This is an opinion editorial by Seb Bunney, co-founder of Looking Glass Education and author of the Qi of Self-Sovereignty newsletter.

“History never repeats itself, but it does often rhyme.” — A quote commonly misattributed to Mark Twain.

Lately, I’ve been pondering whether we are witnessing a rhyming of history.

For those who have had the chance to dig into our monetary history, you may have encountered a little-known policy called Executive Order 6102. It was a momentous attack on the sovereign individual and the free market. An event that corralled U.S. citizens away from gold, into the U.S. dollar and assets from which the U.S. government benefits.

What Was Executive Order 6102?

During the Great Depression, President Franklin D. Roosevelt issued Executive Order 6102 on April 5, 1933, forbidding the hoarding of gold coin, gold bullion and gold certificates within the continental United States.

At that time, the Federal Reserve Act of 1913 required any newly issued dollar bills to be 40% backed by gold. Executive Order 6102 freed the Fed from this restriction as it could coercively obtain more gold than it otherwise would have been able to by restricting the usage of gold and purchasing it back at an exchange rate defined by the government.

Moreover, pushing people out of gold and into U.S. dollars helped strengthen the dollar during a period of monetary expansion and central bank intervention.

This Executive Order was in effect until December 31, 1974, when congress once again legalized private ownership of gold coins, bars and certificates.

With an understanding of Executive Order 6102, I wanted to shed some light on modern government thinking.

In the eye-opening book, “The Mr. X Interviews: Volume 1,” Luke Gromen takes the reader on a journey through the past, present and future macroeconomic environment. Although the book details many captivating events, one event in particular stood out to me. Groman cites a leaked document from the U.S. State Department dated December 10, 1974. Here is an excerpt from that document:

“The major impact of private U.S. ownership, according to the dealers’ expectations, will be the formation of a sizable gold futures market. Each of the dealers expressed the belief that the futures market would be of significant proportion and physical trading would be minuscule by comparison. Also expressed was the expectation that large-volume futures dealing would create a highly volatile market. In turn, the volatile price movements would diminish the initial demand for physical holding and most likely negate long-term hoarding by U.S. citizens.”

Essentially, the government knew that by promoting the gold futures market, gold would experience a significant increase in price volatility, diminishing its desirability and reducing long-term hoarding. More importantly, this document was dated 21 days before they reinstated the ability for individuals to own gold again.

What Does This Mean?

If people are disincentivized to store their hard-earned savings in a stable vehicle such as gold, they must look elsewhere. With equities and corporate bonds exposing the investor to greater risk and volatility, people have two options: government bonds or U.S. dollars, both benefiting the government.

The government has shown that it no longer needs to overtly issue an order such as 6102 to ban the holding of gold. It just needs to reduce gold’s desirability to achieve the same effect.

What Does This Have To Do With The Aforementioned Quote?

In October 2021, the Securities and Exchange Commission (SEC) approved the first Bitcoin futures Exchange Traded Fund (ETF). For the less financially inclined, an ETF is a regulated investment vehicle that simplifies the purchasing of its underlying assets. For instance, if you purchase the SPY ETF, you can own exposure to the hugely popular S&P 500, without purchasing 500 individual stocks.

On its own, the futures market is no cause for alarm, but when the SEC prevents corporations and individuals from purchasing BTC through regulated means, only allowing futures ETFs, we have an issue.

Let me explain.

Companies in the Bitcoin industry have been applying for a “spot Bitcoin ETF” for many years, but to no avail. If this spot ETF were to get accepted, you could invest $100 into the ETF, which would then purchase $100 of bitcoin held by the fund, giving you direct exposure to bitcoin. This would provide pension funds, corporations, asset managers, etc., easier access to bitcoin. But this is not yet available in the U.S.; only a futures ETF is.

If not already evident from the gold futures explanation above, this may pose a threat to bitcoin.

When someone purchases a bitcoin futures ETF, they do not own bitcoin. Instead, they own exposure to an ETF which holds bitcoin futures contracts. In short, this futures ETF purchases contracts for the delivery of bitcoin at a future date. As that date approaches, it rolls the futures contract, selling the old contract and purchasing a new contract further out.

Don’t worry if you don’t quite understand how these ETFs work. The point here is not to understand the functionality but rather the drawbacks.

It is essential to understand two characteristics of futures ETFs over spot ETFs. In regular, functioning markets, if you want the right to buy something at a specified price in the future, you pay a premium over today’s price, and the further out in time you wish to lock in a price, the more premium you pay. Each time the contract is rolled, more premium is paid. This is called roll yield.

Even if bitcoin’s price stays the same throughout the life of the futures contract, the ETF will still decline in value because the ETF is paying a premium to purchase the right to buy bitcoin in the future. As that date nears, it’s selling the contract and purchasing a new one further out in time. This is known as rolling.

A byproduct of this rolling is that any paid premium diminishes as contract expiration approaches (roll yield). This creates a decay in the value of the ETF and is incredibly unfavorable for long-term holders.

As a result, this decay incentivizes short-term trading, increased volatility and short selling of the ETF as a portfolio hedge, suppressing the price.

Is it possible to see the effects of these futures ETFs in action? Below is a chart from Willy Woo. The date of the approval for the first futures ETF was in October 2021.

Immediately preceding the inception of the first regulated futures ETF, we saw a considerable increase in futures dominance. The futures market currently dictates 90% of bitcoin’s price (green line in the chart above).

In summary, just like gold from the 1930s to the 1970s, individuals and corporations alike have no regulated way to purchase bitcoin efficiently for long-term storage. The only difference being in the age of censorship, rather than overtly suppressing what the government deems as unfavorable or infringing on certain aspects of the economy, it can covertly suppress them. However, not all hope should be lost.

Many people and corporations are tirelessly petitioning for the approval of a spot ETF, a way to gain direct exposure to bitcoin. But this begs the question: Is bitcoin one of the last remaining bastions for the free market and self-sovereign individuals, or is it already under the thumb of the central planners?

This is a guest post by Seb Bunney. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Ray Dalio, the founder of the world’s biggest hedge fund Bridgewater Associates, in an exclusive interview with Business Today has said that India should have the highest growth rate in the near future if various indicators and prevailing global factors are considered. Dalio said as India’s neutral stand on geopolitical tensions is a good thing.

He said that the country was opening up to the global capital markets and if that continued, it would be good for the capital market in India, in terms of capital flows.

Here are a few excerpts from his interview:

US Federal Reserve and central banks’ stand on interest rate hike

RD: The inflation rate and the bond yield will have to be high enough to satisfy creditors. So that, bond holders can get higher returns that are above the inflation rate. That’s the current challenge for US Fed because debtors do not want to receive interest rates that are too high.

I think we’re going to have an inflation rate that is probably in the vicinity of 5 per cent-ish. But it’s a very uncertain inflation rate because of all the shocks that we have around it.

The real rate, in other words, the rate above inflation that the interest rate is now at is in the vicinity of 1.5 per cent, a little bit higher than that. So that would mean that they would be probably approaching a 6 per cent, risk-free rate. And the Federal Reserve will put the short-term rate up towards that level. That level of interest rate is very harmful, very damaging to the economy.

Interest rates and inflation

The world, the United States is going to spend a lot more money than it is taking in. In the United States, we will have a budget deficit, which is in the vicinity of 5 per cent of GDP. As is now planned, the Federal Reserve will also sell its bonds, and short-term debt to the tune of about 5 per cent of GDP. That’s 10 per cent of GDP. So that’s going to create a very tight set of circumstances.

At some point, we see that there’s not a demand for that, for various reasons. The real rates are not high enough, the bond market is going down, investors are losing money in it, and so on. And so, there’s a mismatch there. So that will shrink private credit. So those conditions create a bad set of conditions for growth.

Balancing growth and inflation

We need money for poverty alleviation, building infrastructure, repairing Ukraine, spending money for climate change. The big difference between individuals and governments is the governments don’t have that constraint because they can print money. So, I think we have this trade-off. Whenever in history, you have a lot of debt and a lot of financial assets, it becomes very, very difficult for those to be balanced. And we’re now in a shift.

The prior decade, we had falling interest rates. Cash was very cheap, free, almost. And so, the whole investment landscape was very much built around that. Now we’re having this adjustment away from that. So central banks try to balance growth and inflation.

How investors are managing with high interest rates

I think that what you’re going to see is a classic sequence of events, where the interest rate rise is high enough that it is good for the creditor, but bad for the economy. And that when economic conditions become a bigger worry than inflation, you will see them come in and print more money and the value. So, I think it’s very important for investors over the long term, to not hold debt instruments. Over the short term, as long as those exist, then I would say neutral or slightly attractive.

Investment during high inflation, interest rates

Whether whichever country you’re in, whichever currency you’re denominated in, look at the returns relative to inflation. Too many people look at just the level of returns, and they don’t pay enough attention to inflation. Generally, stay away from debt assets, debt denominated assets. Third, have a well-diversified portfolio. Diversification reduces risk without reducing expected returns, if you do it well.

Changing dynamics in global politics

It is now Russia and China. And there are five kinds of wars. There is a trade war, a technology war, a geopolitical influence war, a capital and economic war, and a military war– five of those. We are in the first four of those. If we never go to a military war, we still having damage happening. Because we are still in an environment where globalisation, as we know it, is declining. Because right now in fears of those wars, there is the desire for self-sufficiency. It used to be that the world would come close to producing items and trading items, wherever it was most efficient. That is now changing.

I think India has a great potential. India, I use indicators, we use indicators of the next 10 years growth rate. Some of the indicators are the cost of an educated person. In other words, what is the education level, but also how expensive are they? Barriers to trade and capital flows, level levels of corruption, many different indicators. And on balance, India should have the highest growth rate of any country. And it’s opening up to the global capital markets. If that continues, that’ll be efficient for the capital markets in India, and capital flows.

India is largely taking a neutral position in these conflicts. It of course, needs to develop a very strong leading economy related to technology. It is not the two main competitors in technology development. Big technology platforms and all of that are still of course, the United States and China. And those are going to be cutting edge areas.

India’s level of indebtedness, a number of indicators indicates that it should do very well over the next 10 years. But it’ll be important to have a modernisation, particularly of the capital markets, to bring in the efficiencies.

Tech stocks on NASDAQ (Facebook stocks are down by 40-50%)

So, there was a bubble in tech stocks. Mostly, what’s happening is that a number of these have negative cash flows. That means they didn’t have earnings that will support those prices. And in many cases, they didn’t have earnings. And they relied on either borrowing money to make up the gap or raising venture capital or private equity money. And free money was basically free and plentiful. Money was basically the paradigm. And so, you’re now seeing those companies who have negative cash flows, being severely hurt. Because if the money doesn’t come in, then they’ll go broke, they’ll run out of money, they have to contract and so on. And we’re seeing that happen.

If we look at climate change, or even the environment for pandemics, you know, that’s something that’s also worrying. The surprises for climate are not going to be on the upside, they’re going to be worse.

Climate remediation is estimated to cost $9 trillion a year in order to reach goals which probably won’t be reached, and who’s going to pay for that money? That’s very expensive at this time. So, I think between now and 2024, it’ll become an increasingly difficult period, but there’ll be good inventions, and there’ll be good developments.

A version of this story first appeared in CNN Business’ Before the Bell newsletter. Not a subscriber? You can sign up right here. You can listen to an audio version of the newsletter by clicking the same link.

New York CNN Business

—

What will the Federal Reserve do at its meeting in December? Analysts can speculate all they want, but Fed officialssay they will be using hard economic data to make their next decision.

That means key housing, labor, and inflation reports will likely have outsized effects on the market as investors speculate about what they might mean for the future of interest rates.

What’s happening: No one can move markets like Federal Reserve Chair Jerome Powell — with just a few words on Wednesday he crushed investors’ hopes of an interest rate pivot and sent stocks plunging. “We have a ways to go,” said Powell of the Fed’s current hiking regime meant to fight persistent inflation. “It’s very premature, in my view, to think about or be talking about pausing.”

But Powell did add an important caveat. The Fedcould start to slow the pace of those painful hikes as soon as December. “Our decisions will depend on the totality of incoming data and their implications for the outlook for economic activity and inflation,” Powell said on Wednesday.

So what will the Fed be looking at between today and itsnext policy decision on December 14?

The labor market: The Fed’s biggest worry is the super-tight US labor market, and Friday’s jobs report isn’t likely to soothe any nerves.

The government report is expected to show the economy added another 200,000 positions in October — down from last month, but still a very solid number as demand for employment continues to outpace the supply of labor.

That means more inflation. Businesses have to pay higher wages to attract employees and are able to charge more for their goods and services. The Fed will be looking closely at hourly wage growth in the report. In September, wages rose by 5% from a year ago.

There is a possible upside: Another jobs report in December is expected ahead of the Fed meeting. If both reports show a downward trajectory in employment, that could be enough to placate Fed officials, even if the unemployment rate remains historically low.

Inflation data: Expect new data from two major indexes that measure the pace of inflation ahead of the next Federal Reserve meeting.

The Consumer Price Index (CPI) for October, which tracks changes in the prices of a fixed set of goods and services, is out on November 10.

Core CPI prices, which exclude oil and food, rose 0.6% in September month-over-month, matching August’s pace and coming in well above expectations of a 0.4% increase, not a great sign for the Fed. And analysts expect to see another large 0.5% increasein October.

The Fed will also get to see October data from its favored measure of inflation, Personal Consumption Expenditures (PCE), on December 1.

PCE reflects changes in the prices of goods and services purchased by consumers in the United States. The Fed believes the measure is more accurate than CPI because it accounts for a wider range of purchases from a broader range of buyers.

Housing: The housing market has been deeply impacted by the Fed’s efforts to fight inflation, and is one of the first areas of the economy to show signs of cooling.

The 30-year fixed-rate mortgage averaged 6.95% last week, up from 3.09% just a year ago, and elevated borrowing costs are leading to a decline in demand.

“The housing market was very overheated for the couple of years after the pandemic as demand increased and rates were low,” said Powell on Wednesday. “We do understand that that’s really where a very big effect of our policies is.”

October’s new and existing home sales numbers, due on November 18 and 23, will show the continued impact of that policy ahead of the next meeting.

The US economy is still standing strong in the face of rising interest rates, but things are softening much more quickly across the pond.

The United Kingdom will face hard economic times and elevated interest rates well into next year, officials warned this week.

The Bank of England raised interest rates by three-quarters of a percentage point on Thursday, the biggest hike in 33 years, as it attempts to fight soaring inflation.

But the bank also issued a stark warning. It said that economic output is already contracting and that it expects arecession to continue through the first half of 2024 “as high energy prices and materially tighter financial conditions weigh on spending.”

A two-year recession would be longer than the one that followed the 2008 global financial crisis, though the Bank of England said that any declines in GDP heading into 2024 would likely be relatively small.

The central bank also doesn’t think inflation will start to fall back until next year. That will require more interest rate hikes in the coming months, warned policymakers.

Elon Musk has been busy over at Twitter HQ. Aside from tweeting and deleting a conspiracy theory, he’s talked about implementing some big changes at his $44 billion acquisition. Here’s what’s happened so far:

Layoffs begin: Elon Musk began laying off Twitter employees on Friday morning, according to a memo sent to staff. The email sent Thursday evening notified employees that they will receive a notice by 12 p.m. ET Friday that informs them of their employment status.

The email added that “to help ensure the safety” of employees and Twitter’s systems, the company’s offices “will be temporarily closed and all badge access will be suspended.”

Twitter had around 7,500 employees prior to Musk’s takeover.

Several Twitter employees have already filed a class action lawsuit claiming that the layoffs violate the federal Worker Adjustment and Retraining Notification Act.

The WARN Act requires any company with over 100 employees to give 60 days’ written notice if it intends to cut 50 jobs or more at a “single site of employment.”

Consolidating strength: In less than a week since Musk acquired Twitter, the company’s C-suite appears to have almost entirely cleared out, through a mix of firings and resignations.

Twitter’s board of directors was also dissolved last week, according to a securities filing.

The company filing states that all previous members of Twitter’s board, including recently ousted CEO Parag Agrawal and chairman Bret Taylor, are no longer directors “in accordance with the terms of the merger agreement.” That makes Musk, according to the filing, “the sole director of Twitter.”

Cashing blue checks’ checks: Musk on Tuesday said he planned to charge $8 a month for Twitter’s subscription service, called “Twitter Blue,” with the promise to let anyone pay to receive a coveted blue check mark to verify their account. That’s a steep haircut from his original plan to charge users $19.99 a month to get or keep a verified account.

In a tweet, the world’s richest man used an expletive to describe his assessment of “Twitter’s current lords & peasants system for who has or doesn’t have a blue checkmark.” He added: “Power to the people! Blue for $8/month.”

Advertisers hit pause: Elon Musk wrote an open letter to advertisers just hours before cementing his acquisition of Twitter, explaining that he didn’t want the platform to become a “free-for-all hellscape.” But that attempt at reassuring the advertising industry, which makes up the vast majority of Twitter’s business, doesn’t appear to be working.

General Mills

(GIS), Mondelez International

(MDLZ), Pfizer

(PFE) and Audi

(AUDVF) have reportedly joined a growing list of companies hitting pause on their Twitter advertising in the wake of Musk’s acquisition.

LIVERPOOL, England — On the long picket line outside the gates of Liverpool’s Peel Port, rain-soaked dock workers warm themselves with cups of tea as they listen to 1980s pop.

Dozens of buses, cars and trucks honk in solidarity as they pass.

Dockers’ strikes are not new to Liverpool, nor is depravation. But this latest walk-out at Britain’s fourth-largest port is part of something much bigger, a great wave of public and private sector strikes taking place across the U.K. Railways, postal services, law courts and garbage collections are among the many public services grinding to a halt.

The immediate cause of the discontent, as elsewhere, is the rising cost of living. Inflation in the United Kingdom breached the 10 percent mark this year, with wages failing to keep pace.

But the U.K.’s economic woes long predate the current crisis. For more than a decade, Britain has been beset by weak economic growth, anaemic productivity, and stagnant private and public sector investment. Since 2016, its political leadership has been in a state of Brexit-induced flux.

Half a century after U.S. Secretary of State Henry Kissinger looked at the U.K.’s 1970s economic malaise and declared that “Britain is a tragedy,” the United Kingdom is heading to be the sick man of Europe once again.

The immediate cause of Liverpool dockers’ discontent that brought them to strike is the rising cost of living. | Christopher Furlong/Getty Images

Here in Liverpool, the “scars run very deep,” said Paul Turking, a dock worker in his late 30s. British voters, he added, have “been misled” by politicians’ promises to “level up” the country by investing heavily in regional economies. Conservatives “will promise you the world and then pull the carpet out from under your feet,” he complained.

“There’s no middle class no more,” said John Delij, a Peel Port veteran of 15 years. He sees the cost-of-living crisis and economic stagnation whittling away the middle rung of the economic ladder.

“How many billionaires do we have?” Delij asked, wondering how Britain could be the sixth-largest economy in the world with a record number of billionaires when food bank use is 35 percent above its pre-pandemic level. “The workers put money back into the economy,” he said.

What would they do if they were in charge? “Invest in affordable housing,” said Turking. “Housing and jobs.”

Falling behind

The British economy has been struck by particular turbulence over recent weeks. The cost of government borrowing soared in the wake of former PM Liz Truss’ disastrous mini-budget on September 23, with the U.K.’s central bank forced to step in and steady the bond markets.

But while the swift installation of Rishi Sunak, the former chancellor, as prime minister seems to have restored a modicum of calm, the economic backdrop remains bleak. Spending and welfare cuts are coming. Taxes are certain to rise. And the underlying problems cut deep.

U.K. productivity growth since the financial crisis has trailed that of comparator nations such as the U.S., France and Germany. As such, people’s median incomes also lag behind neighboring countries over the same period. Only Russia is forecast to have worse economic growth among the G20 nations in 2023.

In 1976, the U.K. — facing stagflation, a global energy crisis, a current account deficit and labor unrest — had to be bailed out by the International Monetary Fund. It feels far-fetched, but today some are warning it could happen again.

The U.K. is spluttering its way through an illness brought about in part through a series of self-inflicted wounds that have undermined the basic pillars of any economy: confidence and stability.

The political and economic malaise is such that it has prompted unwanted comparisons with countries whose misfortunes Britain once watched amusedly from afar.

“The existential risk to the U.K. … is not that we’re suddenly going to go off an economic cliff, or that the country’s going to descend into civil war or whatever,” said Jonathan Portes, professor of economics at King’s College London. “It’s that we will become like Italy.”

Portes, of course, does not mean a country blessed with good weather and fine food — but an economy hobbled by persistently low growth, caught in a dysfunctional political loop that lurches between “corrupt and incompetent right-wing populists” and “well-intentioned technocrats who can’t actually seem to turn the ship around.”

“That’s not the future that we want in the U.K,” he said.

Reviving the U.K.’s flatlining economy will not happen overnight. As Italy’s experience demonstrates, it’s one thing to diagnose an illness — another to cure it.

Experts speak of an unbalanced model heavily reliant upon Britain’s services sector and beset with low productivity, a result of years of underinvestment and a flexible labor market which delivers low unemployment but often insecure and low-paid work.

“We’re not investing in skills; businesses aren’t investing,” said Xiaowei Xu, senior research economist at the Institute for Fiscal Studies. “It’s not that surprising that we’re not getting productivity growth.”

But any attempt to address the country’s ailments will require its economic stewards to understand their underlying causes — and those stretch back at least to the first truly global crisis of the 21st century.

Crash and burn

The 2008 financial crisis hammered economies around the world, and the U.K. was no exception. Its economy shrunk by more than 6 percent between the first quarter of 2008 and the second quarter of 2009. Five years passed before it returned to its pre-recession size.

For Britain, the crisis in fact began in September 2007, a year before the collapse of Lehman Brothers, when wobbles in the U.S. subprime mortgage market sparked a run on the British bank Northern Rock.

The U.K. discovered it was particularly vulnerable to such a shock. Over the second half of the 20th century, its manufacturing base had largely eroded as its services sector expanded, with financial and professional services and real estate among the key drivers. As the Bank of England put it: “The interconnectedness of global finance meant that the U.K. financial system had become dangerously exposed to the fall-out from the U.S. sub-prime mortgage market.”

The crisis was a “big shock to the U.K.’s broad economic model,” said John Springford, from the Centre for European Reform. Productivity took an immediate hit as exports of financial services plunged. It never fully recovered.

“Productivity before the crash was basically, ‘Can we create lots and lots of debt and generate lots and lots of income on the back of this? Can we invent collateralized debt obligations and trade them in vast volumes?’” said James Meadway, director of the Progressive Economy Forum and a former adviser to Labour’s left-wing former shadow chancellor, John McDonnell.

A post-crash clampdown on City practises had an obvious impact.

“This is a major part of the British economy, so if it’s suddenly not performing the way it used to — for good reasons — things overall are going to look a bit shaky,” Meadway added.

The shock did not contain itself to the economy. In a pattern that would be repeated, and accentuated, in the coming years, it sent shuddering waves through the country’s political system, too.

The 2010 election was fought on how to best repair Britain’s broken economy. In 2009, the U.K. had the second-highest budget deficit in the G7, trailing only the U.S., according to the U.K. government’s own fiscal watchdog, the Office for Budget Responsibility (OBR).

The Conservative manifesto declared “our economy is overwhelmed by debt,” and promised to close the U.K.’s mounting budget deficit in five years with sharp public sector cuts. The incumbent Labour government responded by pledging to halve the deficit by 2014 with “deeper and tougher” cuts in public spending than the significant reductions overseen by former Conservative Prime Minister Margaret Thatcher in the 1980s.

The election returned a hung parliament, with the Conservatives entering into a coalition with the Liberal Democrats. The age of austerity was ushered in.

Austerity nation

Defenders of then-Chancellor George Osborne’s austerity program insist it saved Britain from the sort of market-led calamity witnessed this fall, and put the U.K. economy in a condition to weather subsequent global crises such as the COVID-19 pandemic and the fallout from the war in Ukraine.

“That hard work made policies like furlough and the energy price cap possible,” said Rupert Harrison, one of Osborne’s closest Treasury advisers.

Pointing to the brutal market response to Truss’ freewheeling economic plans, Harrison praised the “wisdom” of the coalition in prioritizing tackling the U.K.’s debt-GDP ratio. “You never know when you will be vulnerable to a loss of credibility,” he noted.

But Osborne’s detractors argue austerity — which saw deep cuts to community services such as libraries and adult social care; courts and prisons services; road maintenance; the police and so much more — also stripped away much of the U.K.’s social fabric, causing lasting and profound economic damage. A recent study claimed austerity was responsible for hundreds of thousands of excess deaths.

Under Osborne’s plan, three-quarters of the fiscal consolidation was to be delivered by spending cuts. With the exception of the National Health Service, schools and aid spending, all government budgets were slashed; public sector pay was frozen; taxes (mainly VAT) rose.

But while the government came close to delivering its fiscal tightening target for 2014-15, “the persistent underperformance of productivity and real GDP over that period meant the deficit remained higher than initially expected,” the OBR said. By his own measure, Osborne had failed, and was forced to push back his deficit-elimination target further. Austerity would have to continue into the second half of the 2010s.

Many economists contend that the fiscal belt-tightening sucked demand out of the economy and worsened Britain’s productivity crisis by stifling investment. “That certainly did hit U.K. growth and did some permanent damage,” said King’s College London’s Portes.

“If that investment isn’t there, other people start to find it less attractive to open businesses,” former Labour aide Meadway added. “If your railways aren’t actually very good … it does add up to a problem for businesses.”

A 2015 study found U.K. productivity, as measured by GDP per hour worked, was now lower than in the rest of the G7 by a whopping 18 percentage points.

“Frankly, nobody knows the whole answer,” Osborne said of Britain’s productivity conundrum in May 2015. “But what I do know is that I’d much rather have the productivity challenge than the challenge of mass unemployment.”

‘Jobs miracle’

Rising employment was indeed a signature achievement of the coalition years. Unemployment dropped below 6 percent across the U.K. by the end of the parliament in 2015, with just Germany and Austria achieving a lower rate of joblessness among the then-28 EU states. Real-term wages, however, took nearly a decade to recover to pre-crisis levels.

Economists like Meadway contend that the rise in employment came with a price, courtesy of Britain’s famously flexible labor market. He points to a Sports Direct warehouse in the East Midlands, where a 2015 Guardian investigation revealed the predominantly immigrant workforce was paid illegally low wages, while the working conditions were such that the facility was nicknamed “the gulag.”

The warehouse, it emerged, was built on a former coal mine, and for Meadway the symbolism neatly charts the U.K.’s move away from traditional heavy industry toward more precarious service sector employment. “It’s not a secure job anymore,” he said. “Once you have a very flexible labor market, the pressure on employers to pay more and the capacity for workers to bargain for more is very much reduced.”

Throughout the period, the Bank of England — the U.K.’s central bank — kept interest rates low and pursued a policy of quantitative easing. “That tends to distort what happens in the economy,” argued Meadway. QE, he said, is a “good [way of] getting money into the hands of people who already have quite a lot” and “doesn’t do much for people who depend on wage income.”

Meanwhile — whether necessary or not — the U.K.’s austerity policies undoubtedly worsened a decades-long trend of underinvestment in skills and research and development (Britain lags only Italy in the G7 on R&D spending). At British schools, there was a 9 percent real terms fall in per-pupil spending between 2009 and 2019, according to the Institute for Fiscal Studies’ Xu. “As countries get richer, usually you start spending more on education,” Xu noted.

Two senior ministers in the coalition government — David Gauke, who served in the Treasury throughout Osborne’s tenure, and ex-Lib Dem Business Secretary Vince Cable — have both accepted that the government might have focused more on higher taxation and less on cuts to public spending. But both also insisted the U.K had ultimately been correct to prioritize putting its public finances on a sounder footing.

It was February 2018 before Britain finally achieved Osborne’s goal of eliminating the deficit on its day-to-day budget.

Austerity was coming to an end, at last. But Osborne had already left the Treasury, 18 months earlier — swept away along with Cameron in the wake of a seismic national uprising.

***

David Cameron had won the 2015 election outright, despite — or perhaps because of — the stringent spending cuts his coalition government had overseen, more of which had been pledged in his 2015 manifesto. Also promised, of course, was a public vote on Britain’s EU membership.

The reasons for the leave vote that followed were many and complex — but few doubt that years of underinvestment in poorer parts of the U.K. were among them.

Regardless, the 2016 EU referendum triggered a period of political acrimony and turbulence not seen in Westminster for generations. With no pre-agreed model of what Brexit should actually entail, the U.K.’s future relationship with the EU became the subject of heated and protracted debate. After years of wrangling, Britain finally left the bloc at the end of January 2020, severing ties in a more profound way than many had envisaged.

While the twin crises of COVID and Ukraine have muddled the picture, most economists agree Brexit has already had a significant impact on the U.K. economy. The size of Britain’s trade flows relative to GDP has fallen further than other G7 countries, business investment growth trails the likes of Japan, South Korea and Italy, and the OBR has stuck by its March 2020 prediction that Brexit would reduce productivity and U.K. GDP by 4 percent.

Perhaps more significantly, Brexit has ushered in a period of political instability. As prime ministers come and go (the U.K. is now on its fifth since 2016), economic programs get neglected, or overturned. Overseas investors look on with trepidation.

“The evidence that the referendum outcome, and the kind of uncertainty and change in policy that it created, have led to low investment and low growth in the U.K. is fairly compelling,” said professor Stephen Millard, deputy director at the National Institute of Economic and Social Research.

Beyond the instability, the broader impact of the vote to leave remains contentious.

Portes argued — as many Remain supporters also do — that much harm was done by the decision to leave the EU’s single market. “It’s the facts, not the uncertainty that in my view is responsible for most of the damage,” he said.

Brexit supporters dismiss such claims.

“It’s difficult statistically to find much significant effect of Brexit on anything,” said professor Patrick Minford, founder member of Economists for Brexit. “There’s so much else going on, so much volatility.”

Minford, an economist favored by ex-PM Truss, acknowledged that “Brexit is disruptive in the short run, so it’s perfectly possible that you would get some short-run disruption.” But he added: “It was a long-term policy decision.”

Where next?

Plenty of economists can rattle off possible solutions, although actually delivering them has thus far evaded Britain’s political class. “It’s increasing investment, having more of a focus on the long-term, it’s having economic strategies that you set out and actually commit to over time,” says the IFS’ Xu. “As far as possible, it’s creating more certainty over economic policy.”

But in seeking to bring stability after the brief but chaotic Truss era, new U.K. Chancellor Jeremy Hunt has signaled a fresh period of austerity is on the way to plug the latest hole in the nation’s finances. Leveling Up Secretary Michael Gove told Times Radio that while, ideally, you wouldn’t want to reduce long-term capital investments, he was sure some spending on big projects “will be cut.”

This could be bad news for many of the U.K.’s long-awaited infrastructure schemes such as the HS2 high-speed rail line, which has been in the works for almost 15 years and already faces a familiar mix of local resistance, vested interests, and a sclerotic planning system.

“We have a real problem in the sense that the only way to really durably raise productivity growth for this country is for investments to pick up,” said Springford, from the Centre for European Reform. “And the headwinds to that are quite significant.”

For dock workers at Liverpool’s Peel Port, the prospect of a fresh round of austerity amid a cost-of-living crisis is too much to bear. “Workers all over this country need to stand up for themselves and join a union,” insisted Delij.

For him, it’s all about priorities — and the arguments still echo back to the great crash of 15 years ago. “They bailed the bankers out in 2007,” he said, “and can’t bail hungry people out now.”

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Liquidity Is In The Driver Seat

By far, one of the most important factors in any market is liquidity — which can be defined in many different ways. In this piece, we cover some ways to think about global liquidity and how it impacts bitcoin.

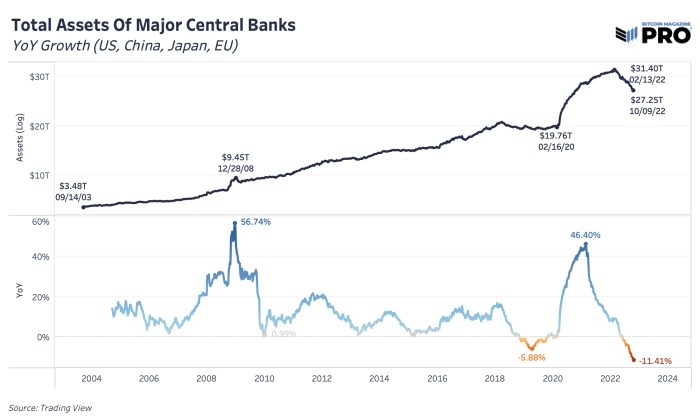

One high-level view of liquidity is that of central banks’ balance sheets. As central banks have become the marginal buyer of their own sovereign debts, mortgage-backed securities and other financial instruments, this has supplied the market with more liquidity to buy assets further up the risk curve. A seller of government bonds is a buyer of a different asset. When the system has more reserves, money, capital, etc. (however one wants to describe it), they have to go somewhere.

In many ways that has led to one of the largest rises in asset valuations globally over the last 12 years, coinciding with the new era of quantitative easing and debt monetization experiments. Central bank balance sheets across the United States, China, Japan and the European Union reached over $31 trillion earlier this year, which is nearly 10X from the levels back in 2003. This was already a growing trend for decades, but the 2020 fiscal and monetary policies took balance sheets to record levels in a time of global crisis.

Since earlier this year, we’ve seen a peak in central bank assets and a global attempt to wind down these balance sheets. The peak in the S&P 500 index was just two months prior to all of the quantitative tightening (QT) efforts we’re watching play out today. Although not the only factor that drives price and valuations in the market, bitcoin’s price and cycle has been affected in the same way. The annual rate-of-change peak in major central banks’ assets happened just weeks prior to bitcoin’s first push to new all-time highs around $60,000, back in March 2021. Whether it’s the direct impact and influence of central banks or the market’s perception of that impact, it’s been a clear macro driving force of all markets over the last 18 months.

There is a global attempt to wind down central bank balance sheets

At a market cap of just fractions of global wealth, bitcoin has faced the liquidity steamroller that’s hammered every other market in the world. If we use the framework that bitcoin is a liquidity sponge (more so than other assets) — soaking in all of the excess monetary supply and liquidity in the system in times of crisis expansion — then the significant contraction of liquidity will cut the other way. Coupled with bitcoin’s inelastic illiquid supply profile of 77.15% with a vast number of HODLers of last resort, the negative impact on price is magnified much more than other assets.

One of the potential drivers of liquidity in the market is the amount of money in the system, measured as global M2 in USD terms. M2 money supply includes cash, checking deposits, savings deposits and other liquid forms of currency. Both cyclical expansions in global M2 supply have happened during the expansions of global central bank assets and expansions of bitcoin cycles.

We view bitcoin as a monetary inflation hedge (or liquidity hedge) rather than one against a “CPI” (or price) inflation hedge. Monetary debasement, more units in the system over time, has driven many asset classes higher. Yet, bitcoin is by far the best-designed asset in our view and one of the best-performing assets to counteract the future trend of perpetual monetary debasement, money supply expansion and central bank asset expansion.

It’s unclear how long a material reduction in the Fed’s balance sheet can actually last. We’ve only seen an approximate 2% reduction from a $8.96 trillion balance sheet problem at its peak. Eventually, we see the balance sheet expanding as the only option to keep the entire monetary system afloat, but so far, the market has underestimated how far the Fed has been willing to go.

The lack of viable monetary policy options and the inevitability of this perpetual balance sheet expansion is one of the strongest cases for bitcoin’s long-run success. What else can central banks and fiscal policy makers do in future times of recession and crisis?

This is an opinion editorial by The Bitcoin General, a Bitcoin proponent, seeker of truth, respecter of individuality and appreciator of freedom.

For decades, the legacy financial establishment has capitalized on its position to manage wealth for the vast majority of investors. On January 3, 2009, Satoshi Nakamotodid something revolutionary: he mined the genesis block of Bitcoin. After witnessing the scandalous events of the great financial crash of 2008, enough was enough. Big banks engaged in reckless conduct with predatory lending practices and incessant greed that drove the world into a global recession. Then came the massive corporate bailouts via the money-printer.

Enter Bitcoin.

Bitcoin forged a new path forward. It was a new opportunity to pursue wealth and financial independence for the commoner. The grip of the financial elites was slowly loosened, as a new digital asset class was created to loosen the grips of government-controlled domestic money.

Bitcoin is “the money of the people” because no central bank, or government controls it. In fact, many governments are so threatened by it, many have imposed heavy restrictions on its use, or have even outright banned it.

Bitcoin is a vehicle of financial independence. It creates more financial freedom to the individual, and keeps government overreach in-check with its robust network. The resistance of the legacy financial and elite establishment only galvanized this point further. The IMF’s disapproval of Bitcoin is very telling. Bitcoin is a threat to the status quo, and its strongest proponents know it.

Change is on the horizon but it’s slow. The legacy financial industry mostly remains critical of bitcoin. Because of the benefits of self-custody, bitcoin eliminates the need for these legacy institutions, or at least reduces their role. Thanks to Nakamoto, nearly every human being on this earth can now exercise the option of self-custody of their wealth and savings.

Of course, one would be remiss in not acknowledging the learning curve of Bitcoin. Those who are tech-savvy will pick it up more quickly. But one can also dive in as deep as they are comfortable doing. If running a node seems too complex, it doesn’t eliminate the options available to use bitcoin as a digital media of exchange. When it comes to bitcoin, investors need to assess their own risk tolerance and time preference and proceed accordingly. For some, the highs and lows of bitcoin might prove to be too much, and for others, not so much.

One primary benefit is freedom. Freedom to purchase, hold or transfer holdings anywhere one desires in the world in record time at a minimal cost. Bitcoin is freedom from the shackles of big banks who work on their time, set their own non-negotiable exorbitant fees.

The sad reality is, the pursuit of financial sovereignty has become a punishable crime in many parts of the world. We saw this in Canada last year when prime minister Justin Trudeau froze bank accounts of citizens who didn’t align with his political beliefs. This was a textbook definition of government overreach.

Of course, it should go without saying that all citizens should pay their income taxes and not use a digital asset class to evade these obligations (one should never condone breaking the law). But choosing the path of financial independence through Nakamoto’s ingenious digital innovation is an option that can no longer be ignored. For those who no longer want to trust the legacy system with their hard-earned money, human ingenuity has blazed a new trail.

The big banks have monopolized money for long enough. They have profited, gamed the system, defrauded the masses and manipulated their way to the top all in the name of greed. Seeing top financial executives outwardly attack Bitcoin proves even further that they see it as a threat. A remote villager in rural Africa can now own bitcoin with as little as a $50 phone. I have even heard of some remote communities using good old fashioned hand-written paper ledgers to buy Bitcoin where the internet access was limited.

And the beauty of it all is bitcoin’s deflationary nature. It is the antithesis of the fiat system which is perpetually inflationary. This is not to say that market dips will not affect bitcoin. At the time of this writing, bitcoin is experiencing a significant dip that has created great amounts of FUD. To win in bitcoin, is to run the marathon. One HODLer once described it as a “head-game that challenges you at every level.” Indeed, the dips will impact some of us. The volatility in bitcoin will test the nerves of many, and possibly even force them to reassess their risk tolerance. There is no advisor to blame, no stock broker to ream out, no fund manager to fire. One must take the time to learn the protocol, understand its potential and jump into the rollercoaster. We’ve seen some extreme highs and some stomach-turning lows. Those with more aversion to risk may need to consider not being leveraged on bitcoin. Don’t be under any illusions — bitcoin is still a risk asset in 2022. But, given the current global financial situation today, it appears to be outperforming the legacy stock market on a whole, as this unprecedented bear market trend continues.

A seasoned investor with years in the trenches once said, “You need to be ready to take a punch. The punch may never come, but you’ll be in a much better psychological position if you are ready for it.” HODLing takes balls.

As simple as it sounds, it’s more than just a linear buy and hold strategy. We need to do our homework. We need to educate ourselves, and learn the protocol and all its potential. Study the critics, watch the debates and learn the arguments of the naysayers. The point is not to agree with them. The point is to educate oneself to know if bitcoin is the right investment tool for them.

Central bank manipulation is at an all-time high. The recent U.K. bond market multi-billion-dollar government buyback is just one example. Fiat values will continue to decline. Central banks will continue to debase domestic currencies and, because most of us are paid with this currency, they will continue to devalue our personal net worth. Policy makers will continue to improvise and manipulate the system. Remember, they still get their weekly paychecks no matter what so they have no real skin-in-the-game. Bitcoin is a break from tradition; a tradition that has essentially let us all down.

This is a guest post by The Bitcoin General. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This story is part of CNN Business’ Nightcap newsletter. To get it in your inbox, sign up for free, here.

New York CNN Business

—

The Nobel in economics is sort of the step-cousin of the Nobel family.

It came about nearly 70 years after its literature and sciences counterparts, in 1969, and is technically called the “Sveriges Riksbank Prize in Economic Sciences.” It is awarded by the Swedish central bank, in honor of the namesake renaissance man Alfred Nobel who established the prizes.

Some scholars really dislike the economics prize, including one of Nobel’s own descendants, who dismissed it as a “PR coup by economists.”

But hey, it still comes with a cash prize. And it’s also pretty useful in reminding the world that economics as an academic field is, frankly, a barely understood hodge-podge of studies that is constantly evolving and so variable it’s almost useless outside of academia. (And I mean that with the utmost respect to economists, who, not unlike journalists, knew what they were doing when they chose their life of suffering.)

Here’s the thing: Ben Bernanke, the former Federal Reserve chairman who guided the US economy through the 2008 financial crisis and subsequent recession, was awarded the Nobel in economics along with two other economists, Douglas Diamond and Philip Dybvig. (Congrats to all the winners, with apologies to Doug and Phil, who will forever be referred to in headlines about the Nobel as “and two other economists.”)

Bernanke, who previously taught at Princeton and earned his Ph.D from MIT, received the award for his research on the Great Depression. In short, his work demonstrates that banks’ failures are often a cause, not merely a consequence, of financial crises.

That was groundbreaking when he published it in 1983. Today, it’s conventional wisdom.

WHY IT MATTERS

The timing is everything here. The Nobel committee has been known to play politics (see: that time Barack Obama was awarded the Nobel Peace Prize after being in office for just eight months). And right now, it is using its spotlight to call attention to the high-stakes gamble playing out at central banks around the world, most notably the Fed.

The rapid run-up in interest rates, led by the US central bank, is causing markets around the world to go haywire. And it’s especially bad news for emerging economies.

Monetary tightening — especially when it is aggressive and synchronized across major economies — could inflict worse damage globally than the 2008 financial crisis and the 2020 pandemic, a United Nations agency warned earlier this month. It called the Fed’s policy “imprudent gamble” with the lives of those less fortunate.

LESSONS FROM HISTORY

On Monday, Diamond, one of the three newly minted Nobel laureates, acknowledged that the rate moves around the world were causing market instability.

But he believes the system is more resilient than it used to be because of hard lessons learned from the 2008 crash, my colleague Julia Horowitz reports.

“Recent memories of that crisis and improvements in regulatory policies around the world have left the system much, much less vulnerable,” Diamond said.

Let’s hope he’s right.

Oh hey, speaking of the Fed inflicting pain: We’re about to see big job losses, according to Bank of America.

Under the rate hikes imposed by Jay Powell & Co, the US economy could see job growth cut in half during the fourth quarter of this year. Early next year, the bank expects to see losses of about 175,000 jobs a month.

The litigation between Elon Musk and Twitter is officially on hold. The two sides now have until October 28 to work out a deal or once again gear up for a courtroom battle.

The big question now is all about the money.

Here’s the deal: Not even the world’s richest person has this kind of cash just lying around. Musk’s wealth is tied up in Tesla stock, which he can’t easily offload for a whole bunch of reasons. He needs to borrow the money, which means he’s got to get banks to pony up.

By most accounts, he’ll be able to make it happen. But the Twitter deal is a harder pitch to make now than it was back in April, when Musk said he’d lined up more than $46 billion in financing, including two debt commitment letters from Morgan Stanley and other unnamed financial institutions, my colleague Clare Duffy writes.

Musk has spent the past several months trashing Twitter as he sought to renege on his offer. Meanwhile, tech stocks have been hammered, ad revenues are declining, and the global economy has inched closer to a recession, sapping investor appetite for risk.

Musk’s legal team said last week the banks that had committed debt financing previously were “working cooperatively to fund the close.”

Twitter is, understandably, skeptical, given the many curve balls Musk has thrown at them since he got involved with the company earlier this year. The company raised concerns last week that a representative for one of the banks testified that Musk had not yet sent a borrowing notice and “has not otherwise communicated to them that he intends to close the transaction, let alone on any particular timeline.”

What’s Musk’s endgame?

No one knows, perhaps least of all Musk. But many legal experts following the case say Musk understood he’d likely lose at trial and then be forced to buy Twitter anyway. He’d rather buy the entire company than be deposed by Twitter’s lawyers and do further damage to Twitter in a trial.

And the banks may not be able to walk away even if they want to.

“The only way they could get out of it is to claim a material adverse effect and that Twitter has changed so much since they agreed to the deal that they no longer want to finance the deal,” said George Geis, professor of strategy at the UCLA Anderson School of Management.

Even if the banks succeeded there, Musk may not be off the hook. The judge in the case could rule that Musk was at fault for the financing falling through — not a far-fetched notion after all the trash-talking — and order him to sue Morgan Stanley to provide the funds or close the deal without it.

Bottom line, it seems like Musk will end up owning Twitter one way or another. And given his only vague musings about what he’d actually do with it, there are a whole host of unknowns lurking in Twitter’s future.

Enjoying Nightcap? Sign up and you’ll get all of this, plus some other funny stuff we liked on the internet, in your inbox every night. (OK, most nights — we believe in a four-day work week around here.)

Pension funds are designed to be dull. Their singular goal — earning enough money to make payouts to retirees — favors cool heads over brash risk takers.

But as markets in the United Kingdom went haywire last week,hundreds ofBritish pension fund managers found themselves at the center of a crisis that forced the Bank of England to step in to restore stability and avert a broader financial meltdown.

All it took was one big shock. Following finance minister Kwasi Kwarteng’s announcement on Friday, Sept. 23 of plans to ramp up borrowing to pay for tax cuts, investors dumped the pound and UK government bonds, sending yields on some of that debt soaring at the fastest rate on record.

The scale of the tumult put enormous pressure on many pension funds by upending an investing strategy that involves the use of derivatives to hedge their bets.

As the price of government bonds crashed, the funds were asked to pony up billions of pounds in collateral. In a scramble for cash, investment managers were forced to sell whatever they could — including, in some cases, more government bonds. That sent yields even higher, sparking another wave of collateral calls.

“It started to feed itself,” said Ben Gold, head of investment at XPS Pensions Group, a UK pensions consultancy. “Everyone was looking to sell and there was no buyer.”

The Bank of England went into crisis mode. After working through the night of Tuesday, Sept. 27, it stepped into the market the next day with a pledge to buy up to £65 billion ($73 billion) in bonds if needed. That stopped the bleeding and averted what the central bank later told lawmakers was its worst fear: a “self-reinforcing spiral” and “widespread financial instability.”

In a letter to the head of the UK Parliament’s Treasury Committee this week, the Bank of England said that if it hadn’t interceded, a number of funds would have defaulted, amplifying the strain on the financial system. It said its intervention was essential to “restore core market functioning.”

Pension funds are now racing to raise money to refill their coffers. Yet there are questions about whether they can find their footing before the Bank of England’s emergency bond-buying is due to end on Oct. 14. And for a wider range of investors, the near-miss is a wake-up call.

For the first time in decades, interest rates are rising quickly around the world. In that climate, markets are prone to accidents.

“What the previous two weeks have told you is there can be a lot more volatility in markets,” said Barry Kenneth, chief investment officer at the Pension Protection Fund, which manages pensions for employees of UK companies that become insolvent. “It’s easy to invest when everything’s going up. It’s a lot more difficult to invest when you’re trying to catch a falling knife, or you’ve got to readjust to a new environment.”

The first signs of trouble appeared among fund managers who focus on so-called “liability-driven investment,” or LDI, for pensions. Gold said he started to receive messages from worried clients over the weekend of Sept. 24-25.

LDI is built on a straightforward premise: Pensions need enough money to pay what they owe retirees well into the future. To plan for payouts in 30 or 50 years, they buy long-dated bonds, while purchasing derivatives to hedge these bets. In the process, they have to put up collateral. If bond yields rise sharply, they are asked to put up even more collateral in what’s known as a “margin call.” This obscure corner of the market has grown rapidly in recent years, reaching a valuation of more £1 trillion ($1.1 trillion), according to the Bank of England.

When bond yields rise slowly over time, it’s not a problem for pensions deploying LDI strategies, and actually helps their finances. But if bond yields shoot up very quickly, it’s a recipe for trouble. According to the Bank of England, the move in bond yields before it intervened was “unprecedented.” The four-day move in 30-year UK government bonds was more than twice what was seen during the highest-stress period of the pandemic.

“The sharpness and the viciousness of the move is what really caught people out,” Kenneth said.

The margin calls came in — and kept coming. The Pension Protection Fund said it faced a £1.6 billion call for cash. It was able to pay without dumping assets, but others were caught off guard, and were forced into a fire sale of government bonds, corporate debtand stocks to raise money. Gold estimated that at least half of the 400 pension programs that XPS advises faced collateral calls, and that across the industry, funds are now looking to fill a hole of between £100 billion and £150 billion.

“When you push such large moves through the financial system, it makes sense that something would break,” said Rohan Khanna, a strategist at UBS.

When market dysfunction sparks a chain reaction, it’s not just scary for investors. The Bank of England made clear in its letter that the bond market rout “may have led to an excessive and sudden tightening of financing conditions for the real economy” as borrowing costs skyrocketed. For many businesses and mortgage holders, they already have.

So far, the Bank of England has only bought £3.8 billion in bonds, far less than it could have purchased. Still, the effort has sent a strong signal. Yields on longer-term bonds have dropped sharply, giving pension funds time to recoup — though they’ve recently started to rise again.

“What the Bank of England has done is bought time for some of my peers out there,” Kenneth said.

Still, Kenneth is concerned that if the program ends next week as scheduled, the task won’t be complete given the complexity of many pension funds. Daniela Russell, head of UK rates strategy at HSBC, warned in a recent note to clients that there’s a risk of a “cliff-edge,” especially since the Bank of England is moving ahead with previous plans to start selling bonds it bought during the pandemic at the end of the month.

“It might be hoped that the precedent of BoE intervention continues to provide a backstop beyond this date, but this may not be sufficient to prevent a renewed vigorous sell-off in long-dated gilts,” she wrote.

As central banks jack up interest rates at the fastest clip in decades, investors are nervous about the implications for their portfolios and for the economy. They’re holding more cash, which makes it harder to execute trades and can exacerbate jarring price moves.

That makes a surprise event more likely to cause massive disruption, and the specter of the next shocker looms. Will it be a rough batch of economic data? Trouble at a global bank? Another political misstep in the United Kingdom?

Gold said the pension industry as a whole is better prepared now, though he concedes it would be “naive” to think there couldn’t be another bout of instability.

“You would need to see yields rise more quickly than we saw this time,” he said, noting the larger buffers funds are now amassing. “It would require something of absolutely historic proportions for that not to be enough, but you never know.”

A version of this story first appeared in CNN Business’ Before the Bell newsletter. Not a subscriber? You can sign up right here. You can listen to an audio version of the newsletter by clicking the same link.

New York CNN Business

—

The global bond market is having a historically awful year.

The yield on the 10-year US Treasury bond, a proxy for borrowing costs, briefly moved above 4% on Wednesday for the first time in 12 years. That’s a bad omen for Wall Street and Main Street.

What’s happening: This hasn’t been a pretty year for US stocks. All three major indexes are in a bear market, down more than 20% from recent highs, and analysts predict more pain ahead. When things are this bad, investors seek safety in Treasury bonds, which have low returns but are also considered low-risk (As loans to the US government, Treasury notes are seen as a safe bet since there is little risk they won’t be paid back).

But in 2022’s topsy-turvy economy, even that safe haven has become somewhat treacherous.

Bond returns, or yields, rise as their prices fall. Under normal market conditions, a rising yield should mean that there’s less demand for bonds because investors would rather put their money into higher-risk (and higher-reward) stocks.

Instead markets are plummeting, and investors are flocking out of risky stocks, but yields are going up. What gives?

Blame the Fed. Persistent inflation has led the Federal Reserve to fight back by aggressively hiking interest rates, and as a result the yields on US Treasury bonds have soared.

So while we’d normally see a rising 10-year yield as a signal that US investors have a rosy economic outlook, that isn’t the case this time. Gloomy investors are predicting more interest rate hikes and a higher chance of recession.

What it means: Portfolios are aching. Vanguard’s $514.5 billion Total Bond Market Index, the largest US bond fund, is down more than 15% so far this year. That puts it on track for its worst year since it was created in 1986. The iShares 20+ Year Treasury bond fund

(TLT) (TLT) is down nearly 30% for the year.

Stock investors are also nervously eyeing Treasuries. High yields make it more expensive for companies to borrow money, and that extra cost could lower earnings expectations. Companies with significant debt levels may not be able to afford higher financing costs at all.

Main Street doesn’t get a break, either. An elevated 10-year Treasury return means more expensive loans on cars, credit cards and even student debt. It also means higher mortgage rates: The spike has already helped push the average rate for a 30-year mortgage above 6% for the first time since 2008.

Going deeper: Still, investors are more nervous about the immediate future than the longer term. That’s spurred an inverted yield curve – when interest rates on short-term bonds move higher than those on long-term bonds. The inverted yield curve is a particularly ominous warning sign that has correctly predicted almost every recession over the past 60 years.

The curve first inverted in April, and then again this summer. The two-year treasury yield has soared in the last week, and now hovers above 4.3%, deepening that gap.

On Monday, a team at BNP Paribas predicted that the inverted gap between the two-year and 10-year Treasury yields could grow to its largest level since the early 1980s. Those years were marked by sticky inflation, interest rates near 20% and a very deep recession.

What’s next: The bond market may face fresh volatility on Friday with the release of the Federal Reserve’s favored inflation measure, the Personal Consumption Expenditure Price Index for August. If the report comes in above expectations, expect bond yields to move even higher.

The Bank of England held an emergency intervention to maintain economic stability in the UK on Wednesday. The central bank said it would buy long-dated UK government bonds “on whatever scale is necessary” to prevent a market crash.

Investors around the globe have been dumping the British pound and UK bonds since the government on Friday unveiled a huge package of tax cuts, spending and increased borrowing aimed at getting the economy moving and protecting households and businesses from sky-high energy bills this winter, reports my colleague Mark Thompson.

Markets fear the plan will drive up already persistent inflation, forcing the Bank of England to push interest rates as high as 6% next spring, from 2.25% at present. Mortgage markets have been in turmoil all week as lenders have struggled to price their loans. Hundreds of products have been withdrawn.

“This repricing [of UK assets] has become more significant in the past day — and it is particularly affecting long-dated UK government debt,” the central bank said in its statement.

“Were dysfunction in this market to continue or worsen, there would be a material risk to UK financial stability. This would lead to an unwarranted tightening of financing conditions and a reduction of the flow of credit to the real economy.”

Many final salary, or defined-benefit, pension funds were particularly exposed to the dramatic sell-off in longer dated UK government bonds.

“They would have been wiped out,” said Kerrin Rosenberg, UK chief executive of Cardano Investment.

The central bank said it would buy long-dated UK government bonds until October 14.

Steep drops in bond prices may be signaling doom and gloom for the economy, but some analysts say short-term bonds are still looking more attractive than equities right now.

“Record low yields have kept fixed income in the shadow of equities for decades,” said analysts at BNY Mellon Wealth Management in a research note. “But the aggressive shift in Fed policy is beginning to change this.”

Central banks around the globe have responded to elevated inflation by hiking interest rates– and bond yields have increased alongside them. The two-year US Treasury bond is currently yielding nearly 4%. That’s still a relatively low return, but better than the S&P 500’s dividend yield of around 1.7%.

“For the first time in several years, bonds are attractive investment options. In addition to providing diversification versus equities…you now get paid for owning them,” wrote Barry Ritholtz of Ritholtz Wealth Management on Wednesday.

Consider the alternative: the S&P is down more than 20% year to date.

The US Bureau of Economic Analysis releases its third estimate for Q2 GDP and US weekly jobless claims.

According to the Financial Stability Board (FSB), a global financial standard-setter, most of the cryptocurrency market should be subject to the same tough rulebook that governs traditional finance.

The FSB, which was born in the wake of the 2008 financial meltdown to stave off further shocks, will propose the plan to rein in crypto to finance ministers and central bankers from the Group of 20 industrialized countries gathering in Washington next week, the plan’s chief architect, Steven Maijoor, told POLITICO.

“A lot of the activities in crypto assets and crypto assets markets resemble activities in the traditional financial system and therefore we take the approach: Same activity, same risk, same regulation,” Maijoor, who sits on the Dutch central bank’s governing board and oversees banking supervision, said in Prague in early September.

The move is set to put major crypto trading platforms on red alert, coming as the U.S. Securities and Exchange Commission seeks to impose securities regulation on cryptocurrencies and as the EU prepares its own rules for digital markets.

More broadly, the FSB’s work on digital assets is likely to act as a cold shower for crypto currencies that seek to expand their services without complying with regulations.

Regulators fear the lack of investor safeguards could see volatility in cryptocurrency markets spilling over into the traditional finance sector, as banks and money managers venture into the market.

Some $2 trillion of the market’s value has evaporated since its highs of November last year, triggering corporate collapses and exposing scams that left millions of crypto investors penniless. Risks within the crypto markets are still contained. But that could quickly change and threats could spill over to financial markets from various channels, according to the European Securities and Markets Authority.

Maijoor will present G20 policymakers with draft recommendations that he’s been developing with a team ofglobal regulators within the FSB since April with the view of securing financial stability as crypto goes mainstream. Countries around the world will need to decide whether new rules are needed for novel arrivals within the crypto market, such as digital wallets. The rest should be captured by new or existing financial rules.

“This is not only related to securities,” said the 58-year-old, who used to lead the EU’s securities regulator before getting a job at De Nederlandsche Bank. “There are also already some crypto activities that are captured by anti-money laundering laws and regulations and we can observe that also, in that case, there is non-compliant behavior.”

The example of companies skirting around dirty money safeguards is an easy one for the Dutchman to give. His central bank in late April fined the world’s biggest crypto exchange, Binance, €3 million for offering services to Dutch citizens without having cleared the required Dutch safeguards against dirty money — gaining a competitive advantage against its rivals. Binance objected to the fine in June.

The Financial Stability Oversight Council, chaired by U.S. Treasury Secretary Janet Yellen, said the crypto industry needs to be brought to heel in several areas | Alex Wong/Getty Images

Ministers and governors will also get updated recommendations on how to regulate global stablecoins, digital tokens that are tied to national currency or a reserve of financial products to keep their value steady. The stablecoin update is separate from the crypto recommendations and came in response to Facebook’s failed bid to introduce a virtual currency for some 2.9 billion social media users around the world.

Maijoor’s work will be subject to consultation, so companies and countries will be able to suggest changes to what will become the global blueprint for supervising the market.

Locking horns

The recommendations could embolden U.S. banking and markets regulators, which are increasingly taking the position that digital asset trading platforms and brokerages should follow existing regulations.

The Financial Stability Oversight Council, which is chaired by U.S. Treasury Secretary Janet Yellen and counts SEC Chair Gary Gensler and the heads of other federal agencies among its members, on Monday released a report that identified several areas where the crypto industry needs to be brought to heel.

“Crypto cannot exist outside of our public policy frameworks. That’s regardless of what [Bitcoin’s pseudonymous creator] Satoshi Nakamoto might have initially thought, or what market participants might say today,” Gensler said during Monday’s FSOC meeting.

Ripple and Coinbase, both major crypto exchanges that have locked horns with Gensler, will be hoping for a different outcome that involves new rules.

Coinbase has argued that crypto assets are more akin to commodities and that the SEC classifying them as securities is like putting a straitjacket on how the market could develop, especially considering those rules were developed in the 1930s. The Commodity Futures Trading Commission would be a far better fit, according to the exchange.

“I think it is reasonable to assume that none of the authors who drafted these securities statutes from the 1930s … did so while thinking of a day when a decentralized, cryptographically-based, automated financial instrument would be adopted en masse by millions of people in the United States and around the world,” Coinbase’s chief policy officer, Faryar Shirzad, wrote in a blog in July.

Sam Sutton contributed reporting from New York.

This article is part of POLITICO Pro

The one-stop-shop solution for policy professionals fusing the depth of POLITICO journalism with the power of technology

A week ago, the Bank of England took a stab in the dark. It raised interest rates by a relatively modest half a percentage point to tackle inflation. It couldn’t know the scale of the storm that was about to break.

Less than 24 hours later, the government of new UK Prime Minister Liz Truss unveiled its plan for the biggest tax cuts in 50 years, going all out for economic growth but blowing a huge hole in the nation’s finances and its credibility with investors.

The pound crashed to a record low against the US dollar on Monday after UK finance minister Kwasi Kwarteng doubled-down on his bet by hinting at more tax cuts to come without explaining how to pay for them. Bond prices collapsed, sending borrowing costs soaring, sparking mayhem in the mortgage market and pushing pension funds to the brink of insolvency.

Financial markets were already in a febrile state because of the rising risk of a global recession and the gyrations caused by three outsized rate increases from a US central bank on the warpath against inflation. Into that “pressure cooker” stumbled the new UK government.

“You need to have strong, credible policies, and any policy missteps are punished,” said Chris Turner, global head of markets at ING.