Bitcoin mining firm CleanSpark has announced the start of construction on a site in Washington, Georgia, set to house 16,000 miners, which could bring the company’s hash rate total to as high as 8.7 EH/s.

The site, which CleanSpark announced the acquisition of in 2022, would contribute to an additional 2.2 EH/s of hash rate for the company. The expansion is estimated to cost nearly $16 million according to the press release sent to Bitcoin Magazine.

“The mining machine fleet at the new phase will consist of Antminer S19j Pro and Antminer S19 XP models, the newest and most power-efficient models of bitcoin mining machines available today,” states the release.

“When we purchased the Washington site in August, we were confident about our ability to quickly expand, adding this 50MW to the existing 36MW of infrastructure,” Zach Bradford, CleanSpark’s CEO commented. “This second phase more than doubles the size of the existing operation. We are looking forward to expanding our relationship with the Washington City community and to be able to support the construction jobs that will come with this expansion.”

Scott Garrison, vice president of business development at the firm, highlighted how the site “uses mainly low-carbon sources of power, employs newest generation tech, and is among the most power-efficient and sustainable bitcoin mining operations.”

Despite the recent wider downturn in the mining industry, CleanSpark has seen a remarkable expansion from just 2.1 EH/s in January 2022, to 6.2 EH/s in December 2022. This expansion, alongside another site buildout in Sandersville, Georgia, is set to continue that rapid growth in the coming year.

Cleanspark, a publicly traded bitcoin miner based in Las Vegas, Nevada, has announced their December 2022 bitcoin mining update, in addition to comments from the CEO reflecting on 2022.

“Among our many accomplishments this year, I’m most proud of increasing our annual bitcoin production by over 200% as we expanded our fleet and the number of mining campuses we own and operate throughout Georgia,” said Zach Bradford, CEO, in the release. “Even in this down market, we are committed to the promise of bitcoin and are proud to be part of the global network that keeps it secure for millions of users across the world.”

The company mined a total of 464 bitcoin in the month of December, to conclude 2022 with a total of 4,621 bitcoin mined. As of December 31, the company held 228 bitcoin while it sold 517 bitcoin in December for operations and growth.

Like other public miners this year, Cleanspark has faced a dramatic downturn in its stock price, just as the price of bitcoin fell similarly. Despite this, when priced in bitcoin, Cleanspark has maintained a relatively steady valuation, and has continued to expand its operations.

In September, mining expert Zack Voell detailed how the energy company turned miner is continuing to grow despite the various headwinds currently present in the bitcoin market. This continued with ASIC acquisitions in the following months, as well as record production of bitcoin in October.

The December report also detailed the company’s operational reactions to the winter storm which ravaged the United States that month, describing how 98% of its machines present in Georgia were powered down due to the conditions. The machines were turned back on as soon as the temperature and humidity levels permitted.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Latest Public Miner Developments

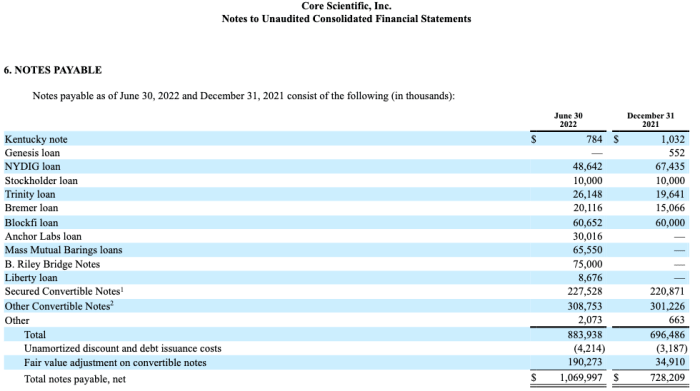

After writing on the potential for public miner capitulation and covering Core Scientific’s possible bankruptcy route, there’s been a wave of miner announcements and developments that show industry-wide risks taking more shape. The major risk is miners’ accumulated debt and lack of cash flow to afford the interest rate on that debt as profit margins are squeezed. The other risk is hash rate (ASIC mining machines) that has been used as collateral to secure this debt financing.

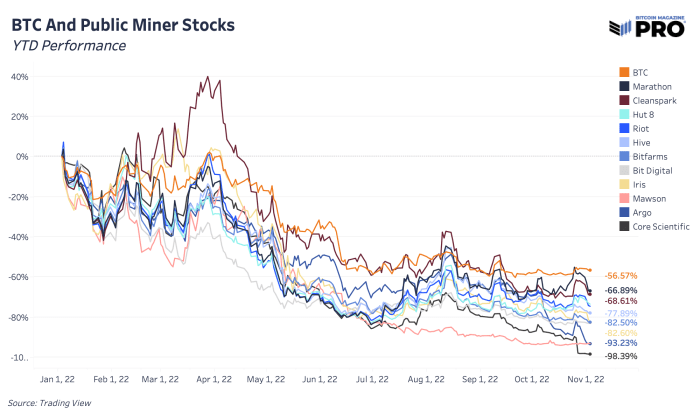

Public miners across the board continue to heavily underperform bitcoin in year-to-date performance. That’s not a new trend but now, as miners start to fall and the survivors emerge, the performance gap starts to widen in a big way. Miners on the edge of going under are down over 90% while the market’s chosen “stronger” miners are more in the 60-70% drawdown range.

Public miner stocks priced in bitcoin

Starting with Core Scientific, there’s a laundry list of firms that are owed money, including BlockFi, NYDIG and Anchor Labs. In total, creditors are owed around $1 billion and even MassMutual Barings (an investment firm owned by Mutual Life Insurance Co.) is on the short list.

Argo Blockchain is one of those at the bottom, now down 93.23% this year. They released the biggest mining news of the week after announcing that a planned $27 million fundraise didn’t go through. Earlier this year, NYDIG agreed to a $70.6 million loan with Argo. Argo also used some of its bitcoin holdings in August to reduce their BTC-backed loan obligations from Galaxy Digital as well.

Iris Energy highlighted in a financing update this week that the company is “currently capable of generating an indicative $2 million of Bitcoin mining monthly gross profit, compared to aggregate required monthly principal and interest payment obligations of $7 million.” After borrowing $71 million from NYDIG which was secured by ASIC machines for one of their outstanding loans and at risk of needing a debt restructuring, Iris has nearly 36,000 machines that may change hands fairly quickly. The company would default on these loans unless they can find a new agreement by November 8.

Stronghold Digital Mining just this week closed on their debt restructuring deal with NYDIG, delivering a fleet of 26,200 miners in exchange for the wipeout of $67.4 million in debt. Stronghold also extended another tranche of debt to be repaid over 36 months instead of 13 to buy more cash runway. The moves have been a strategic action to “rapidly de-lever our balance sheet and enhance liquidity”.

CleanSpark, who’s been in a place of growth and able to buy ASICs at lower prices recently, ended up selling more of their bitcoin holdings (mined 532 BTC and spent 836) last month to support growth and operations. Although many major miners are still maintaining their HODL strategies and bitcoin balances, strong miners will tap into those holdings for growth opportunities or funding operations when absolutely needed.

TeraWulf, another bitcoin miner down 92.38% year-to-date, runs a relatively high debt-to-equity ratio compared to other miners (86%) and has $120 million in debt to start being paid back in spring 2023 at an 11.5% interest rate.

As larger private lenders like BlockFi and NYDIG don’t disclose how much mining debt is on their balance sheets, it’s impossible to know for sure how exposed some of these lenders are to broader mining industry bankruptcy risk on the horizon. These loans may be a reasonable portion of broader financing activities and well equipped to handle the default risk, but it’s a dynamic worth highlighting and to better understand as we expect more miners to face pressure of debt default and/or restructuring over the next few months.

One opinion from Marathon Digital Holdings CEO Fred Thiel, ballparks that 20 or so public miners could be at risk of going bankrupt in what he deems a perfect storm for the industry. There’s no doubt that larger, better positioned miners are looking for potential, favorable acquisition deals to arise fairly soon. Like every other industry before it, major industry consolidation is inevitable and public bitcoin mining looks primed to go through that next phase of its lifecycle. It’s likely we move to a world where there are only a few major bitcoin miner giants with a handful of much smaller miners behind them.

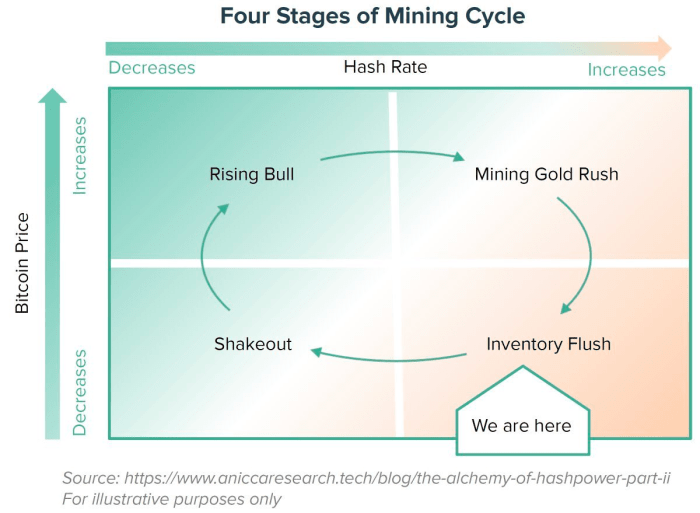

Similarly, it’s entirely possible that as this cycle moves from the bottom right quadrant to the bottom left, cash rich energy producers at both the public and private level start scooping up ASICs to deploy in preparation for the next bull phase.

The biggest risk inherent to the bitcoin market today remains the weak players hanging by a thread underneath the surface. The lack of meaningful price volatility in this $20,000 range is certainly encouraging from the standpoint of buyers and sellers finding a temporary equilibrium. But as the frequency of miner troubles continues to rise, along with the possibility of more fund-based leverage still in the market, max pain unequivocally is lower for industry participants. The brunt of the selling has taken place with bitcoin now at $20,000, but one has to question whether the marginal buyer is of sufficient size to stem the potential selling pressure on the horizon.

We suspect that the pressure is beginning to ramp up on the crypto lenders that did survive the summer contagion, due to the increasing headwinds certain miners are facing in this environment.

CleanSpark Inc., an energy company turned bitcoin miner, produced a record amount of new BTC last month.

The Nasdaq-traded firm said in a statement sent to Bitcoin Magazine that it had mined 532 bitcoin in October, representing a nearly 20% increase from its September production. In addition, the company also shared some updates on its immersion-cooled farm.

“I’m excited to announce that Phase 2 of our immersion-cooled mining campus in Norcross is now officially complete and hashing,” said Zach Bradford, CleanSpark’s CEO, per the statement. “The progress there has translated into another record-breaking month for us, mining a total of 532 bitcoin. And we’ve now seen a 20% increase in our hashrate two months in a row.”

CleanSpark has mined a total of 3,622 BTC so far this year. However, the miner only holds 290 bitcoin on its balance sheet as it has been selling most of its production to cover operating costs. In October, the firm sold 836 BTC to fund “growth and operations” at an average price of approximately $19,340 per bitcoin to proceeds of $16.1 million.

While some bitcoin miners have faced extreme hardship since the digital currency’s price tumbled earlier this year, CleanSpark has grown its business, scooping up miners and facilities at attractive prices. Earlier this week, the firm announced it had purchased nearly 3,900 Bitmain Antminer S19j Pro miners to its mining fleet for $5.9 million, which translates to about $15.50 per terahash. The price tag paid by CleanSpark is low as, according to data from mining services company Luxor Technologies, machines of such efficiency are currently selling at about $23 per terahash.

Last week, CleanSpark hiked its 2022 hash rate forecast by 10% to 5.5 exahash per second (EH/s) from 5 EH/s. As of October 31, 2022, the company’s mining fleet operated with a hash rate of 5.1 EH/s, up 23% from September 2022. Daily bitcoin mined reached 19.2 in October.