Whether by choice or necessity, a growing number of American seniors are working well into their golden years. As of 2024, 23.4% of men and 16.2% of women over the age of 65 were still employed, according to the Bureau of Labor Statistics (BLS) (1).

Many of these seniors are also collecting Social Security benefits while at work. According to the Center for Retirement Research at Boston College, roughly 40% of individuals work after claiming benefits, often for several years (2).

The system allows beneficiaries to earn some employment income, but only up to a certain limit. Beyond these thresholds, benefits are clawed back and withheld. If you’re in this situation, understanding how the rules work and what the threshold is for income in 2026 could be a key part of your financial plans.

Here’s what you need to know.

Working while collecting benefits is permitted. However, income from your work could impact your benefits depending on your age and level of income.

If you’re below Full Retirement Age (FRA), you can earn up to $24,480 in 2026 without impacting your benefits (3). This threshold is adjusted every year and is currently 1,080 higher than the previous year. For every $2 you earn above this threshold, the Social Security Administration (SSA) will withhold $1 in benefits.

These earning restrictions are greatly relaxed in the calendar year you reach FRA. If you reach FRA in 2026, you can earn up to $65,160 — $3,000 more than the previous year — before your benefits are impacted. The withholding rate is also more generous for beneficiaries who reach FRA in 2026. The SSA will withhold only $1 for every $3 in earnings above this threshold.

Once you reach FRA and beyond, the income limit no longer applies. You can earn any amount without impacting your benefits.

Retirees probably have multiple sources of income, and fortunately, the SSA doesn’t consider all forms of income for its earnings test. Simply put, only earned income is used for the test. That means any wages, salaries or bonuses you earn from your employer. If you’re self-employed, only net income is considered for the earnings test.

Most forms of passive income, including other government benefits, investment earnings, interest, pensions, annuities and capital gains, are not included in the test.

In other words, if you’re primarily relying on passive income and only working part-time or on a casual basis, you’re unlikely to hit the thresholds that trigger benefit withholdings.

If you cross the threshold, it’s important to know that the amount withheld is not lost forever and could actually boost your benefits over the long-term.

The SSA’s earnings test is designed to withhold, not eliminate, benefits in early retirement.

Imagine you turn 62 in 2026 and start claiming benefits. You receive $1,200 a month from Social Security and earn $29,000 a year from part-time work. Because that income exceeds the annual earnings limit by $4,520, the agency withholds $2,260 — half of the amount over the threshold. In practical terms, that’s roughly two months of benefits.

If the same pattern continues and you lose about two months of payments each year until you reach full retirement age at 67, the cumulative reduction would add up to roughly 10 months. At that point, Social Security adjusts your benefit as though you had filed 50 months early rather than 60. The difference is noticeable: filing five years early normally yields about 70% of your full benefit, while filing 50 months early lifts it to roughly 74.2%.

Those additional working years can also push your benefit higher if they replace lower-earning years in your 35-year wage record. The program calculates benefits using an average of your highest years of earnings, so stronger income late in your career can lift that average — and your monthly check — for the rest of retirement.

Nevertheless, losing some of your benefits for a few years could still impact your retirement plan and budget, so make sure you account for this earnings test before you retire, claim benefits or take a new job.

Social Security is the foundation for many Americans’ retirement plans. However, not everyone knows all of the details of how the government program works. There are a few foundational rules everyone should know, but many Americans’ knowledge falls short for even the most basic and important rules governing the program.

If you don’t know the basics of how Social Security works, making an informed decision about when to claim your retirement benefits becomes impossible. Applying for benefits too early (or too late) can have serious long-term ramifications on your retirement goals. Unfortunately, almost half of Americans maintain an incorrect belief about how claiming benefits early will impact their monthly benefit, according to a recent survey from Nationwide.

Image source: Getty Images.

A costly mistaken belief

In the survey, 48% of Americans incorrectly identified the following statement as true: “If I claim benefits early, my benefits will go up automatically when reaching full retirement age.”

Most readers will reach full retirement age at 67 despite becoming eligible to claim Social Security benefits at age 62. But there’s no free lunch when it comes to these benefits. The truth is claiming your benefits before you reach full retirement age will permanently reduce your monthly benefit.

The following table shows just how much less you can expect to receive relative to your full retirement age if you claim early.

Claiming Age

% of Full Benefit

62

70%

63

75%

64

80%

65

86.7%

66

93.3%

67

100%

For Americans with a full retirement age of 67 (born in 1960 or later). Table source: Author. Data source: Social Security Administration.

Why is this misunderstanding so prevalent?

There’s a reason why many people may maintain the mistaken belief that you’ll see a bump in benefits upon reaching full retirement age. That’s because sometimes you actually do. But that’s only due to another commonly misunderstood rule: the Social Security earnings test.

The Social Security earnings test says if you earn over a certain amount while collecting retirement benefits before your full retirement age, the Social Security Administration will withhold some of your monthly benefits. The amount withheld is factored back into your monthly benefit once you reach full retirement age. At that point, the earnings test no longer applies, and the SSA no longer withholds any of your benefit.

In this context, the ultimate size of your check is primarily determined by the age at which you initially apply for Social Security. If you never exceed the earnings test threshold in a given year, you’ll never see a change in the amount you collect besides the annual COLA.

Many Americans are unaware of how the Social Security earnings test works as well. Just 56% of survey respondents correctly answered a question about it in Nationwide’s survey.

The earnings test is the exception to the rule, not the rule itself. It’s important to make that distinction to avoid confusion when making a decision about when to claim benefits.

It pays to delay

All things being equal, it’s typically beneficial to wait to claim your benefits, possibly even beyond your full retirement age.

If you opt to wait to claim your benefits, the Social Security Administration will increase your monthly benefit by 2/3 of a percentage point for each month you delay beyond full retirement age. Those delayed retirement credits max out at age 70, which means someone with a full retirement age of 67 can receive a 24% boost to their monthly checks.

A 2019 study from United Income found the majority of seniors (57%) would be better off by waiting until age 70 to claim their retirement benefits. Just 8% would benefit from claiming before age 65.

There are plenty of good reasons to claim early, though.

For one, if the quality of your life with the supplemental income is significantly higher than without, then it probably makes sense to claim it when you need it. There are steps you can take later if your situation improves to mitigate the impact of claiming early.

Another situation is when you have a reasonable expectation that you’ll pass away earlier than your peers. Social Security is designed to pay out roughly the same amount in lifetime benefits for someone living an average life expectancy regardless of when they claim. But if you suffer from a condition that curbs your life expectancy, it might make sense to claim your benefits earlier.

No matter when you decide to claim, be sure you do it with a complete understanding of how your claiming age impacts your monthly benefit and whether or not you should actually expect your benefit to increase in the future.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

Social Security has been one of the most important social programs in the U.S. for decades. For retirement specifically, it provides vital income to millions of Americans across the country. After years of paying Social Security taxes, beneficiaries reap the rewards with a financial safety net of sorts.

However, these benefits aren’t restricted only to people who worked and paid taxes over the years. For example, Social Security allows spousal benefits to support non-working or low-earning spouses in retirement. For any couple that is nearing or in retirement and putting financial plans in place, here are three things they should know about Social Security spousal benefits.

Image source: Getty Images.

1. How Social Security spousal benefits work

Social Security typically calculates a recipient’s monthly benefits using a formula that factors in their 35 highest-earning years of income. But a spouse can receive Social Security benefits based on their partner’s earning record if they’re at least 62 years old or caring for a child under 16 or with a disability.

Assuming the person claiming spousal benefits is at full retirement age, they’re eligible to receive 50% of their spouse’s primary insurance amount too.

For example, if spouse A’s earnings record gives them a monthly benefit of $2,000 at their full retirement age, spouse B could receive up to $1,000 monthly as well. The exact amount will depend on the age at which spouse B claims benefits.

2. The impact of claiming benefits early or late

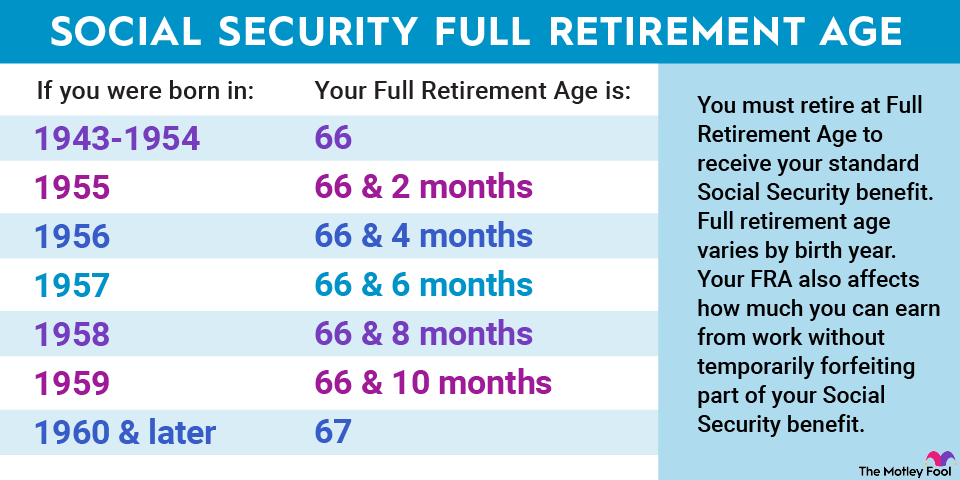

Chart showing Social Security full retirement ages by birth year.

Your full retirement age is one of the most important numbers related to Social Security because it tells you when you’re eligible to receive your primary insurance amount. However, you don’t have to claim benefits at your full retirement age; you can claim them early (which reduces your payout) or delay (which increases your payout).

Claiming Social Security benefits early affects a spouse and their partner receiving spousal benefits in different ways.

Looking first at the person claiming based on their work record, their benefits are reduced by 5/9 of 1% each month before their full retirement age, up to 36 months. Each month after that further reduces benefits by 5/12 of 1%. Here’s an example: Someone with a full retirement age of 67 who claims benefits at 62 will see their monthly benefit reduced 30% from their primary insurance amount.

For the person receiving spousal benefits, benefits are reduced by 25/36 of 1% each month before their full retirement age, up to 36 months, and then they go down 5/12 of 1% each month thereafter. So a person with the same full retirement age (67) claiming spousal benefits at 62 would see their checks reduced 35%.

Although benefits typically increase if you wait beyond your full retirement age, these delayed retirement credits don’t apply to spousal benefits.

3. What happens if a spouse passes away

Social Security spousal and survivors benefits can be closely linked as the latter extends critical financial assistance after a partner has passed away.

If you’re claiming spousal benefits when your partner passes away, Social Security will convert your spousal benefits to survivors benefits. Survivors benefits make you eligible to receive up to 100% of your deceased spouse’s benefit, including any delayed retirement credits they earned prior to their passing. A widow or widower can begin receiving survivors benefits at age 60 (50 if dealing with a disability), but as in the case with spousal benefits, they’ll be reduced if claimed before full retirement age.

You can’t simultaneously receive spousal and survivors benefits, only whichever is higher. Since spousal benefits max out at 50% of the partner’s primary insurance amount, survivors benefits are typically the higher-paying option.

The $21,756 Social Security bonus most retirees completely overlook If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $21,756 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.