast, more skillfully prepared its balance sheet for whatever comes next, making sure it had more capital and thus flexibility.

“They continue to grind away one step at a time, with calculated risks, to show consistent progress,” said Wells Fargo analyst Mike Mayo.

He added that Demchak has proven to be one of the “most independent-thinking bank CEOs.”

The tougher environment has many regional banks actively looking to shrink, but PNC’s stronger position means it remains much more open for business.

Its balance sheet gave it ample room to buy a loan portfolio from Signature Bank after the crypto-heavy bank failed. The $16.6 billion in capital commitments isn’t all that large, but it helps PNC expand its work with private equity.

If the price is right, PNC may also gain valuable customers from competitors whose slimming-down campaigns are prompting them to exit some businesses. Doing so may be “pretty attractive” for PNC, Demchak told analysts Oct. 13 when asked about the possibility.

“We’re intelligent — hopefully, intelligent — takers of risk at the right price,” Demchak said. “We can evaluate what’s out there.”

Becoming a national Main Street bank

Demchak came to PNC in 2002 as chief financial officer, marking his return to his hometown of Pittsburgh after a high-profile stint on Wall Street. Demchak helped lead JPMorgan’s development of credit derivatives products, the type of financial engineering that contributed to the 2008 financial crash.

The Financial Times once called him a “whizz-kid.” Commercial lenders at JPMorgan, wary of mathematical models upending their decades-old way of doing business, called him the “prince of darkness,” according to the book “Fool’s Gold: How the Bold Dream of a Small Tribe at J.P. Morgan Was Corrupted by Wall Street Greed and Unleashed a Catastrophe.”

The idea behind those derivatives was simple. Corporations and investors could already swap the risks tied to interest rates, currencies and commodity prices. If a company feared interest rates or the price of oil would rise, they could protect themselves by swapping that risk with another entity, which took the other side of that bet.

In the mid-1990s, Demchak and the JPMorgan team were on the forefront of applying that same idea to the chance that companies may default on their loans. If used correctly, the innovation could help spread the risk of a loan turning bad — with banks swapping the risk of borrowers defaulting on their loans to investors willing to take bets on those outcomes.

The usage of credit default swaps proliferated. Demchak and the JPMorgan team had focused on using them in the corporate world, where ample data on companies’ financial health made it easier to run statistical analyses.

But other banks and Wall Street firms soon created credit default swaps based on consumer mortgages — where historical data was more sparse and lenders were becoming far too lax. The JPMorgan team had long viewed mortgage derivatives with caution, which insulated the bank when the subprime mortgage crisis hit.

Demchak stuck to that more cautious view when he joined PNC in 2002. The bank took a more conservative approach in the years leading up to the 2008 crisis and limited its exposure to dicier sectors.

At a November 2007 presentation, Demchak noted the bank stayed away from subprime mortgages, had fewer real estate loans than its peers and was cautious on corporate credit conditions. The bank had been selling loans where it could and keeping its balance sheet slim, which reduced its profits but put it in better shape for a downturn that was already starting to brew.

“We didn’t grow the balance sheet as quickly as we could because we were worried about the risk embedded in that, and it is pretty clear today that our position has been validated by the headlines and the real world outcomes,” Demchak said at the 2007 event, according to a FactSet transcript.

PNC’s healthier financial footing helped it acquire National City Corp. when the Cleveland-based bank ran into trouble in 2008. The crisis-era purchase gave PNC a strong presence in the Midwest and turned it into the country’s fifth biggest bank by deposits.

Then-CEO James Rohr, along with his heir-apparent Demchak, continued PNC’s expansion from there. The bank bought the Royal Bank of Canada’s fledgling U.S. retail operations in 2011, giving it hundreds of branches in the Southeast.

The deal-making slowed once Demchak became CEO in 2013. But he struck a major deal in November 2020, buying the U.S. bank of the Spanish giant Banco Bilbao Vizcaya Argentaria, including branches in Texas, California, Arizona and Colorado.

The BBVA USA deal finally accomplished PNC’s mission: taking the bank national. PNC branches now stretch from coast to coast, and the bank is in all 30 of the largest U.S. markets.

However, that deal followed a questionable move from PNC. In May 2020, as COVID-19 uncertainty continued to cloud the economy, PNC sold its stake in the asset-management giant BlackRock. The bank owned 22% of BlackRock, whose boom since PNC bought it in 1995 made it a stellar investment.

Had it waited a few more months, PNC would have reaped far more cash, and not prompted Barron’s to criticize the “folly” in the sale.

On the plus side, PNC was able to use the proceeds to buy BBVA’s U.S. operations a few months later. And since few banks were interested in acquisitions in 2020, PNC was able to get BBVA for fairly cheap, said Poonawala, the Bank of America analyst.

So far, the BBVA deal seems to be going well. Mayo, the Wells Fargo analyst, praised PNC for being able to integrate the two systems together quickly for customers.

But the smooth integration of BBVA is partly thanks to PNC’s long efforts to improve its data infrastructure and make the company more efficient, Mayo said. Those efforts may not be all that exciting, but the integration showed how “10-plus years of back-office restructuring and tinkering pays off,” he said. It’s yet another reason why Mayo calls PNC the “bank of steel,” a nod to its Pittsburgh roots but also the resiliency of its technology and balance sheet.

“It got a bit rusty with the sale of BlackRock for a period, but then it took some of that rust off,” Mayo said, noting PNC “made victory out of defeat” by using the BlackRock sale proceeds to buy BBVA at a great price.

Blythe Masters, who worked for Demchak at JPMorgan and rose to other top roles at the megabank, said he is “one of, if not the, most talented individuals I have worked with or for.

“He is an exceptional judge of talent, an intuitive and detail-oriented risk manager, a deeply strategic thinker and capable of playing a long game,” said Masters, who’s now founding partner of the tech investment firm Motive Partners.

“I’m delighted, but not remotely surprised, that he and his team have made PNC such a great success,” Masters added.

Executives at PNC have said they will be watching how commercial real estate loans tied to office buildings continue to fare.

Bloomberg News

Preparing for a rainy day

How PNC fares in a downturn — assuming the U.S. economy will eventually break its streak of outperforming expectations — remains to be seen.

Like any other bank, it would lose money as consumers fall behind on their payments and businesses struggle to pay back loans. But analysts point to PNC’s solid history of outperforming other banks on credit quality as a sign that its underwriting is solid.

And in the sector that’s currently the biggest source of worry — empty office buildings as some employers offer remote and hybrid work options — PNC’s exposure is relatively low.

Some 2.8% of PNC’s loans were in office-related commercial real estate as of last year, according to a Jefferies analysis of large and regional banks’ office CRE exposures.

While that was above the median of 1.7%, some competitors such as Citizens Financial Group, M&T Bank and Wells Fargo have about 4% of their total loans in office CRE. Several midsize banks that are significantly smaller than PNC have much larger exposures.

Whether office leases will be a major source of trouble in the coming months is unclear. Some argue the pain will be gradual, since office leases often stretch several years and the tenants won’t leave all at once. Others worry vacancy trends, high interest rates and other factors will lead to more stress — particularly at midsize banks that are more exposed.

PNC has been monitoring the situation closely and stashing away reserves to cover the potential souring of office loans.

“We’ll need those reserves because we do think there’s going to be problems in the office space,” Demchak told analysts in July.

For borrowers who do run into problems, PNC is working to figure out other options, such as selling buildings if needed or getting more equity from their investors.

The bank is also giving its own investors a detailed overview of its office loans — whether they’re in downtowns or suburban areas; whether they’re medical offices and thus less exposed to work-from-home trends; and whether any have seen stress thus far.

In some ways, Stephens’ McEvoy said, PNC’s moderate exposures to the office sector lines up with its history. It was less exposed to housing in 2008, but also to the energy sector when a slump there prompted charge-offs at banks around 2015.

“It just seems like PNC always ends up having less exposure to whatever problem lending category is out there,” McEvoy said.

The bank is “not immune to the operating environment,” Poonawala said. But, he added, Demchak’s leadership has instilled confidence that “PNC should be able to navigate whatever the cycle looks like.”

City National Bank has tapped Howard Hammond, a 17-year veteran of Fifth Third Bancorp, as its new CEO to replace Kelly Coffey, who will move to a newly-created role as CEO of the bank’s entertainment unit.

Hammond will relocate to Los Angeles and report to Greg Carmichael, the former CEO of Fifth Third Bancorp, who was named executive chair of City National’s board of directors in September. The appointments are effective Nov. 27, the bank said in a press release. The news was first reported by Variety.

The $96.4 billion-asset City National — long known as the “bank to the stars” because of its extensive Hollywood connections — was acquired by Toronto-based Royal Bank of Canada in 2015.

Coffey has been CEO for five years and was tapped to lead City National by the bank’s longtime former CEO Russell Goldsmith.

In January, City National got hit with a consent order by the Justice Department over allegations that it failed to offer home loans to Black and Hispanic borrowers in Los Angeles County from 2017 to 2020. The bank agreed to pay $31 million in the largest redlining settlement in the agency’s history.

The bank was also burdened with higher funding costs due to soaring interest rates, and pressure to reduce lending capacity as a means of conserving capital and liquidity, RBC CEO Dave McKay said on a recent earnings call. RBC faced pressure to cut costs substantially after City National reported a $38 million loss in the third quarter, which ran from May to July, leading analysts to question how the bank planned a turnaround.

Amid profit woes, City National will get an infusion of new leadership

Hammond, a 30-year banking veteran, will join City National’s board of directors and the executive committee of RBC’s U.S. intermediate holding company. He most recently served as Fifth Third’s executive vice president and head of consumer banking, overseeing 8,000 employees and more than 1,000 branches. He previously served as head of Fifth Third’s retail banking and brokerage unit, and as president and CEO of Fifth Third Securities.

“He is the ideal leader to take City National to its next stage and prepare the bank for future success,” Carmichael said in a press release.

Under the restructured executive lineup, JaHan Wang, City National’s current executive vice president of entertainment banking, will report to Coffey while Martha Henderson will remain vice chairman of entertainment banking.

It was a trading day unlike any other for traders in the $25 trillion Treasury market, with a 30-year bond auction seen as having been partially undermined by a cyberattack on the U.S. unit of a Chinese bank.

In recapping Treasury’s poorly received $24 billion bond auction on Thursday, traders said the weaker-than-expected results likely had at least something to do with this week’s ransomware hit on the American arm of Industrial & Commercial Bank of China, known as ICBC. That attack reportedly caused disruptions across the market and had some impact on liquidity, with the Financial Times citing unnamed sources as saying hedge funds and asset managers were forced to reroute trades.

Traders were grappling on Friday to answer the question of what created the sudden lack of interest at the auction, which went so badly that it also shook up U.S. stock investors. Thursday’s sale was the worst since November 2021, based on the extent to which primary dealers were forced to step in and pick up the slack in demand, one trader said. And it reinforced a recent pattern of weak auctions for the 30-year bond that may not bode well for future sales of that long-dated maturity.

It’s possible that bonds simply “look much less attractive” following a recent “explosive rally” since late October, according to Charlie McElligott, a cross-asset macro strategist at Nomura Securities in New York. However, “this might be the case of ‘more than meets the eye’ to this ‘ugly auction evidencing low demand for duration’ story,” he wrote in a note.

“One dynamic that makes yesterday’s ugly auction results murky was the ICBC cyberattack described across various financial media, which gunked-up anybody who clears UST trades through them, and made it so that many dealers were then likely unable to trade with those clients until resolved, on account of unsettled trades which weren’t able to be matched,” McElligott said.

Adding to Thursday’s uncertainty was another random event. Federal Reserve Chairman Jerome Powell appeared on stage in an International Monetary Fund panel, was interrupted by a climate protester, and then uttered a seven-letter expletive that could be heard on the event’s livestream.

Powell’s policy-related remarks, which indicated the central bank might take further action to control inflation, “didn’t help things and kind of spooked people again,” said John Farawell, head of municipal trading at New York bond underwriter Roosevelt & Cross.

On Friday, the Treasury market found stabilization as buyers returned to segments of government debt in a sign that calm was being restored. A rush of buying was seen on the 30-year bond BX:TMUBMUSD30Y,

sending its yield down to 4.733% and to a third straight weekly decline.

Meanwhile, Bloomberg News reported that the repercussions of the ICBC cyberattack included an inability to deliver U.S. debt that was being pledged as collateral. ICBC’s U.S. unit was forced to rely on a messenger carrying a USB stick across Manhattan to complete disrupted trades, according to the news service, which also described Thursday’s $24 billion 30-year bond auction as one of the worst in a decade.

The ICBC attack “might have had a dramatic impact on the auction. I don’t know how much, but I also can’t imagine it didn’t,” said Tom di Galoma, co-head of global rates trading for BTIG in New York. “When people see that there are trade-settlement issues, there’s a willingness to back off and that’s exactly what happened yesterday. Institutional accounts were saying, ‘We don’t know who is settling this trade.’ If the cyberattack hadn’t happened, I think the auction would have gone a lot better.”

Ben Emons, a senior portfolio manager and head of fixed income for NewEdge Wealth in New York, said that once the Treasury market got upended by the ICBC cyberattack, the bad auction, and the interruption during Powell’s appearance, liquidity on U.S. government debt “was, for a moment, a dark matter.”

U.S. stocks ended sharply higher Friday, more than shaking off weakness seen the previous session in the aftermath of a poor Treasury bond auction and fresh signs that interest rates may stay higher for longer.

Technology stocks drove the bounce, with the Nasdaq Composite leading major indexes to the upside as it and the S&P 500 logged their highest finishes since September.

What happened

The Dow Jones Industrial Average DJIA

rose 391.16 points, or 1.2%, to close at 34,283.10.

The S&P 500 SPX

ended with a gain of 67.89 points, or 1.6%, at 4,415.24.

The Nasdaq Composite COMP

advanced 276.66 points, or 2%, to finish at 13,798.10.

The rally left the Dow with a weekly gain of 0.7%, while the S&P 500 advanced 1.3% and the Nasdaq booked a rise of 2.4%. The Dow saw its highest close since Sept. 20, while the S&P 500 ended at its highest since Sept. 19 and the Nasdaq at its highest since Sept. 14.

Meanwhile, the S&P 500 tested important chart resistance at the 4,400 to 4,415 level, which marks the confluence of previous resistance and the 61.8% Fibonacci retracement of the July-October drop, according to Matthew Weller, global head of research at Forex.com, in a note (see chart below).

Forex.com

“From a bigger picture perspective, bulls will need to see the index conclusively break above 4415 before declaring that the post-July streak of lower lows and lower highs is over,” Weller wrote.

The S&P 500 and Nasdaq Composite ended their longest winning streaks since November 2021 on Thursday, after a poorly-received $24 billion sale of 30-year Treasury bonds.

A calmer bond market may have helped set the tone for stocks. The yield on the 30-year Treasury bond BX:TMUBMUSD30Y

fell 3.2 basis points to 4.733%, after it nearly notched its biggest one-day jump since June 2022. The yield still saw a weekly decline, its third straight.

It was unclear whether the Treasury auction had been affected by a reported ransomware attack against the U.S. unit of the Industrial & Commercial Bank of China that apparently disrupted the U.S. Treasury market.

Thursday’s setback was also tied to comments from Federal Reserve Chairman Jerome Powell, who told an International Monetary Fund panel on Thursday that the central bank was wary of “head fakes” from inflation, and the “2% goal was not assured.”

Much of Powell’s language was nearly identical to remarks he made on Nov. 1, when investors rallied stocks and bonds after the Fed chair didn’t explicitly commit to a further interest rate hike. But the subsequent rally for stocks after the Nov. 1 Fed meeting, with the S&P 500 jumping more than 6% over eight days, and a 50 basis point drop in the 10-year Treasury yield were “overdone and not governed by facts,” said Tom Essaye, founder of Sevens Report Research, in a note.

“Meanwhile, if we think about what the Fed said last week, namely that the rise in the 10-year yield was doing the Fed’s work for it and as a result they may not have to hike rates, then the short/sharp decline in the 10-year yield we’ve seen could essentially remove the reason for the Fed not having to hike rates — and that could put a rate hike back on the table!” he wrote. “That’s essentially what Powell reminded us of yesterday and that, along with the poor Treasury auction, pushed yields higher,” setting up pressure on stocks.

U.S. consumer sentiment fell in November for the fourth month in a row due to worries about higher interest rates as well as war in the Middle East. The preliminary reading of the sentiment survey declined to 60.4 from 63.8 in October, the University of Michigan said Friday. It’s the weakest reading since May.

Investors were also tuning into more comments by Fed officials Friday, including San Francisco Fed President Mary Daly, who said she didn’t know if rates were high enough to bring inflation back down to the central bank’s 2% target.

Lions Gate Entertainment Corp. LGF.A, -0.66%

shares fell 0.7% after the TV, film and media giant reported a surprise second-quarter profit, and stuck with its full-year outlook “even with the negative impact of the strike” by Hollywood’s writers and actors earlier this year.

UBS Group issues $3.5 billion in Additional Tier 1 bonds in the first issuance since the acquisition of Credit Suisse.

It is comprised of two tranches of $1.75 billion of 9.25% perpetual notes redeemable at the option of UBS after five years and $1.75 billion of 9.25% perpetual notes redeemable after 10 years.

“Each issue is a direct, unsecured and subordinated obligation of UBS Group AG,” it said.

“The notes provide that, following approval of a minimum amount of conversion capital by UBS Group AG’s shareholders, upon occurrence of a trigger event or a viability event, the notes will be converted into UBS Group AG ordinary shares rather than be subject to write-down,” UBS added.

A weak session is setting up for Tuesday, with oil under pressure after unexpectedly downbeat China export data. So the preference is for bonds this morning, as stock futures tilt south.

Onto our call of the day, which deals with another worry — a wall of government debt that will be with us for decades. It comes from Bridgewater’s highly regraded co-chief investment officer Bob Prince, who was speaking at the Global Financial Leaders’ Investment Summit on Tuesday, hosted by the Hong Kong Monetary Authority.

Prince touches on asset liability mismatches, such as what was seen during the banking crisis earlier this year. He explains that one big factor behind a crisis is when a certain economic regime exists for an extended period of time and “people extrapolate that into the future on the basis of leverage and asset liability mismatches. Then you get a shift in that regime.”

The events of March, which saw the collapse of SVB, Signature Bank and Silvergate, were a perfect example of that, Prince says. Then he turns to what he calls the “broader effects of a transition from 15 years of abundant free money,” that was first used to battle deleveraging pressures in the financial system in 2008 and then the pandemic.

One long-term effect of that gets particular attention by Prince, who points out how U.S. government Treasury debt to GDP was about 70% in 2008, around where it had been for decades.

“The after effects of offsetting deleveraging and pandemic, you’ve had a massive wealth shift from the public sector to the private sector and that’s left the government with debt to GDP up from 70% up to 120%. And the particular vulnerability of that is in the debt rollovers and the gross issuance that you’re going to see in the coming decades . You’re stuck with that debt until you pay it off and that means you have to roll it over like anybody else does,” said Prince.

“Gross debt issuance will be running at 25% for as far as the eye can see, that means every year you’re issuing 25% of GDP in debt. In 1960, the average amount of debt issuance was 12% of GDP,” he said.

Prince says most people really don’t pay attention to debt rollovers because they just assume those will get done, but notes that when countries have experienced balance of payments crisis in the past, mostly emerging markets, that is because they have been unable to roll over that debt.

In the U.S. case, it’s crucial to look at who is holding the debt, particularly the 27% held by foreign investors and 18% by central banks. “Foreign investors would normally be a reliable source of investment but it does heighten sensitivity to geopolitical risk, and so geopolitical risk converges with debt rollovers and gross issuance of the Treasury is an issue that you need to pay attention to in the coming years.

While not an “acute problem,” he says, it’s a lingering one, and when it comes to central banks it’s also unclear whether their holdings also present a “rollover risk.”

Prince also touches on the fact that that all that “abundant free money” has fueled a private-equity boom, but with interest rates now at 8% instead of 2% or 3%, “the pace and transaction cycle is bound to slow,” and they are starting to see that.

“When we talk to institutional investors around the world, many of them are experiencing liquidity issues right now and the liquidity issues result from the fact so much money was allocated to private assets and the transaction cycle is slowing,” he said.

A team of analysts at Citigroup led by Nathan Sheets have also weighed in on government debt, telling clients in a new note that “it’s unwise for policy makers to experiment or test” where the threshold for too much debt lies. Here’s their chart showing the bleak trajectory:

Dirk Willer, head of global asset allocation at Citigroup, said a debt crisis scenario in the U.S. would likely mean a selloff of risk assets globally. He notes that bonds in rival countries may not be the best bet as they don’t always benefit. And both gold and bitcoin underperformed during the U.K. gilt crisis, so those may be out.

UBSG, +2.79%

swung to a $785 million quarterly loss on lingering effects of its Credit Suisse takeover, but it pulled in $33 billion in new deposits and shares are up.

The U.S. trade deficit climbed 5% in September to $61.5 billion as imports rebounded. Still to come is consumer credit at 3 p.m. Fed Vice Chair for Supervision Michael Barr speaks at 9:15 a.m., followed by Fed Gov. Christopher Waller at 10 a.m.

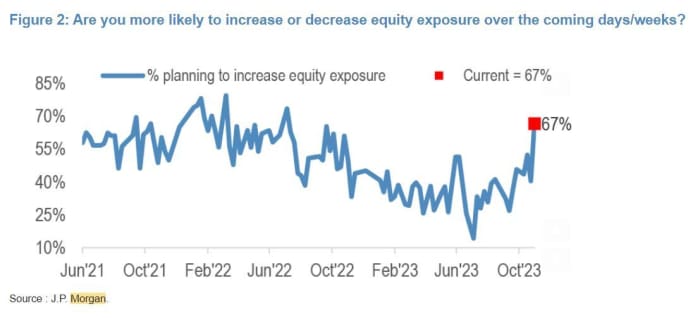

According to this recent JPMorgan survey, two-thirds of investors are ready to start pumping more money into equities, while just 19% plan to increase bond exposure. Also, note that 67% also said they did not expect performance of the Magnificent 7 stocks — Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla and Meta — to “crack before the end of the year.”

Top tickers

These were the top-searched tickers on MarketWatch as of 6 a.m.:

HSBC Holdings PLC’s third-quarter net profit more than doubled as the London-based banking giant continued to benefit from higher interest rates and sharply higher non-interest income.

The Asia-focused lender posted net profit of $5.62 billion for the three months to Sept. 30, up from $2.00 billion in the year-earlier period, it said Monday. HSBC’s pretax profit, the bank’s preferred profit measure, rose to $7.71 billion from $3.23 billion.

The bank’s quarterly revenue rose 40% compared with the same period a year earlier to $16.2 billion. It attributed the growth to the higher interest rate environment, which supported growth in net interest income in all of their global businesses and higher non-interest income.

Its non-interest income rose 97% on year to $6.9 billion, primarily due to the sale of its retail banking operations in France.

The bank’s net interest income, its main source of income, reached $9.25 billion, from $8.01 billion in the same period last year. Its net interest margin increased by 19 basis points to 1.70% from the year-earlier period.

“We have had three consecutive quarters of strong financial performance and are on track to achieve our mid-teens return on tangible equity target for 2023,” HSBC Chief Executive Noel Quinn said.

HSBC reiterated its guidance for 2023 net interest income to be above $35 billion, it said.

The board has approved a third interim dividend of $0.10 per share. It also intends to initiate a further share buyback of up to $3 billion after announcing three share buybacks in 2023 totaling up to $7 billion.