The Imagine America Foundation (IAF), a leading nonprofit dedicated to supporting students pursuing career education, is proud to announce Ambassador Education Solutions as a Gold Level Sponsor for the 2025-2026 academic year.

NAPLES, Fla., September 16, 2025 (Newswire.com)

– Ambassador Education Solutions, a trusted provider of course materials and content integration for career colleges and postsecondary institutions, joins IAF in its mission to promote access, affordability, and success in career-focused education. This sponsorship reflects Ambassador’s ongoing commitment to empowering students and institutions through innovative learning solutions.

“We are thrilled to welcome Ambassador Education Solutions as a Gold Level Sponsor,” said Bob Martin, President and CEO of the Imagine America Foundation. “Their support helps us expand scholarship opportunities, enhance student services, and strengthen our outreach to schools nationwide.”

As a Gold Level Sponsor, Ambassador will play a key role in supporting IAF’s scholarship and award programs, including the Imagine America High School Scholarship, Adult Skills Education Program (ASEP), and Military Award Program (MAP). These initiatives have helped more than 180,000 students pursue their educational goals since the Foundation’s inception.

“We are excited to further our partnership with the Imagine America Foundation,” said Marc Konesco, Senior Vice President of Sales at Ambassador Education Solutions and IAF Board Member. “This collaboration reinforces our commitment to delivering impactful learning experiences and supporting students every step of the way. It presents a meaningful opportunity for us to give back and help shape the future of career education.”

For more information about the Imagine America Foundation and its sponsors, visit www.imagine-america.org.

After winning nearly $500,000 on a $5 sports bet, a New Jersey financial adviser said he is planning to follow some of the advice he gives to clients and put the money to good use.

Travis Dufner, a 32-year-old adviser with Millstone Financial Group in Millstone, N.J., is the bettor who has stepped forward to say he won the $489,378.01 parlay payoff. The wager involved picking 14 players who would score a touchdown over the holiday weekend’s NFL games.

This episode of Innovations in Education, hosted by Kevin Hogan, is sponsored by McGraw Hill.

In this special edition of Innovations in Education, Content Director Kevin Hogan speaks with McGraw Hill’s Patrick Keeney about various aspects of career and technical education (CTE), including its expansion beyond traditional vocational or trade-focused subjects, the importance of soft skills, and the curriculum and teaching methods used in CTE courses for middle school students.

Patrick emphasizes the value of helping students explore different career paths and develop essential skills early in their education. The conversation also highlights the evolving nature of CTE in middle schools and its potential to provide students with a more comprehensive and purposeful educational experience.

Kevin is a forward-thinking media executive with more than 25 years of experience building brands and audiences online, in print, and face to face. He is an acclaimed writer, editor, and commentator covering the intersection of society and technology, especially education technology. You can reach Kevin at KevinHogan@eschoolnews.com

In my day, applying to college meant thumbing through a big paperback encyclopedia of college listings and then pulling out the typewriter and filling in applications. Thirty-some years later as my kid prepares to apply, I need a spreadsheet and access to reams of data that I’m not sure how to process.

I’ve tried doing it the old-fashioned way, by searching through the websites of all the schools my high-school senior is interested in applying to. For each school, you need to find the common data set, a multipage PDF that lists seemingly unrelated stats. Then you need to run the net-price calculator, which attempts to give you a price tag based on the financial information you input. Then you put everything together to try to get some sense of your kid’s chances of getting in and what it might cost you so you can compare the schools to each other.

Of course, there’s an app for that. Well, not so much one app, but several different programs that purport to sort college data in a useful way — some of them free, some by subscription and some through the school. All of it is still confusing and overwhelming for the average family.

Big J Education Consulting is attempting to make it easier with interactive charts, available on its website for free, that allow you to easily sort through data from the common data sets of hundreds of schools, plus some of the company’s own fact-checked and reported updates. Co-owners Jennie Kent and Jeff Levy have been making these charts for years for their own business, and they went high-tech with a new format this year that makes sorting and crunching the data easy enough for a layperson to do.

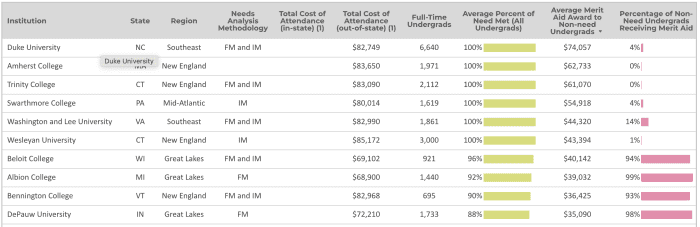

“People think about that common data set as a snapshot, but it’s really more of a collage,” says Kent. “Admissions fills out part, financial aid fills out part. Sometimes numbers are off, and we reach out to institutions. The best that any of us can do with this is to use the common data set.”

Take, for instance, the sometimes outrageous cost-of-attendance number, a sticker price that includes tuition, room and board, books and fees for one year. At the top of their list is Northwestern University in Evanston, Ill., at a whopping $89,394. Levy and Kent say they are hearing from a number of schools that the price for the upcoming year will be over $90,000, at least for international students.

Need-based and merit aid for the class of 2026, sorted by total cost of attendance for out-of-state students.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

You can learn a lot from looking at a chart like this and playing with it according to the choices pertinent to your family. For instance, one thing to note is that if you sort by price, you don’t see prices below $80,000 until you get four pages in. Those are the most expensive 78 out of 427 schools.

To get to the least expensive schools, you have to sort by in-state prices, because most of these will be public institutions that offer special pricing to state residents.

Need-based and merit aid for the class of 2026, sorted by total cost of attendance for in-state students.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

Of course, a school’s list price does not tell you how much it will cost your family to send a student there. The price you pay will depend on your own family’s financial situation, and that’s where all the strategizing comes in — and why families sometimes turn to professionals to crunch this data for them.

To get any kind of handle on that, you have to look at the other columns detailed on the chart below that analyze how much need-based aid a school gives and how much it gives out in so-called merit aid, which college finance experts have taken to calling “tuition discounting,” because it really just represents a coupon value off the sticker price.

If your family falls under the threshold of “need,” which varies by school, you can get a decent picture of what your price may be from the net-price calculator. But if you fall outside of those parameters, you’ll want to know how generous a school is with that tuition discounting. You really have to look at two numbers to figure this out, because the average amount of merit aid can be inflated by the small number of students it goes to.

Need-based and merit aid for the class of 2026, average merit aid awarded to non-need undergrads.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

For instance, according to common-data-set data compiled by Big J, Duke meets all needs of undergraduates and gives out an average of $74,057 in merit awards to non-need undergrads, but it only gives that out to 4% of its full-pay applicants. Whereas Beloit College meets 96% of need but gives out an average of $40,142 in merit awards to 94% of non-need undergrads. Which sounds like the better chance of getting a discount?

You can input your own selection of colleges into this list and do a comparison that way. I input the top colleges on my child’s list and was able to see how they stacked up against each other in terms of merit aid and tuition price. I found that useful for weeding some out.

Playing the early game

None of the price modeling matters if your child doesn’t get into a school in the first place. That’s where strategizing over what type of application to submit matters. A little data visualization on early admission might help you if you want to play that game. And if you pair it with the financial data, you can get a sense of whether it matters at a particular school to apply early, and what it might cost you — since the decision is supposed to be binding.

The choice of whether to apply for early decision is complicated this year because the federal financial-aid form, FAFSA, is not opening until December, and schools cannot typically finalize their aid packages without it. Plus, more colleges across the spectrum are filling their classes with early admits because it maximizes their yield statistics — that is, the number of students who accept their offers. So competition is fierce.

Early-decision and regular-decision acceptance rates for the class of 2026, sorted by early admits as percent of freshman class.

Credit: Jennie Kent, Jeff Levy, and Big J Educational Consulting, 2023

On the Big J chart for early-decision and regular-decision acceptance rates, the schools making the most of this are filling more two-thirds of their classes with early admits. They are also typically accepting students at a far greater rate from the early-decision pool than they are from the regular-decision pool. At Tulane, for instance, the early-decision acceptance rate is 8.6 times greater than that for regular decisions.

Looking at that data might make you feel a little pressure, but remember, at the end of the day, the only school your child should pick for early decision is one that you can afford and that is a good fit for them.

Roughly 125,000 borrowers will have $9 billion in student debt cancelled, the Biden administration announced Wednesday.

The cohort receiving the relief includes three groups of borrowers who have been eligible to have their debt forgiven for years but struggled to access that benefit. They are public servants who have been working for the government or certain nonprofits for more than 10 years and paying on their student loans during that time; borrowers who have been in repayment on their loans for more than 20 years; and borrowers who are severely disabled.

The announcement comes as payments are resuming this month for 28 million student-loan borrowers for the first time in three years, now that the pandemic-era payment pause has ended. Some have reported challenges enrolling in repayment plans and getting correct information from their servicers about their payment amounts.

Student-loan borrower advocates had called on the Biden administration to wipe debt off the books for borrowers who are already eligible for cancellation under the law before resuming repayment. They’ve said that would help alleviate some of the strain the return to repayment is putting on the student-loan system. It wasn’t immediately clear whether borrowers who are part of Wednesday’s announcement will have their debt cancelled right away or need to wait for a period for the discharge to be processed.

Wednesday’s announcement is distinct from the broad-based debt cancellation that’s grabbed headlines in recent months. Earlier this year, the Supreme Court struck down the Biden administration’s plan to cancel up to $20,000 in debt for borrowers earning less than $125,000.

Last week, officials provided more detail on President Joe Biden’s plan to take another stab at mass debt forgiveness. The process to determine the contours of that relief continues, with a set of meetings next week, and likely won’t be resolved for several months.

Part of groups already eligible for relief under the law

The borrowers covered by Wednesday’s announcement are part of groups that were already entitled to debt cancellation under the law, but for years have struggled to access it due to paperwork and technicalities. Officials have faced pressure from advocates for years to smooth the path to relief for these borrowers.

The group includes 53,000 borrowers who are receiving $5.2 billion in cancellations under the Public Service Loan Forgiveness program. That initiative allows borrowers who work for the government and certain nonprofits to have their student debt forgiven after at least 10 years of payments.

But it was notoriously challenging to access. Roughly 1% of borrowers who applied for relief in the first years of the program actually had their debt cancelled. The Biden administration has taken steps to make it easier for borrowers who meet the spirit of the law to overcome technicalities that in the past had stymied their path to forgiveness.

In addition, the Department of Education has approved debt discharges totaling $2.8 billion for nearly 51,000 borrowers who made more than 20 years of payments on their loans, officials announced Wednesday.

For decades, the government has offered federal student-loan borrowers the ability to pay their debt as a percentage of their income and have the remainder cancelled after at least 20 years. The idea was to provide an alternative to borrowers who couldn’t afford to pay off their debt in 10 years through a mortgage-style plan.

But in the first years, borrowers would have been eligible to have their debt forgiven under these income-driven repayment plans, more than 2 million borrowers who were in repayment for more than 20 years were still paying.

Consumer advocates and regulators said that was largely because servicers were steering borrowers towards forbearance — a status that pauses payments, but where the debt still accrues interest and borrowers don’t build credit toward forgiveness — instead of helping them sign up for these plans.

Last year, the Department of Education said it would review borrowers’ payment history to see whether there were periods when they should have been building credit toward forgiveness, but those months weren’t accurately counted. The agency said it would adjust their payment history accordingly. The 51,000 borrowers are part of this group. Already the Biden administration has cancelled the debt of more than 800,000 borrowers through this initiative.

Finally, officials said that nearly 22,000 borrowers who have a total or permanent disability will have about $1.2 billion in student loans cancelled. Borrowers with a disability that is so severe they’ll never work again qualify to have their federal student loans wiped out. But for years, many eligible borrowers found the application process, which historically required them to provide proof of their disability, challenging to navigate.

In 2021, the Biden administration announced it would match borrowers’ data with data at the Social Security Administration, which through its work administering disability benefits has the information that would indicate whether a borrower is eligible for a total and permanent disability discharge. The roughly 22,000 had their debt discharged approved through this data match, the agency said.

“For years, millions of eligible borrowers were unable to access the student-debt relief they qualified for, but that’s all changed thanks to President Biden and this administration’s relentless efforts to fix the broken student-loan system,” Miguel Cardona, the secretary of education, said in a statement announcing the relief.

“Today’s announcement builds on everything our administration has already done to protect students from unaffordable debt, make repayment more affordable and ensure that investments in higher education pay off for students and working families,” he added.

MIAMI, August 16, 2023 (Newswire.com)

– The BeOnAir Network of Media Schools is delighted to congratulate Chief Executive Officer Nancy Rodriguez on her induction into the Florida Association of Postsecondary Schools and Colleges (FAPSC) Hall of Fame. The Hall of Fame honors individuals who have made a significant contribution to the private postsecondary schools and colleges sector in Florida, and Nancy was formally inducted at the FAPSC annual conference in August 2023 alongside six other education sector leaders.

Nancy expressed her appreciation for the recognition: “I have had the pleasure of being involved with this organization for the last 30 years and have met many inspiring pioneers and trailblazers who have worked hard to create educational choice and mentor the next generation of education leaders.”

At BeOnAir Network of Media Schools, our mission is to provide ambitious students with the opportunity to gain real-world experience with hands-on training and a high-quality education. Our diploma programs cover a variety of media fields and are accredited by the Accrediting Commission of Career Schools and Colleges (ACCSC), which is recognized by the U.S. Department of Education. We strive to ensure that our students have access to multiple educational institutions, so they can receive comparable data and be fully protected.

“The challenges that face higher education today will only be resolved by ensuring each student has access to multiple types of educational institutions,” Rodriguez added. “I believe in life-long learning. We no longer live in a society where we can pretend education is a one-size-fits-all solution. I will continue to join the FAPSC organization in fighting for equitable regulations, legislation that allows transparency for all students, and full disclosures on outcomes across the board. For students to be fully protected and have access to educational opportunities, we must ensure they have comparable data from every institution of higher learning.”

We are proud to have Nancy Rodriguez as our leader and her induction into the FAPSC Hall of Fame is a testament to her commitment to providing students with the best possible educational opportunities.

Texas is home to the largest number of borrowers who will benefit from the reform — and debt cancellation, data from the Education Department released Tuesday morning revealed.

The three states with the largest number of borrowers who will see their student debt erased under the fix to the program, known as Income-Driven Repayment, are Texas, California and Florida, according to data from Education Department.

Nearly 64,000 Texans are expected to see around $3.1 billion in student loans canceled as a result of having paid their outstanding balance through the IDR program over the past two decades.

“Republican lawmakers — who had no problem with the government forgiving millions of dollars of their own business loans — have tried everything they can to stop me from providing relief to hardworking Americans,” President Joe Biden said Friday, announcing the plan. “Some are even objecting to the actions we announced today, which follows through on relief borrowers were promised, but never given, even when they had been making payments for decades.”

“The hypocrisy is stunning,” Biden added, “and the disregard for working- and middle-class families is outrageous.”

State

Borrower Count

Debt Eligible for Discharge (in millions)

Texas

63,730

$3,091.80

California

61,890

$2,958.80

Florida

56,930

$3,036.80

New York

42,070

$1,924.10

Georgia

38,590

$2,130.40

At the lower end, loan forgiveness through the IDR fix is least likely to help borrowers in Alaska, Wyoming and Hawaii. In Alaska, only 970 student debtors will see their debt erased through the IDR fix, the federal data revealed.

Last year, the Biden administration and Education Department announced that they would be reviewing borrowers’ accounts to make sure all student-loan borrowers’ monthly payments toward their debt have been accurately counted.

The count is an important part of the Income Driven Repayment program, which allows debtors to pay 20 or 25 years of debt as a percentage of their income and have the remainder forgiven.

Until the fix was announced, few had received loan forgiveness in exchange for paying their debt for 20 to 25 years.

The forgiveness comes as a result of a government program that promised loan forgiveness in exchange for debtors paying back their debt over two decades.

Student-loan payments are poised to resume this fall without smaller balances now that the U.S. Supreme Court has blocked President Joe Biden’s loan cancellation plan.

The Biden administration’s loan forgiveness initiative would have canceled up to $10,000 of debt for eligible borrowers, and in some cases up to $20,000.

But the Supreme Court’s conservative majority ruled on Friday that the executive branch overstepped its authority by trying to wipe out billions in student loan debt on its own.

“Six States sued, arguing that the HEROES Act does not authorize the loan cancellation plan. We agree,” Chief Judge John Roberts said, writing for the 6-3 majority.

Now it’s time for more than 40 million borrowers with federal student loans to figure out their next move. They are staring at more than $1.6 trillion in student loan debt. Add on private student loans, and the number climbs to $1.7 trillion.

Federal student loan payments have been on hold since March 2020.

On Friday, the Department of Education filed notice saying it would embark on a regulatory process that would seek an alternative pathway to student-debt relief. Activists have focused on a provision in the Higher Education Act, allowing the Department of Education to “compromise, waive, or release,” any right to collect on student loans.

Approximately 26 million people had either applied for loan forgiveness or were already eligible for the relief as of late last year, the White House said.

Here’s what to know.

When do student-loan payments restart?

In October, according to the Department of Education. Expect more specifics soon on those payments. “We will notify borrowers well before payments restart,” the department said.

While payments start coming in October, interest starts accumulating on the loans in September. Loan balances have not been accumulating interest since the payment pause started in March 2020, during the pandemic’s early days.

“We will also be in direct touch with borrowers and ramping up our communications with servicers well before repayment resumes to ensure borrowers and their families are receiving accurate and timely information about the return to repayment,” an Education Department spokesperson said.

There’s a range of estimates on how much student-loan borrowers typically pay each month on their loans.

According to Bank of America data, $180 was the median monthly student-loan payment as of January 2020. Federal Reserve research before the pause said the average monthly payment was $393, while the median payment was $222.

Can I lower my payments?

Possibly yes, with a range of income-driven repayment plans through the Education Department. These plans are supposed to make repaying loans more affordable by letting borrowers modify their monthly payments based on their income.

While these plans already exist, the department is reworking them. As a result, more monthly income will be shielded from the calculations on what a person could repay for student loans each month, meaning payments will become more affordable. While the revised plans are not in effect yet, the existing plans are up and running.

Many people will likely struggle to fit a student-loan bill back into their budget — the question is how far that financial hardship will go. Student-loan payments would be hitting at a time when car loan and credit-card delinquencies are already rising from their pandemic lows, according to the Federal Reserve Bank of New York.

Part of the Biden administration’s Supreme Court arguments pointed to the possible economic consequences of resuming student-loan payments without canceling some of the debt.

Without cancellation, there will be a “surge” of loan defaults and delinquencies once payments resume, Solicitor General Elizabeth Prelogar told the justices during oral arguments earlier this year.

When deciding which debts have to get paid first, a student-loan bill might fall behind other monthly debts like a mortgage or a credit-card bill.

Anywhere from roughly one-third to three-quarters of borrowers could miss their first student-loan bill when payments resume, according to projections from the credit score company VantageScore.

A missed first payment — in theory — could eventually lead to an average 49- to 82-point reduction in a credit score ranging from 350 to 850, VantageScore researchers said.

However, President Biden on Friday announced a temporary “ramp-up” — a 12-month grace period for borrowers who miss student-loan payments. If borrowers miss payments during this time, they won’t be reported to any of three main credit bureaus — Equifax EFX, +0.37%,

TransUnion TRU, +1.06%

and Experian EXPGF, +0.80%

— and they won’t go into default.

The ramp-up will run from Oct. 1, 2023 through Sept. 30, 2024.

“This is not the same as the student-loan pause, but during this period — if you miss payments — this ‘on ramp’ will temporarily remove the threat of default or having your credit harmed,” Biden wrote in a tweet Friday.

Prior to the payment pause and Biden’s ramp-up announcement, loan servicers waited for a borrower to miss three straight payments before they reported it to the credit reporting bureaus, according to Scott Buchanan, executive director of the Student Loan Servicing Alliance.

In the meantime, brace for potentially long call hold times, curtailed hours and loan servicer glitches, borrower advocates say. It stems back to Congressional cuts on the funding for vendor contracts that handle the day-to-day details of student-loan repayments.

The Supreme Court knocked down the Biden administration’s plan to cancel up to $20,000 in student debt for a wide swath of borrowers, the court announced Friday.

The decision means that the White House won’t move forward with the plan for now, though it’s possible officials could try to launch a new version of the debt-forgiveness initiative using a different legal authority. Roughly 26 million borrowers applied for or were automatically eligible for debt relief under the Biden administration’s plan, which canceled up to $10,000 in student debt for borrowers earning less than $125,000 and up to $20,000 in federal loans for borrowers who met that criteria and also used a Pell grant in college.

Americans owe $1.7 trillion of student loans and the White House had estimated that more than 40 million borrowers would benefit from the initiative. But almost as soon as the Biden administration announced the debt-forgiveness plan last year, opponents looked for ways to challenge it legally. Ultimately, two cases made it to the high court.

In one case, two student-loan borrowers sued over the debt-relief plan in part because the Department of Education didn’t submit it for public comment. That, they said, resulted in an initiative that arbitrarily left out or limited the amount of relief available to some student loan borrowers, like themselves. The suit filed by the borrowers was backed by the Job Creators Network, a conservative advocacy organization co-founded by Bernard Marcus, the co-founder of Home Depot, who also supported former President Donald Trump.

Six Republican-led states brought the other case on the basis that canceling debt could harm their state coffers.

The court considered two issues in these cases. The first is whether the plaintiffs had standing, or the ability to bring a lawsuit because they’ve been directly harmed by the policy. The second is whether the Biden administration overstepped in its executive authority when issuing the policy. In order for the justices to reach the second issue, or the merits of the case, they had to find that the plaintiffs had standing to sue.

Legal experts, including some who believed the Biden administration didn’t have the authority to authorize the debt-relief plan, were skeptical of the notion that the parties bringing the cases had standing to sue. During oral arguments in February, the court’s three liberal justices also questioned whether the parties who challenged debt forgiveness were actually injured by the policy.

In addition, one of the members of the court’s conservative wing, Justice Amy Coney Barrett, asked pointed questions about the six states’ argument that they had standing to sue in part because the debt-relief plan would injure the state of Missouri. That claim surrounded the Missouri Higher Education Loan Authority, or MOHELA, a state-affiliated organization that services federal student loans. The states had argued if MOHELA lost accounts due to the debt-relief plan, its revenue would decline and that loss would hurt Missouri because of MOHELA’s ties to the state.

Despite these questions, Barrett agreed with the court’s five other conservative judges and found that the states have standing to sue. The three liberal justices dissented.

“MOHELA is, by law and function, an instrumentality of Missouri,” Chief Justice John Roberts wrote in the majority opinion. “It was created by the State, is supervised by the State, and serves a public function. The harm to MOHELA in the performance of its public function is necessarily a direct injury to Missouri itself.”

The court’s decision in the states’ suit allowed the justices to get to the merits of the case. The parties challenging the debt-relief plan argued that the Department of Education went beyond the authority Congress delegated it in discharging student debt. Solicitor General Elizabeth Prelogar argued to the justices that in canceling student debt, the Secretary of Education acted “within the heartland” of the authority Congress provided to him under the HEROES Act, a 2003 law that aims to ensure student-loan borrowers aren’t left worse off by a national emergency.

The court’s conservative majority sided with the states, with a 6-3 decision, striking down the debt-relief plan in its current form.

“The HEROES Act allows the Secretary to ‘waive or modify’ existing statutory or regulatory provisions applicable to financial assistance programs under the Education Act, but does not allow the Secretary to rewrite that statute to the extent of canceling $430 billion of student loan principal,” Roberts wrote.

In the months leading up to the court’s decision, White House officials said there was no backup plan for if the Supreme Court knocked down the debt-forgiveness initiative. Advocates and activists have said that student-loan repayments shouldn’t resume until the Biden administration fulfills its promise to cancel some student debt.

The bill President Joe Biden signed in June to raise the nation’s debt limit requires that the Department of Education end the pause on federal student loan, interest payments and collections 60 days after June 30, 2023. Interest on federal student loans will resume starting September 1 and payments will start to come due in October, according to the Department’s website.

Advocates and activists have said for years that the Higher Education Act provides the Secretary of Education with the authority to discharge student loans. In ruling that the HEROES Act didn’t authorize the Biden administration’s debt-relief plan, the court left the option open for the Biden administration to create a loan-forgiveness program authorized under the HEA.

The court’s decision marks the latest development in a more-than-decade-long push to get the government to cancel student debt en masse. The idea, which has its origins in the Occupy Wall Street movement, made it to the presidential campaign stage during the 2020 cycle and was adopted by the White House last year.

Proponents of student debt cancellation and the Biden administration, have expressed concern that without some kind of relief a large swath of borrowers could slip into delinquency and default with the return of student loan payments later this year.

Student loan borrowers aren’t just the freshly graduated and mid-30s working generations — millions of Americans in their retirement years have student debt to pay back, too.

There are six times as many borrowers ages 60 and older now than there were in 2004, but their debt has increased “19-fold,” according to a report from New America, a public policy think tank. About 3.5 million Americans in this age bracket carry $125 billion in student debt, the report found.

Overall, Americans hold $1.75 trillion in student debt, the World Economic Forum found. The president’s student loan forgiveness plan, which was announced last August and is now in the midst of legal battles in the Supreme Court, would alleviate $10,000 for qualifying borrowers, or $20,000 for those with Pell Grants. At the time of the announcement, the White House said 20 million borrowers would see their debt washed away, and a total of 40 million would find benefit from cancellation.

Student debt has been especially problematic because of “stagnant wages and soaring tuition prices,” AARP said in another report highlighting older borrowers. Around 3% of families headed by someone who was 50 or older had student debt in 1989, with an average balance of $10,000, but by 2016, that figure rose to 9.6%, with an average of $33,000, AARP said.

Whether student debt forgiveness will happen or not is still to be determined. Borrowers have been anxiously awaiting an answer from the Supreme Court over two cases linked to the plan — one that argues whether or not the president had the legal authority to forgive loans, and another case about whether the program has standing. The Supreme Court is expected to release its decision on Friday, the last day of the court’s term before summer break.

Older borrowers have various reasons to carry debt. Some are paying off their own education, while others have taken on student debt for their loved ones. Federal PLUS loans, for example, allow parents to take loans out for their children’s education. Older Americans may have also taken on debt to refine their skills for a promotion, AARP noted in its report.

Student loans can have a rippling impact on retirement savings — not just in allocating a portion of retirement income toward this debt, but also in accruing enough wealth for old age. Graduates with student loans had 50% less in retirement wealth by age 30 than the graduates without this debt, a Boston College Center for Retirement Research study found.

She doesn’t know how much her student-loan bill will be when the years-long pandemic-era freeze on payments ends. Eminger’s loans were transferred during the pandemic to a new servicer, but she’s struggled to communicate with the organization, which could help her learn her monthly payment amount. She’s also rushing to take steps that could provide her access to a loan-forgiveness program for public servants.

“I am very nervous about them starting again,” Eminger, 37, who has about $175,000 in student debt, said of the loan payments. “There’s just a lot of uncertainty and murkiness around it, which for a loan amount of my size is pretty scary.”

After a more than three-year freeze, payments, collections and interest are scheduled to resume on federal student loans later this year. This is the ninth time — spanning two administrations — that the government has threatened to turn payments back on. Once again, borrowers, advocates and servicers are gearing up for a financial and operational headache.

“It’s going to be frustrating for everybody involved — borrowers, servicers, the Department of Education, advocacy organizations like ours,” said Betsy Mayotte, the president of the Institute of Student Loan Advisors, a nonprofit that helps borrowers manage their student loans.

To advocates who pushed officials to delay restarting payments in the past, this moment in many ways looks similar to the months before the freeze was scheduled to end those eight other times. A challenging economy means borrowers’ budgets are still tight and promised fixes to the student-loan system that could help ensure a smooth transition to repayment and make borrowers’ bills more manageable still haven’t materialized.

But a few key factors are different, some of which are upping the pressure on the Biden administration to turn the student-loan system back on: the official end to the pandemic emergency, congressional Republicans taking aim at the payment pause in two pieces of legislation and multiplelawsuits challenging the freeze. Other elements unique to this moment are exacerbating the uncertainty and challenges related to restarting payments. Servicers will have fewer resources than in the past to handle a likely crush of calls.

“The Department remains focused on doing everything in its power to better serve students and borrowers, and we are fully committed to supporting student loan borrowers as they successfully navigate returning to repayment,” a Department of Education spokesperson wrote in an email. “The Department is deeply concerned about the lack of adequate annual funding made available to Federal Student Aid this year,” the spokesperson said, referring to Congress’s decision not to increase funding for FSA, despite the agency’s request. “As the Department has repeatedly made clear, restarting repayment requires significant resources to avoid unnecessary harm to borrowers.”

For Eminger, and other borrowers, part of the anxiety surrounding the restart to payments stems from major upheaval to the student-loan system that’s been announced during the pause that will make her loans more manageable. But accessing these benefits requires both diligence — staying on top of announcements and paperwork — and patience while she and others wait for the full implementation of these initiatives.

“The rules have been changing so much,” Eminger said. “Before the pandemic I felt like I very much understood what I was required to do. I always felt very on top of it. Now it just feels like a completely moving target.”

Kate Eminger says she’s nervous about the looming resumption of student-loan payments.

Courtesy of Kate Eminger

Compounding her uncertainty is a lack of clarity surrounding exactly when payments will resume. In November, President Joe Biden told borrowers they could expect the pause to end in the late summer, but he didn’t give an exact date. In addition, it’s hard for Eminger to see how this deadline for payments to restart is different from all the others, where student-loan bills never materialized. All of that has made it difficult for Eminger to figure out exactly when to take steps to make sure her student-loan payment can fit in with the rest of her budget such as the sale of her car.

“It does not feel real at all,” she said of the restart of student-loan payments. “It would be great to name a date. If they could name a date and if that date felt certain then you could plan.”

Tied up in court

The Biden administration has said that the freeze will end 60 days after litigation surrounding its plan to cancel up to $20,000 in debt for a wide swath of borrowers is resolved or 60 days after June 30, 2023, whichever comes first.

“When payments turn back on, it’s going to be a big problem,” said Eleni Schirmer, a researcher and organizer with the Debt Collective, a debtor activist group, “but to not even be granted the dignity of a clear date of when that happens just makes it even more of a problem.” She described providing a ballpark estimate for the restart of payments instead of an exact date as signaling an “almost cruel indifference” to how resumed monthly student-loan bills will impact borrowers.

That uncertainty could exacerbate the stress that student debt already places on borrowers, according to Daniel A. Collier, an assistant professor of higher education at the University of Memphis, who is studying the impact of student debt on mental health. What he’s found is that people who are the most uncertain about what’s going on with their student loan have the highest rates of psychological distress and suicidal ideation. For example, these borrowers worry they’re not getting an accurate sense of their balance or the number of payments they need to make before qualifying for a forgiveness plan.

“People are concerned about the pause because they don’t know what a restart looks like, this has never been done before,” he said. In the past, when payments have resumed after more limited pauses, delinquencies and defaults spiked — part of the Biden administration’s legal rationale for tying mass debt cancellation to the restart of payments. Borrowers don’t know “when it’s going to start, what their repayments are actually going to be,” Collier added.

Kevin Noonan, who together with his wife has about $100,000 in student debt, said he’s benefited from the pause. The couple has used the extra room in their budget to pay down private student loans. Still, Noonan is “frustrated” with the lack of clarity surrounding the resumed payments and the status of the Biden administration’s loan-forgiveness plan.

“Not knowing is the hardest part,” he said. “I have a Google alert set up, every time student loans come up I check everything. You kind of just have to plan for the worst-case scenario.”

Megan and Kevin Noonan have about $100,000 in student debt.

Courtesy of Kevin Noonan

The decision to tie the resumption of payments to the court’s decision “added an element of unpredictability,” said Persis Yu, managing counsel and deputy executive director at the Student Borrower Protection Center, an advocacy group.

“There’s the choice to not land on a certain date, but there’s also the choice of 60 days,” Yu said, referring to the 60-day delay between the court’s decision and payments resuming.

“I really wonder whether or not 60 days is enough time for borrowers,” she said. “When we think about the amount of work that is really going to have to happen to effectively turn on this system, 60 days does not seem like a lot of lead time.”

Secretary of Education Miguel Cardona said in a congressional hearing this month that the agency is “preparing to restart repayment because the emergency period is over.” He told another congressional panel that the agency is “geared up and ready to go,” to resume payments.

Scott Buchanan, the executive director of the Student Loan Servicing Alliance, a trade group, said that 60 days should be enough time for student-loan servicers to implement the restart. In order to accomplish that, they’ll need to be able to communicate with borrowers in the coming weeks about the end of the payment pause and be allowed to offer flexibilities like forbearance and allowing borrowers to verbally recertify their income for payment plans.

When the end of the payment freeze loomed in the past, servicers didn’t have the go-ahead from the Department of Education to communicate with borrowers, Buchanan said. They still don’t, but servicers have been working closely with officials to discuss the “communication playbook” in recent weeks and hope to roll it out shortly.

The Department of Education “remains in constant contact with servicers,” the department spokesperson wrote in an email, and will be in “direct contact” with borrowers before the end of the payment freeze. “Engaging with servicers to ensure they are communicating directly with borrowers about successfully returning to repayment is an important part of the Department’s efforts to smoothly transition borrowers back into repayment,” the spokesperson wrote.

Still, the uncertainty surrounding exactly when payments will start could create an obstacle to a seamless return to repayment, Buchanan said.

“If you’re a family and you’re planning a budget you need to know what is the date that I need to be prepared to make this payment,” he said. “Having a fuzzy date doesn’t do anyone any good including servicers, but especially for borrowers.”

Borrowers will receive a bill at least 21 days before their payments are scheduled to resume and likely won’t end up having to make a payment until October, Politico reported last month. Officials are also considering offering borrowers a grace period when the freeze ends, according to the report.

Servicers will be implementing plans the department previously developed to restart payments, Buchanan said. But they’ll be working with fewer resources than previously anticipated. The Department of Education cut the amount it’s paying servicers to manage each account. The agency has said the cuts are due to lawmakers’ decision not to increase funding for the Office of Federal Student Aid for the 2023 fiscal year. The lack of funds will mean fewer customer-service representatives and reduced call-center hours, including none on weekends.

“What is the right level of resources? How many staff should you have? It’s not a definable thing,” Buchanan said. “What I can say is having fewer than we had before does not make it better.”

The department spokesperson said the agency will keep working with Congress to fully fund President Biden’s fiscal 2024 budget request. The department asked for a $620 million increase in funding for FSA.

“Restarting repayment requires significant resources to avoid unnecessary harm to borrowers,” the spokesperson wrote in the email.

Members of the Class of 2022 at the University of Delaware.

Mandel Ngan/Agence France-Presse/Getty Images

In addition, the Department of Education recently announced an overhaul of the student-loan servicing system aimed at increasing accountability for servicers. For years, borrowers and advocates have complained that the firms don’t provide borrowers with enough information or the right information. Without that in place, Yu worries that ensuring borrowers have a truly affordable payment will be “a nightmare.”

“At this inflection point where you need the best servicing possible, we don’t have it,” she said. “It seems irresponsible to turn on the payment system into a broken servicing system and into a broken system overall.”

Though the new servicing system won’t go live until 2024, “our servicer contracts continue to include the same requirements that all vendors effectively serve our customers and still provide that servicers compete against each other to maintain low call-abandonment rates,” the department spokesperson wrote.

Fixing servicing is just one of many initiatives from the Biden administration aimed at overhauling the student-loan system in the process of being implemented and won’t be fully realized before the end of the summer.

For example, some borrowers have debts that should be wiped off the books, Yu said. The Biden administration has launched several initiatives over the past few years aimed at making it easier for borrowers to access the forgiveness already available to them under the law. So far, the department has announced more than $66 billion in discharges for nearly 2.2 million borrowers, including public servants, borrowers with severe disabilities and borrowers who were scammed by schools.

Still, there are more borrowers eligible to have their debt canceled under these programs who haven’t received relief, Yu said. “These borrowers are going to be thrown into a system to make payments on loans they shouldn’t be making payments on anymore,” she said.

In addition, a promise to make repaying student loans more manageable hasn’t fully materialized. At the same time that President Biden announced the mass debt-cancellation plan, he also unveiled sweeping changes to the repayment system aimed at making student-loan bills more affordable. But the program, which Biden called “a game changer” when he announced it in August, likely won’t be ready by the end of the summer. It’s also been a target for criticism by conservative advocacy groups and Republican members of Congress.

“The only way that that could be available to borrowers when payments resume is with another extension,” Yu said.

The proposed plan, which the department spokesperson described as “the most affordable student loan plan in history,” builds on an existing income-driven repayment plan called REPAYE. Eligible borrowers who enroll in REPAYE now will have their monthly payments automatically updated as the terms of the new plan are “finalized and implemented, starting later this year,” the spokesperson wrote.

‘Almost like a tax increase’

For many borrowers, the financial burden of resuming student-loan payments will be significant. Thomas Simons, a senior economist at Jefferies, estimates the return to repayment will cost borrowers about $18 billion per month.

“It’s almost like a tax increase for these people,” Simons said. “They have to pay it, [and] it doesn’t get them anything tangible right now.”

The amount borrowers are saving by not making student-loan payments accounts for about 2% of discretionary spending, Simons said. He sees the hit to borrowers’ wallets as analogous to the impact of a payroll-tax increase in 2013, which impacted a smaller share of discretionary spending for a larger number of Americans.

“‘It’s almost like a tax increase for these people. They have to pay it, [and] it doesn’t get them anything tangible right now.’”

— Thomas Simons, senior economist, Jefferies

“If you look at what happened in the economy in 2013 after those tax increases were announced, the first half of the year spending decelerated quite significantly,” he said. “It really didn’t recover until the latter part of the year.”

“I would be very surprised if we don’t see a similar slowdown in spending coming out of this,” Simons added.

And if payments resume in late summer or early fall, as planned, the hits to borrowers’ bank accounts will be arriving at “the worst possible time,” Simons said, when the labor market will likely start to feel the effects of the Federal Reserve’s battle against inflation.

“That could be a double whammy where people are starting to have significant questions about their income and then having a pretty significant expense,” Simons said.

Many borrowers will likely be juggling other bills, too. For one, the costs of rent, groceries and other basic needs have risen since the advent of the coronavirus pandemic. And borrowers’ other debt payments have actually become less manageable in the three years since the freeze was first implemented.

As of September of last year, about 7% of student-loan borrowers who were not in default on their student loans at the start of the pandemic were more than 60 days delinquent on other debt, compared with 6.2% at the beginning of the pandemic, according to the Consumer Financial Protection Bureau. Their monthly payments on other credit products have also increased during the pause period — 46% of borrowers saw their monthly payments on credit cards and car loans increase by at least 10% since the start of the pandemic, the agency found.

For Kelly, a Charleston, W. Va., student-loan borrower and her husband, the freeze on student-loan payments created financial space to take care of emergency expenses, like a leaking roof. Kelly, who declined to use her last name in order to more freely discuss her financial circumstances, owes about $23,000 in student debt from studying to become a paralegal. Her husband owes about $20,000 from his nursing-school studies.

Kelly, 45, found a job in her field after graduating, but was laid off during the pandemic. She started working some side gigs and eventually launched a dog-grooming business. Despite the business’s success and her passion for it, it likely won’t be enough to cover her bills once she has to start paying on her student loan again. She’s considering getting a second job when the payment freeze ends.

“We’re dual-income, no kids. One car is paid off, the other one is modest — a Volkswagen VOW, -0.43%

VWAGY, +0.22%,

” she added. “We don’t finance things, we don’t live a high and mighty life, but it seems like every month we’re budgeting to the penny.”

“I don’t know how much we can cut back,” she added. “Our entertainment as it is, is Netflix NFLX, -1.60%,

or we go out to eat once a month or so. I guess we can cut back on that.

WEST LAFAYETTE, Ind., March 15, 2023 (Newswire.com)

– Skyepack, leading provider of career-connected educational technology and digital content solutions, has been named a School Improvement Technical Assistance Partner by the Indiana Department of Education (IDOE). This partnership will enable Skyepack to support schools in Indiana with Career and Postsecondary Readiness and Sustainable Innovation, two of the three priority areas outlined in the Request for Information (RFI) issued by IDOE.

IDOE’s RFI aims to identify technical assistance partners who can provide highly effective, evidence-based supports to schools and districts in Indiana. Skyepack’s selection as a technical assistance partner is a testament to its expertise and proven track record in providing innovative solutions to improve student outcomes.

“We are honored to be named a School Improvement Technical Assistance Partner by the Indiana Department of Education,” said Eric Davis, CEO of Skyepack. “Career-connected learning has proven to improve student engagement, graduation rates, and college-going rates. We are excited to work with Indiana schools to support Career and Postsecondary Readiness and Sustainable Innovation, and to help create meaningful change that will benefit students for years to come.”

Skyepack’s expertise in building career-connected learning communities between educators, students, and industry will enable it to collaborate with district and school leaders to support the design and implementation of comprehensive support and improvement plans. By aligning its services and support to IDOE’s priority areas, Skyepack aims to help Indiana schools create sustainable systems for career exploration and engagement, and make strategic investments for sustainable innovation.

As a registered entity in good standing with SAM.gov, Skyepack meets all eligibility requirements set forth by IDOE to become an approved technical assistance partner. The company’s services and details will be listed on the Indiana Department of Education’s website and will be made available to district and school leaders identified for Comprehensive Support & Improvement.

About Skyepack

Skyepack is a leading provider of career-connected educational technology and digital content solutions. Its mission is to create transformative learning experiences that engage, empower, and inspire students throughout their educational and career journey. Skyepack partners with educators, institutions and employers to design and deliver customized digital content and tools that improve student outcomes and on-ramps to career pathways. For more information, please visitwww.skyepack.com and https://careerpluspathways.org/greaterlafayette/overview/

In as little as two weeks, obtain the 75-hour Real Estate Salesperson Pre-License Course from PA-approved provider, The CE Shop

Press Release –

Feb 1, 2023 08:15 MST

DENVER, February 1, 2023 (Newswire.com)

– Those seeking a new career path in real estate in Pennsylvania have a new flexible learning option for a career with consistent market demand.

With the one 75-hour Pennsylvania Real Estate Salesperson Pre-License Course requirement, it’s a no-brainer to sign up for one that is interactive, flexible, offered live online with self-paced delivery and provides the opportunity to learn in the best way that works for student schedules and learning preferences. Students can choose to complete the course entirely through the company’s self-paced delivery method, attend live online (synchronous), instructor-led courses, self-paced online (asynchronous), or utilize a combination of both learning methods. Both versions of the course are totally parallel to one another, and they’re split into sections so that students can even choose to take some sections of the course synchronously and other parts asynchronously without missing a beat.

If treated like a 40-hour work week, the education to become a real estate agent in Pennsylvania can be completed swiftly so you can move on with your new real estate career.

The CE Shop teaches through interaction, which is proven to be a far more effective method of learning than simply reading a boring PDF. The CE Shop uses a proprietary content delivery platform, which makes it easy for students to engage with the content needed to grow their business, as well as become a valuable asset to a brokerage. This proprietary learning model and delivery platform has helped students maintain a 91% National Pass Rate.

While many factors influence the annual salary of a real estate agent, according to Indeed.com, full-time Pennsylvania real estate agents can average $70k/year and have a lifetime of tools from The CE Shop to grow your knowledge and potential income. The CE Shop also offers additional certifications like Mortgage Loan Origination and Home Inspection to round out your artillery of professional success tools.

About The CE Shop The CE Shop is the leading provider of professional real estate education with online mortgage, real estate, and home inspection courses available throughout the United States. The CE Shop produces quality education for professionals across the nation, whether they’re veterans in their industry or are looking to launch a new career. We believe that the right education can truly make a difference. Visit TheCEShop.com to learn more.

I’m the first of my generation to own a home and the first to earn this much annually and don’t want to mess this up. How, specifically, can a financial adviser help me?

Getty Images

Question: By the end of 2022, I will have made $350,000 before taxes as the sole breadwinner and head of household. This is a great starting point and I’m very aware how blessed we are to be in this position, but I’m always looking ahead on how to improve. I currently have $88K left in student loans (originally close to $150K) and very little credit card debt (less than $2K with more than $25K available). I have two auto loans totaling $170K for two electric vehicles at 5% interest.

I’ve recently been offered a $200K HELOC at 9%, which would help me bring down some of my monthly payments and do some small home repairs and improvements, but I want to make the right moves. And I’ve also been presented with a few long-term real estate investment opportunities that are rental properties out of state and are currently bringing it 10-12% ROI. But my biggest concern is that after taxes, 401(k) contributions, bills, savings and mortgage ($4,500), on paper I’m paycheck to paycheck. I’d like to use this HELOC to consolidate debt while also participating in some of these investment opportunities. I’m the first of my generation to own a home and the first to earn this much annually and don’t want to mess this up. How, specifically, can a financial adviser help me? (Looking for a new financial adviser too? This tool can help match you with an adviser who might meet your needs.)

Answer: You have a few questions to tackle here, so let’s go one by one. The first being the HELOC. Yes, HELOCs can be a good way to consolidate debt, but the rate you’re being offered isn’t favorable, as average HELOC rates are a little over 6%. “I would ask if 9% is the best rate you can get, because it appears a bit high,” says Chris Chen, certified financial planner at Insight Financial Strategists. What’s more, “I would like you to consider the potential impact that our Fed policy and inflation are having on interest rates, as HELOCs usually have variable interest rates and we’re in an environment with rising rates. You may start at 9% and end up significantly higher,” says Chen.

What’s more, your student loans, car loans and mortgage are all likely less than 9%, so it’s not likely that consolidation via a HELOC would save you money. “You may want to start somewhere different, like the snowball method, where you focus on one loan, usually the smallest one, and direct all of your resources to pay off that loan while maintaining payments on the others,” says Chen. This method could work to finish off your student loans and maybe one of your car loans, to start with.

Have an issue with your financial adviser or have questions about hiring a new one? Email picks@marketwatch.com.

As for those real estate investments, what do you really know about those returns? “With regards to real estate investments, I assume that the 10% to 12% ROI you speak of is the income that you would be getting from the investment. If so, that’s very high and often when you get a return that is significantly higher than the norm, there’s something else that makes the investment less desirable. Be careful,” says Chen. (Looking for a new financial adviser too? This tool can help match you with an adviser who might meet your needs.)

Certified financial planner Kaleb Paddock says you may actually want to work with a money coach before you work with a financial adviser. Whereas a financial adviser assists with developing investment strategies and long-term financial plans, a money coach offers a more educational experience and focuses on shorter term goals for money management. “A money coach will help you with paying off all of your debts, maximize your cash flow and help you create systems and processes to direct your money proactively,” says Paddock.

While having a high income is great, there’s a concept called Parkinson’s Law, which essentially states that your spending will always rise to meet your income no matter how high that income rises, explains Paddock. “Working with a money coach will help you defeat Parkinson’s Law, eliminate your debt and then enable you to supercharge your investing and life planning with a financial adviser,” says Paddock.

A financial adviser could help too, and Danielle Harrison, certified financial planner at Harrison Financial Planning, says to look for one who does comprehensive financial planning and can help you create a more holistic plan for your money. “They can assist you in the creation of both short and long-term goals and then help you by giving guidance on the financial decisions and opportunities you are presented with,” says Harrison.

A financial adviser would also help you take a long-term approach to your money and help you create a spending plan where you don’t feel like you’re living paycheck to paycheck on a $350,000 salary. “Everyone has blind spots when it comes to their finances, so finding a competent financial partner can be invaluable,” says Harrison. (Looking for a new financial adviser too? This tool can help match you with an adviser who might meet your needs.)

Have an issue with your financial adviser or have questions about hiring a new one? Email picks@marketwatch.com.

*Questions edited for brevity and clarity.

The advice, recommendations or rankings expressed in this article are those of MarketWatch Picks, and have not been reviewed or endorsed by our commercial partners.

Student-loan borrowers got a break this week, but that doesn’t mean they can spend more for the holidays.

The Biden administration on Wednesday extended a pause on student loan payments, yet borrowers should prepare for the eventual resumption of payments by saving the amount they would otherwise owe, experts advise.

Expanding its innovation into architecture, multi-vertical education leader Career Certified continues to elevate careers relying on licensure and certification, seeking to attract the 60,000 potential architecture license candidates actively working to pass the ARE® 5.0 Multi-Exam Course each year.

Press Release –

Nov 10, 2022 09:40 MST

DENVER, November 10, 2022 (Newswire.com)

– Today, Career Certified acquired Amber Book, a leader in architecture online exam prep differentiated by its high-quality, engaging and animated content, created with carefully-trimmed topics that focus on high-yield exam areas. Promising continued growth on what has already gained industry attention for online Real Estate, Mortgage Loan Origination, and Home Inspection education, Career Certified has just expanded its impact on education into the architecture arena.

Founded by Michael Ermann—an award-winning architect, an award-winning educator, and the first person to pass all six ARE® 5.0 divisions—Amber Book has seen consistent upward organic growth. This territory was claimed by completely renovating the mindset around test prep education, leaning into unique animation, and developing keen insight into real-world application. Amber Book targets exam prep content to focus on the most relevant areas of the ARE® exam, offering the highest likelihood of passing in the fewest number of hours studying. The innovative content and learning methodology created by Amber Book are meant to net higher ARE® exam pass rates.

What began as an underground following quickly gained momentum from the best-of-the-best in architecture. Amber Book’s free, flagship, weekly online study sessions, “40 Minutes of Competence,” offer engaging problem-based and narrative-based content to those pursuing licensure. Mr. Ermann and the entire team behind Amber Book are fully embedded in the architecture community and recognized as authentic, approachable thought leaders.

“Amber Book embodies so much of our DNA towards innovation to better educate, and if there was ever a rockstar status to claim in architecture, Michael Ermann claimed it early through his dedication to the practice,” Gary Weiss, CEO of Career Certified, said. “As I’ve stated before, our pledge is that within the Career Certified family, enrollees will receive the most innovative, outcome-based, and superior education to deliver career freedom. We simply look to amplify the impact Amber Book has on generations of architects to come.”

The advantage this transaction brings to the marketplace is immeasurable. Career Certified can tap into its operational excellence in sales, marketing, and product innovation while retaining both the team and core of Amber Book and expand into continuing education for architecture (and much more).

“From the beginning, our goal was to help as many practitioners as possible reach licensure,” Michael Ermann, creator of Amber Book, explained. “Collaborating with Career Certified doesn’t only achieve this goal, but also offers us acceleration in innovation for architecture. With this partnership and the operational excellence Career Certified brings to us, we strengthen our leadership and impact the success of more emerging professionals obtaining licensure.”

Career Certified pairs advanced, easy-to-use platforms with a deep understanding of students’ needs, conducive to guiding them as they enter their new careers. Students are provided with the education and ongoing professional development to excel, and ultimately, deliver career freedom. The education is customized to each profession served, providing every student with a strong foundation for success. Career Certified is tailored to career professionals, built by career professionals.

About Amber Book With the video series they’ve created, Amber Book has helped 17,000 emerging professionals study for the architecture licensure exams. Michael Ermann, the course creator, was the first person in the nation to pass all six ARE® 5.0 divisions, and the small portion of the course posted on YouTube has more than 7 million views and more than 35,000 subscribers. Michael is a full-tenured professor at Virginia Tech, where he’s taught design studio, building systems, materials & methods of construction, and advanced architectural acoustics for 21 years. Professor Ermann has won 14 teaching, research and design awards and published the book Architectural Acoustics Illustrated(Wiley, 2015). He’s pretty sure he knows more about these licensure exams than anyone in the world. He will be staying on with Amber Book as it joins with Career Certified.

About Career Certified Career Certified elevates modern education while accelerating success for students in licensed professions. From Pre-Licensing, Licensing, and Continuing Education coursework to tools for the entire lifecycle of a professional’s career, the company pairs an easy-to-use platform and flexible learning options with a deep understanding of students’ needs conducive to guiding them to career freedom. Visit CareerCertified.com to learn more.Career Certified is backed by Waud Capital Partners, a leading growth-oriented private equity firm with total capital commitments of approximately $3.5 billion. For more information, visit waudcapital.com.

For the duration of the acquisition, Tyton Partners served as financial advisor, and Executive Counsel PLC acted as legal advisor, to Amber Book. Kirkland & Ellis LLP acted as legal advisor to Career Certified.

ST. LOUIS (AP) — A federal appeals court late Friday issued an administrative stay temporarily blocking President Joe Biden’s plan to cancel billions of dollars in federal student loans.

The Eighth Circuit Court of Appeals issued the stay while it considers a motion from six Republican-led states to block the loan cancellation program. The stay ordered the Biden administration not to act on the program while it considers the appeal.

The order came just days after people began applying for loan forgiveness. It was not immediately clear how the stay would impact those have already applied.

The court set a deadline of Monday at 5 p.m. CDT for a response for a response from the Biden administration and a 5 p.m. Central Tuesday deadline for any replay from the appellants.

The attorneys for the Republican-led states had asked the court to reconsider their effort to block the Biden administration’s program to forgive the student loan debt.

A notice of appeal to the Eighth U.S. Circuit Court of Appeals was filed late Thursday, hours after U.S. District Judge Henry Autrey in St. Louis ruled that since the states of Nebraska, Missouri, Arkansas, Iowa, Kansas and South Carolina failed to establish standing, “the Court lacks jurisdiction to hear this case.”

Separately, the six states also asked the district court for an injunction prohibiting the administration from implementing the debt cancellation plan until the appeals process plays out.

The plan, announced in August, would cancel $10,000 in student loan debt for those making less than $125,000 or households with less than $250,000 in income. Pell Grant recipients, who typically demonstrate more financial need, will get an additional $10,000 in debt forgiven.

The Congressional Budget Office has said the program will cost about $400 billion over the next three decades. James Campbell, an attorney for the Nebraska attorney general’s office, told Autrey at an Oct. 12 hearing that the administration is acting outside its authorities in a way that will cost states millions of dollars.

The cancellation applies to federal student loans used to attend undergraduate and graduate school, along with Parent Plus loans. Current college students qualify if their loans were disbursed before July 1. The plan makes 43 million borrowers eligible for some debt forgiveness, with 20 million who could get their debt erased entirely, according to the administration.

The announcement immediately became a major political issue ahead of the November midterm elections.

Conservative attorneys, Republican lawmakers and business-oriented groups have asserted that Biden overstepped his authority in taking such sweeping action without the assent of Congress. They called it an unfair government giveaway for relatively affluent people at the expense of taxpayers who didn’t pursue higher education.

Many Democratic lawmakers facing tough reelection contests have distanced themselves from the plan.

Biden on Friday blasted Republicans who have criticized his relief program, saying “their outrage is wrong and it’s hypocritical.” He noted that some Republican officials had debt and pandemic relief loans forgiven.

The six states sued in September. Lawyers for the administration countered that the Department of Education has “broad authority to manage the federal student financial aid programs.” A court filing stated that the 2003 Higher Education Relief Opportunities for Students Act, or HEROES Act, allows the secretary of education to waive or modify terms of federal student loans in times of war or national emergency.

“COVID-19 is such an emergency,” the filing stated.

The HEROES Act was enacted after the Sept. 11, 2001, terrorist attacks to help members of the military. The Justice Department says the law allows Biden to reduce or erase student loan debt during a national emergency. Republicans argue the administration is misinterpreting the law, in part because the pandemic no longer qualifies as a national emergency.

Justice Department attorney Brian Netter told Autrey at the Oct. 12 hearing that fallout from the COVID-19 pandemic is still rippling. He said student loan defaults have skyrocketed over the past 2 1/2 years.

Other lawsuits also have sought to stop the program. Earlier Thursday, Supreme Court Justice Amy Coney Barrett rejected an appeal from a Wisconsin taxpayers group seeking to stop the debt cancellation program.

Barrett, who oversees emergency appeals from Wisconsin and neighboring states, did not comment in turning away the appeal from the Brown County Taxpayers Association. The group wrote in its Supreme Court filing that it needed an emergency order because the administration could begin canceling outstanding student debt as soon as Sunday.

U.S. District Judge Henry Autrey wrote that because the six states — Nebraska, Missouri, Arkansas, Iowa, Kansas and South Carolina — failed to establish they had standing, “the Court lacks jurisdiction to hear this case.”

Suzanne Gage, spokeswoman for Nebraska Attorney General Doug Peterson, said the states will appeal. She said in a statement that the states “continue to believe that they do in fact have standing to raise their important legal challenges.”

Democratic President Joe Biden announced in August that his administration would cancel up to $20,000 in education debt for huge numbers of borrowers. The announcement immediately became a major political issue ahead of the November midterm elections.

Barrett, who oversees emergency appeals from Wisconsin and neighboring states, did not comment in turning away the appeal from the Brown County Taxpayers Association. The group wrote in its Supreme Court filing that it needed an emergency order because the administration could begin canceling outstanding student debt as soon as Sunday.

In the lawsuit brought by the states, lawyers for the administration said the Department of Education has “broad authority to manage the federal student financial aid programs.” A court filing stated that the 2003 Higher Education Relief Opportunities for Students Act, or HEROES Act, allows the secretary of education to waive or modify terms of federal student loans in times of war or national emergency.

“COVID-19 is such an emergency,” the filing stated.

The Congressional Budget Office has said the program will cost about $400 billion over the next three decades. James Campbell, an attorney for the Nebraska attorney general’s office, told Autrey at an Oct. 12 hearing that the administration is acting outside its authorities in a way that will cost states millions of dollars.

The plan would cancel $10,000 in student loan debt for those making less than $125,000 or households with less than $250,000 in income. Pell Grant recipients, who typically demonstrate more financial need, will get an additional $10,000 in debt forgiven.

Conservative attorneys, Republican lawmakers and business-oriented groups have asserted that Biden overstepped his authority in taking such sweeping action without the assent of Congress. They called it an unfair government giveaway for relatively affluent people at the expense of taxpayers who didn’t pursue higher education.

Chris Nuelle, spokesman for Missouri Attorney General Eric Schmitt, said the plan “will unfairly burden working class families with even more economic woes.”

Many Democratic lawmakers facing tough reelection contests have distanced themselves from the plan.

The HEROES Act was enacted after 9/11 to help members of the military. The Justice Department says the law allows Biden to reduce or erase student loan debt during a national emergency. Republicans argue the administration is misinterpreting the law, in part because the pandemic no longer qualifies as a national emergency.

Justice Department attorney Brian Netter told Autrey that fallout from the COVID-19 pandemic is still rippling. He said student loan defaults have skyrocketed over the past 2 1/2 years.

The cancellation applies to federal student loans used to attend undergraduate and graduate school, along with Parent Plus loans. Current college students qualify if their loans were disbursed before July 1.

The plan makes 43 million borrowers eligible for some debt forgiveness, with 20 million who could get their debt erased entirely, according to the administration.

Revolutionizing education for careers relying on licensure and certification, while streamlining the learning process to enhance outcomes and save precious time, Career Certified has a unified learning infrastructure to support bold expansion goals

Press Release –

Oct 3, 2022

DENVER, October 3, 2022 (Newswire.com)