[ad_1]

Mike Mayo, Wells Fargo managing director, joins ‘Closing Bell’ to discuss Mayo’s thoughts on Goldman Sachs post-earnings, the overall bank sector, and more.

[ad_2]

[ad_1]

Mike Mayo, Wells Fargo managing director, joins ‘Closing Bell’ to discuss Mayo’s thoughts on Goldman Sachs post-earnings, the overall bank sector, and more.

[ad_2]

[ad_1]

This photo illustration shows an image of former President Donald Trump reflected in a phone screen that is displaying the Truth Social app, in Washington, DC, on February 21, 2022.

Stefani Reynolds | AFP | Getty Images

The share price of Trump Media closed trading down more than 18% on Monday after the company in a filing said it planned to issue millions of additional shares.

DJT shares closed at $26.61. Trump Media, which created the Truth Social app and trades on the Nasdaq, fell nearly 20% last week.

The company’s dramatic slide came as Donald Trump sat in a Manhattan courtroom for the start of his criminal trial on hush money-related charges. Trump is the majority stakeholder in the company.

Since it began public trading on March 26, Trump Media’s share price has fallen more than 62%, from an opening price of $70.90 that day down to around $27 on Monday.

As a result, its market capitalization has been slashed by nearly $6 billion, leaving it at around $3.7 billion as of Monday.

The company’s intent to issue more common stock was disclosed in a preliminary prospectus filed with the Securities and Exchange Commission.

The shares cannot be issued until a registration statement with the SEC takes effect.

The filing describes a plan to offer more than 21.4 million shares of common stock, issuable “upon the exercise of warrants,” the filing shows. Stock warrants give their holder the ability to buy shares at a predetermined price within a certain time frame.

Trump Media predicted in the filing that it will receive “up to an aggregate of approximately $247.1 million from the exercise of the Warrants.”

The closing price of Trump Media’s warrants was $13.69 as of Friday, according to the filing. The warrants are being traded on the Nasdaq under the ticker “DJTWW.” That ticker fell more than 15% on Monday.

The company also seeks to offer the resale of up to 146.1 million shares of stock from “selling securityholders,” 114.8 million of which are held by Trump himself. Trump owns 78.8 million shares of the company, and stands to obtain 36 million “earnout shares” if the stock stays above $17.50 for enough trading days.

Trump’s current stake in the company — nearly 60% of its shares — was worth more than $2.2 billion at Monday morning’s share price. Trump is not allowed to sell his shares until a six-month lockup period expires.

The lockup period is a condition of Trump Media’s long-delayed merger with the shell company Digital World Acquisition Corp., which was finalized March 25.

Trump, whose social media following was massively diminished after he switched to Truth Social following his suspension from Twitter and Facebook in 2021, has tried to encourage his followers to flock to the fledgling app. It is unclear if they have heeded Trump’s call: The company has not publicly released key performance indicators, including the number of active Truth Social users.

It has, however, revealed a net loss of $58.2 million on revenue of just $4.1 million in 2023.

“The stock valuation is detached from the reality of the financials,” said Ben Silverman, head of Verity Research.

But if the stock price holds high enough for the company to issue earnout shares, Trump and other insiders could be in line to receive a windfall worth more than $1 billion at current trading prices.

[ad_2]

[ad_1]

David Solomon, Chairman & CEO Goldman Sachs, speaking on CNBC’s Squawk Box at the World Economic Forum Annual Meeting in Davos, Switzerland on Jan. 17th, 2024.

Adam Galici | CNBC

Goldman Sachs is scheduled to report first-quarter earnings before the opening bell Monday.

Here’s what Wall Street expects:

Goldman Sachs CEO David Solomon has taken his lumps in the past year, but hope is building for a turnaround.

Dormant capital markets and missteps tied to Solomon’s ill-fated push into retail banking should give way to stronger results this year.

Rivals JPMorgan Chase and Citigroup posted better-than-expected trading results and a rebound in investment banking fees in the first quarter; investors will be disappointed if Goldman doesn’t show similar gains.

Unlike more diversified rivals, Goldman gets most of its revenue from Wall Street activities. That can lead to outsized returns during boom times and underperformance when markets don’t cooperate.

After pivoting away from retail banking, Goldman’s new emphasis for growth has centered on its asset and wealth management division. The business could see gains from buoyant markets at the start of the year, though it also has taken write-downs tied to commercial real estate in the past.

Solomon may also field questions about the latest examples of an exodus in senior managers, including his global treasurer Philip Berlinski and Beth Hammack, co-head of the bank’s global financing group.

On Friday, JPMorgan, Citigroup and Wells Fargo each posted quarterly results that topped estimates.

This story is developing. Please check back for updates.

[ad_2]

[ad_1]

Iranians are waving Iranian flags and a Palestinian flag as they celebrate Iran’s IRGC UAV and missile attack against Israel on April 14, 2024.

Nurphoto | Nurphoto | Getty Images

Iran rained a deluge of drones and missiles on Israel on Saturday night in response to a suspected Israeli strike that killed top Iranian officials in Syria, in a deep escalation of Middle East tensions.

Israel said it identified 300 “threats of various types” and eliminated “99%” of those bound for Israeli soil, according to an update from an Israel Defense Forces spokesperson, Rear Admiral Daniel Hagari. He said a 10-year-old girl was “severely injured by shrapnel” but reported no additional casualties, adding that “several launches” were also made toward Israel from Iraq, Yemen and Lebanon.

Last night marked the first instance of a direct attack on Israel from Iranian territory. Iran-backed factions – such as Palestinian militant group Hamas, Lebanon’s Hezbollah, Yemeni Houthi and Bashar al-Assad’s Syrian administration – have engaged militarily with the Jewish state.

Earlier on Saturday, Iran’s Revolutionary Guards had seized a cargo ship in the Strait of Hormuz, claiming a connection to Israel.

Iran’s chief of staff of the armed forces, Major General Mohammad Bagheri, said that Tehran’s operation had now concluded and would involve no further actions, in comments carried by Iran’s state-owned Islamic Republic News Agency.

Israel and Iran have been on the cusp of direct conflict since the start of Israel’s military campaign in the Gaza Strip, which came in response to Hamas’ terror attack of Oct. 7. Iran vowed revenge after a suspected Israeli strike on an Iranian consulate in Damascus, Syria, on April 1, which killed several top Iranian military commanders.

“We will not be able to comment on the claims regarding a strike in Damascus,” an Israeli foreign ministry spokesperson told CNBC by email, adding, “Iran’s attack on Israel on the night of April 14th is a direct attack on a sovereign nation, its use of proxies for the last decades and the destabilizing effect of the Ayatollah regime in the region and beyond must end.”

Israel’s Ambassador to the U.N., Gilad Erdan, has also called an emergency meeting of the U.N. Security Council and “demanded that they condemn Iran’s attack on Israel and designate the Iranian Revolutionary Guard Corps as a terror organization.”

The European Union has blasted Tehran’s offensive: “The EU strongly condemns the unacceptable Iranian attack against Israel,” EU High Representative Josep Borrell said late Saturday on social media. “This is an unprecedented escalation and a grave threat to regional security.”

U.S. President Joe Biden also denounced the Iranian strike on Saturday as “unprecedented” and convened G7 leaders to “coordinate a united diplomatic response to Iran’s brazen attack,” according to a White House statement.

“While we have not seen attacks on our forces or facilities today, we will remain vigilant to all threats and will not hesitate to take all necessary action to protect our people,” he added.

Relations between stalwart allies Washington and Israel had appeared to slightly chill in recent weeks, with Biden warning further support would hinge on Israel taking steps to protect civilians and humanitarian aid workers in the Gaza enclave.

But the U.S. – alongside the U.K. and France, according to Israeli military – intervened to mitigate last night’s Iranian attack and the assault could reignite urgency to pass a key $95 billion bill including funding for Israel and Ukraine, which has passed the Senate but stagnated on Republican opposition in the U.S. House of Representatives.

“In light of Iran’s unjustified attack on Israel, the House will move from its previously announced legislative schedule next week to instead consider legislation that supports our ally Israel and holds Iran and its terrorist proxies accountable,” said House leader Steve Scalise on social media.

“Congress must also do its part. The national security supplemental that has waited months for action will provide critical resources to Israel and our own military forces in the region,” Mitch McConnell, Senate Republican leader, said in a statement. “We cannot hope to deter conflict without demonstrating resolve and investing seriously in American strength.”

Oil futures prices are in focus after intermittently swelling in recent months on trade disruptions and delays caused by Red Sea maritime attacks from Yemen’s Houthi, who claim solidarity with the Palestinian people.

Iran is also home to vast oil resources, which it has been largely routing toward China since the U.S. reimposed sanctions during Donald Trump’s administration.

The Tel Aviv Stock Exchange’s flagship index, the TA-35, was down 0.38% at 10:23 a.m. London time.

In aviation, several airlines grounded or diverted service through the Middle East, following the Iranian attack. Jordan, Iraq and Lebanon have reopened their airspaces after brief closures on Saturday in the wake of the offensive, Reuters reports.

— CNBC’s Emma Graham contributed to this report

[ad_2]

[ad_1]

Emily Roland, John Hancock co-chief investment strategist, and Bob Elliott, Unlimited CEO, joins ‘Closing Bell Overtime’ to talk the day’s market action.

[ad_2]

[ad_1]

Jonathan Raa | Nurphoto | Getty Images

The price of Trump Media closed trading Friday down nearly 20% for the week.

DJT shares, which dropped by more than 8% within the first hour of trading Friday, eked out a slight gain by the end of the day.

Shares closed up 18 cents at $32.59, an increase of around .5%.

That closing price was more than $38 lower than what its shares first sold for when the social media company began public trading on March 26.

Shares of Trump Media, which owns the Truth Social app, have dropped by 47.4% so far in April wiping out billions of dollars in the company’s market capitalization.

Former President Donald Trump is the biggest shareholder in the company, owning nearly 60% of its stock. Trump on Monday is set to start jury selection for his criminal trial in Manhattan Supreme Court on charges of falsifying business records related to a 2016 hush money payment to porn star Stormy Daniels.

Trump Media on March 26 opened its first day of trading with a price of $70.90 per share, hitting a high of nearly $80 later that same day. During trading that day, the company’s market capitalization topped $9.5 billion.

By Friday’s close, Trump Media’s market cap stood at $4.45 billion — a whopping $5 billion lower than the high it hit more than two weeks ago.

Trump Media began public trading a day after it merged with the shell company Digital World Acquisition Corp., which was created to help a private firm go public.

Trump Media last year had revenue of just $4.1 million, and reported a net loss of $58 million.

That performance and the relatively high price of the company’s stock have drawn keen interest from short sellers, who make trades that are effectively bets that a company’s share price will drop.

As of this week, so-called short interest in DJT was $208.7 million, with 5.44 million shares shorted, according to Ihor Dusaniwsky, managing director of predictive analytics at S3 Partners, a leading financial data marketplace platform.

There were fewer than 100,000 shares of Trump Media available to borrow to sell short. Traders who want to sell stock short must borrow shares to sell, with the expectation that they will later buy back the same number of shares at a lower price to return them to the lender, pocketing the price difference between the trades.

Trump Media has 136.7 million outstanding shares.

A week ago, traders who wanted short Trump Media shares had to pay up to 900% in annual financing costs, meaning they would need a then-$30-per-share drop within a month to break even on their trade, Dusaniwsky said.

Since then, however, financing costs for short trades in Trump Media had sharply fallen, to 200%.

Trump Media was launched after the social media giant X, then known as Twitter, banned Trump from that app on the heels of the Jan. 6, 2021, invasion of the U.S. Capitol by a mob of his supporters.

Trump, who is the presumptive Republican presidential nominee, frequently posts on Truth Social. He has used the app to condemn the four pending criminal cases he faces, along with civil lawsuits that have resulted in judgments against him topping $500 million.

Trump this week hosted a party at his Mar-a-Lago club in Palm Beach, Florida, to celebrate Trump Media.

“I think that Truth has become so important. It’s strong, it’s dedicated,” Trump told attendees, according to a report on the RSBN news site.

“Remember we have no debt, and we have over $200 million dollars in cash, which is very liquid,” Trump said of the company, whose CEO is former Republican congressman Devin Nunes.

— Additional reporting by CNBC’s Nick Wells

[ad_2]

[ad_1]

Wells Fargo customers use the ATM at a bank branch on August 08, 2023 in San Bruno, California.

Justin Sullivan | Getty Images

Wells Fargo reported better-than-expected earnings results on Friday, but some weakness under the hood is putting a lid on the bank’s stock. Stay the course: Shares should move higher as management continues to shake off regulatory punishments for past misdeeds.

[ad_2]

[ad_1]

Citigroup on Friday posted first-quarter revenue that topped analysts’ estimates, helped by better-than-expected results in the bank’s investment banking and trading operations.

Here’s how the company performed, compared with estimates from LSEG, formerly known as Refinitiv:

The bank said profit fell 27% from a year earlier to $3.37 billion, or $1.58 a share, on higher expenses and credit costs. Adjusting for the impact of FDIC charges as well as restructuring and other costs, Citi earned $1.86 per share, according to LSEG calculations.

Revenue slipped 2% to $21.10 billion, mostly driven by the impact of selling an overseas business in the year-earlier period.

Investment banking revenue jumped 35% to $903 million in the quarter, driven by rising debt and equity issuance, topping the $805 million StreetAccount estimate.

Fixed income trading revenue fell 10% to $4.2 billion, edging out the $4.14 billion estimate, and equities revenue rose 5% to $1.2 billion, topping the $1.12 billion estimate.

The bank also posted an 8% gain to $4.8 billion in revenue in its Services division, which includes businesses that cater to the banking needs of global corporations, thanks to rising deposits and fees.

Shares of the bank fell nearly 2% Friday.

Citigroup CEO Jane Fraser previously said that her sweeping corporate overhaul would be complete by March, and that the firm would give an update to severance expenses along with first-quarter results.

“Last month marked the end to the organizational simplification we announced in September,” Fraser said in the earnings release. “The result is a cleaner, simpler management structure that fully aligns to and facilitates our strategy.

Last year, Fraser announced plans to simplify the management structure and reduce costs at the third-biggest U.S. bank by assets. The bank on Friday reiterated its medium term targets for returns hitting at least 11% and generating at least $80 billion in revenue this year.

JPMorgan Chase reported results earlier Friday, and Goldman Sachs reports on Monday.

[ad_2]

[ad_1]

Jamie Dimon, President and CEO of JPMorgan Chase, speaking on CNBC’s “Squawk Box” at the World Economic Forum Annual Meeting in Davos, Switzerland, on Jan. 17, 2024.

Adam Galici | CNBC

JPMorgan Chase is scheduled to report first-quarter earnings before the opening bell Friday.

Here’s what Wall Street expects:

JPMorgan will be watched closely for clues on how banks fared at the start of the year.

While the biggest U.S. bank by assets has navigated the rate environment well since the Federal Reserve began raising rates two years ago, smaller peers have seen their profits squeezed.

The industry has been forced to pay up for deposits as customers shift cash into higher-yielding instruments, squeezing margins. Concern is also mounting over rising losses from commercial loans, especially on office buildings and multifamily dwellings, and higher defaults on credit cards.

Still, large banks are expected to outperform smaller ones this quarter, and expectations for JPMorgan are high. Analysts believe the bank can boost guidance for 2024 net interest income as the Federal Reserve is forced to maintain interest rate levels amid stubborn inflation data.

Analysts will also want to hear what CEO Jamie Dimon has to say about the economy and the industry’s efforts to push back against efforts to cap credit card and overdraft fees.

Wall Street may provide some help this quarter, with investment banking fees for the industry up 11% from a year earlier, according to Dealogic.

Shares of JPMorgan have jumped 15% this year, outperforming the 3.9% gain of the KBW Bank Index.

Wells Fargo and Citigroup are scheduled to release results later Friday, while Goldman Sachs, Bank of America and Morgan Stanley report next week.

This story is developing. Please check back for updates.

[ad_2]

[ad_1]

A woman walks past Wells Fargo bank in New York City, U.S., March 17, 2020.

Jeenah Moon | Reuters

What a difference a year makes.

[ad_2]

[ad_1]

Traders work on the floor at the New York Stock Exchange (NYSE) in New York City, U.S., February 7, 2024.

Brendan Mcdermid | Reuters

The benefits of scale will never be more obvious than when banks begin reporting quarterly results on Friday.

Ever since the chaos of last year’s regional banking crisis that consumed three institutions, larger banks have mostly fared better than smaller ones. That trend is set to continue, especially as expectations for the magnitude of Federal Reserve interest rates cuts have fallen sharply since the start of the year.

The evolving picture on interest rates — dubbed “higher for longer” as expectations for rate cuts this year shift from six reductions to perhaps three – will boost revenue for big banks while squeezing many smaller ones, adding to concerns for the group, according to analysts and investors.

JPMorgan Chase, the nation’s largest lender, kicks off earnings for the industry on Friday, followed by Bank of America and Goldman Sachs next week. On Monday, M&T Bank posts results, one of the first regional lenders to report this period.

The focus for all of them will be how the shifting view on interest rates will impact funding costs and holdings of commercial real estate loans.

“There’s a handful of banks that have done a very good job managing the rate cycle, and there’s been a lot of banks that have mismanaged it,” said Christopher McGratty, head of U.S. bank research at KBW.

Take, for instance, Valley Bank, a regional lender based in Wayne, New Jersey. Guidance the bank gave in January included expectations for seven rate cuts this year, which would’ve allowed it to pay lower rates to depositors.

Instead, the bank might be forced to slash its outlook for net interest income as cuts don’t materialize, according to Morgan Stanley analyst Manan Gosalia, who has the equivalent of a sell rating on the firm.

Net interest income is the money generated by a bank’s loans and securities, minus what it pays for deposits.

Smaller banks have been forced to pay up for deposits more so than larger ones, which are perceived to be safer, in the aftermath of the Silicon Valley Bank failure last year. Rate cuts would’ve provided some relief for smaller banks, while also helping commercial real estate borrowers and their lenders.

Valley Bank faces “more deposit pricing pressure than peers if rates stay higher for longer” and has more commercial real estate exposure than other regionals, Gosalia said in an April 4 note.

Meanwhile, for large banks like JPMorgan, higher rates generally mean they can exploit their funding advantages for longer. They enjoy the benefits of reaping higher interest for things like credit card loans and investments made during a time of elevated rates, while generally paying low rates for deposits.

JPMorgan could raise its 2024 guidance for net interest income by an estimated $2 billion to $3 billion, to $93 billion, according to UBS analyst Erika Najarian.

Large U.S. banks also tend to have more diverse revenue streams than smaller ones from areas like wealth management and investment banking. Both should provide boosts to first-quarter results, thanks to buoyant markets and a rebound in Wall Street activity.

Furthermore, big banks tend to have much lower exposure to commercial real estate compared with smaller players, and have generally higher levels of provisions for loan losses, thanks to tougher regulations on the group.

That difference could prove critical this earnings season.

Concerns over commercial real estate, especially office buildings and multifamily dwellings, have dogged smaller banks since New York Community Bank stunned investors in January with its disclosures of drastically larger loan provisions and broader operational challenges. The bank needed a $1 billion-plus lifeline last month to help steady the firm.

NYCB will likely have to cut its net interest income guidance because of shrinking deposits and margins, according to JPMorgan analyst Steven Alexopoulos.

There is a record $929 billion in commercial real estate loans coming due this year, and roughly one-third of the loans are for more money than the underlying property values, according to advisory firm Newmark.

“I don’t think we’re out of the woods in terms of commercial real estate rearing its ugly head for bank earnings, especially if rates stay higher for longer,” said Matt Stucky, chief portfolio manager for equities at Northwestern Mutual.

“If there’s even a whiff of problems around the credit experience with your commercial lending operation, as was the case with NYCB, you’ve seen how quickly that can get away from you,” he said.

[ad_2]

[ad_1]

Beat Wittman, partner at Porta Advisors, reviews new Swiss banking regulation and its potential impact on UBS in the wake of its absorption of Credit Suisse.

[ad_2]

[ad_1]

Federal Reserve officials at their March meeting expressed concern that inflation wasn’t moving lower quickly enough, though they still expected to cut interest rates at some point this year.

At a meeting in which the Federal Open Market Committee again voted to hold short-term borrowing rates steady, policymakers also showed misgivings that inflation, while easing, wasn’t doing so in a convincing enough fashion. The Fed currently targets its benchmark rate between 5.25%-5.5%

As such, FOMC members voted to keep language in the post-meeting statement that they wouldn’t be cutting rates until they “gained greater confidence” that inflation was on a steady path back to the central bank’s 2% annual target.

“Participants generally noted their uncertainty about the persistence of high inflation and expressed the view that recent data had not increased their confidence that inflation was moving sustainably down to 2 percent,” the minutes stated.

In what apparently was a lengthy discussion about inflation at the meeting, officials cited geopolitical turmoil and rising energy prices as risks to pushing inflation higher. They also cited the potential that looser policy could add to price pressures.

On the downside, they cited a more balanced labor market, enhanced technology along with economic weakness in China and a deteriorating commercial real estate market.

They also discussed higher-than-expected inflation readings in January and February. Chair Jerome Powell said that it’s possible the two months readings were caused by seasonal issues, though he added it’s hard to tell at this point. There were members at the meeting who disagreed.

“Some participants noted that the recent increases in inflation had been relatively broad based and therefore should not be discounted as merely statistical aberrations,” the minutes stated.

That part of the discussion was partly relevant considering the release came the same day that the Fed received more bad news on inflation.

The consumer price index, a popular inflation gauge though not the one the Fed most closely focuses on, showed a 12-month rate of 3.5% in March. That was both above market expectations and represented an increase of 0.3 percentage point from February, giving rise to the idea that hot readings to start the year may not have been an aberration.

Following the CPI release, traders in the fed funds futures market recalibrated their expectations. Market pricing now implies the first rate cut to come in September, for a total of just two this year. Previous to the release, the odds were in favor of the first reduction coming in June, with three total, in line with the “dot plot” projections released after the March meeting.

The discussion at the meeting indicated that “almost all participants judged that it would be appropriate to move policy to a less restrictive stance at some point this year if the economy evolved broadly as they expected,” the minutes stated. “In support of this view, they noted that the disinflation process was continuing along a path that was generally expected to be somewhat uneven.”

In other action at the meeting, officials discussed the possibility of ending the balance sheet reduction. The Fed has shaved about $1.5 trillion off its holdings of Treasurys and mortgage-backed securities by allowing up to $95 billion in proceeds from maturing bonds to roll off each month rather than reinvesting them.

There were no decisions made or indications about how the easing of what has become known as “quantitative tightening” will happen, though the minutes said the roll-off would be cut by “roughly half” from its current pace and the process should start “fairly soon.” Most market economists expect the process to begin in the next month or two.

The minutes noted that members believe a “cautious” approach should be taken.

[ad_2]

[ad_1]

A New York Community Bank stands in Brooklyn on February 08, 2024 in New York City.

Spencer Platt | Getty Images

New York Community Bank, the regional lender that needed a $1 billion-plus lifeline last month, is offering the country’s highest interest rate for a savings account.

NYCB raised the annual percentage yield offered via its online arm, My Banking Direct, to 5.55%, higher than any other bank’s widely available account, according to Ken Tumin, an analyst who tracks rates for his website DepositAccounts.

The standout rate could be a sign that NYCB is facing funding pressure, Tumin said.

“It looks like they’re trying really hard to attract deposits,” Tumin said. “My Banking Direct has been around for a long time, more than 10 years, so them having an aggressive rate could be a sign of neediness” for funding.

NYCB’s woes began in January, when it said it was preparing for far greater losses on commercial real estate loans than analysts had expected. That set off a downward spiral in its stock price, downgrades from rating agencies and multiple management changes. The bank announced a capital injection from investors led by former Treasury Secretary Steven Mnuchin’s Liberty Strategic Capital on March 6.

In the month before the rescue was announced, NYCB shed 7% of its deposits, falling to $77.2 billion by March 5, the bank said in a presentation.

During a conference call held after the capital raise, analysts asked how NYCB managed to retain so much of its deposits during the tumultuous period.

“We didn’t do anything crazy relative to deposit pricing,” NYCB chairman Sandro DiNello replied. “We didn’t go out and offer 6% CDs or something like that in order to make the numbers look good, if that’s what you’re concerned with.”

NYCB didn’t return a call for comment on its funding strategy.

Joseph Otting, a former comptroller of the currency, took over as the bank’s CEO on April 1, about a week before the rate increase.

Despite the turnaround plan, shares of NYCB still trade for under $4 apiece and are off more than 68% year to date.

Other banks offering rates higher than 5% right now tend to be newer or smaller players than NYCB, according to Tumin.

Among established banks, the average high-yield savings rate is about 4.4%, and several of them (including American Express, Goldman Sachs and Ally) have dropped rates in the past month, he said. The NYCB rate also tops accounts listed on NerdWallet and Bankrate.

Customer deposits at My Banking Direct are insured by the FDIC up to the standard $250,000.

Over the past two years, savings account rates have broadly been on the rise.

Since the regional banking crisis consumed Silicon Valley Bank and First Republic last year, smaller players have been forced to pay higher rates for deposits compared to giants like JPMorgan Chase in order to compete, said Matt Stucky, chief portfolio manager for equities at Northwestern Mutual.

“When a bank has to go out and advertise a much higher rate, it’s typically because they have a deposit problem,” Stucky said. “It’s not hard for customers to switch banks anymore.”

[ad_2]

[ad_1]

Jamie Dimon, CEO of JPMorgan Chase, testifies during the Senate Banking, Housing and Urban Affairs Committee hearing titled Annual Oversight of Wall Street Firms, in the Hart Building on Dec. 6, 2023.

Tom Williams | Cq-roll Call, Inc. | Getty Images

Jamie Dimon, the veteran CEO and chairman of JPMorgan Chase, said he was convinced that artificial intelligence will have a profound impact on society.

In his annual letter to shareholders released Monday, Dimon chose AI as the first topic in his update of issues facing the biggest U.S. bank by assets — ahead of geopolitical risks, recent acquisitions and regulatory matters.

“While we do not know the full effect or the precise rate at which AI will change our business — or how it will affect society at large — we are completely convinced the consequences will be extraordinary,” Dimon said.

The impact will be “possibly as transformational as some of the major technological inventions of the past several hundred years: Think the printing press, the steam engine, electricity, computing and the Internet.”

Dimon’s letter, read widely in the business world because of his status as one of the most successful leaders in finance, hit a wide variety of topics. The CEO said that he had ongoing concerns about inflationary pressures and reiterated his warning that the world may be entering the riskiest era in geopolitics since World War II.

But his focus on AI, first mentioned in Dimon’s annual letter in 2017, stood out. The technology, which has gained in prominence since ChatGPT became a viral sensation in late 2022, can generate human-sounding responses to queries. Enthusiasm for AI has fueled the meteoric rise in chipmaker Nvidia and helped propel tech names to new heights.

JPMorgan now has more than 2,000 AI and machine learning employees and data scientists working on 400 applications including fraud detection, marketing and risk controls, Dimon said. The bank is also exploring the use of generative AI in software engineering, customer service and ways to boost employee productivity, he said.

The technology could ultimately touch all of the bank’s roughly 310,000 employees, assisting some workers while replacing others, and forcing the company to retrain workers for new roles.

“Over time, we anticipate that our use of AI has the potential to augment virtually every job, as well as impact our workforce composition,” Dimon said. “It may reduce certain job categories or roles, but it may create others as well.”

Here are excerpts from Dimon’s letter:

“Many key economic indicators today continue to be good and possibly improving, including inflation. But when looking ahead to tomorrow, conditions that will affect the future should be considered… All of the following factors appear to be inflationary: ongoing fiscal spending, remilitarization of the world, restructuring of global trade, capital needs of the new green economy, and possibly higher energy costs in the future (even though there currently is an oversupply of gas and plentiful spare capacity in oil) due to a lack of needed investment in the energy infrastructure.”

“Equity values, by most measures, are at the high end of the valuation range, and credit spreads are extremely tight. These markets seem to be pricing in at a 70% to 80% chance of a soft landing — modest growth along with declining inflation and interest rates. I believe the odds are a lot lower than that.”

“If long-end rates go up over 6% and this increase is accompanied by a recession, there will be plenty of stress — not just in the banking system but with leveraged companies and others. Remember, a simple 2 percentage point increase in rates essentially reduced the value of most financial assets by 20%, and certain real estate assets, specifically office real estate, may be worth even less due to the effects of recession and higher vacancies. Also remember that credit spreads tend to widen, sometimes dramatically, in a recession.”

“There is little real collaboration between practitioners — the banks — and regulators, who generally have not been practitioners in business…. Unfortunately, without collaboration and sufficient analysis, it is hard to be confident that regulation will accomplish desired outcomes without undesirable consequences. Instead of constantly improving the system, we may be making it worse.”

“Russia’s invasion of Ukraine and the subsequent abhorrent attack on Israel and ongoing violence in the Middle East should have punctured many assumptions about the direction of future safety and security, bringing us to this pivotal time in history. America and the free Western world can no longer maintain a false sense of security based on the illusion that dictatorships and oppressive nations won’t use their economic and military powers to advance their aims — particularly against what they perceive as weak, incompetent and disorganized Western democracies. In a troubled world, we are reminded that national security is and always will be paramount, even if its importance seems to recede in tranquil times.”

“One common sense and modest step would be for social media companies to further empower platform users’ control over what they see and how it is presented, leveraging existing tools and features — like the alternative feed algorithm settings some offer today. I believe many users (not just parents) would appreciate a greater ability to more carefully curate their feeds; for example, prioritizing educational content for their children.”

“The acquisition of a major company entails a lot of complexity. People tend to focus on the financial and economic outcomes, which is a reasonable thing to do. And in the case of First Republic, the numbers look rather good. We recorded an accounting gain of $3 billion on the purchase, and we told the world we expected to add more than $500 million to earnings annually, which we now believe will be closer to $2 billion.”

JPMorgan acquired most of the assets of First Republic last year for more than $10 billion after regulators seized the firm amid the regional banking crisis.

[ad_2]

[ad_1]

The mammoth integration of failed bank Credit Suisse into its former rival UBS will act as a “case study,” UBS CEO Sergio Ermotti said Friday, one that will show that big bank mergers should be allowed.

“It’s going to be a case study to be evaluated globally, but also particularly in Europe, where eventually the necessity of creating stronger banks, and stronger and more competitive banks from a global standpoint of view, is in my point of view a necessity,” Ermotti told CNBC’s Steve Sedgwick at an event at the Ambrosetti Spring Forum in Italy.

“Of course, we can’t just rely on a crisis to create or facilitate the merger of banks,” Ermotti said.

“It’s good to have strong players that can be part of the solution, like UBS was in the Credit Suisse case. … But it cannot be just that part. So in that sense, I think that the real issue is, there has to be a political desire to facilitate something like that. So it’s not the reality of today,” he added.

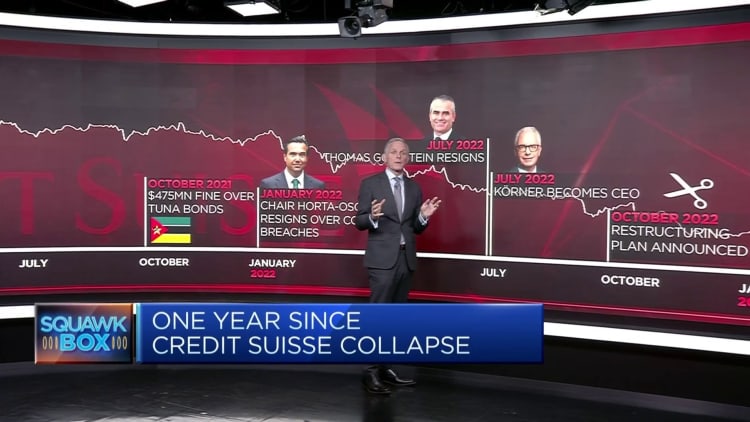

Credit Suisse collapsed in March 2023 after years of underperformance, scandals and risk management crises. UBS in June completed its takeover of the 167-year-old bank in a deal controversially brokered by Swiss authorities.

The Swiss National Bank has said the size of the new entity flags potential competition issues that will need to be monitored.

Ermotti said Friday, “The good news is that, in my view, in many countries, there is a recognition that they want to protect their banks or financial institutions as national champions, which is an implied or explicit recognition of their value for their economies.”

“But the bad news is that they don’t realize that in order to really be meaningful, and go to the next level of their contribution in their economies, they will need to be also more competitive globally. But without a banking union, without a capital markets union, it’s going to be very, very difficult for Europe to compete with U.S. large banks.”

Unlike in the U.S., European economies continue to rely on the banking sector for business financing; and Europe has a “completely different playing field and a lack of critical mass,” Ermotti said.

“So I hope, I’m not so convinced it’s going to happen soon, but I hope eventually one day those kinds of mergers between big banks will be allowed and we can contribute to that by showing that it’s possible. In the meantime, I think that in many countries, critical mass and synergies can be created by further rounds of local mergers,” he said.

[ad_2]

[ad_1]

UBS logo is seen at the office building in Krakow, Poland on February 22, 2024.

Jakub Porzycki | Nurphoto | Getty Images

UBS on Tuesday announced a new share repurchase program of up to $2 billion, with up to $1 billion of that total expected to take place this year.

“As previously communicated, in 2024 we expect to repurchase up to USD 1bn of our shares, commencing after the completion of the merger of UBS AG and Credit Suisse AG which is expected to occur by the end of the second quarter,” the bank said in a statement.

“Our ambition is for share repurchases to exceed our pre-acquisition level by 2026.”

The new program follows the completion of the 2022 buyback, during which 298.5 million of it shares were purchased. This represented 8.62% of its stock worth $5.2 billion, according to UBS.

The bank’s 2022 share repurchase program concluded last month.

Buybacks take place when firms purchase their own shares on the stock exchange, reducing the portion of shares in the hands of investors. They offer a way for companies to return cash to shareholders — along with dividends — and usually coincide with a company’s stock moving higher, as shares get scarcer.

UBS has undertaken the mammoth task of integrating Credit Suisse’s business, after announcing in late March 2023 that former chief Sergio Ermotti would return for a second spell as CEO.

Figures last week showed that Ermotti earned 14.4 million Swiss francs ($15.9 million) in 2023, following his surprise return. The bank in February reported a second consecutive quarterly loss on the back of integration costs, but continued to deliver strong underlying operating profits.

Shares are up more than 6% so far this year.

— CNBC’s Elliot Smith contributed to this article.

[ad_2]

[ad_1]

NVIDIA’s founder and CEO Jensen Huang speaks during the annual Nvidia GTC Artificial Intelligence Conference at SAP Center in San Jose, California, on March 18, 2024.

Josh Edelson | Afp | Getty Images

This week’s strong market pushed three of our portfolio stocks well clear of our current price targets. Since these rallies look like they have legs, we’re taking our numbers up.

[ad_2]