Exxon Mobil Corp. said in a filing late Wednesday that its third-quarter profit is likely to get a bump of around $1 billion from rising crude prices.

Exxon XOM, -3.74%

estimated between $900 million and $1.3 billion more than second-quarter profit due to crude-price changes, and between $200 million and $400 million in gas-price changes.

The energy giant is expecting $600 million to $400 million less as a result of thinner margins for its chemicals, however.

Exxon shares dropped 0.5% in the extended session after ending the regular trading day down 3.7%. The stock late last month ended at a record, according to data going back to November 1972.

Exxon is slated to report third-quarter earnings in early November, with FactSet consensus calling for adjusted earnings of $2.35 a share on sales of $85.6 billion. That would compare with adjusted EPS of $4.45 on sales of $112 billion in the third quarter of 2022.

So far this year, Exxon shares have gained nearly 2%, compared to an advance of around 10% for the S&P 500 index SPX.

Two things investors can be sure about: Nothing lasts forever and the stock market always overreacts. The spiking of yields on long-term U.S. Treasury securities has been breathtaking, and it has led to remarkable declines for some sectors and possible bargains for contrarian investors who can commit for the long term.

First we will show how the sectors of the S&P 500

have performed. Then we will look at price-to-earnings valuations for the sectors and compare them to long-term averages. Then we will screen the entire index for companies trading below their long-term forward P/E valuation averages and narrow the list to companies most favored by analysts.

Here are total returns, with dividends reinvested, for the 11 sectors of the S&P 500, with broad indexes below. The sectors are sorted by ascending total returns this year through Monday.

Returns for 2022 are also included, along with those since the end of 2021. Last year’s weakest sector, communications services, has been this year’s strongest performer. This sector includes Alphabet Inc. GOOGL

and Meta Platforms Inc. META,

which have returned 52% and 155% this year, respectively, but are still down since the end of 2021. To the right are returns for the past week and month through Monday.

On Monday, the S&P 500 Utilities sector had its worst one-day performance since 2020, with a 4.7% decline. Investors were reacting to the jump in long-term interest rates.

Here is a link to the U.S. Treasury Department’s summary of the daily yield curve across maturities for Treasury securities.

The yield on 10-year U.S. Treasury notes

jumped 10 basis points in only one day to 4.69% on Monday. A month earlier the 10-year yield was only 4.27%. Also on Monday, the yield on 20-year Treasury bonds

rose to 5.00% from 4.92% on Friday. It was up from 4.56% a month earlier.

The Treasury yield curve is still inverted, with 3-month T-bills

yielding 5.62% on Monday, but that was up only slightly from a month earlier. An inverted yield curve has traditionally signaled that bond investors expect a recession within a year and a lowering of interest rates by the Federal Reserve. Demand for bonds pushes their prices down. But the reverse has happened over recent days, with the selling of longer-term Treasury securities pushing yields up rapidly.

Another way to illustrate the phenomenon is to look at how the Federal Reserve has shifted the U.S. money supply. Odeon Capital analyst Dick Bove wrote in a note to clients on Friday that “the Federal Reserve has not deviated from its policy to defeat inflation by tightening monetary policy,” as it has shrunk its balance sheet (mostly Treasury securities) to $8.1 trillion from $9 trillion in March 2022. He added: “The M2 money supply was $21.8 trillion in March 2022; today it is $20.8 trillion. You cannot get tighter than these numbers indicate.”

Then on Tuesday, Bove illustrated the Fed’s tightening and the movement of the 10-year yield with two charts:

Odeon Capital Group, Bloomberg

Bove said he believes the bond market has gotten it wrong, with the inverted yield curve reflecting expectations of rate cuts next year. If he is correct, investors can expect longer-term yields to keep shooting up and a normalization of the yield curve.

This has set up a brutal environment for utility stocks, which are typically desired by investors who are seeking dividend income. In a market in which you can receive a yield of 5.5% with little risk over the short term, and in which you can lock in a long-term yield of about 5%, why take a risk in the stock market? And if you believe that the core inflation rate of 3.7% makes a 5% yield seem paltry, keep in mind that not all investors think the same way. Many worry less about the inflation rate because large components of official inflation calculations, such as home prices and car prices, don’t affect everyone every year.

We cannot know when this current selloff of longer-term bonds will end, or how much of an effect it will have on the stock market. But sharp declines in the stock market can set up attractive price points for investors looking to go in for the long haul.

Screening for lower valuations and high ratings

A combination of rising earnings estimates and price declines could shed light on potential buying opportunities, based on forward price-to-earnings ratios.

Let’s look at the sectors again, in the same order, this time to show their forward P/E ratios, based on weighted rolling 12-month consensus estimates for earnings per share among analysts polled by FactSet:

Sector or index

Current P/E to 5-year average

Current P/E to 10-year average

Current P/E to 15-year average

Forward P/E

5-year average P/E

10-year average P/E

15-year average P/E

Utilities

82%

86%

95%

14.99

18.30

17.40

15.82

Real Estate

76%

80%

81%

15.19

19.86

18.89

18.72

Consumer Staples

93%

96%

105%

18.61

19.92

19.30

17.64

Healthcare

103%

104%

115%

16.99

16.46

16.34

14.72

Financials

88%

92%

97%

12.90

14.65

14.08

13.26

Materials

100%

103%

111%

16.91

16.98

16.42

15.27

Industrials

88%

96%

105%

17.38

19.84

18.16

16.56

Energy

106%

63%

73%

11.78

11.17

18.80

16.23

Consumer Discretionary

79%

95%

109%

24.09

30.41

25.39

22.10

Information Technology

109%

130%

146%

24.20

22.17

18.55

16.54

Communication Services

86%

86%

94%

16.41

19.09

19.00

17.43

S&P 500

94%

101%

112%

17.94

19.01

17.76

16.04

DJ Industrial Average

93%

98%

107%

16.25

17.49

16.54

15.17

Nasdaq Composite Index

92%

102%

102%

24.62

26.71

24.18

24.18

Nasdaq-100 Index

97%

110%

126%

24.40

25.23

22.14

19.43

There is a limit to how many columns we can show in the table. The S&P 500’s forward P/E ratio is now 17.94, compared with 16.79 at the end of 2022 and 21.53 at the end of 2021. The benchmark index’s P/E is above its 10- and 15-year average levels but below the five-year average.

If we compare the current sector P/E numbers to 5-, 10- and 15-year averages, we can see that the current levels are below all three averages for four sectors: utilities, real estate, financials and communications services. The first three face obvious difficulties as they adjust to the rising-rate environment, while the real-estate sector reels from continuing low usage rates for office buildings, from the change in behavior brought about by the COVID-19 pandemic.

Your own opinions, along with the pricing for some sectors, might drive some investment choices.

A broader screen of the S&P 500 might point to companies for you to research further.

We narrowed the S&P 500 as follows:

Current forward P/E below 5-, 10- and 15-year average valuations. For stocks with negative earnings-per-share estimates for the next 12 months, there is no forward P/E ratio so they were excluded. For stocks listed for less than 15 years, we required at least a 5-year average P/E for comparison. This brought the list down to 138 companies.

“Buy” or equivalent ratings from at least two-thirds of analysts: 41 companies.

Here are the 20 companies that passed the screen, for which analysts’ price targets imply the highest upside potential over the next 12 months.

There is too much data for one table, so first we will show the P/E information:

U.S. stocks have risen sharply in 2023, with a small number of technology companies driving an ever-increasing share of the stock-market gains.

While the 11.7% year-to-date gains for the large-cap benchmark S&P 500 index SPX

show 2023 has been a “good year” for stocks, that hardly tells the whole story, said Jonathan Krinsky, the technical strategist at BTIG.

The U.S. stock market has seen the median return for shares in the S&P 500 index rise merely 1.1% in 2023, which is “a different planet” compared with their median gain of 16.2% in 2014, when the benchmark index recorded a yearly advance of 11.4%, Krinsky said in a Sunday note (see chart below).

SOURCE: BTIG ANALYSIS, BLOOMBERG

The Russell 3000 RUA

— a barometer that represents approximately 98% of the American equities — had a median return of negative 2.2% this year, but the index has gained 11.3% year to date, wrote Krinsky, citing BTIG and Bloomberg data. In 2014, the median return for the Russell 3000 was 6.9%, and it recorded a yearly gain of 10.4%.

Meanwhile, the median year-to-date return for stocks in the S&P 1500, which includes all shares in the S&P 500, S&P 400 MID

and S&P 600 SML

and covers approximately 90% of U.S. stocks, rose a merely 0.1% versus the index’s 11.2% advance this year, said Krinsky. The S&P 1500 recorded a median return of 8.8% in 2014 and was up 10.9%.

So far in 2023, investors have struggled to brush off a rise in Treasury yields primarily triggered by the Federal Reserve bumping up interest rates and the risk of recession, with hope that the stock-market rally hasn’t run out of steam yet.

However, the S&P 500 and the Nasdaq Composite COMP

Friday locked in their worst month of the year, down 4.9% and 5.8%, respectively, according to FactSet data.

Treasury yields continued to rise on Monday with the yield on the 2-year BX:TMUBMUSD02Y

up 6.4 basis points to 5.110%, while the yield on the 10-year Treasury BX:TMUBMUSD10Y

jumped 11 basis points to 4.682%. The 10-year rate ended at its highest level since Oct. 12, 2007, according to Dow Jones Market Data.

As a result, investors were hoping October and the last quarter of 2023 could bring some relief to the scorching summer selloff they had to endure in markets. Historically, the fourth quarter has been the best quarter for the U.S. stock market, with the S&P 500 index up nearly 80% dating back to 1950 and gaining more than 4% on average, according to data compiled by Carson Group.

“It seems to us that a rally [in the fourth quarter] is the consensus view based on the fact that seasonals tend to work that way,” Krinsky said. “While October is a strong month on ‘average’, it has been down ten of the last 30 years, with eight of those years losing 1.77% or more.”

In other words, when October is good it tends to be really good, but when it’s bad it tends to be quite bad, Krinsky added.

U.S. stocks finished mostly higher on Monday with the Dow Jones Industrial Average DJIA

down 0.2%, while the S&P 500 ended flat and the Nasdaq edged up 0.7%, according to FactSet data.

Stelco and U.S. Steel didn’t immediately respond to a request for comment

A bid, if it happened, would be surprising. U.S. Steel is much larger than Stelco. The Canadian steel maker shipped about 2.6 million tons of steel in 2022, while U.S. Steel shipped about 15 million. Stelco’s enterprise value, including stock and debt, is about $1 billion. U.S. Steel’s is about $9 billion.

“That makes it an upstart and we suppose the key to handicapping its chances is knowing who it is partnered with. If that partner is an investor with deep pockets, we won’t be so quick to dismiss Stelco’s chances,” wrote Gordon Haskett analyst Don Bilson in a report Friday. “For now, however, we’re going to view it as a long shot.”

Stelco likely would need a partner to complete a merger.

The possible bid is surprising in another way, too. Stelco was actually once owned by U.S. Steel. The American firm bought it 2007 after Stelco filed for bankruptcy protection. Stelco filed for bankruptcy again in 2014 and was purchased by Bedrock Industries in 2017 before listing as a public company again later that year.

“Recent history has not been kind to companies that have tried to recombine with a former partner,” added Bilson, citing

(PARA) shares are down about 70% since the merger plan was announced in August 2019.

That bids are emerging for U.S. Steel isn’t surprising, though. On Aug. 13, the company said it was exploring strategic options, which could include a sale of the company. Since then, steel maker

(CLF) and steel service center Esmark have announced bids.

Esmark processes and distributes steel, rather than producing it. The company didn’t announce financing with its bid and has dropped out of the process.

(MT) was reportedly considering a bid. ArcelorMittal didn’t comment on a potential bid, which also would have been a little odd. Arcelor sold its U.S. operations to Cliffs in 2020.

U.S. Steel stock was about $23 a share before its announcement and bids started to emerge. The Cliffs bid, which is a mix of cash and stock, and is the only current bid with hard numbers attached to it, is currently worth $32.21 a share.

U.S. Steel stock was at $31.80 on Friday, up 1.8%. The

Investors in index funds have been well rewarded by a high concentration in the largest technology companies over the past decade. But there are also continuing warnings about the risk of such heavy concentrations, even in index funds that track the S&P 500. Solutions are offered to limit this risk, but if you expect Big Tech to continue to drive the broad market returns over the coming years, why not make an even more focused bet?

Comparisons of three index-fund approaches highlight how successful concentration in the “Magnificent Seven” has been.

GOOG, -0.32%,

Tesla Inc. TSLA, +9.37%

and Meta Platforms Inc. META, +1.67%.

We have listed them in the order of their concentration within the Invesco S&P 500 ETF Trust SPY,

which tracks the S&P 500 SPX.

The U.S. benchmark index is weighted by market capitalization, as is the Nasdaq Composite Index COMP

and the Russell indexes.

SPY is 27.6% concentrated in the Magnificent Seven. One way to play the same group of 500 stocks but eliminate concentration risk is to take an equal-weighted approach to the index, which has worked well for certain long periods. But here, we’re focusing on how well the concentrated strategy has worked.

Let’s take a look at the group’s concentration in three popular index approaches, then look at long-term performance and consider what happened in 2022 as rising interest rates helped crush the tech sector.

Here are the portfolio weightings for the Magnificent Seven in SPY, along with those of the Invesco QQQ Trust QQQ,

which tracks the Nasdaq-100 Index NDX

and the Invesco S&P 500 Top 50 ETF XLG

:

The same group of seven companies (eight stocks with two common share classes for Alphabet) is at the top of each exchange-traded fund’s portfolio, although the top seven for QQQ aren’t in the same order as those for SPY and XLG. QQQ’s weighting was changed recently as the underlying Nasdaq-100 underwent a “special rebalancing” last month.

Here’s a five-year chart comparing the performance of the three approaches. All returns in this article include reinvested dividends.

FactSet

QQQ has been the clear winner for five years, but it is also worth noting how well XLG has performed when compared with SPY. This “top 50” approach to the S&P 500 incorporates many stocks that aren’t listed on the Nasdaq and therefore cannot be included in QQQ, which itself is made up of the largest 100 nonfinancial companies in the full Nasdaq Composite Index COMP, +0.45%.

Examples of stocks held by XLG that aren’t held by QQQ include such non-tech stalwarts as Berkshire Hathaway Inc. BRK.B, +0.77%,

Johnson & Johnson JNJ, +0.79%,

Procter & Gamble Co. PG, +0.94%,

Home Depot Inc. HD, -0.12%

and Nike Inc. NKE, -0.42%.

Now let’s go deeper into long-term performance. First, here are the total returns for various time periods:

There is no 20-year return for XLG because this ETF was established in 2005.

For five years and longer, QQQ has been the runaway leader, but for 5, 10 and 15 years, XLG has also beaten SPY handily, with broader industry exposure.

Something else to consider is that during 2022, when SPY was down 18.2%, XLG fell 24.3% and QQQ dropped 32.6%.

For disciplined long-term investors, the tech pain of 2022 may not seem to have been a small price to pay for outperformance. And it may have been easier to take the pounding when holding SPY or even XLG that year.

Here’s a look at the average annual returns for the three ETFs:

So the question remains — do you believe that the largest technology companies will continue to lead the stock market for the next decade at least? If so, a more concentrated index approach may be for you, provided you can withstand the urge to sell into a declining market, such as the one we experienced last year.

Here is something else to keep in mind. In a note to clients on Monday, Doug Peta, the chief U.S. investment strategist at BCA, made a fascinating point: “The only novel development is that all the heaviest hitters now hail from Tech and Tech-adjacent sectors and are therefore more prone to move together than they were at the end of 2004, when the seven largest stocks came from six different sectors. “

Nothing lasts forever. Peta continued by suggesting that investors who are tired of big tech taking all the glory “need only wait.”

“[I]f history is any guide, their time at the top of the capitalization scale will be short,” he wrote.

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

U.S. banks and regional banks fell across the board on Tuesday, after S&P Global Ratings downgraded five smaller players after a review of risk related to funding, liquidity and asset quality with a focus on office commercial real estate.

Adding to the gloom, Republic First Bancorp. Inc.’s stock FRBK, -41.90%

tanked by 39%, after Nasdaq told the company that its stock would be delisted on Wednesday, after it failed to file its annual report in time.

S&P’s move comes just days after Fitch Ratings analyst Christopher Wolfe reduced his operating environment score for U.S. banks to aa- from aa due to the unknown path of interest rate hikes and regulatory changes facing the sector.

And Moody’s Investors Service just two weeks ago upset investors when it downgraded some lenders and said it was reviewing ratings on bigger banks, including Bank of New York Mellon BK, -1.71%,

State Street STT, -1.59%

and Northern Trust NTRS, -1.73%.

The S&P 500 Financials Sector has fallen for seven consecutive days, and is on pace for its longest losing streak since April 7, 2022, when it also fell for seven straight trading days.

Individual bank names are also performing poorly, with Goldman Sachs Group Inc. GS, -0.94%

and Citigroup Inc. C, -1.68%

down for 10 of the past 11 days and Charles Schwab Corp. SCHW, -4.84%

down 11 straight days.

Goldman alone has fallen for seven straight days for a total loss of 6.3%. It’s the longest losing streak since Feb. 28, 2020, when it also fell for seven straight days as the pandemic was taking hold.

The KBW Nasdaq Regional Banking Index KBWR

is down for 11 straight days. and the KBW Nasdaq Bank Index BKX

is down for seven straight days.

S&P downgraded Associated Banc. Corp. ASB, -4.20%,

Comerica Inc. CMA, -3.82%,

KeyCorp KEY, -3.58%,

UMB Financial Corp. UMBF, -2.42% % and Valley National Bancorp. VLY, -4.19%

by one notch and said the outlook on all five is stable.

The rating agency affirmed ratings on Zions Bancorp ZION, -4.17%

and maintained a negative outlook, meaning it could downgrade them again in the near-term. And it affirmed ratings and a stable outlook on Synovus Financial Corp. SNV, -3.37%

and Truist Financial Corp. TFC, -1.36%

“We reviewed these 10 banks because we identified them as having potential risks in multiple areas that could make them less resilient than similarly rated peers ,” S&P said in a statement.

“For instance, some that have seen greater deterioration in funding—-as indicated by sharply higher costs or substantial dependence on wholesale funding and brokered deposits—-may also have below-peer profitability, high unrealized losses on their assets, or meaningful exposure to CRE.”

The steep rise in interest rates orchestrated by the Federal Reserve over the past year has raised deposit costs as banks are now competing for savers seeking higher returns and that’s forced some to pay up on deposits and discourage their clients from heading to other institutions and instruments.

However, S&P said about 90% of the banks it rates have stable outlooks and just 10% have negative ones. None have positive outlooks.

The widespread stable outlooks shows that stability in the U.S. banking sector has improved significantly in recent months.

S&P is expecting FDIC-backed banks in aggregate to earn a relatively healthy ROE of about 11% in 2023.

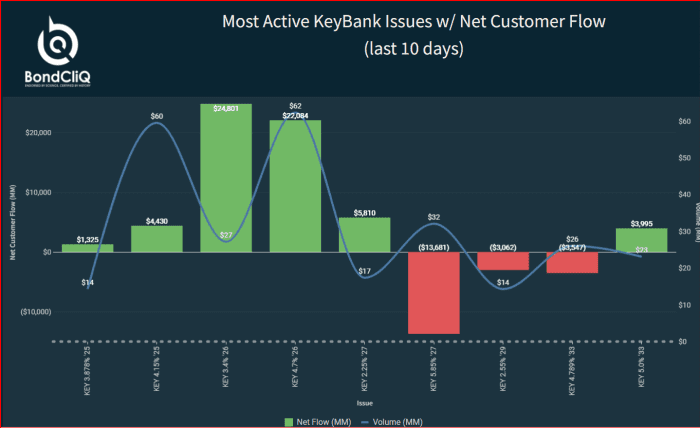

KeyCorp. and Comerica both fell more than 3% on the news. Of the two, KeyCorp. has more outstanding debt and its 10-year bonds widened by about 5 to 10 basis points, according to data solutions provider BondCliq Media Services.

As the following chart shows, the bonds have seen better selling on Wednesday with buyers emerging around midmorning.

KeyBank net customer flow (intraday). Source: BondCliQ Media Services

The next chart shows customer flow over the last 10 days.

Most active KeyBank issues with net customer flow (last 10 days). Source: BondCliQ Media Services

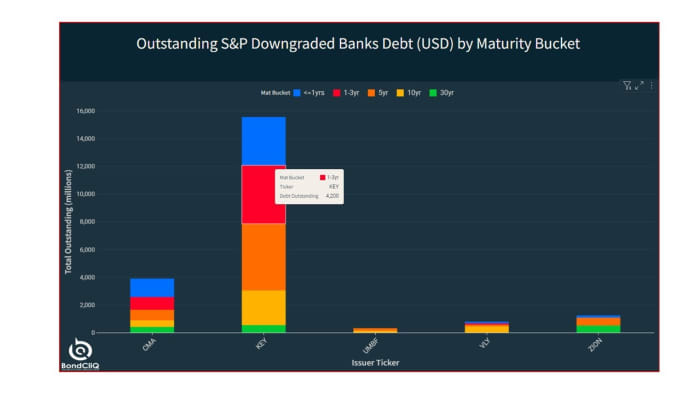

The next chart shows the outstanding debt of the downgraded banks, with KeyCorp. clearly the leader with almost $16 billion of bonds.

Outstanding S&P downgraded banks debt USD by maturity bucket. Source: BondCliQ Media Services

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

The second-quarter earnings season so far is showing that one trend that featured in the first quarter has not gone away.

“Greedflation,” or the practice of companies raising prices to protect their profit margins, is alive and well, based on the number of companies that have so far acknowledged raising prices yet again, even as inflation readings have come down and as some acknowledge that their input costs are falling.

At the same time, companies continue to emphasize on earnings calls that their customers are showing signs they are weary of higher prices and are shopping more frequently at more stores, while spending less per trip.

“Across industries, we’ve seen the same story over and over the last two years,” said Liz Zelnick, director of economic security and corporate power at Accountable.US, a liberal-leaning consumer-advocacy group.

“CEOs claim outside forces made them gouge consumers, then turn around and give themselves raises and boast of record profits and billions in new investor handouts,” she said, referring to the billions of stock buybacks and dividend payouts the same companies have made.

On a call with analysts, Chief Executive Jon Moeller signaled more price increases to come, which he attributed to the company’s innovation pipeline, which is creating must-have products.

“If you look back historically, pricing has been a positive contributor to our top-line growth for something like 48 out of the 51 last quarters and again as we strengthen our innovation program even further, that will provide opportunities to continue to benefit from modest pricing,” said Moeller, according to a FactSet transcript.

The company blew past earnings estimates with adjusted per-share earnings of $1.37, ahead of the $1.32 FactSet consensus, and sales of $20.6 billion, versus the $20 billion FactSet consensus.

Gross margin increased 380 basis points from a year ago, driven by 340 basis points of pricing benefit and 290 basis points of productivity savings.

Coca-Cola Co. KO, -1.51%

also swept past estimates and raised guidance after the drinks and snacks giant increased prices by 10%. The company’s adjusted operating margin rose to 31.6% from 30.6% a year ago.

Conagra Brands Inc. CAG, -0.62%

raised prices by up to 17%, which Chief Executive Sean Connolly described as “inflation-justified.” The parent of brands such as Birds Eye, Duncan Hines, Hunt’s, Orville Redenbacher’s and Slim Jim also reported that its customers are buying less food to stretch their budgets.

“[W]hile we did lose share in the quarter, as price gaps have stayed wider for longer than we would have liked, we are managing the business for the long term and still generated mid-single-digit top-line growth within the range of what we expected,” Chief Executive Miguel Patricio said.

The company, parent to brands including Kraft Mac and Cheese, Heinz Ketchup, Jell-O and Lunchables, indicated on the post-earnings conference call with analysts that rather than increasing discounting, or just cutting prices, it will remain focused on protecting margins, which has been allowing it to accelerate investment in the business, particularly in marketing, research and development and technology.

Besides, as Chief Financial Officer Andre Maciel said, the gaps between Kraft’s prices and those of competitors are not getting worse. “If anything, they are slightly getting better,” Maciel said, according to an AlphaSense transcript.

Considering the market-share losses and with inflation coming down, “do you think you took too much price, given you said you took price ahead of competitors, and they have not followed?” UBS analyst Cody Ross asked on the conference call.

CEO Miguel Patricio’s answer was simple: “No.”

“I mean, we had very high inflation. And we are leaders in the vast majority of categories where we play. And it’s our role as leader to try to compensate … this inflation with price increases,” Patricio said. “So I would do everything again. I mean we can always go back on price if we think we have to or when we have to. But we had to lead price increases.”

All of that leaves families to foot the bill for higher food prices, said Accountable.US’s Zelnick.

The Consumer Staples Select Sector SPDR exchange-traded fund XLP

has gained 1.2% in the year to date, while the SPDR S&P Retail ETF XRT

has gained 10.3%. The S&P 500 XRT

has gained 17%.

The second-quarter earnings season so far is showing that one trend that featured in the first quarter has not gone away.

“Greedflation,” or the practice of companies raising prices to protect their profit margins, is alive and well, based on the number of companies that have so far acknowledged raising prices yet again, even as inflation readings have come down and as some acknowledge that their input costs are falling.

At the same time, companies continue to emphasize on earnings calls that their customers are showing signs they are weary of higher prices and are shopping more frequently at more stores, while spending less per trip.

“Across industries, we’ve seen the same story over and over the last two years,” said Liz Zelnick, director of economic security and corporate power at Accountable.US, a liberal-leaning consumer-advocacy group.

“CEOs claim outside forces made them gouge consumers, then turn around and give themselves raises and boast of record profits and billions in new investor handouts,” she said, referring to the billions of stock buybacks and dividend payouts the same companies have made.

On a call with analysts, Chief Executive Jon Moeller signaled more price increases to come, which he attributed to the company’s innovation pipeline, which is creating must-have products.

“If you look back historically, pricing has been a positive contributor to our top-line growth for something like 48 out of the 51 last quarters and again as we strengthen our innovation program even further, that will provide opportunities to continue to benefit from modest pricing,” said Moeller, according to a FactSet transcript.

The company blew past earnings estimates with adjusted per-share earnings of $1.37, ahead of the $1.32 FactSet consensus, and sales of $20.6 billion, versus the $20 billion FactSet consensus.

Gross margin increased 380 basis points from a year ago, driven by 340 basis points of pricing benefit and 290 basis points of productivity savings.

Coca-Cola Co. KO, -0.49%

also swept past estimates and raised guidance after the drinks and snacks giant increased prices by 10%. The company’s adjusted operating margin rose to 31.6% from 30.6% a year ago.

Conagra Brands Inc. CAG, -0.75%

raised prices by up to 17%, which Chief Executive Sean Connolly described as “inflation-justified.” The parent of brands such as Birds Eye, Duncan Hines, Hunt’s, Orville Redenbacher’s and Slim Jim also reported that its customers are buying less food to stretch their budgets.

“[W]hile we did lose share in the quarter, as price gaps have stayed wider for longer than we would have liked, we are managing the business for the long term and still generated mid-single-digit top-line growth within the range of what we expected,” Chief Executive Miguel Patricio said.

The company, parent to brands including Kraft Mac and Cheese, Heinz Ketchup, Jell-O and Lunchables, indicated on the post-earnings conference call with analysts that rather than increasing discounting, or just cutting prices, it will remain focused on protecting margins, which has been allowing it to accelerate investment in the business, particularly in marketing, research and development and technology.

Besides, as Chief Financial Officer Andre Maciel said, the gaps between Kraft’s prices and those of competitors are not getting worse. “If anything, they are slightly getting better,” Maciel said, according to an AlphaSense transcript.

Considering the market-share losses and with inflation coming down, “do you think you took too much price, given you said you took price ahead of competitors, and they have not followed?” UBS analyst Cody Ross asked on the conference call.

CEO Miguel Patricio’s answer was simple: “No.”

“I mean, we had very high inflation. And we are leaders in the vast majority of categories where we play. And it’s our role as leader to try to compensate … this inflation with price increases,” Patricio said. “So I would do everything again. I mean we can always go back on price if we think we have to or when we have to. But we had to lead price increases.”

All of that leaves families to foot the bill for higher food prices, said Accountable.US’s Zelnick.

The Consumer Staples Select Sector SPDR exchange-traded fund XLP

has gained 1.2% in the year to date, while the SPDR S&P Retail ETF XRT

has gained 10.3%. The S&P 500 XRT

has gained 17%.

The Institute for Supply Management’s manufacturing index is due for release Tuesday, which outside of inflationary periods (i.e., now), tends to be one of the more important economic indicators for financial markets, given its record as a bellwether.

ISM manufacturing data during the current rate-hike cycle (in red) has lagged other periods.

Even compared to other rate-hike cycles, the ISM manufacturing series has been one of the worst in history, points out Jason Daw, head of North America rates strategy at RBC Dominion Securities. Daw makes the case that the U.S. economy overall is not very strong for this period of the cycle, and the manufacturing data, not just ISM but also industrial production, has been particularly feeble.

But the call of the day comes from JPMorgan’s economic team. They note that while global manufacturing stalled in the first half, the non-manufacturing components rose at a 3.2% annualized rate, allowing the global economy to grow at an above trend 2.7% rate.

The team led by Bruce Kasman say that the typical channels through which weak manufacturing would bring down the broader economy haven’t materialized. “A major channel by which weakness in goods sectors broadens out is through depressing corporate income and pricing power. While our start-of-year outlook anticipated elevated wage gains to pressure corporate profits, the surprising strength in [first-half] global GDP was accompanied by upside surprises to inflation,” they say. In turn, there have been solid gains in both labor income and profits, and while margins have come off their peaks, they are well above pre-pandemic levels.

Business hiring, they add, is the ultimate signal of confidence, and employment growth has continued even though expectations have soured.

Now, say the JPMorgan team, the stage is set for a goods sector recovery. Labor income, when adjusted for inflation, is rising, while finished goods inflation is falling sharply.

Also, business capital spending continues to expand, particularly in emerging economies outside of China. And importantly, inventories are swinging from a drag to a lift. In the first half, the step down in the pace of stock building depressed global industrial production by 3.4 percentage points.

“Even if the pace of stockbuilding was only to level off, the impulse to global industry would be material. Add to that a potential desire to align the pace to firming demand growth and the boost could generate a jump in factory output in the coming months,” they say.

Finally, they note, the tech spending decline after the 2020 to 2021 surge looks to be ending, and global motor vehicle production is picking up as supply-chain bottlenecks ease.

The markets

After an okay finish for the S&P 500 SPX, -0.29%

to a strong July, U.S. stock futures ES00, -0.36%

NQ00, -0.42%

were a bit lower as the seasonally weak month of August commenced. Gold futures GC00, -1.28%

were trading below $2,000 an ounce. The dollar DXY, +0.42%

rose.

The ISM report is due out at 10 a.m. Eastern, when the job openings and construction spending reports also come out. Monthly auto sales also will be released throughout the day.

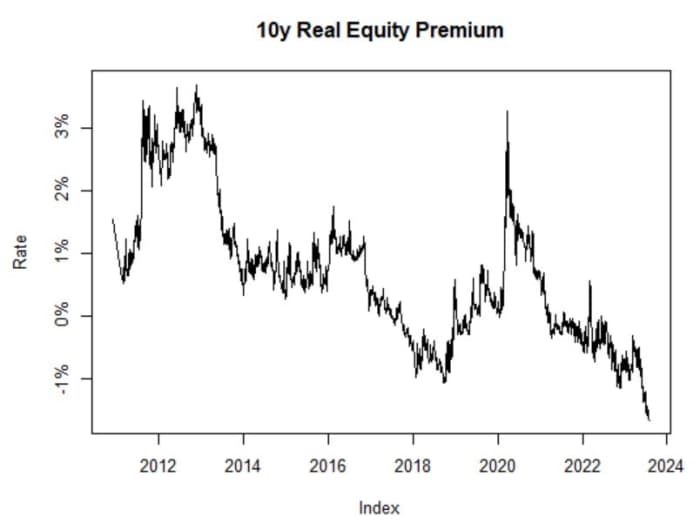

The inflation-adjusted equity premium is looking pretty bleak. That’s calculated by taking the expected return to the S&P 500 and subtracting 10-year TIPS yields. “While admittedly this graphic is skewed by the few megacaps trading at huge multiples, it’s sobering nonetheless,” says Michael Ashton, better known as the Inflation Guy.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Listen to the Best New Ideas in Money podcast with MarketWatch financial columnist James Rogers and economist Stephanie Kelton.

KYIV — An overnight naval drone attack against a Russian tanker in the Black Sea signals a potential new front in the Ukraine war, with Kyiv delivering its strongest message to date that it is willing to target Moscow’s all-important shipments of oil and fuel.

The battle for supremacy in the Black Sea is ramping up fast, with massive implications for global energy and food security. The attack on the tanker off Crimea came only a day after another Ukrainian marine drone — a flat, arrowhead-shaped vessel packed with explosives — targeted a Russian naval base near the port of Novorossiysk, badly damaging a warship.

“The tanker was damaged in the Kerch Strait during an attack by the Ukrainian Armed Forces,” Russia’s state-run TASS news agency reported on Saturday. “The crew is safe, the Maritime Rescue Center informed us. The engine room was damaged. Two tugboats arrived at the scene of an emergency with a tanker in the Kerch Strait, the question of the towing vessel is being resolved,” it said.

Russia’s Federal Marine and River Transport Agency reported it was a SIG oil and chemical tanker — a ship whose owner, St. Petersburg-based company Transpetrochart, was sanctioned by the U.S. in 2019 for supplying jet fuel for Russian forces in Syria.

Tensions are rising in the Black Sea after Russia last month announced it was withdrawing from the U.N.-brokered Black Sea Grain Initiative and started attacking Ukrainian ports on the Black Sea coast and on the Danube River with missiles, destroying tens of thousands of tons of Ukrainian grain.

After those attacks and the blockade, Ukrainian officials issued a statement in July that Russian vessels will be no longer safe in the Black Sea. Kyiv’s defense ministry said in a statement that such vessels “may be considered by Ukraine as carrying military cargo with all the corresponding risks” from midnight Friday.

On Saturday, Kyiv announced a “war risk area” around Russian ports on the Black Sea, specifically citing the ports of Novorossiysk, Anapa, Gelendzhik, Tuapse, Sochi and Taman. The declaration will be in effect from August 23 “until further notice,” it said.

‘Completely legal’

Marine Traffic, an online maritime tracking site, has the latest position of the SIG tanker fixed near the Kerch Strait “at anchor.”

Russia’s Marine and River Transport Agency reported all 11 crew members on board were safe and that the tanker was struck in the engine room near the waterline on the starboard side, presumably as a result of an attack by a marine drone. By morning, the water pouring to the engine room has been staunched, and the vessel was afloat, Russian official said.

Ukraine almost never directly takes responsibility for these kinds of attacks. However, Vasyl Malyuk, head of the Security Service of Ukraine, or SBU, has previously claimed responsibility for the attacks on the Crimean bridge and hinted that there will be more similar attacks soon.

“Anything that happens with the ships of the Russian Federation or the Crimean Bridge is an absolutely logical and effective step in relation to the enemy. Moreover, such special operations are conducted in the territorial waters of Ukraine and are completely legal,” Malyuk said in a statement on Saturday.

“So, if the Russians want that to stop, they should leave the territorial waters of Ukraine and our land. And the sooner they do it, the better it will be for them. Because we will one hundred percent defeat the enemy in this war.”

Waters near Russian-occupied Crimea and the Kerch Strait are Ukrainian territorial waters, according to international maritime law.

“Since 1991, Russia has systematically used the territorial waters of Ukraine to organize armed aggressions: against the Georgian people and against the people of Syria,” the Ukrainian Defense Ministry said in a social media post on Saturday.

“Today, they terrorize peaceful Ukrainian cities and destroy grain, condemning hundreds of millions to starvation. It’s time to say to the Russian killers, ‘It’s enough.’ There are no more safe waters or peaceful harbors for you in the Black and Azov Seas,” the ministry said.

Offshore oil drillers were about the worst place to be in 2020 as oil prices were falling and demand for crude seemed to be seeping away. Now, the stocks may be the ones to own as investors realize that oil will be needed to make the world go around for decades.

The numbers: Two U.S. regional gauges of manufacturing sentiment showed signs in June that they may be improving after a rough patch, according to data released Thursday.

The Philadelphia Federal Reserve’s manufacturing index slipped further to a reading of negative 13.7 in June from negative 10.4 in the prior month, but economists had expected a reading of negative 14.8, according to a Wall Street Journal survey of economists. This is the tenth straight negative reading.

Orders for manufactured goods rose 0.4% in April, the Commerce Department said Monday. It is the fourth increase in factory-goods orders in the past five months.

Economists surveyed by the Wall Street Journal were expecting a 0.6% rise.

The gain was led by transportation equipment. Excluding that sector, orders were down 0.2%.

Durable-goods orders rose 1.1% in April, unrevised from the initial estimate last week. The advance durable-goods data is always released ahead of the full report. Nondurable-goods orders fell 0.1% in April.

Orders for nondefense capital goods, excluding aircraft, rose a revised 1.3% in April, down slightly from the prior estimate of a 1.4% increase. The gain was led by computers and machinery.

A spokesperson for JPMorgan Chase & Co. on Friday has confirmed statements on social media that some customers are seeing duplicate transactions and fees on their checking accounts.

“We’re sorry,” the spokesperson said in an email to MarketWatch. “We’re working to resolve the issue and will automatically reverse any duplicates and adjust any related fees.”

JPMorgan Chase JPM, +2.10%

customers on Twitter and other social-media outlets said payments made through Zelle were showing up twice.

“PSA!!!,” said Twitter user @haunteraIIA. “Anyone waking up to duplicate zelle charges from chase, my call just went through and was told the duplicate charge should be credited within 24hours. they’re having issues with this today. i was on hold for an hour, so just in case anyone else wakes up freaked out lol.”

Zelle is jointly owned by six banks: JPMorgan, Truist Financial Corp. TFC, +3.62%,

Capital One COF, +4.00%,

U.S. Bancorp USB, +4.00%,

PNC Financial Services Group Inc. PNC, +3.21%

and Wells Fargo & Co. WFC, +2.95%.

A spokesperson from Chase clarified that the problems are confined to its customers.

Imagine a court hearing where the plaintiff is not a person, but a damaged river, lake or mountain.

That’s the vision of a movement of conservationists — gaining traction across the Continent — that believes granting basic legal rights to nature can help protect it from threats like deforestation, biodiversity loss, chemicals pollution and climate change.

“We usually think about nature as an object” that “serves us,” such as a swimming pool or a natural park, said Eduardo Salazar, a lawyer involved in the successful push to grant legal rights to Mar Menor, a large saltwater lagoon in Murcia in southeastern Spain polluted by the overuse of nitrogen fertilizers by nearby farmers.

Granting an ecosystem legal status on “the same level” as individuals can help alter social attitudes to nature, he said, and give it important new protections.

The lagoon last year became the first ecosystem on the Continent to be granted a status comparable to that of a person following a campaign backed by more than 600,000 people.

Activists are now trying to replicate the model elsewhere.

In Poland, a group of activists this week will complete the last leg of a 43-day-long march along the Oder River aimed at drawing attention to their campaign to grant the polluted ecosystem — which runs along the German-Polish border — the legal status of a person.

After a massive die-off last summer killed thousands of fish in the Oder, campaigners fear the ecosystem may be headed for another ecological disaster, pointing to Poland’s failure to rein in industrial emissions that are thought to have contributed to the incident.

“There is a lot of suffering going on in this river,” said Przemek Siewior, a climate activist who joined the march. Giving the fragile ecosystem legal rights is “a really good tool for people to try to save it,” he argued.

A ‘voice’ for nature

The so-called rights of nature movement, which originated in the United States some 50 years ago, has gained traction in recent years thanks to growing attention to the importance of protecting nature as part of combating climate change and biodiversity loss.

A growing number of countries — including Uganda, Ecuador and New Zealand — have laws granting ecosystems legal rights, and court rulings in India and Colombia have recognized such rights and stressed the government’s duty to protect it. Just last month, Panama gave rights to sea turtles in a bid to protect them against pollution and poaching.

In Europe, campaigners are hoping to ride the coattails of the Mar Menor movement, with citizens’ initiatives pushing for similar recognition for the North Sea in the Netherlands and the Loire River in France, for example.

The Loire River bed at Loireauxence was completely dried out because of extreme heat in September 2022 | Damien Meyer/AFP via Getty Images

At the movement’s core is a call for a fundamental rethink of the way people relate to and understand ecosystems. But more tangibly, campaigners also stress the importance of ensuring ecosystems can be represented in court.

In New Zealand, granting legal personhood to the Whanganui River was seen as a key step to ensure the Indigenous Māori community living in its vicinity gets more say on the health of the ecosystem.

The Spanish law giving Mar Menor a right “to exist as an ecosystem and to evolve naturally” ensures it will be represented by a group of caretakers, made up of scientists, local politicians and citizens.

Inspired by the Spanish example, the Oder River movement last month published a draft law to protect the ecosystem that would include establishing a 15-person committee to represent the river. Three would be appointed by the state, four by municipalities and eight by NGOs; a group of 10 scientists would advise the committee.

That structure would “give the Oder River a democratic representation” and a “voice that it currently just doesn’t have,” said Gaweł Andrzejewski, the coordinator of the Oder River march.

The process is still in its early stages: Drafted by a lawyer in collaboration with civil society, the draft bill is mostly meant to “stir and start the conversation” with politicians and NGOs, said Andrzejewski.

Practical impact

Critics argue that such representation is largely symbolic and doubt it can do much to help protect and restore ecosystems.

Setting up committees to represent an ecosystem gives “power to particular people” to make decisions about what is or isn’t in its interest, said Michael Livermore, a professor of law at the University of Virginia who specializes in environmental law, among other topics.

But there’s no guarantee that they’ll make the right call, or that it’ll be heeded. “I think part of the issue with a legal right is that you still run into problems, like what’s best for an ecosystem? And who’s going to make that decision?” he said.

In Ecuador, for example, environmental activists challenged a large-scale mining project located in one of the most biodiversity-rich areas of the planet, saying it violated nature’s rights — but the court ruled against them, arguing that the government’s interests to exploit the resource were important enough to override the nature rights argument.

Giving ecosystems legal status also does not guarantee protection — granting the Indian Ganges River legal personhood in 2017 has not prevented it from deteriorating, for example.

Livermore argues there are more efficient alternatives to protecting nature, such as preserving people’s rights to organize, providing protections for environmental organizations or improving decision-making processes to give more power to Indigenous communities.

Companies have so far remained relatively quiet on the movement — to Livermore, that’s a sign that giving rights to nature doesn’t pose much of a challenge.

“If it’s such a powerful tool to protect the environment, why don’t the special interests that worry about that, who would be opposed to very strong environmental protections, why aren’t they fighting it?” he said.

The numbers: The Philadelphia Federal Reserve said Thursday its gauge of regional business activity rose to negative 10.4 in May from negative 31.3 in the prior month. Any reading below zero indicates deteriorating conditions. This is the ninth straight negative reading and the eleventh in the last twelve months.

Economists polled by the Wall Street Journal expected a negative 20 reading in May.

Key details: The barometer on new orders increased 13.8 points but remained at negative 8.9 in May. The shipments index rose slightly to negative 4.7. The measure on six-month business outlook worsened to negative 10.3 in May from negative 1.5 in the prior month.

Big picture: The continued contraction in activity is a sign that U.S. manufacturing continues to struggle.

The Philadelphia Fed index is closely followed to give economists an advance signal of factory conditions across the country.

Things move quickly in the world of artificial intelligence. It is easy to sit back and complain about developments that could be disruptive, but sometimes investors are best served by putting emotions aside and observing new developments and how they affect markets. Could AI developments and related trends make you a lot of money?

Below is a new screen showing a group of AI-oriented companies expected to increase their sales most rapidly through 2025, based on consensus estimates among analysts polled by FactSet. Then we show expected revenue growth rates for the largest AI-oriented companies in the screen.

Over the long haul, many businesses might perform more efficiently by employing AI. Maybe this technology can create an economic revolution similar to the one that moved the majority of the working population away from agricultural labor during the 19th and 20th centuries.

Back in February, we screened 96 stocks held by five exchange-traded funds focused on AI and related industries and listed the 20 that analysts thought would rise the most over the following 12 months.

Three months is a long time for AI, and the shakeout hasn’t even started.

There is no way to predict how politicians will react to perceived or real threats of AI and machine learning. And the largest U.S. tech players are doing everything they can to employ the new technology and remain dominant. But that doesn’t mean they will grow more quickly than smaller AI-focused players.

A new AI stock screen

Once again we will begin a screen with these five ETFs:

The Global X Robotics & Artificial Intelligence ETF BOTZ, +0.97%

BOTZ was established 2016 and has $1.8 billion in assets under management. The fund tracks an index of companies listed in developed markets that are expected to benefit from the increased utilization of robotics and AI. There are 44 stocks in the BOTZ portfolio, which is weighted by market capitalization and rebalanced once a year. Its largest holding is Intuitive Surgical Inc. ISRG, +0.53%,

which makes up 10% of the portfolio, followed by Nvidia Corp. NVDA, +3.30%

at 9.4%.

The iShares Robotics and Artificial Intelligence Multisector ETF IRBO, +1.64%

holds 116 stocks that are equal-weighted, as it tracks a global index of companies that derive at east 50% of revenue from robotics or AI, or have significant exposure to related industries. This ETF was launched in 2018 and has $304 million in assets.

The $246 million First Trust Nasdaq Artificial Intelligence & Robotics ETF ROBT, +1.83%

has 107 stocks in its portfolio, with a modified weighting based on how directly companies are involved in AI or robotics. It was established in 2018.

The Robo Global Artificial Intelligence ETF THNQ, +1.81%

has $26 million in assets and was established in 2020. I holds 69 stocks and isn’t concentrated. It uses a scoring system to weight its holdings by percentage of revenue derived from AI, with holdings also subject to minimum market capitalization and liquidity requirements.

The newest ETF on this list is the WisdomTree Artificial Intelligence and Innovation Fund WTAI, +2.42%,

which was established in December and has $13 million in assets and holds 73 stocks in an equal-weighted portfolio. According to FactSet, stocks are handpicked and selected companies “generate at least 50% of their revenue from AI and innovation activities, including those related to software, semiconductors, hardware technology, machine learning and innovative products.”

Altogether and removing duplicates, the five ETFs hold 270 stocks of companies in 23 countries. We first narrowed the list to 197 covered by at least nine analysts and for which consensus sales estimates are available through calendar 2025. We used calendar-year estimates because some companies have fiscal years that don’t match the calendar.

Here are the 20 screened AI-related companies expected by analysts to have the highest compound annual growth rates (CAGR) for sales from 2023 through 2025. Sales estimates are in millions of U.S. dollars. The list also shows which of the above five ETFs holds each stocks.

Click the tickers for more about each company or ETF.

Click here for Tomi Kilgore’s detailed guide to the wealth of information for free on the MarketWatch quote pages.

We have screened for expected revenue growth, rather than for earnings or cash flow, because in a newer tech-oriented business area, investors are most likely to consider the top line as companies sacrifice profits to build market share.

It is important to do your own research if you consider purchasing any individual stock, to form your own opinion about a company’s ability to remain competitive over the long term. Starting from the top of the list, BioXcel Therapeutics Inc. BTAI, -2.47%

is expected to show exponential sales growth, but that is from a low expected baseline this year.

What about the largest AI-related companies held by these ETFs?

Here are the largest 20 companies in the screen by market capitalization, ranked by expected sales CAGR from 2022 through 2025. Once again the sales estimates are in millions of U.S. dollars, but the market caps are in billions.

The numbers: The cost of U.S. imported goods rose 0.4% in April, the Labor Department said Friday. This was the first increase this year.

Economists polled by the Wall Street Journal had forecast a 0.3% gain.

Over the past 12 months, the costs of imports has dropped 4.8%. That followed a 12.5% gain in the prior year.

Key details: The cost of imported fuel rose 4.5% in April after a 3.9% drop in the prior month. This was the first increase since last June.

The cost of imports excluding fuel were flat in April after a 0.5% decline in the prior month. Over the past year, nonfuel import prices are down 1.9%.

Exports prices rose 0.2% in April. They are down 5.9% over the past year.

Big picture: The stronger dollar last year dampened import prices and was a source of disinflation, but with the dollar softer this year, prices are firming.

One sign perhaps of the weaker dollar is that consumer goods prices ex-autos rose 0.2% in April and are up 1.1% annualized over the past three months, said Michael Gapen, U.S. economist at Bank of America Securities.

What are they saying? “Perhaps imported inflation is the first early signal of how brutal the fight against inflation will be in the coming months. Investors and traders should remember that the Fed’s target is 2%,” said Alex Kuptsikevich, senior market analyst at FXPro.