Automating your finances generally means setting up automatic payments for bills and recurring investment or savings deductions from your bank account. It may sound tedious to set up but once most bill payments are automated, experts say it can bring structure to your finances and set your budget up for success.

“It goes a long way to automate things and make your life easier,” Marques said. “Even if you’re quite a proactive person, it just makes it easier to stay on track and ensure that you’re making progress toward your goals.” She said it takes away the ability to negotiate with yourself. For example, people with a spend-first mindset might put off savings contributions. But if that amount is automated, it is easier to think of it as a bill. “You just get it done,” she said.

Automation supports, not replaces, budgeting

Another benefit is avoiding late fees or charges on bills and credit cards. Marques said anything from rent to utilities to savings to investing can be automated. For variable bills, such as a credit card, she suggested automating the credit card bill payment at a minimum amount and paying off the rest manually each month.

But automation doesn’t replace the need for budgeting. Budgeting will always be a key pillar in personal finance planning, said Michael Bergeron, certified credit counsellor and manager at Credit Canada. “The automation just supports. It’s a strategy that helps us stay within our budget,” he said. For example, if you’ve paid off your debt, that money can now be automated to allocate elsewhere, such as savings or investments—and that insight only happens when you keep up with your budget.

Know what can (and can’t) be automated

However, many people don’t know how to automate payments. Bergeron said the first step to automation is having a structured budget, which caters to needs, wants, and other priorities. “Once we have a structured budget in place, then we can look at what are we going to automate,” he said.

Marques said a simple way to know what can be automated is by listing all your fixed recurring expenses, such as rent or mortgage, car insurance, and phone bill, among others. Then, look at the days you get paid and start aligning bill payments and savings to your paydays. For example, fixed payments, such as rent, can be aligned with the paycheque that comes in right before the due date and can be set up for automatic deductions. Most recurring payments for bills and savings can be easily set up with online banking platforms or utility services such as network providers or insurance firms.

Bergeron said people still need to keep a close eye on their bank statements to make sure there are no double charges, technical errors, or overdraft charges. Also, some automation setups may have an end date, which means you’d have to reset the payments. “If you don’t pay close attention to that, then obviously some missed and late payments could take place,” he said.

It’s likely not possible to automate all your variable expenses, such as grocery bills or fuel expenses. “There will always be some form of money management structure that you have to manually take the lead on to make sure we’re following our budget to the best of our capabilities,” he said.

Article Continues Below Advertisement

While automation is likely to work for most people, Bergeron said it could be challenging for those who aren’t technologically savvy. He said if there’s a barrier, he doesn’t recommend automating finances until they understand the value and benefits of it. “But for the majority, it is a highly valued benefit for most people,” Bergeron said.

Get free MoneySense financial tips, news & advice in your inbox.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

Budgets aren’t just for businesses and governments — families need them too. But in 2025, keeping one was no easy task. Here are financial tips for 2026.

Budgets aren’t just for businesses and governments — families need them too. But in 2025, keeping one was no easy task. From furloughs to inflation, many personal budgets were pushed to the brink, Harrine Freeman, CEO of H.E. Freeman Enterprises, told WTOP.

“A lot of things have happened this year to kind of throw people off their square and it makes it difficult to stay on track with your budget,” Freeman, leader of the D.C.-based financial planning company, said.

She said many families faced reduced income, medical issues and new caregiving responsibilities, which made budgeting even harder. Some had to cut holiday costs by asking relatives to bring food or stay in rental houses instead of hosting for a week.

For those who went off track, Freeman said the priority now is getting back on track and learning from mistakes.

Start by deciding why you want a budget, she said. Do you want to manage spending, recover from a financial crisis or save for something big?

“It’s easier to create a budget or stick to it when you have a goal associated with it,” Freeman said.

Goals should be realistic and tied to something tangible, such as saving for a vacation or a down payment on a home.

Once you’re ready, she suggested beginning with a clear account of how much money your family brings in and spends.

“Start with how much money you make after taxes, and then look at all of your monthly expenses, and then any other expenses you have,” Freeman said.

Include utilities, rent or mortgage and subscriptions. Check for automatic price increases and cancel “ghost charges” or subscriptions you no longer use.

“If you have any of those, you definitely want to cancel those immediately and make sure that they’re actually canceled,” Freeman said.

Go line by line and cut what you can. Reducing coffee shop visits, for example, frees up money for savings.

Don’t make your budget too confining.

“You don’t want to make it too restrictive, because you want to allow to have some fun with your money,” she said.

Always include savings. Freeman recommended automating deposits into accounts you can’t easily access.

“You want to have at least three to six months’ worth of savings in your budget. And the best way to do that is to make it automatic,” she said.

Plan for inflation by assuming expenses will rise 5% to 10% next year.

Freeman also said reviewing your budget regularly is critical.

“Review it at least every two weeks … so you can catch any areas where you need to adjust,” she said.

If you’re tackling debt, choose a method that motivates you: Pay off the smallest balances first for quick wins, or start with high-interest accounts to save money long-term.

And don’t treat credit cards as extra cash, she advised.

Freeman said budgeting can feel overwhelming but remember: Changes are temporary and mistakes happen.

“Don’t give up on yourself. Don’t beat yourself up if you make a mistake. Don’t beat yourself up if you overspend, learn from your mistakes, grow from them, and set up a plan so you don’t make those same mistakes again,” she said.

Get breaking news and daily headlines delivered to your email inbox by signing up here.

After nearly two months without new consumer price data, the Bureau of Labor Statistics released its latest report Thursday, providing a glimpse at energy costs, food prices and other everyday expenses.

According to the consumer price index, inflation slowed in November, with prices rising 0.2% over the 0.3% observed in September. (BLS could not collect October data because of the government shutdown.)

Still, inflation remains stubbornly high. Compared with a year ago, consumer costs are up about 2.7%.

Thursday’s report came just a day after President Donald Trump delivered a prime-time address from the White House in which he largely discussed affordability concerns, from housing costs to grocery prices, saying the U.S. is “poised for an economic boom.”

“The last administration and their allies in Congress looted our treasury for trillions of dollars, driving up prices and everything at levels never seen before. I am bringing those high prices down and bringing them down very fast.”

In truth, of the 11 everyday costs tracked month to month by the consumer price index, only five have decreased since January.

Here’s a closer look at the president’s claims and how prices are changing, or not, during his second term in office.

To see the average U.S. price of a specific good, click on the drop-down arrow below and select the item you wish to view.

Eggs

In the wake of all-time highs set earlier this year, egg prices have collapsed in recent months.

That downward trend continued in November, with the price dropping a whopping 63 cents from September and settling at $2.86 per dozen. It’s the first time since June 2024 that the average nationwide price for a dozen large Grade A eggs registered below the $3 mark.

This steep drop-off in prices is a result of a declining number of bird flu cases in commercial and backyard flocks. In the first two months of 2025, tens of millions of birds were affected by highly pathogenic avian influenza across 39 states, according to U.S. Department of Agriculture data. With entire flocks culled to prevent the spread of the virus, the egg supply was strained, leading to shortages in stores and record costs for consumers.

Following another spike in cases in the early fall, the number of new infections appears to be subsiding again, with less than 2 million U.S. birds affected in the past two months. More notably, zero outbreaks among egg-laying chickens have been reported in November and December.

Consequently, costs are “falling rapidly” as highlighted by Trump in his prime-time address earlier this week.

“The price of eggs is down 82% since March, and everything else is falling rapidly. And it’s not done yet, but boy are we making progress. Nobody can believe what’s going on.”

While egg prices have dropped considerably from March’s record high of $6.23 per dozen, the difference of roughly $3.37 from March to November represents a 54% decrease — not the 82% cited by the president.

In a statement given to the Tribune, a White House official clarified that he was referring to wholesale costs, not retail prices.

Milk

The cost of milk also saw a measurable decrease from the previous month, falling 13 cents.

A gallon of fresh, fortified whole milk is now priced at $4.00 — that’s 2.5% less than it was in December 2024, before Trump took office.

Bread

The average price of white bread fell in November to $1.79 per pound, marking a three-year low for the pantry staple. Time for bread pudding, anyone?

Bananas

The cost of bananas fell slightly from September’s all-time highs, dropping just a fraction of a cent to $0.66 per pound in November.

Recent price inflation is likely a byproduct of the president’s trade war, with tariffs imposed on the country’s top banana suppliers like Guatemala, Ecuador, Costa Rica, Colombia, Honduras and Mexico — all of which are currently subject to an import tax of at least 10%.

But in mid-November, Trump took action to combat rising grocery costs, announcing that some agricultural products would be exempt from tariffs due to “current domestic demand for certain products” and “current domestic capacity to produce certain products.”

Both fresh and dried bananas were among the listed exemptions, indicating that lower prices may be around the corner.

Oranges

No data on orange prices was available for November.

However, in September, the cost of navel oranges was listed at $1.80 per pound, less than a cent shy of record highs and nearly 18% more than they were at the start of the Trump administration.

Drastically low domestic orange production combined with steep tariffs on foreign growers have been helping to push costs skyward. But, as with bananas, oranges are now exempt from most reciprocal tariffs.

Tomatoes

As of November, the cost of field-grown tomatoes was $1.83 per pound. That price is 8 cents lower than the previous month of data and down roughly 12% since Trump took power.

The change is somewhat abnormal given the growing season, as prices typically rise in the fall and peak in the early winter months, and could be attributable to the Trump administration’s recent course reversal on many of its tomato tariffs.

Chicken

The cost of fresh, whole chicken fell for a fourth consecutive month, to $2.04 per pound — its lowest price in a year.

Rising feed costs and the effects of bird flu on the poultry supply chain have driven persistently higher prices, but with the number of cases dropping again, we could see lower prices in the new year.

Still, the average cost is only about 2 cents less than it was when President Joe Biden left the White House.

Ground beef

Ground beef is getting more expensive.

After shoppers saw some relief in September from climbing costs, the price of ground beef jumped another 18 cents.

Rising costs can be attributed to a confluence of factors. The U.S. cattle inventory is the lowest it’s been in almost 75 years, and severe drought in parts of the country has further reduced the feed supply, per the USDA. Additionally, steep tariff rates on top beef importers also played a part in higher prices stateside, but as of Nov. 13 high-quality cuts, processed beef and live cattle are exempt from most countries’ levies.

Still, since the change of administrations, ground beef costs have ballooned by 18% — translating to $1 per pound price increases at the grocery store.

As of November, a pound of 100% ground beef chuck would set you back about $6.50.

Electricity

Electric costs have also been steadily rising.

At approximately 19 cents per kilowatt-hour, the current price of electricity is a fraction of a cent off August’s high. According to the U.S. Energy Information Administration, the average American household uses 899 kWh every four weeks, translating to a monthly bill of about $170.

Thankfully, the White House appears to be working to mitigate mounting costs. In his presidential address, Trump claimed that within the next 12 months his administration will have opened 1,600 new electrical generating plants.

“Prices on electricity and everything else will fall dramatically,” Trump said.

For many Americans, relief is needed. Since last December, the average price of electricity per kilowatt-hour has increased more than 7%.

Gasoline

Declining gas prices were another highlight of Trump’s Wednesday night remarks.

The cost of gasoline has tumbled from the record-setting prices Americans saw three summers ago under Biden, and just last month, the price at the pump dropped more than 10 cents per gallon.

“On day one I declared a national energy emergency,” Trump said. “Gasoline is now under $2.50 a gallon in much of the country. In some states, it by the way, just hit $1.99 a gallon.”

According to the latest CPI data, the average nationwide cost for a gallon of regular unleaded gasoline is $3.23. And though prices are noticeably lower than they were two to three years ago, that average remains higher than it was just a year ago and up nearly 3% during the Trump presidency.

Prices in Chicago, meanwhile, are about the same month-over-month, costing an average of $3.29 per gallon, according to EIA data.

Natural gas

Bucking its previous downward trend, piped utility gas, or natural gas, is another expense that’s climbing. The nationwide cost jumped 3 cents in November, landing at $1.64 per therm.

On average, Americans are paying close to 8% more to heat their homes, ovens and stovetops than when Biden left office. Year-over-year, that gap is even more drastic: a roughly 10% change or difference of 15 cents per therm.

As 2025 draws to a close, it’s a great time to reflect on the year and set yourself up for success in 2026. Whether you’re building new habits or refining your financial strategy, Laurie Winters, Chase Community Manager in Atlanta, shares practical tips to strengthen your financial health journey.

Q: What’s been a key financial health learning for you in 2025? A: This year, I’ve been really inspired by the enthusiasm in Atlanta for financial education. People here aren’t afraid to dream big—buy a home, save for retirement, plan for college, or grow their business—and are really excited about the process to get there. One of the most rewarding parts of my job is helping connect them with the tools and knowledge to turn those dreams into reality.

One trend that stands out is the increasing complexity of fraud and scams. These can have a serious impact on anyone’s financial wellbeing. That’s why I’ve made it a priority to host workshops focused on fraud prevention—covering the latest scams, warning signs, and practical steps to help safeguard your personal information. Staying informed and proactive is the best way to keep yourself and your loved ones safe.

Q: As the year wraps up, what should the Atlanta community keep in mind about their finances? A: The new year is a fresh start, and it’s the great time to build habits that set you up for success. Here are a few ways to get started:

Think of your budget as your personal roadmap—it shows you exactly where your money is going and helps you steer toward your goals. Take a little time each month to track your income and expenses. When you set a budget that truly reflects your priorities, you’re not just managing money—you’re empowering yourself to make confident decisions

Saving doesn’t have to be overwhelming. Even small, consistent deposits can grow into something meaningful over time. Try automating your savings so it happens without you even thinking about it—like paying yourself first. Watching your savings grow, no matter the amount, is a powerful way to build financial security and peace of mind.

Your credit score is more than just a number—it’s a key that can unlock new opportunities, from buying a home to starting a business. Strengthen your credit by paying bills on time and keeping your balances manageable.

Q: What are some tips for your neighbors to start the new year on the right financial foot? A: No matter where you are in your financial journey, I think everyone should do a year-end financial check-up. Review your budget and savings, set realistic goals, and make a plan you can stick to in the new year. Anyone can visit their local Chase branch and ask about getting access to a financial health check-up at no cost—available to all, no matter who you bank with. Our teams live, work, and are rooted here – and we are deeply committed to uplifting the communities and serving our neighbors every day.

As Community Manager, I’m focused on financial education and community partnership to help strengthen financial health journeys. I host free workshops on essential topics like budgeting, saving, building credit, and preventing fraud and scams. These workshops are open to all, not just Chase customers, and can help you start the new year on the right foot.

Q: What financial health initiatives are you excited about in 2026? A: I’m especially excited to help demystify credit for our community. Credit can feel intimidating, but it’s actually a powerful tool that can help you unlock new opportunities—whether that’s buying a home, starting a business, or simply getting better rates on everyday purchases. In my workshops, I break down the basics: why it’s important to know your credit score, how to check it, and simple steps you can take to improve it—like paying bills on time, keeping balances low, and avoiding unnecessary debt. We also talk about how your credit score can be a stepping stone to achieving your biggest goals. My advice? Don’t shy away from learning about credit. The more you understand, the more control you have over your financial future.

Q: How can neighbors get involved and benefit from your community work? A: Getting involved is easy—and it can make a real difference in your financial journey. We have Community Managers in every state and D.C., all dedicated to supporting their local neighborhoods. Our free workshops cover essential topics like budgeting, saving, building credit, and protecting yourself from fraud and scams. These sessions are open to everyone, not just Chase customers, and are designed to be practical and welcoming. Whether you’re looking for guidance, want to ask questions, or just want to connect with others who are working toward similar goals, we’re here for you. I encourage you to join us, bring a friend, and take advantage of the resources and support available right in your community.

Q: If you could give one piece of financial advice to the community for 2026, what would it be? A: My top advice is to be proactive: take the time to review your finances, set clear and achievable goals, and create a plan to reach them. Don’t wait for a crisis or a big life event to get started—small steps today can lead to big results tomorrow. And remember, you don’t have to do it alone. Our team is here to help, whether you need a quick check-up, want to talk through your options, or need help building a plan. You don’t need to be a Chase customer to benefit from our expertise and support. We’re committed to helping our neighbors build a stronger, more resilient financial future—one step at a time.

The bottom line

The end of the year is the perfect time to reset your financial goals and take positive steps toward a stronger future. Stop by your local Chase branch for a free financial check-up, sign up for one of my free workshops, and let our team help you start 2026 with confidence.

For informational/educational purposes only: Views and strategies described on this article or provided via links may not be appropriate for everyone and are not intended as specific advice/recommendation for any business. Information has been obtained from sources believed to be reliable, but JPMorgan Chase & Co. or its affiliates and/or subsidiaries do not warrant its completeness or accuracy. The material is not intended to provide legal, tax, or financial advice or to indicate the availability or suitability of any JPMorgan Chase Bank, N.A. product or service. You should carefully consider your needs and objectives before making any decisions and consult the appropriate professional(s). Outlooks and past performance are not guarantees of future results. JPMorgan Chase & Co. and its affiliates are not responsible for, and do not provide or endorse third party products, services, or other content.

Deposit products provided JPMorgan Chase Bank, N.A. Member FDIC. Equal Opportunity Lender.

For many newcomers to Canada, personal and financial goals can feel like they are pulling in opposite directions. You want to say yes to everything—travel, dinners out, live music, social events—but you’re also thinking about building an emergency fund, saving for retirement, and staying out of debt. Add to that the cost of settling in, a limited credit history, and (in many cases) living off savings or a survival job, and it becomes clear that trying to do it all right away can be risky.

This article isn’t about me, but I will say this: my family and I chose to focus on building a strong financial foundation before chasing all the extras. At the same time, we were very aware of how easy it is to fall into the trap of grinding so hard that you lose steam. If the journey to build a better life becomes joyless, it can be hard to remember why you moved in the first place.

You can’t do everything at once—and that’s okay

The truth is that it’s hard to prioritize when you’re trying to settle in and feel like you belong. The urge to do and see everything is real. But when your early days in Canada are being funded by personal savings—or worse, high-interest credit—impulsive spending can get dangerous fast.

Without a financial plan, it’s easy to overspend—and because newcomers often have no credit history, the only credit products available may come with steep interest rates and strict limits. One misstep can quickly spiral. Instead of trying to do everything, consider what really matters most in the short term. What helps you feel grounded? What creates forward momentum? What is truly urgent, and what can wait?

Focus on the foundation

There’s a difference between building a life and decorating it. In those early months, start with the essentials—the things that give you stability, reduce your stress, and set you up for long-term success.

Earning, saving and spending in Canada: A guide for new immigrants

Here are a few financial goals that are worth tackling early.

1. Build your credit history

Get a secured credit card, if necessary, and use it for manageable expenses like phone bills or groceries. Pay it off in full every month. This helps you build a strong credit profile, which will eventually open doors to lower interest rates and better financial products.

featured

Best for guaranteed approval

Home Trust Secured Visa Card

Build your credit with guaranteed approval regardless of your credit history for no annual fee (deposit required).

GO TO SITE

Interest Rates:

19.99% purchase, 19.99% cash advance, N/A balance transfer

featured

Best for debt management

MBNA True Line Mastercard credit card

An ideal option for cardholders looking to consolidate and manage debt.

GO TO SITE

Interest Rates:

12.99% purchase, 24.99% cash advance, 17.99% balance transfer

Best for rewards

Secured Neo Mastercard

Rebuilt your credit with a secured card while earning cash back on your everyday purchases.

GO TO SITE

Interest Rates:

19.99% purchase, 22.99% cash advance, N/A balance transfer

2. Set up an emergency fund

Even if you’re starting small, building a financial cushion gives you breathing room. Try to set aside enough to cover one month of basic expenses, and grow it over time.

Article Continues Below Advertisement

3. Understand the Canadian financial system

This includes learning the difference between TFSAs, RRSPs, RESPs, and more. Many financial institutions, community organizations, and nonprofit agencies offer newcomer-specific resources. Take advantage of them.

Compare the best TFSA rates in Canada

4. Avoid high-interest debt

Unless absolutely necessary, avoid payday loans or quick-cash offers. These products often have extremely high interest rates and can lead to long-term financial stress. If you are unsure, ask questions. Get advice before you borrow.

5. Make small progress on long-term goals

Even small, regular contributions to your child’s education fund or your own retirement savings can have an outsized impact over time. The key is to get started.

But don’t put life on hold

Now here’s the important part: building a financial foundation does not mean you have to live a joyless life. You didn’t move here to just pay bills and build spreadsheets; you moved here for something more. And if you strip away everything fun or fulfilling in the name of discipline, you may find yourself questioning whether the move was worth it.

What helped me was learning to make room for both—a night out every now and then, a concert ticket, a staycation with my family. Nothing extravagant, just moments that reminded us that we were here to live, not just survive.

If you plan for it, joy doesn’t have to be expensive, it just needs to be intentional.

A quote that changed my perspective

I recently saw a quote on Instagram that stayed with me:

“Your life will change when you realize you are not building wealth for the things you can buy. You are building wealth for the problems you won’t have. The emergency that doesn’t devastate you. The opportunity you can take. The pressure you don’t feel. Wealth is peace, not possessions.”

An emotional, fear-based response, a financial scarcity mindset often sends people down a rabbit hole of overthinking, instilling beliefs that they will never have enough money to live comfortably and that they will always be stuck in some form of financial turmoil. This mindset can harm one’s long-term financial wellbeing and quality of life, experts say.

Why your money mindset might be holding you back

“The mindset plays a very big role in keeping people stuck in the financial situation they’re in,” said Jeri Bittorf, a financial wellness co-ordinator with Resolve Counselling Services Canada. Bittorf said she frequently encounters clients who have a scarcity mindset in her line of work. Sometimes, people hold onto fears that they will never be able to earn more or reduce their expenses, and their situation will never get better.

That emotional response usually comes from some sort of trauma around money, said Kalee Boisvert, a financial adviser at Raymond James Ltd. It could stem from childhood experiences, such as growing up poor, but it can also be established later in life from a perceived lack of resources, or by hearing stories of people around you unable to pay their rent or afford groceries, Boisvert said.

“Sometimes, this money scarcity has come from stories that people have heard and almost taken on as their own or the fear of that,” she said.

Best savings accounts in Canada

Find the best and most up-to-date savings rates in Canada using our comparison tool

Boisvert picks up on red flags of a scarcity mindset among her clients when she hears comments such as: “I’m terrible with money; I’m scared that I’ll never be able to retire; I should be doing a better job or should be doing more.” That’s “money scarcity mindset working in the background,” she said.

Boisvert said the mindset can lead to confidence and self-worth issues, which eventually spill into everyday life decisions about jobs, partners you choose or the residence you choose to live in.

Understanding your money past is key to changing your financial future

Bittorf said it’s important to get to the root cause of this mindset, and that journaling plays an important role in unpacking patterns and beliefs around money. “I have them start at, like, the earliest ages of memory, around five years old,” she said.

Bittorf uses prompt questions about financial security growing up such as if their parents talked about money, whether they experienced financial arguments at home and if they fit in financially at school. “I want them to be thinking about all of those things because those are going to influence the decisions you make now, even if you don’t realize it,” she said.

Article Continues Below Advertisement

Sometimes, Bittorf encourages her clients to create vision boards about what they’re passionate about and what their future selves look like with an abundance mindset. That creates an excitement to pursue those plans. “If they were to get out of this life situation, what are the goals?” she would ask clients.

Building abundance through mindful money habits

While unpacking financial patterns is foundational, Bittorf said it comes down to real steps, such as setting up a budget, tracking money and breaking up broader financial goals into smaller, actionable steps. That also means making some tough decisions, such as cutting out expenses where needed or changing jobs. “You know you’re strong enough to do that. And there’s a lot of support out there,” Bittorf said.

For Boisvert, breaking out of the scarcity mindset has been a conscious effort in her own personal journey. If she had not broken free from this mindset growing up, she thinks her response to money would’ve been to save and put everything away instead of aligning her spending to what she really cares about.

“Knowing that I grew up with the scarcity mindset that I had to really work hard to overcome, when I talk to (my daughter) about money, I just say money is a tool and it’s a tool that helps us achieve things,” Boisvert said.

For those stuck in the cycle, she suggested separating facts from fiction and practising gratitude. “If you’re feeling this fear and dread, and you’re looking at the numbers and you have the money to pay the bills and the rent, then it’s just about giving yourself a reminder, ‘Well, right now I am safe. Is this an old story coming up for me?’” Boisvert said.

Get free MoneySense financial tips, news & advice in your inbox.

The Canadian Press is Canada’s trusted news source and leader in providing real-time stories. We give Canadians an authentic, unbiased source, driven by truth, accuracy and timeliness.

Most companies treat budgeting like a year-end checkbox. They wait until November or December, then rush to fill in numbers. By the time the budget is complete, it already reflects a past that no longer exists and leaves leadership reactive rather than proactive.

Rushing the budget process creates risk. Instead of providing clarity, hurried budgets deliver constraints. They lock teams into flawed assumptions, stifle strategic conversations, and handicap leadership in the face of change.

Psychology helps explain why. Daniel Kahneman and Amos Tversky first described the planning fallacy in “Judgment under Uncertainty.” Later empirical work by Roger Buehler, Dale Griffin, and Michael Ross found that even when people recall past delays, they still predict that future tasks will proceed smoothly. Daniel Kahneman expanded these insights for executives in Thinking, Fast and Slow. Compressing budgeting into a few frantic weeks magnifies these biases and undermines accuracy and foresight.

What the research says about timing

An Inc.com Featured Presentation

Timing and structure both matter. A 2021 Journal of Consumer Research study documents “budget depreciation,” showing that budgets set too far in advance lose their constraining power as the pain of payment fades, which can increase overspending unless the budget is refreshed.

For businesses, the takeaway is clear. Start budgeting early enough to allow strategic alignment, and build in regular refresh cycles so the budget remains relevant and motivating throughout the year. Harvard Business Review outlines agile budgeting disciplines that preserve flexibility while maintaining financial rigor. Boston Consulting Group similarly recommends shorter cycles, relative targets, and scenario-based planning in uncertain environments.

Stories from the field

A mid-sized SaaS company we worked with began its budget planning in September. Leadership aligned around strategy first, then built base-case and upside scenarios. By January, they were adjusting resources in real time, shifting capital where opportunities emerged and tightening controls where inefficiencies surfaced. The result was a year defined by agility rather than retrenchment.

Contrast this with a manufacturing client that delayed until December. Their budget locked in faulty assumptions. By the first quarter they were over budget, underinvesting, and scrambling to recalibrate. Instead of using the budget as a guide, leadership was fighting fires.

Another example comes from a professional services firm. They historically waited until November to create their budget, often defaulting to last year’s numbers plus a modest increase. When encouraged to begin the process in September, they instead identified growth opportunities in new markets, reallocated resources toward high-margin services, and trimmed underperforming lines of business. By the time the new year began, the leadership team had both clarity and conviction about where to invest. The earlier start transformed their budget from a backward-looking ledger into a forward-looking playbook.

September as the starting line

Beginning in September transforms budgeting from an accounting exercise into a leadership discipline. It creates the time and structure to align ambition with strategy, test assumptions before they calcify, and prepare for multiple futures.

The most effective budgeting processes include:

Strategic anchoring. Start with ambition, not arithmetic. Define what the business needs to achieve before assigning numbers.

Scenario modeling. Build multiple versions of the future, including best case, base case, and downside, while assumptions are still flexible.

Accountability rhythms. Establish checkpoints throughout the year so the budget drives alignment and action.

Budgets as living frameworks. Treat the budget as dynamic. Revisit and refine it regularly as conditions shift.

Even advanced methods like zero-based budgeting (ZBB) work best when launched early and refreshed consistently. McKinsey shows how ZBB can help organizations reallocate resources toward growth.

Practical takeaways for leaders

If you want your budget to drive results rather than simply record them, consider these practices:

Begin budgeting in September. Give yourself the gift of time for alignment, discussion, and iteration rather than compression and compromise.

Lead with strategy before spreadsheets. Start with vision, goals, and desired outcomes. Then let the numbers follow, rather than letting the numbers dictate.

Model multiple scenarios. Resist the temptation to assume one future. By preparing for upside, base, and downside cases, you give yourself agility when reality deviates from the plan.

Establish quarterly reviews. A budget is not a document to be filed away. Use it as a framework for continuous review, refreshing assumptions every few months to keep it relevant and motivating.

Embed accountability. Assign clear ownership for budget drivers, and create rhythms of accountability so financial leadership is shared across the organization.

Waiting until late fall to budget means you begin the year already behind. The best leaders do not wait. They start early, using September to turn budgeting into a blueprint for clarity, agility, and growth.

Federal workers checking their finances to see how they’ll fare if the government shutdown drags on may find themselves fighting gut-wrenching anxiety.

Federal workers checking their finances to see how they’ll fare if the government shutdown drags on may find themselves fighting gut-wrenching anxiety.

And Kathleen Borgueta, a former federal employee, knows exactly how that feels.

She lost her job at the U.S. Agency for International Development in January, and had to scramble to deal with a host of new expenses as the mother of a newborn son.

“I would make sure you have all of your HR forms saved,” Borgueta said, adding that federal workers that are currently being furloughed should make sure the documents are easily accessible.

Borgueta founded Pivoting Parents, which works to help former federal workers make the transition to new careers.

She also said federal workers should be familiar with their own benefits, especially if they find themselves out of a job.

“I know countless people who didn’t get the amounts they thought they were going to get for vacation payouts and things like that,” Borgueta said.

Don’t hesitate to contact your landlord or mortgage company to let them know you are experiencing interruption in pay, she said.

Reach out to utility companies — many in the D.C. area have posted notifications that indicate customers impacted by the shutdown can get help with payment options.

“Verizon, my internet, was willing to work with me when I told them that I was a displaced worker,” Borgueta said.

As a new mom, Borgueta was facing medical bills, and advised those in a similar situation to inquire about payment options and whether you can get those bills reduced.

“It is well worth negotiating — talking to a real person and asking about payment plans,” she said.

Aside from fiscal fitness, Borgueta advised furloughed federal workers to tend to their mental health.

“I’ve been through government shutdowns. Sometimes they’re short, sometimes they’re long,” she said. “Make sure that you have the supports that you need to take care of yourself and to take care of your family.”

Resist the urge to withdraw and shoulder your burdens on your own, she said.

“I would really recommend leaning on in-person networks — people you do know who are also going through these experiences — and not just doomscrolling,” she said. “Ask for help.”

Borgueta said she leaned heavily on in-person communities, and said the D.C. region has a wide range of resources, from career coaching to accessing certification for in-demand skills.

Filing for unemployment benefits: Nuts and bolts

Michele Evermore, senior fellow at the National Academy of Social Insurance, a nonpartisan, nonprofit organization, told WTOP her advice for former federal workers when applying for unemployment insurance.

“Be prepared to provide the last 18 months in pay stubs plus your SF8 form and your SF50 form,” she said.

But she said furloughed workers shouldn’t panic if they can’t access those forms.

“You can file an affidavit confirming what your wages were, but it’s just a little more time consuming than a regular unemployment insurance claim,” Evermore said.

Evermore said unemployment benefits will not cover a furloughed workers’ living expenses. Weekly benefits range from $440 a week in D.C. to $378 a week in Virginia. In Maryland, weekly payments are as high as $430.

“That’s not a lot of income, but it’s better than zero,” Evermore said.

After filing for unemployment, Evermore said, expect to wait.

“It will take a while because, in general, timeliness means you get paid within two to three weeks,” she said.

One thing that anyone receiving unemployment benefits should realize is that those benefits will be taxed.

“States will give you the option of withholding now or paying later. I would really encourage people to just withhold now and make sure you’re not stuck with an unexpected tax bill next year,” she said.

One last bit of advice, said Evermore: keep your unemployment benefits password.

“In some states, if you don’t keep your password for the unemployment insurance system and you get logged out, you’ll have to actually call and get mailed a password. So make sure you keep that someplace safe,” she said.

Get breaking news and daily headlines delivered to your email inbox by signing up here.

Since 2002, Sue has provided content creation, editing, and consulting services to corporate clients through her business CodeWord Communications. Here, she talks about her formative experiences along the road to becoming a self-employment expert—and the right way to use debt.

Who are your money/finance/investing heroes?

As a freelance writer, I had an early gig reviewing business books, several of which were financial. That gave me insight into the fact that people actually wrote books about money that helped demystify elements like the stock market and other terms. I wish money management had been taught in high school; I would have preferred that class over other math that I never use as an adult. Suze Orman was one of my favourites from those early reads for her practical advice and encouragement that anyone could understand and manage their finances.

How do you like to spend your free time?

I like walking—both in nature and cities—travelling, and seeing new places. I like reading and listening to podcasts and audio books. I also like writing fiction and poetry, although it’s sometimes exhausting to make time for creative writing after a full day as a professional writer.

If money were no object, what would you be doing right now?

I’ve always wanted to be a writer, but when I became an adult, I realized that I also needed to make a living. So I started working as a journalist and content writer. While I enjoy any kind of writing, I still like writing fiction, so I’d probably flip the time so that I’m writing my creative work during the day instead of after hours.

What was your earliest memory about money?

My earliest money memory was being given a dollar allowance from my parents for chores. (I was dusting and cleaning bathrooms; my younger brother was vacuuming. To this day these are our favourite chores. I love the quick fix of a good bathroom polish.) We would walk to our local depanneur in the Montreal suburbs and my brother would buy a big item, like a can of Coke or a chocolate bar, and I would stuff as much penny candy as I could into a little brown bag to last the week.

I think math became important for that transaction as I made the money stretch as far as possible (was it better to buy five gummy bears at two cents each or a 10-cent lollipop?). I also learned that different people want and value different things, as I never brought my brother over to my way of thinking nor converted to his.

What’s the first thing you remember buying with your own money?

Besides penny candy, I think a cassette tape of the soundtrack to the movie Cocktail. Also books from Scholastic.

What was your first job?

After babysitting, my first real job was as a cashier at K-mart, where I also worked in the garden centre when I was 15. I still remember the stress when your cash register tape jammed, and I can still tell the difference between impatiens and petunias.

Article Continues Below Advertisement

I’m not sure what I did with my first paycheque, although probably saved some for a band camp later that summer, which is when I had to quit because my manager wouldn’t give me the week off.

What was the biggest money lesson you learned as an adult? What would you do differently today?

Probably saving earlier. I recall a bank having an ad in the subway about the difference in results between the person who started saving at 23 years old and the person who started saving at 30. The problem is that I think I saw that ad at 28 so I felt already behind. Also, I hated that nerd who had the wherewithal to start saving at 23.

A related lesson as a freelancer was to save my money for income taxes and HST in a separate place so you have it when it comes to tax time. It’s very easy to spend if it isn’t in a separate account.

What’s the best money advice you’ve ever received?

Paying off debt with the highest interest rates first (i.e. credit cards). But also, I learned myself the advantage of having credit available (and saying yes to a lower-interest line of credit) as a way to balance out my freelance business since mostly I’m paid 30 days after I submit an invoice. I’ve also learned to proactively ask for a percentage up front if I’m working on a larger project—say 30% to 50%.

What’s the worst money advice you’ve ever received?

I haven’t received this advice directly, but I find all-or-nothing money advice annoying. Especially the one about how much you can save by avoiding fancy coffees. I’m not a fancy coffee regular but if that’s the spend that earns you an hour of work at a table in a coffee shop or picks up your day, then it’s fine. Treats are okay in moderation and money is also for buying a nice life today, not just saving for the future.

Would you rather receive a large sum of money all at once or a smaller amount of money everyweek/month for life?

As a freelancer, I regularly receive large sums of money at the middle and end of projects and then nothing for a few weeks, so I am curious what it would be like to have regular deposit every week.

What do you think is the most underrated financial advice, tip, or strategy?

Focusing individually on whether each purchase is a good idea. Just because something fits in your budget doesn’t mean it’s a reasonable splurge. I don’t think I’ve ever paid over $100 for a handbag, so if I see one priced at $500, that’s just not for me. Also knowing the current cost of items that you buy regularly so you’re not tricked by marketing or “sales” to think you’re getting a great deal. I know when the toilet paper really is a good sale.

What is the biggest misconception people have about growing money?

That there’s a magic age past which it’s too late. I started saving more in my 30s and I think it’s never too late. It just means I have a lot more room in my RRSP to continue filling up.

The agency said Tuesday its consumer price index for September was up 1.6% from a year ago compared with a year-over-year increase of 2% in August.

It was the slowest annual pace for inflation since February 2021 when it was 1.1%.

Gasoline prices in September fell 10.7% compared with a year earlier. Excluding gasoline, the annual pace of inflation was 2.2% in September.

Meanwhile, rent prices increased at a slower pace in the month but remained elevated as they rose 8.2% compared with a year ago following a year-over-year gain of 8.9% in August.

Grocery prices increased 2.4%, rising faster than overall inflation

Statistics Canada said prices for food purchased from stores rose faster than overall inflation as they increased 2.4% in September, the same rate as in August. Prices for fresh or frozen beef gained 9.2%, while edible fats and oils rose 7.8% and eggs increased 5%.

Prices for food purchased from restaurants rose 3.5% compared with 3.4% in August.

The inflation report is the last major piece of economic data before the Bank of Canada’s interest rate decision on Oct. 23.

The central bank, which has a target of 2% for inflation, has cut its key interest rate three times so far this year to bring it to 4.25%.

If you’re like the 50% of Americans in this 2017 report, then you might be living paycheck to paycheck.

Even though the economy has seen significant improvement and people are earning more, there are still those who can barely make ends meet every month. This is something that makes you stop and think.

The biggest cause of this disparity is the fact that most people are neck-deep in debt.

Whether it’s because they want their lifestyle to reflect their earnings or they are afraid of missing the latest trends in fashion and technology, many Americans spend more than they can afford.

Having financial problems can take a toll on a person’s health and damage relationships.

But there are ways to correct the issue. In this article, we’ll talk about how to stop spending money on unnecessary things in order to achieve true happiness and freedom.

First, let’s discuss the reasons for our overspending.

7 Reasons Why We Overspend

1. We overspend because it is now too easy to swipe a card or click the “buy” button.

To be honest, plastic just doesn’t feel the same as holding onto paper cash.

It is easy to use credit and overspend more than you would if you had cash because you may not even look to see how high your credit card balance is, or how small your checking account balance is.

When you count out your dollar bills when you’re buying something, you’re aware of the amount of money that you are giving up. Researchers have even named this behavior “the pain of payment.”

But this doesn’t happen when you pay with a card or buy something online. You don’t have to look at the total before signing for the purchase, which is why this can easily lead to overspending.

2. We believe that it’s socially acceptable to incur debts.

If you have a balance on your credit card every month, or are swimming in endless student loan debt, adding some more debt may not feel like a big deal.

It may even seem to be the “norm” among the people you know. Incurring debt may even feel like a valuable investment.

In fact, one study found that among people between the ages of 18 and 27, credit card and other loan debt was directly correlated with a higher level of self-esteem and a feeling of more control over one’s life.

However, this feeling fades with age, likely as people start realizing how long it will take to pay off the debt that they have incurred.

3. We do not track our expenses, nor have a budget.

A recent survey found that only 41% of Americans use a budget and actually track their expenses against that budget each month.

This suggests that most people have no idea how much money they should be spending every month in different areas of their lives, such as food, living expenses, car payments, entertainment, and clothing.

Without having a budget for these expenses, it is easy to go overboard without realizing it.

4. We use retail therapy as a way to numb or momentarily escape pain.

A recent study found that over half of Americans admit to turning to “retail therapy” during times of stress. Additionally, 62% of shoppers have made purchases to cheer themselves up, and 28% have made purchases to celebrate something.

When people think of retail therapy, escape, entertainment, and excitement usually come to mind. Online shopping is increasingly noted as being a type of “mini mental vacation.”

Shopping is a pretty mindless, relaxing activity—especially if you’re not buying anything. However, sometimes, when you come across just the right thing, you feel like you have to buy it.

5. We have no clear idea how much our net income is (after paying our bills, taxes, and other deductibles every month).

Sure, you know what your salary is, but have you ever broken that down into your expenses? Even if you believe your salary is relatively high, bills and expenses add up quickly, and the numbers may be shocking once you add them up.

Don’t just think about your mortgage and cell phone bill—take into account your car insurance, personal property taxes, and the money you spend on the weekends for entertainment.

Create a spreadsheet that has your income and expenses on it to see how much money you have left at the end of the month. Chances are, it isn’t quite as high as you may think.

6. We are in denial about our own spending habits.

If you refuse to track your spending or create a budget, or you convince yourself that you can’t afford to save money, you’re probably in denial about your overspending.

Overspending doesn’t just mean that you are spending too much money on things that you don’t need, it also means that you could be spending too much money on things that you try to convince yourself that you need.

Most people are neck-deep in debt, spending more than they can afford because they are afraid of missing the latest trends in fashion and technology.

When you’re not in denial, you are able to limit your purchases to just the things that you need, not the things that you want in the moment—which is a good sign that you have control over your finances.

7. Ads compel us to buy stuff we don’t need. We have a fear of missing out, and overspend to keep up with the rest of society.

Everyone wants to keep up with the people around them, and acquire all of the new material items that are popping up. Social media has added to this problem for two reasons.

First, you see people that you know in pictures wearing the coolest new clothes or having the hottest new bags.

Second, companies are able to advertise on social media—especially the more expensive items that are probably outside of your budget. In fact, your browsing activity can help companies send you very targeted adds to try to pique your interest.

But research shows that 39% of people have spent money they didn’t have in order to keep up with their friends, and 36% of people don’t think that they can keep up with their friends for one more year without going into debt.

So while there are a lot of reasons that people overspend, there are also several reasons why you should focus on saving money.

Hopefully, you will find these reasons to be compelling, and realize that the things that cause people to overspend are not worth it in the long run.

Why You Should Focus on Saving Money

It makes you feel more in control of your life.

When you are secure in the knowledge that you have some money saved, you can feel that you have a better grip on things.

You don’t have to feel like you always have to depend on other people to help you get out of a bind because you have the money put aside for emergencies when you need it.

You also know your spending limits. If you stick to them, you will be able to control exactly where your money goes, and live in line with your priorities and values by spending more money in certain areas and less money in others.

It improves your health.

Knowing that you have some funds set aside helps you feel less stressed about making ends meet. And the truth is, a lot of people cite finances as being their biggest source of stress. This peace of mind helps reduce your risk of hypertension and other diseases.

As a result of financial stress, people often lose sleep, have anxiety, obsess over past financial decisions, and even fight with their spouses.

What’s more, money stress can feel like it will last forever when you’re in the thick of it, which may make it feel even worse.

It helps your weight loss goals.

There is a positive correlation between saving money and losing weight. Most people spend their income by eating out, and eating fast-food fare is the main reason for the rise of obesity in the United States.

Eliminating this unhealthy eating habit not only helps you save money, but also allows you to have healthier meal options and the opportunity to slim down.

In fact, some of the healthiest foods in the world are actually the least expensive. Buying produce that is in season, along with whole grains and beans, will provide your body with all of the nutrition that it needs to stay healthy.

If you stop spending money on restaurant food, you will save more money than you could imagine, and you will start to drop weight quickly.

When you are secure in the knowledge that you have some money saved, you can feel that you have a better grip on things.

It is good for the environment.

If you are conscious about your use of electricity and water, then you reduce the amount on your monthly utility bills. By deciding to live more thriftily, you can maximize the 3 R’s: reducing, reusing, and recycling.

Even if you are spending a little bit more money up front for an eco-friendly car, you will be saving money in the long run on gas, while also helping to save the environment. The same goes with upgrades to your home, such as insulated windows or efficient appliances.

While these things cost a bit more in the beginning, they will greatly reduce your monthly bills and therefore pay for themselves in no time. Also, they help save electricity and keep the environment clean.

It helps you become more independent financially.

Being financially independent means having the freedom to make choices that are not dependent on your monthly paycheck. Everyone defines “wealth” differently, but one thing that most people agree on is that wealth equates to financial independence and a savings account to depend on.

This means that you have the freedom to make decisions in your life independently from earning your paycheck.

This may mean that you can help out family members financially, take vacations every year, or choose personal satisfaction over salary when considering what type of job you want.

Financial independence doesn’t necessarily mean that you’re rich—it simply means that you don’t have to depend on your paycheck or other people if something comes up.

You have something to use in case of emergencies.

Unforeseen circumstances could include being injured and unable to work, needing a major auto or home repair, losing a job, or having to fly out to another state for a close relative’s funeral.

These examples all require you to spend money, and having set aside some in savings can help prevent you from going into debt.

When these unexpected things occur, you will be relieved to be able to turn to your savings account rather than having to take out a loan or incur debt. It is best to have about six months’ worth of savings set aside to pay all of your living expenses in case you lose your job.

In this eight-minute video, Matt D’Avella talks about money and the overspending issues we face, gives reasons why we might not manage money properly, and provides tips on how to manage personal finance through a minimalist approach.

11 Tips on How to Stop Spending Money

1. Understand what psychological triggers compel you to spend.

In many cases, figuring out how to stop spending money relates to identifying the emotional and psychological triggers that lead to your spending.

By removing your habit triggers, you will no longer have the opportunity or the temptation to spend money that you don’t have.

It could be that you’re unhappy (emotional), with shopaholics (peer pressure), in a Christmas crafts fair or your favorite dollar store (environment), or trying to keep up with a luxurious way of life (lifestyle).

When you know these triggers are going to be present, make sure to just carry a little bit of cash with you instead of hanging on to your credit card. This will help limit your spending.

The important thing is that you surround yourself with people and environments that will not tempt you to go overboard with your spending.

When you pay for things with cash, you see how much money you have and how much you’re giving away. Paying in cash forces you to only spend what you have.

Cut up any credit cards that are specific to one store, and try to only keep one main credit card open, if any. Make sure you pay off the entire balance each month so you don’t incur interest.

3. Spend only the money actually available to you.

The cash envelope system is a good way to stick to your budget and use only the money that is actually available to you.

Based on your budget, put the amount of cash that you can spend in every category (such as food, clothing, and entertainment) into an envelope every month. Once the cash is gone, it’s gone for the month. This will force you to budget properly and not overspend.

By paying with cash, you will not rely on credit, and you won’t spend money that you don’t have. The cash envelope trick will encourage you to get creative and resourceful with your spending.

If you overspend one month and don’t have any money left to go to the movies with your friends, you will have to come up with new ways to save money, or think of less expensive ways to hang out with your friends.

4. If you think you need to buy an item, ask yourself a couple of questions:

a. What value will it add to my life? If the item brings happiness or serves a purpose, then the purchase is worth it. But look at your motives.

Do you want to buy the item because it will truly add to your life, or are you trying to impress someone else? Before you purchase something, give it some serious consideration.

b. Do I need this item to get through the day? If you answered no, then the purchase can wait, and perhaps you’ll realize that you don’t need the item at all.

c. How often will I use this item? If this is something that you will probably use once and then leave in a closet to gather dust, pass on it. Also, is this item something that you could borrow from a friend if you only intend to use it a few times?

The infographic below shows examples of items you should not be spending your money on if you want to live a happier life.

5. “Shop” in your closet for clothes.

The average American throws away about 80 pounds of clothes every year. If you feel the urge to buy new clothes, try looking into your closet first for something that you may have only worn once.

You might be able to put together an outfit that you had never thought of, or put together some of your existing clothes to meet a current trend that you hadn’t thought of before.

First, you need to get your closet organized and fix any clothes that have holes or are missing buttons. Then take out some jewelry cleaner and get all of the tarnish off of your old jewelry to make it look new again.

If you can get your basics looking great, you will have enough clothes to last you through the whole season.

6. Develop good money habits.

Becoming financially savvy is a way of increasing your savings and adding value to your life. Good money habits are all about small changes and critical adjustments in your mindset.

For example, you can create rules for yourself, such as waiting one month before buying something that you see to give yourself time to really consider it (or forget about it). Or, you can tell yourself that you have to get rid of two items that you own for every one item that you purchase.

It is also important to examine your frugal habits to make sure that they are indeed worth it. For example, if you are driving 10 minutes out of your way to save a few dollars on gas, it probably isn’t worth your time or the extra mileage on your car.

The best thing you can do is to keep things simple and create a budget that you can stick to. Don’t let your finances get too complicated by using multiple apps and creating several spreadsheets. This will increase your chances of giving up your good spending habits. Just keep it simple.

For more on these habits, take a few minutes to check out the video below:

7. Avoid eating out.

In addition to spending less money by cooking your own meals, not eating out also means you’re in control of how healthy your meals are. Yes, eating out is easy and it saves time. But if you’re spending $8 on a fast-food lunch every day, that’s $240 per month.

The key is to create a plan to avoid eating out. Start by meal planning and prepping food on Sundays to last you through the week.

A lot of people don’t feel like cooking when they get home from work, so avoid that by doing it all ahead of time. And you don’t even have to make everything from scratch. Using frozen vegetables is both cheap and healthy.

8. Embrace minimalism.

Minimalism is intentionally living with just the things you really need. It allows you to see and appreciate the value of what you have in life. It also discourages you from buying more stuff.

Minimalism is becoming increasingly popular for several reasons. Not only does it save money because it forces you to differentiate between essential items and non-essential items, but it also is environmentally friendly because it reduces waste.

Minimalism also offers a life with a reduced amount of stress, fewer distractions, and an increased amount of freedom

Finally, while consumerism is alive and well, there is a growing number of people who are starting to see through the fiction of the claim that every new product will actually make your life more fulfilling. While people often try to find happiness in new possessions, they are typically left unfulfilled.

In this 15-minute TEDx video, Ryan Nicodemus and Joshua Fields Millburn, known to their readers as The Minimalists, share their thoughts on what makes people truly rich, the definition of minimalism, and finding happiness and value in their lives.

9. Be aware of financial pitfalls as you become successful.

When you begin to earn a significant amount of money, it is tempting to buy stuff that reflects your current lifestyle. Learn to avoid lifestyle creep to keep your spending at bay.

If you start making more money or your bills decrease, boost your savings rather than making your lifestyle more lavish.

Don’t make former luxuries into your new everyday rituals—those things will no longer be special, and you will be back in the financial situation that you were in before your net income increased.

10. Get stuff for free.

If you need some items, why not try getting them secondhand through an online community whose members give stuff away for free in their areas, such as Freecycle?

You can also ask around to friends and family if you need something specific. Whether you want to borrow it or keep it, most people are holding onto all kinds of things that they have no use for anymore.

11. Use your free time for hobbies.

When you are busy doing things you love, not only will you keep life interesting, but you’ll also have less time for shopping.

Spending your time doing hobbies is fulfilling and can be as inexpensive as you want it to be. Find your passion and put your time and energy into cultivating your talents or knowledge in that area.

Find a friend who shares your hobby and team up to do it together. Adding the element of a human connection to any activity you are doing makes it all the more fulfilling.

Final Thoughts on How to Stop Spending Money

Today we’ve learned that most Americans have difficulty managing their finances, despite the fact that they’re earning more in recent years.

We’ve also discussed the solutions to financial issues, with the primary action being making a change in your spending habits.

We hope that the suggestions listed here on how to stop spending money on unnecessary stuff will lead you to a life full of true and lasting happiness and financial freedom.

If you are interested to learn more about positive financial habits, head over the following posts for helpful tips on how to achieve financial stability and success.

Well, you apply. But make sure you’re applying for the right card and that you have a high chance of being approved. You see, the credit card company will check your credit history, and that can affect your current credit score. So, don’t apply for a bunch and hope for the best, as that could make it look like you are at risk for having access to too much credit. The good news: There are many types of credit cards in Canada, including those for newcomers to Canada, students and even those with bad or no credit. Check out our rankings for the best credit cards in Canada for your situation.

Once you have a credit card you will want to maintain good credit habits, like paying it off on time and paying more than the required minimum payment. Here are some other articles that will help you navigating your first credit card in Canada.

Read:

Why is credit history important?

Say you want to rent an apartment. Your credit history is vital because most landlords will want to see your credit score and credit report to judge whether you’ll pay your rent on time. If you get the apartment, you’ll want an internet connection—and for this, too, the large providers will query your credit score.

If you need to buy or lease a car, your credit history will not only determine whether you’re approved for a loan, but also what interest rate you’re offered: the higher your credit score, the lower the interest rate. Insurance companies may check your credit history before providing coverage. And finally, if you want to buy a home, your credit history is key to qualifying for a mortgage, as well as what mortgage interest rates lenders will offer. A lower rate could save you tens of thousands of dollars over the life of your mortgage.

Read:

How to build a good credit history when you have no credit history

Credit history is usually built organically as people start using credit. In Canada, young people who have reached the age of majority (18 or 19, depending on where they live) can apply for a credit card and start building a history of borrowing and repayment.

If you’re a newcomer to Canada, or if you’re a student, recent grad or young adult who doesn’t have much of a credit history, your credit score may be low—which is a hurdle in getting approved for credit. It’s a frustrating cycle—you need credit history to access credit, and you need credit to build that history. So, what’s the solution? Here are a few steps anybody can take to build their credit history:

There might be affiliate links on this page, which means we get a small commission of anything you buy. As an Amazon Associate we earn from qualifying purchases. Please do your own research before making any online purchase.

If you’re looking to achieve financial security, increase your family’s wealth, and experience peace of mind, then you might want to commit to a budgeting habit.

There are different budgeting plans out there designed for families, many of which have been developed to ensure that households have enough funds available for their everyday needs.

When families commit to the budgeting habit, they reap the following benefits:

Freedom from debt

Comfortable way of life, with more funds available for things that the family considers important

Keeps unnecessary spending (and the waste that accompanies it) to a minimum

Teaches family members to use money wisely and encourages mindful decision-making

Ideally, a budget should be written down. This can be done on actual paper, a spreadsheet, or a budgeting app.

In this article, you’ll find a collection of free budget printables that you can use to track your family’s expenses.

Read on and check out the awesome designs we’ve rounded up for this collection.

Reach your financial goals with this Budget Planner bundle.

Featuring templates for tracking your credit score health, income and expenses, debt repayment, and budget, each fillable and printable planner is designed to help you monitor everything that has to do with your hard-earned money.

Achieve financial freedom in no time with this planner bundle.

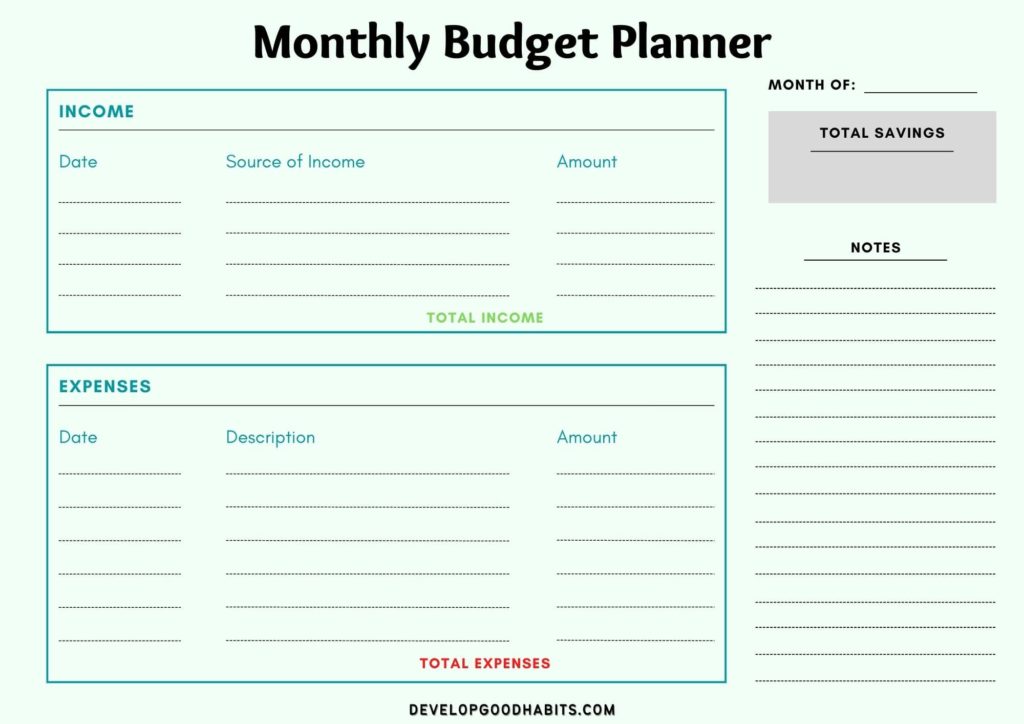

If you’re new to budget tracking, you might want to use this fairly straightforward tracker we’ve created. All the information you need about your monthly expenditures is available at a glance.

This tracker has spaces allocated for recording expenses as they occur throughout the month, with a description of each expense, the amount, and the date.

You can indicate the type of expense in the “category” column. At the bottom of the page is a section for writing down the total expenses incurred for the month.

Do you often wonder why you’re overshooting your monthly budget? Our budget planner is designed to help track your total monthly income and your total monthly expenses.

Another section of this planner is allocated for writing notes and your total savings for the month.

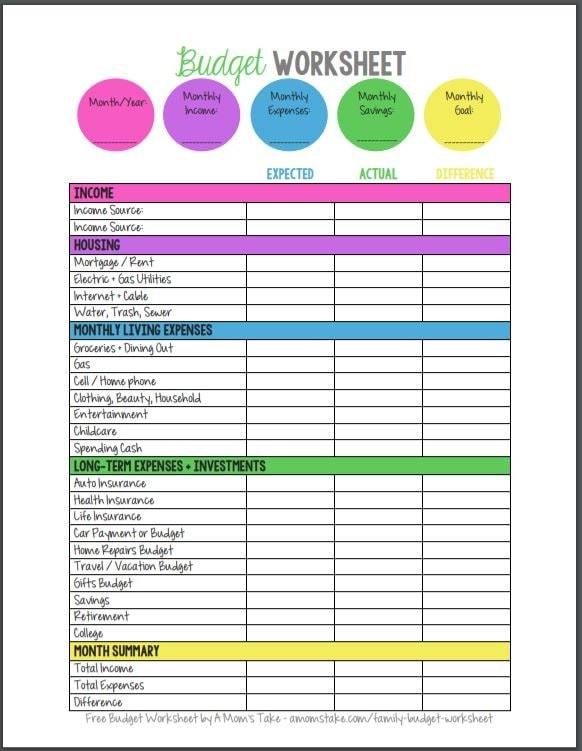

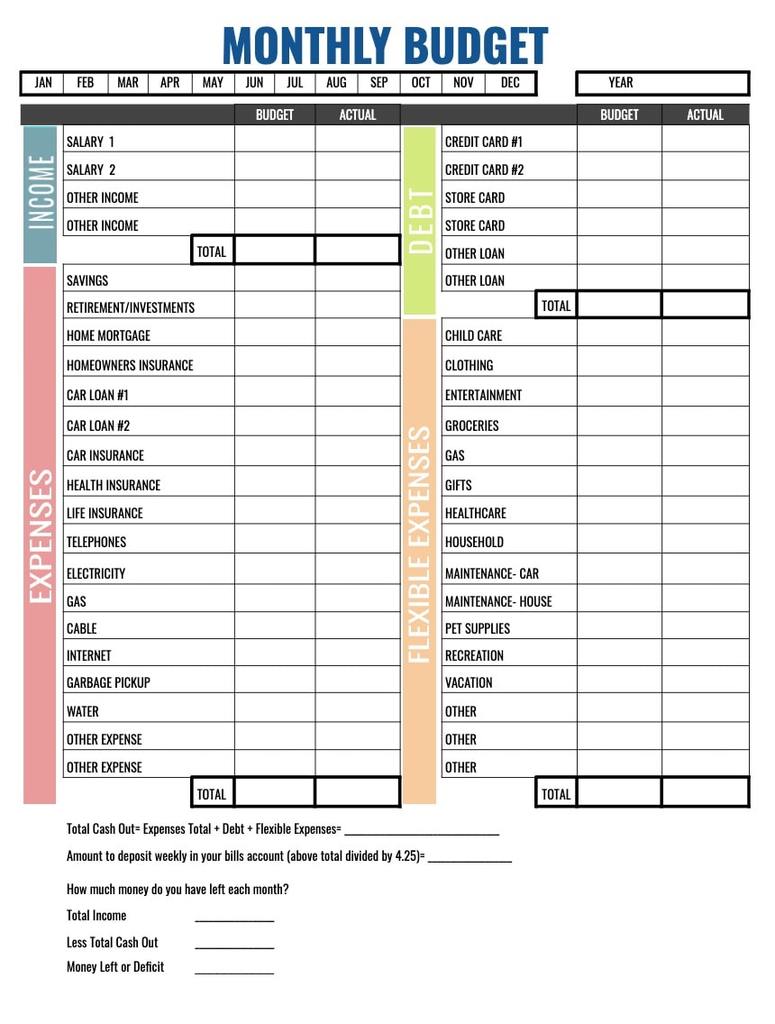

This budget worksheet includes a list of typical items that need budgeting in a household. These are grouped into main categories, such as

Housing

Monthly living expenses

Long-term expenses + investments

There is also a column to allow for checking of the actual amount of deficit or savings that a family has at the end of the month. This feature is quite helpful for preventing uncontrolled spending.

In this budget template example, each item on the household’s monthly expense list is categorized according to whether it’s a regular expense, flexible expense, or debt.

Households that utilize a budget system to manage their finances report positive results.

For example, budgeting has helped families understand what things they are able and unable to afford every month. This paves the way for many families to save up and buy things that they truly want.

9. Monthly Budget Sheet

This well-designed budget sheet will keep your budgeting on track. It provides ready access to information, whether you’re within budget or already in a deficit for the month.

If you’d like, you can use the pre-filled sheet, which features a categorized list of expenses that most families have.

Some of the categories include:

Housing

Food

Debts

Medical

Charity

There are also areas for creating a savings plan, specifying your family’s monthly income, and indicating a starting balance for savings and debt.

Not keen on the pre-filled template? The sheet also comes in a blank format, making it easier to customize according to your family’s monthly spending.

10. Minimalist Monthly Budget Template

This template has a simple, clean design, making it ideal for those who are looking for a minimalist aesthetic.

It allows you to keep track of income, savings, fixed expenses, and variable expenses. Furthermore, it provides a summary of your funds for the whole month for quick reference.

11. The Budget Tracker

This next example is also a pretty straightforward budget worksheet that will help you keep track of all your monthly household expenses in one place.

This template is also very versatile and can be used for tracking different types of budgets.

12. Template for the Monthly Budget

This template has areas for writing down the amount allocated for a specific expense, the actual amount spent, and the difference between the two, which gives you a quick overview so you know if you’ve overshot or are still within budget.

A “Notes” column lets you enter important, relevant information about each specific expense on the list.

Knowing how much money your family has spent each month month can encourage the members of the household to be more conscious about spending.

Maybe some of the money you save this month can go into the family savings?

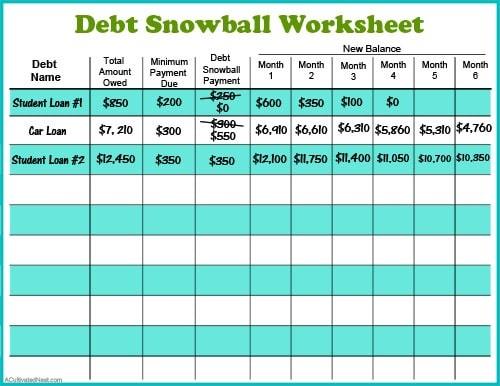

13. Zero Based Budget

Thezero based budgeting system encourages you to justify all household expenses every month.

This is different from traditional budgeting, where a company or household simply builds upon a previous budget and deducts from or adds to the amount allocated for each item.

Only when new expenses come up do budgeters using the traditional method need to justify them, which can result in unnecessary spending.

This template is designed to work with the zero based budget system. It allows you to plan your household’s spending every month, from the ground up.

14. Household Budget Template

If you’re new to budgeting, you might want a no-frills budget template.

This printable is perfect for this.

There are spaces for writing the following information for your monthly budgeting:

Monthly, yearly, and long-term financial goals

Bills and expenses, as well as their specifics

Amount and date due

Column to indicate if the bill/expense has already been paid

This template also features a very apt quote from Albert Einstein:

“Learn from yesterday, live for today, hope for tomorrow.”

15. Budget Planner With Mini Bills Tracker

This budget tracker has provisions for tracking family expenses, such as:

Bills

Pets