[ad_1]

Most investors want to keep things simple, but digging a bit into details can be lucrative — it can help you match your choices to your objectives.

The JPMorgan Equity Premium Income ETF

JEPI,

has been able to take advantage of rising volatility in the stock market to beat the total return of its benchmark, the S&P 500

SPX,

while providing a rising stream of monthly income.

The objective of the fund is “to deliver a significant portion of the returns associated with the S&P 500 Index with less volatility,” while paying monthly dividends, according to JPMorgan Asset Management. It does this by maintaining a portfolio of about 100 stocks selected for high quality, value and low price volatility, while also employing a covered-call strategy (described below) to increase income.

This strategy might underperform the index during a bull market, but it is designed to be less volatile while providing high monthly dividends. This might make it easier for you to remain invested through the type of downturn we saw last year.

JEPI was launched on May 20, 2020, and has grown quickly to $18.7 billion in assets under management. Hamilton Reiner, who co-manages the fund with Raffaele Zingone, described the fund’s strategy, and its success during the 2022 bear market and shared thoughts on what may lie ahead.

Outperformance with a smoother ride

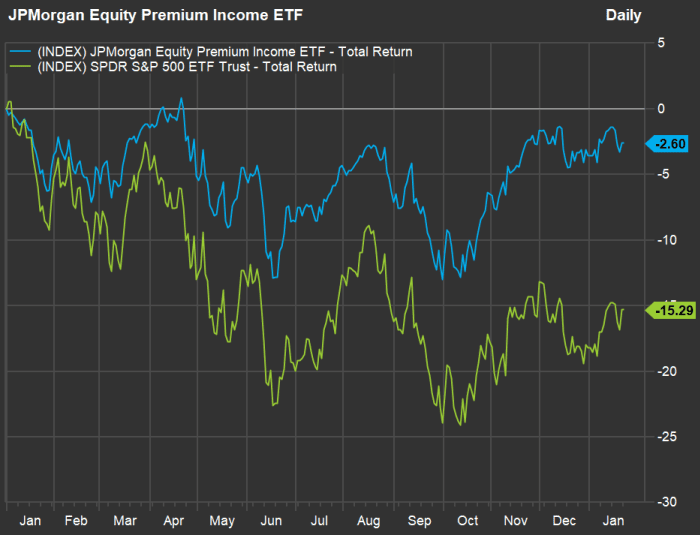

First, here’s a chart showing how the fund has performed from when it was established through Jan. 20, against the SPDR S&P 500 ETF Trust

SPY,

both with dividends reinvested:

JEPI has been less volatile than SPY, which tracks the S&P 500.

FactSet

Total returns for the two funds since May 2020 pretty much match, however, JEPI has been far less volatile than SPY and the S&P 500. Now take a look at a performance comparison for the period of rising interest rates since the end of 2021:

Rising stock-price volatility during 2022 helped JEPI earn more income through its covered call option strategy.

FactSet

Those total returns are after annualized expenses of 0.35% of assets under management for JEPI and 0.09% for SPY. Both funds have had negative returns since the end of 2021, but JEPI has been a much better performer.

““Income is the outcome.””

The income component

Which investors JEPI is designed for? “Income is the outcome,” Reiner responded. “We are seeing a lot of people using this as an anchor tenant for income-oriented portfolios.”

The fund quotes a 30-day SEC yield of 11.77%. There are various ways to look at dividend yields for mutual funds or exchange-traded funds and the 30-day yield is meant to be used for comparison. It is based on a fund’s current income distribution profile relative to its price, but the income distributions that investors actually receive will vary.

It turns out that over the past 12 months, JEPI’s monthly distributions have ranged between 38 cents a share and 62 cents a share, with a rising trend over the past six months. The sum of the past 12 distributions has been $5.79 a share, for a distribution yield of 10.53%, based on the ETF’s closing price of $55.01 on Jan. 20.

JEPI invests at least 80% of assets in stocks, mainly selected from those in the S&P 500, while also investing in equity-linked notes to employ a covered call option strategy which enhances income and lowers volatility. Covered calls are described below.

Reiner said that during a typical year, investors in JEPI should expect monthly distributions to come to an annualized yield in the “high single digits.”

He expects that level of income even if we return to the low-interest rate environment that preceded the Federal Reserve’s cycle of rate increases that it started early last year to push down inflation.

JEPI’s approach may be attractive to investors who don’t need the income now. “We also see people using it as a conservative equity approach,” Reiner expects the fund to have 35% less price volatility than the S&P 500.

Getting back to income, Reiner said JEPI was a good alternative even for investors who were willing to take credit risk with high-yield bond funds. Those have higher price volatility than investment-grade bond funds and face a higher risk of losses when bonds default. “But with JEPI you don’t have credit risk or duration risk,” he said.

An example of a high-yield bond fund is the iShares 0-5 Year High Yield Corporate Bond ETF

SHYG,

It has a 30-day yield of 7.95%.

When discussing JEPI’s stock selection, Reiner said “there is a significant active component to the 90 to 120 names we invest in.” Stock selections are based on recommendations of JPM’s analyst team for those that are “most attractively priced today for the medium to long term,” he said.

Individual stock selections don’t factor in dividend yields.

Covered call strategies and an example of a covered-call trade

JEPI’s high income is an important part of its low-volatility total-return strategy.

A call option is a contract that allows an investor to buy a security at a particular price (called the strike price) until the option expires. A put option is the opposite, allowing the purchaser to sell a security at a specified price until the option expires.

A covered call option is one an investor can write when they already own a security. The strike price is “out of the money,” which means it is higher than the stock’s current price.

Here’s an example of a covered call option provided by Ken Roberts, an investment adviser with Four Star Wealth Management in Reno, Nev.

-

You bought shares of 3M Co.

MMM,

+1.63%

on Jan. 20 for $118.75. - You sold a $130 call option with an expiration date of Jan. 19, 2024.

- The premium for the Jan. 24, $130 call was $7.60 at the time that MMM was selling for $118.75.

- The current dividend yield for MMM is 5.03%.

- “So the maximum gain for this trade before the dividend is $18.85 or 15.87%. Add the divided income and you’ll get 20.90% maximum return,” Roberts wrote in an email exchange on Jan. 20.

If you had made this trade and 3M’s shares didn’t rise above $130 by Jan. 19, 2024, the option would expire and you would be free to write another option. The option alone would provide income equivalent to 6.40% of the Jan. 20 purchase price in the period of a year.

If the stock rose above $130 and the option were exercised, you would have ended up with the maximum gain as described by Roberts. Then you would need to find another stock to invest in. What did you risk? Further upside beyond $130. So you would have written the option only if you had decided you would be willing to part with your shares of MMM for $130.

The bottom line is that the call option strategy lowers volatility with no additional downside risk. The risk is to the upside. If 3M’s shares had doubled in price before the option expired, you would still wind up selling them for $130.

JEPI pursues the covered call options strategy by purchasing equity-linked notes (ELNs) which “combine equity exposure with call options,” Reiner said. The fund invests in ELNs rather than writing its own options, because “unfortunately option premium income is not considered bona fide income. It is considered a gain or a return of capital,” he said.

In other words, the fund’s distributions can be better reflected in its 30-day yield, because option income probably wouldn’t be included.

One obvious question for a fund manager whose portfolio has increased quickly to almost $19 billion is whether or not the fund’s size might make it difficult to manage. Some smaller funds pursuing narrow strategies have been forced to close themselves to new investors. Reiner said JEPI’s 2% weighting limitation for its portfolio of about 100 stocks mitigates size concerns. He also said that “S&P 500 index options are the most liquid equity products in the world,” with over $1 trillion in daily trades.

Summing up the 2022 action, Reiner said “investing is about balance.” The rising level of price volatility increased options premiums. But to further protect investors, he and JEPI co-manager Raffaele Zingone also “gave them more potential upside by selling calls that were a bit further out of the money.”

Don’t miss: These 15 Dividend Aristocrat stocks have been the best income builders

[ad_2]