Christine Lagarde, president of the European Central Bank (ECB).

Bloomberg | Bloomberg | Getty Images

Goldman Sachs changed its expectations for European Central Bank policy, arguing that recent data, comments from board members, and fewer concerns over the banking sector has allowed for further hawkish action.

The investment bank had lowered its expectations for the ECB’s terminal policy rate to 3.5% in the wake of the collapse of Silicon Valley Bank earlier this year. The event sparked concerns that central banks were moving at too fast a pace and needed to take a break from increasing rates.

However, “banking tensions have receded in recent weeks as the risk of an outright U.S. banking crisis has declined sharply and European bank stock/wholesale funding measures have retraced a large proportion of their large drop in early March,” Goldman Sachs analysts said in a research note Monday.

The bank now believes it will stop hiking (the so-called terminal rate) at 3.75%. The ECB’s benchmark rate has been at 3% since its latest rate decision in March.

In addition, Goldman Sachs said that inflation data is still “very strong,” fueling the argument for more rate hikes. Headline inflation across the euro zone dropped to 6.9% in March, according to preliminary data. In February, the headline rate stood at 8.5%.

Despite this drop, core inflation — which excludes volatile energy, food, alcohol and tobacco prices — rose slightly from the previous month, highlighting the persistence of high prices in the region’s economy.

Olli Rehn, the governor of the Bank of Finland and a member of the ECB’s board, said that “inflation is still by far too high.” Speaking to CNBC last week at the IMF Spring meetings, he added that the central bank must “carry on and act consistently.”

At the March meeting, the ECB did not provide any guidance for upcoming rate decisions, saying these will be data-dependent and happen on a meeting-by-meeting basis.

However, ECB watchers expect a rate increase of 25 or 50 basis points when the Governing Council meets next month.

“We view the choice between 25 basis points and 50 basis points in May as a close call given receding banking risks, growth resilience and ongoing strength in underlying inflation,” Goldman Sachs said.

However, the investment bank is, for the moment, working under the assumption that the ECB will push rates higher by 25 basis points at the May, June and July meeting.

“Reasons for a more gradual speed of tightening from here include that the recent banking stresses are likely to leave some mark on bank lending, we expect some cooling in sequential core inflation in coming months, and the uncertainty around the global outlook has risen,” the analysts said.

Christine Lagarde, president of the European Central Bank, said she has “huge confidence” the US will not allow the country to default on its own debt during an interview on CBS’ “Face the Nation” Sunday.

“I just cannot believe that they would let such a major, major disaster happen,” Lagarde said, adding if a debt default did happen, it would have a “very, very negative impact” both in the US and around the world.

“(The US is) a major leader in economic growth around the world. It cannot let that happen,” Lagarde said.

The US government is in a partisan standoff for negotiations to resolve the debt crisis. If Congress doesn’t address the debt ceiling, the US could potentially face its first-ever default as early as this summer or as late as the fall. Lagarde said she understands politics, but “there is a time when the higher interest of a nation has to prevail.”

The former International Monetary Fund managing director remained optimistic about the recovery of the global economy, despite the Federal Reserve indicating a mild recession later this year.

“If you look at all the forecasts at the moment, it’s all positive,” Lagarde said. “It’s been slightly downgraded, but overall, we have a recovery.”

Governments and central banks have a “narrow path” to navigate, Lagarde said, and they have to “adopt the right policies.”

The IMF, of which Lagarde was the former head, holds a dimmer outlook. It now expects economic growth to slow from 3.4% in 2022 to 2.8% in 2023. Its estimate in January had been for 2.9% growth this year.

“Uncertainty is high, and the balance of risks has shifted firmly to the downside so long as the financial sector remains unsettled,” the organization said in its latest report.

Economists predict banks are getting more cautious about lending money after the collapse of Silicon Valley Bank in March, escalating fears of a credit crisis.

Lagarde said the ECB will have to measure the effects of bank activity in the US and Switzerland. The collapse of Silicon Valley Bank and Signature Bank, as well as Swiss banking giant Credit Suisse being forced to merge with UBS, induced turmoil in the banking sector.

“If (banks) don’t lend too much credit, and if they manage their risk, it might reduce the work that we have to do to reduce inflation,” Lagarde said. “But if they reduced too much credit, then it will weigh on growth excessively.”

Regarding China, Lagarde said she understands the competition between the two countries but hopes they can have a dialogue. She said trade should not be confrontational between China and the US.

“I’m on the same page as Henry Kissinger or Kevin Rudd, the new Australian Ambassador (to the US),” Lagarde said. “Conflict is not unavoidable.”

“Choosing” between the US and China economies would “lead to economic downside the amount of which is uncertain.”

FRANKFURT ― The markets are jittery and inflation still needs taming. Coming together, those two things put the European Central Bank in a real bind.

Fight one fire and it could cause the other to flare. The ECB can keep raising interest rates to try to get inflation under control, but that risks fueling financial market tensions. Conversely, it can give banks some breathing space by slowing its rate-hiking, but that carries the danger of prolonging the region’s economic malaise.

Frankfurt’s official line is that it can do both with no serious consequences. Many economists in the eurozone don’t buy that.

In private, it’s a dilemma that splits the ECB’s decision-makers, and even in public differences of opinion are bubbling to the surface. Here’s what’s at stake:

Why is the ECB raising rates?

The idea is that increasing interest rates subdues inflation because it makes consumers and businesses less likely to borrow ― so that results in reduced spending.

As inflation has started to pick up since last summer, the ECB has raised interest rates at a record pace. They’ve gone from -0.5 to 3 percent as the annual rate of price rises has surged to a eurozone record 10.6 percent inOctober.

The Bank tries to keep inflation at 2 percent so it’s currently way off target.

How this contributed to the crisis

The unpleasant side effect is that with rising borrowing costs (because of higher interest rates), the value of bonds that banks hold usually fall. This gives investors a bad case of the jitters. After the collapse in March of lenders like Silicon Valley Bank and Credit Suisse ― though their problems seemed unconnected ― it was this that prompted concerns they might not be the only institutions with troubles, and fueled contagion fears around the globe.

But Lagarde plowed on regardless

The ECB remained unfazed in the face of emerging banking troubles: It delivered a previously signaled 0.5 percentage-point rate increase in March, less than a week after SVB failed and at a time when Swiss banking giant Credit Suisse was teetering.

Following that decision, ECB President Christine Lagarde stressed that she sees no trade-off between ensuring price stability and financial stability.

In fact, she said the Bank could continue to lift rates while addressing banking troubles with other tools.

The case against

Many economists disagree with Lagarde that the battle for price stability can be pursued without risking financial stability.

The ECB delivered 0.5 percentage-point rate increase in March, less than a week after SVB failed | Patrick T. Fallon/AFP via Getty Images

Claiming so “should be a career-ending statement,” said Stefan Gerlach, chief economist at EFG Bank in Zurich and a former deputy governor of the Central Bank of Ireland. “This is the idea of the ‘separation principle’ of 2008 revisited. That wasn’t a good idea then, and isn’t now either,” he added.

What’s the separation principle?

In 2008, at the start of the financial crisis, as well as in 2011, when the sovereign debt crisis hit, the ECB adhered to the idea that interest rates could be used to ensure price stability at the same time as other measures, such as generous liquidity injections, could ease market tension.

But this just added to the problems and had to be unwound quickly.

This time around, the Portuguese member on the ECB Governing Council, whose country suffered particularly under the consequences of the sovereign debt crisis, is less blasé than Lagarde.

“Our history tells us that we had to backtrack a couple of times already during processes of tightening given threats to financial stability. We cannot risk that this time,” Mario Centeno told POLITICO in an interview.

The case for Lagarde

After the initial fears that troubles could spread across the eurozone, investor nerves have calmed and bank shares started to recover. At the same time, new data showed that underlying inflation pressures kept rising, suggesting that Lagarde and her colleagues were right to stick to their guns ― at least for now.

If that’s the case, March’s interest rate rise ― what Commerzbank economist Jörg Krämer described as “necessary” investment in the central bank’s credibility ― will have paid off.

Market turmoil actually helps

The nervous markets could help the ECB to reach its inflation target without having to raise interest rates as aggressively as previously thought.

Banks tend to slap an additional risk premium on their lending rates which raises the cost of borrowing money for consumers and business. So banks end up doing part of the tightening job for the central bank.

ECB Vice President Luis de Guindos suggested as much in an interview released last month, though he cautioned that it was too early to assess how much impact exactly it may have.

What’s the endgame?

The challenge for the ECB is to strike the right balance. If it doesn’t it risks either the repeat of 2008-style financial troubles or a return to the stagflationary period (low growth on top of high inflation) that roiled the Continent in the 1970s.

If it raises rates too aggressively, bank failures followed by a recession risks forcing the ECB into an interest rate U-turn for the third time, creating massive credibility risks. Conversely, if they don’t hike enough, the central bank may lose a grip on inflation, which is its main mandate.

The only way Lagarde can win is to deliver both price stability and financial stability. In that sense, there is no trade-off ― one without the other just won’t be enough.

Germany’s Chancellor Olaf Scholz said Deutsche Bank is profitable after shares dipped more than 10% during European trading.

Ludovic Marin | Afp | Getty Images

BRUSSELS — European leaders on Friday were keen to stress that the region’s banking sector was stable and sound following Deutsche Bank‘s sudden slide as markets opened for trade.

German Chancellor Olaf Scholz told reporters at an EU summit that Deutsche Bank is a profitable business with no reasons for concern.

The German lender “has modernized, organized the way it works. It is a very profitable bank and there is no reason to be concerned,” he said, according to a translation.

Shares of the German lender traded more than 14% lower at one point Friday after a Thursday evening surge for its credit default swaps — a type of contract to insure against a default. This comes just days after the emergency rescue of Credit Suisse and the collapse of Silicon Valley Bank as well as several measures from authorities stateside to avoid contagion across the financial sector.

French President Emmanuel Macron also told reporters in Brussels that the banking system is solid, while European Central Bank President Christine Lagarde said the euro area is resilient because it has strong capital and solid liquidity positions.

“The euro area banking sector is strong because we have applied the regulatory reforms agreed internationally after the Global Financial Crisis to all of them,” she said, according to EU sources.

The 27 EU leaders were gathered for their usual end of quarter meeting. Geopolitics dominated the first day of talks, but the banking turmoil ended up being the focus for Friday. This became the case, in particular, as the leaders’ conversations developed in parallel to the sharp sell-off in Deutsche Bank shares.

In the run up to the gathering, European officials had expressed their frustration with the lack of regulatory controls in the United States, where the recent banking turmoil first emerged. They have been nervous about potential contagion to their own banking sector, mainly as it’s not been that long since European banks were in the depths of the global financial crisis.

“The banking sector in Europe is much stronger, because we have been through the financial crisis,” Estonia Prime Minister Kaja Kallas told CNBC Thursday.

In the wake of the 2008 shock, European banks underwent massive restructuring and had to significantly shore up their balance sheets.

But the EU is still somewhat vulnerable to shocks given that it has a monetary union within the euro area, where 20 nations share the euro, but lacks a fiscal union. Fiscal policy is still the responsibility of the individual governments rather than one single institution.

“We need to progress on completing the banking union; further work is also necessary to create a truly European capital markets,” Lagarde also told the 27 EU heads of state on Friday.

The banking union is a set of laws introduced in 2014 to make European banks more robust. The debate has been politically sensitive, but the reality that high interest rates are here to stay has made it even more pressing.

The idea for a true capital markets union is to make lending easier across the region, where often national bureaucracy can differ from country to country.

In a statement, it pledged to “stay the course in raising interest rates significantly at a steady pace” and, in unusually firm language, said it intended to hike by another 50 basis points in March.

Inflation in the euro zone eased in the last two months of 2022 but the economic indicator is still well-above the 2% mandate of the European Central Bank.

Jeff Greenberg | Universal Images Group | Getty Images

Inflation in the euro zone dropped for a third consecutive month in January on the back of a significant fall in energy costs.

Headline inflation in the euro zone came in at 8.5% in January, according to preliminary data released Wednesday. In December, the rate was recorded at 9.2%.

Energy remained the biggest cost driver in January, but once more softened from previous levels. Energy charges fell to an estimated 17.2% in January, down from 25.5% in December. However, food costs rose slightly from 13.8% in December to 14.1% in January.

The 20-member region has gone through substantial price increases in 2022, after Russia’s invasion of Ukraine pushed up energy and food costs across the bloc. However, the latest data provides further evidence that inflation has started to ease.

Core inflation, which strips out energy and food costs, stood at 5.2% in December — in line with the previous month.

“The key point is that core inflation was unchanged at a record 5.2% so the ECB will remain very hawkish,” Jack Allen-Reynolds, senior Europe economist at Capital Economics, said via email.

The performance of Europe’s main index over the last 12 months.

“The apparent decline in euro-zone headline inflation in January, from 9.2% in December to 8.5%, came as a big surprise. But we wouldn’t be shocked if it was revised up significantly when the final euro-zone data are released on 23rd February,” he added, citing delays in receiving official data from Germany.

“The upshot is that the larger-than-expected drop in headline inflation won’t deter the ECB from raising interest rates by 50 basis points tomorrow,” Allen-Reynolds said.

In a note to clients last week, Morgan Stanley had said that “a 50 basis point hike in February seems like a done deal, with the Council discussion to centre on the size of rate hikes in March and beyond.”

Market participants will be looking for clues on the central bank’s next steps. The main ECB rate is currently at 2%, but market expectations suggest an increase to 3.5% by the end of the first six months of the year, according to Reuters.

“Investors will be looking ahead to whether Christine Lagarde doubles down on previous signals for another half-percent hike in March and what words she uses to describe any future additional tightening,” Tom Hopkins, portfolio manager at BRI Wealth Management, said Wednesday via email.

Unemployment in the euro zone seemed steady at 6.6% in December . This is in line with the previous two monthly readings and also reduces fears of a significant recession in the euro zone.

Data released Tuesday showed a better-than-expected growth activity in the euro zone at the end of 2022 — despite economic contractions in Germany and Italy, the euro zone grew 0.1% in the fourth quarter of last year.

[The stream is slated to start at 8:45 EST. Please refresh the page if you do not see a player above at that time.]

European Central Bank President Christine Lagarde is due to give a press conference following the bank’s latest monetary policy decision.

The ECB, the central bank of the 19 nations that share the euro currency, opted for a smaller rate hike this time around, taking its key rate from 1.5% to 2%.

It also said that from the beginning of March 2023 it would begin to reduce its balance sheet by 15 billion euros ($16 billion) per month on average until the end of the second quarter of 2023.

This is an opinion editorial by Federico Rivi, an independent journalist and author of the Bitcoin Train newsletter.

We are raising interest rates “because we are fighting inflation. Inflation has come out of practically nothing.” So said European Central Bank President Christine Lagarde, host of the Irish talk show Late Late Show on Friday, October 28, 2022. Words apparently contradicting a statement that came shortly afterwards in the same interview. Inflation, she said, is caused “by Russian President Vladimir Putin’s war in Ukraine. […] This energy crisis is causing massive inflation that we have to defeat.”

The Rate Hike

The day before the interview the European Central Bank had raised interest rates by a further 75 basis points, bringing the total growth applied in the last three meetings to 2%: the highest level since 2009. In all likelihood it will not end there, as the Governing Council plans to “raise rates further to ensure a timely return of inflation to its medium-term objective of 2 per cent.”

According to the latest data, the rise in prices in the euro area has actually reached levels never seen in the last 20 years: +9.9% in September compared to the same month last year. Countries like Latvia, Lithuania and Estonia are seeing price increases of 22%, 22.5% and 24.1% respectively.

In the widespread consensus on the meaning of the term inflation, however, there is a major inconsistency. A distortion of the real concept that leads leaders, experts – and consequently the media – to attribute different causes to the word, depending on the convenience of the moment. When the cause, in reality, is always and only one.

Inflation And Price Increases Are Different

For many, inflation is now synonymous with rising prices. This is not just a widespread belief but a meaning that has also been adopted by economics textbooks and the official language. According to Cambridge Dictionary inflation is “a general, continuous increase in prices.”

But is this really the case? Bitcoin teaches one thing: Don’t trust, verify. And by verifying, a problem emerges: the reversal of cause and effect.

Inflation is treated as the effect of a certain event: an energy crisis, a chip shortage, a drought can all lead to higher prices for goods and services in certain sectors. But in reality inflation, in its original meaning, does not mean the rise in prices, it indicates its cause.

The clue comes directly from etymology: inflation comes from the Latin word inflatio, itself a derivative of inflare, i.e. toinflate. Think about inflating a balloon: the act of inflare (inflating) is when air is blown from the mouth into the balloon: the cause. The immediate consequence is the expansion of the volume of the balloon that is taking in air: the effect.

Pumping new air into the balloon is the action that leads to its expansion. The same reasoning applies to money: the very act of printing money is inflation and its consequence is an increase in prices. This reversal of cause and effect was already referred to in the late 1950s as semantic confusion by one of the most prominent economists of the Austrian school, Ludwig von Mises:

“There is nowadays a very reprehensible, even dangerous, semantic confusion that makes it extremely difficult for the non-expert to grasp the true state of affairs. Inflation, as this term was always used everywhere and especially in this country, means increasing the quantity of money and bank notes in circulation and the quantity of bank deposits subject to check. But people today use the term “inflation” to refer to the phenomenon that is an inevitable consequence of inflation, that is the tendency of all prices and wage rates to rise. The result of this deplorable confusion is that there is no term left to signify the cause of this rise in prices and wages.”

If, therefore, there can be many causes of price increases, there cannot be as many causes of inflation because it is itself an origin of price increases. It would be much more adequate and intellectually honest to say that the decrease in purchasing power can result from several factors including inflation, i.e. the printing of money.

Money Flooding

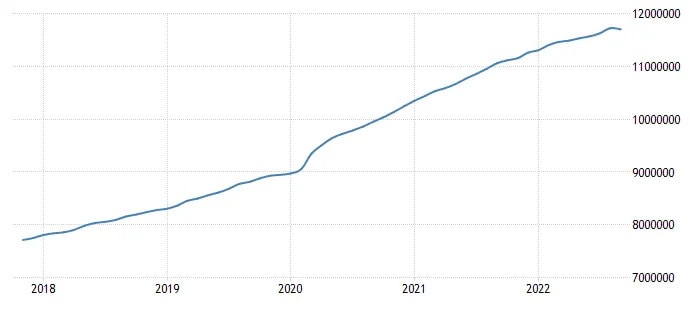

So how has the European Central Bank behaved in terms of monetary issuance in recent years? The most effective figure to understand this is the ECB balance sheet, which shows the countervalue of assets held: those assets for which the Eurotower does not pay but acquires by creating new currency. As of October 2022, the ECB held almost EUR 9 trillion. Before the pandemic, at the beginning of 2019, it had around 4,75 trillion. Frankfurt has almost doubled its money supply in three and a half years.

If we measure the amount of euros circulating in the form of banknotes and deposits – the figure defined as M1 – the number is slightly more reassuring, but not much: at the beginning of 2019 there were almost EUR 8.5 trillion in circulation, today there are 11.7 trillion. A growth of 37.6%.

Are we really sure, then, that this price growth – or as it is wrongly called by everyone, inflation – comes from nowhere? Or that it is just a consequence of the war in Ukraine? Given the amount of money supply injected into the market in the last three years, we should count ourselves lucky that the average price growth of goods and services is still stuck at 10%, due to the restrictions of the pandemic and the subsequent economic crisis we are entering.

What does Bitcoin have to do with all this? Bitcoin has everything to do with it because it was born as an alternative to the economic catastrophes for which central banks continue to make themselves responsible. An alternative to the bubbles of unsustainable growth alternating with ruinous crises caused by the market manipulation of the interventionist utopia. Bitcoin cannot tell the world that “inflation came from nowhere,” because its code is public and everyone can check its monetary policy. A policy that does not change and cannot be manipulated. It is fixed and will remain so. 2.1 quadrillion satoshis. Not one more.

This is a guest post by Federico Rivi. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Christine Lagarde, president of the European Central Bank speaks at an event. The central bank is due to meet in mid-December for more monetary policy decisions.

Bloomberg | Bloomberg | Getty Images

The European Central Bank could be about to answer a lingering question in the coming weeks that could have major repercussions for financial markets.

At its December meeting, the ECB is set to discuss and reveal more concrete details on how it will unwind 8.8 trillion euros ($9.21 trillion) from its balance sheet — in a process known as quantitative tightening.

For years, the central bank has been ultra loose with its monetary policy, buying sovereign debt across Europe to keep borrowing costs low for governments and, subsequently, for individuals to help stimulate growth.

However, with inflation at record highs and a number of rate hikes under its belt, markets are now awaiting details on how and when the ECB will sell these bonds.

“The biggest question in December is what they’ll do regarding QT,” Marchel Alexandrovich, European economist at Saltmarsh Economics, told CNBC over the phone.

Back in October, ECB President Christine Lagarde said the discussions over bond sales will consider three main factors: the inflation outlook, the measures taken so far, and the transmission lag — given that it takes a while for any monetary decision to have an impact on the economy.

Speaking Monday, Lagarde confirmed the timeline. “In December, we will also lay out the key principles for reducing the bond holdings in our asset purchase program portfolio,” she told European lawmakers.

ECB officials have suggested that the process will be “gradual” and “predictable” — meaning it’s not likely to be meeting dependent.

At the moment, the central bank is applying a meeting-by-meeting approach to interest rate decisions, arguing there is a high degree of uncertainty preventing it from guiding the markets with more detail in the medium term.

“It is appropriate that the balance sheet is normalized over time in a measured and predictable way,” Lagarde said Monday.

As such, economists do not expect every detail to be outlined in December.

“In December, the ECB will lay out some general principals about how it intends to conduct QT but not yet specify the precise amounts and timings of the balance sheet run-off,” Franziska Palmas, senior Europe economist at Capital Economics, said via email.

She added that the upcoming changes to the balance sheet will likely be applied only to the APP (Asset Purchase Program) holdings and not to PEPP (Pandemic Emergency Purchase Program).

APP started in mid-2014 to deal with persistently low inflation levels. It was frozen between January and October 2019 and then lasted until July 2022. On the other hand, PEPP was a more flexible bond purchase program introduced during the coronavirus pandemic.

As part of the broader stimulus actions, the ECB has been reinvesting profits it made during these asset purchases. Instead of starting to unwind its balance sheet by selling the actual bonds, some expect the ECB to stop these reinvestments.

“The ECB will shrink APP holdings only by ceasing to reinvest the proceeds of maturing APP assets, not by actively selling them. The pace of QT may be particularly slow initially, with the ECB still reinvesting the majority of the proceeds from maturing assets,” Palmas said.

Economists at Nomura also expect the ECB to slow down these reinvestments as a first step in reducing its balance sheet.

“We believe the ECB will allow only 1/3 of APP portfolio redemptions to be rolled off, with the remainder reinvested,” they said in a research note after the last ECB meeting. This is seen starting in the second quarter of 2023, according to the same note.

Frederik Ducrozet, the head of macroeconomic research at Pictet Wealth Management and an avid ECB watcher, said the bank “will probably introduce so-called caps on monthly reinvestments under the APP programme, up to which the ECB will stop reinvesting the proceeds of maturating securities.”

He added that this would likely start in March.

The ECB’s cumulative net purchases of government debt as of October 2022 stood at 2.74 trillion euros.

Euro zone inflation rose above the 10% level in the month of October, highlighting the severity of the cost-of-living crisis in the region and adding more pressure on the European Central Bank.

Preliminary data on Monday from Europe’s statistics office showed headline inflation came in at an annual 10.7% last month. This represents the highest ever monthly reading since the euro zone’s formation. The 19-member bloc has faced higher prices, particularly on energy and food, for the past 12 months. But the increases have been accentuated by Russia’s invasion of Ukraine in late February.

This proved to be the case once again, with energy costs expected to have had the highest annual rise in October, at 41.9% from 40.7% in September. Food, alcohol and tobacco prices also rose in the same period, jumping 13.1% from 11.8% in the previous month.

Monday’s data comes after individual countries reported flash estimates last week. In Italy, headline inflation came in above analysts’ expectations at 12.8% year-on-year. Germany also said inflation jumped to 11.6% and in France the number reached 7.1%. The different values reflect measures taken by national governments, as well as the level of dependency that there nations have, or had, on Russian hydrocarbons.

There are, however, euro nations where inflation rose by more than 20%. This includes Estonia, Latvia and Lithuania.

The European Central Bank — whose primary target is to control inflation — on Thursday confirmed further rate hikes in the coming months in an attempt to bring prices down. It said in a statement that it had made “substantial progress” in normalizing rates in the region, but it “expects to raise interest rates further, to ensure the timely return of inflation to its 2% medium-term inflation target.”

The ECB decided to raise rates by 75 basis points for a second consecutive time last week.

Speaking at a subsequent press conference, ECB President Christine Lagarde said the likelihood of a recession in the euro zone had intensified.

Growth figures released Monday showed a GDP (gross domestic product) figure of 0.2% for the euro area in October. This is after the region grew at a rate of 0.8% in the second quarter. Only Belgium, Latvia and Austria registered GDP rates below zero.

So far, the 19-member bloc has dodged a recession but an economic slowdown is evident. Several economists predict there will be a contraction in GDP during the current quarter.

The euro traded below parity against the U.S. dollar in early European trading hours Monday and ahead of the new data releases, and barely moved after the new figures. The euro has been weaker against the greenback and that’s also something the ECB has been concerned about with concerns that this will push up inflation in the euro zone even further.

Christine Lagarde, president of the European Central Bank, is expected to announce another 75 basis points hike.

Bloomberg | Bloomberg | Getty Images

While the European Central Bank is largely expected to announce another rate hike Thursday, market players are seemingly more concentrated on two other policy tools as the region edges toward a recession.

The central bank has been contemplating inflation being at record highs but an economy that is slowing, with many economists predicting a recession before the end of the year. If the ECB takes a very aggressive stance in increasing rates to deal with inflation, there are risks that it tips the economy into further trouble.

Amid this context, the ECB is widely seen raising rates by 75 basis points later this week. This would be the second consecutive jumbo hike and the third increase this year.

“The ECB will likely raise its three policy rates by 75 basis points and suggest that it will go further at its next few policy meetings without providing a clear guidance on the size and number of steps to come,” Holger Schmieding, chief economist at Berenberg, said in a note Tuesday.

Given the inflationary pressures — the September inflation rate came in at 10% — analysts are pricing in at least another 50 basis point hike in December. The bank’s main rate is currently at 0.75%.

“A growing consensus seems to be in favour of having the deposit rate at 2% by the end of the year, implying a 50 basis point hike in December, with a reassessment of the economic and inflation outlook in early 2023,” Frederik Ducrozet, head of macroeconomic research at Pictet Wealth Management, said in a note Friday.

Rates aside, there are two questions on the minds of market players that need answering: When will the ECB start unwinding its balance sheet, in a process known as quantitative tightening, and what will happen to the lending conditions for banks in the near future. The ECB has undertaken years of quantitative easing, where it buys assets like government bonds to simulate demand, following the euro crisis of 2011 and the Covid-19 outbreak in 2020.

“When it comes to QT, boring is beautiful,” Ducrozet said, adding that he expects the process to start in the second quarter of 2023. QT is expected “to be predictable, gradual, and passive, starting with the end of reinvestments under the Asset Purchase Programme (APP) but not actively selling bonds any time soon,” he said.

Camille De Courcel, head of European rates strategy at BNP Paribas, said in a note Monday that the central bank might wait until the December meeting to provide details on QT but that it is likely to start reducing its balance sheet by about 28 billion euros on average per month when it does happen.

But perhaps the biggest uncertainty at this stage is whether lending conditions will change for European banks.

“We think Thursday [the ECB] will unveil a decision on the TLTRO, either its remuneration, or its cost. We think the new measure will only come into effect, in December,” De Courcel said.

The targeted longer-term refinancing operations, or TLTROs, is a tool that provides European banks with attractive borrowing conditions — hopefully giving these institutions more incentives to lend to the real economy.

Because the ECB has been increasing rates faster than the central bank initially expected, European lenders are benefiting from the attractive loan rates via TLTROs while also making more money from the higher interest rates.

“The optics are bad against the backdrop of a historical shock to households’ income, and political pressure cannot be ignored,” Ducrozet said.

The euro traded marginally higher against the U.S. dollar on Wednesday at $0.997. The weakness of the common currency has been a concern for the central bank though it repeatedly states that it does not target the exchange rate.