According to a report by the global investment bank Morgan Stanley, signs indicate that the cyclical “crypto winter” bear market, which has plagued the cryptocurrency industry, may finally end.

The report explores the historical pattern of Bitcoin’s (BTC) performance following halving events that occur approximately every four years. Furthermore, the report estimates that the next halving event could occur around April 2024.

The Cyclical Nature Of Crypto Markets

Per the report, Bitcoin, the dominant cryptocurrency, is a barometer for the overall crypto market. One distinctive feature of Bitcoin is its halving process, which creates scarcity and helps maintain its value.

Every four years, the number of BTC generated every 10 minutes is halved. This deliberate reduction in supply has historically affected Bitcoin’s price, often triggering a bullish market rally.

Previous cycles have witnessed three notable bull runs that lasted 12 to 18 months after each halving event.

The four-year cryptocurrency cycle aligns with the seasons, providing a framework to understand market behavior:

According to Morgan Stanley, summer represents the phase immediately following a halving event, during which Bitcoin’s price gains are typically observed until it reaches a new peak.

Fall signifies when Bitcoin surpasses its previous high, attracting media attention, new investors, and businesses. This phase indicates that the bull market is nearing its end.

Winter characterizes the bear-market decline, initiated by profit-taking and selling pressure from investors, resulting in price drops. This phase persists until the next market trough, typically around 13 months.

Spring is the phase leading up to the next halving event, during which Bitcoin’s price generally recovers from the cycle’s low point. However, investor interest tends to remain relatively weak during this period.

Gauging Indicators To Ascertain The Transition From Winter To Spring

Determining whether crypto spring has truly arrived requires considering several factors. These include the time elapsed since the last peak, the magnitude of Bitcoin’s drawdown from its high, miner capitulation, the Bitcoin price-to-thermocap multiple, exchange-related issues, and price action.

These indicators can provide insights into whether the market has reached a trough or is still experiencing crypto winter.

While the report suggests that crypto winter may be in the past and crypto spring is on the horizon, it emphasizes the importance of learning more about the crypto market’s cyclical tendencies.

The daily chart shows BTC’s sideways price action over the past 24 hours. Source: BTCUSDT on TradingView.com

BTC is trading at $28,500, showing a modest recovery in the past 24 hours after an unsuccessful attempt to stabilize above $30,000 on Monday, followed by a subsequent decline to the $28,000.

Notwithstanding this recent volatility, Bitcoin has maintained substantial gains across various time frames. It has experienced a notable surge of 7.4% over the past seven days, 4% over the past fourteen days, 5% over the past thirty days, and an impressive 49% surge over one year.

Featured image from Shutterstock, chart from TradingView.com

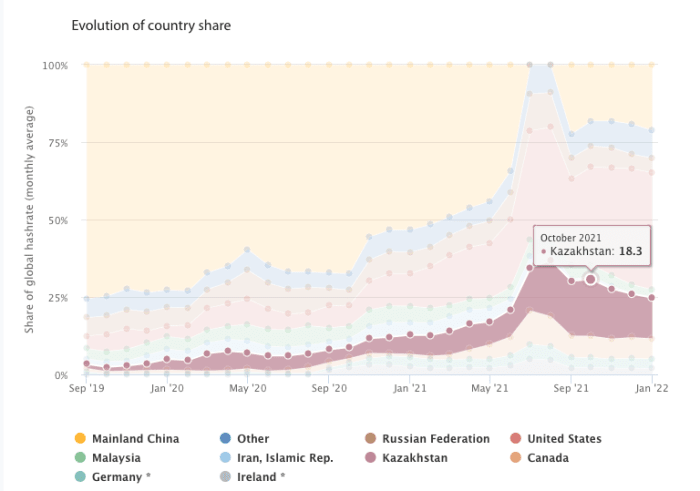

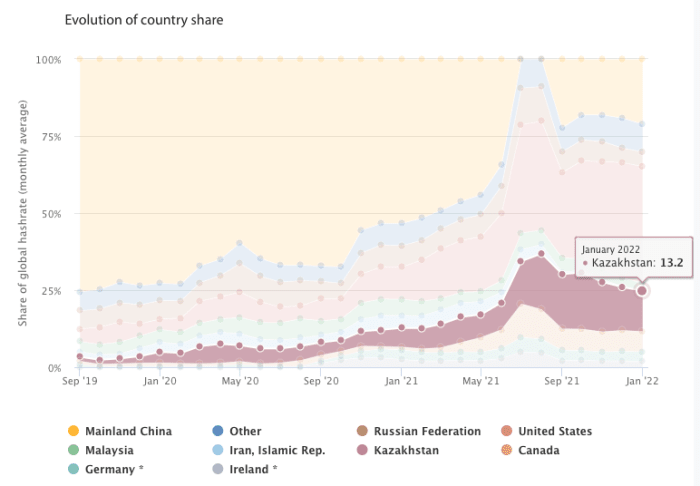

Kazakhstan was, at its height, the second-largest Bitcoin mining nation on earth. Then, within a year, it capitulated. While mainstream news commentators were quick to pick through the reasons for why Kazakh authorities turned against Bitcoin mining operations, the consequence this had on the greening of the network went unreported.

But because Kazakhstan is fuelled 87.6% by fossil fuel, less mining there means a higher clean energy mix for the Bitcoin network.

How much higher?

That’s what I asked myself. And the answer I found was surprising.Source

But what has not been widely reported is that by January 2022 (the last time Cambridge University updated its Bitcoin mining map), it had already fallen to 13.2% of global hash rate.

The regulated curtailment of mining. Bitcoin mining can now only legally occur at the off-peak hours of midnight to 8:00 a.m. and on weekends: a reduction from 168 mining hours per week to only 64 mining hours per week.

Running some calculations, even at the most bullish upper threshold, Kazakhstan now represents at best 6.4% of global hash rate.

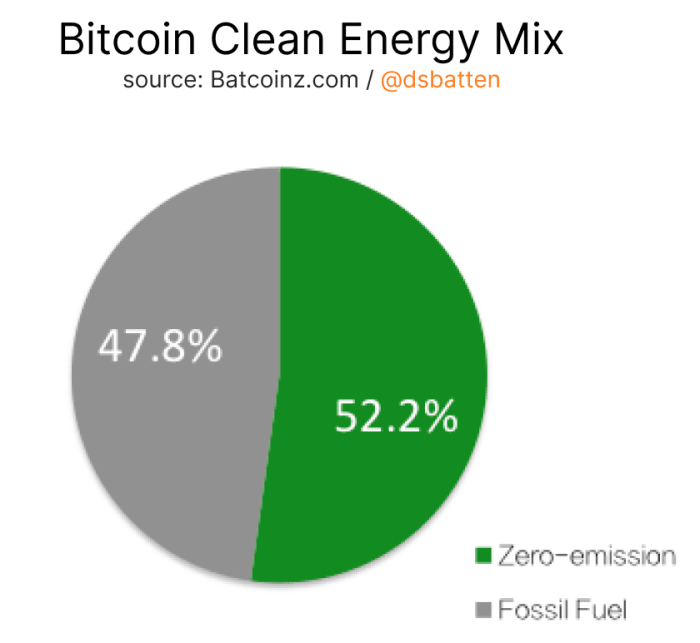

So, what does this mean for Bitcoin’s clean energy mix?

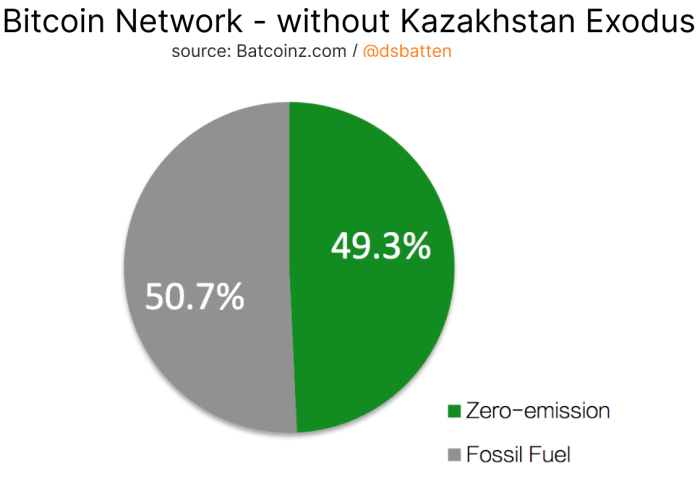

It makes a pretty significant difference, as you can see. The exodus from Kazakhstan flipped the network to become a majority clean-energy user. I ran a simulation on my energy source model with Kazakhstan still at 18.3% of global hash rate. Here’s what that would have looked like: majority fossil fuel use.

Because Kazakhstan uses so much coal (a much heavier greenhouse-gas emitter than natural gas) the difference to emissions is even more significant. At 18.3% of total hash rate, Bitcoin emissions would’ve been 36 metric tons of carbon dioxide equivalent C(MTCO2e). But at current levels, emissions are only 32.4 MtCO2e. That’s a 10% reduction in emissions.

Ten percent emission reduction is significant. There are few industries in the world that have achieved this within a year. And if there were, you would likely have heard all about it.

An important sidenote: Have you ever seen a Bitcoin mining unit with its own internal combustion engine? Neither have I. Bitcoin mining, like electric vehicles (EVs), uses electricity as its power source. As such, if an EV can claim to be zero emissions, then so can Bitcoin mining. So, when we talk about emission, we are talking about the indirect emissions caused by the component of electricity that was generated using fossil fuels.

In summary: The Bitcoin network keeps tracking in the right direction, but you have to dig to find this out.

And some final thoughts on where we are heading:

According to my model, the Bitcoin network uses 4.7% more clean energy now than it did even just a year ago. The factors that have led to this are:

The below is an excerpt from a recent year-ahead report written by the Bitcoin Magazine PRO analysts. Download the entire report here.

Bitcoin Magazine PRO sees incredibly strong fundamentals in the Bitcoin network and we are laser-focused on its market dynamic in the context of macroeconomic trends. Bitcoin aims to become the world reserve currency, an investment opportunity that cannot be understated.

In our year-ahead report, we analyzed seven notable factors that we recommend investors pay attention to in the coming months.

Convicted Bitcoin Investors

We can put investor conviction into perspective by looking at the number of unique Bitcoin addresses holding at least 0.01, 0.1 and 1 bitcoin. This data shows that bitcoin adoption continues to grow with a growing number of unique addresses holding at least these amounts of bitcoin. While it is entirely possible for individual users to hold their bitcoin in multiple addresses, the growth of unique Bitcoin addresses holding at least 0.01, 0.1 and 1 bitcoin indicate that more users than ever before are buying bitcoin and holding it in self-custody.

Unique bitcoin addresses continues to grow across the board.

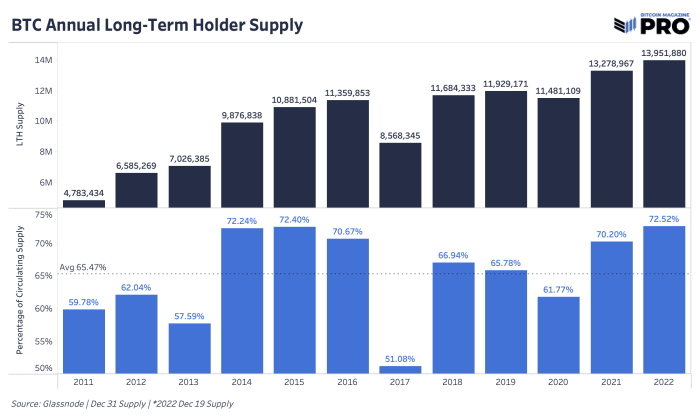

Another promising metric is the amount held by long-term holders, which has increased to almost 14 million bitcoin. Long-term holder supply is calculated using a threshold of a 155-day holding period, after which dormant coins become increasingly unlikely to be spent. As of now, 72.49% of the bitcoin in circulation is not likely to be sold at these prices.

Long-term holder supply reached 72.52% of the circulating bitcoin supply.

There is a large subset of bitcoin investors who are accumulating the digital asset no matter the price. In a December 2022 interview on “Going Digital,” Head of Market Research Dylan LeClair said, “You have people all over the world that are acquiring this asset and you have a huge and growing cohort of people that are price-agnostic accumulators.”

With a growing number of unique addresses holding bitcoin and such a significant amount of bitcoin being held by long-term investors, we are optimistic for bitcoin’s advancement and rate of adoption. There are many variables that demonstrate the potential for asymmetric returns as demand for bitcoin increases and adoption increases worldwide.

Total Addressable Market

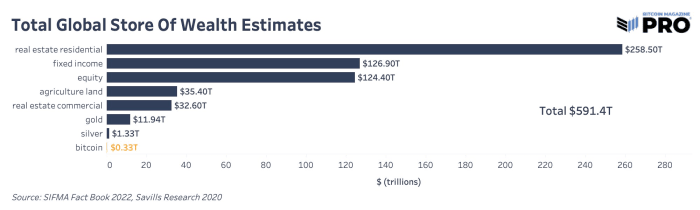

During monetization, a currency goes through three phases in order: store of value, medium of exchange and unit of account. Bitcoin is currently in its store-of-value phase as demonstrated by the long-term holder metrics above. Other assets that are frequently used as stores of value are real estate, gold and equities. Bitcoin is a better store of value for many reasons: it is more liquid, easier to access, transport and secure, easier to audit and more finitely scarce than any other asset with its hard-cap limit of 21 million coins. For bitcoin to acquire a larger share of other global stores of value, these properties need to remain intact and prove themselves in the eyes of investors.

Estimations of global stores of wealth.

As readers can see, bitcoin is a tiny fraction of global wealth. Should bitcoin take even a 1% share from these other stores of value, the market cap would be $5.9 trillion, putting bitcoin at over $300,000 per coin. These are conservative numbers from our viewpoint because we estimate that bitcoin adoption will happen gradually, and then suddenly.

Transfer Volume

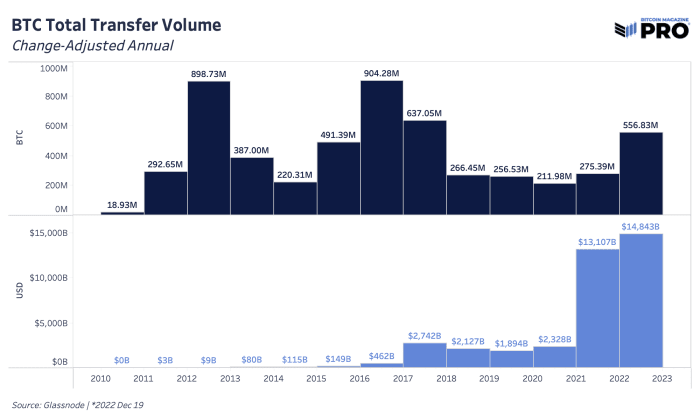

When looking at the amount of value that was cleared on the Bitcoin network throughout its history, there is a clear upward trend in USD terms with a heightened demand for transferring bitcoin this year. In 2022, there was a change-adjusted transfer volume of over 556 million bitcoin settled on the Bitcoin network, up 102% from 2021. In USD terms, the Bitcoin network settled just shy of $15 trillion in value in 2022.

Bitcoin transfer volume was higher than ever in USD terms.

Bitcoin’s censorship resistance is an extremely valuable feature as the world enters into a period of deglobalization. With a market capitalization of only $324 billion, we believe bitcoin is severely undervalued. Despite the drop in price, the Bitcoin network transferred more value in USD terms than ever before.

Rare Opportunity In Bitcoin’s Price

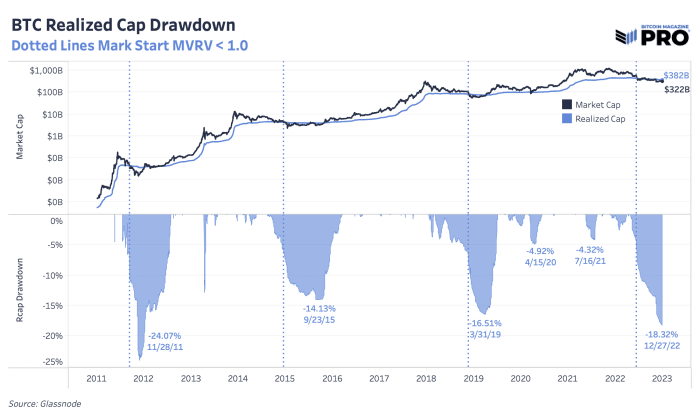

By looking at certain metrics, we can analyze the unique opportunity investors have to purchase bitcoin at these prices. The bitcoin realized market cap is down 18.8% from all-time highs, which is the second-largest drawdown in its history. While the macroeconomic factors are something to keep in mind, we believe that this is a rare buying opportunity.

The realized cap drawdown in 2022 was the second largest in bitcoin’s history.

Relative to its history, bitcoin is at the phase of the cycle where it’s about as cheap as it gets. Its current market exchange rate is approximately 20% lower than its average cost basis on-chain, which has only happened at or near the local bottom of bitcoin market cycles.

Current prices of bitcoin are in rare territory for investors looking to get in at a low exchange rate. Historically, purchasing bitcoin during these times has brought tremendous returns in the long term. With that said, readers should consider the reality that 2023 likely brings about bitcoin’s first experience with a prolonged economic recession.

Macroeconomic Environment

As we move into 2023, it’s necessary to recognize the state of the geopolitical landscape because macro is the driving force behind economic growth. People around the world are experiencing a monetary policy lag effect from last year’s central bank decisions. The U.S. and EU are in recessionary territory, China is proceeding to de-dollarize and the Bank of Japan raised its target rate for yield curve control. All of these have a large influence on capital markets.

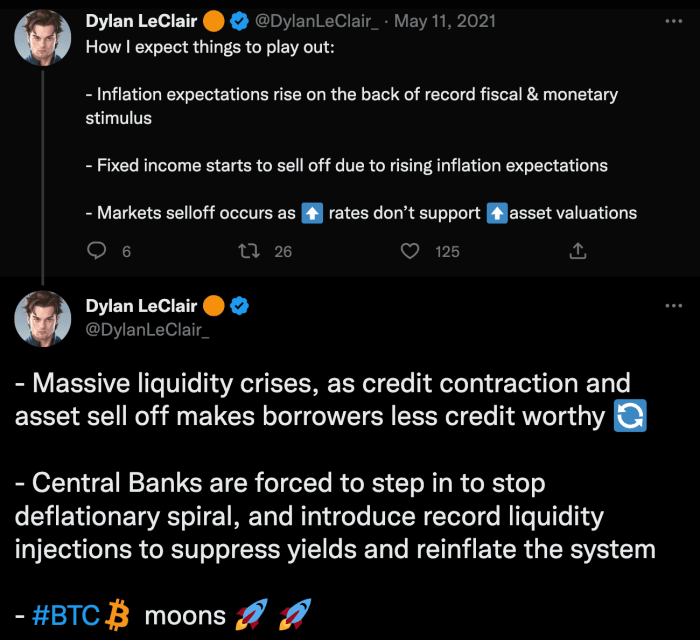

Nothing in financial markets occurs in a vacuum. Bitcoin’s ascent through 2020 and 2021 — while similar to previous crypto-native market cycles — was very much tied to the explosion of liquidity sloshing around the financial system after COVID. While 2020 and 2021 was characterized by the insertion of additional liquidity, 2022 has been characterized by the removal of liquidity.

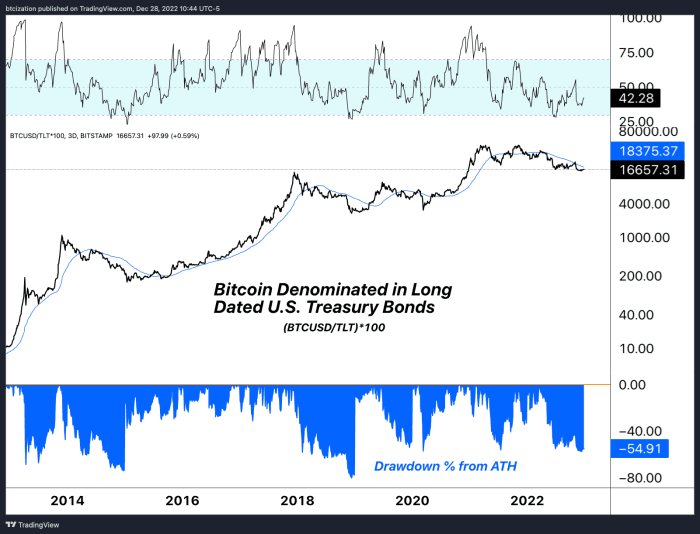

Interestingly enough, when denominating bitcoin against U.S. Treasury bonds (which we believe to be bitcoin’s largest theoretical competitor for monetary value over the long term), comparing the drawdown during 2022 was rather benign compared to drawdowns in bitcoin’s history.

As we wrote in “The Everything Bubble: Markets At A Crossroads,” “Despite the recent bounce in stocks and bonds, we aren’t convinced that we have seen the worst of the deflationary pressures from the global liquidity cycle.”

In “The Bank of Japan Blinks And Markets Tremble,” we noted, “As we continue to refer to the sovereign debt bubble, readers should understand what this dramatic upward repricing in global yields means for asset prices. As bond yields remain at elevated levels far above recent years, asset valuations based on discounted cash flows fall.” Bitcoin does not rely on cash flows, but it will certainly be impacted by this repricing of global yields. We believe we are currently at the third bullet point of the following playing out:

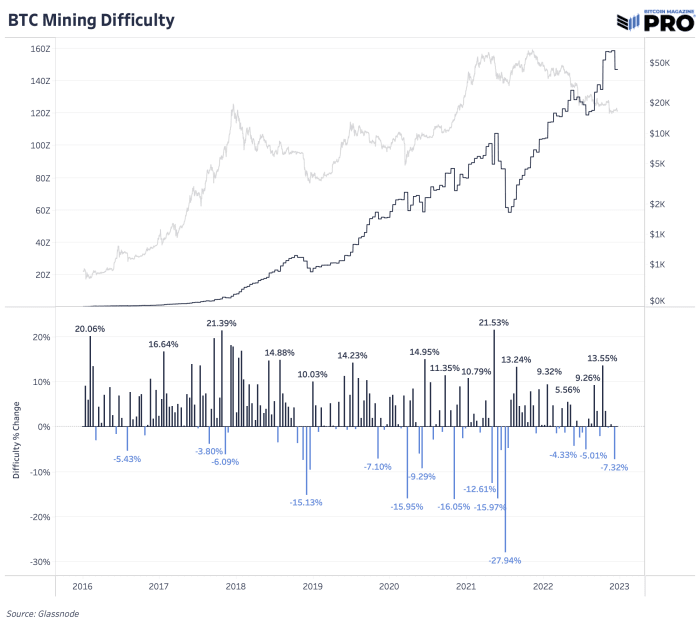

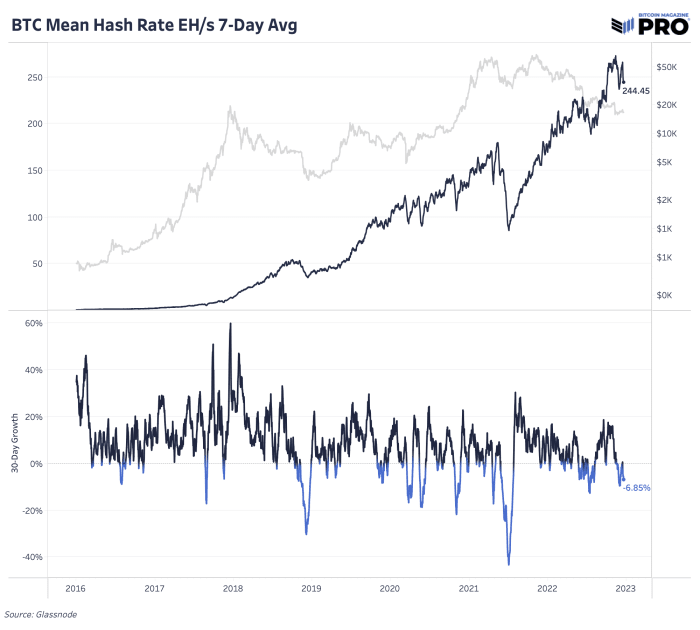

While the multitude of negative industry and worrying macroeconomic factors have had a major dampening on bitcoin’s price, looking at the metrics of the Bitcoin network itself tell another story. The hash rate and mining difficulty gives a glimpse into how many ASICs are dedicating hashing power to the network and how competitive it is to mine bitcoin. These numbers move in tandem and both have almost exclusively gone up in 2022, despite the significant drop in price.

Bitcoin mining difficulty continues to rise.

Bitcoin hash rate continues to rise.

By deploying more machines and investing in expanded infrastructure, bitcoin miners demonstrate that they are more bullish than ever. The last time the bitcoin price was in a similar range in 2017, the network hash rate was one-fifth of current levels. This means that there has been a fivefold increase in bitcoin mining machines being plugged in and efficiency upgrades to the machines themselves, not to mention the major investments in facilities and data centers to house the equipment.

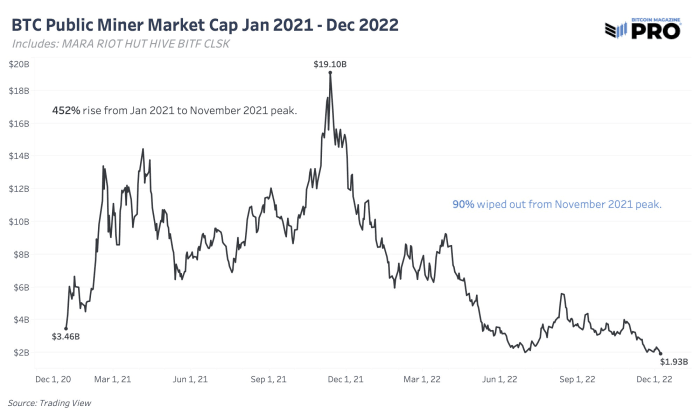

Because the hash rate increased while the bitcoin price decreased, miner revenue took a beating this year after a euphoric rise in 2021. Public miner stock valuations followed the same path with valuations falling even more than the bitcoin price, all while the Bitcoin network’s hash rate continued to rise. In the “State Of The Mining Industry: Survival Of The Fittest,” we looked at the total market capitalization of public miners which fell by over 90% since January 2021.

The market cap of all public mining equities has dropped by 9

We expect more of these companies to face challenging conditions because of the skyrocketing global energy prices and interest rates mentioned above.

Increasing Scarcity

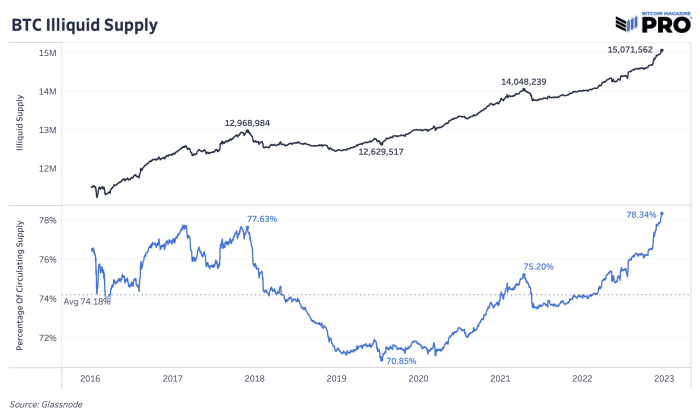

One way to analyze bitcoin’s scarcity is by looking at the illiquid supply of coins. Liquidity is quantified as the extent to which an entity spends their bitcoin. Someone that never sells has a liquidity value of 0 whereas someone who buys and sells bitcoin all the time has a value of 1. With this quantification, circulating supply can be broken down into three categories: highly liquid, liquid and illiquid supply.

Illiquid supply is defined as entities that hold over 75% of the bitcoin they deposit to an address. Highly liquid supply is defined as entities that hold less than 25%. Liquid supply is between the two. This illiquid supply quantification and analysis was developed by Rafael Schultze-Kraft, co-founder and CTO of Glassnode.

Bitcoin’s illiquid supply continues to grow.

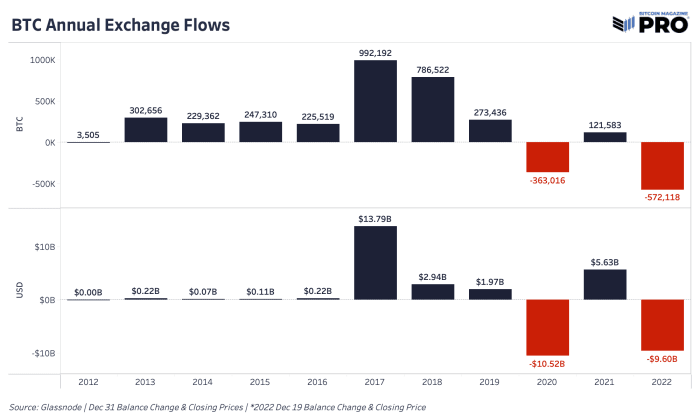

2022 was the year of getting bitcoin off exchanges. Every recent major panic became a catalyst for more individuals and institutions to move coins into their own custody, find custody solutions outside of exchanges or sell off their bitcoin entirely. When centralized institutions and counterparty risks are flashing red, people rush for the exit. We can see some of this behavior through bitcoin outflows from exchanges.

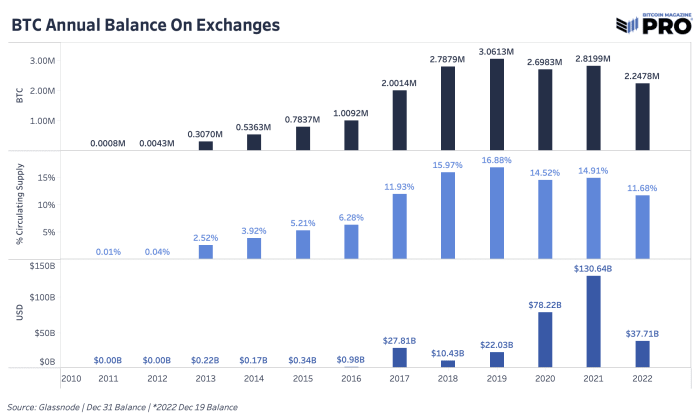

In 2022, 572,118 bitcoin worth $9.6 billion left exchanges, marking it the largest annual outflow of bitcoin in BTC terms in history. In USD terms, it was second only to 2020, which was driven by the March 2020 COVID crash. 11.68% of bitcoin supply is now estimated to be on exchanges, down from 16.88% back in 2019.

Exchanges saw a massive decrease in the bitcoin balances on their platforms.

Bitcoin balance on exchanges decreased in 2022.

These metrics of an increasingly illiquid supply paired with historic amounts of bitcoin being withdrawn from exchanges — ostensibly being removed from the market — paint a different picture than what we’re seeing with the factors outside of the Bitcoin network’s purview. While there are unanswered questions from a macroeconomic perspective, bitcoin miners continue to invest in equipment and on-chain data shows that bitcoin holders aren’t planning to relinquish their bitcoin anytime soon.

Conclusion

The varying factors detailed above give a picture for why we are long-term bullish on the bitcoin price going into 2023. The Bitcoin network continues to add another block approximately every 10 minutes, more miners keep investing in infrastructure by plugging in machines and long-term holders are unwavering in their conviction, as shown by on-chain data.

With bitcoin’s ever-increasing scarcity, the supply side of this equation is fixed, while demand is likely to increase. Bitcoin investors can get ahead of the demand curve by averaging in while the price is low. It’s important for investors to take the time to learn how Bitcoin works to fully understand what it is they are investing in. Bitcoin is the first digitally native and finitely scarce bearer asset. We recommend readers learn about self-custody and withdraw their bitcoin from exchanges. Despite the negative news cycle and drop in bitcoin price, our bullish conviction for bitcoin’s long-term value proposition remains unfazed.

North America became the leading hub of bitcoin mining activity after China’s abrupt ban in May 2021. While the United States has grabbed most of the news headlines and a significant portion of investor attention, Canada has also solidified its role as a global leader in mining. From industrial mining farms to off-grid guerrilla mining operations, Canada is home to miners of all stripes.

But the final months of 2022 saw several provinces target bitcoin miners and suspend any new grid connections while “environmental assessments” were initiated. This article provides an overview of the localized changes in regulatory posture toward miners.

Mining Regulations In Canada

In late 2022, Hydro-Quebec announced its proposal for the province to stop selling cheap power to cryptocurrency miners, as reported by The Wall Street Journal. The proposal called for the Canada Energy Regulator to suspend the allocation of 270 megawatts requested by cryptocurrency miners. Bitcoin miners in Quebec already recognize that local regulations are too restrictive for easy growth, but this new proposal could make mining in the province even harder.

Right after Thanksgiving, Manitoba announced its plans to halt any new electric grid connections for cryptocurrency mining operations. The suspension will last 18 months from November 2022 to allow for a review of the externalities from the mining industry’s energy demands, according to the province’s finance minister. The 37 currently-operating mining facilities in Manitoba will not be affected for now. But recent requests for new connections from 17 different operators have been suspended, according to CBC.

Just before Christmas, British Columbia made headlines for its efforts to stop mining growth to assess the environmental impacts of cryptocurrency mining operations. An 18-month moratorium has been placed on accepting any new requests for electrical grid connections exclusively from bitcoin mining companies. The province said at the time that 21 applications that were pending approval have been suspended. Assessing how bitcoin mining affects the province’s “environmental goals” is the stated reason for B.C.’s 18-month suspension.

Before these grid connection limitations, Canada had long stood as a global hub for cryptocurrency growth generally and bitcoin mining activity in particular, with a loose estimate of 7% of global hash rate operating within its borders. But several localities are starting to make miners feel not so welcome. Two is a coincidence, three is a trend, as the adage says.

All the way at the top of the Canadian government, the current prime minister, Justin Trudeau, has made it no secret that he frowns on the entire cryptocurrency industry. After his conservative counterpart Pierre Poilievre voiced strong support for Bitcoin, Trudeau wasted no time firing back by calling his rival’s views “irresponsible” and cryptocurrency “volatile.” From his personal Twitter, however, Trudeau has never tweeted about crypto, bitcoin or mining.

The Canadian Mining Landscape

Mining discourse generally references “North America” collectively or “the U.S.” individually. But Canada plays a significant role in bolstering the hash rate staying online across the North American region. And, for the most part, Canadian miners endure much harsher climates than their southern counterparts. For example, Upstream Data CEO Steve Barbour shared pictures on Twitter of the underappreciated, destructive effects of harsh Canadian weather on bitcoin mining operations. Frozen cables, iced hardware and large snow drifts do not make for ideal mining conditions.

But some of the most well-known public and private mining companies operate or are headquartered in Canada. For publicly-traded firms, the list includes Bitfarms, SATO Technologies, Hut 8 and more. The roster of private companies based or operating in Canada includes Compass Mining, Bitfury, Upstream Data and others. Nearly all of these brands are quasi-household names in the bitcoin economy and often play key roles in advocating for and educating about Bitcoin. Canada’s footprint in the bitcoin market is not small.

Reacting To Regulatory Changes

Local hostility to operational bitcoin mining expansions may be recent news in Canada, but the broader industry is no stranger to this sentiment. The entire industry banded together to vociferously oppose a proposed two-year moratorium in New York for fossil-fuel-powered mining expansion projects. In late November 2022, the bill passed. The move was cheered by other left-leaning politicians. And Canada seems to be copying their playbook.

Canada’s new posture toward miners also imitates another international mining hotspot: Kazakhstan. After absorbing an abundance of mining activity that left China, Kazakhstan started proposing power consumption limitations for new mining activity in October 2021.

So, how are Canadian miners reacting?

News of Quebec’s proposal to suspend any new grid connections was widely shared among Bitcoin social circles on Twitter. Unsurprisingly, the chatter was uniformly negative and critical.

Upstream Data’s Barbour was not altogether shocked, though. Taking to Twitter, he noted that Quebec is “once again” censoring bitcoin miners. Why are the proposed grid connection limitations unsurprising? Because miners “compete with utilities,” according to Barbour.

“Expect increasing discrimination,” he tweeted.

Despite changing regulatory sentiment, some of Canada’s biggest miners still plan to expand. Bitfarms said it “continues to look to expand its operations in Québec and add more jobs across the region” in a press release published shortly after news of Hydro-Quebec’s proposal broke. Quantifying Bitfarm’s impact on the local economy, the press release added, “Bitfarms has invested over CAD$350 million in Québec since its inception and currently employs over 100 employees.”

Canada’s Choice

Political favor or hostility toward Bitcoin ultimately means very little for the long-term success of the network. In the short term, however, regulatory limitations can make life very difficult for mining companies trying to process transactions and find new blocks. Any regulatory opposition from Canada is highly unlikely to rival China’s all-out ban from 2021. But multiple localities suspending all new requests for grid connections is extremely disruptive all the same.

Canadian provinces now face a choice: risk losing hash rate to other jurisdictions or embrace mining and the heavily-documented socioeconomic benefits it affords.

This is a guest post by Zack Voell. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

“Contagion” is the most popular word in crypto after the disastrous fallout of the past year. And dominos keep falling as investors painfully realize how closely intertwined the entire cryptocurrency industry is. Hundreds of billions of dollars were incinerated.

And bitcoin mining companies have not completely avoided this. In fact, a unique type of mining business failed catastrophically, which could provide valuable lessons for future entrepreneurs. The combination of crypto lending and crypto mining was showcased in two high-profile companies: BlockFi and Celsius. Both of these companies are now bankrupt. What happened?

This article explores the histories, downfalls and lessons of both organizations.

The Crypto Lending Businesses’ Mining Interests

Even the most casual crypto observer would be familiar with the two industry-leading crypto lending businesses that went bust in 2022. What may be less widely known is that both of these companies also maintained significant bitcoin mining units. BlockFi and Celsius were not only the go-to names for centralized crypto lending, they also heavily invested in bitcoin mining. And when both companies sank, so did their mining teams.

BlockFi announced its new mining operations in May 2021 in the form of a partnership with Blockstream and its long-standing mining unit. Exactly how much hash rate BlockFi is managing through Blockstream has not been disclosed, and the current status of BlockFi’s hash rate at Blockstream facilities is also not fully known. But the lending company said it viewed mining as a complement to its financial service offerings.

Celsius also invested heavily in bitcoin mining, with $500 million spent on its mining efforts as of November 2021. In an older interview, former Celsius CEO Alex Mashinsky said the company operated 22,000 mining machines, most of which were Antminer S19 models. Like BlockFi, Mashinsky described his company’s mining efforts as a strategic complement to its lending business.

To be clear, BlockFi and Celsius were not the only companies operating at the intersection of mining and lending. Mining companies lending their coins to other institutional market participants (e.g., trading firms) is not uncommon. And it’s not unreasonable to assume other, smaller lending firms also had exposure to the mining industry. But BlockFi and Celsius were unparalleled in the combined scale of both their lending and mining operations. Both companies were also bankrupted as a direct result of the fallout from the stunning collapse of FTX.

Tale Of Two Bankruptcies

Both companies — Celsius and BlockFi — have now filed for bankruptcy.

In June 2022, Celsius announced it was pausing all withdrawals. The next month, the company filed for Chapter 11 bankruptcy. Machinsky abruptly resigned in the middle of the bankruptcy proceedings but not before reportedly withdrawing $10 million.

The bankruptcy of Celsius Mining came just months after it announced its plans to go public. But the company planned to continue mining throughout its bankruptcy proceedings, and defended these plans vigorously. Celsius said its mining operations were key to the company’s restructuring efforts. But mining isn’t cheap. In the first two weeks of mining through bankruptcy, Celsius Mining burned $40 million, according to reporting by The Wall Street Journal. At the time, Celsius Mining told the court it expected the mining operations to become profitable by January 2023.

Shortly after Thanksgiving, BlockFi also filed for bankruptcy. Its bitcoin mining operations have not played as prominent a role in the proceedings as Celsius’ has. No reports found for this article indicate that Blockstream’s agreement with BlockFi has been terminated or otherwise interrupted.

But the BlockFi-hosted mining operations were not its only mining-related concerns. In addition to hashing for itself, the company also originated loans to other mining entities. BlockFi’s corporate account addressed this matter on Twitter one month before filing for bankruptcy. Some reports indicate that BlockFi could have suffered up to $80 million in losses from its exposure to Core Scientific, for example.

Why Mine And Lend?

Why a lending company wants to mine bitcoin at all is a question worth answering. The precise answers to this vary, but here’s a simple explanation of one potential motivation: By essentially acting as “crypto savings banks” and lending bitcoin (and other cryptocurrencies) to various retail and institutional counterparties, institutions like BlockFi, for example, had minimal exposure at best to bitcoin’s parabolic upside. Its borrower clients, on the other hand, had full exposure to the market’s volatility. In theory, spinning up a mining operation could give lenders more material risk exposure with larger potential profits.

But the lending business — especially given how some of the crypto financial institutions manage their books — carries enough counterparty risk and operational complexity by itself, one would think. The mining business is notoriously ruthless and complicated, which places new entrants at massive disadvantages even in the best market conditions. Managing a mining unit in addition to a core lending service is beyond doubly tough compared to running only one or the other business, since business complexity scales exponentially, not linearly. Although successfully running a joint lending/mining business is not impossible, it certainly is not for an inexperienced or risk averse founder.

In short, after a decade of institutionalized mining growth, there are good reasons why most mining companies are only mining companies — not hybrid businesses with other core offerings outside of mining. Sure, some miners play the role of lender in limited cases, as previously mentioned. But their core business is mining. Doing anything else is often too much to manage.

Don’t Rinse And Repeat

2022 was a brutal year for all of “crypto,” but especially for miners and lenders. Both high-profile companies that combined the two businesses ended in bankruptcy. Unfortunately, the “crypto” industry has a goldfish-like memory and is more likely to repeat rather than avoid these mistakes. But, hopefully, the future includes severe adjustments in accepted practices for lenders and also strong recovery from well-managed, bear-market-hardened mining companies. If not, the pain and suffering of the 2022 bear market was for nothing.

This is a guest post by Zack Voell. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This mainly stems from the worry that miner revenue will not be enough to offer adequate security in the future, post block subsidy. Bitcoin miners play a crucial part in securing the network by proposing blocks of transactions which nodes then verify, accept and update to the Bitcoin ledger. Competing against other miners to propose this new block to the chain, miners use intense computing power to complete the proof-of-work consensus algorithm, and win the right to propose the new block.

Simplified, the concern is that the transaction fee portion of the miner rewards will not be raised enough to make up for the loss of the block subsidy, resulting in decreased security for the Bitcoin network and an increased likelihood in attacks as miners are no longer incentivized to participate. My view, though, is that most who are worried about this are misunderstanding Bitcoin’s long-term game theory, incentive mechanisms, scalability and adoption potential.

With that being said, this is a topic that should probably be discussed more publicly and not shrugged off as a non-issue. There are people advocating for tail emissions to be added, creating an increase to Bitcoin’s 21 million supply as a solution to the security budget (settlement finality) issue, which is concerning.

I believe the solution (if you can call it that) is already baked into the Bitcoin incentive structure and adoption curve. There are two parts: one, transaction fees scaling with Bitcoin adoption and as a security measure and two, Bitcoin mining transitioning to an auxiliary tool.

Transaction Fee Scaling

When this issue is raised, it usually comes from somebody with a misunderstanding of how or why transaction fees will increase or advocating for proof of stake (here’s an example). Ironically, one of the reasons for increased transaction fees could be a natural defensive reaction to an attack from a bad actor mining empty blocks to prevent users from transacting. If empty blocks are being mined, the mempool will fill with Bitcoin transactors that are raising fees, competing with each other to get in the next block. Riot Blockchain and Blockware Solutions released an incredible report outlining how this and similar attacks would be met with naturally-occuring defense mechanisms from the Bitcoin immune system, most resulting in much higher transaction fees:

“Under an empty block attack or other attacks attempting to stop users from transacting, it is in the self-interest of Bitcoin users to raise their transactions’ fees to get into the next block. The more empty blocks (the longer the attack lasts), the more pending transactions in the mempool. Transaction fees could soar from 1 sat/vbyte to 1,000+ sats/vbyte. The reward for one block could go from close to 0 BTC to 10+ BTC assuming the current maximum block size of 1,000,000 vbytes. The system is antifragile, and an empty block attack would be met by an endless market based counterattack of high transaction fees. And knowledge of this counterattack would likely deter the attacker from this attack in the first place.”

Another example of fees raising as a result of the network defending itself would be a reaction to miners attempting to censor merchants. This example is covered more in depth in this article:

“If a majority miner is not accepting transactions from merchants then the censored merchants must either increase their fees or not transact at all. If a merchant cannot move their bitcoins then they effectively have no value for the duration in which they are being censored. We can deduce that, due to personal time preference, a merchant who is being censored will be willing to pay a higher confirmation fee proportional to the duration in which they are being censored, up to the theoretical maximum in which the fee is the entirety of the transaction.”

In addition to naturally-occuring defensive incentives that would result in increased transaction fees, there are also countless arguments for transaction fees increasing as a result of Bitcoin adoption, specifically as a medium of exchange.

As adoption increases, competition to add transactions to Bitcoin’s scarce block space will increase, and this increases current fees, which then creates further demand for scaling solutions. The market will continue to present these scaling solutions as demanded — some popular solutions now include exchanges batching transactions, the Lightning Network and other Layer 2 and Layer 3 developments that can ultimately bundle thousands of Bitcoin transfers into one transaction that settles on-chain.

When you understand Bitcoin’s adoption curve, it is completely reasonable to assume that the majority of normal user transactions will occur on additional layers or sidechains. Final settlement of these more efficiently-bundled transfers will occur on-chain, along with transactions that want increased security or institutions moving large values. The final settlement would warrant a much higher transaction fee.

The second route that should lower concern around miners dropping offline and reducing the overall security of the network is increased efficiency and a newer realization that Bitcoin miners can act as an auxiliary tool for other business practices. A highly-overlooked development in the mainstream lately has been the Bitcoin miners’ incentive to pursue stranded, wasted or excess energy.

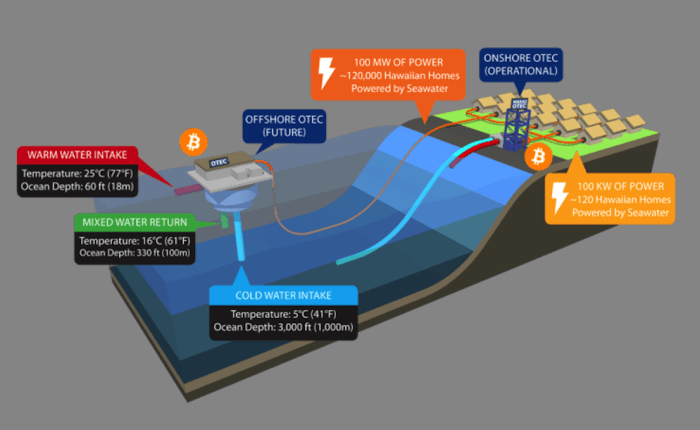

Bitcoin mining offers a unique and new proposal for society, where untapped or un-transportable energy can now be instantly sold to the Bitcoin network on-site via mining. One of the most interesting innovations in this sector is ocean thermal energy conversion (OTEC) merging with Bitcoin.

There is an incredibly in depth article on how OTEC and Bitcoin can further energy production and efficiency here:

“Bitcoin has the potential to help unlock between 2 to 8 terawatts of clean, continuous and year-round baseload power — for one billion people — by harnessing the thermal energy of the oceans. that turns Earth’s oceans into an enormous renewable solar battery.

“It does this by combining warm tropical surface water and deep cold seawater to create a conventional heat engine. This simple idea is perfectly suited to be expanded to a planetary scale by Bitcoin’s unique appetite for purchasing and consuming stranded energy from the prototypes and pilot plants that will be required to prove it works. Furthermore, by harnessing virtually unlimited quantities of cold water for cooling co-located ASIC miners, OTEC may very well be the most efficient and most ecological way to mine Bitcoin.”

This is just one example of how mining can become even more efficient over time, and with increased efficiency comes continued network security as it makes less sense for miners to go offline.

Bitcoin mining is also now becoming an auxiliary tool for other industrial processes. Bitcoin miners can pair with different industries and businesses and offer enormous benefits to seemingly-normal business practices. One mind-blowing example: ASICs used to mine Bitcoin generate heat, this heat can be used to boil water and create steam, condensing the water again is a form of purification, and ultimately this can result in water distillation that was subsidized by mining, as was discussed in a recent Troy Cross interview.

These ASICs that generate heat also need to be cooled with fans. Another mind-blowing concept is combining mining with businesses or industries that naturally create cool air. An example that Cross discussed was carbon capture facilities, which integrate enormous fan banks as part of their normal business operations. Pairing these fan banks with a mining operation subsidizes the cost of ASIC cooling.

As these innovations get more developed, simply adding Bitcoin mining to countless unrelated industries and businesses that generate cooling or need heating will improve efficiency and reduce costs. Bitcoin mining is already heating greenhouses and distilling whiskey, while at the same time monetizing stranded or wasted energy.

Over time, Bitcoin mining will continue to be paired with industries that make mining or normal business operations more profitable. Eventually it will be ridiculous to not use your businesses’ naturally-generated heat or wasted energy on Bitcoin miners, or if your business happens to have enormous fan banks, it will become ridiculous to not point them at ASICs. All of this results in more positively-incentivized miners over time which maintains network security and has the potential to counterbalance the shrinking block subsidy.

The combination of Bitcoin’s adoption naturally leading to increased transaction fees over time and Bitcoin mining shifting into an auxiliary tool for a wide range of independent industries demonstrate how the long-term security of the network is something to be optimistic about.

This is a guest post by Dillon Healy. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This is an opinion editorial by Will Szamosszegi, founder and CEO of bitcoin mining hosting service Sazmining.

Money and energy are two of the most fundamental aspects of an economy because both are universal. Energy is required to transform raw materials into final consumer goods and services. Money is required to store wealth, calculate revenue and losses and trade for goods and services that you couldn’t acquire through barter.

Although Bitcoin drastically improves humanity’s relationship with both energy and money, the problems that plague both energy and money are likely to survive a Bitcoin standard, even if they become lesser in severity. With respect to energy, government regulations, subsidies and bans will continue to have sway. With respect to money, governments will, in all likelihood, continue to employ second-layer fiat money that citizens are forced to use.

Government Meddling In Energy

The United States government has been trying to centrally plan the energy sector since 1789, well before fiat currency reached its “final form” in the fateful year of 1971. In extensive research on the topic of the U.S. government’s history of subsidizing the energy sector, DBL Investors managing partner Nancy Pfund and economics graduate student Ben Healey made several sober discoveries (though they favor government intervention in the energy sector, to be sure):

Although not a direct subsidy, the U.S. government raised a tariff on the sale of British coal in 1789 to benefit the American coal industry. This was only two years after delegates at the Constitutional Convention explicitly fought to include the “gold and silver clause” in the U.S. Constitution. This clause made its way into Article One of the founding document, where it lives on as stating that individual states were not allowed to “make any Thing but gold and silver Coin a Tender in Payment of Debts.” In other words, the political apparatus of the time, though far more monetarily constrained than our present-day Leviathan State, was still able to exert its will over the energy sector.

To be fair, tariffs are easier for a government to enact than subsidies, since only the latter requires the government to have money to spare. But history shows subsidies, too, have existed before the fiat standard went into full effect in 1971. For example, the Price-Anderson Act of 1957 forced the federal government to subsidize nuclear energy by paying for the damages incurred by a nuclear disaster.

Hydropower, too, has been federally subsidized since at least the 1890s, though quantifying the size of these subsidies is challenging. Earth Track, a think tank that works to standardize energy subsidy data, estimates that the U.S. federal government has provided about $2.7 billion (in 2010 dollars) to hydropower from the nation’s inception until 2010. Naturally, this timespan covers a range of different monetary regimes.

Government Meddling In Money

As much certainty as many in the Bitcoin community have about bitcoin becoming the next global reserve asset, governments are unique institutions and can damage our relationship with money, even after bitcoin becomes the new gold.

Governments also wield the threat of violence and incarceration via the military-industrial complex to retain economic power.

For example, imagine that the U.S. government/central bank accepts the new bitcoin monetary regime and even holds it on its balance sheet. Surely by this time, the global economic order will have vastly changed for the better — however, if governments are still around, they are likely still using the threat of violence and/or incarceration to collect taxes. To keep some Layer 2 fiat currency alive, all they have to do is mandate that taxes be paid in said fiat currency. People will then have no choice but to obtain this currency in order to hand it over to the tax man.

To be sure, there are several reasons that such a scheme may not work. For one, “competition” between governments might pressure them to ease up on forcing fiat currencies on citizens who are using Bitcoin and Bitcoin-based Layer 2 technologies in their daily lives. Secondly, ideological pressure from citizens might pressure politicians to give up on creating their own fiat currencies for fear of career suicide. And finally, governments themselves may view such a scheme as being more trouble than it is worth, since a Bitcoin-based economy has the potential to grow at a much greater rate than a Bitcoin-fiat hybrid economy would.

We Must Remain Vigilant

With respect to both energy and money, the government may still intervene after bitcoin has become the next global reserve asset and after Bitcoin mining has forever improved our relationship with money. In this sense, Bitcoin’s inevitable victory is only the beginning — we may still have to fend off meddling bureaucrats. To be sure, freedom-loving Bitcoiners will be in a much better position to do so then than we are now. Nevertheless, we must not rest on our laurels.

What can we do to truly exorcize the State from money and energy? The same thing that we do now: explain our ideas.

We want a free market in energy so that the most cost-effective forms of energy are discovered and made profitable over inefficient alternatives. Furthermore, subsidies, tariffs and regulations in the energy sector hamper innovation. For all we know, absent so much intervention throughout the centuries, our world would be powered by cold fusion, oceans and nuclear energy by now.

And government-imposed money, even if somehow backed by bitcoin, would throw sand in the gears of capital accumulation and economic calculation. The cost of accumulating capital would rise, since we’d need to keep some garbage money in our back pocket for tax season. In other words, the production of all sorts of goods and services would never come to pass, since they’d no longer be affordable. And entrepreneurs’ ability to calculate profits or losses becomes more difficult, since there is no longer a single immutable measuring stick (bitcoin), but also an unpredictable fiat currency still trading alongside Satoshi Nakamoto’s creation.

Our job will not be finished, even after Bitcoin wins the money game and Bitcoin mining wins the energy game, as governments won’t quit. But our ideas will be so much easier to sell by that point, that I, for one, am looking forward to the battles ahead.

This is a guest post by Will Szamosszegi. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Japan’s largest electric power company is about to start mining bitcoin.

Tokyo Electric Power Company (TEPCO) Power Grid is partnering with TRIPLE-1, a local semiconductor designer and developer, to mine bitcoin with excess energy across the country, CoinDesk first reported. TEPCO is the country’s largest electric power company in total assets, per Statista data.

TEPCO is the utility behind the Fukushima nuclear reactor, which in 2011 was struck by an earthquake and huge tsunami that knocked out some of its cooling systems, allowing three reactors to melt down. The power company later admitted that it had failed to take stronger measures to prevent such disasters. TEPCO is still suffering from the accident, as compensation for victims is taking a toll on its profitability to this day. Now, its power transmission and distribution company, TEPCO Power Grid, is seeking ways to monetize surplus power with bitcoin mining through its wholly-owned subsidiary Agile Energy X.

TEPCO is joining major global energy companies in jumping on the bitcoin mining bandwagon. And a common denominator for most of them is a need to monetize excess power, something BTC mining does very well. ConocoPhillips is selling stranded gas to bitcoin miners in the Bakken, an oil-abundant region in the U.S. –– a similar strategy to what Exxon is doing. The oil giant reportedly has an agreement with Crusoe Energy Systems to redirect gas that would otherwise be wasted from an oil well pad to mobile bitcoin mines. TEPCO’s setup also goes along those lines.

According to a translated version of a Wednesday statement by the Japanese energy giant, Agile Energy X signed a memorandum of understanding with TRIPLE-1 on November 11 to build a constructive strategic partnership. Through the collaboration, Agile aims to deploy distributed data centers throughout Japan that repurposes surplus electricity from renewable energy with semiconductors from TRIPLE-1.

A pilot project has already been set up on the premises of TEPCO Power Grid’s office in the Tokyo metropolitan area, per the statement. “We have started experiments to confirm the system behavior and the impact on the power grid when equipment is operated with a large amount of power on the scale of 1,500 kW, and have confirmed that the equipment can operate normally.”

TEPCO’s bitcoin mining pilot venture in Tokyo with TRIPLE-1. (Image/TEPCO)

“TRIPLE-1’s state-of-the-art process technology will be used for the computational computers used in this project, and we will exclusively introduce semiconductors with extremely high power performance,” per the statement. “We believe that selecting and introducing energy-saving products that have a low environmental impact is an important initiative toward the realization of a carbon-neutral society.”

Bitcoin mining companies continue struggling to survive the ongoing bear market. Dreams of outperforming bitcoin as a public mining company are long gone. Bankruptcies and lawsuits make routine headlines. And even Wall Street analysts that were once bullish on bitcoin mining investment opportunities now say they’re “pulling the plug” until the market improves. But exactly how bad is the current bear market?

It’s always darkest before dawn, as the adage says. And compared to previous bear markets, the mining industry looks much closer to the end of a turbulent market phase than the beginning of it. This article explores a bunch of data sets from the current and previous bear markets to contextualize the state of the industry and how the mining sector is faring. From hardware lifecycles and miner balances, to hash rate growth and hash price declines, all of these data tell a unique story about one of Bitcoin’s most important economic sectors.

Mining Revenue Is Evaporating

When bitcoin’s price drops, it’s not surprising that dollar-denominated mining revenue also drops. But it has – a lot. Roughly 900 BTC are still mined every day and will be until the next halving in 2024. But the fiat price for those bitcoin has plummeted this year, meaning miners have far fewer dollars for expenses like electricity, maintenance and the servicing of loans.

As the chart below demonstrates, in November, the entire bitcoin mining industry earned less than $500 million from processing transactions and issuing new coins. The bar chart below shows this monthly revenue compared to the past five years. November mining revenue marks a two-year low for monthly earnings.

This past month marked a two-year low for Bitcoin mining company revenue.

Potential Hash Rate Uptrend Reversal

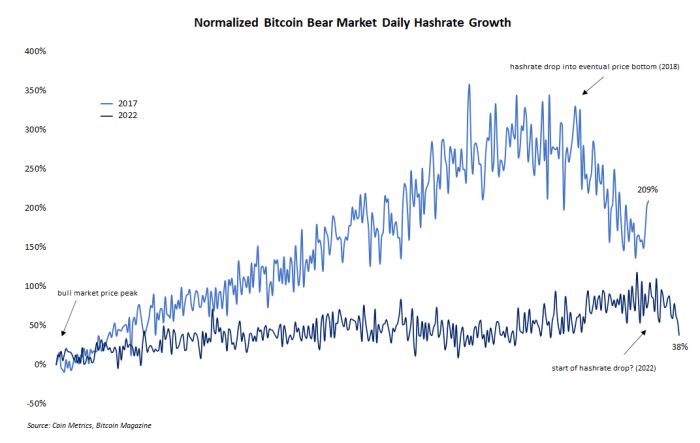

Comparing the current bear market to the previous one in 2018 offers some interesting insights into how the mining industry has changed and how it has remained the same. One such comparison is hash rate growth during downward price trends. It’s not uncommon to see hash rate grow during bear markets. The annotated line chart below shows normalized hash rate growth during the 2018 and 2022 bear markets from bitcoin’s price peak to the drawdowns’ history (or current) lows.

So far in this bear market, Bitcoin hash rate has only grown.

But one thing that is obviously missing from the above chart is a correction in hash rate growth during the later period of the bearish phase. In 2018, for example, the growth trend clearly changed course and dropped as the market eventually found a low for bitcoin’s price. But in the current market, hash rate has only grown. Perhaps a slight drop in hash rate through late November signals a trend change, but the question is still open.

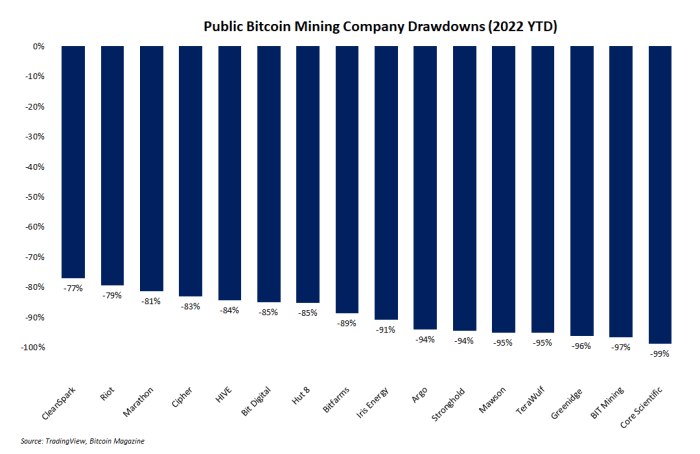

Collapse Of Public Mining Companies

Perhaps the most brutal bitcoin mining chart of all shows the drawdowns of publicly-traded mining companies this year. It’s no secret that the past year has been brutal for bitcoin, other cryptocurrencies, and the global economy in general. But mining companies in particular have been clobbered. Over half of these companies have seen their share prices fall over 90% since January. Only two — CleanSpark and Riot Blockchain — have not dropped more than 80%.

Mining companies in general are often considered to be a high-beta investment in bitcoin, meaning when bitcoin goes up, mining stock prices go up more. But this market dynamic cuts both ways, and when bitcoin falls, the downside for mining stocks is even more brutal. The bar chart below shows the massacre these stocks have endured.

Bitcoin mining stocks have been massacred.

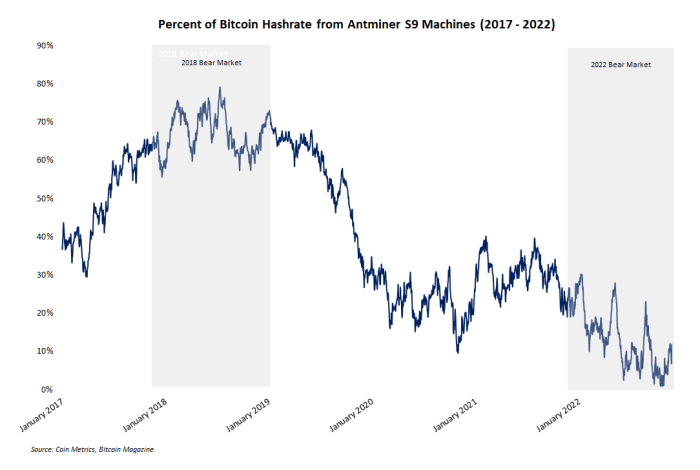

The Rise And Fall Of Bitcoin Mining’s ‘AK-47’

An underappreciated hallmark of the current bitcoin bear market is the precipitous decline in hash rate contributed by Bitmain’s Antminer S9 machines. This model of mining machine is occasionally referred to as the “AK-47” of mining because of its durability and reliable performance. And at one point in the 2018 bear market, the S9 was king. Nearly 80% of Bitcoin’s total hash rate came from this Bitmain model during the depths of the previous bear market.

But the current bear market tells a completely different story. Thanks to new, more efficient hardware and a vice-grip squeeze on mining profit margins, the percentage of hash rate from S9s dropped below 2% in early November. The annotated line chart below shows the rise and fall of this machine.

The Antminer S9 has seen a remarkable fall.

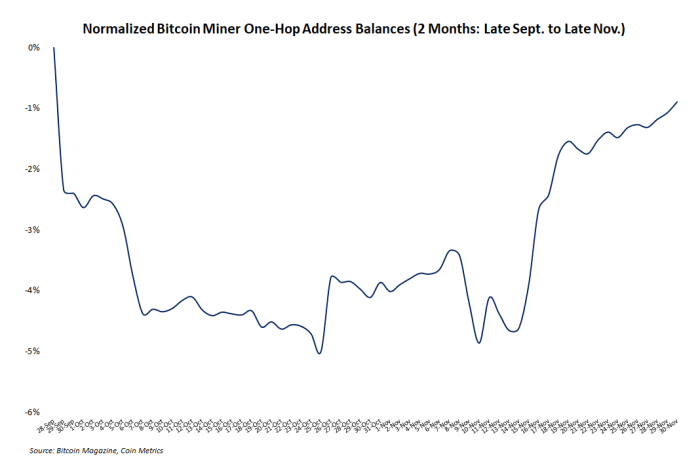

Miner Balance Retraces Its Sell Off

The past few months have been disastrous for the “crypto” industry as exchange wars, insolvent custodians and other forms of financial contagion swept the market. Many bitcoin investors like to assume their segment of the industry is mostly insulated from the chaos of the rest of “crypto,” but this is usually false. In the case of miners, who are notoriously bad at timing the market, some panic was evident as address balances and miner outflows appeared to drop and spike, respectively.

But this activity was short lived. The line chart below shows that miner address balances have almost fully retraced their drop from late September through October. In short, miners appear to be back in HODL mode, impervious to exogenous market events. Whether the bear market is over or not is unknown. But miners seem to be accumulating more than selling.

Miners appear to be back in HODL mode.

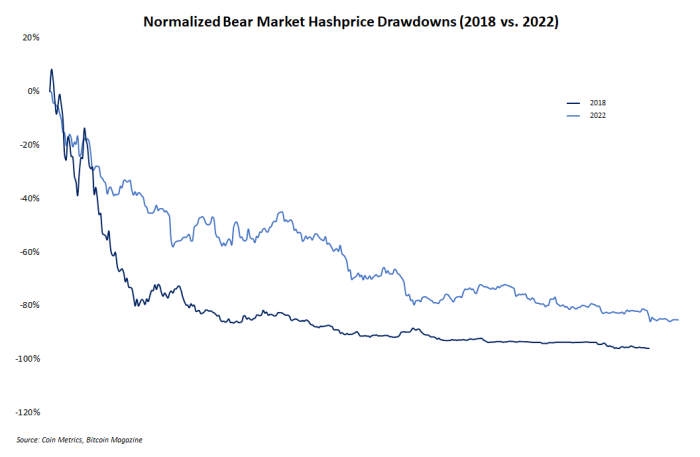

Hash Price Drop Today Vs. 2018

Hash price is one of the most popular economic metrics for miners to track, even though few people outside of the mining sector understand it. In short, this metric represents the dollar-denominated revenue expected to be earned per marginal unit of hash rate. And like everything else in the bear market, hash price has fallen significantly. But its decline is not unusual, especially when it’s compared to the hash price decline in 2018.

Shown in the chart below are normalized hash price drawdowns from 2018 and 2022. Readers will notice the fairly similar slope and size of the drawdowns. 2018 was slightly steeper. 2022 to date has been shallower but longer. But both were and are brutal for fledgling mining operations.

This 2022 hash price drawdown has been shallower but longer than its 2018 equivalent.

The Next Phase Of Mining

Boom and bust cycles are a natural series of events for any properly functioning market. The bitcoin mining sector is no exception. For the past year, mining has seen its weaker, unprepared operators weeded out as the excesses from the bull market are brought to account. Now, in the depths of a bearish period, the real builders can continue to expand their operations and build a solid foundation for the next phase of euphoric bullishness.

This is a guest post by Zack Voell. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This is an opinion editorial by Zack Voell, a bitcoin mining and markets researcher.

Bitcoin miners often suffer the brunt of bear market woes thanks to some of the industry’s highest capital expenditures, smallest margins and most unreliable infrastructure. Although the current bearish phase has been one of Bitcoin’s shallowest drawdowns, miners have suffered more than ever.

Layoffs, bankruptcies, lawsuits and other negative press have battered one of Bitcoin’s most prominent sectors. But every bear market eventually finds a bottom — the pain climaxes and things slowly begin to recover. A variety of data suggest mining has reached this point of its market cycle, which could offer a bit of optimism going into the new year.

This article is not intended to offer financial or investment advice of any kind. On the contrary, its intended purpose is data-driven analysis of the current state of the bitcoin mining sector in context of some exogenous and endogenous influences that could shape its near-term future.

Understanding Capitulation

Before diving into the data, it might help to understand what “capitulation” is. The term is commonly used in financial markets to reference an acute and often dramatic crescendo of fear or widespread surrender by investors or businesses during the throes of depressed market conditions. Basically, everyone says, “It’s over. We can’t take this anymore.” For mining, capitulation basically means the economics became so bad and operating margins are so thin that miners chose to quit or simply cannot operate anymore and are squeezed out of the market.

Wall Street Analysts Turn Bearish

One of the hallmark signs of miner capitulation (in this author’s opinion) at the current stage of the ongoing bear market is the full pivot from financial analysts who report on publicly-traded mining companies. For the past 12 months, these analysts have preached about the upside potential of bitcoin mining stocks. But now they are “pulling the plug.” This language was used by Chris Brendler of DA Davidson to describe his outlook on the mining sector. Since July, Brendler has said that the current market conditions were a good time to buy mining stocks, as reported by CoinDesk.

In December 2021, JPMorgan’s analyst Reginald Smith also wrote a memo that said one particular mining company — Iris Energy — has “more than 100% upside.” He also suggested the current stock price was at a “deep discount.” Shares of the company were trading around $14 at the time of the memo. No they’re trading below $2… an even deeper discount!

If Wall Street giving up on mining isn’t capitulation, then what is?

Bitcoin Hash Rate Starts Dropping

For the entirety of the bear market to date, the Bitcoin hash rate has steadily grown larger, forcing difficulty increase after increase on struggling miners. But that trend might be changing. In early December, the next adjustment is set to drop by almost 11% at the time of writing. This drop will be caused by hash rate falling, which is notably off its recent all-time highs and currently sitting near 240 exahashes per second (EH/s).

Normally a dip in hash rate and difficulty would not be too significant. But seven of the past nine difficulty adjustments have been positive. And in context of the incessant hash rate growth and subsequent hash price collapse, the apparent trend reversal for hash rate is notable. Some miners appear to be throwing in the metaphorical towel and taking their machines offline. Discussing the hash rate and difficulty on Twitter in context of whether miners were capitulating, Foundry Senior Vice President Kevin Zhang simply replied, “Yes.”

Bitcoin Miners Are Re-Accumulating

Generating fear, uncertainty and doubt (FUD) around on-chain movements of bitcoin from miner addresses is a popular pastime for Twitter influencers. And observing miner balances can be helpful. Current data shows notably larger balances compared to just a month ago. In short, net selling activity by miners appears to have subsided and their stockpiles of bitcoin are on the rise again.

Bitcoin mining address balances have seen small reductions over the past year. But the line chart below shows data that indicate a trend reversal is beginning. One-hop miner balances have increased by over 3%, or roughly 85,000 BTC since early October. Perhaps miners decided it’s time to HODL again.

Bitcoin miners may have decided it’s time to HODL again.

Miner Outflows Spiked And Fell

One other piece of on-chain data that fuels mining FUD is outflows — the activity of miner addresses moving coins from those addresses to some other location. In mid-November, these outflows spiked to their highest level since June, which could indicate that fear and panic in the market has affected at least a few miners. Not surprisingly, the spike in outflows occurred at the same time as the collapse of FTX and its subsequent fallout were making headlines.

It should be noted that any inferences from on-chain data like outflows are informed guesstimates at best. Bitcoin network data is a useful tool for contextualizing certain market events, but it is far from infallible or un-manipulatable. But miners are notoriously bad at timing markets, and the timing of this sudden spike in coin movements could reasonably suggest some panicking miners. In the following week, however, outflows fell back to normal levels and have remained there as of the time of this writing.

Did miners panic near the market bottom? Very possibly.

Bitcoin Mining In 2023

Assuming the above analysis is correct and capitulation has occurred, the market will not immediately recover. As the dust settles and survivors emerge, the process of building and scaling more mining infrastructure will be as slow, expensive and tedious as ever. Winners are built in the bear market, and after some of the largest mining companies have sold bitcoin balances down to nearly zero and even sold significant amounts of mining hardware in desperate attempts to stay operational, all that’s left is survival or bankruptcy.

Of course, things could always get worse overnight. But this article suggests the weak and panicked have been squeezed out, and the time for recovery is here. Now is the time to be optimistic, not bearish.

This is a guest post by Zack Voell. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Powering bitcoin mining machines with literal garbage is an emerging trend within the mining sector as a crop of new companies focus on harnessing this abundant and otherwise wasted energy resource. Contrary to the prevalent political narrative that bitcoin mining destroys the planet, the efforts of these landfill miners demonstrate that nothing could be further from the truth.

In fact, the net positive effects of these mining teams are enough to silence environmental critics forever. This article explores the early stages of companies building mining operations at landfills and looks at the potential opportunities that this resource — read: trash — presents for Bitcoin.

Bitcoin’s Emerging Trash Trend

Most instances of discussing landfills and bitcoin together usually involve very early adopters who mined absurd amounts of cheap bitcoin on their computers and subsequently lost or discarded their hard drives that contained fortunes. One early bitcoin miner is even planning an expensive landfill excavation project to retrieve half a billion dollars in misplaced digital gold. Another landfill made headlines because of its response to an inordinately large amount of “incompressible foam” that one bitcoin mining company tried to dump.

These crazy stories aside, today’s bitcoin miners target landfills for power to earn new bitcoin, not as targets for retrieving old ones. Vespene Energy and XcelPlus International are two of the earliest entrants into this new segment of the bitcoin mining industry. I have heard of other similar projects currently building in stealth will join them following public announcements coming in the next year or two. In a recent study on the environmental effects of bitcoin mining, the White House directly mentioned landfill-focused bitcoin mining efforts.

But not all approaches to landfill-powered bitcoin mining are the same. Vespene, for example, “uses landfill methane to fuel bitcoin mining,” according to its website. This business model can quickly affect a non-trivial amount of methane emissions reduction at scale since landfill waste is responsible for about 11% of global methane emissions. XcelPlus, by comparison, uses plasma gasification machines to generate thermal energy and also earn disposal fees for the trash it receives from landfills on top of bitcoin mining rewards — a nice two-for-one deal!

Quantifying The Global Garbage Supply

So, exactly how abundant is trash as a resource for bitcoin mining? The short answer is: very.

Here’s a bit of data to detail just how plentiful the world’s supply of garbage is:

Getting an accurate tally of how many landfills exist in the world is almost impossible (Google certainly isn’t any help). But there’s a garbage clock that provides a real-time count of how much trash is created each day. Landfills can be an energy bonanza for bitcoin miners.

North America has made headlines for becoming an emerging Mecca to bitcoin mining companies. So, for the purpose of this article, it’s worth noting that the U.S. alone is home to more than 3,000 active landfills and roughly 10,000 inactive ones. Canada has roughly 3,000 landfills of its own, according to a discussion paper published earlier this year. Both countries were listed in the top-five total trash producing nations. And both countries ranked as the top two countries by per capita waste generation.

The line chart below visualizes annual growth in the world’s total garbage supply from estimates published by Smithsonian Magazine in an article asking when the world will hit “peak garbage.” The answer? Not any time soon.

Garbage has some unique advantages as a fuel source that readers should not overlook. For one thing, its abundance opens a massive opportunity for potential hash rate growth as landfill methane capture and plasma gasification infrastructure is installed. And the data cited in the previous section more than corroborates the plentifulness of trash. For another, landfills are globally distributed — trash is everywhere. Similar to the distribution of the Bitcoin network itself, miners can go almost anywhere to turn trash into energy for bitcoin mining. Also, this form of energy is truly stranded and wasted, making miners not just a buyer of last resort for this resource, but also one of the only buyers. Landfill methane reduction by other means is limited.

Lastly, and most importantly, bitcoin mining at landfills supercharges the environmentally-friendly narratives around bitcoin mining that counteract seemingly non-stop climate activist criticisms. Some reports label landfills as “super emitters.” Landfills are the world’s third-largest anthropogenic source of methane. And of the trillions of pounds of trash produced each year, some “extremely conservative” estimates suggest barely 33% of that waste is handled in any sort of environmentally-conscious manner.

The stage could not be better set for bitcoin miners to consume literal trash and reduce methane emissions. XcelPlus, for example, flatly states the pollution-reduction advantages of its form of bitcoin mining. According to its website, “The amount of energy consumed by the Bitcoin mining process is vast, expensive and polluting… By funneling waste coal, garbage and other hazardous waste streams through our XcelPlus Plasma gasifier, it can convert 50 tons of waste per day into energy.”

It’s not hyperbolic to say this could be game over for environmental criticisms of bitcoin mining.

The Future Of Trash And Bitcoin

Most of the headlines from the past few years about miners using stranded energy resources have focused on conventional fuels like solar, natural gas and others. But garbage production is almost unending, to the point that some analysts say we are “running out of room” to store it all. And now, bitcoin mining companies are building and deploying technology to harness literal trash as an energy source for mining. Not only is this a somewhat infinitely renewable resource (using the term in an unconventional but not inaccurate way), but powering the Bitcoin network with trash also undercuts environmental criticisms of bitcoin since the benefits of limiting trash emissions are indisputable.

Landfill mining puts the resourcefulness and creativity of bitcoin mining on full display as magic internet money entrepreneurs use energy resources that no one else will or can exploit. Soon, infrastructure for the honey badger of money will be supported by actual garbage, making the world’s largest decentralized financial network more resistant than ever.

This is a guest post by Zack Voell. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This is an opinion editorial by AlbertaHodl, a Canadian dairy and beef farmer and a passionate bitcoin miner.

This is a farmer’s perspective on why it is a good idea to mine bitcoin.

I was born and raised on a farm. I acquired an economics, business and hard-work degree without actually finishing any post-secondary schooling. Times were tough. My dad split the farm with his brother in 1998. As a 10-year-old, I busted my ass along with my 13-year-old brother because we didn’t have a choice. Money was tight. Interest rates had finally reached “normal” levels and commodity prices were not great, but life was good. Since then, we have been able to successfully expand our operation, buy bigger and better equipment, more land and more animals. Here we are today, in the same boat as a lot of other farmers and ranchers: Big enough to earn a living, but wondering what to do now.

Land around us is pushing $15,000 per acre. Regardless of where you farm, the costs are getting out of hand. New and even used equipment is starting to seem out of reach and low interest rates were about the only positive thing if you needed a loan. Well, kiss that goodbye. When you add on political regulations, fertilizer and labor costs, many of us farmers are reconsidering the next item on our ever-growing wish list. It’s pretty tough to sum up a generic return on investment that includes inputs, irrigation costs, seeding costs, etc., but any farmer is well aware of the long-term investment that equipment, land and animals are. Land doesn’t even pay itself off, but we justify it by using the rest of our operation’s income to squeak in one more parcel, a few more pairs of animals or that bigger piece of equipment that will save us time and money in order for us to buy another tractor, seeder, sprayer, a few more pairs of animals or that one more precious field.

It’s a continual cycle that we have grown accustomed to — a fiat mindset of the modern-day slave. Cheap credit incentivizes borrowing for the boat, the toys, the bigger house, etc; it never ends.

As a lifelong farmer, I understand the hesitancy of exploring other options, doing something new, going outside of our comfort zone. I really do. Bitcoin? Heard about it in 2017. It sounded like a scam, so I didn’t bother to look into it.

I should have.

2020 came around and our family farm was shaken by the politics surrounding COVID-19. We were at a loss. Nothing made sense. The world, and especially Canada, seemed to be going to shit. We had our faith and I cannot begin to explain how much that played a role in our sanity and confusion through the difficult times we were facing. Like many farmers, we were asset rich, but cash poor.

Through the ups and the downs, I stumbled across Bitcoin. Little old me, out in the country, starting to learn and understand money, the timechain, cold storage, proof of work — all the things related to Bitcoin.

Trying to learn as much as I can has made my head spin at times, but I felt hope right away. Bitcoin is hope! My goal is to show why bitcoin is a good investment and good for you if you understand it enough to HODL.

Multigenerational farms naturally have a low time preference so if you understand Bitcoin, then why not start mining the asset that is harder than the land we farm? Being Canadian, property rights have very quickly become a glaring concern.

Since the Justin Trudeau-led government froze bank accounts, many people have woken up to the fact that nothing is really their own anymore. We don’t own our money and we can’t own property without paying multiple taxes. If we have a good year and make lots of money, we have to pay even more taxes. It’s a vicious cycle.

Farmers and ranchers always rely on hard assets for retirement, but watching farmers in the Netherlands and Europe getting bought out as regulations and high energy prices force their hand is a reminder that only bitcoin can truly be yours. This has many of us thinking that maybe the assets that we plan to use for retirement and pass down to our children aren’t quite as safe as we once thought.

Most farmers are looking at a time frame of 10-20 years for return on investment. We now have an option that may return that in much less time. We will gladly buy the neighbor’s farm or field with interest rates at 3-5%. Is it time to consider taking the down payment going toward the next long-term investment and instead buy a shed, some ASICs, a few fans and start a personal stack free of know-your-customer (KYC) tracking? Instead of another $500,000 loan for land, you could take out a smaller loan to get bitcoin mining machines going. There are many benefits: lots of rural power available, machines are a business tax write-off, so instead of buying that nitrogen at $800 per ton, that expensive piece of farming equipment or some more animal pairs, you buy some miners.

Hypothetically, the bitcoin mined could be distributed to whomever you want. Maybe it stays on the farm balance sheet. Maybe it’s part of your succession plan and goes to your kids. Maybe it becomes your retirement savings. That’s the beauty of bitcoin! You get to decide.

If you are running any sort of successful farm, you should be able to deduct the power bill from other income. So even in bear markets when the hash price drops drastically, you can justify keeping machines running. Instead of putting your heart and soul into another piece of land, maybe start mining instead. There are no hail issues, calving problems, drought years or unseen input-cost headaches. You lock in your power, get your electrician to run some wire and some ethernet cord, add some fans and you’re getting a return on investment.

The labor to keep a bunch of ASICs running is much less than one hour per week using grid power. And the machines have the potential to pay out in the hardest asset in the world!

When I first proposed purchasing some bitcoin using our farm’s treasury, my father was beyond skeptical. It was something he didn’t understand, but he did see the need for a sound money that couldn’t be inflated. After numerous conversations, we purchased some to hold on the farm’s balance sheet. We kept going down the rabbit hole and used some of that bitcoin to purchase miners. Over the next month, it was late nights of building out the shed, the tunnel, running wires and waiting for the machines to arrive. The setup was a bit overwhelming at times and relied heavily on a few very helpful Bitcoin Twitter friends to work through the kinks.

Finally, we were hashing. Then came the moment I was waiting for: My Dad said, “Hey, if this bitcoin thing really takes off then my succession planning for the non-farm kids will be a whole lot easier.” He’s at retirement age, yet he understood the implications of a monetary system out of the control of the State.

Not sure where to start? I’m a millennial that hardly uses a computer anymore, but I was able to figure it out. Not sure about power, ethernet and airflow? Talk to an electrician for help with the power needs and reach out to myself or a number of more knowledgeable people on Bitcoin Twitter. Many people took time out of their day to give me suggestions and advice. Mining is not as difficult as you’d think and ASICs are cheap right now. Write them off as business expenses, spend some time researching and start acquiring satoshis.

As a farmer, I always want to trust people, but one of my biggest worries was getting my hands on miners without getting scammed. I hardly knew what bitcoin was, let alone how to transact with it. I was terrified of losing our farm’s bitcoin. Fortunately, I listened to a John Vallis podcast with Steve Barbour from Upstream Data. The way Barbour talked about business operations, economics and integrity immediately gave me a feeling of trust.

I reached out to Upstream Data and asked if they could hook me up. For me, a big part of the deal was being able to pick them up in person at their warehouse; the key, I suppose, was to verify instead of just trusting them. I knew they put trust in me as well if they were willing to have me pick up the miners at their facility. They did their part and I was more than happy to make the drive and pick them up and have a couple beverages with the guys. There are many reliable suppliers out there and I’m not going to say one is better than another.

Currently I’m trying to acquire access to some natural gas wells that have been abandoned on and around our property. Imagine the cost minimization if you don’t have to pay for power from the grid. Imagine creating value from the Earth’s core with no permission.