Police officers leave Silicon Valley Banks headquarters in Santa Clara, California on March 10, 2023.

Noah Berger | AFP | Getty Images

Silicon Valley Bank employees received their annual bonuses Friday just hours before regulators seized the failing bank, according to people with knowledge of the payments.

The Santa Clara, California-based bank has historically paid employee bonuses on the second Friday of March, said the people, who declined to be identified speaking about the awards. The payments were for work done in 2022 and had been in process days before the bank’s collapse, the sources said.

This year, bonus day happened to fall on SVB’s final day of independence. The institution, in the throes of a bank run triggered by panicked venture capital investors and startup founders, was seized by the Federal Deposit Insurance Corporation (FDIC) around midday Friday.

On Friday, SVB CEO Greg Becker addressed workers in a two-minute video in which he said that he no longer made decisions at the 40-year-old bank, according to the people.

The size of the payouts couldn’t be determined, but SVB bonuses range from about $12,000 for associates to $140,000 for managing directors, according to Glassdoor.com.

SVB was the highest-paying publicly traded bank in 2018, with employees getting an average of $250,683 for that year, according to Bloomberg.

After its seizure, the FDIC offered SVB employees 45 days of employment, the people said. The bank had 8,528 employees as of December.

A spokesman for the FDIC declined to comment on the bonuses.

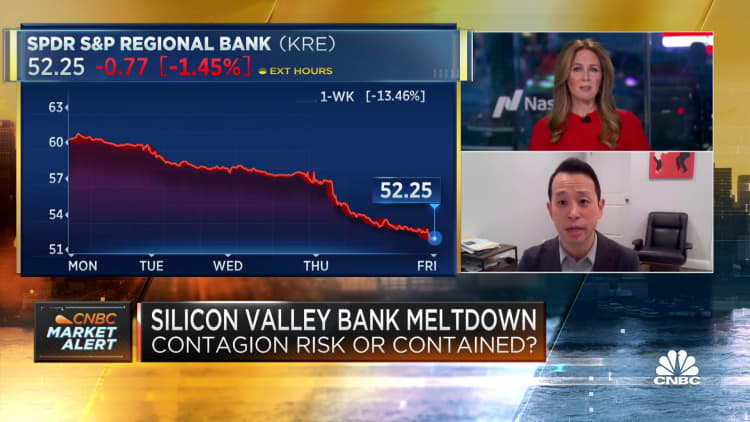

Within 48 hours, a panic induced by the very venture capital community that SVB had served and nurtured ended the bank’s 40-year-run.

Regulators shuttered SVB Friday and seized its deposits in the largest U.S. banking failure since the 2008 financial crisis and the second-largest ever. The company’s downward spiral began late Wednesday, when it surprised investors with news that it needed to raise $2.25 billion to shore up its balance sheet. What followed was the rapid collapse of a highly-respected bank that had grown alongside its technology clients.

Even now, as the dust begins to settle on the second bank wind-down announced this week, members of the VC community are lamenting the role that other investors played in SVB’s demise.

“This was a hysteria-induced bank run caused by VCs,” Ryan Falvey, a fintech investor at Restive Ventures, told CNBC. “This is going to go down as one of the ultimate cases of an industry cutting its nose off to spite its face.”

A Brinks armored truck sits parked in front of the shuttered Silicon Valley Bank (SVB) headquarters on March 10, 2023 in Santa Clara, California.

Justin Sullivan | Getty Images

The episode is the latest fallout from the Federal Reserve‘s actions to stem inflation with its most aggressive rate hiking campaign in four decades. The ramifications could be far-reaching, with concerns that startups may be unable to pay employees in coming days, venture investors may struggle to raise funds, and an already-battered sector could face a deeper malaise.

Shares of Silicon Valley Bank collapsed this week.

The roots of SVB’s collapse stem from dislocations spurred by higher rates. As startup clients withdrew deposits to keep their companies afloat in a chilly environment for IPOs and private fundraising, SVB found itself short on capital. It had been forced to sell all of its available-for-sale bonds at a $1.8 billion loss, the bank said late Wednesday.

The sudden need for fresh capital, coming on the heels of the collapse of crypto-focused Silvergate bank, sparked another wave of deposit withdrawals Thursday as VCs instructed their portfolio companies to move funds, according to people with knowledge of the matter. The concern: a bank run at SVB could pose an existential threat to startups who couldn’t tap their deposits.

SVB customers said CEO Greg Becker didn’t instill confidence when he urged them to “stay calm” during a call that began Thursday afternoon. The stock’s collapse continued unabated, reaching 60% by the end of regular trading. Importantly, Becker couldn’t assure listeners that the capital raise would be the bank’s last, said a person on the call.

All told, customers withdrew a staggering $42 billion of deposits by the end of Thursday, according to a California regulatory filing.

By the close of business that day, SVB had a negative cash balance of $958 million, according to the filing, and failed to scrounge enough collateral from other sources, the regulator said.

Falvey, a former SVB employee who launched his own fund in 2018, pointed to the highly interconnected nature of the tech investing community as a key reason for the bank’s sudden demise.

Prominent funds including Union Square Ventures and Coatue Management blasted emails to their entire rosters of startups in recent days, instructing them to pull funds out of SVB on concerns of a bank run. Social media only heightened the panic, he noted.

“When you say, `Hey, get your deposits out, this thing is gonna fail,’ that’s like yelling fire in a crowded theater,” Falvey said. “It’s a self-fulfilling prophecy.”

Another venture investor, TSVC partner Spencer Greene, also criticized investors who “were wrong on the facts” about SVB’s position.

“It appears to me that there was no liquidity issue until a couple of VCs called it,” Greene said. “They were irresponsible, and then it became self-fulfilling.”

Thursday evening, some SVB customers received emails assuring them that it was “business as usual” at the bank.

“I’m sure you’ve been hearing some buzz about SVB in the markets today so wanted to reach out to provide some context,” one SVB banker wrote to a client, according to a copy of the message obtained by CNBC.

“It is business as usual at SVB,” the banker wrote. “Understandably there may be questions and I want to make myself available if you have any concerns.”

By Friday, as shares of SVB continued to sink, the bank ditched efforts to sell shares, CNBC’s David Faber reported. Instead, it was looking for a buyer, he reported. But the flight of deposits made the sale process harder, and that effort failed too, Faber said.

A customer stands outside of a shuttered Silicon Valley Bank (SVB) headquarters on March 10, 2023 in Santa Clara, California.

Justin Sullivan | Getty Images

Falvey, who started his career at Wells Fargo and consulted for a bank that was seized during the financial crisis, said that his analysis of SVB’s mid-quarter update from Wednesday gave him confidence. The bank was well capitalized and could make all depositors whole, he said. He even counseled his portfolio companies to keep their funds at SVB as rumors swirled.

Now, thanks to the bank run that ended in SVB’s seizure, those who remained with SVB face an uncertain timeline for retrieving their money. While insured deposits are expected to be available as early as Monday, the lion’s share of deposits held by SVB were uninsured, and it’s unclear when they will be freed up.

“The precipitous deposit withdrawal has caused the Bank to be incapable of paying its obligations as they come due,” the California financial regulator stated. “The bank is now insolvent.”

David Solomon, chief executive officer of Goldman Sachs Group Inc., during an event on the sidelines on day three of the World Economic Forum (WEF) in Davos, Switzerland, on Thursday, Jan. 19, 2023.

Stefan Wermuth | Bloomberg | Getty Images

When David Solomon was chosen to succeed Lloyd Blankfein as Goldman Sachs CEO in early 2018, a spasm of fear ran through the bankers working on a modest enterprise known as Marcus.

The man who lost out to Solomon, Harvey Schwartz, was one of several original backers of the firm’s foray into consumer banking and was often seen pacing the floor in Goldman’s New York headquarters where it was being built. Would Solomon kill the nascent project?

The executives were elated when Solomon soon embraced the business.

Their relief was short-lived, however. That’s because many of the decisions Solomon made over the next four years — along with aspects of the firm’s hard-charging, ego-driven culture — ultimately led to the collapse of Goldman’s consumer ambitions, according to a dozen people with knowledge of the matter.

The idea behind Marcus — the transformation of a Wall Street powerhouse into a Main Street player that could take on giants such as Jamie Dimon’s JPMorgan Chase — captivated the financial world from the start. Within three years of its 2016 launch, Marcus — a nod to the first name of Goldman’s founder — attracted $50 billion in valuable deposits, had a growing lending business and had emerged victorious from intense competition among banks to issue a credit card to Apple’s many iPhone users.

But as Marcus morphed from a side project to a focal point for investors hungry for a growth story, the business rapidly expanded and ultimately buckled under the weight of Solomon’s ambitions. Late last year, Solomon capitulated to demands to rein in the business, splitting it apart in a reorganization, killing its inaugural loan product and shelving an expensive checking account.

The episode comes at a sensitive time for Solomon. More than four years into his tenure, the CEO faces pressure from an unlikely source — disaffected partners of his own company, whose leaks to the press in the past year accelerated the bank’s strategy pivot and revealed simmering disdain for his high-profile DJ hobby.

Goldman shares have outperformed bank stock indexes during Solomon’s tenure, helped by the strong performance of its core trading and investment banking operations. But investors aren’t rewarding Solomon with a higher multiple on his earnings, while nemesis Morgan Stanley has opened up a wider lead in recent years, with a price to tangible book value ratio roughly double that of Goldman.

That adds to the stakes for Solomon’s second-ever investor day conference Tuesday, during which the CEO will provide details on his latest plan to build durable sources of revenue growth. Investors want an explanation of what went wrong at Marcus, which was touted at Goldman’s previous investor day in 2020, and evidence that management has learned lessons from the costly episode.

“We’ve made a lot of progress, been flexible when needed, and we’re looking forward to updating our investors on that progress and the path ahead,” Goldman communications chief Tony Fratto said in a statement. “It’s clear that many innovations since our last investor day are paying off across our businesses and generating returns for shareholders.”

The architects of Marcus couldn’t have predicted its journey when the idea was birthed offsite in 2014 at the vacation home of then-Goldman president Gary Cohn. While Goldman is a leader in advising corporations, heads of state and the ultrawealthy, it didn’t have a presence in retail banking.

They gave it a distinct brand, in part to distance it from negative perceptions of Goldman after the 2008 crisis, but also because it would allow them to spin off the business as a standalone fintech player if they wanted to, according to people with knowledge of the matter.

“Like a lot of things that Goldman starts, it began not as some grand vision, but more like, ‘Here’s a way we can make some money,’” one of the people said.

Ironically, Cohn himself was against the retail push and told the bank’s board that he didn’t think it would succeed, according to people with knowledge of the matter. In that way, Cohn, who left in 2017 to join the Trump administration, was emblematic of many of the company’s old guard who believed that consumer finance simply wasn’t in Goldman’s DNA.

Once Solomon took over, in 2018, he began a series of corporate reorganizations that would influence the path of the embryonic business.

From its early days, Marcus, run by ex-Discover executive Harit Talwar and Goldman veteran Omer Ismail, had been purposefully sheltered from the rest of the company. Talwar was fond of telling reporters that Marcus had the advantages of being a nimble startup within a 150-year-old investment bank.

The first of Solomon’s reorganizations came early in his tenure, when he folded it into the firm’s investment management division. Ismail and others had argued against the move to Solomon, feeling that it would hinder the business.

Solomon’s rationale was that all of Goldman’s businesses catering to individuals should be in the same division, even if most Marcus customers had only a few thousand dollars in loans or savings, while the average private wealth client had $50 million in investments.

In the process, the Marcus leaders lost some of their ability to call their own shots on engineering, marketing and personnel matters, in part because of senior hires made by Solomon. Marcus engineering resources were pulled in different directions, including into a project to consolidate its technology stack with that of the broader firm, a step that Ismail and Talwar disagreed with.

“Marcus became a shiny object,” said one source. “At Goldman, everyone wants to leave their mark on the new shiny thing.”

Besides the deposits business, which has attracted $100 billion so far and essentially prints money for the company, the biggest consumer success has been its rollout of the Apple Card.

What is less well-known is that Goldman won the Apple account in part because it agreed to terms that other, established card issuers wouldn’t. After a veteran of the credit-card industry named Scott Young joined Goldman in 2017, he was flabbergasted at one-sided elements of the Apple deal, according to people with knowledge of the matter.

“Who the f— agreed to this?” Young exclaimed in a meeting shortly after learning of the details of the deal, according to a person present.

Some of the customer servicing aspects of the deal ultimately added to Goldman’s unexpectedly high costs for the Apple partnership, the people said. Goldman executives were eager to seal the deal with the tech giant, which happened before Solomon became CEO, they added.

Young declined to comment about the outburst.

The rapid growth of the card, which was launched in 2019, is one reason the consumer division saw mounting financial losses. Heading into an economic downturn, Goldman had to set aside reserves for future losses, even if they don’t happen. The card ramp-up also brought regulatory scrutiny on the way it dealt with customer chargebacks, CNBC reported last year.

Beneath the smooth veneer of the bank’s fintech products, which were gaining traction at the time, there were growing tensions: disagreements with Solomon over products, acquisitions and branding, said the people, who declined to be identified speaking about internal Goldman matters.

Ismail, who was well-regarded internally and had the ability to push back against Solomon, lost some battles and held the line on others. For instance, Marcus officials had to entertain potential sponsorships with Rihanna, Reese Witherspoon and other celebrities, as well as study whether the Goldman brand should replace that of Marcus.

The CEO was said to be enamored of the rise of fast-growing digital players such as Chime and believed that Goldman needed to offer a checking account, while Marcus leaders didn’t think the bank had advantages there and should continue as a more focused player.

One of the final straws for Ismail came when Solomon, in his second reorganization, made his strategy chief, Stephanie Cohen, co-head of the consumer and wealth division in September 2020. Cohen, who is known as a tireless executive, would be even more hands-on than her predecessor, Eric Lane, and Ismail felt that he deserved the promotion.

Within months, Ismail left Goldman, sending shock waves through the consumer division and deeply angering Solomon. Ismail and Talwar declined to comment for this article.

Ismail’s exit ushered in a new, ultimately disastrous era for Marcus, a dysfunctional period that included a steep ramp-up in hiring and expenses, blown product deadlines and waves of talent departures.

Now run by two former tech executives with scant retail experience, ex-Uber executive Peeyush Nahar and Swati Bhatia, formerly of payments giant Stripe, Marcus was, ironically, also cursed by Goldman’s success on Wall Street in 2021.

The pandemic-fueled boom in public listings, mergers and other deals meant that Goldman was en route to a banner year for investment banking, its most profitable ever. Goldman should plow some of those volatile earnings into more durable consumer banking revenues, the thinking went.

“People at the firm including David Solomon were like, ‘Go, go, go!’” said a person with knowledge of the period. “We have all these excess profits, you go create recurring revenues.”

In April 2022, the bank widened testing of its checking account to employees, telling staff that it was “only the beginning of what we hope will soon become the primary checking account for tens of millions of customers.”

But as 2022 ground on, it became clear that Goldman was facing a very different environment. The Federal Reserve ended a decade-plus era of cheap money by raising interest rates, casting a pall over capital markets. Among the six biggest American banks, Goldman Sachs was most hurt by the declines, and suddenly Solomon was pushing to cut expenses at Marcus and elsewhere.

Amid leaks that Marcus was hemorrhaging money, Solomon finally decided to pull back sharply on the effort that he had once championed to investors and the media. His checking account would be repurposed for wealth management clients, which would save money on marketing costs.

Now it is Ismail, who joined a Walmart-backed fintech called One in early 2021, who will be taking on the banking world with a direct-to-consumer digital startup. His former employer Goldman would largely content itself with being a behind-the-scenes player, providing its technology and balance sheet to established brands.

For a company with as much self-regard as Goldman, it would mark a sharp comedown from the vision held by Solomon only months earlier.

“David would say, ‘We’re building the business for the next 50 years, not for today,’” said one former Goldman insider. “He should’ve listened to his own sound bite.”

Wells Fargo laid off hundreds of mortgage bankers this week as part of a sweeping round of cuts triggered by the bank’s recent strategic shift, CNBC has learned.

The layoffs were announced Tuesday and ensnared some top producers, including a few bankers who surpassed $100 million in loan volumes last year and who recently attended an internal sales conference for high achievers, according to people with knowledge of the situation.

Under CEO Charlie Scharf, Wells Fargo is pulling back from parts of the U.S. mortgage market, an arena it once dominated. Instead of seeking to maximize its share of American home loans, the bank is focusing mostly on serving existing customers and minority communities. The shift comes after sharply higher interest rates led to a collapse in loan volumes, forcing Wells Fargo, JPMorgan Chase and other firms to cut thousands of mortgage positions in the past year.

Those cut this week at Wells Fargo included mortgage bankers and home loan consultants, a workforce spread around the country, who are compensated mostly on sales volume, according to the people, who declined to be identified speaking about personnel matters.

The company cut bankers who operated in areas outside of its branch footprint and who therefore didn’t fit in the new strategy of catering to existing customers, the people said. Those cuts include bankers across the Midwest and the East Coast, one of the people said.

Some of those people were successful enough last year to be flown to a resort in Palm Desert, California, for a company-sponsored conference earlier this month. Palm Desert is a luxury enclave known for its warm weather, golf courses and proximity to Palm Springs.

It’s common practice in finance to reward top salespeople with multiday events held in swanky resorts that combine recognition, recreation and educational sessions. For instance, JPMorgan’s mortgage division is holding a sales conference in April.

A Wells Fargo spokeswoman said the bank has communicated with affected employees, provided severance and career guidance, and tried to retain as many workers as possible.

“We announced in January strategic plans to create a more focused home-lending business,” she said. “As part of these efforts, we have made displacements across our home-lending business in alignment with this strategy and in response to significant decreases in mortgage volume.”

The bank will also continue to serve customers “in any market in the United States” through its centralized sales channel, she added.

While this latest round of cuts wasn’t based on employees’ performance, Wells Fargo has also been cutting mortgage workers who don’t meet minimum standards of production.

In areas with expensive housing, that could be a minimum of at least $10 million worth of loans over the past 12 months, said one of the sources.

Last month, the bank said that mortgage volumes continued to shrink in the fourth quarter, falling 70% to $14.6 billion. Wells Fargo said it almost 11,000 fewer employees at the end of 2022 than in 2021.

The January mortgage announcement, reported first by CNBC, led recruiters to swarm top performers in the hopes of poaching them, according to one of the people.

Scharf addressed employees in a Jan. 25 town hall meeting in which he reiterated his rationale for the mortgage retrenchment.

Pedestrians pass a Wells Fargo bank branch in New York, U.S., on Thursday, Jan. 13, 2022.

Victor J. Blue | Bloomberg | Getty Images

Wells Fargo is unveiling a new platform to boost digital engagement with its 2.6 million wealth management clients, CNBC has learned.

The service, called LifeSync, lets users create and track progress on financial goals, ingest content tied to their plans and contact their advisors, according to Michael Liersch, head of advice and planning at the bank’s wealth division. It will be delivered through a mobile app update in late March, he said.

“These are the things that will really enhance the client-advisor experience, and they’re not available on the mobile app today,” Liersch said. “This is a really big platform enhancement for clients and advisors to collaborate around their goals and connect what clients want to accomplish with what our advisors are doing.”

Banks are jockeying to provide their customers with personalized experiences via digital channels, and this tool should enable Wells Fargo to boost satisfaction and loyalty. CEO Charlie Scharf has highlighted wealth management as one source of growth for the company, along with credit cards and investment banking, amid his efforts to overhaul the bank and appease regulators.

Wells Fargo is a major player in American wealth management, with $1.9 trillion in client assets and 12,027 financial advisors as of December.

But its client assets haven’t grown since the end of 2019, when they also stood at $1.9 trillion. Under Scharf’s streamlining efforts, Wells Fargo sold its asset management business and dropped international wealth clients in 2021.

The trajectory of the asset figure “primarily is a reflection of the volatility seen over the last few years,” according to a bank spokesperson.

With its new offering, Wells Fargo hopes to turn the tide. The bank may eventually opt to offer a financial planning tool to its broader banking population, said Liersch. That would follow the move that Bank of America made in 2019, when it unveiled a digital planning tool called Life Plan.

“We wanted to solve for that more complex experience first, and then develop the client-directed capability which is absolutely in our consideration set,” Liersch said.

A day after U.S. forces completed its troop withdrawal from Afghanistan, refugees board a bus taking them to a processing center upon their arrival at Dulles International Airport in Dulles, Virginia, September 1, 2021.

Kevin Lamarque | Reuters

WASHINGTON — House Republicans on Friday called on the Biden administration to release information about the chaotic U.S. departure from Afghanistan.

In a series of letters sent to senior leadership at the departments of Defense, State, Homeland Security, and the U.S. Agency for International Development, GOP lawmakers requested all documents, communications and information related to what they called the Biden administration’s “disastrous military and diplomatic withdrawal from Afghanistan.”

“U.S. servicemen and women lost their lives, Americans were abandoned, taxpayer dollars are unaccounted for, the Taliban gained access to military equipment, progress for Afghan women was derailed, and the entire area is now under hostile Taliban control,” wrote Republican Rep. James Comer of Kentucky and other key GOP representatives.

“The American people deserve answers and the Biden Administration’s ongoing obstruction of this investigation is unacceptable,” added Comer, the chairman of the House Oversight and Accountability Committee.

The U.S. finished its withdrawal from the airport in Kabul on Aug. 31, 2021. The departure effectively ended a two-decade conflict that began shortly after the terrorist attacks of Sept. 11, 2001.

Biden ordered the full withdrawal of approximately 3,000 U.S. troops from Afghanistan in April 2021. At the time, he asked all American servicemembers to leave the war-weary country by Sept. 11 of that year. He later moved the deadline up to the end of August.

The U.S. launched its war in Afghanistan in October 2001, weeks after the Sept. 11 attacks. The Taliban at the time offered sanctuary to al-Qaeda, which planned and carried out the devastating terrorist attacks on the World Trade Center and the Pentagon.

Taliban fighters patrol in Wazir Akbar Khan neighborhood in the city of Kabul, Afghanistan, Wednesday, Aug. 18, 2021.

Rahmat Gul | AP

People who want to flee the country continue to wait around Hamid Karzai International Airport in Kabul, Afghanistan on August 25, 2021.

Anadolu Agency | Anadolu Agency | Getty Images

In the final week of the withdrawal, terrorists from the group ISIS-K killed 13 U.S. service members and dozens of Afghans in an attack outside the airport. U.S. forces launched strikes to try to thwart other attacks.

Biden and first lady Jill Biden traveled to Dover Air Force Base to meet privately with the families of the fallen U.S. service members before they watched the dignified transfer of American flag-draped caskets from a C-17 military cargo plane to a vehicle. The process takes place for every U.S. servicemember killed in action.

Goldman Sachs has dropped plans to develop a Goldman-branded credit card for retail customers, another casualty of the firm’s strategic pivot, CNBC has learned.

Not long ago, CEO David Solomon told analysts that the bank was developing its own card, which would’ve made use of the platform Goldman created for its Apple Card partnership.

It was part of an ambitious vision Solomon had for serving everyday Americans by stretching beyond the core competencies of the 154-year old investment bank. A Goldman card would’ve been part of a suite of products, including a digital checking account, to help enhance the profit margins and loyalty of its retail efforts, according to people with knowledge of the matter.

That vision unraveled after Solomon bowed to pressure to stem losses from its consumer businesses as storm clouds gathered on the U.S. economy last year. In October, the bank split its retail operations in a corporate overhaul and later said it was shuttering its Marcus personal loans business and shelving plans to widely offer a checking account.

When it scaled back plans to become the primary bank for the masses, the rationale for a Goldman card evaporated, said one of the people, who declined to be identified speaking about a former employer.

Executives had believed consumers would covet a card from Goldman Sachs. After all, Apple had insisted that Goldman Sachs was etched on the back of its titanium cards, not the Marcus brand that Goldman unveiled in 2016, according to a person with knowledge of the matter.

It would allow the bank to be more choosy with who it approved as customers and wouldn’t require sharing revenue with a partner, as it does with Apple.

But launching its own card would be even more expensive than partnering with an outside brand, as Goldman would’ve footed the cost of acquiring customers and enticing them with rewards. Card giants including JPMorgan Chase and Citigroup have a combination of co-brand products with airlines and retailers and their own direct cards.

The concept of a Goldman card first surfaced in Oct. 2021 when an analyst asked Solomon about his consumer product roadmap. One idea was to use the card technology created to service Apple Card customers for its own card, he said.

“We have our own credit card platform that I think is really differentiated, and we’re onboarding both other partnerships, but also have the opportunity for a proprietary card that’s in development,” Solomon said.

Although the idea of a card offered with a suite of banking products was mentioned as recently as last summer by Goldman executive Stephanie Cohen, little had been done to actually develop it, according to people with knowledge of the situation.

The bank’s ambitions in consumer finance outstripped its ability to execute on them, Solomon acknowledged last month. It didn’t help that its existing card products caught the attention of regulators including the Consumer Financial Protection Bureau.

“The idea of a consumer-facing proprietary Goldman Sachs credit card was discussed but never became a meaningful part of our strategy,” said a spokesman for the New York-based bank.

A closer shot of Ukraine President Volodymyr Zelenskyy and the Ministry of Economy (MoE) meeting with senior members of J.P. Morgan.

Coutesy: JP Morgan Summit

Ukraine’s government signed an agreement with JPMorgan Chase to help advise the war-afflicted country on its economy and future rebuilding efforts.

Ukraine’s Ministry of Economy signed a memorandum of understanding with a group of executives from the New York-based bank on Thursday aimed at rebuilding and developing the country, according to a statement from President Volodymyr Zelenskyy.

One year into its conflict with Russia, which invaded in February 2022, Ukraine’s government is laying the groundwork to help rebuild the country. The invasion has cost thousands of civilian lives and set off Europe’s largest refugee crisis since the Second World War. It also ignited a corporate exodus from Russia, and has helped galvanize support for Ukraine.

JPMorgan will tap its debt capital markets operations, payments, and commercial banking and infrastructure investing expertise to help the country stabilize its economy and credit rating, manage its funds, and advance its digital adoption, according to a person with knowledge of the agreement.

Of particular importance is advising the nation on efforts to raise private funds to help it rebuild and invest for future growth in areas including renewable energy, agriculture and technology.

“The full resources of JPMorgan Chase are available to Ukraine as it charts its post-conflict path to growth,” CEO Jamie Dimon said in a statement.

Dimon added JPMorgan was proud of its support for Ukraine and was committed to its people. The bank led a $20 billion debt restructuring for the country last year and has committed millions of dollars in support for its refugees.

Rt. Hon. Tony Blair, Former Prime Minister Great Britain and Condoleezza Rice, 66th U.S. Secretary of State conducted a discussion with Ukraine President Volodymyr Zelensky @ annual JPMorgan Summit held Feb 10.

Courtesy: JP Morgan Summit

On Friday, Zelenskyy spoke via teleconference with guests of JPMorgan’s annual wealth management summit in Miami after the agreement was signed. The discussion was moderated by ex-U.K. Prime Minister Tony Blair and former Secretary of State Condoleezza Rice.

Traders work on the floor of the New York Stock Exchange on Wall Street in New York City.

Angela Weiss | Afp | Getty Images

Wall Street just pulled off its biggest IPO in four months, giving bankers hope that the market for newly-listed company shares is stirring to life.

The solar technology firm Nextracker raised $638 million by selling about 15% more shares than expected, sources told CNBC Wednesday.

The listing, which began trading Thursday, shows that the stock market’s rebound this year is reviving appetite for new companies from mutual fund and hedge fund managers, said Michael Wise, JPMorgan Chase‘s vice chairman for equity capital markets.

Wall Street’s so-called IPO window, which allows companies to readily tap investors for new stock, has been mostly shut for the past year. Proceeds from public listings plunged 94% last year to the lowest level since 1990 as the Federal Reserve raised interest rates. The upheaval removed a key generator of fees for investment banks in 2022, leading to industrywide layoffs, and forced private companies to cut workers in a bid to “extend their runway.”

Private companies extend their runway by stretching budgets — usually by cutting expenses, like employees— to avoid raising capital or going public until market conditions improve.

“The window seems like it’s cracked open right now,” Wise told CNBC in a phone interview. “The strong market performance since the beginning of this year has investors and issuers back and engaged; many companies are now going through pre-IPO, testing-the-waters processes.”

On the heels of the Nextracker listing, other renewable energy firms are planning to list in the U.S., including Tel Aviv-based Enlight, according to bankers. New York-based JPMorgan is lead advisor on both of those deals.

Morgan Stanley is also seeing a “higher degree of investor engagement regarding bringing IPOs to market” than during most of last year, according to Andrew Wetenhall, Morgan Stanley’s co-head of equity capital markets in the Americas.

Morgan Stanley, JPMorgan and Goldman Sachs are three of the top advisors on public listings globally, according to Dealogic data.

But the market isn’t open to just anyone. Investors have soured on the prospects of unprofitable companies, and many tech listings from 2020 and 2021 are still underwater.

In-favor sectors now include green energy, thanks in part to the Inflation Reduction Act; biotech companies with promising drug trials; retail brands that have held up well in the current environment; and parts of the financial sector like insurance, bankers said.

The common theme is that newly-listed companies need to be profitable, in sectors that are doing well or at least aren’t especially sensitive to rising interest rates.

“This market is opening, it is not wide open,” Wetenhall said. “The parties that should bring their deals in this environment probably have a set of features that fit the current investor sentiment.”

A bigger test of the market is coming as Johnson & Johnson has filed to take its Kenvue consumer health unit public, continuing a trend of IPOs led by spinoffs. That’s because Kenvue’s implied market capitalization is north of $50 billion, and investors have been eager for larger listings, according to a banker. That listing could happen as early as April, another banker said.

Waiting in the wings are other companies, ranging from delivery giant Instacart, payments processor Stripe, Fortnite owner Epic games, sports clothing retailer Fanatics and digital banking provider Chime.

Instacart’s listing could happen as soon as midyear, according to a banker with knowledge of the situation. With Stripe, however, management may pursue options to remain private for longer, this banker said.

A broader return to IPO listings will likely come in the second half of the year at the earliest, especially for most tech and fintech names, which are still generally out of favor.

“Tech has been very quiet,” said a different banker who declined to be identified, speaking frankly. “I think it’s going to take a while for that to recover.”

The solar technology company Nextracker priced its initial public offering just above its stated $20 to $23 per share range, people with knowledge of the transaction told CNBC.

The order book for Fremont, California-based Nextracker was “well subscribed,” meaning demand allowed the company to exceed expectations on pricing, sources who declined to be identified speaking about the process told CNBC earlier Wednesday.

The IPO is expected to raise about $638 million by selling 26.6 million shares at $24 each, which is well above the $535 million upper limit the company said it was seeking in a filing last week. That is also before the so-called greenshoe option that allows bankers to sell more stock, the people said.

The development is a good sign for the moribund IPO market. Proceeds from public listings fell 94% last year after the Federal Reserve began its most aggressive rate-increasing campaign in decades. Investors soured on the shares of unprofitable tech companies in particular, many of which are still underwater after listing in 2020 and 2021.

The Nextracker IPO is arguably the first meaningful public listing this year as it is set to be the biggest U.S. IPO since autonomous driving firm Mobileye raised $990 million in October.

Nextracker will begin trading on the Nasdaq exchange Thursday morning under the symbol NXT, according to one of the people.

The company, which was a subsidiary of manufacturer Flex, sells hardware and software that enables solar panels to follow the movement of the sun, improving the output of solar power plants.

JPMorgan Chase was lead advisor on the transaction, according to a regulatory filing.

WASHINGTON –U.S. Secretary of State Antony Blinken will postpone his trip to China next week following a suspected Beijing-operated spy balloon looming over parts of Montana.

“After consultations with our interagency partners, as well as with Congress, we have concluded that the conditions are not right at this moment for Secretary Blinken to travel to China,” a senior State Department official said Friday on a background briefing with reporters.

Blinken, who was slated to depart for Beijing on Friday evening, was scheduled to meet with his Chinese counterpart, Minister of Foreign Affairs Qin Gang, and potentially Chinese President Xi Jinping, as well.

The official declined to say when Blinken would reschedule his travel to China, saying only that the department would “determine when the conditions are right.”

Chinese authorities said Friday that the balloon operating over U.S. airspace was a civilian weather balloon intended for scientific research. But the State Department said that was immaterial.

“We have noted the PRC statement of regret, but the presence of this balloon in our airspace is a clear violation of our sovereignty as well as international law and is unacceptable that this has occurred,” the official said.

While Blinken has postponed his travel, the U.S. and China have not suspended communication over the incident.

“From the moment this incident occurred, we have been in regular and frequent contact with our Chinese counterparts and I do anticipate that will continue,” said the State Department official, who asked not to be identified to discuss a sensitive intelligence matter.

China’s Foreign Ministry said in a statement that westerly winds had caused the airship to stray into U.S. territory, describing the incident as a result of “force majeure” — or greater force — for which it was not responsible. “The airship comes from China and is of a civilian nature, used for scientific research such as meteorology,” according to a Google translation of a statement on the foreign ministry’s website.

On Thursday, a senior U.S. defense official told reporters that the U.S. was aware of the balloon and was confident that it was China’s.

The official, who spoke on the condition of anonymity as ground rules established by the Pentagon, added that President Joe Biden was briefed on the matter. Following consultations with senior leaders, including Joint Chiefs of Staff Chairman Gen. Mark Milley and Defense Secretary Lloyd Austin, Biden decided the U.S. would not shoot down the balloon, the official said.

“We had been looking at whether there was an option yesterday over some sparsely populated areas in Montana,” said the official, who noted it was decided the possible debris field from the balloon could cause damage on the ground and that its intelligence collection potential has “limited additive value” compared with Chinese spy satellites.

“We wanted to take care that somebody didn’t get hurt or property wasn’t destroyed,” said the official, who noted that the balloon does not pose a threat to civil aviation because of its high altitude.

On Capitol Hill, members of Congress sounded alarms and sought more information from the Biden administration.

House Speaker Kevin McCarthy, R-Ca., said he had requested a briefing for the so-called “Gang of Eight,” the Republican and Democratic leaders of both the House and Senate, and the leaders from both parties of the Senate and House intelligence committees.

Sen. Jon Tester, D-Mont., who represents the state where the balloon was first identified, said he is in contact with Defense Department and intelligence officials over the matter, but expressed frustration at the lack of detail.

“We are still waiting for real answers on how this happened and what steps the Administration took to protect our country, and I will hold everyone accountable until I get them,” Tester said in a statement Friday.

The Senate was not in a full session Friday, but Tester’s office said he will receive a classified briefing in a secure facility as soon as he returns to Washington.

Florida Sen. Marco Rubio, the top Republican on the Senate Intelligence Committee, said the military should have shot down the balloon.

“It was a mistake to not shoot down that Chinese spy balloon when it was over a sparsely populated area,” Rubio tweeted on Friday.

“This is not some hot air balloon, it has a large payload of sensors roughly the size of two city buses & the ability to maneuver independently,” Rubio added.

This story is developing. Please check back for updates.

David Solomon, Chairman & CEO of Goldman Sachs, speaking on Squawk Box at the WEF in Davos, Switzerland on Jan. 23rd, 2023.

Adam Galica | CNBC

Goldman Sachs CEO David Solomon will get a $25 million compensation package for his work last year, the bank said Friday in a regulatory filing.

The package includes a $2 million base salary and variable compensation of $23 million, New York-based Goldman said in the filing. Most of Solomon’s bonus — 70%, or $16.1 million — is in the form of restricted shares tied to performance metrics, while the rest is paid in cash, the bank said.

related investing news

Solomon’s pay, while large, is about 29% lower than the $35 million he was granted for his 2021 performance. Similarly, Goldman’s full-year earnings fell by 48% to $11.3 billion amid sharp declines in investment banking and asset management revenue, the company said last week.

While the bank was primarily hit by industrywide slowdowns in capital markets activity as the Federal Reserve raised interest rates, Solomon also faced his own set of issues. Goldman was forced to scale back its ambitions in consumer finance and lay off nearly 4,000 workers in two rounds of terminations in recent months.

David Solomon, chief executive officer of Goldman Sachs Group Inc., during a Bloomberg Television at the Goldman Sachs Financial Services Conference in New York, US, on Tuesday, Dec. 6, 2022.

Michael Nagle | Bloomberg | Getty Images

Goldman Sachs is scheduled to report fourth-quarter earnings before the opening bell Tuesday.

Here’s what Wall Street expects:

related investing news

Earnings: $5.48 per share, 49% lower than a year earlier, according to Refinitiv

Revenue: $10.83 billion, 14% lower than a year earlier.

Trading Revenue: Fixed Income $2.31 billion, Equities $2.14 billion

Investing Banking: $1.75 billion

How long will the investment banking drought last?

That’s one of the top questions analysts will have for Goldman CEO David Solomon.

While the fourth quarter was an ugly one for bankers — Wall Street rivals JPMorgan Chase and Citigroup each posted declines in investment banking revenue of nearly 60% last week — analysts question the odds of a rebound sometime later this year.

They’ll also want to hear Solomon’s views on headcount and expenses after the bank laid off up to 3,200 employees last week, as well as details about Goldman’s consumer operations as it scales back ambitions there.

Goldman shares have climbed 8.9% this year going into Tuesday’s trading, compared with a 6.7% advance for the KBW Bank Index.

Last week, JPMorgan Chase and Bank of America topped profit expectations on surging net interest income, while Wells Fargo and Citigroup posted mixed results. Morgan Stanley is also scheduled to release results Tuesday.

This story is developing. Please check back for updates.

Jamie Dimon, CEO of JPMorgan Chase, testifies during the Senate Banking, Housing, and Urban Affairs Committee hearing titled Annual Oversight of the Nations Largest Banks, in Hart Building on Thursday, September 22, 2022.

Tom Williams | CQ-Roll Call, Inc. | Getty Images

JPMorgan Chase is scheduled to report fourth-quarter earnings before the opening bell Friday.

Here’s what Wall Street expects:

related investing news

Earnings: $3.07 per share, 7.9% lower than a year earlier, according to Refinitiv.

Revenue: $34.3 billion, 13% higher than a year earlier.

Provision for credit losses $1.96 billion, according to StreetAccount

Trading revenue: fixed income $3.76 billion, equities $1.92 billion

Investment banking revenue: $1.57 billion

JPMorgan, the biggest U.S. bank by assets, will be closely watched for clues on how the industry is navigating an economy at a crossroads.

Analysts are expecting a mixed bag of conflicting trends from banks. Higher rates will help lenders earn more interest income, but some of that boost will be offset by larger provisions for expected loan losses as the economy slows.

Wall Street won’t likely come to the rescue. Investment banking revenue is expected to plunge 50% in the wake of frozen IPO markets and subdued deals, Barclays analyst Jason Goldberg said in a Jan. 11 note.

That will be partly offset by a 10% rise in trading revenue, thanks to a boost from fixed income operations, he wrote.

Of greater interest, perhaps, is what JPMorgan CEO Jamie Dimon says about the economy. The veteran CEO rattled markets last year when he said an economic “hurricane” caused by the Federal Reserve was headed for the U.S.

Shares of JPMorgan have climbed 4% this year, compared with the 6% rise of the KBW Bank Index.

Dimon said in June that he was preparing the bank for an economic “hurricane” caused by the Federal Reserve and Russia’s war in Ukraine.

Al Drago | Bloomberg | Getty Images

JPMorgan Chase on Thursday shut down the website for a college financial aid platform it bought for $175 million after alleging that the company’s founder created nearly 4 million fake customer accounts.

The country’s biggest bank acquired Frank in Sept. 2021 to help it deepen relationships with college students, a key demographic, a Chase executive told CNBC at the time.

related investing news

JPMorgan touted the deal as giving it the “fastest-growing college financial planning platform” used by more than five million students at 6,000 institutions. It also provided access to the startup’s founder Charlie Javice, who joined the New York-based bank as part of the acquisition.

Months after the transaction closed, JPMorgan said it learned the truth after sending out marketing emails to a batch of 400,000 Frank customers. About 70% of the emails bounced back, the bank said in a lawsuit filed last month in federal court.

Javice, who had approached JPMorgan in mid-2021 about a potential sale, lied to the bank about her startup’s scale, the bank alleged. Specifically, after being pressed for confirmation of Frank’s customer base during the due diligence process, Javice used a data scientist to invent millions of fake accounts, according to JPMorgan.

“To cash in, Javice decided to lie, including lying about Frank’s success, Frank’s size, and the depth of Frank’s market penetration in order to induce JPMC to purchase Frank for $175 million,” the bank said. “Javice represented in documents placed in the acquisition data room, in pitch materials, and through verbal presentations [that] more than 4.25 million students had created Frank accounts to begin applying for federal student aid using Frank’s application tool.”

Instead of gaining a business with 4.25 million students, JPMorgan had one with “fewer than 300,000 customers,” JPMorgan said in the suit.

A lawyer for Javice told the Wall Street Journal that JPMorgan had “manufactured” reasons to fire her late last year to avoid paying millions of dollars owed to her. Javice has sued JPMorgan, saying that the bank should front legal bills she incurred during its internal investigations.

“After JPM rushed to acquire Charlie’s rocketship business, JPM realized they couldn’t work around existing student privacy laws, committed misconduct and then tried to retrade the deal,” attorney Alex Spiro told the Journal. “Charlie blew the whistle and then sued.”

Spiro, a partner with Quinn Emanuel, didn’t immediately return a call from CNBC.

JPMorgan spokesman Pablo Rodriguez had this response:

“Our legal claims against Ms. Javice and Mr. Amar are set out in our complaint, along with the key facts,” he said. “Ms. Javice was not and is not a whistleblower. Any dispute will be resolved through the legal process.”

The alleged fraud perpetrated by Javice and one of her executives “materially damaged JPMC in an amount to be proven at trial, but not less than $175 million,” JPMorgan said in its suit.

Regardless of the outcome of this legal scuffle, this is an embarrassing episode for JPMorgan and its CEO Jamie Dimon. In a bid to fend off encroaching competitors, JPMorgan has gone on a buying spree of fintech companies in recent years, and Dimon has repeatedly defended his technology investments as necessary ones that will yield good returns.

The fact that a young founder in an industry known for shaky metrics and a “fake it ’til you make it” ethos managed to dupe JPMorgan calls into question how stringent the bank’s due diligence process is.

In an interview at the time of the deal, Javice marveled at how far she had come in just a few years leading her startup.

“Today is my first day employed by someone else, ever,” Javice told CNBC. “I mean it still feels very much like, pinch me, did this really happen?”

As a result of the legal scuffle, JPMorgan shut down Frank early Thursday morning.

“Frank is no longer available” the website now reads. “To file your Free Application for Federal Student Aid (FAFSA), visit StudentAid.gov.”

Wells Fargo is stepping back from the multi-trillion dollar market for U.S. mortgages amid regulatory pressure and the impact of higher interest rates.

Instead of its previous goal of reaching as many Americans as possible, the company will now offer home loans to existing bank and wealth management customers and borrowers in minority communities, CNBC has learned.

The dual factors of a lending market that has collapsed since the Federal Reserve began raising rates last year and heightened regulatory oversight — both industrywide, and specific to Wells Fargo after its 2016 fake accounts scandal — led to the decision, said consumer lending chief Kleber Santos.

“We are acutely aware of Wells Fargo’s history since 2016 and the work we need to do to restore public confidence,” Santos said in a phone interview. “As part of that review, we determined that our home lending business was too large, both in terms of overall size and its scope.”

It’s the latest, and perhaps most significant, strategic shift that CEO Charlie Scharf has undertaken since joining Wells Fargo in late 2019. Mortgages are by far the biggest category of debt held by Americans, making up 71% of the $16.5 trillion in total household balances. Under Scharf’s predecessors, Wells Fargo took pride in its vast share in home loans — it was the country’s top lender as recently as 2019, according to industry newsletter Inside Mortgage Finance.

Now, as a result of this and other changes that Scharf is making, including pushing for more revenue from investment banking and credit cards, Wells Fargo will more closely resemble megabank rivals Bank of America and JPMorgan Chase. Both companies ceded mortgage share after the 2008 financial crisis.

Following those once-huge mortgage players in slimming down their operations has implications for the U.S. mortgage market.

As banks stepped back from home loans after the disaster that was the early 2000’s housing bubble, non-bank players including Rocket Mortgage quickly filled the void. But these newer players aren’t as closely regulated as the banks are, and industry critics say that could expose consumers to pitfalls. Today, Wells Fargo is the third biggest mortgage lender after Rocket and United Wholesale Mortgage.

As part of its retrenchment, Wells Fargo is also shuttering its correspondent business that buys loans made by third-party lenders and “significantly” shrinking its mortgage servicing portfolio through asset sales, Santos said.

The correspondence channel is a significant pipeline of business for San Francisco-based Wells Fargo, one that became larger as overall loan activity shrank last year. In October, the bank said 42% of the $21.5 billion in loans it originated in the third quarter were correspondence loans.

The sale of mortgage servicing rights to other industry players will take at least several quarters to complete, depending on market conditions, Santos said. Wells Fargo is the biggest U.S. mortgage servicer, which involves collecting payments from borrowers, with nearly $1 trillion in loans, or 7.3% of the market, as of the third quarter, according to data from Inside Mortgage Finance.

Altogether, the shift will result in a fresh round of layoffs for the bank’s mortgage operations, executives acknowledged, but they declined to quantify exactly how many. Thousands of mortgage workers were terminated or voluntarily left the company last year as business declined.

The news shouldn’t be a complete surprise to investors or employees. Wells Fargo employees have speculated for months about changes coming after Scharf telegraphed his intentions several times in the past year. Bloomberg reported in August that the bank was considering paring back or halting correspondent lending.

“It’s very different today running a mortgage business inside a bank than it was 15 years ago,” Scharf told analysts in June. “We won’t be as large as we were historically” in the industry, he added.

Wells Fargo said it was investing $100 million towards its goal of minority homeownership and placing more mortgage consultants in branches located in minority communities.

“Our priority is to de-risk the place, to focus on serving our own customers and play the role that society expects us to play as it relates to the racial homeownership gap,” Santos said.

The mortgage shift marks what is potentially the last major business change Scharf will undertake after splitting the bank’s operations into five divisions, bringing in 12 new operating committee members and creating a diversity segment.

In a phone interview, Scharf said that he didn’t anticipate doing other major changes, with the caveat that the bank will need to adapt to changing conditions.

“Given the quality of the five major businesses across the franchise, we think we’re positioned to compete against the very best out there and win, whether it’s banks, non-banks or fintechs,” he said.

People enter the Goldman Sachs headquarters building in New York, U.S., on Monday, June 14, 2021.

Michael Nagle | Bloomberg | Getty Images

Goldman Sachs is laying off fewer employees than feared, but the cut is still a deep one.

The global investment bank is letting go of as many as 3,200 employees starting Wednesday, according to a person with knowledge of the firm’s plans.

That amounts to 6.5% of the 49,100 employees Goldman had in October, which is below the 8% reported last month as the upper end of possible cuts.

The final figure, reported earlier by Bloomberg, is a result of internal discussions between business heads and top management over the last month, said the person, who declined to be identified speaking about personnel decisions.

Goldman CEO David Solomon kicked off Wall Street’s layoff season in September and then opted to enact the industry’s deepest cuts so far. Bank employee levels swelled over the last two years in response to a boom in deals and trading activity, but the good times didn’t last: IPO issuance plunged 94% last year because of suddenly inhospitable markets, according to SIFMA data.

Now, with concerns that the economy will slow further this year, Goldman is pulling back on headcount in case stock and bond issuance and mergers don’t rebound. Solomon is also scaling back his ambitions in consumer banking, resulting in part of the layoffs.

Other investment banks are adopting a “wait and see” attitude in the coming weeks. If revenues are tracking below estimate in February and March, the industry could cut more workers, said a person familiar with a leading Wall Street firm’s processes.

Ether has hugely outperformed bitcoin since both cryptocurrencies formed a bottom in June 2022. Ether’s superior gains have come as investors anticipate a major upgrade to the ethereum blockchain called “the merge.”

Yuriko Nakao | Getty Images

U.S. banking regulators warned financial institutions on Tuesday that dealing with cryptocurrency exposes them to an array of risks, including scams and fraud.

“The events of the past year have been marked by significant volatility and the exposure of vulnerabilities in the crypto-asset sector,” the regulators said in a joint statement from the Federal Reserve, Federal Deposit Insurance Corp. and the Office of the Comptroller of the Currency. The comments come just weeks after the spectacular collapse of crypto exchange FTX.

related investing news

The regulators said the risks include: “fraud and scams among crypto-asset sector participants” and “contagion risk within the crypto-asset sector resulting from interconnections among certain crypto-asset participants.”

During the crypto boom, when financial players seemed to announce a new crypto partnership on a weekly basis, bank executives said they needed further guidance from regulators before dealing more directly with bitcoin and other cryptocurrencies in retail and institutional trading businesses.

Now, about two months after the bankruptcy filing of FTX, the industry has been exposed as rife with poor risk management, interconnected risks and outright fraud.

While the statement indicated that regulators were still assessing how banks could adopt crypto while adhering to their various mandates for consumer protection and anti-money laundering, they seemed to give a clue as to which direction they were headed.

“Based on the agencies’ current understanding and experience to date, the agencies believe that issuing or holding as principal crypto-assets that are issued, stored, or transferred on an open, public, and/or decentralized network, or similar system is highly likely to be inconsistent with safe and sound banking practices,” the regulators said.

They also said that they have “significant safety and soundness concerns” with banks that focus on crypto clients or that have “concentrated exposures” to the sector.

Partygoers with unicorn masks at the Hometown Hangover Cure party in Austin, Texas.

Harriet Taylor | CNBC

Bill Harris, former PayPal CEO and veteran entrepreneur, strode onto a Las Vegas stage in late October to declare that his latest startup would help solve Americans’ broken relationship with their finances.

“People struggle with money,” Harris told CNBC at the time. “We’re trying to bring money into the digital age, to redesign the experience so people can have better control over their money.”

related investing news

But less than a month after the launch of Nirvana Money, which combined a digital bank account with a credit card, Harris abruptly shuttered the Miami-based company and laid off dozens of workers. Surging interest rates and a “recessionary environment” were to blame, he said.

The reversal is a sign of more carnage to come for the fintech world.

Many fintech companies — particularly those dealing directly with retail borrowers — will be forced to shut down or sell themselves next year as startups run out of funding, according to investors, founders and investment bankers. Others will accept funding at steep valuation haircuts or onerous terms, which extends the runway but comes with its own risks, they said.

Top-tier startups that have three to four years of funding can ride out the storm, according to Point72 Ventures partner Pete Casella. Other private companies with a reasonable path to profitability will typically get funding from existing investors. The rest will begin to run out of money in 2023, he said.

“What ultimately happens is you get into a death spiral,” Casella said. “You can’t get funded and all your best employees start jumping ship because their equity is underwater.”

Thousands of startups were created after the 2008 financial crisis as investors plowed billions of dollars into private companies, encouraging founders to attempt to disrupt an entrenched and unpopular industry. In a low interest rate environment, investors sought yield beyond public companies, and traditional venture capitalists began competing with new arrivals from hedge funds, sovereign wealth and family offices.

The movement shifted into overdrive during the Covid pandemic as years of digital adoption happened in months and central banks flooded the world with money, making companies like Robinhood, Chime and Stripe familiar names with huge valuations. The frenzy peaked in 2021, when fintech companies raised more than $130 billion and minted more than 100 new unicorns, or companies with at least $1 billion in valuation.

“20% of all VC dollars went into fintech in 2021,” said Stuart Sopp, founder and CEO of digital bank Current. “You just can’t put that much capital behind something in such a short time without crazy stuff happening.”

The flood of money led to copycat companies getting funded anytime a successful niche was identified, from app-based checking accounts known as neobanks to buy now, pay later entrants. Companies relied on shaky metrics like user growth to raise money at eye-watering valuations, and investors who hesitated on a startup’s round risked missing out as companies doubled and tripled in value within months.

The thinking: Reel users in with a marketing blitz and then figure out how to make money from them later.

“We overfunded fintech, no question,” said one founder-turned-VC who declined to be identified speaking candidly. “We don’t need 150 different neobanks, we don’t need 10 different banking-as-a-service providers. And I’ve invested in both” categories, he said.

The first cracks began to appear in September 2021, when the shares of PayPal, Block and other public fintechs began a long decline. At their peak, the two companies were worth more than the vast majority of financial incumbents. PayPal’s market capitalization was second only to that of JPMorgan Chase. The specter of higher interest rates and the end of a decade-plus-long era of cheap money was enough to deflate their stocks.

Many private companies created in recent years, especially those lending money to consumers and small businesses, had one central assumption: low interest rates forever, according to TSVC partner Spencer Greene. That assumption met the Federal Reserve’s most aggressive rate-hiking cycle in decades this year.

“Most fintechs have been losing money for their entire existence, but with the promise of ‘We’re going to pull it off and become profitable,’” Greene said. “That’s the standard startup model; it was true for Tesla and Amazon. But many of them will never be profitable because they were based on faulty assumptions.”

Even companies that previously raised large amounts of money are struggling now if they are deemed unlikely to become profitable, said Greene.

“We saw a company that raised $20 million that couldn’t even get a $300,000 bridge loan because their investors told them `We are no longer investing a dime.’” Greene said. “It was unbelievable.”

All along the private company life cycle, from embryonic startups to pre-IPO companies, the market has reset lower by at least 30% to 50%, according to investors. That follows the decline in public company shares and a few notable private examples, like the 85% discount that Swedish fintech lender Klarna took in a July fundraising.

Now, as the investment community exhibits a newfound discipline and “tourist” investors are flushed out, the emphasis is on companies that can demonstrate a clear path toward profitability. That is in addition to the previous requirements of high growth in a large addressable market and software-like gross margins, according to veteran fintech investment banker Tommaso Zanobini of Moelis.

“The real test is, does the company have a trajectory where their cash flow needs are shrinking that gets you there in six or nine months?” Zanobini said. “It’s not, trust me, we’ll be there in a year.”

As a result, startups are laying off workers and pulling back on marketing to extend their runway. Many founders are holding out hope that the funding environment improves next year, although that is looking increasingly unlikely.

As the economy slows further into an expected recession, companies that lend to consumers and small businesses will suffer significantly higher losses for the first time. Even profitable legacy players like Goldman Sachs couldn’t stomach the losses required to create a scaled digital player, pulling back on its fintech ambitions.

“If loss ratios are increasing in a rate increasing environment on the industry side, it’s really dangerous because your economics on loans can get really out of whack,” said Justin Overdorff of Lightspeed Venture Partners.

Now, investors and founders are playing a game of trying to determine who will survive the coming downturn. Direct-to-consumer fintechs are generally in the weakest position, several venture investors said.

“There’s a high correlation between companies that had bad unit economics and consumer businesses that got very large and very famous,” said Point72’s Casella.

Many of the country’s neobanks “are just not going to survive,” said Pegah Ebrahimi, managing partner of FPV Ventures and a former Morgan Stanley executive. “Everyone thought of them as new banks that would have tech multiples, but they are still banks at the end of the day.”

Beyond neobanks, most companies that raised money in 2020 and 2021 at nosebleed valuations of 20 to 50 times revenue are in a predicament, according to Oded Zehavi, CEO of Mesh Payments. Even if a company like that doubles revenue from its last round, it will likely have to raise fresh funds at a deep discount, which can be “devastating” for a startup, he said.

“The boom led to some really surreal investments with valuations that cannot be justified, maybe ever,” Zehavi said. “All of these companies across the world are going to struggle, and they will need to be acquired or shut down in 2023.”

As in previous down cycles, however, there is opportunity. Stronger players will snap up weaker ones through acquisition and emerge from the downturn in a stronger position, where they will enjoy less competition and lower costs for talent and expenses, including marketing.

“The competitive landscape shifts the most during periods of fear, uncertainty and doubt,” said Kelly Rodriques, CEO of Forge, a trading venue for private company stock. “This is when the bold and the well capitalized will gain.”

While sellers of private shares have generally been willing to accept bigger valuation discounts as the year went on, the bid-ask spread is still too wide, with many buyers holding out for lower prices, Rodriques said. The logjam could break next year as sellers become more realistic about pricing, he said.

Bill Harris, co-founder and CEO of Personal Capital

Source: Personal Capital.

Eventually, incumbents and well-financed startups will benefit, either by purchasing fintechs outright to accelerate their own development, or picking off their talent as startup workers return to banks and asset managers.

Though he didn’t let on during an October interview that Nirvana Money would soon be among those to shutter, Harris agreed that the cycle was turning on fintech companies.

But Harris — founder of nine fintech companies and PayPal’s first CEO — insisted that the best startups would survive and ultimately thrive. The opportunities to disrupt traditional players are too large to ignore, he said.

“Through good times and bad, great products win,” Harris said. “The best of the existing solutions will come out stronger and new products that are fundamentally better will win as well.”

Charles Scharf, chief executive officer of Wells Fargo & Co., listens during a House Financial Services Committee hearing in Washington, D.C., U.S., on Tuesday, March 10, 2020.

Andrew Harrer | Bloomberg | Getty Images

Wells Fargo agreed to a $3.7 billion settlement with the Consumer Financial Protection Bureau over customer abuses tied to bank accounts, mortgages and auto loans, the regulator said Tuesday.

The bank was ordered to pay a $1.7 billion civil penalty and “more than $2 billion in redress to consumers,” the CFPB said in a statement. In a separate statement, the San Francisco-based company said that many of the “required actions” tied to the settlement were already done.

related investing news

“The bank’s illegal conduct led to billions of dollars in financial harm to its customers and, for thousands of customers, the loss of their vehicles and homes,” the agency said in its release. “Consumers were illegally assessed fees and interest charges on auto and mortgage loans, had their cars wrongly repossessed, and had payments to auto and mortgage loans misapplied by the bank.”

The resolution lifts one overhang for the bank, which has been led by CEO Charlie Scharf since October 2019. In October, the bank set aside $2 billion for legal, regulatory and customer remediation matters, igniting speculation that a settlement was nearing.

But other regulatory hurdles remain: Wells Fargo is still operating under consent orders tied to its 2016 fake accounts scandal, including one from the Fed that caps its asset growth.

Furthermore, the bank said that fourth-quarter expenses would include a $3.5 billion operating loss, or $2.8 billion after taxes, from the incremental costs of the CFPB civil penalty and customer remediation efforts, as well as other legal matters. The bank is still expected to post an overall profit when it reports results in mid January, according to a person with knowledge of the matter.

Shares of the bank rose 1.2% in early trading.

“This far-reaching agreement is an important milestone in our work to transform the operating practices at Wells Fargo and to put these issues behind us,” Scharf said in his statement. “We and our regulators have identified a series of unacceptable practices that we have been working systematically to change and provide customer remediation where warranted.”

CFPB Director Rohit Chopra said Wells Fargo’s “rinse-repeat cycle of violating the law” hurt millions of American families and that the settlement was an “important initial step for accountability” for the bank.

This story is developing. Please check back for updates.