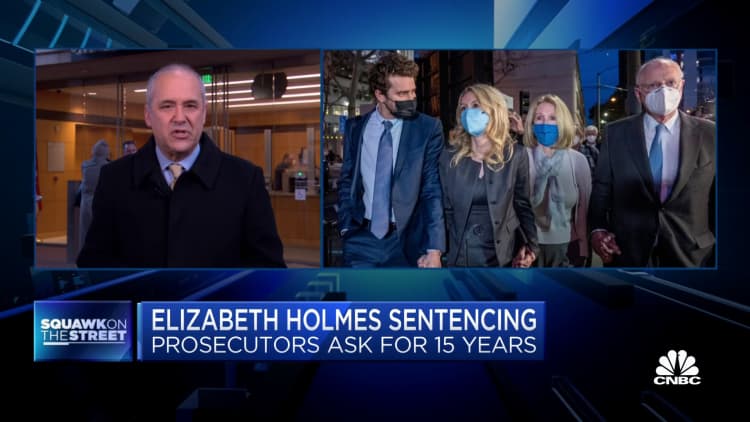

Theranos founder Elizabeth Holmes was sentenced Friday to more than 11 years in prison for fraud after deceiving investors about the purported efficacy of her company’s blood-testing technology. She was ordered to surrender on April 27.

Holmes was convicted in January in the U.S. District Court for the Northern District of California. She cried while speaking to the court ahead of her sentencing on Friday.

“I loved Theranos. It was my life’s work,” Holmes said. “My team meant the world to me. I am devastated by my failings. I’m so so sorry. I gave everything I had to build my company.”

Her defense team argued she should face a maximum sentence of 18 months, according to court filings. Instead, she was given 135 months, which amounts to 11 years and three months, behind bars.

The Wall Street Journal first broke the story of how Theranos’ blood-testing technology was struggling to meet expectations in 2015. Whistleblowers and other witnesses came forth to provide detailed accounts of how Holmes and former operating chief Ramesh “Sunny” Balwani deceived patients, partners, investors and employees about the company’s progress and the capabilities of its technology.

Once valued at $9 billion by private investors, Theranos shut down in 2018.

“Thank you for having me. Thank you for the courtesy and respect you have shown me,” she said Friday. “I have felt deep pain for what people went through because I failed them. To investors, patients, I am sorry.”

Prosecutors sought a 15 year sentence for the pregnant 38-year-old former billionaire and Silicon Valley celebrity. In July, Balwani, who was romantically involved with Holmes years earlier, was found guilty of 12 criminal fraud charges. His sentencing is set for next month.

U.S. District Court Judge Edward Davila, who presided over Holmes’ trial, handed down the sentence.

The erstwhile billionaire had attempted to move for a new trial after a former employee appeared at her doorstep in August to speak with her. Holmes’ partner, Billy Evans, told the court that the former employee made remorseful remarks at their shared residence.

But that employee, Adam Rosendorff, told the court that his remarks were due to distress at the thought of a child spending time without their mother. The Theranos founder gave birth in July to her first child, and is expecting another.

Holmes’ sentencing comes as another young tech former billionaire icon, Sam Bankman-Fried, faces a daunting future, following the sudden collapse of his cryptocurrency exchange FTX last week. Bankman-Fried hasn’t been charged with a crime, but he’s in legal jeopardy after revelations that his company was unable to give depositors their money back because some of it was used to fund risky, losing bets.

Satya Nadella, chief executive officer of Microsoft Corp., during the company’s Ignite Spotlight event in Seoul, South Korea, on Tuesday, Nov. 15, 2022. Nadella gave a keynote speech at an event hosted by the company’s Korean unit. Photographer: SeongJoon Cho/Bloomberg via Getty Images

SeongJoon Cho | Bloomberg | Getty Images

The CEO of Microsoft says he is bullish about Asia, especially China and India, as Microsoft plans to build more data centers around the world.

“Absolutely. We’re very, very bullish about what’s happening in Asia,” Satya Nadella, chairman and CEO of Microsoft, told CNBC’s Tanvir Gill in an interview Thursday, adding that Microsoft is investing in at least 11 regions.

“We’re absolutely committed to all of these countries and in China too. Today, we primarily work to support multinational companies that operate in China and multinational companies out of China.”

He also added that India has been a “massive growth market” after emerging from the pandemic.

“Microsoft’s presence in India was about mostly multinational companies operating in India. But for now, it’s completely changed,” he said.

“It’s the reverse where these companies who are innovating in India, whether it’s the big large conglomerates, or the new startups, are all using [artificial intelligence] cloud technology to be able to innovate and create services that are obviously popular in India and elsewhere,” he told CNBC.

Microsoft in October announced a round of layoffs affecting less than 1% of its employees. Meanwhile, Meta is cutting 11,000 workers, while Snap is laying off more than 1,000 people.

“The current labor markets are much more resilient,” said Nadella, adding that most companies from energy firms to banks and retailers need software engineers.

He added that no industry is immune to macroeconomic issues. “So everyone has to manage the costs and demand properly,” he said.

“One of the fascinating things about the U.S. is the amount of capital that’s getting invested,” he said, adding that new industrial infrastructure such as fabrication plants, power plants and battery factories are being built.

“I am much more focused on observing where what is happening in terms of new growth inside the United States. So I’m very, very optimistic about the U.S. and the world.”

Nadella replaced billionaire Steve Ballmer as Microsoft CEO in 2014. Prior to that, Nadella was executive vice-president of Microsoft’s cloud and enterprise group.

Microsoft shares were at $241.73 in after-hours trade. Shares have dropped 27.8% year-to-date.

— This is a developing story. Please check back for updates.

The logo of Crypto.com is seen at a stand during the Bitcoin Conference 2022 in Miami Beach, Florida, April 6, 2022.

Marco Bello | Reuters

As the crypto universe reckons with the fallout of FTX’s rapid collapse last week and tries to figure out where the contagion may head next, questions have been swirling around Crypto.com, a rival exchange that’s taken a similarly flashy approach to marketing and celebrity endorsements.

Like FTX, which filed for bankruptcy protection on Friday, Crypto.com is privately held, based outside the U.S. and offers a range of products for buying, selling, trading and storing crypto. The company is headquartered in Singapore, and CEO Kris Marszalek is based in Hong Kong.

Crypto.com is smaller than FTX but still ranks among the top 15 global exchanges, according to CoinGecko. FTX spooked the market not just by its speedy downfall but also because the company was unable to honor withdrawal requests, to the tune of billions of dollars, from users who wanted to retrieve their funds during the run on the firm. When it became clear that FTX didn’t have the liquidity necessary to give users their money, concern mounted that rivals may be next.

Twitter lit up over the weekend with speculation that Crypto.com was facing problems, and crypto experts held Twitter Spaces sessions to discuss the matter. Meanwhile, revelations landed on Sunday that, in October, Crypto.com mistakenly sent more than 80% of its ether holdings, or about $400 million worth of the cryptocurrency, to Gate.io, another crypto exchange. It was only after the transaction was exposed through public blockchain data that Marszalek acknowledged the mishap.

Kris Marszalek, CEO of Crypto.com, speaking at a 2018 Bloomberg event in Hong Kong, China.

Paul Yeung | Bloomberg | Getty Images

Changpeng Zhao, CEO of rival exchange Binance, fanned the flames of speculation, tweeting on Sunday that if an exchange has to move large amounts of crypto before or after it demonstrates the wallet addresses, “it is a clear sign of problems.” He added, “Stay away.”

Confidence is clearly shaken. Crypto.com’s native Cronos (CRO) token has dropped nearly 40% in the last week. The crumbling of FTX’s FTT token was one sign of the crisis that company faced.

“I would just get your money out of Crypto .com now,” said Adam Cochran, an investor in blockchain projects and founder of Cinneamhain Ventures, in a tweet over the weekend. “If they are full reserves they shouldn’t care if you sit on the sidelines for a week, but their handling of this hasn’t met the bar.”

Marszalek has spent the early part of the week trying to reassure users and regulators that the business is fine. On Monday, he said on YouTube that the company had a “tremendously strong balance sheet” and that it’s “business as usual” with deposits, withdrawals and trading activity. He followed up with a tweet Monday evening, indicating that “the withdrawal queue is down 98% within the last 24 hours.”

He spoke to CNBC’s “Squawk Box” on Tuesday morning, answering questions about the state of his company, the market and how he’s differently positioned than FTX. He said in the interview that the company has engaged with over 10 regulators about the “shocking events” surrounding FTX and how to keep them from happening again.

“I understand that right now in the market, you’ve got a situation where everyone is done taking people’s word for anything,” Marszalek said. “We focused on demonstrating our strength and stability through our actions.”

Marszalek acknowledged that Crypto.com, like other exchanges, has faced increased withdrawals since the FTX news broke, but he said his platform has since stabilized.

FTX CEO Sam Bankman-Fried said his company’s assets were “fine” two days before he was desperate for a rescue because of a liquidity crunch. It’s a familiar tactic. Alex Mashinsky, CEO of the now bankrupt crypto lending platform, Celsius, reassured customers of solvency days before halting wtihdrawals and ultimately filing for bankruptcy.

The exterior of Crypto.com Arena on January 26, 2022 in Los Angeles, California.

Rich Fury | Getty Images

There are other similarities, too.

Just as FTX signed a massive deal last year with the NBA’s Miami Heat for naming rights to the team’s arena, Crypto.com agreed to pay $700 million last November to put its name and logo on the arena that hosts the Los Angeles Lakers, among other teams in L.A. FTX had Tom Brady and Steph Curry promoting its products. Crypto.com reeled in Matt Damon as a pitchman. Both companies bought Super Bowl ads and partnered with Formula One.

Marszalek has personal issues from his past that may also be concerning. The Daily Beast reported in November 2021 that Marszalek departed his last job “amid accusations from customers and business partners that they had been ripped off.” The Australian company was called Ensogo, and it offered online coupons. It abruptly shut down in 2016.

According to documents filed with the Australian Securities Exchange, Ensogo requested its stock be suspended from trading in June 2016. The board accepted Marszalek’s resignation at that time and the company said in a filing that it “is yet to announce the appointment of a new CEO.”

A spokesperson for Crypto.com told the Daily Beast that the board decided to shutter Ensogo, and “there was never a finding of wrongdoing under Kris’s leadership.”

Last week, Crypto.com released unaudited information about its assets to blockhain analytics firm Nansen, who used the information to create a chart showing where those assets were held. One startling revelation: Crypto.com had 20% of its assets in wallets in shiba inu, a so-called “meme token” that exists purely for speculation, building off the shiba-inu dog image of the similarly popular joke token, dogecoin.

When asked by CNBC on Tuesday if Crypto.com holds tokens on its balance sheet, Marszalek said it’s a “very conservatively run business” that holds “mostly fiat and stablecoins as our source of capital.”

“Yeah but how much?” asked CNBC’s Becky Quick, reminding Marszalek that FTX had “billions of dollars” in its self-created FTT token before it declared bankruptcy.

Marszalek declined to say.

“We’re a privately held company,” he said, adding that he’s not going to provide specifics “about our balance sheet.”

He was quick to say that the company is “very well capitalized,” and reiterated comments from his YouTube session on Monday, telling CNBC that the company has “a very strong balance sheet” with “zero debt and zero leverage in the business, and we are cash flow positive.”

The company has already been hammered during the crypto winter, which has pushed bitcoin and ether down by two-thirds this year. In recent months, Crypto.com reportedly slashed over one-quarter of its workforce. Daily trading volume in CRO is down to about $365 million, according to data from Nomics. Last year, that figure was above $4 billion.

Marszalek’s main goal now is evident: avoid an FTX-type run that could see the company lose a boatload of customers. But he also wants to make it abundantly clear that all the reserves are available to honor any withdrawal requests, and that there’s no hedge fund activity taking place with user deposits.

“We run a very simple business,” he said. “We give 70 million users globally access to digital currencies and take a fee for that.”

Coinbase and Binance have similarly been on media tours trying to assuage customer concerns.

Blockchain.com CEO Peter Smith expects the whole way that crypto enthusiasts hold their investments to change dramatically. Smith, whose company operates an exchange and offers a crypto wallet, told CNBC last week that consumers don’t need to trust third parties to hold their crypto funds, and are increasingly doing it themselves.

“You’re going to see people shift toward crypto on their own private keys,” Smith said, adding that the company has about 85 million users who already do it that way. “The ultimate reality and coolest part of crypto is you can store your funds on your own private key where you have no counterparty exposure.”

From a governance standpoint, FTX was uniquely troubled. The company had no board, no finance chief and no head of compliance, despite raising billions of dollars, some from top firms like Sequoia and Tiger Global, and racing to a $32 billion valuation.

Marszalek has a more traditional corporate structure. Crypto.com has a four-person advisory board as well as a CFO, a head of legal and a senior vice president of risk and operations. That doesn’t mean there can’t be fraud (see: Theranos) or bad behavior (read: WeWork), but it’s at least a sign that some controls are in place as Crypto.com and other players try to weather a crypto winter that keeps getting colder.

“We feel quite good about where we are as a company and our operations,” said Marszalek, pointing out that the company generated over $1 billion in revenue last year and has topped that number this year. “What worries me is the impact of this collapse on the whole industry. It sets us back a good couple of years in terms of the industry’s reputation.”

Sam Bankman-Fried’s cryptocurrency exchange FTX has filed for Chapter 11 bankruptcy protection in the U.S., according to a company statement posted on Twitter. Bankman-Fried has also stepped down as CEO and has been succeeded by John J. Ray III, though the outgoing chief will stay on to assist with the transition.

Approximately 130 additional affiliated companies are part of the proceedings, including Alameda Research, Bankman-Fried’s crypto trading firm, and FTX.us, the company’s U.S. subsidiary.

In the 23-page bankruptcy filing obtained by CNBC, FTX indicates it has more than 100,000 creditors, assets in the range of $10 billion to $50 billion, as well as liabilities in the range of $10 billion to $50 billion. Bankman-Fried also indicated he wishes to appoint Stephen Neal as the firm’s new chairman of the board.

CNBC reached out to Adam Landis, founding partner of Landis Rath & Cobb LLP, who filed the Chapter 11 proceedings on behalf of FTX. CNBC did not immediately hear back to our request for comment.

“The immediate relief of Chapter 11 is appropriate to provide the FTX Group the opportunity to assess its situation and develop a process to maximize recoveries for stakeholders,” said the new FTX chief, Ray.

“The FTX Group has valuable assets that can only be effectively administered in an organized, joint process. I want to ensure every employee, customer, creditor, contract party, stockholder, investor, governmental authority and other stakeholder that we are going to conduct this effort with diligence, thoroughness and transparency,” continued Ray.

He added that stakeholders should understand that events have been fast moving, that the new team is engaged only recently and that they should review the materials filed on the docket of the proceedings over the coming days for more information.

It caps off a tumultuous week for one of the biggest names in the sector.

In the space of days, FTX went from a $32 billion valuation to bankruptcy as liquidity dried up, customers demanded withdrawals and rival exchange Binance ripped up its nonbinding agreement to buy the company. FTX founder Bankman-Fried admitted on Thursday that he “f—ed up.”

Anthony Scaramucci, founder of SkyBridge Capital and short-time Trump communications director, flew to the Bahamas this week to help Bankman-Fried as an investor and friend. When Scaramucci got there, he says, it appeared beyond the point of a simple liquidity rescue. He said he didn’t see evidence of this mishandling when he and other investors first screened FTX as a potential business partner.

“Duped I guess is the right word, but I am very disappointed because I do like Sam,” Scaramucci said Friday morning on CNBC’s “Squawk Box.” “I don’t know what happened because I was not an insider at FTX.”

An FTX spokesperson did not immediately respond to CNBC’s request for comment on this story, including on Scaramucci’s remarks.

In a short period of time, FTX expanded into non-crypto elements of life, such as pop culture. For example, in the past Super Bowl, it aired a commercial featuring comedian Larry David, in which David turned down an opportunity to invest in crypto. “Ehh, I don’t think so. And I’m never wrong about this stuff. Never.”

GameStop is winding down its partnership with FTX, according to people familiar with the matter. Under the agreement, announced in September, GameStop sold FTX gift cards in select stores and while FTX promoted the retailer on its exchange.

The winding down of business agreements, like the one with GameStop, will likely continue following the FTX bankruptcy filing.

The Chapter 11 proceedings exclude the following subsidiaries: LedgerX LLC, FTX Digital Markets Ltd., FTX Australia Pty Ltd., and FTX Express Pay Ltd.

— CNBC’s Jack Stebbins and Lillian Rizzo contributed to this report.

Binance is backing out of its plans to acquire FTX, the company said Wednesday, leaving Sam Bankman-Fried’s crypto empire on the verge of collapse.

The reversal comes one day after Binance CEO Changpeng Zhao announced that the world’s largest cryptocurrency firm had reached a non-binding deal to buy FTX’s non-U.S. businesses for an undisclosed amount, rescuing the company from a liquidity crisis. Earlier this year, FTX was valued at $32 billion by private investors.

“In the beginning, our hope was to be able to support FTX’s customers to provide liquidity,” Binance said in a tweet on Wednesday. “But the issues are beyond our control or ability to help.”

On Monday night, facing a liquidity crunch, Bankman-Fried was scrambling to raise money from venture capitalists and other investors before he went to Binance, according to sources with knowledge of the matter. Zhao initially agreed to step in, but his company quickly changed course, citing reports of “mishandled customer funds and alleged U.S. agency investigations.”

It’s unclear who is next in line to buy the beleaguered crypto exchange. Bankman-Fried told investors that the company is facing a shortfall of up to $8 billion from withdrawal requests and needs emergency funding, according to a person familiar with the matter.

Read more about tech and crypto from CNBC Pro

The disintegration of the Binance-FTX deal is the latest chapter in a shocking collapse that’s rocked the crypto world this week. Bankman-Fried tried to reassure investors just on Monday that the company’s assets were fine. But after Binance’s Zhao said publicly that his company was selling its holdings in FTX’s native token FTT, the selloff was on, and FTX could do nothing to stop it.

One of Silicon Valley’s most prominent VC firms, Sequoia Capital, sank $210 million into the company, according to reporter Eric Newcomer. FTX was telling investors recently that its operating income in 2022 was projected to drop to $144 million this year, down from $338 million in 2021, while revenue was projected to rise to $1.1 billion from $1 billion last year, Newcomer reports.

Bankman-Fried said on Tuesday that customers had demanded withdrawals to the tune of $6 billion. He also deleted tweets from the prior day indicating that FTX had enough assets to cover clients’ holdings.

Zhao told Binance employees in a memo earlier on Wednesday that he “did not master plan” the collapse of FTX. He said FTX going down is “not good for anyone in the industry” and employees should not “view it as a win for us.”

He also told them not to trade FTT tokens while this ordeal unfolds.

“If you have a bag, you have a bag,” he wrote. “DO NOT buy or sell.”

FTT had already lost 80% of its value between Monday and Tuesday, falling to $5 and wiping out more than $2 billion in a day. It fell by more than half on Wednesday to around $2.30, shrinking the total value of circulating tokens to roughly $308 million.

Cryptocurrencies have plummeted amid the deal turmoil, with bitcoin falling 15% on Wednesday after a 13% drop on Tuesday. It’s trading below $16,000 for the first time since November 2020. Ether, meanwhile, has plunged more than 30% over the past two days and is close to falling below $1,000.

Here’s the company’s full statement:

“As a result of corporate due diligence, as well as the latest news reports regarding mishandled customer funds and alleged US agency investigations, we have decided that we will not pursue the potential acquisition of FTX.com.

In the beginning, our hope was to be able to support FTX’s customers to provide liquidity, but the issues are beyond our control or ability to help.

Every time a major player in an industry fails, retail consumers will suffer. We have seen over the last several years that the crypto ecosystem is becoming more resilient and we believe in time that outliers that misuse user funds will be weeded out by the free market.

As regulatory frameworks are developed and as the industry continues to evolve toward greater decentralization, the ecosystem will grow stronger.”

Correction: FTX was telling investors its operating income was projected to drop to $144 million this year, down from $338 million in 2021.

Meta is laying off 13% of its staff, or more than 11,000 employees, CEO Mark Zuckerberg said in a letter to employees Wednesday.

“Today I’m sharing some of the most difficult changes we’ve made in Meta’s history,” Zuckerberg said in the letter. “I’ve decided to reduce the size of our team by about 13% and let more than 11,000 of our talented employees go. We are also taking a number of additional steps to become a leaner and more efficient company by cutting discretionary spending and extending our hiring freeze through Q1.”

Shares of Meta were up about 4% in premarket trading.

The layoffs come amid a tough time for Facebook parent company Meta, which provided lukewarm guidance in late October for its upcoming fourth-quarter earnings that spooked investors and caused its shares to sink nearly 20%.

Investors have been concerned about Meta’s rising costs and expenses, which jumped 19% year over year in the third quarter to $22.1 billion. The company’s overall sales declined 4% to $27.71 billion in the quarter while its operating income dropped 46% from the previous year to $5.66 billion.

“I want to take accountability for these decisions and for how we got here. I know this is tough for everyone, and I’m especially sorry to those impacted.” Zuckerberg said.

He said Meta is making reductions in every organization but that recruiting will be disproportionately affected since the company plans to hire fewer people in 2023. The company extended its hiring freeze through the first quarter with a few exceptions, Zuckerberg said.

“This is a sad moment, and there’s no way around that. To those who are leaving, I want to thank you again for everything you’ve put into this place,” he added.

Impacted employees will receive 16 weeks of pay plus two additional weeks for every year of service, Zuckerberg said. Meta will cover health insurance for six months.

Meta is heavily investing in the metaverse, which generally refers to a yet-to-be developed digital world that can be accessed by virtual reality and augmented reality headsets. This hefty bet has cost Meta $9.4 billion so far in 2022, and the company anticipates that losses “will grow significantly year-over-year.”

Zuckerberg said during a call with analysts as part of its third-quarter earnings report that Meta plans to “focus our investments on a small number of high priority growth areas” during the next year.

“That means some teams will grow meaningfully, but most other teams will stay flat or shrink over the next year,” Zuckerberg said. “In aggregate, we expect to end 2023 as either roughly the same size, or even a slightly smaller organization than we are today.”

Meta counts more than 87,000 employees as of the end of September.

Here’s Mark Zuckerberg’s letter to employees:

“Today I’m sharing some of the most difficult changes we’ve made in Meta’s history. I’ve decided to reduce the size of our team by about 13% and let more than 11,000 of our talented employees go. We are also taking a number of additional steps to become a leaner and more efficient company by cutting discretionary spending and extending our hiring freeze through Q1.

I want to take accountability for these decisions and for how we got here. I know this is tough for everyone, and I’m especially sorry to those impacted.

How did we get here?

At the start of Covid, the world rapidly moved online and the surge of e-commerce led to outsized revenue growth. Many people predicted this would be a permanent acceleration that would continue even after the pandemic ended. I did too, so I made the decision to significantly increase our investments. Unfortunately, this did not play out the way I expected. Not only has online commerce returned to prior trends, but the macroeconomic downturn, increased competition, and ads signal loss have caused our revenue to be much lower than I’d expected. I got this wrong, and I take responsibility for that.

In this new environment, we need to become more capital efficient. We’ve shifted more of our resources onto a smaller number of high priority growth areas — like our AI discovery engine, our ads and business platforms, and our long-term vision for the metaverse. We’ve cut costs across our business, including scaling back budgets, reducing perks, and shrinking our real estate footprint. We’re restructuring teams to increase our efficiency. But these measures alone won’t bring our expenses in line with our revenue growth, so I’ve also made the hard decision to let people go.

How will this work?

There is no good way to do a layoff, but we hope to get all the relevant information to you as quickly as possible and then do whatever we can to support you through this.

Everyone will get an email soon letting you know what this layoff means for you. After that, every affected employee will have the opportunity to speak with someone to get their questions answered and join information sessions.

Some of the details in the US include:

Severance. We will pay 16 weeks of base pay plus two additional weeks for every year of service, with no cap.

PTO. We’ll pay for all remaining PTO time.

RSU vesting. Everyone impacted will receive their November 15, 2022 vesting.

Health insurance. We’ll cover the cost of healthcare for people and their families for six months.

Career services. We’ll provide three months of career support with an external vendor, including early access to unpublished job leads.

Immigration support. I know this is especially difficult if you’re here on a visa. There’s a notice period before termination and some visa grace periods, which means everyone will have time to make plans and work through their immigration status. We have dedicated immigration specialists to help guide you based on what you and your family need.

Outside the US, support will be similar, and we’ll follow up soon with separate processes that take into account local employment laws.

We made the decision to remove access to most Meta systems for people leaving today given the amount of access to sensitive information. But we’re keeping email addresses active throughout the day so everyone can say farewell.

While we’re making reductions in every organization across both Family of Apps and Reality Labs, some teams will be affected more than others. Recruiting will be disproportionately affected since we’re planning to hire fewer people next year. We’re also restructuring our business teams more substantially. This is not a reflection of the great work these groups have done, but what we need going forward. The leaders of each group will schedule time to discuss what this means for your team over the next couple of days.

The teammates who will be leaving us are talented and passionate, and have made an important impact on our company and community. Each of you have helped make Meta a success, and I’m grateful for it. I’m sure you’ll go on to do great work at other places.

What other changes are we making?

I view layoffs as a last resort, so we decided to rein in other sources of cost before letting teammates go. Overall, this will add up to a meaningful cultural shift in how we operate. For example, as we shrink our real estate footprint, we’re transitioning to desk sharing for people who already spend most of their time outside the office. We’ll roll out more cost-cutting changes like this in the coming months.

We’re also extending our hiring freeze through Q1 with a small number of exceptions. I’m going to watch our business performance, operational efficiency, and other macroeconomic factors to determine whether and how much we should resume hiring at that point. This will give us the ability to control our cost structure in the event of a continued economic downturn. It will also put us on a path to achieve a more efficient cost structure than we outlined to investors recently.

I’m currently in the middle of a thorough review of our infrastructure spending. As we build our AI infrastructure, we’re focused on becoming even more efficient with our capacity. Our infrastructure will continue to be an important advantage for Meta, and I believe we can achieve this while spending less.

Fundamentally, we’re making all these changes for two reasons: our revenue outlook is lower than we expected at the beginning of this year, and we want to make sure we’re operating efficiently across both Family of Apps and Reality Labs.

How do we move forward?

This is a sad moment, and there’s no way around that. To those who are leaving, I want to thank you again for everything you’ve put into this place. We would not be where we are today without your hard work, and I’m grateful for your contributions.

To those who are staying, I know this is a difficult time for you too. Not only are we saying goodbye to people we’ve worked closely with, but many of you also feel uncertainty about the future. I want you to know that we’re making these decisions to make sure our future is strong.

I believe we are deeply underestimated as a company today. Billions of people use our services to connect, and our communities keep growing. Our core business is among the most profitable ever built with huge potential ahead. And we’re leading in developing the technology to define the future of social connection and the next computing platform. We do historically important work. I’m confident that if we work efficiently, we’ll come out of this downturn stronger and more resilient than ever.

We’ll share more on how we’ll operate as a streamlined organization to achieve our priorities in the weeks ahead. For now, I’ll say one more time how thankful I am to those of you who are leaving for everything you’ve done to advance our mission.

Mark”

Watch: Meta has to go back to their core advertising business and double down.

After a Covid outbreak at a Foxconn factory in Zhengzhou, China, some workers chose to go home. Pictured here are the shuttle buses on Oct. 30, 2022.

VCG | Getty Images

Apple said in a statement on Sunday that it has temporarily reduced iPhone 14 production because of Covid-19 restrictions at its primary iPhone 14 Pro and iPhone 14 Pro Max assembly plant in Zhengzhou, China.

The factory, operated by Foxconn, is operating at “significantly reduced capacity,” Apple said. It warned that it would ship fewer units and that customers would experience longer wait times when ordering devices.

Apple’s warning brings up the possibility that it may sell fewer iPhones in the December quarter because it is having trouble making enough to meet demand. It previously signaled slowing growth in the December quarter last month.

It said that it continues to see strong demand for the affected models, which are higher-priced than other iPhone models and start at $999 and $1099.

In the past week, China has ordered lockdowns in Zhengzhou, where Apple does the majority of its iPhone production. The factory in China has grappled with employees fleeing the facility because of its Covid policies and outbreaks, according to Reuters.

China continues to pursue a “zero-Covid” policy that requires facilities like the iPhone facility in Zhengzhou to operate as “closed loops,” where workers isolate in dorms and work in factories separated from the outside world.

It currently takes 31 days to receive an iPhone 14 Pro if ordered from Apple’s website, longer than the average 2-day lead time for less-expensive iPhone models, JPMorgan analyst Samik Chatterjee said in a note on Sunday.

PayPal shares fell more than 5% in after-hours trading, despite beating earnings and revenue expectations for the third quarter, as the company’s Q4 revenue estimate came in behind analysts’ expectations.

Here’s what PayPal reported:

Earnings per share (EPS): $1.08 per share, ex-items, vs. 96 cents expected, according to a Refinitiv survey of analysts

Revenue: $6.85 billion, vs. $6.82 billion expected, according to Refinitiv

The company estimated Q4 revenues to come in at $7.38 billion, which is less than the $7.74 billion consensus expectations, according to analysts surveyed by Refinitiv

PayPal raised EPS guidance for the full fiscal year, saying it’s benefited from “ongoing productivity initiatives.” It expects to add 8 to 10 million net new active users in the fiscal year.

The company said it’s working with Apple to enhance its offerings for PayPal and Venmo, including by letting U.S. merchant customers accept contactless payments through their mobile wallets and adding PayPal and Venmo network-branded credit and debit cards to the Apple Wallet.

AMD shares rose as much as 6% in extended trading on Tuesday after the chipmaker indicated its server chip business will grow in the quarters ahead, even as earnings and quarterly guidance failed to meet Wall Street’s expectations.

Here’s how the company did:

Earnings: 67 cents per share, adjusted, vs. 68 cents per share as expected by analysts, according to Refinitiv.

Revenue: $5.57 billion, vs. $5.62 billion as expected by analysts, according to Refinitiv.

Overall, AMD’s revenue grew by 29% year over year in the fiscal third quarter, which ended Sept. 24, according to a statement. Net income fell 93% to $66 million, mainly because of AMD’s $49 billion acquisition in February of Xilinx, a maker of chips called field-programmable gate arrays.

On Oct. 6, AMD issued preliminary results for the fiscal third quarter that lagged guidance it provided in August, because of fewer chip shipments in a weaker PC market than expected. The stock fell almost 14%, its largest decline since March 2020. AMD has been preparing for the PC market to be lackluster in the fiscal fourth quarter, CEO Lisa Su said on a conference call with analysts.

For the full year, AMD said it sees $23.5 billion in revenue, down from the $26.3 billion forecast the company gave in August. Analysts polled by Refinitiv had expected $23.88 billion. The company contracted its adjusted gross margin outlook to 52% from 54% in August.

AMD said its Data Center segment generated $1.61 billion in revenue in the fiscal third quarter, up 45% and slightly below the StreetAccount consensus of $1.64 billion. The unit includes contributions from Xilinx and distributed computing startup Pensando, which AMD bought for $1.9 billion.

The chipmaker has seen healthy demand for shipments of its server chips that carry the code name Genoa. AMD plans to launch Epyc data center chips on Nov. 10.

“We’ve had very good progress at the North American cloud vendors and we continue to believe that although there may be some near-term, let’s call it optimization, of, let’s call it individual footprints and efficiencies at individual cloud vendors, over the medium term,” Su said. “As we go into 2023, we expect growth in that market, particularly customers moving more workloads to AMD, just given the strength of our product portfolio and overall general coming forward.”

Su said cloud revenue more than doubled and increased sequentially, while revenue from server makers targeting big companies was down sequentially. She said AMD has seen enterprise customers taking longer to make decisions and being slightly more conservative on capital expenditures.

The data center business “at least for now, looks decent, and quite a bit better than what’s going on with Intel,” said Stacy Rasgon, senior semiconductor analyst at Bernstein, in an interview on CNBC’s “Closing Bell: Overtime” after AMD announced its results. “There’s a lot of uncertainty about what they were going to say about data center, particularly in the wake of Intel’s report where Intel had called for the market to decline in Q4. This is probably why the stock is up now. The guide itself is quite weak, but it seems likely that it’s isolated to PCs.”

The Gaming segment produced $1.63 billion in revenue. That was up about 14% and in line with the $1.63 billion consensus among analysts surveyed by StreetAccount. The company touted healthy demand for console chips for Microsoft and Sony as the holidays approach.

The Embedded segment that includes some Xilinx sales delivered $1.3 billion, up from $79 million in the year-ago quarter and in line with the $1.3 billion StreetAccount consensus.

AMD’s Client unit, which the chipmaker had warned about in October, generated $1.02 billion in revenue. That was down nearly 40% but in excess of the $1.17 billion StreetAccount consensus. Four days after AMD gave preliminary results, technology industry researcher Gartner said third-quarter PC shipments fell 19.5%, the steepest decline the company has seen since it started following the market in the mid-1990s. During the quarter AMD announced Ryzen 7000 desktop PC chips, and the company pointed to positive reviews of the products.

AMD “worked closely with our customers to reduce downstream inventory,” Su said.

All four of the segments delivered slightly more revenue than AMD had said to expect in its October warning.

“We will continue to invest in our strategic priorities around the data center, embedded and commercial markets, while tightening expenses across the rest of the business,” Su said. The company will control operating expenses and headcount growth, said Devinder Kumar, AMD’s finance chief.

Notwithstanding the after-hours fluctuation, AMD stock has plummeted 58% so far this year, while the S&P 500 is down 19% over the same period.

Other than Apple, it was a brutal earnings week for Big Tech.

Alphabet, Amazon, Meta and Microsoft combined lost over $350 billion in market cap after offering concerning commentary for the third quarter and the remainder of the year. Between slowing revenue growth — or declines in Meta’s case — and efforts to control costs, the tech giants have found themselves in an unfamiliar position after unbridled growth in the past decade.

Third-quarter results this week came against the backdrop of soaring inflation, rising interest rates and a looming recession. Apple bucked the trend after beating expectations for revenue and profit. The stock on Friday had its best day in over two years.

On the opposite end of the spectrum was Meta, which has seen its stock price collapse in 2022. Facebook’s parent came up short on earnings, recorded its lowest average revenue per user in two years and said sales in the fourth quarter will likely decline for a third straight period.

“There are a lot of things going on right now in the business and in the world, and so it’s hard to have a simple ‘We’re going to do this one thing, and that’s going to solve all the issues,’” Meta CEO Mark Zuckerberg said on the company’s earnings call on Wednesday.

Meta’s stock had its worst week since the company’s IPO in 2012, plunging 24% over the past five days. Microsoft fell 2.6% for the week, due to a 7.7% decline on Wednesday after the company gave weak guidance for the year-end period and missed estimates for cloud revenue.

Things were also bleak at Amazon, which dropped 13%. A gloomy fourth-quarter forecast along with a dramatic slowdown in its cloud-computing unit were largely to blame for the sell-off.

While Amazon Web Services saw expansion slow to 27.5% from 33% in the prior period, Google’s cloud group, which is significantly smaller, sped up to almost 38% growth from around 36%. Google plans to keep spending in cloud even as it intends to rein in headcount overall growth in the next few quarters.

“We are excited about the opportunity, given that businesses and governments are still in the early days of public cloud adoption, and we continue to invest accordingly,” Ruth Porat, Alphabet CFO, said on a conference call with analysts on Tuesday. “We remain focused on the longer-term path to profitability.”

However, results from the rest of Google parent Alphabet were less impressive. The company’s core advertising business grew just slightly, and YouTube’s ad revenue dropped from the prior year. The reverse was true for Amazon, which is playing catchup to Google and Facebook in digital advertising. In Amazon’s ad business, revenue growth accelerated to 30% from 21%, topping analysts’ estimates.

“Advertisers are looking for effective advertising, and our advertising is at the point where consumers are ready to spend,” said Brian Olsavsky, the company’s finance chief. “We have a lot of advantages that we feel that will help both consumers and also our partners like sellers and advertisers.”

Analyst Aaron Kessler at Raymond James lowered his price target on Amazon stock to $130 from $164 after the results. But he maintained his equivalent of a buy rating on the stock and said the company’s “robust advertising growth” has the potential to help Amazon fatten up its margin.

As investors continue to rotate away from tech, they’re finding money-making opportunities in other parts of the market that had previously lagged behind software and internet names. The Dow Jones Industrial Average rose 3% this week, the fourth weekly gain in a row for the index. Prior to 2021, the Dow had underperformed the Nasdaq for five straight years.

On Elon Musk’s first day in control of Twitter, the company has started laying off employees, including data engineers, according to CNBC’s Deirdre Bosa.

This is breaking news. Please check back for updates.

Iranians protest to demand justice and highlight the death of Mahsa Amini, who was arrested by morality police and subsequently died in hospital in Tehran under suspicious circumstances.

Mike Kemp | In Pictures via Getty Images

A bipartisan group of 13 lawmakers urged several U.S. tech CEOs to do more to help Iranian people stay connected to the internet as their government seeks to censor communications amid ongoing protests.

The Iranian regime has taken aggressive measures to block citizens from the internet and anti-government messages as people across the country continue to protest its restrictive standards. The protests began after 22-year-old Mahsa Amini died while in the custody of Iran’s so-called morality police, who had accused her of improperly wearing her hijab, an Islamic head-covering for women.

In the letter to the CEOs of Amazon, Apple, Google, Meta, Microsoft and cloud service DigitalOcean, the lawmakers asked the executives to be “more proactive” in getting important services to Iran. The Treasury Department last month issued guidance on U.S. sanctions on Iran to make clear that social media platforms, video conferencing and cloud-based services that deliver virtual private networks can operate in Iran.

“While we appreciate some of the steps your companies have taken, we believe your companies can be more proactive in acting pursuant to the broad authorization provided in GLD-2,” the lawmakers wrote, referencing the general license used to issue sanctions guidance.

They specifically pointed to four different types of tools they’d like to see the companies work to get into the hands of the Iranian people: cloud and hosting services, messaging and communication tools, developer and analytics tools and access to app stores.

The lawmakers said these types of tools would help Iranian citizens stay connected to the internet in secure ways amid government-imposed shutdowns and reduce their reliance on domestic infrastructure. The availability of multiple secure communications tools would make it harder for the Iranian regime to shut down all of them at once, they wrote.

The lawmakers also said that giving the Iranian people access to developer tools and app stores would allow them to “create and harden” their own communications apps and security tools and give them a place to distribute them without government surveillance.

Reps. Tom Malinowski, D-N.J., Claudia Tenney, R-N.Y., and Sens. Bob Menendez, D-N.J. and Marsha Blackburn, R-Tenn., took the lead in the letter.

“Iranians are fearlessly risking their lives for their fundamental rights and dignity,” they wrote. “Your tools and services may be vital in their efforts to pursue these aspirations, and the United States should continue to make every effort to assist them.”

A Google spokesperson said in a statement the company is working on ways to “ensure continued access to generally available communications tools like Google Meet and our other Internet services.” Google launched location sharing in Iran on Google Maps in September to let people let loved ones know where they are and the Jigsaw team within Google is working to make its tool more widely available so users in Iran can run their own VPNs that resist blocking, the spokesperson added.

Meta did not provide a comment. The Facebook-owner had made Instagram and WhatsApp available in Iran, but the services have been restricted by the government.

The other companies named in the letter did not immediately respond to CNBC’s requests for comment.

Meta Platforms CEO Mark Zuckerberg speaks at Georgetown University in Washington on Oct. 17, 2019.

Andrew Caballero-Reynolds | AFP | Getty Images

Apple recently updated its App Store guidelines with changes that, yet again, impact Facebook’s ad business.

The new rule, introduced Monday, says that companies like Meta, which owns Facebook and Instagram, can offer apps that allow people to buy and manage advertising campaigns in dedicated apps without using Apple’s payment system, but it considers buying an ad in a social media app to be a digital purchase, from which Apple takes a 30% cut.

Meta wasn’t happy with the change. A Meta spokesperson told CNBC, “Apple continues to evolve its policies to grow their own business while undercutting others in the digital economy.”

The episode is the latest skirmish from companies like Meta that feel that Apple has too much power over mobile distribution and the ever expanding and changing rules of Apple’s App Store, which is the only way to install apps on an iPhone.

Meta and Apple have been battling for years, but the rivalry has grown more heated recently after Apple introduced App Tracking Transparency in the iPhone operating system last year. The privacy feature allows users to decline to offer app developers like Meta a unique device ID that can be used to track ad performance. Meta says the change could cost it $10 billion this year.

Meta and Apple also appear poised to compete in the world of consumer hardware, after Meta released the Quest Pro headset and Apple has been developing a competing VR headset for years that could reportedly launch next year.

Apple told CNBC that even before the new guideline the company considered social boosts to be the kind of digital purchase that needed to use Apple in-app purchases, and that the rule is more of a clarification than a new restriction.

“For many years now, the App Store guidelines have been clear that the sale of digital goods and services within an app must use In-App Purchase,” an Apple spokesman told CNBC. “Boosting, which allows an individual or organization to pay to increase the reach of a post or profile, is a digital service — so of course In-App Purchase is required. This has always been the case and there are many examples of apps that do it successfully.”

This individual restriction has long been a sticking point, and Meta, back when it was still named Facebook, negotiated with Apple over social media boosts and whether they would fall under Apple’s digital purchase rules, according to The Wall Street Journal.

Boosting features are offered by several social media companies. But most, like Twitter, already use Apple’s in-app purchase mechanism that lists boosted posts for $9.99 on Apple’s App Store. TikTok sells coins, or a currency used to promote posts, through in-app purchases as well.

For Meta, it thinks Apple’s recent clarification crosses a line in taking a piece of advertising revenue, not just app sales. Meta points to previous Apple executive statements, some made as part of the Epic Games trial over App Store rules, where it said it didn’t take a cut of ads.

“Apple previously said it didn’t take a share of developer advertising revenue, and now apparently changed its mind. We remain committed to offering small businesses simple ways to run ads and grow their businesses on our apps,” the Meta spokesperson told CNBC.

Apple isn’t asking for a cut of every ad served through the Facebook or Instagram apps. But Meta clearly feels targeted by Apple’s increasing power over its platforms, and worries that the company could argue that it deserves a piece of Meta’s total ad sales through its ads manager app, according to The Verge, which first reported Meta’s complaint.

It’s unclear how big the boost market is. Most big advertisers use dedicated portals or apps to buy ads. Eric Seufert, an ads industry watcher and the founder of Mobile Dev Memo, wrote Monday that he suspects it is a “negligible proportion of revenue” to the social media companies.

In Alphabet’s third-quarter earnings call on Tuesday, Philipp Schindler, Google’s chief business officer, blamed a slowdown in revenue growth in part on reduced ad spending by cypto companies and other financial firms.

“In the third quarter, we did see a pullback in spend by some advertisers in certain areas in search,” Schindler said. “For example in financial services, we saw a pullback in the insurance, loan, mortgage, and crypto subcategories.”

Google’s overall ad growth of 6% in the quarter was the weakest for any period since 2013, other than one quarter at the beginning of the pandemic. YouTube ad revenue shrank from a year earlier. CEO Sundar Pichai said the “challenging macro climate” is having an impact on Google’s ad business.

Schindler referenced the crypto pullback twice, but he didn’t provide any additional color or specifics. The cryptocurrency industry has been battered in 2022, as investors have fled risky assets and sold out of digital coins and the related stocks that they bid up the prior couple years.

Bitcoin and ethereum have both lost close to 60% of their value this year. Crypto exchange Coinbase, which went public in 2021, is down by over 70%. Meanwhile, the industry has been beset by bankruptcies as hedge funds and lenders saw their liquidity dry up and, in some cases, were forced to default on debt. Celsius Network, Voyager Digital and Three Arrows Capital are some of the more notable names that were forced into bankruptcy.

Elsewhere, companies have downsized. Blockchain.com laid off 25% of its staff in July, Coinbase cut 18% of its workforce the prior month, and Crytpo.com has undertaken two rounds of layoffs this year.

For Google, there’s hope that the crypto sell-off represents just a short-term blip, as the company sees clear opportunities for growth in the future. Earlier this month, Google said it will rely on Coinbase to start letting customers pay for cloud services with cryptocurrencies in 2023. Additionally, Coinbase will move data-related applications to Google’s cloud infrastructure from Amazon Web Services, which the company has relied on for years.

— CNBC’s Jennifer Elias and Jordan Novet contributed to this report.

Microsoft CEO Satya Nadella gestures during a session at the World Economic Forum annual meeting in Davos on May 24, 2022.

Fabrice Coffrini | AFP | Getty Images

Microsoft reported earnings after the bell. Here are the results.

Earnings per share (EPS): $2.35 vs $2.30 expected, according to Refinitiv

Revenue: $50.12 billion, vs. $49.61 billion expected, according to Refinitiv

Analysts have lowered their estimates in recent weeks because of a decline in PC unit shipments and the stronger U.S. dollar. They expect 9.5% revenue growth year over year, which would be the slowest growth since 2017. In July, Microsoft’s finance chief, Amy Hood, had told analysts to expect revenue growth to be 2% lower than it otherwise would be because of currency fluctuations.

Technology industry researcher Gartner said earlier this month that PC shipments in the quarter fell 19.5% year over year, and chipmaker AMD earlier this month issued lower-than-expected preliminary quarterly results tied to a “weaker than expected PC market and significant inventory correction actions across the PC supply chain.” A slowing PC market could cause weakness in Microsoft’s revenue from the Windows operating system.

Analysts expect Microsoft’s Azure cloud revenue to grow 36.4% on an annualized basis, compared with 40% growth in the previous quarter, according to a survey of 14 analysts conducted by CNBC. Analysts polled by StreetAccount expect 36.9% Azure growth.

During the quarter, Microsoft started rolling out the first annual update to its Windows 11 operating system since releasing the original version last year, and the company announced plans to slow down its pace of hiring said it was cutting less than 1% of employees. Microsoft also introduced Viva Engage, a portal in the Teams communication app where co-workers can share video stories.

The quarterly results will include small adjustments in the way that Microsoft reports revenue. Revenue from HoloLens augmented-reality devices will appear in the More Personal Computing segment instead of the Intelligent Cloud segment. Microsoft adjusted its forecast for the segments by about $100 million in connection with the change.

Microsoft shares have fallen about 26% so far this year, while the S&P 500 stock index is down almost 20% over the same period.

Executives will discuss the results and issue guidance on a conference call starting at 5:30 p.m. ET.

This is breaking news. Please check back for updates.

In a new proposed settlement, the Federal Trade Commission is seeking to hold a tech CEO accountable to specific security standards, even if he moves to a new company.

The agency announced Monday that its four commissioners had voted unanimously to issue a proposed order against alcohol delivery platform Drizly and its CEO James Cory Rellas for allegedly failing to implement adequate security measures, which eventually resulted in a data 2020 breach exposing personal information on about 2.5 million consumers.

The FTC claims that despite being alerted to the security concerns two years before the breach, Drizly and Rellas did not do enough to protect their users’ information.

While settlements like this are not that uncommon for the FTC, its decision to name the CEO and have the stipulations follow him beyond his tenure at Drizly exemplifies an approach favored by Democratic Chair Lina Khan. Some progressive enforcers have argued that naming tech executives in their lawsuits should create a stronger deterrence signal for other potential violators.

The proposed order, which is subject to a 30 day public comment period before the commission votes on whether to make it final, would require Rellas to implement an information security program at future companies where he’s the CEO, a majority owner or a senior officer with information security responsibilities, provided the company collects consumer information from more than 25,000 people.

Though Republican Commissioner Christine Wilson voted with the agency’s three Democrats to impose the proposed settlement against Drizly, she objected to naming Rellas as an individual defendant. In a statement, Wilson wrote that naming Rellas will not result in putting “the market on notice that the FTC will use its resources to target lax data security practices.”

“Instead, it has signaled that the agency will substitute its own judgement about corporate priorities and governance decisions for those of companies,” she wrote, adding that given CEOs’ broad overviews of their businesses, it’s best left to companies rather than regulators to determine what the chief executive should pay regular attention to.

In a joint statement, Khan and Democratic Commissioner Alvaro Bedoya responded to Wilson’s argument, writing that “Overseeing a big company is not an excuse to subordinate legal duties in favor of other priorities. The FTC has a role to play in making sure a company’s legal obligations are weighed in the boardroom.”

The order against Drizly would also require the company to destroy personal data it has collected but no longer needs, limit future data collection and establish a comprehensive security program including training for employees and controls on who can access data.

“We take consumer privacy and security very seriously at Drizly, and are happy to put this 2020 event behind us,” a Drizly spokesperson said in a statement.

A car passes by Facebook’s corporate headquarters location in Menlo Park, California, on March 21, 2018.

Josh Edelson | AFP | Getty Images

Facebook’s plans to cut costs combined with the company’s relaxed remote work policies set the stage for a bunch of shuttle bus staffers to lose their jobs.

WeDriveU, a key vendor that Meta uses for its commuter shuttles, said it will be reducing staff in and around the social media company’s Silicon Valley headquarters by nearly 100 people beginning in November, according to an employment filing viewed by CNBC. Most are drivers, and some are dispatchers, operations managers and supervisors.

Meta shuttle vendor Hallcon Corporation, meanwhile, said it’s laying off 63 staffers from its San Francisco location around Nov. 25, due to a “significant draw down of client services,” according to a separate filing.

“Some employees may be maintained or recalled to work,” a human resources director at Hallcon wrote in the filing. “However, no Hallcon Company employee who is being laid off should count on being recalled.”

Meta has cut shuttle staffers from other contractor firms as well, according to Stacy Murphy, vice president of Teamsters Bay Area Local 853, a union with over 15,000 members in industries including transportation. Murphy said all of the layoffs are coming from one company: Meta.

Meta janitorial staff protests job cuts.

Silicon Valley Rising

“All four vendors are losing people,” Murphy said, referring to the companies that work with Meta.

The layoffs are landing as Meta looks to cut costs by 10% or more over the coming months in response to macroeconomic challenges and the company’s general underperformance. Meta reported its first-ever revenue decline in the second quarter and is expected to record another drop when third-quarter numbers land next week.

The stock is trading near its lowest since early 2019 and is one of the worst performers this year in the S&P 500.

Bus drivers who shuttled Facebook employees around the Bay Area as the company expanded at a rapid clip over the past decade are in a particularly precarious position. Not only is the company now pulling back on costs but it’s also maintaining more flexibility than its tech peers in allowing employees to work from wherever they want.

The company opened its office back up to employees in March but gave staffers the option to work remote permanently or in a hybrid model. Many of San Francisco’s small businesses are struggling to stay afloat because of the changes in the workplace.

Murphy, along with union members, plan to protest Facebook’s cuts, saying it’s “the worst time” to reduce staff as blue-collar workers face rising costs in a market that remains among the priciest in the country. “It’s crazy,” she said of the rising prices.

Hallcon and WeDriveU did not return requests for comment.

In July, CNBC reported that Meta had canceled a contract with custodial workers at its headquarters, resulting in job cuts. Earlier this month, janitorial service workers rallied outside of Meta Shop, a retail space in Burlingame, California, to protest working conditions as well as the cuts. The rally was organized by a labor coalition called Silicon Valley Rising and South Bay coalition. Workers held up signs that read “Justice for Janitors” and alleged the company isn’t treating its essential workers fairly.

Meta janitorial staff protests job cuts.

Silicon Valley Rising

Murphy said Meta has cut dozens of shuttle staff over the last three months but that the latest notification of layoffs represents “the biggest we’ve ever seen.”

Teamsters organized a rally for Thursday afternoon at the busiest intersection around Facebook’s headquarters to protest Meta’s cutbacks. Murphy said one of the union’s efforts is to put pressure on the company to ask employees to return to offices.

“Other tech companies are demanding they come back — why haven’t they?” Murphy said. “They want to stay at home and that impacts all of the people that support the company’s overall performance.”

One of the company’s flat aviation-specific Starlink antennas is seen on top of an aircraft.

SpaceX

SpaceX rolled out aviation-specific Starlink satellite internet service on Tuesday, with Elon Musk’s company looking to expand further into the inflight WiFi market.

The company is charging $150,000 for the hardware needed to connect a jet to Starlink, with monthly service costs between $12,500 a month and $25,000 a month. Deliveries to aviation customers are scheduled to “start in mid-2023,” the company said, and reservations require a $5,000 initial payment.

SpaceX advertises “global coverage” through a flat-panel antenna that customers would install on top of an aircraft. SpaceX said it is seeking Federal Aviation Administration certificates for a variety of aircraft, most of which are typically owned and operated as private jets.

As for the quality of the service, SpaceX says Starlink aviation customers can expect speeds up to 350 Megabits per second, “enabling all passengers to access streaming-capable internet at the same time.”

“Passengers can engage in activities previously not functional in flight, including video calls, online gaming, virtual private networks and other high data rate activities,” SpaceX said on its Starlink website.

SpaceX won’t install the antennas, however, noting that customers “will have to arrange the installation with a provider.”

But the company’s aviation service does not require a long-term contract, with SpaceX saying “all plans include unlimited data” and the “hardware is under warranty for as long as you subscribe to the service.”

One of the company’s flat aviation-specific Starlink antennas is seen on top of an aircraft.

This latest offering marks a direct challenge to leading inflight connectivity provider Gogo. But William Blair analyst Louie DiPalma said in a note to investors on Wednesday that the Starlink product “appears to be too big and too expensive to challenge” Gogo’s position in the small-to-midsize business jet market and that “this will likely come as a welcome relief to Gogo investors.”

“Starlink’s entry into the business jet connectivity market has pressured Gogo shares. We anticipate that Gogo will be able to fend off competition because of its unique air-to-ground cellular network. Gogo is the dominant provider of inflight connectivity for business jets, and serves over 6,600 business jets with its cellular network and an additional 4,500 aircraft with [satellite] connectivity,” DiPalma said.

Morgan Stanley analysts wrote in a note that, while Starlink’s “premium pricing” is expected to have “a relatively limited impact to Gogo in the near-term,” SpaceX’s new service “highlights growing competitive intensity in a market that Gogo has historically dominated with >80% market share.”

Starlink is the SpaceX’s plan to build an interconnected internet network with thousands of satellites, designed to deliver high-speed internet to anywhere on the planet. SpaceX has launched nearly 3,500 Starlink satellites into orbit, and the service had about 500,000 subscribers as of June. The company has raised capital steadily to fund development of both Starlink and its next-generation rocket Starship, with $2 billion brought in just this year.

The FCC has authorized SpaceX to provide mobile Starlink internet service, with the company’s product offerings now including services to residential, business, RV, maritime and aviation customers.

Shoppers queue in like outside the Apple store during the launch day of the new iPhone 14 series smartphones in Hong Kong, on September 16, 2022.

Miguel Candela | Anadolu Agency | Getty Images

The closely-watched consumer price index continues to show headline inflation in the U.S. hovering at levels last seen in the mid-1980s.

Prices for a wide variety of goods and services, including food, airfare, and gasoline rose in the latest reading released last week. All told, on a 12-month basis, headline inflation was up 8.2%, according to the Bureau of Labor Statistics, which publishes the CPI.

But one product category monitored by the CPI recorded a 22% plunge, showing deflation: Smartphones.

That might seem counterintuitive. Most phones are expensive and prices for the best ones aren’t going down. Apple released new iPhones in September at the same U.S. prices as last year’s options, for example. And Samsung’s high-end devices cost as much as $1,800 this year. Average selling prices for smartphones continue to climb in markets around the world.

It turns out, smartphones aren’t getting cheaper. They’re getting better. And that’s why CPI shows them deflating instead of inflating like lots of other goods.

Here’s why: Normally, the CPI likes to compare prices for identical items which don’t change much from year-to-year. So, it might compare eggs against eggs, for example. But in the case of smartphones, BLS has to control for devices that get better each year. If smartphones are improving and the price is staying the same, then BLS records a price decline.

“There’s been a lot of declines in the [smartphone] index. And that’s really just in large part dealing with the quality improvements,” said Jonathan Church, an economist at BLS.

Twice a year, BLS looks at the new smartphone models and measures how they’ve improved — whether they have better cameras, displays, or other new methods.

“For smartphones, we’re talking about things like screen size, RAM, processor speed, phone camera or rear camera, whether it’s foldable, or things like that,” Church said.

Then, BLS makes a “quality adjustment.” If the price of the new iPhone didn’t rise, but it received new features, then the CPI would consider that device to be more valuable than the old one, and it assumes consumers get more value for the same money.

Estimating the size of the quality adjustments is done with a hedonic modeling method and BLS uses data from a third-party dataset that includes smartphone specs.

Or, as BLS puts it: “If a replacement smartphone is different from its predecessor and the value of the difference in quality can be accurately estimated, a quality adjustment can be made to the previous item’s price to include the estimated value of the difference in quality.”

BLS has indexed smartphone technologies to a starting point in late 2019, when Apple’s newest device was the iPhone 11 and Samsung’s best was the Galaxy S10. In fact, smartphone prices have been deflating since 2019, according to the CPI.

Eventually, Church said, smartphones may mature into the kind of product that would see price increases and inflation. But the rate of improvement would have to slow down.

“It’s really only that a certain mature point in the cycle that their price will start to go up again,” Church said. “It seems pretty early in the lifecycle still, smartphones in general.”

A shopper looks at a wall fully occupied with iPhone case covers at the American multinational technology company Apple store in Hong Kong. China’s consumer prices rose at a slower-than-expected pace in August amid heatwaves and Covid-19 flare-ups, while producer inflation eased to the lowest since February 2021, official data showed.

Budrul Chukrut | Lightrocket | Getty Images

Employees at an Apple store in Oklahoma City voted on Friday to join a union, marking the second unionized Apple store in the U.S.

The vote is a defeat for Apple, which has opposed unionization efforts around the country. It’s a win for Communications Workers of America, which now represents the workers at an Apple store after separate unionization efforts at stores in Georgia and New York City stalled.

The tally was 56 votes in favor and 32 opposed. Approximately 94 employees were eligible to join CWA. Voting took place earlier this week.

“The Penn Square Apple retail workers are an amazing addition to our growing labor movement, and we are thrilled to welcome them as CWA members,” CWA Secretary-Treasurer Sara Steffens said in a statement.

“We believe the open, direct and collaborative relationship we have with our valued team members is the best way to provide an excellent experience for our customers, and for our teams,” Apple said in a statement, adding that since 2018 it has increased its starting wages in the U.S. by 45%.

The National Labor Relations Board will certify the votes in the coming week. After that, Apple is required to bargain with the union over working conditions.

Apple has opposed the union, according to a CWA filing earlier this month, which alleged that Apple management held anti-union meetings and threatened to withhold perks from stores that unionized.

Apple’s first unionized U.S. store, represented by the International Association of Machinists and Aerospace Workers in Maryland, is preparing to begin formal negotiations with Apple. According to Bloomberg News, Apple told staff there that it would not get some perks such as tuition pre-payment or access to online courses, because it would need to be negotiated with the union.

Apple is one of the most valuable companies in the world, reporting over $365 billion in global sales in 2021. It has about 270 stores in the U.S.