[ad_1]

Courtesy of Redfin.

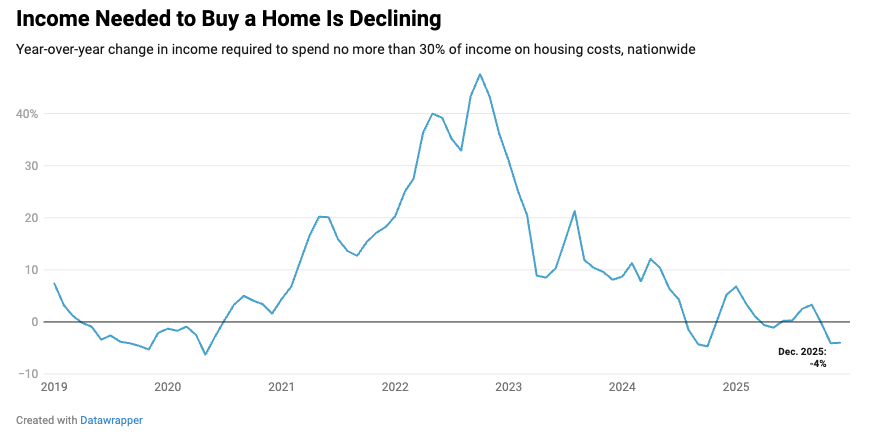

After five years of worsening, housing affordability has finally started to improve, according to a new Redfin study.

The amount Americans needed to earn declined 4% year over year in December, from $115,870 to $111,252, marking the second month in a row of declines after rising in nearly every month for five years in a row. Income needed to buy a home peaked at $122,000 in June.

Redfin attributed the improvement to lower mortgage rates and slowing home-price growth. The median home sale price in December was $426,747, up slightly from December 2024, but mortgage rates have fallen from 7% last year to about 6.1% now. Those factors brought the median monthly mortgage payment down from $2,800 to $2,675.

“The housing affordability crisis is showing signs of easing as costs come down slightly but meaningfully, opening the door for more Americans to make the jump to homeownership,” said Chen Zhao, Redfin’s head of economics research. “While housing remains historically expensive, the trajectory is finally starting to reverse, with the door to buying a home opening a bit wider rather than closing tighter. But while affordability is improving, Americans are contending with other obstacles on the road to buying a home, like nerves about layoffs and economic uncertainty.”

Redfin considers a home affordable if a buyer taking out a mortgage spends no more than 30% of their income on monthly housing payments. Redfin based its analysis on median home sale prices, prevailing mortgage rates and property tax payments.

Courtesy of Redfin.

While affordability is improving, the typical U.S. household does not earn enough to afford the median-priced home. The typical American household earns just $86,185, about $25,000 less than needed, according to the report.

On a local level, affordability is improving in 37 of the 50 largest U.S. cities, led by Dallas, where required earnings fell 7.4%, and followed by Sacramento, California, and Jacksonville, Florida, where the amount needed was down 6.8% and 5.9%, respectively.

On the flip side, the amount homebuyers needed to earn actually increased in some cities, led by Detroit (up 3.6%) and followed by Chicago (3.5%) and St. Louis (3%)

The typical household could actually afford to buy a median-priced home in only 12 metros, led by Pittsburgh, where buyers needed to earn $66,168, and the typical household earned $82,188, followed by St. Louis, where $73,984 is needed, and the typical household earned $87,471, and Cleveland, where $66,725 was needed, and the typical income was $76,912.

[ad_2]

John Yellig

Source link