[ad_1]

New data shows more Americans are filing for bankruptcy, the latest indication that price pressures and an uneven economy are leaving some households strapped for cash.

Total consumer bankruptcy filings jumped 12% from 478,752 in 2024 to 533,949 in 2025, according to Epiq AACER, a platform that provides U.S. bankruptcy filing data. Epiq, which tracks Chapter 7, Chapter 11 and Chapter 13 filings, relies on data provided through the U.S. Courts’ PACER system, an electronic database that houses federal court records.

The surge in filings comes as American consumers — and businesses — face a slate of economic pressures, ranging from sticky inflation to elevated borrowing costs, experts told CBS News.

John Rao, a senior attorney with the National Consumer Law Center, said Americans typically hold off on filing for bankruptcy as long as they can, meaning the conditions that led them to file for bankruptcy may not necessarily be tied to current economic issues.

“There is often a lag before economic conditions translate to higher bankruptcies,” he said.

Still, he said the rising cost of medical insurance, mounting credit card debt and the restart of student loan repayments are serving as some of the major catalysts for bankruptcies. Inflation has also made it tougher for Americans to cover expenses while paying down their debt, he added.

“There comes a point where the mounting bills, the increasing balances on credit cards, all those things just weigh people down so much,” Rao said.

A December CBS News poll found most Americans are struggling to afford basic living costs in the U.S., including health care, food and housing.

A bankruptcy filing can provide consumers with a financial reset, stopping collection calls and wiping out some or all of their debt. But the relief comes with trade-offs: Bankruptcy can severely damage a credit score, delay the ability to buy a home and make it tougher to qualify for loans in the future.

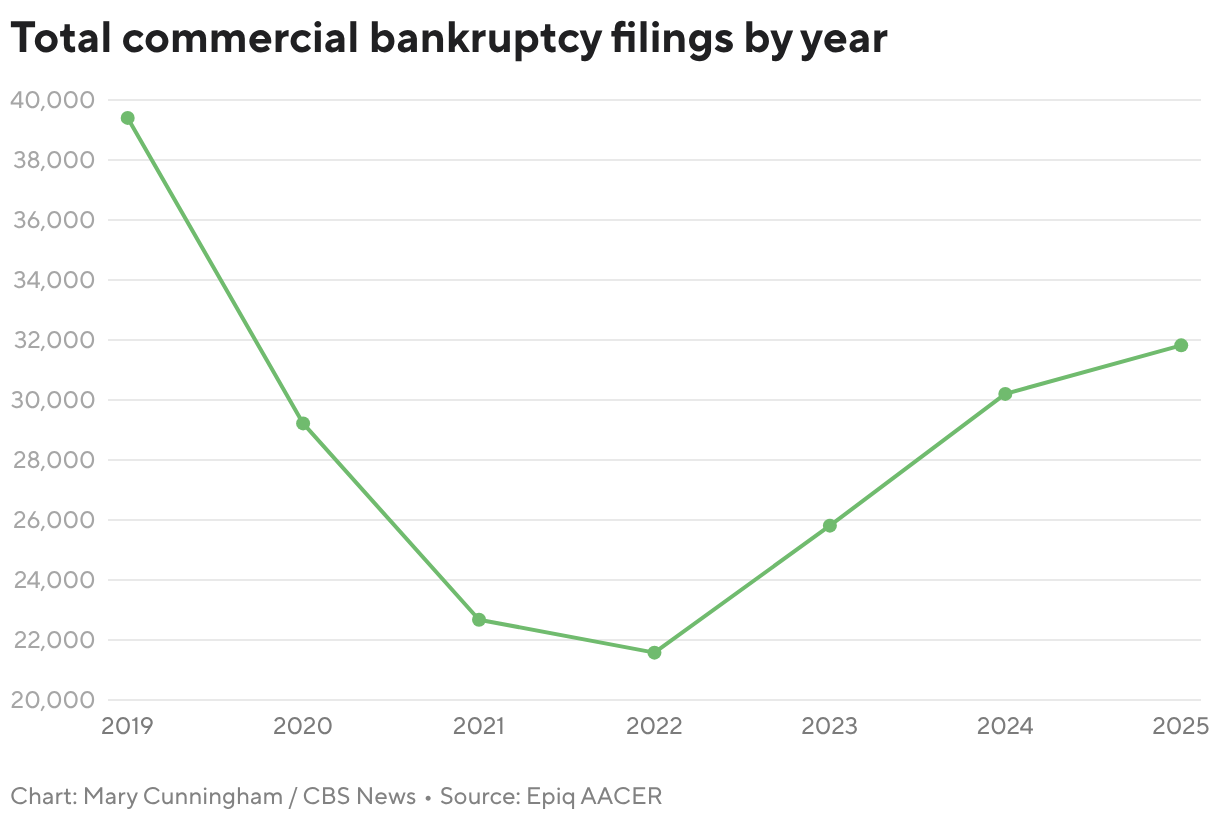

Commercial filings drift higher

Commercial bankruptcies are also on the rise, with filings up 5% from 2024 to 2025, according to Epiq AACER’s data. In 2025, consumers lost a number of national and regional retailers — including Forever 21 and Joann Fabrics — that failed to stay afloat even after seeking bankruptcy protection.

Chapter 11 bankruptcies, which allow companies to restructure their finances, were up just 1% from 2024 to 2025, driven by higher interest rates in 2023 and 2024 along with inflation, according to Christopher Ward, the co-chair of bankruptcy and restructuring at Polsinelli Law Firm.

Among the most notable recent filings is Saks Global, which filed for Chapter 11 on Wednesday. The parent company of Saks Fifth Avenue, Neiman Marcus and Bergdorf Goodman said it has secured financing that will allow it to keep stores open as the bankruptcy proceeds.

Pre-pandemic normalization

Experts emphasized that the increase in commercial and consumer bankruptcies represents a return to pre-pandemic norms.

Bankruptcies dipped during COVID as an injection of government funding helped prop up cash-strapped businesses and American households. Forbearance plans also gave some mortgage payers and car owners more financial breathing room, said Michael Hunter, vice president of Epiq AACER.

However, once those temporary relief measures faded, bankruptcy filings drifted higher, with data showing an upward trend since 2022.

“We’re just slowly coming back to pre-COVID levels,” Hunter said. “Is it a huge event? No. Is it a big increase from what we’ve experienced over the past five years? Yes.”

While the overall number of bankruptcies is still below their pre-COVID levels, they could start to accelerate, Rao told CBS News.

“There’s a good chance that filings will even be higher through this year and even into next year,” he said.

[ad_2]