LONDON — The British pound is on firmer footing since the appointment of new Prime Minister Rishi Sunak, but Wall Street still sees further vulnerability over the next 12 months.

After falling to a record low against the dollar of below $1.04 on Sep. 25 following the disastrous fiscal policy announcements that would eventually lead to the resignation of former Prime Minister Liz Truss, sterling had recovered to around $1.139 by Thursday morning, but remains down over 15% year-to-date.

Sunak’s planned return to a more traditionally conservative fiscal policy agenda mostly stabilized markets and reduced expectations for more aggressive interest rate hikes from the Bank of England, offering respite to the currency.

In a note Monday, Deutsche Bank vice president and FX strategist Shreyas Gopal said the “crisis” chapter on the U.K. can now close, with the pound now likely to trade as a “normal” currency, but noted that downward pressure from large external financing needs and low real rates remains.

“The U.K.’s external financing needs remain large and, on current market pricing, real yields are still too low compared to other major currencies. As long as the global risk environment remains weak this leaves the pound vulnerable and the likely trend lower,” Gopal said.

The Bank of England is expected to raise interest rates by 75 basis points on Thursday, its biggest hike since 1989, but economists expect the central bank to adopt a more dovish tone and ultimately fall short of the terminal rate of almost 5% priced in by the market.

“In all, we remain bearish on the pound and believe GBP weakness will return for the rest of the year,” Gopal said.

“In the volatility space, the market has rightly assessed that the tails have narrowed for the pound, in line with our view, and we take profit on our short volatility recommendations from earlier this month.”

The U.K.’s long-running current account deficit has been exacerbated by soaring energy prices, which have added almost 2% of gross domestic product to the country’s trade deficit over the past year while placing a historic squeeze on household incomes. U.K. real wages fell at a record rate in the second quarter and inflation hit a 40-year high of 10.1% in September.

Gopal suggested that as a result, private sector savings may fall further in the coming quarters in order to sustain consumption of essential goods, while the government’s new fiscal plans, set to be laid out in full later this month, will likely mean public sector borrowing will exert less downward pressure on the trade balance.

The government has also promised further details on a more targeted version of the Energy Price Guarantee scheme, which will reduce government spending but will further cement the U.K.’s likely recession.

“This should lead to import compression and a (cyclical) improvement in the current account balance — though as a fraction of GDP this impact is likely to be less pronounced,” Gopal said.

“Beyond this, two other offsets include the recent fall in gas prices, with the further from their peak that gas prices settle the better for the external accounts.”

While the recent news flow has been more positive for the U.K. current account, Deutsche Bank does not believe it will prevent external deficits growing “wider than usual and wider than other developed market peers.”

A dovish shift in monetary policy would be seen as negative for the pound given how much tightening is priced in. What’s more, the removal of fiscal support during a particularly tough economic downturn may be “easier said than done,” according to Goldman Sachs.

“Taking these things together, we are revising our Sterling forecasts in a more positive direction, but still expect some further GBP underperformance ahead,” Kamakshya Trivedi, head of global FX, rates and EM strategy at Goldman, said in a note last week.

Goldman last week upgraded its three-, six- and 12-month outlooks for the pound to $1.10, $1.11 and $1.22 from a previous projection of $1.05, $1.08 and $1.19.

Not the last crisis for the UK

Despite the persistent vulnerabilities, however, analysts do not see a return to the record lows seen in late September. In a note Tuesday, BMO Capital Markets suggested that a less hawkish posture from the Bank of England was unlikely to trigger an aggressive near-term sell-off of the pound, nor would a more restrictive stance create buying pressure.

“The U.K. economy and the GBP still have numerous macroeconomic and balance of payments (BoP) headwinds to face. However, one of the more appealing features of the U.K. macro picture is that it’s generally beneficial to be the first to have had a crisis and emerge from it on the other side,” said Stephen Gallo, European head of FX strategy at BMO.

On a longer-term horizon, however, Gallo said the Canadian investment bank was skeptical that 2022 will have marked the last crisis for the U.K., whether around the currency, balance of payments or fiscal policy.

“We would argue that overall UK risk premia should be higher today than during the prior 10-year period. However, the most aggressive phase of the re-pricing seems to be fading in the distance of the rearview mirror,” he added.

After a Covid outbreak at a Foxconn factory in Zhengzhou, China, some workers chose to go home. Pictured here are the shuttle buses on Oct. 30, 2022.

Vcg | Visual China Group | Getty Images

BEIJING — China’s decision to maintain Covid controls is pushing companies to look to factories outside the country, according to The Economist Intelligence Unit.

“What we are hearing from companies [is] they are moving ahead with their supply chain diversification plans because this start-stop economy is here to stay,” said Nick Marro, global trade leader at The Economist Intelligence Unit.

“If it’s an on-off economy, if things can’t get done, that impacts decision-making,” he said. “We don’t expect companies to leave China. We just expect them to diversify their footprint, China plus one.”

Beijing’s stringent Covid controls helped the country resume work while the rest of the world still struggled with the pandemic in 2020. While other countries have relaxed most restrictions and chosen to “live with Covid,” Beijing has increased virus testing requirements and broad controls since Shanghai was locked down for two months earlier this year.

Authorities have tried to keep important factories in production under what’s called a closed-loop system, in which employees live and work at the same site, or at most only travel between work and home.

A Covid outbreak at Apple supplier Foxconn’s factory in the last few weeks shows the continued challenges factories face in trying to maintain operations while keeping infections from spreading.

“I don’t think we can really extrapolate just from one case, but this is noteworthy because it shows a kind of breakdown in that closed-loop system,” Marro said.

Foxconn did not respond to a CNBC request for comment.

“Obviously if they don’t change this Covid zero policy we are going to see cases like this happening again and again,” said Patrick Chen, head of research for CLSA in Taiwan. He said he expects little change in the policy unless vaccination rates increase.

“I don’t see much of an incremental cost associated with these closed-loop management or production, but there will certainly be some negative impact to the employee morale or the overall quality in the production yield,” he said, noting Foxconn has announced monetary incentives to keep employees at the factory.

Typically, Chen said workers at factories like Foxconn’s receive a monthly salary of about $1,000.

While Foxconn’s Zhengzhou factory handles important iPhone manufacturing, Chen said weak demand for the smartphone means production disruptions have less of an impact.

The global smartphone market declined by 12% in the third quarter from a year ago, although Apple held up with slight growth, according to Counterpoint Research.

At the end of the day, it’s that uncertainty which is the biggest problem for investors.

Nick Marro

Economist Intelligence Unit

Just under a third of respondents said they were increasing investment in the country, the survey found. But that figure was down from 38% last year.

CLSA’s Chen said the rising cost of running a sizeable operation in China has prompted tech companies to move manufacturing for less complex products outside the country.

However, he noted it’s difficult for Apple to find another 200,000 to 300,000 workers — as there are at the Foxconn Zhengzhou factory — to make the iPhone outside of China, except in India.

In the last few weeks, China has announced measures to encourage more foreign investment in manufacturing and specific industries such as animation and beer brewing. The level of implementation remains unclear, especially when controlling Covid outbreaks remains the priority for now.

“Foreign businesses want to be in China, and the companies that are still in the market, I think we can take them at face value when they say they are committed to the Chinese market,” EIU’s Marro said. “They are kind of waiting for signals that the operational environment and the macroeconomic environment will improve.”

“The biggest problem is those signals aren’t coming,” he said. “At the end of the day, it’s that uncertainty which is the biggest problem for investors.”

— CNBC’s Arjun Kharpal contributed to this report.

Uber reported a third-quarter loss, but its shares still closed 11% higher after it beat revenue estimates and gave strong fourth-quarter guidance. CEO Dara Khosrowshahi painted an optimistic picture in a prepared statement Tuesday, saying the company delivered a “strong quarter” and is “well positioned to deliver expanding profitability over the coming quarters.” Despite Tuesday’s rally, shares of Uber are still down more than 30% year-to-date — in part due to the broad market weakness this year but also a reflection of continued concerns over Uber’s rising costs and path to profitability. With such a mixed picture, should investors buy the dip on Uber, or should they continue to stay on the sidelines? ‘Not for the faint of heart’ Tech analyst Mark Mahaney believes Uber is “not for the faint of heart” and requires a “patient and long term growth investor.” But he sees the company as the “best way to play the global growth in ride sharing and delivery.” “This is a high-risk asset. But for those who are looking for growth and future profit assets — which is a very tough thing to do in this market — there’s Uber. It’s a company that offers you growth at scale, and we think substantial profitability in the future,” Mahaney, senior managing director and head of the internet research team at Evercore ISI, told CNBC’s “Street Signs Asia” on Wednesday. He said Uber operates in a global ride sharing and delivery market that is valued at $2 trillion. He believes the company is poised to grow its bookings by about 30% from its current customer base of 90 million. While Uber’s growth potential is undeniable, investors have long been skeptical about its ability to do so profitably. But Mahaney believes there is now evidence that Uber has turned a corner — after the company turned free cash flow positive for the first time in the June quarter. The company will generate about $4 billion in free cash flow in 2024 and $5 billion in 2025, he estimates. “If you put reasonable multiples on that, you can get a double in the stock, if you are willing to look out a year or two. So that’s why we like Uber, kind of the best way to play the global growth in ride sharing and in delivery,” he said. Read more ‘Very attractive’: Buy this automaker to play massive pent-up demand in U.S., fund manager says Forget Tesla? Citi and HSBC name 2 alternatives to play the EV boom Goldman’s Jeff Currie reveals ‘the best’ hedge against inflation, rate hikes and geopolitical risks He likens Uber’s current stage of growth to the early days of Amazon , noting that the latter also took many years to reach positive free cash flow, but once that “free cash flow point was reached, things just started spiraling up.” “I’m not sure if [Uber] is as good of a company. But the end markets are extremely large here. And that’s the Uber pitch. It’s still early stage, but you just hit that free cash flow inflection, and you get a lot of market cap creation when that inflection point gets hit,” he said. Mahaney said he finds it “interesting” that Uber is up 50% since the middle of the year. “That’s not arbitrary … It’s popping on free cash flow. The market is now [thinking], we have had two quarters in a row. That’s not a trend, but your 3Q comes in and your 4Q comes, this stock will continue to rerate,” he added. Mahaney said Uber’s higher margin mobility business is now recovering as the pandemic weans, while the company’s regulatory challenges have been “overstated.” “It’s a diversified business. This is not just ride sharing, and it’s not just delivery … the nice cost and revenue synergies between those two segments. And again, it’s the global leader in each of these verticals,” he said. Not real strength Louis Navellier, founder and chief investment officer at Navellier & Associates, believes Tuesday’s rally was merely a “big short covering rally.” “Short covering should never be confused with real strength,” he said. Navellier noted that Uber’s operating earnings are still negative, and he won’t “touch it” till the company “actually earns money.” “And obviously it has another earnings miss on which it likes to do big time. And I just don’t have confidence that they’re going to be able to monetize this,” he said. Even if Uber starts making money, Navellier warned that the current environment of “very low multiples” may be a headwind for the company. “You can see that even when the company starts earning money as Tesla has in recent years, Wall Street still crushed it because the multiple may be too high. We are now in an environment of very low multiples on Wall Street,” he said. To be sure, Navellier is not against buying Uber shares — he’s just not touching the stock for now, given the current challenging macro backdrop. “I realize Wall Street love disruptors … I would put Uber in the disrupter camp and there will be a time for it, but it’s not now. People are just too scared and they’re too conservative. So, it’s just not the time,” he said.

Turns out that jet setter Elon Musk is quite the jet collector.

The billionaire (or billion air?) owner of Tesla, Space X, and recently Twitter, has a small fleet of four private aircrafts— three Gulstreams and one Dassault.

According to a report by news website Austonio, Musk plans to add a new baby to the family. He recently ordered a Gulfstream G700, the latest model from the business jet giant. The plane is expected to be delivered to him in early 2023.

The Gulfstream G700 has an estimated price of $75 million. That sounds like a lot until you compare it to Saudi Prince Al Waleed’s Airbus A380, which goes for a breezy $500 million.

Still, the G700 is something to behold. Gulfstream calls it “the most spacious, innovative, and flexible cabin in the industry.” The galley boasts four living areas, seats up to 19 people, and sleeps up to 13.

The jet’s Rolls-Royce Pearl engines launch it to speeds of 690 mph and can fly 27.5 hours without refueling.

Not to be left out, the pilots also enjoy a first-class travel experience. The state-of-the-art flight deck boasts ten touchscreen monitors, heads-up displays like you’d find on a fighter jet, and sidestick controls.

Musk is sure to put plenty of miles on his new plaything. According to flight records obtained by The Washington Post, he took 250 trips in 2018 across Asia, Europe, Latin America, and the Middle East. Total miles traveled: 150,000.

Nice wings, bad air

But not everyone is celebrating Musk’s recent purchase. Scientists and environmentalists say the climate impact of these private jets is enormous.

A 2021 study by Transport & Environment found that just 1% of people cause 50% of global aviation emissions. The math is not difficult to figure out.

Fewer people flying in bigger, carbon-emitting planes disproportionately impact the environment.

Data shows that the wealthiest 10% in the world are responsible for the same amount of carbon dioxide in a year as the poorest 10% are over in more than two decades.

The Federal Reserve on Wednesday approved a fourth consecutive three-quarter point interest rate increase and signaled a potential change in how it will approach monetary policy to bring down inflation.

In a well-telegraphed move that markets had been expecting for weeks, the central bank raised its short-term borrowing rate by 0.75 percentage point to a target range of 3.75%-4%, the highest level since January 2008.

The move continued the most aggressive pace of monetary policy tightening since the early 1980s, the last time inflation ran this high.

Along with anticipating the rate hike, markets also had been looking for language indicating that this could be the last 0.75-point, or 75 basis point, move.

The new statement hinted at that policy change, saying when determining future hikes, the Fed “will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

Economists are hoping this is the much talked about “step-down” in policy that could see a rate increase of half a point at the December meeting and then a few smaller hikes in 2023.

This week’s statement also expanded on previous language simply declaring that “ongoing increases in the target range will be appropriate.”

The new language read, “The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”

On balance, Powell dismissed the idea that the Fed may be pausing soon though he said he expects a discussion at the next meeting or two about slowing the pace of tightening.

He also reiterated that it may take resolve and patience to get inflation down.

“We still have some ways to go and incoming data since our last meeting suggests that the ultimate level of interest rates will be higher than previously expected,” he said.

Still, Powell repeated the idea that there may come a time to slow the pace of rate increases. He has said this at recent news conferences

“So that time is coming, and it may come as soon as the next meeting or the one after that. No decision has been made,” he said.

The chairman also expressed some pessimism about the future. He noted that he now expects the “terminal rate,” or the point when the Fed stops raising rates, to be higher than it was at the September meeting. With the higher rates also comes the prospect that the Fed will not be able to achieve the “soft landing” that Powell has spoken of in the past.

“Has it narrowed? Yes,” he said in response to a question about whether the path has narrowed to a place where the economy doesn’t enter a pronounced contraction. “Is it still possible? Yes.”

However, he said the need for still-higher rates makes the job more difficult.

“Policy needs to be more restrictive, and that narrows the path to a soft landing,” Powell said.

Along with the tweak in the statement, the Federal Open Market Committee again categorized growth in spending and production as “modest” and noted that “job gains have been robust in recent months” while inflation is “elevated.” The statement also reiterated language that the committee is “highly attentive to inflation risks.”

The rate increase comes as recent inflation readings show prices remain near 40-year highs. A historically tight jobs market in which there are nearly two openings for every unemployed worker is pushing up wages, a trend the Fed is seeking to head off as it tightens money supply.

Concerns are rising that the Fed, in its efforts to bring down the cost of living, also will pull the economy into recession. Powell has said he still sees a path to a “soft landing” in which there is not a severe contraction, but the U.S. economy this year has shown virtually no growth even as the full impact from the rate hikes has yet to kick in.

At the same time, the Fed’s preferred inflation measure showed the cost of living rose 6.2% in September from a year ago – 5.1% even excluding food and energy costs. GDP declined in both the first and second quarters, meeting a common definition of recession, though it rebounded to 2.6% in the third quarter largely because of an unusual rise in exports. At the same time, housing demand has plunged as 30-year mortgage rates have soared past 7% in recent days.

On Wall Street, markets have been rallying in anticipation that the Fed soon might start to ease back as worries grow over the longer-term impact of higher rates.

The Dow Jones Industrial Average has gained more than 13% over the past month, in part because of an earnings season that wasn’t as bad as feared but also due to growing hopes for a recalibration of Fed policy. Treasury yields also have come off their highest levels since the early days of the financial crisis, though they remain elevated. The benchmark 10-year note most recently was around 4.09%.

There is little if any expectation that the rate hikes will halt anytime soon, so the anticipation is just for a slower pace. Futures traders are pricing a near coin-flip chance of a half-point increase in December, against another three-quarter point move.

Current market pricing also indicates the fed funds rate will top out near 5% before the rate hikes cease.

The fed funds rate sets the level that banks charge each other for overnight loans, but spills over into multiple other consumer debt instruments such as adjustable-rate mortgages, auto loans and credit cards.

While the Fed hinted at slowing the pace of interest rate hikes after increasing rates by another 75 basis points today, the market is expected to remain under pressure as a soft landing still looks impossible. However, this bear market also presents the perfect opportunity for bargain hunters to increase stakes in resilient businesses Walmart (WMT) and Gartner (IT) available at attractive valuations before Wall Street realizes their rebound potential. Read on….

shutterstock.com – StockNews

As widely expected, the Fed has raised interest rates by 75 basis points for the fourth consecutive time today. While the central bank intends to reduce the pace in the future, the market volatility is not expected to ease anytime soon, with recession worries remaining intense.

While institutional fund managers on Wall Street sell their stocks and run for the hills to protect their market gains, bargain hunters may consider this golden opportunity to scoop up quality stocks available at discounted valuations.

Therefore, attractively valued stocks of fundamentally strong companies, Walmart Inc. (WMT) and Gartner, Inc. (IT),could be suitable investments before they are in vogue on Wall Street.

As a world-renowned big box retailer, WMT offers opportunities to shop an assortment of merchandise and services at everyday low prices (EDLP) in retail stores and through e-commerce platforms. The company operates through three segments: Walmart U.S.; Walmart International; and Sam’s Club.

On October 27, 2022, WMT and Netflix (NFLX) announced an in-store expansion of the popular Netflix Hub in more than 2,400 stores. It would offer customers a brand-new streaming gift card, fan-favorite exclusives, and more.

On October 26, WMT announced the completion of the renovations made to the retrofitted regional distribution center in Texas, transforming it into a high-tech automation center. This investment is set to modernize Walmart’s vast supply chain network.

Also, on October 26, WMT and ANGI HomeServices Inc. (ANGI) announced the launch of a new product integration where customers who purchase nearly any Christmas lighting from Walmart can easily add installation by a pro on Angi. Since this bundling would provide additional value to customers, it is expected to impact the topline for both companies positively.

For the second quarter of the fiscal year 2023 ended July 2022, WMT’s total revenues increased 8.4% year-over-year to $152.86 billion. The company’s consolidated net income attributable to WMT increased 20.4% from the prior-year period to $5.15 billion, up 23.7% year-over-year. WMT’s total assets stood at $247.20 billion as of July 31, 2022, compared to $238.55 billion a year ago.

In terms of forward EV/Sales, WMT is currently trading at 0.75x, 57.3% lower than the industry average of 1.75x. Also, its forward Price/Sales multiple of 0.65 compares to the industry average of 1.24.

WMT’s revenue and EPS for the fiscal year ending January 2024 are expected to increase 3.1% and 12.8% year-over-year to $613.68 billion and $6.60, respectively. The company has an impressive earnings surprise history since it surpassed consensus EPS estimates in three of the trailing four quarters.

The stock has gained 8.7% over the past month to close the last trading session at $141.69.

WMT’s POWR Ratings reflect solid prospects. The stock has an overall rating of A, equating to a Strong Buy in our proprietary rating system. The POWR Ratings assess stocks by 118 different factors, each with its own weighting.

WMT has grade B for Growth, Stability, Sentiment, and Quality. It is ranked #5 of 38 stocks within the A-rated Grocery/Big Box Retailers industry

Click here to see the additional POWR Ratings of WMT for Value and Momentum.

IT operates as a global research and advisory company. The company operates through three segments: Research; Conferences; and Consulting. It also provides solutions for various IT-related priorities, including IT cost optimization, digital transformation, and IT sourcing optimization.

For the third quarter of the fiscal year 2022 ended September 30, IT’s revenues increased 15.2% year-over-year to $1.33 billion. During the same period, the company’s adjusted EBITDA increased 8.9% year-over-year to $332 million, while the adjusted net income increased 12.2% year-over-year to $193 million. The company’s adjusted EPS came in at $2.41, up 18.7% year-over-year.

In terms of forward P/E, IT is currently trading at 33.07x, 11.6% lower than its 5-year average of 37.40x. The stock’s forward EV/EBITDA multiple of 21.29 is 1.6% below its 5-year average of 21.64. Also, its forward Price/Sales multiple of 4.44 compares with its 5-year average of 3.59.

Analysts expect IT’s revenue for the fiscal year 2022 to increase 13.9% year-over-year to $5.39 billion. The company’s EPS for the current year is expected to increase 3.1% year-over-year to $9.50. The company has topped the consensus EPS estimates in each of the trailing four quarters, extending its impressive earnings surprise history.

Over the past month, the stock has gained 16.5% to close the last trading session at $325.

IT’s strong fundamentals, and steady growth prospects are reflected in its POWR Ratings. The stock has an overall rating of B, which translates to a Buy in our proprietary rating system. It has an A grade for Quality.

We have also given IT grades for Growth, Value, Momentum, Stability, and Sentiment. Get all IT ratings here.

WMT shares were trading at $140.84 per share on Wednesday afternoon, down $0.85 (-0.60%). Year-to-date, WMT has declined -1.50%, versus a -19.84% rise in the benchmark S&P 500 index during the same period.

About the Author: Santanu Roy

Having been fascinated by the traditional and evolving factors that affect investment decisions, Santanu decided to pursue a career as an investment analyst. Prior to his switch to investment research, he was a process associate at Cognizant.

With a master’s degree in business administration and a fundamental approach to analyzing businesses, he aims to help retail investors identify the best long-term investment opportunities.

The Satori Fund founder Dan Niles shares his macro analysis of the large-cap tech sector, when he thinks the market will hit the bottom, and which names he thinks are poised to rebound going into 2023.

Opinions expressed by Entrepreneur contributors are their own.

You are a business owner but aren’t in the tech industry, so why would you need to focus heavily on adapting technology in your daily workflow? Some people may say you don’t need to. However, I’m here to put a bug in your head and prove how technology is critical to any business across any vertical. And that includes you!

We know technology can be intimidating. It also can be complex, and there are seemingly endless options. So, is it worth the cost, integration headaches and question if you are picking the right ones? Yes! Here are my top three reasons to focus on technology, and I’ll explain how to integrate it into your business:

1. Not applying technology means you could face a technology deficit

Let’s face it, not having a line item in your books for technology and software subscriptions means your company will hit a point where you can’t grow any further. Whether your marketing team will be missing major data points for essential customer acquisition or your efficiencies will eventually put you behind, your competition could pass you by (we’ll get to this one more in the next point). No matter the roadblock you will hit, the point is your growth will have to slow down or halt. You don’t want to wait until that point to use technology once the train has left the station without you!

No matter your business or vertical, your most valuable resource is your team. How can you empower your team to work smarter, not harder, and ultimately produce the best results? The answer is with the right technology! Even if your staff has been set in their ways and doesn’t want to learn a new program, you must pick the right operational systems and offer proper training. A minor setback in the learning curve will mean a huge uptick in productivity.

I once ran into a mid-sized company that was technologically behind due to not prioritizing this aspect of its business. This inadequacy caused marketing and sales to lag compared to its competitors. I likened their technological powers and abilities to taking a knife to a gunfight.

If a company can increase its operational automation in the marketing space, that would allow it to understand its target customer and truly understand how to sell to its market in an efficient and results-driven way.

A data warehouse and congruent CRM would allow this business to properly segment and hit goals for its best marketing demographic more accurately. Identifying, understanding and addressing low-hanging fruit, such as abandoned shopping cart funnels, is crucial.

When you are focused on results, technology almost always needs to be integrated to increase efficiencies and drive sales in the long run. And it’s always easier and cheaper to integrate the right technology early to ensure your team is trained and using it along the way!

3. You’re increasing your footprint of liabilities without the right technology

I’ve seen every range of technology integration, from the tech-savvy millennial CEO who relies on data and analytics for every business decision to the companies that don’t integrate it at all and still use a pen and paper within every significant department. However, if you are closer to the latter, you are potentially putting your team at a huge safety risk. If you have only minimal or wrong technology, you could be putting your customers, reputation and finances at risk too!

I’ve even seen clients using only a single source for major bookkeeping and documentation, like Excel. One wrong move or fat-fingered mistake can change your calculations completely. Or worse, delete everything! If that isn’t risky, I don’t know what is.

Technology can feel overwhelming, which is often why we hear people stay away from adding it to their daily workflow. However, there are simple ways to make that change. Start with finding a company to give you a technical audit — which is often cheaper than you might expect. Take their advice and then apply it in chunks.

You may not need to go from 0 to 100 in the first week. You can slowly add, integrate and manage critical technology into various departments as you feel comfortable. And as I mentioned earlier, a key to tech success is training! Empower your team to take the tech leap with you and work on this together. Everyone can learn a new trick, and it could even be fun! Finally, ensure that you have a base infrastructure to make the ideal environment for success. This includes having the basic technology hardware and compatible systems in place.

Take this article as your sign to take the first step and better your business with tech!

Why have stocks jumped from the October lows and more investors have become bullish? But why have many bears refused to throw in the towel? What is it that they see points to lower lows for the S&P 500 (SPY) in the months ahead? Let’s review the updated bull vs. bear debate including how best to trade this tricky market environment.

shutterstock.com – StockNews

There are signs things are getting better on the inflation front. And yet signs that things are getting worse on economic front.

This contradiction creates a very confusing gumbo for investors to digest. And likely explains why we continue to teeter on the edge of bear market territory at 3,855.

Let’s talk about these competing themes and how it has created 2 different scenarios for the stock market outlook. One bullish and one bearish.

I share which scenario is most likely and what it means for our trading plan in this week’s Reitmeister Total Return commentary.

Market Commentary

Let’s start with the Fed’s game plan as clearly spelled out in Chairman Powell’s Jackson Hole speech in August:

This is a long-term battle to get inflation back to 2% target

Do NOT expect lower Fed rates through 2023

Expect “economic pain” which was further described as below trend growth and a weakening of employment.

Now let’s remember that this speech quickly sobered up investors who were enjoying a 18% summer rally up to 4,300 for the S&P 500 (SPY). A month later we were making new lows below 3,600.

The Fed cherishes clarity and consistency in their communication. And thus, I say that any investor who thinks there will be a meaningful change in policy announced Wednesday, only a couple months after the Jackson Hole speech, is smoking something that is still quite illegal.

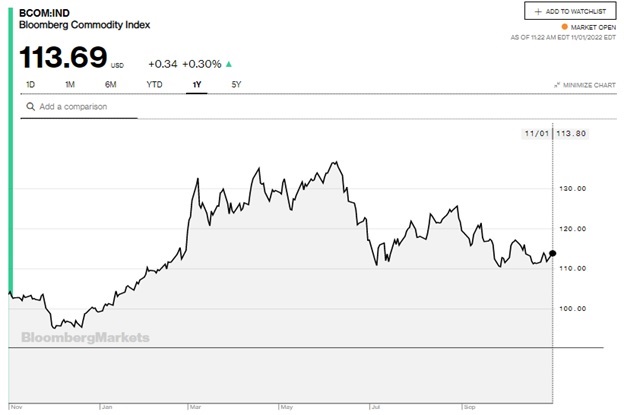

Yet bulls do have some things to cheer such as clear signs of moderating inflation. Almost every key commodity is well off their highs this year. The Bloomberg Commodity Index shows the price trend improving.

This moderation of inflationary pressures is what is behind the hope the Fed will not raise rates as aggressively in the future…and thus would create less damage to the overall economy. This has some folks calling bottom leading to the strong October rally (and hopes for beginning of new bull market).

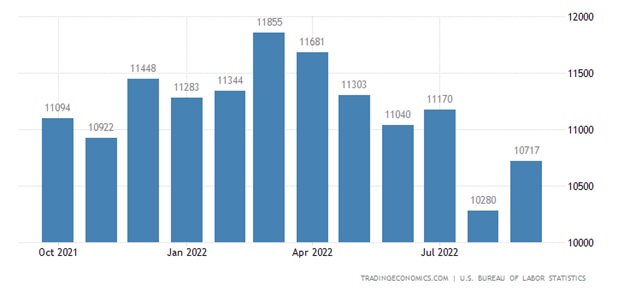

On the other hand, commodity prices are just one part of the inflationary picture. Don’t forget the “stickier” elements such as house prices and rents. Even more important is wage inflation. That got a JOLT in the wrong direction Tuesday morning (pun intended 😉

See below the trend of job openings tracked in the monthly JOLTs report. For the previous 5 months it was trending lower which meant fewer job openings…which pointed to hopefully less wage inflation in the future. That is why the jump in that report Tuesday morning was greeted with an immediate stock sell off as it reignited inflationary fears.

Simultaneously to the JOLTs report was the release of ISM Manufacturing. As expected, that continues to move closer to recessionary levels with a reading of 50.2 with forward looking New Orders component a notch lower at 49.2. (Under 50 = contraction)

Here are some of the key statements recorded by ISM to go along with the Manufacturing report to provide color commentary on what is happening now and what it means for the future (bold put in by me for emphasis):

“Customers are canceling some orders. Inventories of finished goods increasing. Expect some bounce back as some customers may be waiting for commodity prices to decline (further).” [Chemical Products]

“Growing threat of recession is making many customers slow orders substantially. Additionally, global uncertainty about the Russia-Ukraine (war) is influencing global commodity markets.” [Food, Beverage & Tobacco Products]

“We have seen a general pullback in available capital budgets from our customers, and that is having a significant impact on our sales in the fourth quarter.” [Machinery]

“Customer demand has been slower for two months. Production is decreasing our inventory and (we are) implementing forecasts carefully. The headwind seems to be very strong, so we need to be prepared for that.” [Fabricated Metal Products]

“International conditions loom large and seem very foreboding. Overall, we still think 2023 will be a positive year, with at least some moderate growth.” [Nonmetallic Mineral Products]

“Lead times are improving. Plastic prices are coming down.” [Plastics & Rubber Products]

“Prices are continuing a slight decline. Suppliers are trying to hold off decreases, but competition is increasing.” [Miscellaneous Manufacturing]

Net-net these statements reiterate the main point of my commentary today. That being clear signs the economy is slowing. But so too inflationary pressures are easing.

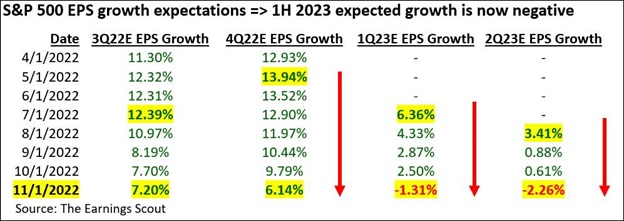

Now let me add one more element to consider before I get to my final conclusions. See the negative trend for the S&P 500 (SPY) earnings outlook as we are now more than half way through Q3 earnings season.

This data shows an across the board reduction in earnings estimates for coming quarters. In particular, you will see that Q1 and Q2 of 2023 are now expected to end with negative growth. This corresponds with a growing number of economists pointing to a recession forming in the first half of 2023.

These statistics were put together by Nick Raich who went on to say that Wall Street is being far too optimistic about the outlook. Meaning that the full measure of estimates cuts are not yet showing up and thus is recommending to clients that they expect more stock price downside until we see more of the typical 15-20% earnings loss that corresponds with recessions.

Now we get down to the tricky part. That being to determine which is the more likely scenario going forward.

Scenario 1: Inflation moderates sooner than expected leading to less total Fed intervention and creation of soft landing for economy. In this case, it is not unreasonable to say that we have reached market bottom and new bull market emerging.

Scenario 2: We have already opened up Pandoras box with the economy. Once the wheels are in motion to move towards recession, then the economy can go through a vicious cycle that grinds lower and lower. In this case the bear market is still in play with likely bottom closer to 3,000.

Which scenario is right?

I believe Scenario 2 is much more likely and why I remain bearish. However, Scenario 1 is a possible outcome that needs to be monitored closely.

Until investors are convinced which scenario is correct, then expect increased volatility as we have seen this past week. Heck, Tuesday alone was a prime example.

That being where the market opens up +1% and then immediately gives it all back and then some after the JOLTs and ISM Manufacturing reports. Then it stuck like glue around 3,855 which is an interesting support/resistance level.

Remember that 3,855 is the bear market dividing line representing a 20% drop from the all time highs of 4,818. That is as good of spot as any to have a tug of war over the future of the stock market.

Given history, the odds of soft landing are very low. Famed investor Mohamed El-Erian talks about the same thing in this new article: Chances of Soft Landing are “Meager”.

Like El-Erian, my outlook skews bearish. That is why my portfolio is constructed to profit as stock prices head lower.

However, I am sleeping with one eye open for the possibility that the soft landing scenario does emerge victorious where I would gladly switch to a more bullish stance.

Unfortunately, with the jobs market still too hot, then that inflationary pressure alone will keep the Fed on a rate hike war path which doesn’t end favorably for the economy and stock prices.

What To Do Next?

Discover my special portfolio with 9 simple trades to help you generate gains as the market descends further into bear market territory.

This plan has been working wonders since it went into place mid August generating a robust gain for investors as the S&P 500 (SPY) tanked.

And now is great time to load back up as we make even lower lows in the weeks and months ahead.

If you have been successful navigating the investment waters in 2022, then please feel free to ignore.

However, if the bearish argument shared above does make you curious as to what happens next…then do consider getting my updated “Bear Market Game Plan” that includes specifics on the 9 unique positions in my timely and profitable portfolio.

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”) CEO, Stock News Network and Editor, Reitmeister Total Return

SPY shares were trading at $384.97 per share on Tuesday afternoon, down $1.24 (-0.32%). Year-to-date, SPY has declined -18.01%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

The ongoing change in consumer behavior has led many businesses to reimagine and rebuild their digital marketing efforts, as social media now makes up for a majority of online interaction and digital communication between brands and consumers.

Due – Due

Advancements in tech gave access to consumers for social media

Advancements in technology and software gave way to the widespread adoption of several innovative digital tools. These tools include the Internet of Things (IoT), mobile networks, and technologies that once seemed foreign to consumers. On the back of this upgrade, we now see businesses having better access to markets and consumers previously considered remote or out of reach.

Many more consumers are online, working from home

As a growing number of consumers move their work, studies, and leisure interests online — the same majority of online users are being shaped into social media users at the same time.

Social media has perhaps surpassed its original definition; today, it’s become an online ecosystem that brings users closer to each other. But at the same time, users are in direct contact with the brands or businesses they would interact with regularly.

Social media is the way forward for small businesses

Today we see more than 4.26 billion social media users worldwide, according to recent figures by Statista. This figure is set to increase over the coming years, visiting more than 6 billion global citizens using social media by 2027.

Against this backdrop, we’re seeing businesses taking better advantage of social media and what it can do for their business growth prospects.

Social media is a fantastic marketing tool

Social media has become a marketing tool, a consumer-focused platform that utilizes several advanced tech capabilities. For example, deep machine learning and Artificial Intelligence (AI), among other business tools, help businesses to reach the right target audience and to get deeper analytical insight into their growing customer base.

Social media has proven its business success, and it’s talking loud and clear.

According to a Harris Poll on behalf of Sprout Social, around 55% of consumers are learning about new brands online or through social media. Additionally, 43% of consumers are increasing their social media activity to discover new products and services.

More so, around 80% of company executives believe investing in social media tools and tactics is crucial for business growth and development.

With more than 160 million businesses already using popular social media sites such as Facebook and now Meta, consumers remain interested in the brands and companies that can add a human personality to the business or organization.

While growth has remained steady, and consumer interest remains elevated, keeping social engagement online means that businesses will need to upscale their efforts with the right automation tools while at the same time ensuring proper marketing budget allocation that will build strong brand loyalty among the online community.

Each question helps build a loyal following through constant engagement — but requires having the right automation tools to bring the brand to life.

Aside from this, automated social media tools — you’ll want to ensure ongoing commitment to mundane social and digital marketing tasks.

The digital ad options for social media

With an array of digital ad options, choosing an automation software tool that fits your small business needs can seem daunting.

In the following list, we briefly discuss the most popular and widely used automation tools being used by businesses across a spectrum of different industries.

SocialPilot

SocialPilot offers small to medium enterprises a simple yet versatile social media automation tool that provides them with a full range of features, from calendar and client management to content curation and media scheduling.

On top of the basic features included within the SocialPilot product offering, businesses will see a range of scheduling features that automate reels, stories, images, text, and video posting from a single launching pad.

Perhaps one of the more striking features is the helpful analytics business owners can download onto their computers in PDF format. Any growing business must consider the analytical aspects of its social media engagement to build a strong performing social media marketing strategy.

Sprout Social

One of the more familiar names when it comes to social media automation tools, SproutSocial has a broad range of capabilities, including engagement analytics and various publishing features.

Although considered one of the more advanced automation options on the market, Sprout Social has become a trusted household name among digital marketers and small business owners. Sprout Social gives businesses more leverage to utilize several publishing and automation tools to help build robust engagement.

At the core of Sprout Social is Sprout Queue, simple software that makes it possible for any person to line up several posts at preset times.

On top of this, the Sprout Queue features also give users better insight into when their audience is most active online, allowing them to line up their posts according to these times.

Buffer

Buffer is affordable and straightforward enough for any small business owner or entrepreneur to use and requires a minimal workforce when getting started.

Like similar automation tools, Buffer makes it easy for users to schedule and publish their online content and preset times or days.

The automated publishing features can work across multiple accounts, making it much less tedious to keep track of content management and reporting across various social media accounts.

Basic features that come with their lower-tier pricing include automated publishing, content management, and post-scheduling, among others.

Another robust feature integrated within the platform is machine learning which automatically detects when a post receives a question or comment to help users prioritize swift responses.

Buffer is nimble, but some more advanced features will have users paying somewhat more, but even at that price point, it’s still more affordable than other popular automated tools.

BuzzSumo

While not primarily seen as an automated posting tool, BuzzSumo gives business owners a more extensive understanding of managing their content marketing strategies.

For those only starting with their social media marketing strategies, BuzzSumo might initially seem a bit too intimidating. Still, with integrated analytic tools that work across popular social media platforms, users will have a deeper insight into the performance of their posts.

While it may take a bit more time to become comfortable with the range of features and tools, BuzzSumo helps business owners research the proper online and social media trends within their respective industries.

Sendible

Working on Sendible helps users manage their content and social media campaigns from a single dashboard while simultaneously ensuring one-by-one campaign scheduling for various social media accounts.

A prominent drawing point of Sendible is that it allows users to schedule their content a week or month in advance; more so, it’s possible to automate scheduling for as long as one needs.

Additionally, there is space for users to seamlessly curate content according to different social media platforms and include several striking features such as emojis, attachments, and more.

Although there is a robust offering of services and features, pricing might seem a bit out of range for the average small business owner. This is perhaps one of the most significant drawbacks, but if one can look past the higher subscription costs, Sendible is a powerful tool nonetheless.

CoSchedule

To help small business owners streamline their projects better and organize all their social media content more seamlessly, CoSchedule combines conventional features and advanced capabilities on a core management dashboard.

With CoSchedule, users can focus on various social media projects at once while at the same time working across several social channels.

As with some other automation tools, CoSchedule allows one to upload and schedule up to 365 social media posts at once, translating into roughly one year worth of planning that can be done in a single sitting.

Running recurring campaigns and top-performing content is also a bit easier as the platform’s ReQueue features allow for ongoing analytics insight and content automation.

Meetedgar

Perhaps not the most widely known social media automation tool out there, Meetedgar offers a unique service offering that makes it a lot simpler and easier to schedule posts across different platforms, including Facebook, Instagram, Twitter, Pinterest, and LinkedIn.

Although their relatively unique offering isn’t that different from what one will get on other platforms, it does come with a category-based option, allowing users to schedule posts according to different categories and arrange them as needed.

While Meetedgar is simple enough for anyone to use, it does mean that some other vital features might not be included, making scheduling posts harder to manage as the business and social media grow.

PromoRepublic

PromoRepublic does hit all the spots regarding social media management and calendar scheduling. Still, on top of this, it includes an attractive design feature that allows users to access a library of more than 100,000 visual templates.

The emphasis on design means that users will constantly have access to creative and exciting templates that they can incorporate with their social media strategies, making it much easier to publish engaging posts.

There are some other interesting features, such as graphics editor tools and analytic reports. Still, seeing as the design takes up a sizable portion of PromoRepublic’s base, it does make it harder to integrate with other apps seamlessly, and there are no collaboration features that can be used with other businesses and clients.

NapoleonCat

Think of NapoleonCat as the deep machine and AI-rich automation tool that helps users to set predetermined responses for repetitive questions in comments or private messages. Although social media channels such as Facebook and Instagram already allow business owners to set up automated responses, NapoleonCat does that and makes room for post automation all in one simple dashboard.

Among its robust features, users can enjoy post scheduling for multiple platforms and profiles while also managing several platforms, including Facebook, Instagram, Twitter, Youtube, and Google My Business, among other popular platforms. There is also a report feature, which can give more analytical insight into post and strategy performance.

Despite the weight NapoleonCat carries, it does come with a 24-hour wait period to download data from new profiles. On top of this, users may feel that the user interface is somewhat outdated in terms of what the program can do.

SocialBee

For bloggers, journalists and writers, SocialBee is a straightforward social media publishing tool that helps users to construct a posting strategy around new blog posts. This is done through the RSS functionality that automatically allows users to create new posts whenever they publish online content.

There is also a feature that gives the option to organize different posts into several categories, which means that social media feeds will be more diversified and remain engaging at all times.

Like other previously mentioned tools, SocialBee has a robust analytics feature, and there is an option to set up time-sensitive posts that can be removed after a preset time. All-in-all, it’s a decently priced automation tool, but some business owners might not find all the right tools they are looking for from the get-go.

To finish off

As a business owner, there is a lot to consider in terms of social media marketing and building an online reputation through social interaction and constantly keeping followers engaged with creative yet high-quality content.

For bust business owners, there is an array of social media automation tools that makes the posting and engagement work a lot more manageable while at the same time helping them build a striking image and online brand.

These tools are only at the very start of their existence. We can expect in the near future that similar platforms will become more advanced.

Delivering innovative features is a current quest from many social media automation tools.

The future will see better and more advanced tools and social media strategies that will take us to the next level –all within one simplified ecosystem.

The U.S. central bank has raised the benchmark short-term borrowing rate a total of six times this year, including 75 basis point increases in June, July and September, in an effort to cool down inflation, which is still near 40-year highs and causing most consumers to feel increasingly cash strapped. A basis point is equal to 0.01 of a percentage point.

A policy statement after the announcement noted that the Fed is considering the “cumulative” impact of its hikes so far when determining future rate increases. Economists are hoping this signals plans to “step-down” the pace of increases going forward, which could mean a half point hike at the December meeting and then a few smaller raises in 2023. Still, stocks tumbled after Federal Reserve Chair Jerome Powell said there were more rate hikes ahead.

“Americans are under greater financial strain, there’s no question,” said Chester Spatt, professor of finance at Carnegie Mellon University’s Tepper School of Business and former chief economist of the Securities and Exchange Commission.

The federal funds rate, which is set by the central bank, is the interest rate at which banks borrow and lend to one another overnight. Although that’s not the rate consumers pay, the Fed’s moves still affect the borrowing and saving rates they see every day.

By raising rates, the Fed makes it costlier to take out a loan, causing people to borrow and spend less, effectively pumping the brakes on the economy and slowing down the pace of price increases.

“Unfortunately, the economy will slow much faster than inflation, so we’ll feel the pain well before we see any gain,” said Greg McBride, Bankrate.com’s chief financial analyst.

Already, “mortgage rates have rocketed to 16-year highs, home equity lines of credit are the highest in 14 years, and car loan rates are at 11-year highs,” he said.

• Mortgage rates are already higher. Even though 15-year and 30-year mortgage rates are fixed and tied to Treasury yields and the economy, anyone shopping for a home has lost considerable purchasing power, in part because of inflation and the Fed’s policy moves.

Along with the central bank’s vow to stay tough on inflation, the average interest rate on the 30-year fixed-rate mortgage hit 7%, up from below 4% back in March.

On a $300,000 loan, a 30-year, fixed-rate mortgage at December’s rate of 3.11% would have meant a monthly payment of about $1,283. Today’s rate of 7.08% brings the monthly payment to $2,012. That’s an extra $729 a month or $8,748 more a year, and $262,440 more over the lifetime of the loan, according to LendingTree.

The increase in mortgage rates since the start of 2022 has the same impact on affordability as a 35% increase in home prices, according to McBride’s analysis. “If you had been approved for a $300,000 mortgage in the beginning of the year, that’s the equivalent of less than $200,000 today.”

For home buyers, “adjustable-rate mortgages may continue to be more popular among consumers seeking lower monthly payments in the short term,” said Michele Raneri, vice president of U.S. research and consulting at TransUnion. “And consumers looking to tap into available home equity may continue to look towards HELOCs,” she added, rather than refinancing.

Yet adjustable-rate mortgages and home equity lines of credit are pegged to the prime rate, so those will also increase. Most ARMs adjust once a year, but a HELOC adjusts right away. Already, the average rate for a HELOC is up to 7.3% from 4.24% earlier in the year.

• Credit card rates are rising. Since most credit cards have a variable rate, there’s a direct connection to the Fed’s benchmark. As the federal funds rate rises, the prime rate does as well, and your credit card rate follows suit within one or two billing cycles.

That means anyone who carries a balance on their credit card will soon have to shell out even more just to cover the interest charges. “This latest interest rate hike will most acutely impact those consumers who do not pay off their credit card balances in full through higher minimum monthly payments,” Raneri said.

Because of this rate hike, consumers with credit card debt will spend an additional $5.1 billion on interest, according to an analysis by WalletHub. Factoring in the rate hikes from March, May, June, July, September and November, credit card users will wind up paying around $25.6 billion more in 2022 than they would have otherwise, WalletHub found.

Already credit card rates are near 19%, up from 16.34% in March. “That’s the highest since the Fed began tracking in 1994 and is more than a full percentage point higher than the previous record set back in 2019,” according to Matt Schulz, chief credit analyst at LendingTree. And rates are only going to continue to rise, he said. “We’ve still got a ways to go before those rates hit their peak.”

The best thing you can do now is pay down high-cost debt — “0% balance transfer credit cards are still widely available, especially for those with good credit, and can help you avoid accruing interest on the transferred balance for up to 21 months,” Schulz said.

“That can be an absolute godsend for folks struggling with card debt,” he added.

Otherwise, consolidate and pay off high-interest credit cards with a lower-interest home equity loan or personal loan, Schulz advised.

• Auto loans are more expensive. Even though auto loans are fixed, payments are getting bigger because the price for all cars is rising along with the interest rates on new loans, so if you are planning to buy a car, you’ll pay more in the months ahead.

The average interest rate on a five-year new car loan is currently 5.63%, up from 3.86% at the beginning of the year and could surpass 6% with the central bank’s next moves, although consumers with higher credit scores may be able to secure better loan terms.

Paying an annual percentage rate of 6% instead of 5% would cost consumers $1,348 more in interest over the course of a $40,000, 72-month car loan, according to data from Edmunds.

Still, it’s not the interest rate but the sticker price of the vehicle that’s causing an affordability problem, McBride said. “Rising rates doesn’t help, certainly.”

• Student loans vary by type.Federal student loan rates are also fixed, so most borrowers won’t be affected immediately. But if you are about to borrow money for college, the interest rate on federal student loans taken out for the 2022-2023 academic year are up to 4.99%, from 3.73% last year and 2.75% in 2020-2021.

If you have a private loan, those loans may be fixed or have a variable rate tied to the Libor, prime or T-bill rates, which means that as the Fed raises rates, borrowers will likely pay more in interest, although how much more will vary by the benchmark.

Currently, average private student loan fixed rates can range from 3.22% to 14.96%, and from 2.52% to 12.99% for variable rates, according to Bankrate. As with auto loans, they vary widely based on your credit score.

• Only some savings account rates are higher. The silver lining is that the interest rates on savings accounts are finally higher after several consecutive rate hikes.

Thanks, in part, to lower overhead expenses, top-yielding online savings account rates are as high as 3.5%, according to Bankrate, much higher than the average rate from a traditional, brick-and-mortar bank.

“Savers are seeing the best yields since 2009 — if they’re willing to shop around,” McBride said. Still, because the inflation rate is now higher than all of these rates, any money in savings loses purchasing power over time.

Now is the time to boost that emergency savings, McBride advised. “Not only will you be rewarded with higher rates but also nothing helps you sleep better at night than knowing you have some money tucked away just in case.”

“More broadly, it makes sense to be more cautious,” Spatt added. “Recognize that employment is maybe less secure. It’s reasonable to expect we’ll see unemployment going up, but how much remains to be seen.”

Traders are trying to sniff out a pivot from the Federal Reserve, and that means investors should start thinking about how to change their portfolios if interest rates start to fall. The Fed is expected to hike its benchmark rate by 0.75 percentage point Wednesday, but some central bankers have signaled that they are worried about going too far and causing a recession. That means that market rates could fall, even if the Fed continues to hike for the next few months. This is especially true for longer-dated bonds, which are less sensitive to the meeting-to-meeting changes by the Fed and more reflective of long-term expectations. The 10-year Treasury yield has already eased off its highs from mid-October. This means it may be time to turn the page in the playbook for investors. The most direct way to play this phenomenon would be to buy Treasury ETFs. Bond yields move opposite of price, so the ETFs should go up in value. And because yields are so high, the funds should still feature solid income for investors — even if the Fed starts to cut rates next year. There are several large ETFs on the market focused on Treasurys, including the iShares’ 7-10 Year Treasury Bond ETF (IEF) and 20+ Year Treasury Bond ETF (TLT) . They both have fees of 0.15%. Similarly, Vanguard offers the Intermediate-Term Treasury ETF (VGIT) , which has a fee of just 0.04%. Corporate bonds carry more risk than Treasurys, but should rally if Treasury yields fall. Intermediate-Term Corporate Bond Index Fund ETF (VCIT) also has an expense ratio of 0.04%. There are also some equity funds that were hit particularly hard by higher rates, and they could be due for a relief rally in store when rates fall. However, these could be riskier than the Treasury funds because the Fed is concerned about a recession, which could hurt these stocks even if rates fall. One of those areas is homebuilders. The U.S. housing market has slowed sharply as interest rates have soared, and the SPDR S & P Homebuilders ETF (XHB) has fallen more than 30% year to date. A recession could mean that housing continues to struggle, but consumers and builders may be comfortable taking on new projects if they believe mortgage rates have topped out. Growth stocks are another group that could benefit from a decline in rates. These companies are often valued based on far-off earnings, which become less attractive when discount rates are higher. Passive funds like the iShares Russell 1000 Growth ETF (IWF) could offer a relatively cheap way to get exposure to these types of stocks. That may make funds like the Invesco S & P 500 GARP ETF (SPGP) , focused on growth at a reasonable price, worth a look. The fund has an expense ratio of 0.33%, but it carries a five-star rating from Morningstar.

There’s something about the latest crypto crash that makes it different from previous downturns.

Artur Widak | Nurphoto | Getty Images

The ongoing crypto winter is “only going to get worse” as the industry recalibrates to a higher interest rate world, according to the co-founder of blockchain platform Tezos.

Asked about the fall in price of many crypto assets this year, Kathleen Breitman said: “A lot of this was inflated on cheap money, and a lot of this was backed by basically, like, VCs trying to pump.”

“There was a lot of easy money going into the system and I think it was artificially stoking a number of different things, mainly valuations of these companies,” she told CNBC’s Karen Tso Wednesday at the Web Summit conference in Lisbon, Portugal.

Breitman cited NFT marketplace OpenSea, where trading volume plunged from $2.9 billion in September 2021 to $349 million in September 2022, according to data from Dune Analytics.

“Clearly there is a phenomenon that has kind of crested and gone away in a lot of these markets, but meanwhile they’re saddled with a $13 billion valuation,” Breitman said.

“So I think there’s a lot of cheap money that went in, valuations went super sky high, you had people scrambling to make those valuations justified in some form, usually through cheap tactics like yield farming, and now that the easy money’s gone away, all that’s left is we’re getting communities, I hope,” she continued.

On whether the pause in Federal Reserve rate hikes that economists expect next year could see crypto markets rally, Breitman said there would still be a shift in crypto and tech valuations being based on anticipatory benefits to actual user growth; and without the ability to keep using “cheap tactics” to get “easy come, easy go” users in the door.

“Crypto hasn’t been evaluated by that metric, and neither has technology in the last 10 years that we’ve had low interest rates,” Breitman told CNBC. “It remains to be seen, but basically I think what you’ll find is the things that are useful are going to thrive.”

“But that’s the small minority of crypto applications, whether people want to admit it or not.”

Tezos, which Breitman also co-founded, is a smart contract platform, like the better-known Ethereum, but that allows token holders to vote on changes to the platform before they are enacted every few months.

Usage of the network has increased on 2021, Breitman said, driven by demand from the art world, where digital artists are minting art on the blockchain and trading it. This use is providing one of the only sources of organic growth in the industry more broadly, she said.

The notion of the end of the era of easy money in crypto is one that analysts have been discussing in recent months amid the downturn.

Some industry figures believe the recent relative price stabilization of assets such as bitcoin, which has been trading between $18,000 and $25,000 for the last four months after experiencing massive volatility, is positive for the industry.

Antoni Trenchev, co-founder of crypto lender Nexo, previously told CNBC bitcoin’s performance was “a strong sign that the digital assets market has matured and is becoming less fragmented.”

Correction: The text of this story been been updated to accurately describe Kathleen Breitman’s job title.

European gas prices are expected to drop to 85 euros megawatt hour in the coming months, said Goldman Sachs

Krisztian Bocsi | Bloomberg | Getty Images

Goldman Sachs predicts that European natural gas prices would drop by about 30% in the coming months as nations gain a temporary upper hand on supply issues.

The Dutch Title Transfer Facility (TTF) is Europe’s main benchmark for natural gas prices. It traded at around 120 euros per megawatt hour on Tuesday. But Goldman Sachs expects this benchmark to fall to 85 euros per megawatt hour in the first quarter of 2023, according to a research note published last week.

This would mark a significant change to the levels seen back in August. At the time, Russia’s unprovoked invasion of Ukraine and the subsequent pressures on Europe’s energy mix pushed prices to historic figures — above 340 euros per megawatt hour.

The recent cooling in gas prices has derived from several factors: Europe’s gas storage is basically full for this winter season; temperatures this fall have been milder than expected thus delaying the start of a period of heavy usage; and there is an oversupply of liquefied natural gas (LNG).

Recent reports have pointed to about 60 vessels waiting to discharge their LNG cargo in Europe. Some of these shipments were bought during the summer and are just arriving now as storage fills up. Indeed, the latest data compiled by industry group Gas Infrastructure Europe shows storage levels in Europe are sitting at 94%.

Despite optimism on lower gas prices in the near term, which may alleviate some of the cost-of-living crisis, there’s plenty of pressure on European leaders to secure supplies in the medium term.

“Our commodity team forecasts a further decline to 85 euros in the first quarter before sharply picking up into next summer as storage levels are rebuilt,” Goldman Sachs analysts said in the research note. Their forecasts point to a surge in prices to just below 250 euros per megawatt hour by the end of July.

Natural gas prices are expected to pick up after the first three months of 2023 due to several factors.

Fatih Birol, executive director of the International Energy Agency, told CNBC’s Julianna Tatelbaum Friday that only a very small amount of new LNG will hit the market next year. “If China economy sees a rebound, next year the LNG import of China may also increase together with Europe,” he said.

Read more about energy from CNBC Pro

China was the world’s top importer of LNG in 2021, according to the U.S. Energy Information Administration. However, due to its strict Covid-19 policy, the Chinese economy has had to deal with a number of lockdowns which have dented growth. Any change in this political approach would increase demand for LNG and push up prices for European buyers too.

Additionally, gas storage has been helped by Russian supplies which the EU has been trying to ween itself off. Even Xavier Bettel, the prime minister of Luxembourg, an EU nation, acknowledged in October that storage was full with Russian gas. Russian supplies have since been severely disrupted and it’s Europe’s aim to be completely free from Russian fossil fuels.

The CEO of EDP, Portugal’s utilities firm, summed it up when speaking to CNBC’s “Squawk Box Europe” Friday. “Certainly we are in a much better place than we were a couple of months ago,” Miguel Stilwell d’Andrade said, but “we should expect a lot of volatility going forward.”

In June 2020, Warner Music Group Corp. (NASDAQ:WMG) made some noise when it announced its arrival as a publicly traded music player. Press the fast-forward button and two years later, the company’s stock dipped below IPO levels.

MarketBeat.com – MarketBeat

As the music industry conglomerate slid into the low-20’s, the market tuned out talk of a comeback tour and volume dried up big time. That changed dramatically last week.

The trading volume was on full blast after Apple announced a plan to raise its prices on Apple Music and Apple TV+ (as well as the Apple One bundle which includes both services).

Warner Music Group shares jumped more than 8% on the news and continued to see elevated activity throughout the week. Spotify also moved higher.

Let’s listen in to why this is a potential catalyst for the group.

Why is Apple’s Price Increase Good For Warner Music Group?

Like everything else, consumers are paying more to listen to their favorite artists and binge-watch their favorite shows these days. Last week, Apple became the latest to hike the cost of its streaming services following Netflix, Disney+ and others.

Monthly subscriptions to Apple Music and Apple TV+ are going up by $1 and $2 respectively. This brings Apple Music to $10.99 per month and the Apple One bundle to $16.95 for individual plans.

Why? With licensing fees on the rise, content creation is getting more expensive. Meanwhile, ad spending is slowing. As a result, the consumer is asked to pay more and the streamers potentially make more.

Apple’s move impacts music services like WMG, Spotify, and Universal Music Group because these competitors are likely to raise their own prices. Spotify hasn’t budged from its $9.99 rate for over 10 years but management hinted at U.S. price hikes in its Q3 earnings call.

Warner Music Group is a special case. In addition to its digital music offerings, the company sells a full slate of old school vinyl, cassettes and CDs across music genres. All of these prices along with those of the clothing and accessories available at the Warner Music Store stand to trend higher. And absent a parallel increase in costs, WMG stands to rake in greater profits.

Near-term inflationary pressures aside, Apple’s decision signals that the streaming music industry has pricing power and a positive growth outlook. The company wouldn’t bump prices if it didn’t anticipate consumers will pay up, which suggests streaming demand will persevere over the long haul.

The ripple effect of the Apple increase is also a boon to content creators themselves. When prices go up, artists and songwriters bank more when their stuff gets streamed.

What is Warner Music Group’s Growth Strategy?

When you own four top record labels as WMG does, the growth can come from anywhere. Atlantic Records, Warner Records, Elektra and Parlophone make the company a greatest hits collection for all things music. Add in all the other music labels under the Warner umbrella and you get a catalog of more than 1.4 million copyrights, including classic and modern hits alike.

It is the diversified revenue streams that make WMG intriguing from an investment perspective. The below industry P/E and 2.4% dividend aren’t too shabby either.

Even though Warner Music covers all music mediums, digital is the clear growth driver. It’s no secret the world is shifting to streaming music platforms, leaving nostalgic physical music playing second fiddle.

In fiscal Q3, revenue increased 12% and profits more than doubled. The consolidated streaming business was a solid contributor and is expected to be leaned on going forward.

So too is international expansion. New music service launches like The Music Station creative hub in Spain and Warner Music Israel stand to augment growth. The company also recently partnered with Polish concert promoter BIG Idea.

And no media conglomerate would be complete without NFT exposure. A collaboration with Bose on the Stickmen Toys NFT collection peaked at the number two spot on Open Sea for 24-hour volume and topped the one thousand Ethereum milestone.

Will Warner Music Group Stock Keep Going Up?

Price increases seem likely to happen at Warner Music Group. Given the popularity of its artist portfolio and streaming services, this could send growth to higher decibels in 2023.

Prior to the Apple news, Wall Street was mostly bullish on WMG’s long-term prospects. Price increases that are absorbed by loyal music fans should only support this.

In fact, the last six research firms’ opinions of the stock have been bullish. A few weeks back, Goldman Sachs started coverage with a buy rating. This set the stage for others to chime in with buy ratings and similar targets, which imply at least 10% upside from here.

This would bring the stock back to its IPO level and a potential new base to build on. Yes, it’s been a rocky Nasdaq debut for WMG, but the band of buyers may be getting back together.

The Federal Reserve is expected to raise interest rates by three-quarters of a percentage point Wednesday and then signal that it could reduce the size of its rate hikes starting as soon as December.

Markets are primed for the fourth 75-basis point hike in a row, and investors are anticipating the Fed will slow down its pace before winding down the rate-hiking cycle in March. A basis point is equal to 0.01 of a percentage point.

“We think they hike just to get to the end point. We do think they hike by 75. We think they do open the door to a step down in rate hikes beginning in December,” said Michael Gapen, chief U.S. economist at Bank of America.

Gapen said he expects Fed Chair Jerome Powell to indicate during his press briefing that the Fed discussed slowing the pace of rate hikes but did not commit to it. He expects the Fed would then raise interest rates by a half percentage point in December.