David Solomon, CEO, Goldman Sachs, speaks during the Milken Institute Global Conference in Beverly Hills, California, April 29, 2019.

Kyle Grillot | Bloomberg | Getty Images

Goldman Sachs is preparing for its third round of layoffs since September as Wall Street firms adjust to a slump in deals activity.

The company is expected to trim fewer than 250 jobs in the coming weeks, a person with knowledge of the New York-based bank’s plans said Tuesday.

Goldman Sachs, led by CEO David Solomon, was among the first major Wall Street firms to trim jobs in September, cutting a few hundred positions. It then slashed more jobs in January, releasing about 3,200 employees. Morgan Stanley announced about 3,000 job cuts this month, and JPMorgan Chase cut about 500 jobs, CNBC reported last week.

But Goldman is more tied to the ups and downs of Wall Street than its rivals. Its combined 16% drop in first-quarter trading and advisory revenue contributed to a disappointing start to the year.

Managing directors and some partners will be affected by the Goldman cuts, according to the person, who declined to be identified speaking about layoffs. The Wall Street Journal reported the news earlier Tuesday.

Goldman had 45,400 employees as of March 31, a 6% decline from the fourth quarter of 2022.

Clarification: This story was updated to reflect that JPMorgan Chase had cut about 500 jobs last week.

JPMorgan Chase & Co. headquarters in New York, US, on Wednesday, Jan. 18, 2023.

Gabby Jones | Bloomberg | Getty Images

JPMorgan Chase cut about 500 positions this week, mostly among technology and operations groups, according to people with knowledge of the move.

The cuts were spread across the New York-based firm’s main divisions of retail and commercial banking, asset and wealth management and its corporate and investment bank, said the people, who declined to be identified speaking about personnel matters.

Like many financial firms, JPMorgan periodically trims staff during the year, even as it hires thousands more workers to fill roles. The bank has about 13,000 open positions, said one of the people.

Under CEO Jamie Dimon, JPMorgan has been in growth mode as of late, most recently by acquiring failed regional bank First Republic in a government-brokered deal. This week, JPMorgan offered positions to about 85% of First Republic’s roughly 7,000 workers.

JPMorgan had 296,877 employees as of March 31, 8% higher than a year earlier.

The bank declined to comment about its personnel decisions.

Jamie Dimon, chief executive officer of JPMorgan Chase, is planning his first visit to mainland China in four years as the American bank prepares to host three conferences in Shanghai at the end of May.

Giulia Marchi | Bloomberg | Getty Images

JPMorgan Chase is developing a ChatGPT-like software service that leans on a disruptive form of artificial intelligence to select investments for customers, CNBC has learned.

The company applied to trademark a product called IndexGPT this month, according to a filing from the New York-based bank.

IndexGPT will tap “cloud computing software using artificial intelligence” for “analyzing and selecting securities tailored to customer needs,” according to the filing.

The viral success of OpenAI’s ChatGPT technology last year has forced entire industries to grapple with the arrival of artificial intelligence. ChatGPT, which uses massive language models to create human-sounding responses to questions, has ignited an arms race among tech giants and chipmakers over what is seen as the next foundational innovation.

The technology has a range of possible uses in finance. Banks including Goldman Sachs and Morgan Stanley have already begun testing it for internal use. That includes ways to help Goldman engineers create code or answer Morgan Stanley financial advisors‘ queries.

But JPMorgan may be the first financial incumbent aiming to release a GPT-like product directly to its customers, according to Washington D.C.-based trademark attorney Josh Gerben.

“This is a real indication they might have a potential product to launch in the near future,” Gerben said.

“Companies like JPMorgan don’t just file trademarks for the fun of it,” he said. The filing includes “a sworn statement from a corporate officer essentially saying, ‘Yes, we plan on using this trademark.’”

JPMorgan must launch IndexGPT within about three years of approval to secure the trademark, according to the lawyer. Trademarks typically take nearly a year to be approved, thanks to backlogs at the U.S. Patent and Trademark Office, he said.

The applications are typically vaguely written to give companies the broadest possible protections, Gerben said.

But JPMorgan’s filing does specify that IndexGPT uses the same flavor of A.I. popularized by ChatGPT; the bank plans to use A.I. powered by “Generative Pre-trained Transformer (GPT) models.”

“It’s an A.I. program to select financial securities,” Gerben said. “This sounds to me like they’re trying to put my financial advisor out of business.”

Financial advisors have long feared the arrival of technology good enough to displace their role in markets. Those fears have largely yet to materialize.

Wealth management firms, including Morgan Stanley and Bank of America’s Merrill, offer simple roboadvisor services, but that hasn’t stopped their human advisors from gathering billions of dollars more in assets.

Earlier this week, executives at JPMorgan touted their progress in applying A.I. across operations at the company’s annual investor conference.

The bank, which employs 1,500 data scientists and machine-learning engineers, is testing “a number of use cases” for GPT technology, said global tech chief Lori Beer.

“We couldn’t discuss A.I. without mentioning GPT and large language models,” Beer said. “We’ve recognized the power and opportunity of these tools and are committed to exploring all the ways they can deliver value for the firm.”

Rick Rieder, BlackRock’s Chief Investment Officer of Global Fixed Income, speaks during a Reuters investment summit in New York, November 7, 2019.

Lucas Jackson | Reuters

NEW YORK – When the bond chief of the world’s biggest asset manager looks at the U.S. right now, he sees a lot to like.

A combination of resilient government, corporate and consumer spending, improving homebuilder data, $1.5 trillion in excess savings and low unemployment tell BlackRock’s Rick Rieder that the American economy is faring better than many expected.

“I think the U.S. economy’s in much better shape than people give credit” for, Rieder said Tuesday at an event at BlackRock’s New York headquarters.

“There’s this thesis that you will have a dramatic slowdown,” he said. “When you break down the numbers, it’s just not apparent.”

Talk of an impending recession has been building as the impact of the Federal Reserve’s interest rate increases ripple through the economy. The collapse of three midsized banks this year have stoked concerns that lenders will rein in access to credit, further slowing down the economy. Still, employment figures have confounded expectations, most recently for April, when nonfarm payrolls jumped by 253,000.

“When people talk about, ‘We’re going to a recession or a deep recession,’ it’s pretty unusual [or] almost impossible when you have an unemployment rate of 3.4%,” Rieder said.

Rieder, a three-decade veteran of the markets who oversees $2.4 trillion in assets, said he expects the Fed to pause rate increases at its next meeting. While the central bank could raise rates once more after that, he said that its rate-hiking campaign is largely done.

That expectation, combined with slowing inflation, gives investors a good backdrop, even if he does expect the economy to slow later this year, Rieder said.

The biggest threat to Rieder’s thesis is a potential U.S. default on its sovereign debt, which could usher in panic and be “potentially catastrophic” for the economy, according to experts including JPMorgan Chase CEO Jamie Dimon. Treasury Secretary Janet Yellen has said that the U.S. could lose the ability to pay its bills as soon as June 1.

Rieder puts a “very high probability” of the Biden administration striking a deal with Republican lawmakers, he said.

“I’ve never seen so much money sitting in cash, and a lot of it” waiting for a debt ceiling resolution before being deployed, he said.

James Gorman said Friday he plans to resign as Morgan Stanley‘s CEO within the year, setting off a succession race atop one of Wall Street’s dominant firms.

The bank’s board has narrowed its CEO search to three “very strong” internal candidates, Gorman told shareholders at the New York-based firm’s annual meeting.

related investing news

Gorman, 64, will take on the executive chairman role “for a period of time” after stepping down as CEO, he said.

“The specific timing of the CEO transition has not been determined, but it is the board’s and my expectation that it will occur at some point in the next 12 months,” Gorman said.

“That is the current expectation in the absence of a major change in the external environment,” he added.

Since taking over in 2010, Gorman has pulled off one of the more successful transformations on Wall Street. Through a series of savvy acquisitions, Morgan Stanley rebounded after nearly capsizing during the 2008 financial crisis to become a wealth management juggernaut.

The bank began that journey in 2009, when Morgan Stanley purchased Smith Barney from Citigroup in the throes of the financial crisis, gaining thousands of financial advisors. It then spent more than $20 billion to acquire discount brokerage E-Trade and investment manager Eaton Vance in 2020, adding scale and heft to the bank’s nontrading operations.

As a result, Morgan Stanley has become an asset-gathering machine: Gorman has said his bank can add roughly $1 trillion in assets every three years, eventually getting to $10 trillion.

“It is hard to argue that James Gorman has not been one of the elite CEOs in the financial services industry, taking over the company coming out of the” 2008 financial crisis and sharply improving its returns, KBW analyst David Konrad said in a research note.

The firm’s investors have rewarded it with one of the top valuations among big bank peers. That’s because shareholders favor the steadier revenue streams generated by wealth and asset management over the more volatile fees from trading and advisory businesses.

Shares of Morgan Stanley have tripled during Gorman’s tenure.

Morgan Stanley shares during CEO James Gorman’s tenure.

Morgan Stanley’s internal CEO candidates are the men leading the bank’s three main businesses, according to people with knowledge of the situation.

Ted Pick and Andy Saperstein, who run the bank’s capital markets and wealth management divisions respectively, have also been co-presidents since 2021. Dan Simkowitz runs the bank’s smallest division, investment management, and was named co-head of strategy in 2021.

The announcement makes official Gorman’s desire to hand over the reins to another executive. Gorman has said publicly for the past few years that he didn’t plan on staying much longer as CEO, and on Friday he joked that he wouldn’t die while holding the title.

Gorman has “no plans to go out like Logan Roy,” the fictional CEO from HBO’s “Succession” series, he told investors.

Goldman Sachs, known more for its Wall Street bankers than its technology, has just spun out the first startup from its internal incubator.

The company, a networking platform for employees called Louisa, was funded and owned by the New York-based investment bank until a few weeks ago, when it became independent, according to founder-CEO Rohan Doctor.

Now Doctor is hustling to grow his client base beyond the confines of Goldman, whose employees have used Louisa for the past two and a half years. The software automatically creates user profiles from an employer’s databases and pulls in newsfeeds to proactively connect people who might benefit from knowing each other, he said.

“Think of Louisa as an A.I.-powered LinkedIn on steroids,” Doctor, 42, said this week in an interview. “We have smart profiles and a smart network, and Louisa reads millions of articles a week from 250 providers and begins connecting people” based on possible deals gleaned from news, he said.

Under CEO David Solomon, Goldman has sought to speed up its digital makeover by hiringGoogle and Amazonexecutives and asking employees to pitch leaders on startup ideas. Louisa was part of the inaugural class of Goldman’s incubator program, which encourages employees with startup ideas to develop them in-house.

Doctor, a 17-year Goldman veteran who had stints in Hong Kong and London as head of bank solutions, got the idea for Louisa after landing a massive deal in 2018.

The elation of securing the transaction, a complex risk transfer between a bank and an insurer worth tens of millions of dollars, was followed by nagging questions: How did Doctor pull it off, and was it repeatable?

“The real answer was serendipity, happenstance,” he said. “It was dumb luck that me and another guy got thirsty at the same time, go to a [bar] in London and start exchanging information.”

Rohan Doctor, CEO and founder of Louisa

Source: Goldman Sachs

There has to be a better way, thought Doctor. Professional services firms like Goldman rely on the expertise and contacts of their employees, but there’s a limit to how many colleagues anyone can know.

“This is costing companies billions of dollars in terms of missed opportunities, disconnected colleagues and fractured client experiences,” he said.

So he moved to New York from Hong Kong and began hiring programmers for his nascent effort.

The company’s name originally referred to Louisa Goldman Sachs, the youngest daughter of Marcus Goldman and wife of Samuel Sachs. But, seeing as how Doctor has to cater to competitors of Goldman, the startup’s name now refers more generally to a “renowned warrior,” he said.

Louisa has more than 20,000 monthly active users, according to Goldman, which declined to say how much it spent launching the company.

Doctor has begun signing up clients besides Goldman, including a commercial bank and a venture capital fund with nearly $100 billion in assets, he said. They will focus initially on a small subset of five or six professional services clients before broadening their efforts, he said.

He believes two factors make his startup especially timely.

The arrival of generative A.I. technology like OpenAI’s ChatGPT has created excitement in an otherwise subdued environment for technology firms, he said.

“What OpenAI has done is just phenomenal,” he said. “We can use it to sort of map out what’s in people’s minds and how they want to describe themselves in seconds.”

Further, remote and hybrid work has disrupted the way employees interact, creating the need for a networking platform like Louisa, Doctor said.

“The way it used to be done if you had a question, you’d lean back on a crowded trading floor and ask around,” he said. “Hybrid is here to stay, even at places that don’t want it, and asking around no longer works.”

JPMorgan Chase and Company President and CEO Jamie Dimon testifies before a Senate Banking, Housing, and Urban Affairs hearing on “Annual Oversight of the Nation’s Largest Banks”, on Capitol Hill in Washington, U.S., September 22, 2022.

Elizabeth Frantz | Reuters

JPMorgan Chase CEO Jamie Dimon said Thursday that markets will be gripped by panic as the U.S. approaches a possible default on its sovereign debt.

An actual default would be “potentially catastrophic” for the country, Dimon told Bloomberg in a televised interview. Dimon said he expects that worst-case scenario will be avoided, however, because lawmakers will be forced to respond to growing concern.

related investing news

“The closer you get to it, you will have panic” in the form of stock market volatility and upheaval in Treasurys, he said.

Dimon joined a host of business figures and administration officials making dire predictions about the consequences of failing to raise or suspend the U.S. debt limit and allowing the world’s largest economy to default on its bonds. Treasury Secretary Janet Yellen has said the idea that the country could default should be “unthinkable” and would lead to economic disaster.

“If it gets to that panic point, people have to react, we’ve seen that before,” Dimon said.

But “it’s a really bad idea, because panic becomes something that is not good,” he added. “It could affect other markets around the world.”

JPMorgan, the biggest U.S. bank with about $3.7 trillion in assets, has been preparing for the risk of an American default, Dimon said.

Such an event would ripple through the financial world, impacting “contracts, collateral, clearing houses, and affect clients definitely around the world,” he said.

The bank’s so-called war room has been gathering once weekly, a rate that will shift to daily meetings around May 21 and then three meetings daily after that, he said.

He exhorted politicians from both major U.S. parties to compromise and avoid a ruinous outcome.

In the wide-ranging interview, Dimon said he speaks daily to regional bank executives amid concerns sparked by the Silicon Valley Bank collapse in March. Last week, JPMorgan emerged as the winner in the government-brokered auction for First Republic.

Regional banks are “quite strong” and will have good financial results, but managers are worried because of the bank runs that have taken down three firms, he said.

“I think we have to assume there’ll be a little bit more” to the regional banking crisis, he said.

Berkshire Hathaway CEO Warren Buffett on Saturday assailed regulators, politicians and the media for confusing the public about the safety of U.S. banks and said that conditions could worsen from here.

Buffett, when asked about the recent tumult that led to the collapse of three mid-sized institutions since March, launched into a lengthy diatribe about the matter.

related investing news

“The situation in banking is very similar to what it’s always been in banking, which is that fear is contagious,” Buffett said. “Historically, sometimes the fear was justified, sometimes it wasn’t.”

Berkshire Hathaway has owned banks from early on in Buffett’s nearly six-decade history at the company, and he’s stepped up to inject confidence and capital into the industry on several occasions. In the early 1990s, Buffett served as CEO of Salomon Brothers, helping rehabilitate the Wall Street firm’s tattered reputation. More recently, he injected $5 billion into Goldman Sachs in 2008 and another $5 billion in Bank of America in 2011, helping stabilize both of those firms.

He remains ready, with his company’s formidable cash pile, to act again if the situation calls for it, Buffett said during his annual shareholders’ meeting.

“We want to be there if the banking system temporarily gets stalled in some way,” he said. “It shouldn’t, I don’t think it will, but it could.”

The core problem, as Buffett sees it, is that the public doesn’t understand that their bank deposits are safe, even those that are uninsured. The Berkshire CEO has said regulators and Congress would never allow depositors to lose a single dollar in a U.S. bank, even if they haven’t made that guarantee explicit.

The fear of regular Americans that they could lose their savings, combined with the ease of mobile banking, could lead to more bank runs. Meanwhile, Buffett said that he keeps his personal funds at a local institution, and isn’t worried despite exceeding the threshold for FDIC coverage.

“The messaging has been very poor, it’s been poor by the politicians who sometimes have an interest in having it poor,” he said. “It’s been poor by the agencies, and it’s been poor by the press.”

Buffett also turned his ire on bank executives who took undue risks, saying that there should be “punishment” for bad behavior. Some bank executives may have sold company stock because they knew trouble was brewing, he added.

For example, First Republic, which was seized and sold to JPMorgan Chase after a deposit run, sold its customers jumbo mortgages at low rates, which was a “crazy proposition,” he said.

“If you run a bank and screw it up, and you’re still a rich guy… and the world goes on, that’s not a good lesson to teach people,” he said.

Berkshire has been unloading bank shares, including that of JPMorgan Chase and Wells Fargo, since around the start of the 2020 pandemic.

Recent events have only “reconfirmed my belief that the American public doesn’t understand their banking system,” Buffett said.

He reiterated several times that he had no idea how the current situation will unfold.

“That’s the world we live in,” Buffett said. “It means that a lighted match can turn into a conflagration, or be blown out.”

Shareholders watch Warren Buffett and Charlie Munger from the overflow room during the Berkshire Hathaway annual meeting on Saturday, May 6, 2023, in Omaha, Neb.

Berkshire Hathaway CEO Warren Buffett said Saturday that regulators avoided a financial disaster by making sure that Silicon Valley Bank customers didn’t lose money in the firm’s collapse.

The sudden downfall of SVB in March forced the Federal Deposit Insurance Corp. to seize the bank, selling some of its assets to First Citizens weeks later.

The FDIC protected SVB customers in the process by invoking the systemic risk exception during the March tumult, allowing the regulator to make all depositors whole, even if their accounts exceeded the $250,000 coverage threshold.

“It would’ve been catastrophic” if regulators hadn’t done that, Buffet said during his annual shareholder meeting.

Allowing uninsured depositors to lose money would’ve “started a run on every bank in the country,” he said.

So the move, which brought criticism because it protected venture capital investors, startups and other sophisticated players, was “inevitable” in Buffett’s view.

Protecting uninsured depositors contributed to the estimated $20 billion hit that the FDIC’s Deposit Insurance Fund took in the SVB receivership. The biggest U.S. banks are expected to cover the economic cost of that through special fees.

This story is developing. Please check back for updates.

As Wall Street’s slump in IPOs and mergers deepens this year, top advisory firms including Morgan Stanley, Bank of America and Citigroup have turned to job cuts in recent weeks.

Morgan Stanley plans to eliminate roughly 3,000 positions by the end of June, according to a person with knowledge of the plans.

related investing news

That equates to roughly 5% of the New York-based bank’s workforce when excluding the financial advisors and support staff who will be spared in the cuts, the person said. The layoffs are expected to impact banking and trading staff the most, according to Bloomberg, which reported the moves earlier.

A historic boom in deals ignited by the pandemic was followed by a bust that began last year after the Federal Reserve started raising rates to hit the brakes on an overheating economy. The IPOs, debt issuance and mergers that feed Wall Street have all remain muted this year. For instance, IPO volumes are 74% lower than last year, according to Dealogic data.

For Morgan Stanley, the cuts show that Wall Street is wrangling with expenses as the slump drags on for longer than expected. The bank already cut about 2% of its workforce in December, CNBC reported.

Last month, analysts criticized Morgan Stanley for posting higher first-quarter costs while revenue declined. Expenses in the firm’s investment bank and wealth management division hurt profit margins in particular.

The bank’s moves aren’t isolated. The industry’s job cuts began in September, when Goldman Sachs reinstated a practice of culling those it perceives to be low performers. Nearly all the major Wall Street firms followed, and Goldman itself had to resort to another, deeper round of layoffs in January.

In recent weeks, big bank peers including Citigroup and Bank of America have cut a few hundred jobs each, relatively surgical cuts that should position the banks well when a rebound in deals finally arrives.

Last week, top boutique advisor Lazard said it planned to cut 10% of its workforce this year. The step was necessitated by restrained capital markets activity and wage inflation that pumped up salaries across banking.

“Candidly, things are not feeling as good as they were in December or January,” Chief Executive Ken Jacobs told Bloomberg.

Jamie Dimon, chairman and chief executive officer of JPMorgan Chase & Co., during a Bloomberg Television interview at the JPMorgan Global High Yield and Leveraged Finance Conference in Miami, Florida, US, on Monday, March 6, 2023.

Marco Bello | Bloomberg | Getty Images

The crisis that led to the downfall of three regional U.S. banks in recent weeks is largely over after the resolution of First Republic, according to JPMorgan Chase CEO Jamie Dimon.

JPMorgan emerged as the winner of a weekend auction for First Republic after regulators decided that time had run out on a private sector solution. The Federal Deposit Insurance Corporation seized the bank and New York-based JPMorgan announced early Monday that it was acquiring nearly all of the deposits and most of the assets of First Republic.

“There are only so many banks that were offsides this way,” Dimon told analysts in a call shortly after the deal was announced.

“There may be another smaller one, but this pretty much resolves them all,” Dimon said. “This part of the crisis is over.”

In the wake of the sudden collapse in March of Silicon Valley Bank and Signature Bank, investors have punished other lenders that had similar characteristics to SVB. Companies with the highest percentage of uninsured deposits and losses on their balance sheet were most scrutinized.

The March turmoil exposed poor management by some midsized banks that essentially bet that interest rates wouldn’t rise; when rates did rise, the banks were caught “offsides” with unrealized losses from bonds on their balance sheet.

But the $30 billion injection of deposits into First Republic last month bought time for the industry, allowing mid-sized banks to report first-quarter results in recent weeks that in many cases showed a stabilization of deposits. That eased investors’ fears that many more lenders would soon topple.

Down the road, investors are still exposed to risks created by the Federal Reserve’s interest rate hikes and their impact on assets including real estate, Dimon added.

A view of the First Republic Bank logo at the Park Avenue location, in New York City, March 10, 2023.

David Dee Delgado | Reuters

The Californian financial regulator has taken possession of First Republic, resulting in the third failure of an American bank since March, after a last-ditch effort to persuade rival lenders to keep the ailing bank afloat failed.

JPMorgan Chase Bank will assume all deposits, including uninsured deposits, and “substantially all assets” of the bank, according to a release early Monday.

The California Department of Financial Protection and Innovation said it had taken possession of the bank and appointed the Federal Deposit Insurance Corporation receiver of the bank. The FDIC accepted JPMorgan’s bid for the bank’s assets.

Since the sudden collapse of Silicon Valley Bank in March, attention has focused on First Republic as the weakest link in the U.S. banking system. Like SVB, which catered to the tech startup community, First Republic was also a California-based specialty lender of sorts. It focused on serving rich coastal Americans, enticing them with low-rate mortgages in exchange for leaving cash at the bank.

But that model unraveled in the wake of the SVB collapse, as First Republic clients withdrew more than $100 billion in deposits, the bank revealed in its earnings report April 24. Institutions with a high proportion of uninsured deposits like SVB and First Republic found themselves vulnerable because clients feared losing savings in a bank run.

Shares of First Republic are down 97% so far this year as of Friday’s close.

That deposit drain forced First Republic to borrow heavily from Federal Reserve facilities to maintain operations, which pressured the company’s margins because its cost of funding is far higher now. First Republic accounted for 72% of all borrowing from the Fed’s discount window recently, according to BCA Research chief strategist Doug Peta.

On April 24, First Republic CEO Michael Roffler sought to portray an image of stability after the events of March. Deposit outflows have slowed in recent weeks, he said. But the stock tanked after the company disavowed its previous financial guidance and Roffler opted not to take questions after an unusually brief conference call.

The bank’s advisors had hoped to persuade the biggest U.S. banks to help First Republic once again. One version of the plan circulated recently involved asking banks to pay above-market rates for bonds on First Republic’s balance sheet, which would enable it to raise capital from other sources.

But ultimately the banks, which had banded together in March to inject $30 billion of deposits into First Republic, couldn’t agree on the rescue plan and regulators took action, ending the bank’s 38-year run.

This story is developing. Please check back for updates.

A First Republic bank branch in Manhattan on April 24, 2023 in New York City.

Spencer Platt | Getty Images

U.S. regulators have asked banks for their best and final takeover offers for First Republic by Sunday afternoon, in a move that authorities hope will calm markets and cap a period of uncertainty for regional lenders.

JPMorgan Chase and PNC are likely bidders for the ailing lender, which would be seized in receivership and immediately sold to the winning bank, according to people with knowledge of the situation. The Wall Street Journal reported those banks’ interest late Friday.

Other companies are likely to step up. Bank of America is among several other institutions that are weighing a potential bid for First Republic, according to people with knowledge of the matter.

This is breaking news. Please check back for updates.

The best hope for avoiding a collapse of ailing lender First Republic hinges on how persuasive one group of bankers can be with another group of bankers.

Advisors to First Republic will attempt to cajole the big U.S. banks who’ve already propped it up into doing one more favor, CNBC has learned.

The pitch will go something like this, according to bankers with knowledge of the situation: Purchase bonds from First Republic at above-market rates for a total loss of a few billion dollars – or face roughly $30 billion in FDIC fees when First Republic fails.

It’s the latest twist in a weekslong saga sparked by the sudden collapse of Silicon Valley Bank last month. Days after the government seized SVB and Signature, mid-sized banks hit by severe deposit runs, the country’s biggest banks banded together to inject $30 billion in deposits into First Republic. That solution proved fleeting after the depth of the company’s problems became known.

If the First Republic advisors manage to convince big banks to purchase bonds for more than they are worth — to take the hit of investment losses for the good of the banking system, as well as their own welfare — then they are confident that other parties will step up to help the bank recapitalize itself.

The advisors have already lined up potential purchasers of new First Republic stock in that scenario, according to the sources.

These investment bankers are now seeking to create a sense of urgency. CNBC’s David Faber, who first reported on the latest rescue plan Tuesday, said that the coming days are crucial for First Republic.

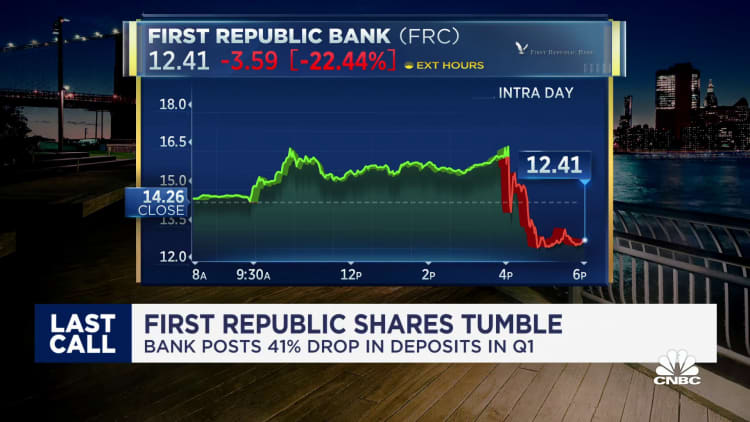

The bank’s stock has been in freefall since disclosing Monday that its deposits fell a staggering 40.8% recently, leaving it with $104.5 billion in deposits, including the infusion from big banks. Analysts covering the company published pessimistic reports after CEO Michael Roffler opted not to take any questions after a brief 12-minute conference call.

“Now that the earnings are out, once you’ve got a window to act, it’s time to do it,” said one of the bankers, who asked for anonymity to speak candidly. “You never know what will happen if you wait, and you don’t want to be dealing with an emergency situation.”

For years, First Republic was the envy of peers as its focus on rich Americans helped turbocharge growth and allowed it to poach talent. But that model broke down in the aftermath of the SVB failure as its wealthy customers quickly pulled uninsured deposits.

Lazard and JPMorgan Chase were hired last month to advise First Republic, according to media reports.

The key advantage of the advisors’ plan, they say, is that it allows First Republic to offload some, but not all of its underwater bonds. In a government receivership, the whole portfolio must get marked down at once, resulting in what Morgan Stanley analysts estimated to be a $27 billion hit.

One complication, however, is that the advisors are relying on the U.S. government to summon bank CEOs together to explore possible solutions.

There have been false starts already: One top-four U.S. bank said that the government told them to be ready to act on the First Republic situation this past weekend, but nothing happened.

While the exact contour of any deal is a matter for negotiation and could include a special purpose vehicle or direct purchases, several possibilities address the bank’s ailing balance sheet.

First Republic loaded up on low-yielding assets including Treasuries, municipal bonds and mortgages, making what was essentially a bet that interest rates wouldn’t rise. When they did, the bank found itself with tens of billions of dollars in losses. The bank is weighing the sale of $50 billion to $100 billion in debt, Bloomberg reported Tuesday.

By drastically reducing the size of its balance sheet, the bank’s capital ratios will suddenly be far healthier, paving the way for it to raise more funds and continue as an independent company.

Other possible, but less-likely moves include converting the big bank’s deposits into equity, or even finding a buyer. But a suitor hasn’t emerged in the past month, and isn’t likely given that any purchaser would also own the losses on First Republic’s balance sheet.

That has led sources close to the big banks to believe that the most likely scenario for First Republic is government receivership, which is how SVB and Signature were resolved.

Those close to the banks were hesitant to endorse a plan in which they would have to recognize losses for overpaying for bonds. They also expressed distrust of government-brokered deals after some of the pacts from the 2008 financial crisis ended up being costlier than expected.

But the failures of SVB and Signature – the two biggest since the 2008 financial crisis – cost the FDIC Deposit Insurance Fund many billions of dollars, which is paid for by member banks. They also benefited the buyers who were able to cherry-pick the best assets while the FDIC retains underwater bonds, the First Republic advisors noted.

Advisors referred to the private-market solutions as the “open bank” option, while government receivership is the “closed-banked” scenario.

But there is a third possibility: the bank grinds on as is, slowly losing yet more value amid probable quarterly losses, talent flight and unceasing doubts.

“Time, by the way, is not the bank’s friend,” analyst Don Bilson wrote Tuesday. “If anything, last night’s discouraging update will make it even harder for First Republic to keep what it has.”

Morgan Stanley CEO James Gorman participates in a conversation-style interview with Economic Club of Washington in Washington September 18, 2013.

Yuri Gripas | Reuters

Morgan Stanley on Wednesday topped estimates for first quarter profit and revenue on better-than-expected trading results.

Here’s how the company did:

Earnings of $1.70 per share, vs. $1.62 Refinitiv estimate

Revenue of $14.52 billion, vs. $13.92 billion estimate.

The New York-based bank said earnings fell 19% to $2.98 billion, or $1.70 a share, from a year earlier on declines in investment banking and trading. Companywide revenue slipped 2% to $14.52 billion.

As revenues dipped, expenses at the bank climbed 4% to $10.52 billion, mostly fueled by higher-than-expected compensation costs. Expenses came in $430 million higher than the StreetAccount estimate.

Higher costs helped hurt profit margins at the bank’s wealth division and investment bank, analyst Mike Mayo of Wells Fargo said in a research note. He also said that when excluding the benefit of a low tax rate, the bank would’ve earned $1.64 per share.

Shares of the bank dropped 3.8% in premarket trading.

Under CEO James Gorman, Morgan Stanley has become a wealth management giant thanks to a string of acquisitions. The bank gets most of its revenue from wealth and investment management, steadier businesses that help to offset volatile trading and banking results.

“The investments we have made in our wealth management business continue to bear fruit as we added a robust $110 billion in net new assets this quarter,” Gorman said in the earnings release. “Equity and fixed Income revenues were strong, although investment banking activity continued to be constrained.”

Wealth management revenue climbed 11% from the year-earlier period to $6.56 billion, matching the StreetAccount estimate. The increase was fueled by a rise in net interest income amid higher rates and loan growth, which offset lower asset management revenues as markets declined.

First-quarter trading revenue dipped from a year ago as Wall Street comes down from a pandemic-era boom, but Morgan Stanley’s traders managed to top expectations by roughly $250 million.

The bank’s fixed income traders produced $2.58 billion in revenue, exceeding the $2.33 billion StreetAccount estimate. Equities trading revenue of $2.73 billion edged out the $2.65 billion estimate.

Investment banking revenue dropped 24% to $1.25 billion on fewer completed M&A deals and lower stock and debt issuance, edging out the $1.2 billion estimate.

Finally, the bank’s smallest business, investment management, saw revenues drop 3% to $1.29 billion, just below the $1.34 billion estimate, as management fees decreased amid declining markets.

At the start of a conference call with analysts, Gorman addressed the turmoil sparked by the March collapse of two American regional banks.

“In my view, we are not in a banking crisis, but we have had and may still have a crisis among some banks,” Gorman said. “I consider the condition not remotely comparable to 2008.”

He added that there was “no doubt” that Morgan Stanley would acquire more companies in wealth management, though nothing was imminent.

Morgan Stanley shares have climbed 5.7% this year before Wednesday, outperforming the 16% decline of the KBW Bank Index.

David Solomon, chief executive officer of Goldman Sachs Group Inc., during a Bloomberg Television at the Goldman Sachs Financial Services Conference in New York, US, on Tuesday, Dec. 6, 2022.

Michael Nagle | Bloomberg | Getty Images

Goldman Sachs is scheduled to report first-quarter earnings before the opening bell Tuesday.

Here’s what Wall Street expects:

Earnings: $8.10 per share, 25% lower than a year earlier, according to Refinitiv.

Revenue: $12.79 billion, 1.1% lower than a year earlier.

Trading Revenue: Fixed Income $4.16 billion, Equities $2.9 billion, per StreetAccount.

Investing Banking Revenue: $1.44 billion

How did Goldman’s traders perform last quarter?

The answer to that question will determine whether Goldman exceeds or misses expectations for the first three months of this year.

Unlike its more diversified rivals, Goldman gets the majority of its revenue from Wall Street activities including trading and investment banking. With the advisory business remaining subdued because the IPO window remains mostly shut, it’s up to traders to pick up the slack.

Heading into the quarter, analysts wondered whether turmoil during March — in which two American banks failed and a global investment bank was forced to merge with a longtime rival — would provide a good or bad backdrop to trading.

That question was seemingly answered by JPMorgan Chase and Citigroup, both of which beat estimates in part because of better-than-expected fixed income trading. Goldman has one of the biggest bond shops on Wall Street, so expectations are high.

So far this earnings season, big banks have mostly outperformed their smaller peers, helped by an influx of deposits after Silicon Valley Bank’s meltdown. But since retail banking plays a small — and probably shrinking — role at Goldman, much more focus will be on how trading and investment banking fared, and what expectations are for later this year.

Separately, analysts will want to hear what has come of CEO David Solomon’s proclamation in February that Goldman was weighing “strategic alternatives” for its consumer platforms business. That has been interpreted as potentially selling off the GreenSky business it acquired recently or offloading credit-card partnerships with Apple and others.

And they’ll likely ask for details about Goldman’s part in helping Apple offer new savings accounts; the product launched with a higher interest rate than the bank’s own Marcus product has.

Goldman shares have dipped 1.1% this year before Tuesday, a better showing than the nearly 17% decline of the KBW Bank Index.

Jamie Dimon, chief executive officer of JPMorgan Chase & Co., during a Bloomberg Television interview in London, U.K., on Wednesday, May 4, 2022.

Chris Ratcliffe | Bloomberg | Getty Images

Investors and businesses should plan for interest rates to remain higher for longer than currently expected by the market, according to JPMorgan Chase CEO Jamie Dimon.

The world saw what happened last month when higher rates and a sudden deposit run exposed bad management at Silicon Valley Bank. Earlier, rising rates and a surging dollar sparked a meltdown in U.K. sovereign debt last September, Dimon reminded analysts Friday during a conference call.

“People need to be prepared for the potential of higher rates for longer,” Dimon said on the call.

“If and when that happens, it will undress problems in the economy for those who are too exposed to floating rates, for those who are too exposed to refi risk,” he said, referring to loans that reset at market rates. “Those exposures will be in multiple parts of the economy.”

Higher rates jammed up swaths of the economy this year, from regional bankers who had bet on low rates to consumers who can no longer afford mortgages or credit card debt. The Federal Reserve has pushed its core rate higher by roughly 5 full percentage points in the past year as it sought to subdue stubbornly high inflation.

Ironically, it was the recent regional banking crisis that sparked wagers that an economic slowdown would force the Fed to pivot and cut rates later this year. That assumption has helped underpin stock levels in recent weeks on the hope for a return to a lower-rate environment.

For its part, the biggest U.S. bank by assets studies how benchmark rates closer to 6% would impact the company, Dimon said. That flies against market assumptions that the Federal Reserve will begin cutting rates in the back half of this year, reaching below 4% by January.

Dimon said he told “all” his bank’s clients to prepare for the risk of higher rates.

“Now would be the time to fix it,” he said. “Do not put yourself in a position where that risk is excessive for your company, your business, your investment pools, etc.”

Higher rates would put additional pressure on mid-sized banks like First Republic that were damaged in last month’s tumult; the value of their bond holdings moves lower as rates rise. First Republic is being advised by JPMorgan and Lazard.

While he expects regional banks to post “pretty good numbers” next week, there is the risk of “additional bank failures,” Dimon said.

Jamie Dimon, chairman and chief executive officer of JPMorgan Chase & Co., during a Bloomberg Television interview at the JPMorgan Global High Yield and Leveraged Finance Conference in Miami, Florida, US, on Monday, March 6, 2023.

Marco Bello | Bloomberg | Getty Images

JPMorgan Chase is scheduled to report first-quarter earnings before the opening bell Friday.

Here’s what Wall Street expects:

Earnings: $3.41 per share, 29.7% higher than a year earlier, according to Refinitiv.

Revenue: $36.24 billion, 14.7% higher than a year earlier.

Deposits: $2.31 trillion, according to StreetAccount.

Provision for credit losses: $2.27 billion.

Trading Revenue: Fixed income $5.29 billion, Equities $2.86 billion.

JPMorgan, the biggest U.S. bank by assets, will be watched closely for clues on how the industry fared after the collapse of two regional lenders last month.

Analysts expect a mixed bag of conflicting trends. For instance, JPMorgan likely benefited from an influx of deposits after Silicon Valley Bank and Signature Bank experienced fatal bank runs.

But the industry has been forced to pay up for deposits as customers shift holdings into higher-yielding instruments like money market funds. That will probably curb banks’ gains from rising interest rates amid the Federal Reserve’s efforts to tame inflation.

The flow of deposits through American financial institutions is the top concern of analysts and investors this quarter. That’s because smaller banks faced pressure last month as customers sought the perceived safety of megabanks including JPMorgan and Bank of America. But the bigger picture may be that deposits are leaving the regulated banking system overall as customers realize they can earn higher yields outside checking and saving accounts.

Another key question will be whether JPMorgan and others are tightening lending standards ahead of an expected U.S. recession, which could constrict economic growth this year by making it harder for consumers and businesses to borrow money.

Banks have begun setting aside more loan loss provisions on expectations for a slowing economy later this year, and that could weigh on results. JPMorgan is expected to post a $2.27 billion provision for credit losses, according to the StreetAccount estimate.

Wall Street may provide little help this quarter, with investment banking fees likely to remain subdued thanks to the still-shut IPO market. CFO Jeremy Barnum said in February that investment banking revenue was headed for a 20% decline from a year earlier, and that trading was trending “a little bit worse” as well.

Finally, analysts will want to hear what JPMorgan CEO Jamie Dimon has to say about the economy and his expectations for how the regional banking crisis will develop. JPMorgan has played a central role in propping up a client bank, First Republic, which teetered last month, in part by leading efforts to inject it with $30 billion in deposits.

Shares of JPMorgan are down about 4% this year, outperforming the 31% decline of the KBW Bank Index.

Federal Reserve Board Vice Chair for Supervision Michael S. Barr testifies at a Senate Banking, Housing and Urban Affairs Committee hearing on “Recent Bank Failures and the Federal Regulatory Response” on Capitol Hill in Washington, March 28, 2023.

Evelyn Hockstein | Reuters

The run on Silicon Valley Bank’s deposits this month went far deeper than was initially known.

Since the day regulators seized SVB, it was public knowledge that panicked customers withdrew $42 billion from the bank on March 9 on concerns that uninsured deposits were at risk.

But that pales in comparison to what would’ve gone out the next day, Michael Barr, vice chair for supervision at the Federal Reserve, testified Tuesday before the Senate Banking Committee. Regulators shuttered SVB on March 10 in the biggest bank failure since the 2008 financial crisis.

“That morning, the bank let us know that they expected the outflow to be vastly larger based on client requests,” Barr said. “A total of $100 billion was scheduled to go out the door that day.”

The combined withdrawal figure of $142 billion represents a staggering 81% of SVB’s $175 billion in deposits as of the end of last year. The dizzying pace at which money left SVB shows how quickly bank runs can happen when social media heightens panic and online banking allows for quick transactions.

Lawmakers summoned top U.S. banking regulators to Washington to explain why Silicon Valley Bank and Signature Bank collapsed earlier this month. Barr and others pointed to mismanagement by bank executives, and noted that banks with assets of more than $100 billion may need stricter rules. The former CEOs of the banks did not attend.

In fact, Fed supervisors began warning SVB management about the risk that higher interest rates posed to the bank’s balance sheet in November 2021, Barr testified. The bank “failed to address” Fed concerns in a timely way, exposing the company to its deposit run this month.

SVB’s final days as an independent bank were a roller coaster of emotions. After SVB management “spooked” investors and customers with its “belated” attempt to raise capital late Wednesday, March 8, the situation appeared to have calmed early Thursday, Barr testified.

“But later Thursday afternoon, deposit outflows started and by Thursday evening, we learned that more than $42 billion, as you indicated, had rushed out of the bank,” he said.

Fed staff worked around the clock on March 9 to save the bank, searching for enough collateral to borrow additional billions of dollars from the Fed’s discount window to honor withdrawal requests, Barr said.

The morning SVB was seized, regulators believed they may have solved the bank’s shortfall, only to run into a $100 billion wall of withdrawals.

“They were not able to actually meet their obligations to pay their depositors over the course of that day and they were shut down,” Barr said.

First Republic Bank headquarters is seen on March 16, 2023 in San Francisco, California, United States.

Tayfun Coskun | Anadolu Agency | Getty Images

The surge of deposits moving from smaller banks to big institutions including JPMorgan Chase and Wells Fargo amid fears over the stability of regional lenders has slowed to a trickle in recent days, CNBC has learned.

Uncertainty caused by the collapse of Silicon Valley Bank earlier this month triggered outflows and plunging share prices at peers including First Republic and PacWest.

The situation, which roiled markets globally and forced U.S. regulators to intervene to protect bank customers, began improving around March 16, according to people with knowledge of inflows at top institutions. That’s when 11 of the biggest American banks banded together to inject $30 billion into First Republic, essentially returning some of the deposits they’d gained recently.

“The people who panicked got out right away,” said the person. “If you haven’t made up your mind by now, you are probably staying where you are.”

The development gives regulators and bankers breathing room to address strains in the U.S. financial system that emerged after the collapse of SVB, the go-to bank for venture capital investors and their companies. Its implosion happened with dizzying speed this month, turbocharged by social media and the ease of online banking, in an event that’s likely to impact the financial world for years to come.

Within days of its March 10 seizure, another specialty lender Signature Bank was shuttered, and regulators tapped emergency powers to backstop all customers of the two banks. Ripples from this event reached around the world, and a week later Swiss regulators forced a long-rumored merger between UBS and Credit Suisse to help shore up confidence in European banks.

The dynamic has put big banks like JPMorgan and Goldman Sachs in the awkward position of playing multiple roles simultaneously in this crisis. Big banks are advising smaller ones while participating in steps to renew confidence in the system and prop up ailing lenders like First Republic, all while gaining billions of dollars in deposits and being in the position of potentially bidding on assets as they come up for sale.

The broad sweep of those money flows are apparent in Federal Reserve data released Friday, a delayed snapshot of deposits as of March 15. While large banks appeared to gain deposits at the expense of smaller ones, the filings don’t capture outflows from SVB because it was in the same big-bank category as the companies that gained its dollars.

Although inflows into one top institution have slowed to a “trickle,” the situation is fluid and could change if concerns about other banks arise, said one person, who declined to be identified speaking before the release of financial figures next month. JPMorgan will kick off bank earnings season on April 14.

At another large lender, this one based on the West Coast, inflows only slowed in recent days, according to another person with knowledge of the matter.

JPMorgan, Bank of America, Citigroup and Wells Fargo representatives declined to comment for this article.

The moves mirror what one newer player has seen as well, according to Brex co-founder Henrique Dubugras. His startup, which caters to other VC-backed growth companies, has seen a surge of new deposits and accounts after the SVB collapse.

“Things have calmed down for sure,” Dubugras told CNBC in a phone interview. “There’s been a lot of ins and outs, but people are still putting money into the big banks.”

The post-SVB playbook, he said, is for startups to keep three to six months of cash at regional banks or new entrants like Brex, while parking the rest at one of the four biggest players. That approach combines the service and features of smaller lenders with the perceived safety of too-big-to-fail banks for the bulk of their money, he said.

“A lot of founders opened an account at a Big Four bank, moved a lot of money there, and now they’re remembering why they didn’t do that in the first place,” he said. The biggest banks haven’t historically catered to risky startups, which was the domain of specialty lenders like SVB.

Dubugras said that JPMorgan, the biggest U.S. bank by assets, was the largest single gainer of deposits among lenders this month, in part because VCs have flocked to the bank. That belief has been supported by anecdotal reports.

For now, attention has turned to First Republic, which has teetered in recent weeks and whose shares have lost 90% this month. The bank is known for its success in catering to wealthy customers on the East and West coasts.

Regulators and banks have already put together a remarkable series of measures to try to save the bank, mostly as a kind of firewall against another round of panic that would swallow more lenders and strain the financial system. Behind the scenes, regulators believe the deposit situation at First Republic has stabilized, Bloomberg reported Saturday.

First Republic has hired JPMorgan and Lazard as advisors to come up with a solution, which could involve finding more capital to remain independent or a sale to a more stable bank, said people with knowledge of the matter.

If those fail, there is the risk that regulators would have to seize the bank, similar to what happened to SVB and Signature, they said. A First Republic spokesman declined comment.

While the deposit flight from smaller banks has slowed, the past few weeks have exposed a glaring weakness in how some have managed their balance sheets. These companies were caught flat-footed as the Fed engaged in its most aggressive rate hiking campaign in decades, leaving them with unrealized losses on bond holdings. Bond prices fall as interest rates rise.

It’s likely other institutions will face upheaval in the coming weeks, Citigroup CEO Jane Fraser said during an interview on Wednesday.

“There could well be some smaller institutions that have similar issues in terms of their being caught without managing balance sheets as ably as others,” Fraser said. “We certainly hope there will be fewer rather than more.”