The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

The next FOMC meeting is on February 1, where the Federal Reserve will determine their next policy decision regarding interest rates. This article covers how the market expects the Fed to respond, what readers should watch for regarding changes in the expected path and the potential second-order effects of said changes.

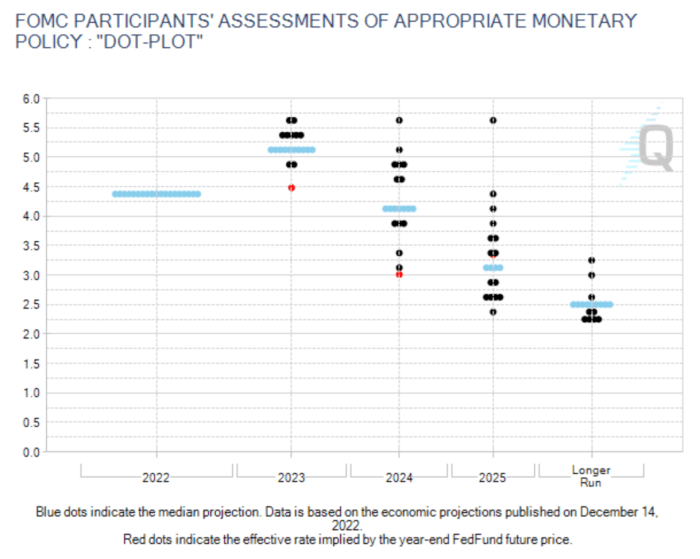

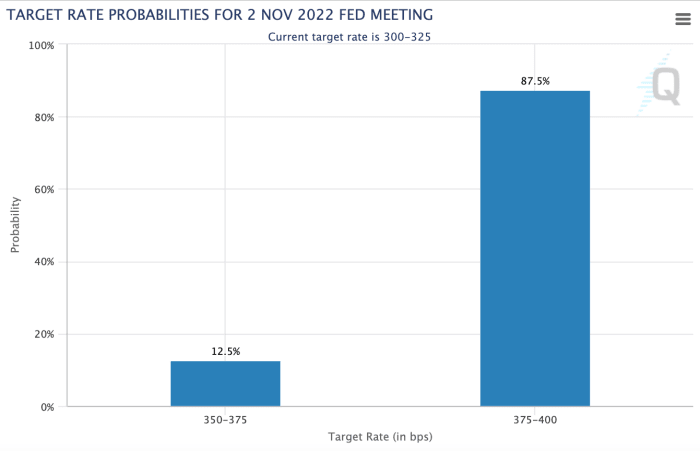

The current expectation is an interest rate hike of +0.25%, with the market assigning a near 100% certainty of this outcome, setting the policy rate to 4.5%-4.75%.

The Fed’s expected course for 2023 is to keep rates elevated, with several Fed Governors recently stressing the need to keep policy rates sufficiently restrictive in order to make sure inflation does not stage a comeback after initial signs of slowing, like it did in the 1970s.

“So, as I mentioned, it is important that overall financial conditions continue to reflect the policy restraint that we’re putting in place to bring inflation down to 2 percent. We think that financial conditions have tightened significantly in the past year. But our policy actions work through financial conditions. And those, in turn, affect economic activity, the labor market, and inflation. So what we control is our policy moves in the communications that we make. Financial conditions both anticipate, and react to, our actions.

“I would add that our focus is not on short-term moves, but on persistent moves. And many, many things, of course, move financial conditions over time. I would say it’s our judgment today that we’re not at a sufficiently restrictive policy stance yet, which is why we say that we would expect that ongoing hikes would be appropriate.”

Pricing In The Transitory Inflation

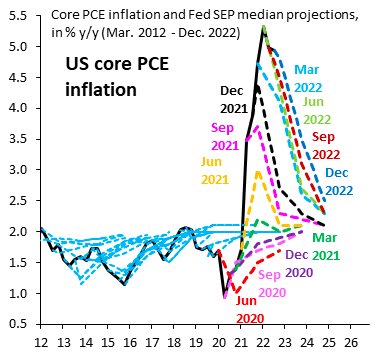

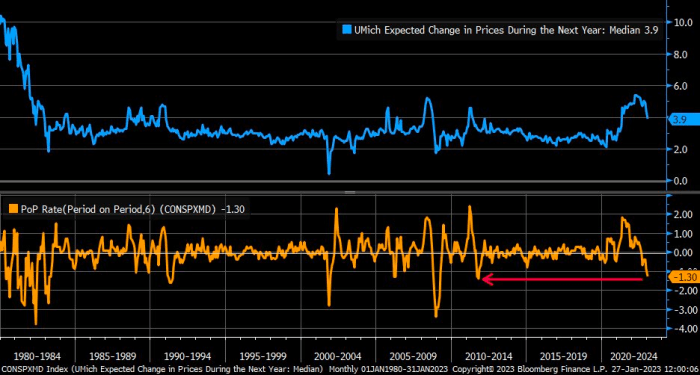

Global risk assets have been in rally mode to start the year, as market participants increasingly expect the inflationary scare that rattled financial assets in 2022 to abate in 2023 and beyond. While the optimistic expectations for abating inflation would certainly be bullish for risk-assets — given that it would lead to the return of lower interest rates — one would be wise to keep in mind the frivolous nature of inflation forecasting from the Fed, as shown below. A return to the 2% target is nearly always the expectation.

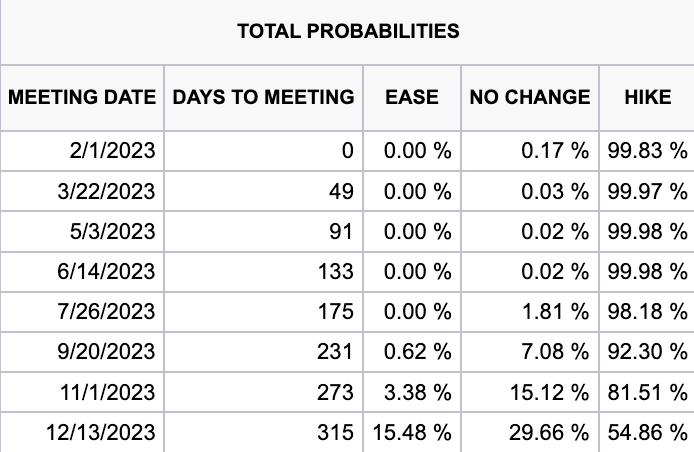

With inflation abating and policy rates staying elevated, the market believes that a “sufficiently restrictive” policy will manifest in 2023, with 1.31% worth of cuts coming in 2024.

Expected rate cuts in 2024 priced by the market

Once inflation becomes entrenched into consumer expectations and labor markets, history has shown that it takes a monumental effort from central banks tightening policy rates in order to squash the inflation.

As noted by Liz Ann Sonders of Charles Schwab, the 6-month change in inflation expectations is the largest it’s been since 2011, an indication that monetary tightening has begun to work its way into the real economy.

With a rate hike of 25 basis points all but confirmed tomorrow, the market will pay close attention to the content and tone of Chairman Powell’s speech in regards to the future path of policy rates. We believe that “higher for longer” is a tone that the Fed will continue to communicate with the market.

However, on a long enough timeline, the inevitable outcome is clear. Just ask the U.S. Treasury for their projections…

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Analyzing On-Chain Bottom Indicators

In this week’s dashboard release, we highlighted some key on-chain metrics we like to track. In this article, we want to walk through more of those in detail. Across bitcoin’s short history, many on-chain cyclical indicators are currently pointing to what looks to be a classic bottom in bitcoin price. Market extremes — potential tops and bottoms — are where these indicators have proven to be the most useful.

On-chain indicators overlaid with previous bitcoin price bottoms.

However, these indicators need to be considered alongside many other macroeconomic factors and readers should consider the possibility that this could be another bear market rally — as we still sit below the 200-week moving average price of around $24,600. That being said, if price can sustain above $20,000 in the short-term, the bullish metrics paint a compelling sign for more long-term accumulation here.

A major tail risk is a possible market-wide selloff in risk assets that are currently pricing a “soft landing” style scenario along with the potentially incorrect expectations of a Federal Reserve policy pivot in the second half of this year. Many economic indicators and data still point to the likelihood that we’re in the midst of a bear market similar to 2000-2002 or 2007-2008 and the worst has yet to unfold. This secular bear market is what’s different about this bitcoin cycle compared to any other in the past and what makes it that much harder to use historical bitcoin cycles after 2012 as perfect analogues for today.

All that being said, from a bitcoin-native perspective, the story is clear: Capitulation has clearly unfolded, and HODLers held the line.

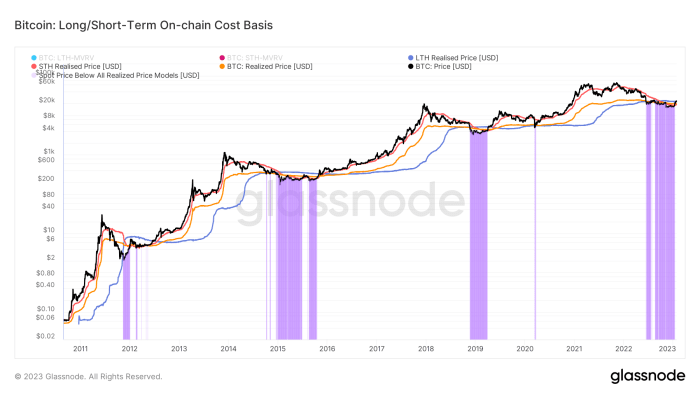

Given the transparent nature of bitcoin ownership, we can view various cohorts of bitcoin holders with extreme clarity. In this case, we are viewing the realized price for the average bitcoin holder as well as the same metric for both long-term holders (LTH) and short-term holders (STH).

The realized price, STH realized price and LTH realized price can give us an understanding of where various cohorts of the market are in profit or underwater.

A look at realized price for short- and long-term holders.

On a monthly basis, realized losses have flipped to realized profits for the first time since last April.

Capitulation and loss taking has flipped to profit realization across the network, which is a very healthy sign of thorough capitulation.

There is a strong case to be made that given the current elasticity of bitcoin’s supply — as evidenced by the historically small number of short-term holders or rather the large number of long-term holders — it will be challenging to shake out current market participants. Especially considering the gauntlet endured over the previous 12 months.

Statistically, long-term bitcoin holders are usually unfazed in the face of bitcoin price volatility. The data shows a healthy amount of accumulation throughout 2022, despite a massive risk-off event in both the bitcoin and legacy market.

While liquidity dynamics in legacy markets should be noted, the supply-side dynamics for bitcoin look to be as strong as ever. All it will take for a significant price appreciation will be a small influx of newfound demand.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

An independent bitcoin rally or a high-beta move? Either way, bitcoin holders are celebrating the latest action to start 2023. Bitcoin has shown some significant momentum and has powered through every key short-term price level across daily moving averages and on-chain realized prices. In fact, every major high-beta play in the market is showing the same strength which gives us more caution than confidence in this latest short squeeze highlighted last week in “Bitcoin Rips To $21,000, Shorts Demolished In Biggest Squeeze Since 2021.”

As much as we would like to see an independent bitcoin move higher, there’s plenty of signs in the market showing the opposite is likely. We’ve seen a relatively meaningful bounce in the most oversold names of 2022, with a short squeeze and subsequent round of FOMO off the 2022 lows.

Bitcoin versus high beta returns.

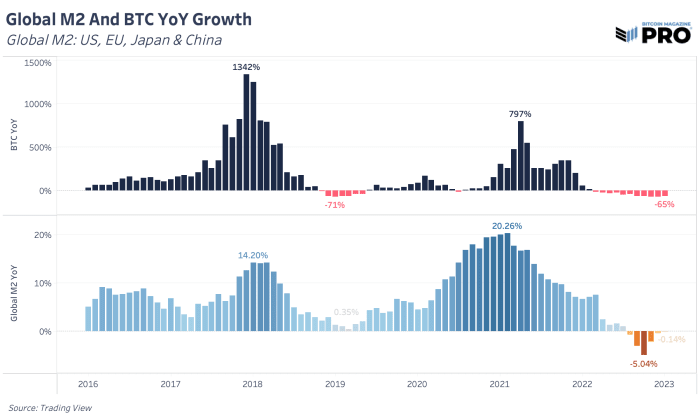

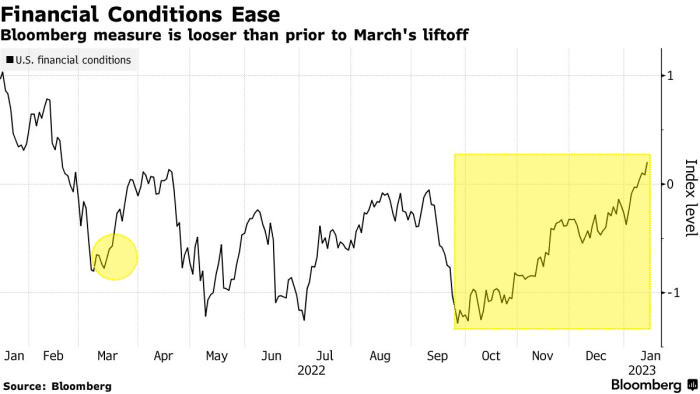

This recent risk rally has seen implied equity market volatility drift to new lows as the U.S. dollar continues to weaken over the short-term, National Financial Conditions Index (NFCI) loosens and global M2 money supply contracts at a much slower pace relative to the last few months.

Global M2 mapped against bitcoin’s year-over-year growth.

Net liquidity, a model we highlighted in our previous piece, shows a contraction compared to last year but hasn’t changed much over the last few months. If we’re to see a sustained rally continue, we’d like to see growth in net liquidity over the next couple of months to be the main driver accompanying this move.

In their recent meeting minutes, members of the Federal Reserve expressed concern about the “unwarranted easing in financial conditions” caused by the run-up in risky assets and subsequently hindering their efforts to cool inflation.

With the Bank of Japan deciding on whether to loosen their monetary policy, this could cause the carry trade to unwind. We view this to be one of the few ways where both the dollar could fall at the same time as global equity markets weaken, with equities repricing due to rising costs of U.S. capital.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

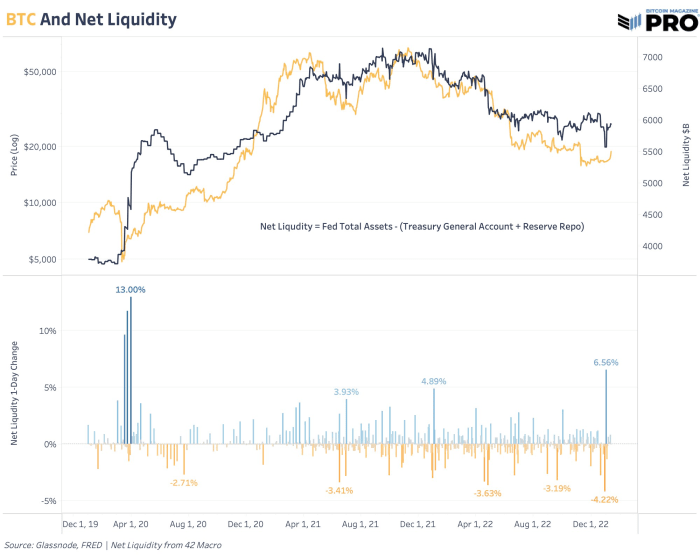

Net Liquidity And Moving Averages

One of the most useful models in tracking the cyclical tops for both the S&P 500 Index and bitcoin since March 2020 has proven to be net liquidity, an original model by 42 Macro. Net liquidity tracks the changes in Federal Reserve total assets, the U.S. Treasury general account balance and the reverse repo facility. A lower net liquidity translates to less capital available to deploy in markets. We find it useful as a key macro indicator to assess current liquidity conditions and how bitcoin trades in the market.

Bitcoin has acted as a liquidity sponge throughout its life and contracting liquidity in all markets has had a significant impact on the bitcoin price and trajectory. Ultimately, that’s one of the main drivers of our core long-term thesis that bitcoin’s growth depends on an environment of perpetual monetary debasement and expanding liquidity to work against current levels of unsustainable sovereign debt and deflationary forces. In the short-term, it’s not clear when overall liquidity will increase again en masse. That’s the trillion dollar question and the topic of conversation on which everyone is speculating. Net liquidity provides a view into that trajectory as a measure that’s updated weekly with fresh data.

Bitcoin is seeing some of its largest relative strength since January 2021, but it also comes at a time when we’re seeing a significant daily uptick in net liquidity after a period of historically low volatility. The uptick is driven by a much lower reverse repo balance since the start of the year. With the Fed’s position of “higher for longer,” a projected view of Core CPI at 3.5% for 2023 and continued balance sheet runoff, we will likely see net liquidity decline — barring a spontaneous or emergency policy reversal.

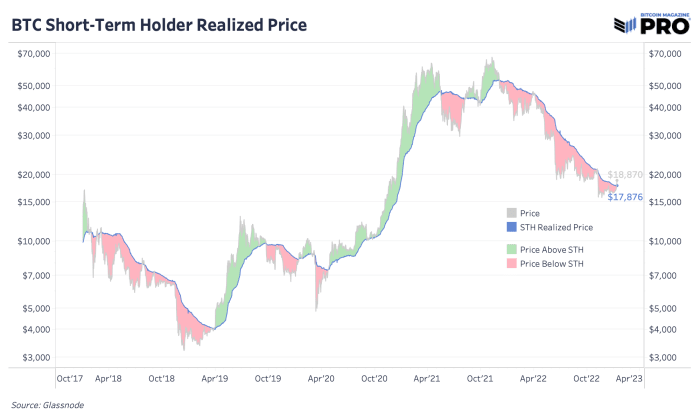

Price has broken above the short-term holder realized price. That’s happened only a few times in this bear market and these events were short-lived. As this price reflects the average on-chain cost basis of the more recent buyers, it will be key to see if these market participants are looking to sell here at cost or if they will stay to continue with the momentum.

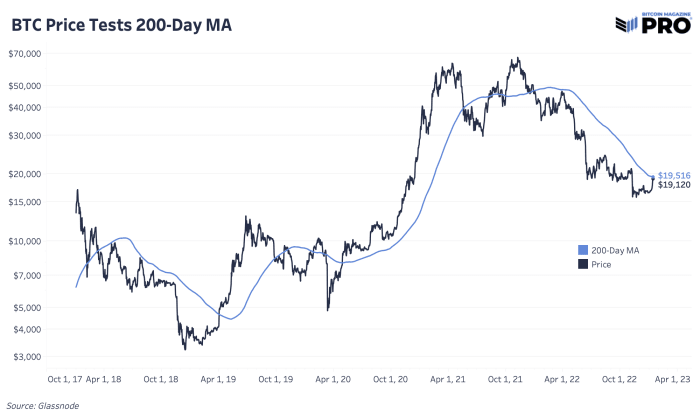

The 200-day moving average may seem somewhat arbitrary, but the mere fact that many technical traders and momentum- and trend-based investors monitor this level gives it significance. A clean break above could mean continued strength for bitcoin in the coming days and weeks ahead.

The price action to start the new year has been quite the promising sign for bitcoin bulls. Similarly, over the last week, shorts as a percentage of futures liquidations has reached its highest level in the history of the data. While shorts have been decimated as of late, it’s likely that this immediate upside could be capped.

While there is a long way to go in terms of surpassing previous bull market heights, the year-to-date performance has been hopeful following a year where the industry practically imploded.

Overall, this is a promising start to 2023.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

The below is an excerpt from a recent year-ahead report written by the Bitcoin Magazine PRO analysts. Download the entire report here.

Bitcoin Magazine PRO sees incredibly strong fundamentals in the Bitcoin network and we are laser-focused on its market dynamic in the context of macroeconomic trends. Bitcoin aims to become the world reserve currency, an investment opportunity that cannot be understated.

In our year-ahead report, we analyzed seven notable factors that we recommend investors pay attention to in the coming months.

Convicted Bitcoin Investors

We can put investor conviction into perspective by looking at the number of unique Bitcoin addresses holding at least 0.01, 0.1 and 1 bitcoin. This data shows that bitcoin adoption continues to grow with a growing number of unique addresses holding at least these amounts of bitcoin. While it is entirely possible for individual users to hold their bitcoin in multiple addresses, the growth of unique Bitcoin addresses holding at least 0.01, 0.1 and 1 bitcoin indicate that more users than ever before are buying bitcoin and holding it in self-custody.

Unique bitcoin addresses continues to grow across the board.

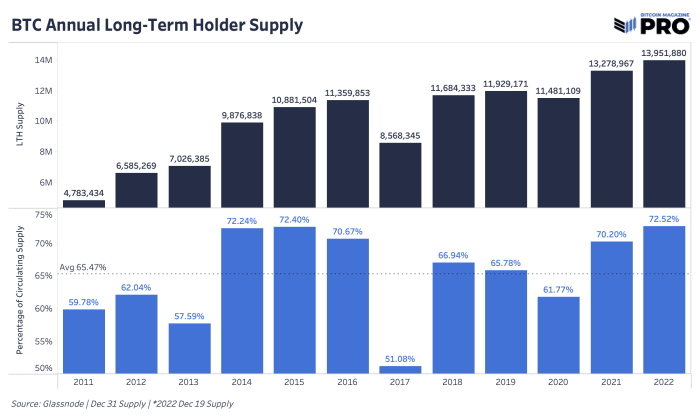

Another promising metric is the amount held by long-term holders, which has increased to almost 14 million bitcoin. Long-term holder supply is calculated using a threshold of a 155-day holding period, after which dormant coins become increasingly unlikely to be spent. As of now, 72.49% of the bitcoin in circulation is not likely to be sold at these prices.

Long-term holder supply reached 72.52% of the circulating bitcoin supply.

There is a large subset of bitcoin investors who are accumulating the digital asset no matter the price. In a December 2022 interview on “Going Digital,” Head of Market Research Dylan LeClair said, “You have people all over the world that are acquiring this asset and you have a huge and growing cohort of people that are price-agnostic accumulators.”

With a growing number of unique addresses holding bitcoin and such a significant amount of bitcoin being held by long-term investors, we are optimistic for bitcoin’s advancement and rate of adoption. There are many variables that demonstrate the potential for asymmetric returns as demand for bitcoin increases and adoption increases worldwide.

Total Addressable Market

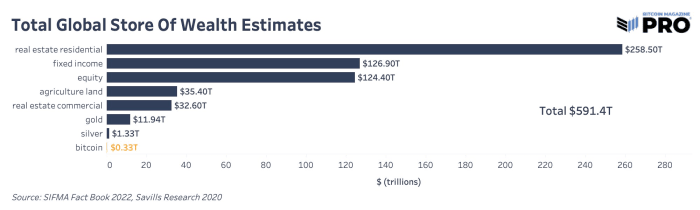

During monetization, a currency goes through three phases in order: store of value, medium of exchange and unit of account. Bitcoin is currently in its store-of-value phase as demonstrated by the long-term holder metrics above. Other assets that are frequently used as stores of value are real estate, gold and equities. Bitcoin is a better store of value for many reasons: it is more liquid, easier to access, transport and secure, easier to audit and more finitely scarce than any other asset with its hard-cap limit of 21 million coins. For bitcoin to acquire a larger share of other global stores of value, these properties need to remain intact and prove themselves in the eyes of investors.

Estimations of global stores of wealth.

As readers can see, bitcoin is a tiny fraction of global wealth. Should bitcoin take even a 1% share from these other stores of value, the market cap would be $5.9 trillion, putting bitcoin at over $300,000 per coin. These are conservative numbers from our viewpoint because we estimate that bitcoin adoption will happen gradually, and then suddenly.

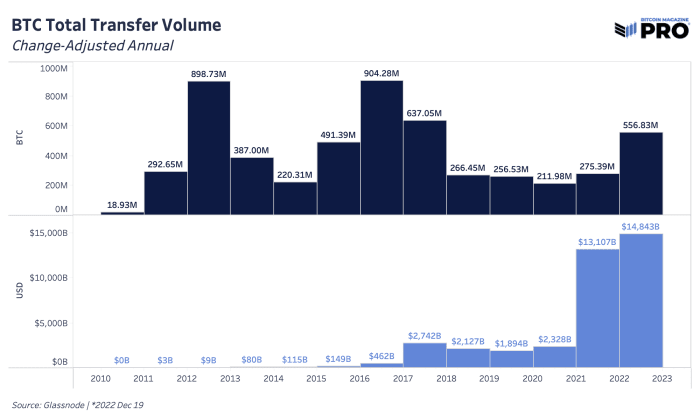

Transfer Volume

When looking at the amount of value that was cleared on the Bitcoin network throughout its history, there is a clear upward trend in USD terms with a heightened demand for transferring bitcoin this year. In 2022, there was a change-adjusted transfer volume of over 556 million bitcoin settled on the Bitcoin network, up 102% from 2021. In USD terms, the Bitcoin network settled just shy of $15 trillion in value in 2022.

Bitcoin transfer volume was higher than ever in USD terms.

Bitcoin’s censorship resistance is an extremely valuable feature as the world enters into a period of deglobalization. With a market capitalization of only $324 billion, we believe bitcoin is severely undervalued. Despite the drop in price, the Bitcoin network transferred more value in USD terms than ever before.

Rare Opportunity In Bitcoin’s Price

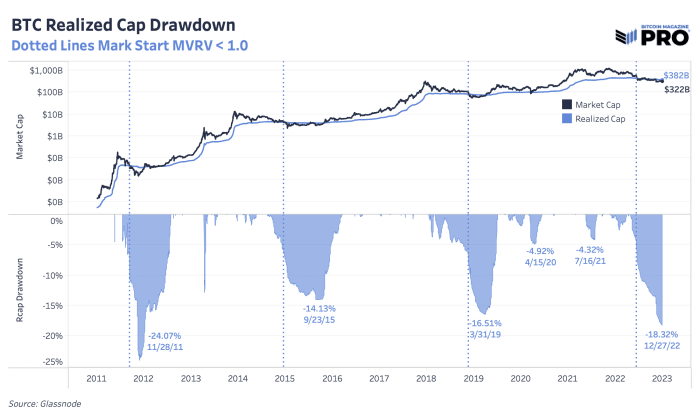

By looking at certain metrics, we can analyze the unique opportunity investors have to purchase bitcoin at these prices. The bitcoin realized market cap is down 18.8% from all-time highs, which is the second-largest drawdown in its history. While the macroeconomic factors are something to keep in mind, we believe that this is a rare buying opportunity.

The realized cap drawdown in 2022 was the second largest in bitcoin’s history.

Relative to its history, bitcoin is at the phase of the cycle where it’s about as cheap as it gets. Its current market exchange rate is approximately 20% lower than its average cost basis on-chain, which has only happened at or near the local bottom of bitcoin market cycles.

Current prices of bitcoin are in rare territory for investors looking to get in at a low exchange rate. Historically, purchasing bitcoin during these times has brought tremendous returns in the long term. With that said, readers should consider the reality that 2023 likely brings about bitcoin’s first experience with a prolonged economic recession.

Macroeconomic Environment

As we move into 2023, it’s necessary to recognize the state of the geopolitical landscape because macro is the driving force behind economic growth. People around the world are experiencing a monetary policy lag effect from last year’s central bank decisions. The U.S. and EU are in recessionary territory, China is proceeding to de-dollarize and the Bank of Japan raised its target rate for yield curve control. All of these have a large influence on capital markets.

Nothing in financial markets occurs in a vacuum. Bitcoin’s ascent through 2020 and 2021 — while similar to previous crypto-native market cycles — was very much tied to the explosion of liquidity sloshing around the financial system after COVID. While 2020 and 2021 was characterized by the insertion of additional liquidity, 2022 has been characterized by the removal of liquidity.

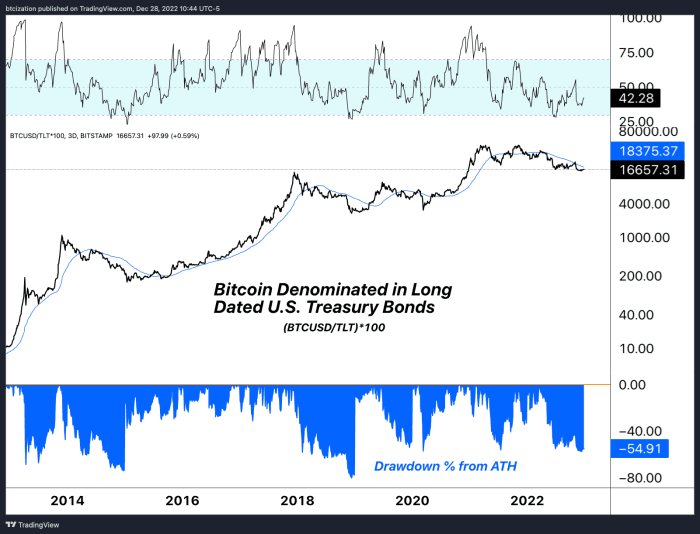

Interestingly enough, when denominating bitcoin against U.S. Treasury bonds (which we believe to be bitcoin’s largest theoretical competitor for monetary value over the long term), comparing the drawdown during 2022 was rather benign compared to drawdowns in bitcoin’s history.

As we wrote in “The Everything Bubble: Markets At A Crossroads,” “Despite the recent bounce in stocks and bonds, we aren’t convinced that we have seen the worst of the deflationary pressures from the global liquidity cycle.”

In “The Bank of Japan Blinks And Markets Tremble,” we noted, “As we continue to refer to the sovereign debt bubble, readers should understand what this dramatic upward repricing in global yields means for asset prices. As bond yields remain at elevated levels far above recent years, asset valuations based on discounted cash flows fall.” Bitcoin does not rely on cash flows, but it will certainly be impacted by this repricing of global yields. We believe we are currently at the third bullet point of the following playing out:

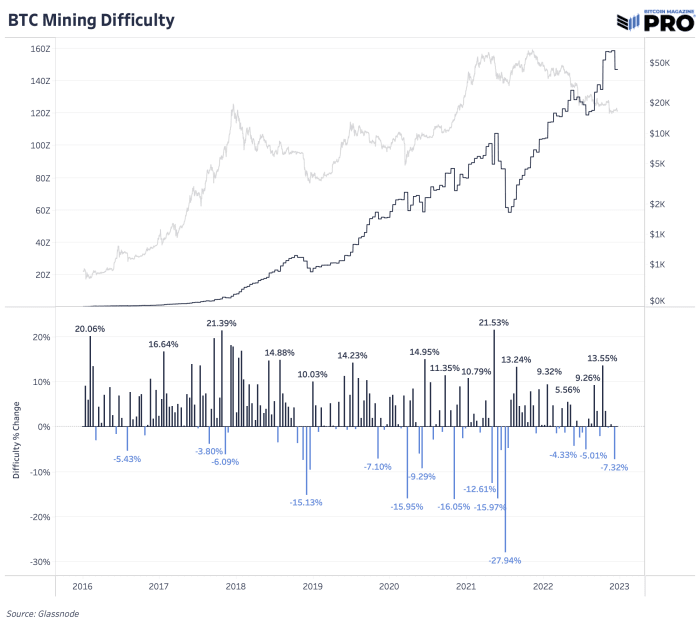

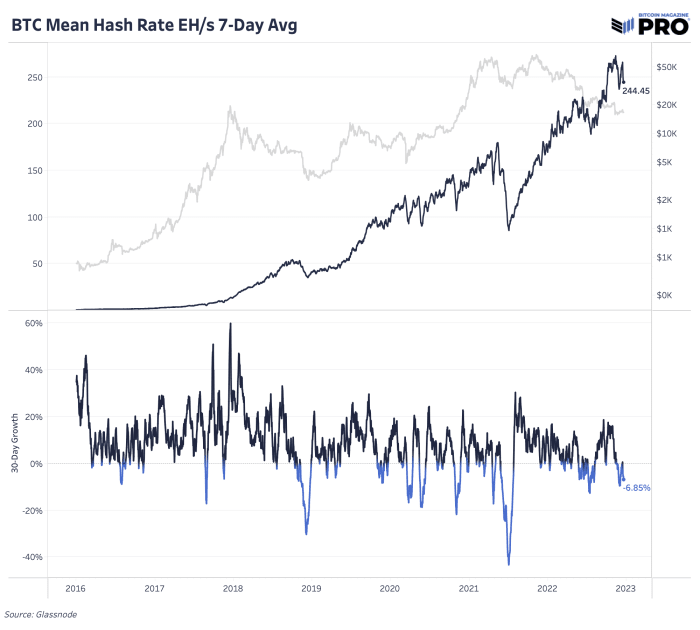

While the multitude of negative industry and worrying macroeconomic factors have had a major dampening on bitcoin’s price, looking at the metrics of the Bitcoin network itself tell another story. The hash rate and mining difficulty gives a glimpse into how many ASICs are dedicating hashing power to the network and how competitive it is to mine bitcoin. These numbers move in tandem and both have almost exclusively gone up in 2022, despite the significant drop in price.

Bitcoin mining difficulty continues to rise.

Bitcoin hash rate continues to rise.

By deploying more machines and investing in expanded infrastructure, bitcoin miners demonstrate that they are more bullish than ever. The last time the bitcoin price was in a similar range in 2017, the network hash rate was one-fifth of current levels. This means that there has been a fivefold increase in bitcoin mining machines being plugged in and efficiency upgrades to the machines themselves, not to mention the major investments in facilities and data centers to house the equipment.

Because the hash rate increased while the bitcoin price decreased, miner revenue took a beating this year after a euphoric rise in 2021. Public miner stock valuations followed the same path with valuations falling even more than the bitcoin price, all while the Bitcoin network’s hash rate continued to rise. In the “State Of The Mining Industry: Survival Of The Fittest,” we looked at the total market capitalization of public miners which fell by over 90% since January 2021.

The market cap of all public mining equities has dropped by 9

We expect more of these companies to face challenging conditions because of the skyrocketing global energy prices and interest rates mentioned above.

Increasing Scarcity

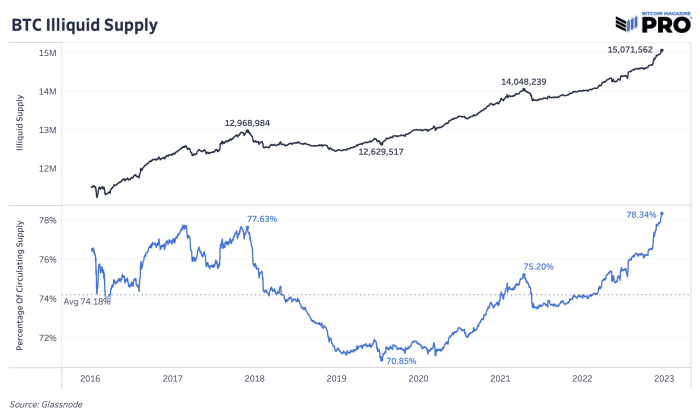

One way to analyze bitcoin’s scarcity is by looking at the illiquid supply of coins. Liquidity is quantified as the extent to which an entity spends their bitcoin. Someone that never sells has a liquidity value of 0 whereas someone who buys and sells bitcoin all the time has a value of 1. With this quantification, circulating supply can be broken down into three categories: highly liquid, liquid and illiquid supply.

Illiquid supply is defined as entities that hold over 75% of the bitcoin they deposit to an address. Highly liquid supply is defined as entities that hold less than 25%. Liquid supply is between the two. This illiquid supply quantification and analysis was developed by Rafael Schultze-Kraft, co-founder and CTO of Glassnode.

Bitcoin’s illiquid supply continues to grow.

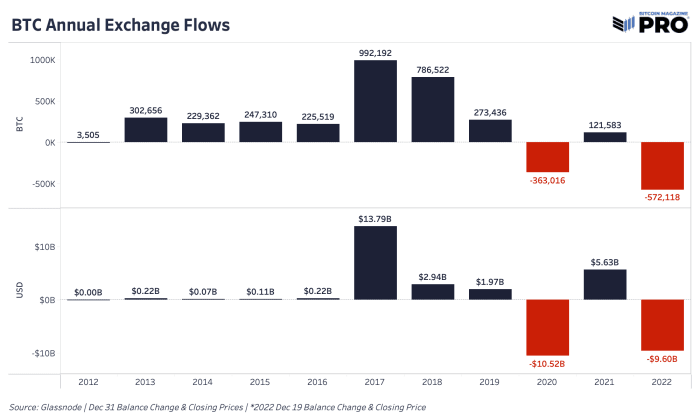

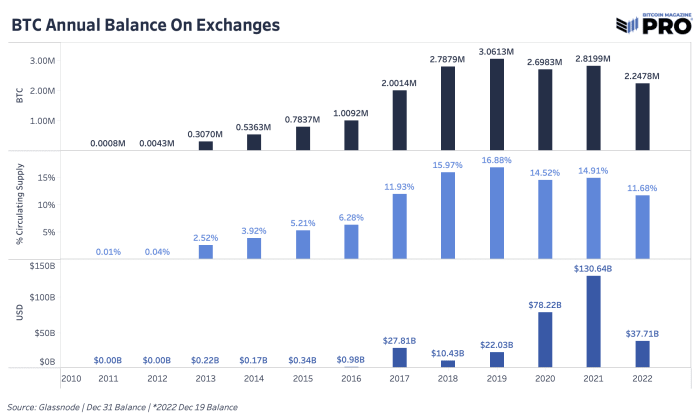

2022 was the year of getting bitcoin off exchanges. Every recent major panic became a catalyst for more individuals and institutions to move coins into their own custody, find custody solutions outside of exchanges or sell off their bitcoin entirely. When centralized institutions and counterparty risks are flashing red, people rush for the exit. We can see some of this behavior through bitcoin outflows from exchanges.

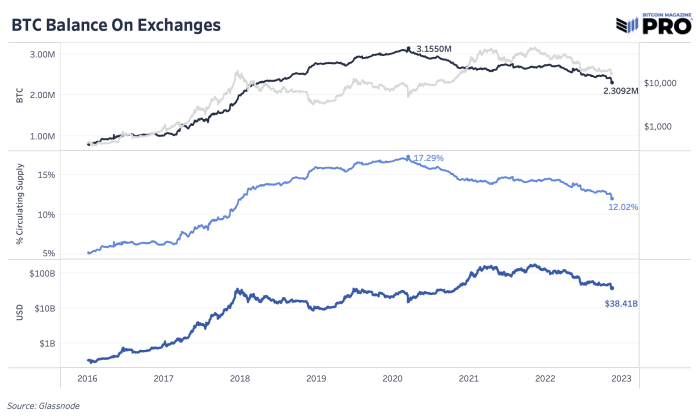

In 2022, 572,118 bitcoin worth $9.6 billion left exchanges, marking it the largest annual outflow of bitcoin in BTC terms in history. In USD terms, it was second only to 2020, which was driven by the March 2020 COVID crash. 11.68% of bitcoin supply is now estimated to be on exchanges, down from 16.88% back in 2019.

Exchanges saw a massive decrease in the bitcoin balances on their platforms.

Bitcoin balance on exchanges decreased in 2022.

These metrics of an increasingly illiquid supply paired with historic amounts of bitcoin being withdrawn from exchanges — ostensibly being removed from the market — paint a different picture than what we’re seeing with the factors outside of the Bitcoin network’s purview. While there are unanswered questions from a macroeconomic perspective, bitcoin miners continue to invest in equipment and on-chain data shows that bitcoin holders aren’t planning to relinquish their bitcoin anytime soon.

Conclusion

The varying factors detailed above give a picture for why we are long-term bullish on the bitcoin price going into 2023. The Bitcoin network continues to add another block approximately every 10 minutes, more miners keep investing in infrastructure by plugging in machines and long-term holders are unwavering in their conviction, as shown by on-chain data.

With bitcoin’s ever-increasing scarcity, the supply side of this equation is fixed, while demand is likely to increase. Bitcoin investors can get ahead of the demand curve by averaging in while the price is low. It’s important for investors to take the time to learn how Bitcoin works to fully understand what it is they are investing in. Bitcoin is the first digitally native and finitely scarce bearer asset. We recommend readers learn about self-custody and withdraw their bitcoin from exchanges. Despite the negative news cycle and drop in bitcoin price, our bullish conviction for bitcoin’s long-term value proposition remains unfazed.

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Although it feels like a lifetime ago, only two months have passed since Genesis announced their need for a $1 billion liquidity injection in the aftermath of the FTX and Alameda fallout. As weeks dragged on without a resolution, details of the story have become more public, building up to fraud allegations against Digital Currency Group (DCG) that were announced by Gemini co-founder and president, Cameron Winklevoss. Gemini is still trying to recover $900 million in assets from Genesis that were used to generate yield for their Earn customers.

Left unresolved and only growing larger, DCG and Genesis problems weigh heavily on the bitcoin market as there are many answers needed and various possible outcomes that have yet to play out.

The biggest question of all is what will happen to the Grayscale Bitcoin Trust (GBTC) and how these issues will potentially impact the bitcoin price. GBTC has been the preferred vehicle for many to obtain regulated bitcoin exposure and it has also been a breeding ground for speculative arbitrage strategies throughout the previous swings going from a premium to a discount to net asset value (NAV). An approved bitcoin spot ETF in the United States would have likely solved these issues, but we’re still far from that happening.

It’s easiest to start with the GBTC shares on DCG’s balance sheet which are estimated to be around 9.67% of the entire supply. In the event that DCG needs to raise cash or goes down the path of Chapter 11 bankruptcy, selling these shares is potentially an option. Selling into an already illiquid market puts more pressure on the historically low GBTC discount. DCG holds approximately 67 million shares in a market that trades less than 4 million shares a day. However, a more important factor is that by law, DCG can sell no more than 1% of shares outstanding every quarter. It would take them around 2.5 years of constant selling to sell their entire stake.

Another path — the most likely one — is that the GBTC, along with Grayscale’s other trusts, find their way into the hands of a new sponsor and manager. Valkyrie has already proposed to do exactly this:

Give an option for investors to redeem shares at NAV through a Regulation M filing request (although it’s not clear a Regulation M request would get approved by the SEC).

Lower fees from 200 basis points to 75.

Attempt to offer investors redemptions in both cash and spot bitcoin.

The option for a new manager gives investors an opportunity to get out of investments at NAV.

The GBTC product is still a cash cow for Grayscale and DCG, raking in 2% management fees — in perpetuity. Across all major trust products, Grayscale is collecting over $300 million this year from management fees alone. Rather than liquidate the entire trust in the worst case scenario, there will be many willing buyers to take on management of the vehicle without a U.S. spot bitcoin ETF available in the market.

However, liquidation is not a non-zero possibility. In the event of a Grayscale insolvency or bankruptcy, voluntarily liquidation could be pursued unless 50% of shares vote to transfer to a new sponsor. There is upside to DCG liquidating the trust as there’s money to be made from their shares closing to NAV, but that likely results in selling bitcoin on the open market. No one wants to see 632,000 bitcoin — approximately 3.3% of current supply — become selling pressure in the market. In the unlikely scenario where complete liquidation of the trust is undertaken with USD cash being returned to shareholders, one could presume that much of the selling would be absorbed through OTC deals with interested investors. At this point, this is purely hypothetical.

New information is coming to light that has the potential to change the superstructure in regard to the dynamic between Grayscale and the shareholders of Grayscale products. We will continue to write about developments in the coming weeks.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

As we head into 2023, we want to highlight the latest state of bitcoin’s volume and volatility after a recent wave of capitulation. Last time we touched on these dynamics was in “The Bitcoin Ghost Town” in October, where we highlighted that an extremely low volume and low volatility period in bitcoin price, GBTC and the options market was a concerning sign for the next leg lower. This played out in early November.

Fast forward and the trends of declining volume and low volatility are back once again. Although this could be indicative of another leg lower to come in the market, it’s more likely indicative of a complacent and decimated market that few participants want to touch.

Even during the November 2021 capitulation period, there was a historically low period of volatility. Sometimes the most market pain can be felt when having to wait for a clear change in trends. The bitcoin price is providing that pain as we’ve yet to see the type of explosion in market volatility that has defined market pivots and major directional moves in the past.

SPX Bottoms

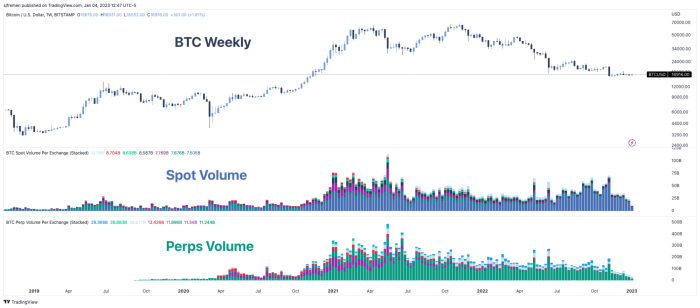

While there are many different ways to define, classify and estimate bitcoin volume in the market, they all show the same thing: September and November 2021 were the peak months of action. Since then, volume in both the spot and perpetual futures markets have been in steady decline.

Bitcoin volume across spot and perpetual futures markets

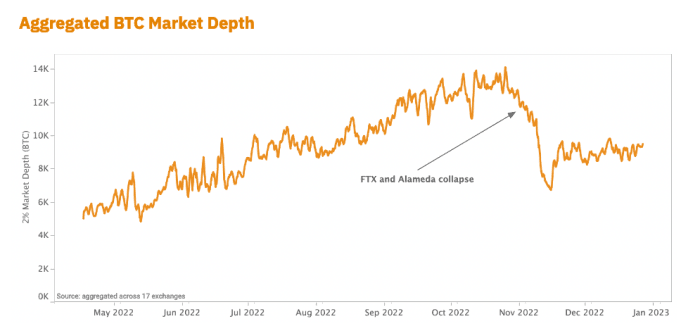

Overall market depth and liquidity has also taken a major hit after the collapse of FTX and Alameda. Their destruction has led to a large liquidity hole, which is yet to be filled due to the lack of market makers currently in the space.

By far, bitcoin is still the most liquid market of any other cryptocurrency or “token,” but it’s still relatively illiquid compared to other capital markets since the whole industry has been crushed over the last few months. Lower market depth and liquidity means assets are prone to more volatile shocks as single, relatively large orders can have a greater impact on market price.

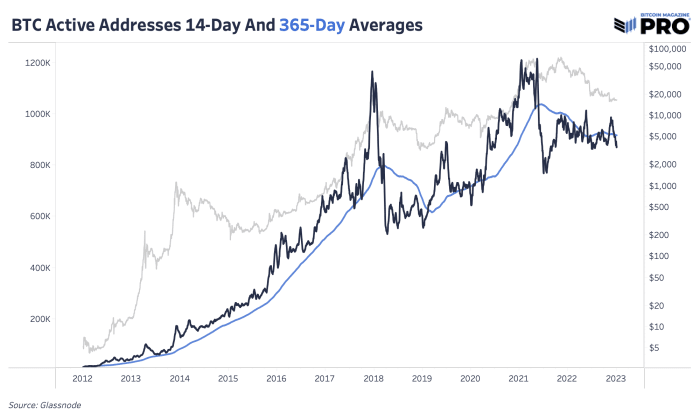

As expected in the current environment, we’re also seeing more market complacency when looking at on-chain data. Although continuing to rise over time, the number of active addresses — unique addresses active as either a sender or receiver — remain fairly stagnant over the last few months. The chart below highlights the 14-day moving average of active addresses falling below the running average over the last year. In previous bull market conditions, we’ve seen growth in active addresses outpace the existing trend fairly significantly.

Moving averages of active bitcoin adresseses

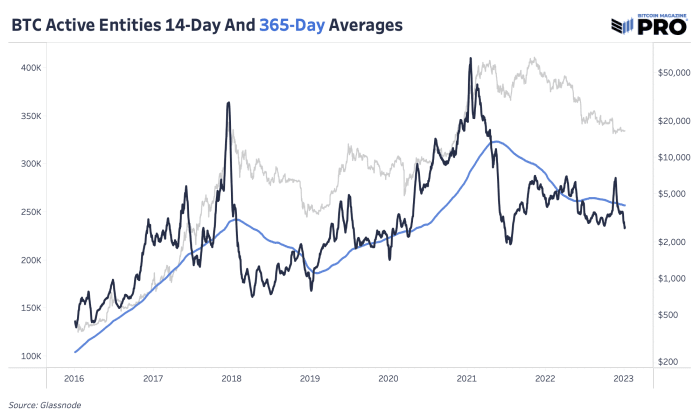

Since address data has its flaws, looking at Glassnode’s data for active entities shows us the same trend. Overall, bear markets reversing are the result of many factors, including growth in new users and an increase in on-chain activity.

Moving averages of active bitcoin entities

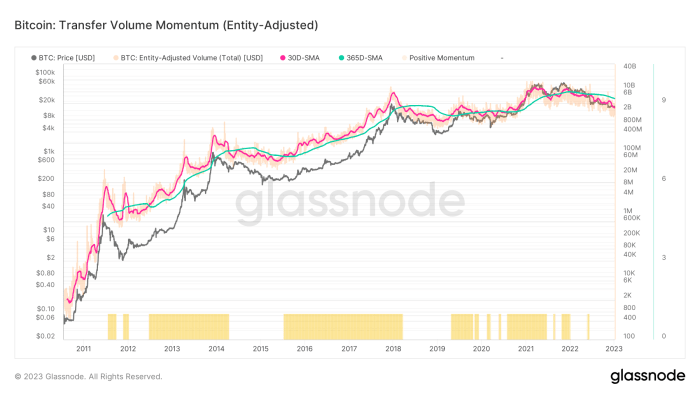

Bitcoin transfer volume momentum

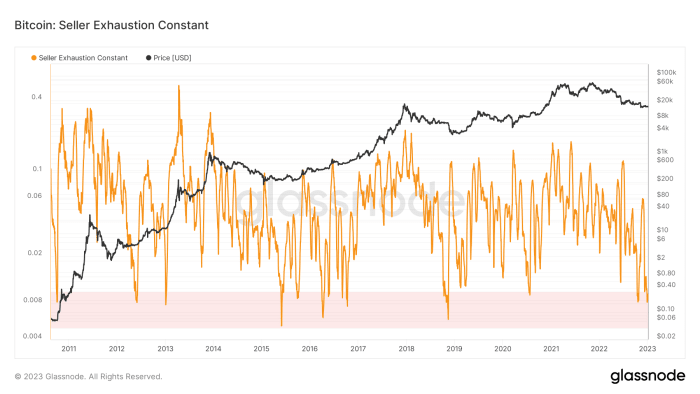

Bitcoin seller exhaustion levels

In our July 11 release “When Will The Bear Market End?”, we made the case that the brunt of the price-based capitulation had already been felt, while the real pain ahead was in the form of a time-based capitulation.

“A look at previous bitcoin bear market cycles shows two distinct phases of capitulation:

“The first is a price-based capitulation, through a series of sharp selloffs and liquidations, as the asset draws down anywhere from 70 to 90% below previous all-time-high levels.

“The second phase, and the one that is spoken of far less often, is the time-based capitulation, where the market finally begins to find an equilibrium of supply and demand in a deep trough.” — Bitcoin Magazine PRO

We believe time-based capitulation is where we stand today. While exchange rate pressures can certainly intensify over the short term — given the macroeconomic headwinds that remain — the conditions that look likely to persist over the short and medium term look to be a sustained period of chop with extremely low levels of volatility that leave both traders and HODLers questioning when volatility and exchange rate appreciation will return.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

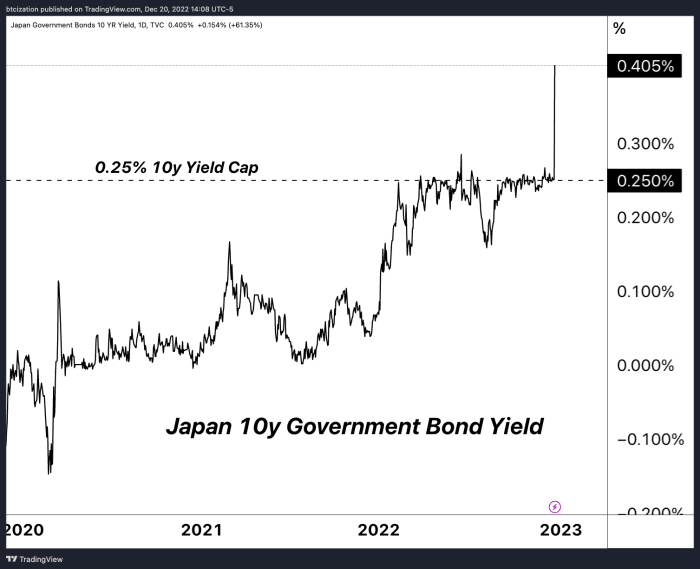

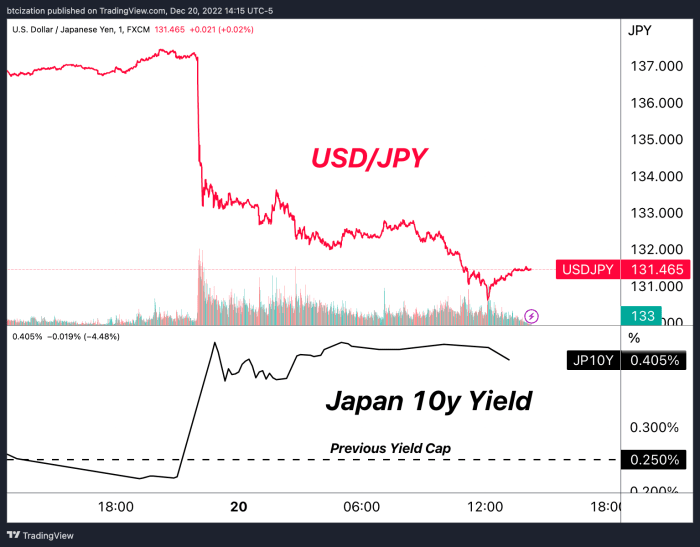

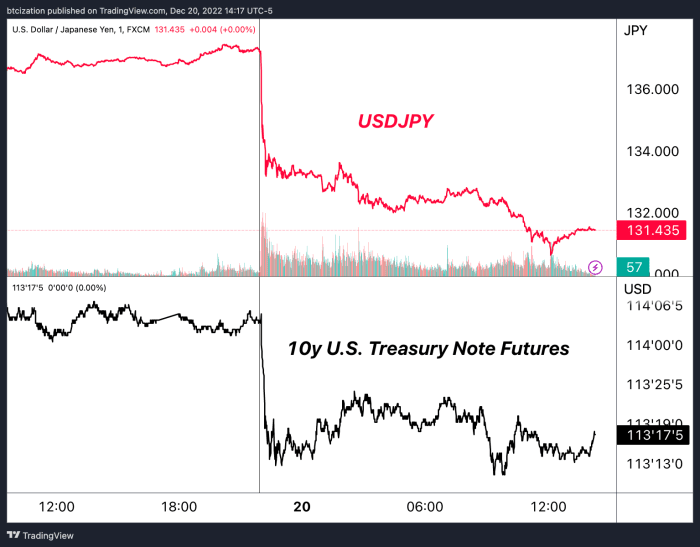

On the evening of December 19, the Bank of Japan (BOJ) announced it had increased its cap on 10-year bond yields from 0.25% to 0.5%, while keeping short- and long-term interest rates unchanged.

The cap at the 0.25% level had been suppressing global bond markets with the use of an unlimited money printer for Japanese debt. This in turn caused a significant deterioration of the yen against the dollar, while the BOJ used its immense pile of Treasurys to occasionally defend the currency against speculators.

While absolutely massive in its change for market dynamics, the move still leaves the BOJ far below its peers in terms of policy rate, which is mainly due to the demographics of Japan and its debt-to-GDP statistics.

This yield-cap increase, which was unexpected by economists, caused an immediate jump in the yen and a slide in global government bonds, sending shockwaves through global financial markets. It also led to a surge in Japanese bank stocks, as investors anticipated improved earnings for financial institutions.

Bank of Japan Governor Haruhiko Kuroda laughing as he hikes rates for the world.

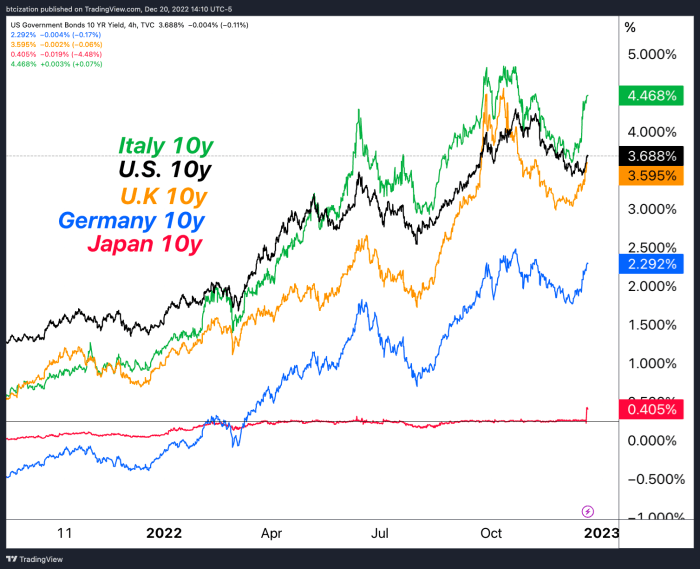

As the BOJ tightens policy, Japanese debt becomes relatively more attractive and the yen appreciates. This causes rates to tighten in U.S. markets, but causes the dollar to weaken relative to foreign exchange markets.

As bond yields remain at elevated levels far above recent years, asset valuations based on discounted cash flows fall. While many market participants are waiting for the return of 2021-like conditions for various financial markets, understanding how the change in debt markets affects all other liquid markets and relative valuations is key.

A historic interest expense shock is occurring in tandem with the largest absolute drawdown in asset prices ever. We expect the turbulence only picks up from here.

While the bitcoin market has had a massive deleveraging of its own already, the “pain trade” (as many think of it) could simply be an extended period of sideways consolidation as the legacy market dominos start to fall at an increasing frequency.

We expect the next secular bull market to be spurred by accommodative monetary policy responses to the conditions that are developing now. Global financial market liquidity conditions, credit worthiness and asset price valuations likely fall further from here — until the fiat monetary overlords decide to start debasing. For better or worse, this is the name of the game on the fiat monetary standard.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Binance: FUD Or Legitimate Questions?

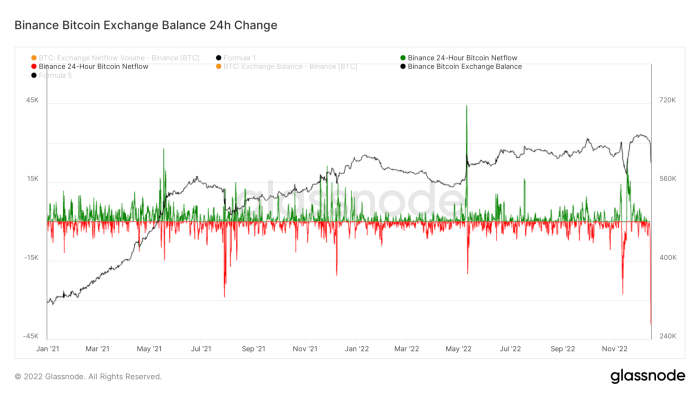

By far, one of the biggest winners in the aftermath of the FTX collapse has seemed — on the surface — to be Binance. After only having 7.82% market share of the bitcoin supply on exchanges in 2018, their share is now 27.50% despite a much broader trend of bitcoin supply leaving exchanges. The bitcoin balance on Binance now totals 595,864 BTC, which is 3.1% of outstanding supply, worth $10.58 billion. This bitcoin belongs to their customers and reflects a growing trend in market share over the last few years that has made Binance the largest bitcoin and cryptocurrency exchange in the world.

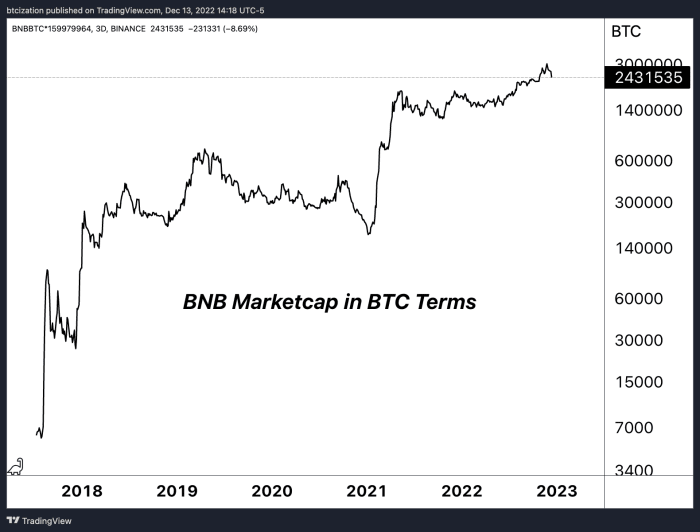

Binance now controls approximately 60% of the spot and derivatives volume in the entire market. It’s hard to see how any exchange in the space can be a “winner” in the current market conditions, but one could make the case for Binance, with the exchange’s growing strength in a decimated industry. On top of that, Binance’s BNB token, the native currency of Binance’s own Ethereum-competing Layer 1 blockchain, is still one of the better performing tokens when valued in bitcoin terms this year.

Yet, is this recent “strength” everything that it seems or is it a facade? We’ve learned over the last month that no company is safe in this industry right now (especially exchanges) and questions are growing around Binance’s practices, solvency, BNB token value and the overall state of their business over the last few weeks. Is it FUD or legit? Let’s try to break some of it down, addressing the concerns through an objective and skeptical lens.

Binance Flows

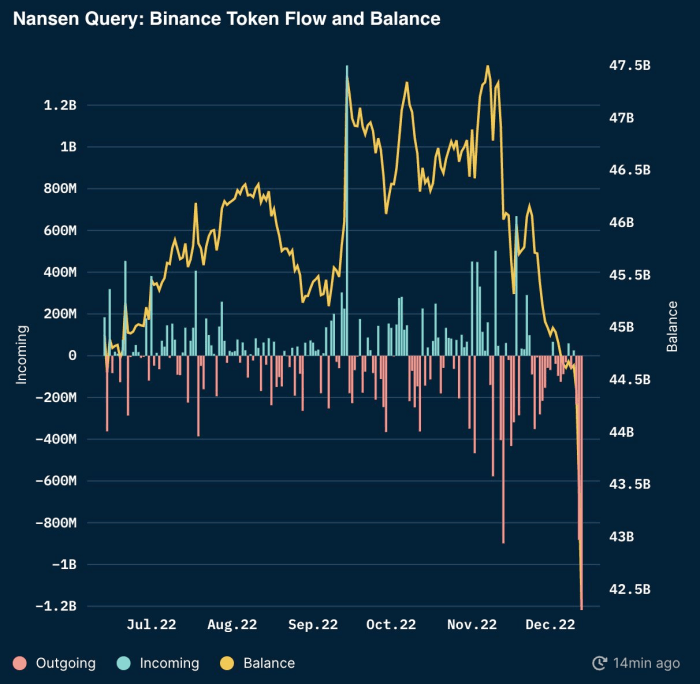

We’ve seen significant outflows from Binance across different various tokens and bitcoin when looking at both Nansen and Glassnode tracking. Across ETH and ERC20 tokens, Binance saw $3 billion leaving the exchange in its largest single-day outflow since June. Across Nansen total wallet tracking, all Binance balances are estimated at $62.5 billion with around 50% of those balances in stablecoins across BUSD and USDT.

According to Glassnode, the total bitcoin exchange balance on Binance is down around 6-7% over the last day, after reaching a peak on December 1. Although balances remain above 500,000 bitcoin and Binance has shown a rising trend of bitcoin balances on the platform this year, this is a significant move for outflows in just 24 hours. As a general comparison, the trend of bitcoin exchange balances was a much different story for FTX, whose balance had been falling heavily since June. Binance outflows over the last couple days are a bit alarming and raise questions: Is this a one-off event and just business as usual or is this the start of something more?

Binance sees its biggest ever bitcoin outflow in a 24-hour period.

The main cause for concern is not whether Binance has any bitcoin/crypto or not. We can transparently see that the firm controls tens of billions worth of crypto assets. What isn’t exactly clear, similar to FTX, is whether the firm has commingled users funds or whether the firm has any outstanding liabilities against user assets.

Binance CEO Changpeng Zhao (CZ) has said that the firm has no liabilities with any other firms, but as recent months have shown, words don’t mean all that much. While we are not claiming that CZ is lying to the public about the state of Binance finances, we have no way to prove otherwise.

CZ’s response as to whether the company was going to audit liabilities against user assets was, “Yes, but liabilities are harder. We don’t owe any loans to anyone. You can ask around.”

Unfortunately, “ask around” isn’t a satisfactory enough answer for an ecosystem supposedly built around the ethos of “don’t trust, verify.”

While there is no doubt that Binance is an industry giant in the crypto derivatives industry, how do we know the firm isn’t doing similar things as past actors in regards to trading against clients using user funds and/or proprietary data. Things like the former Chief Legal Officer of Coinbase departing Binance U.S. last summer after just three months as the CEO leaves one with many questions.

To add to our skepticism, the price of the Binance exchange token BNB is near all-time highs in bitcoin terms, appreciating an astounding 828% against bitcoin in the last 785 calendar days.

Is BNB really worth approximately 14% of all bitcoin that will ever exist?

The coming weeks will be full of headlines around the state of global crypto regulation in a post-FTX world. In a 48-hour period, Reuters published news stating that the U.S. Justice Dept is split over charging Binance, Binance withdrawals for bitcoin and aggregate stablecoin pairs have hit all-time highs and the BNB exchange token has fallen 10% relative to bitcoin.

Out of an abundance of caution, we will continue to urge readers operating on any centralized exchange — of which Binance is most definitely included — to look into self custody solutions. There have been far too many instances of incompetence and/or misconduct from exchanges.

It’s not that we don’t trust CZ or Binance, it’s the fact that we don’t trust anyone.

The whole point of bitcoin is we now have an asset that is truly the liability of no one. Verify the ownership of an open distributed network with cryptography; don’t trust permissioned IOUs. With the mix of regulatory concerns about the global crypto derivatives industry, a questionable exchange token with unbelievable relative performance over the last two years and a shaky proof-of-reserves attestation — that was incorrectly claimed to be an audit and had industry CEOs raising eyebrows — we find the need to urge our readers to evaluate their counterparty risk.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

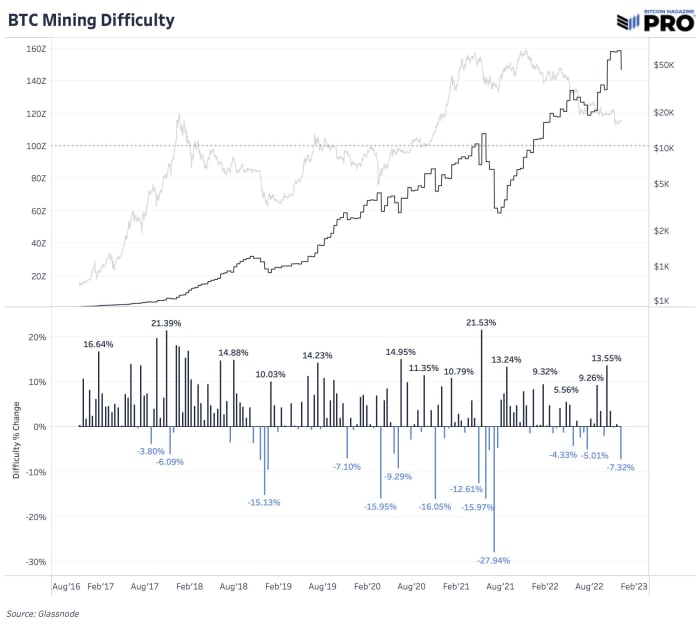

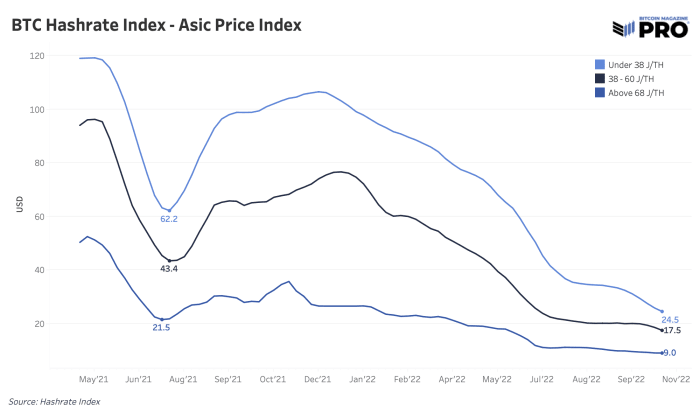

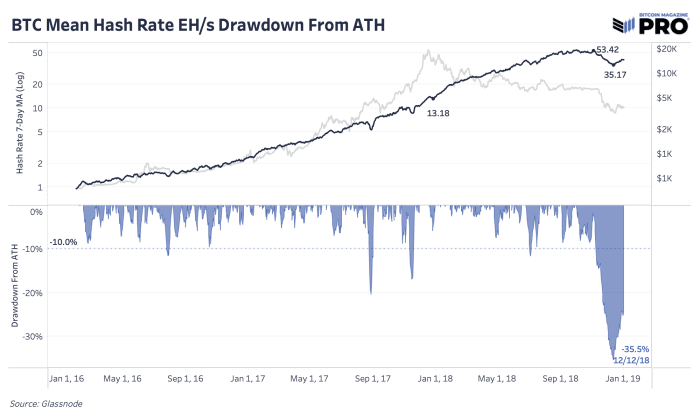

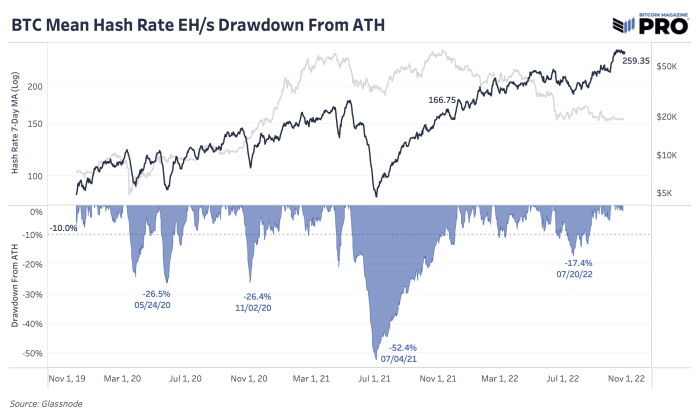

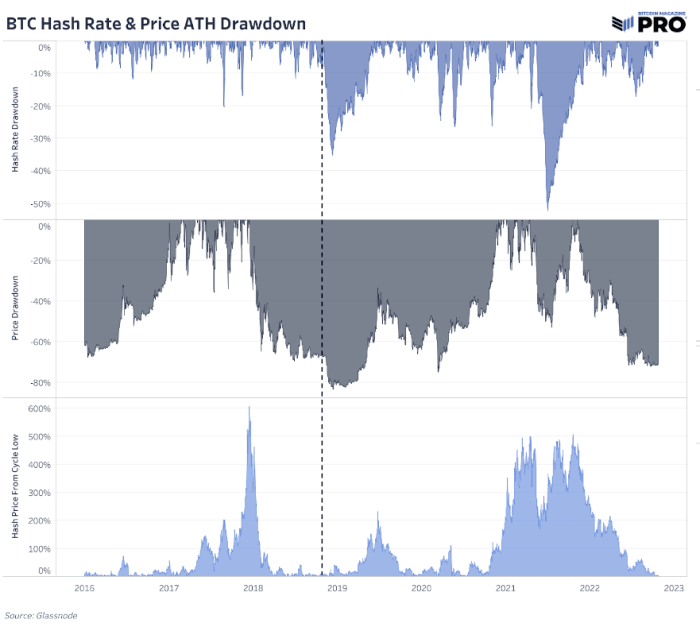

Record Downward Difficulty Adjustment

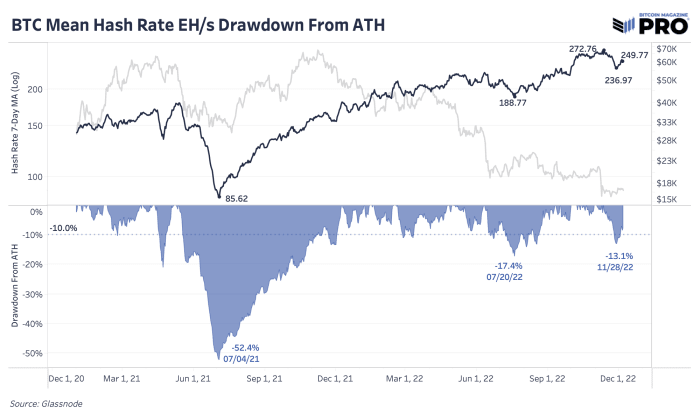

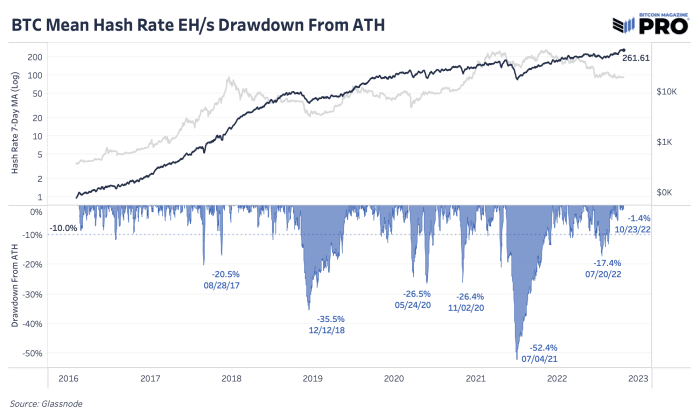

The mining industry continues to take a beating as rising energy inflation, debt burdens and depressed bitcoin prices take their toll. At the end of November, we saw a 13.1% decline in hash rate from all-time highs. However, of the major hash rate declines since 2016, that’s still relatively small compared to the handful of down periods over 15% during that time.

The latest 7.32% downward difficulty adjustment is a direct response to all of that hash rate going offline. As we stand today, the hash rate is right around 250 EH/s and down 7.84% from its all-time high of approximately 273 EH/s. This is the largest downward difficulty adjustment we’ve seen since July 2021, when we saw a series of downward difficulty adjustments following the Chinese mining ban. This should bring some temporary relief to current miners, but it’s too early to say if this trend in declining hash rate has already concluded.

Mining difficulty had its largest drawdown since July 2021

The hash rate drawdown from all-time highs is less than the average bear market

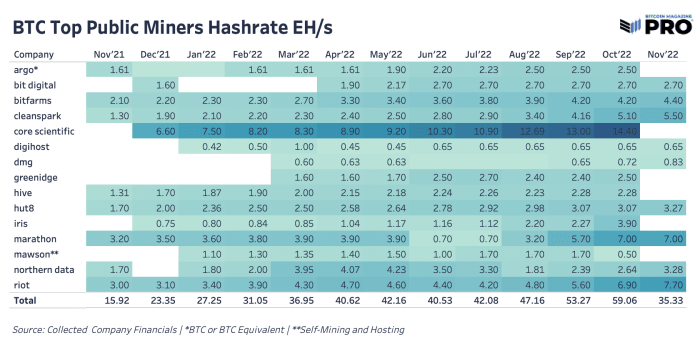

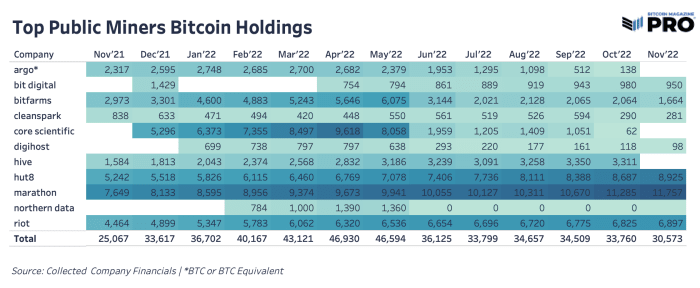

Even with the latest drawdown in hash rate, we’re not seeing announcements come from major public miners. Most public miners’ hash rate is either flat or is growing over the last month.

Public bitcoin miners hash rate remains steady

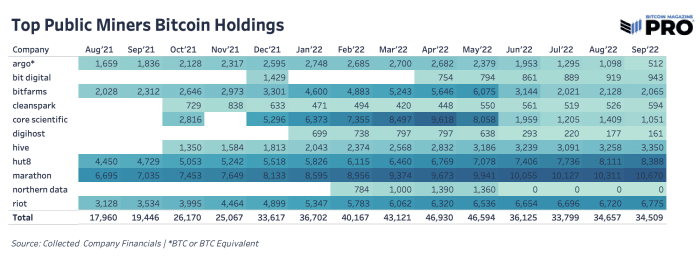

From those who have provided monthly production updates so far, bitcoin holdings are largely rising from the biggest three treasuries across Riot, Marathon and Hut 8 accounting for 27,579 bitcoin. Bitfarms sold a meaningful amount from their treasury which is likely related to paying down their current debt facilities.

Bitcoin holdings are rising from the largest mining companies

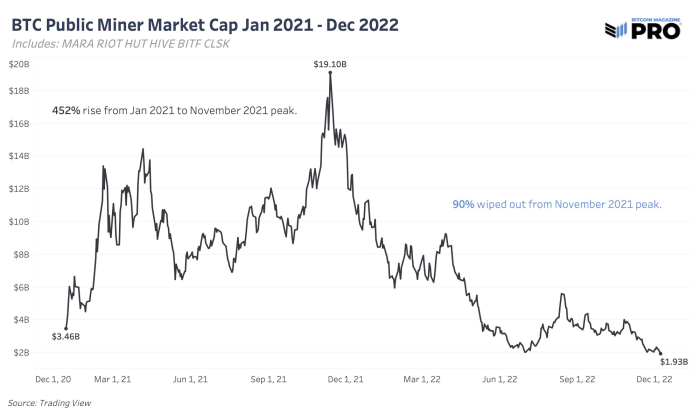

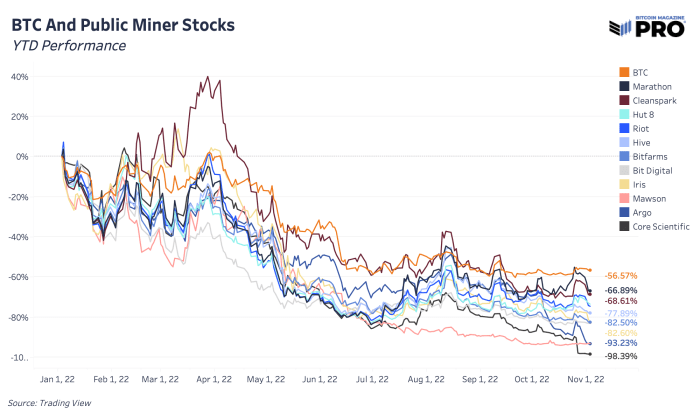

In bitcoin terms, miners’ stock performance continues to fall this year when looking at year-to-date returns versus bitcoin performance. The hash price bear market is alive and well, which has been a core thesis for us when evaluating the current prospects of investing in public miners versus bitcoin. Any miner outperformance in bitcoin short-term has proven to be an opportunity in the market to reprice the equity lower.

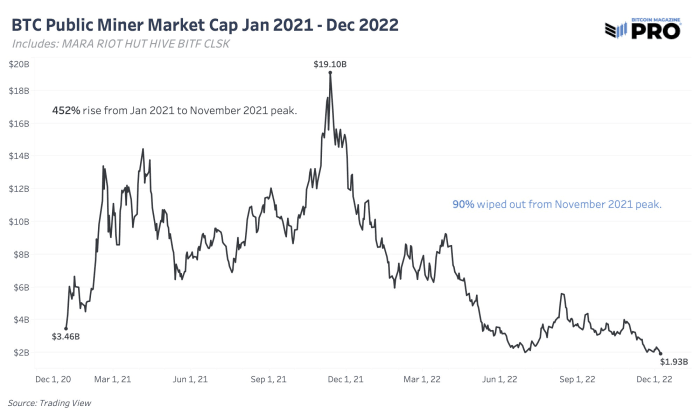

Looking at the market caps of a proxy basket of six public bitcoin miners shows just how much value has been wiped out from 2021. After a 452% rise in value to its November 2021 peak of $19.1 billion, the market wiped out 90% of value in less than a year.

The market cap of public miners has fallen over 90% since all-time highs

While the worst of the drawdown of public miner market capitalizations and hash price (miner revenue per tera hash) has already taken place, we expect that the tough conditions can last for a sustained period of time, squeezing many market participants along the way. The recent downward difficulty adjustment brought about some relief, but it is barely sufficient for many miners who purchased the bulk of their machines in 2021, expecting $30,000 as their “worst-case scenario.”

Throw in an environment where global energy prices and interest rates have skyrocketed and many operations are facing immensely difficult circumstances — particularly hosting facilities where companies serve as intermediaries for customers looking to reap the benefits of mining bitcoin. The elephant in the room for the state of the mining industry is the reality that some of the industry’s biggest hosting facilities are either already bankrupt, teetering on the edge of bankruptcy or are completely out of deployable hash rate for idle ASICs.

We will be intently watching hash rate and the state of the mining industry going forward. Although the industry has been bludgeoned over the course of 2022, we suspect it isn’t out of the woods quite yet.

The beauty of bitcoin and capitalism is that only the strong will survive. Regardless, blocks will continue to be mined every approximately 10 minutes.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

On-Chain Data Trends

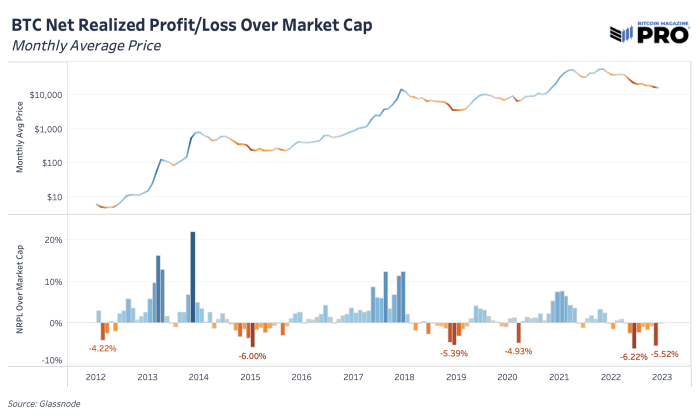

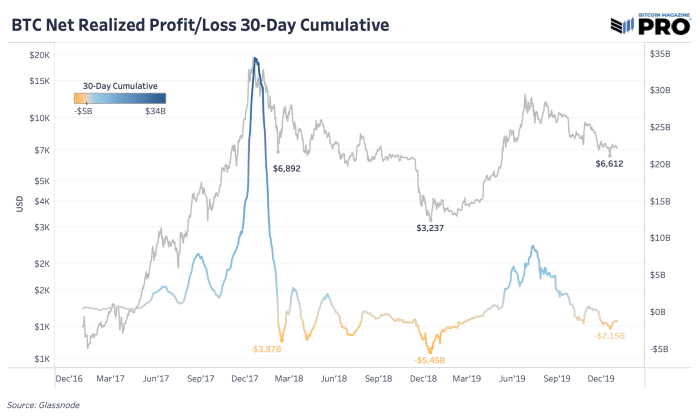

November was a painful month. By looking at on-chain realized profit and loss data, we can see that this was true for many forced-sellers of bitcoin. Before any bitcoin price bottom, a hallmark sign that you want to see is extended periods of forced selling, capitulation and rise in realized losses. One way to view this is by looking at the sum of realized profit and loss for each month relative to bitcoin’s total market cap. We saw these bottom signals in November 2022, and similarly in the July 2022 Terra/LUNA crash, March 2020 COVID fear and December 2018 cycle bottom capitulation events.

Net realized profit/loss over market cap

Looking at the 2018 cycle, the end was marked by excess realized losses, although this was much different with the forced liquidations and cascades of private balance sheet leverage and paper bitcoin unwinding that we saw this year.

30-day cumulative net realized profit/loss

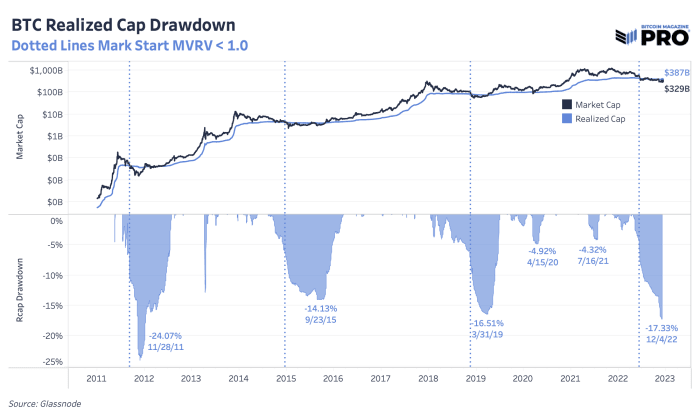

We’ve talked about the current drawdown in bitcoin’s price and how that compares to previous cycles many times over the last few months. Another way to look at cyclical drawdowns is to focus on bitcoin’s realized market capitalization — the average cost basis of the network which tracks the latest price where each UTXO moved last. With price being more volatile, realized price is a more stable view of bitcoin’s growth and capital inflows. The realized market capitalization is now down 17.33% which is significantly higher than 2015 and 2018 cycles of 14.13% and 16.51%, respectively.

Bitcoin realized cap drawdown

As for duration, we’re 176 total days into the price being below bitcoin’s realized price. Those aren’t consecutive days as price can temporarily go above realized price, but price trends below realized price in bear market periods. For context, trends in 2018 were short-lived at around 134 days and the trends in 2014-15 lasted 384 days.

On one hand, bitcoin’s realized market capitalization has taken a significant hit in the previous round of capitulation. That’s a promising bottom-like sign. On the other hand, there’s a case to be made that price being below realized price could easily last another six months from historical cycles and the lack of capitulation in equity markets is still a major headwind and concern.

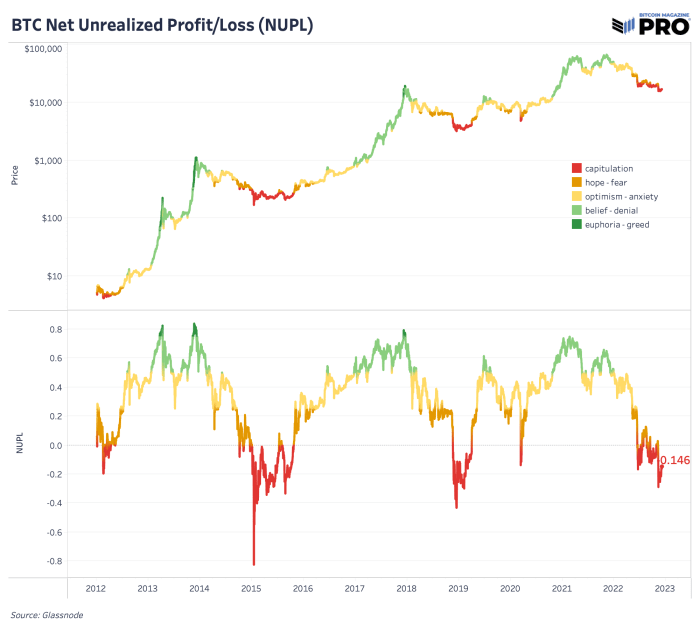

Net unrealized profit/loss

As per the net-unrealized-profit/loss (NUPL) ratio, we are firmly in the capitulation phase. NUPL can be calculated by subtracting the realized cap from market cap and dividing the result by the market cap, as described in this article authored by By Tuur Demeester, Tamás Blummer and Michiel Lescrauwaet.

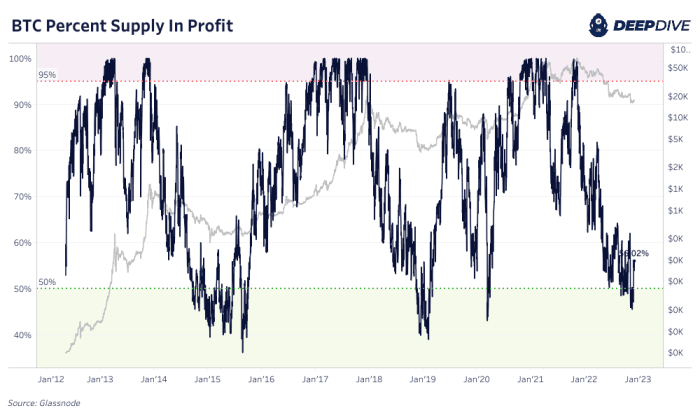

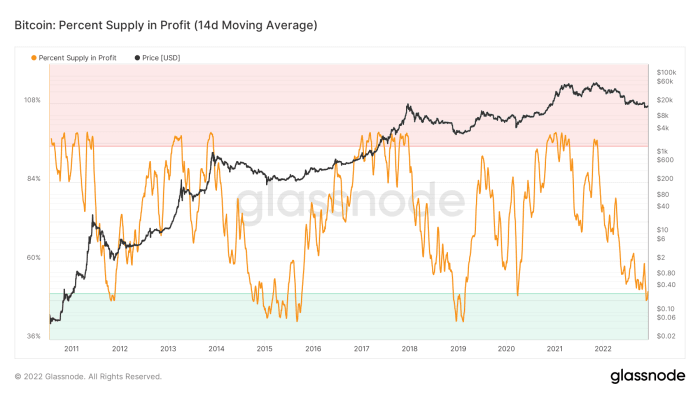

There is no denying it: For bitcoin-native cycles, we are firmly in the capitulation phase. Currently, only 56% of circulating supply was last moved on-chain in profit. On a two-week moving average basis, under 50% supply was last moved above the current exchange rate, which is something that has only ever happened in the depths of previous bear-market lows.

Percent of bitcoin supply in profit

14-day moving average of the percent of bitcoin supply in profit

When thinking of the bitcoin exchange rate, the numerator side of the equation is historically cheap. The Bitcoin network continues to produce a block approximately every 10 minutes in an unabated fashion, as hash rate ticks higher and as the ledger offers an immutable settlement layer for global value. The speculation, leverage and fraud of the previous cycle is washing to shore and bitcoin continues to exchange hands.

Bitcoin is objectively cheap relative to its all time history and adoption phases. The real question over the immediate future is the denominator. We have talked at length about the global liquidity cycle and its current track. Despite being historically cheap, bitcoin is not immune to a sudden strengthening in the dollar because nothing truly is. Exchange rates are relative and if the dollar is squeezing higher, then everything else will subsequently fall — at least momentarily. As always, position sizing and time preference is key for all.

As for the catalyst for a surge higher in the dollar denominator of the bitcoin exchange rate (BTC/USD), there are 80 trillion possible catalysts…

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Powell’s Speech And Contracting ISM PMI

We want to zoom out and revisit the broader macroeconomic picture and analyze some of the latest data that came out this week, which will heavily influence the market direction over the next few months.

After Jerome Powell’s Brooking Institution speech, it’s clear that markets are chomping at the bit to move higher with any possible Federal Reserve narrative and pivot scenario. There’s over hedging, short squeezes, options market dynamics and forced buying. This is beyond our expertise to say exactly why markets are exploding with volatility on any given data point or new Powell speech. However, these types of events and market movements have nearly always been a sign of unhealthy and heightened volatile swings in bear markets. Despite more talk from Powell with nothing new really said, markets perceived the speech as more “dovish” with his commentary around the concern of overdoing rate hikes. Yet, if this is another bear market rally taking shape for the major indices, we seem to be close to that rally turning over yet again.

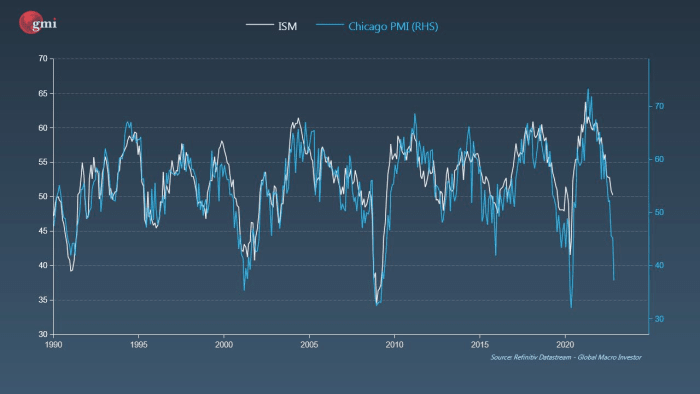

What is also concerning and expected to continue, is the trend of economic contraction as told by the data from the ISM manufacturing index (PMI). Today’s latest release shows a print of 49.0 below market expectations of 49.7. New orders are contracting, the backlog of orders are contracting and prices are decreasing. By all measures and survey responses, these are the signs of demand softening, conditions worsening and the economy moving into more cautious territory. The ISM PMI data highly correlates to the less impactful Chicago PMI data which just printed contraction lows similar to 2000, 2008 and 2020. This is the sign of an economic recession starting in the manufacturing sector.

What does economic contraction mean for financial markets? It’s typically bad news when there’s a sustained contraction trend of ISM PMI below 50 and even below 40s playing out. It seems we’re in the early stages of a larger contraction trend playing out: The despair phase of the market.

The specific question for the bitcoin and macro relationship is now: Was this industry-leverage wipeout and capitulation event enough selling to mute the potential probability and effects of an equity bear market meltdown? Will bitcoin flatline and form a bottom if equities are to follow similar past bear market drawdown paths?

We’ve still yet to see a real blowout in stock market volatility which has always impacted bitcoin. It’s been a core part of our thesis this year that bitcoin will follow traditional equity markets to the downside.

The magnitude of the long-duration debt in real terms was, and still is, the biggest story here.

Furthermore, what does this mean going forward for asset valuations?

The below is an excerpt from the Bitcoin Magazine Pro report on the rise and fall of FTX. To read and download the entire 30-page report, follow this link.

The Beginnings

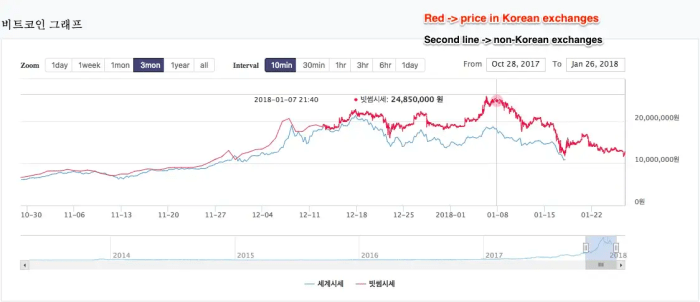

Where did it all start for Sam Bankman-Fried? As the story goes, Bankman-Fried, a former international ETF trader at Jane Street Capital, stumbled upon the nascent bitcoin/cryptocurrency markets in 2017 and was shocked at the amount of “risk-free” arbitrage opportunity that existed.

In particular, Bankman-Fried said the infamous Kimchi Premium, which is the large difference between the price of bitcoin in South Korea versus other global markets (due to capital controls), was a particular opportunity that he took advantage of to first start making his millions, and eventually billions …

The real story, while possibly similar to what SBF liked to tell to explain the meteoric rise of Alameda and subsequently FTX, looks to have been one riddled with deception and fraud, as the “smartest guy in the room” narrative, one that saw Bankman-Fried on the cover of Forbes and touted as the “modern day JP Morgan,” quickly changed to one of massive scandal in what looks to be the largest financial fraud in modern history.

The Start Of The Alameda Ponzi

As the story goes, Alameda Research was a high-flying proprietary trading fund that used quantitative strategies to achieve outsized returns in the cryptocurrency market. While the story was believable on the surface, due to the seemingly inefficient nature of the cryptocurrency market/industry, the red flags for Alameda were glaring from the start.

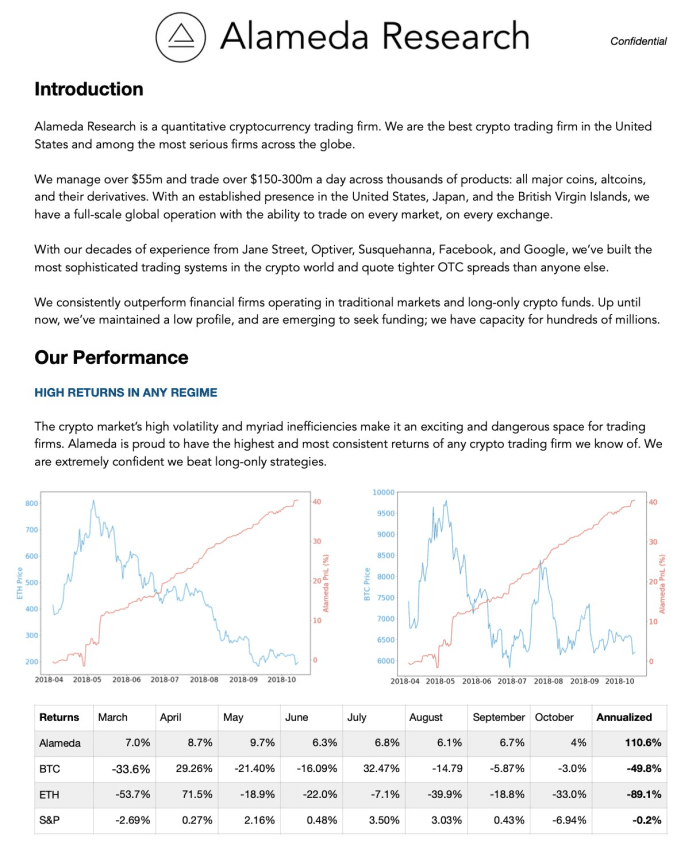

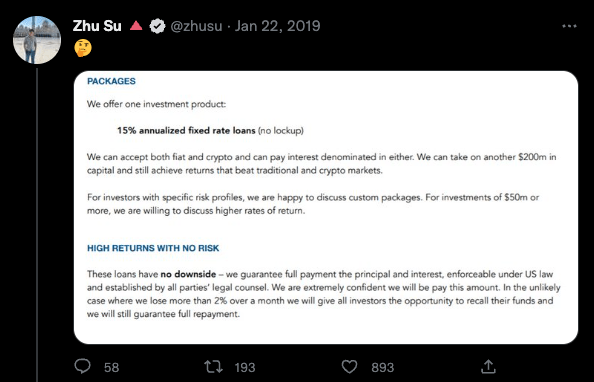

As the fallout of FTX unfolded, previous Alameda Research pitch decks from 2019 began to circulate, and for many the content was quite shocking. We will include the full deck below before diving into our analysis.

The deck contains many glaring red flags, including multiple grammatical errors, including the offering of only one investment product of “15% annualized fixed rate loans” that promise to have “no downside.”

All glaring red flags.

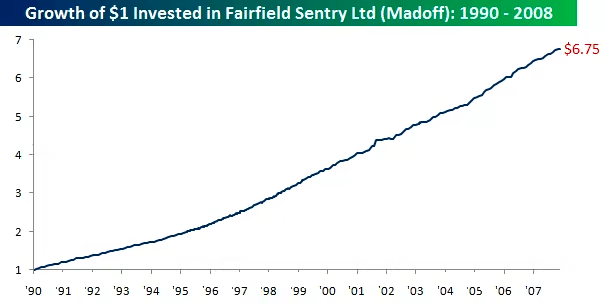

Similarly, the shape of the advertised Alameda equity curve (visualized in red), which seemingly was up and to the right with minimal volatility, while the broader cryptocurrency markets were in the midst of a violent bear market with vicious bear market rallies. While it is 100% possible for a firm to perform well in a bear market on the short side, the ability to generate consistent returns with near infinitesimal portfolio drawdowns is not a naturally occurring reality in financial markets. Actually, it is a tell-tale sign of a Ponzi scheme, of which we have seen before, throughout history.

The performance of Bernie Madoff’s Fairfield Sentry Ltd for nearly two decades operated quite similarly to what Alameda was promoting via their pitch deck in 2019:

Up-only returns regardless of broader market regime

Minimal volatility/drawdowns

Guaranteeing the payout of returns while fraudulently paying out early investors with the capital of new investors

Stated returns by Bernie Madoff’s fund

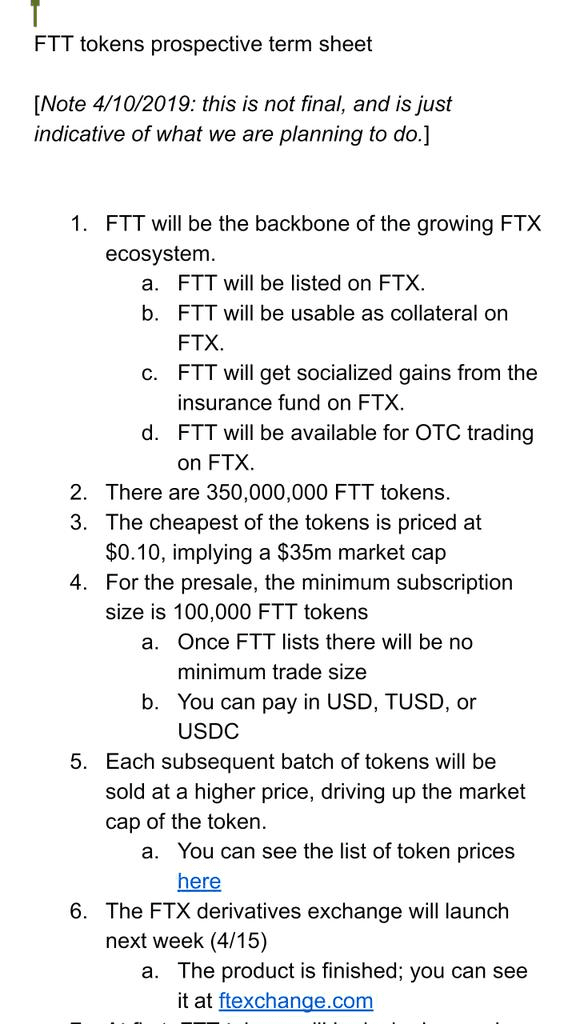

It appears that Alameda’s scheme began to run out of steam in 2019, which is when the firm pivoted to creating an exchange with an ICO (initial coin offering) in the form of FTT to continue to source capital. Zhu Su, the co-founder of now-defunct hedge fund Three Arrows Capital, seemed skeptical.

Approximately three months later, Zhu took to Twitter again to express his skepticism about Alameda’s next venture, the launch of an ICO and a new crypto derivatives exchange.

“These same guys are now trying to launch a “bitmex competitor” and do an ICO for it. 🤔” – Tweet, 4/13/19

Beneath this tweet, Zhu said the following while posting a screenshot of the FTT white paper:

“Last time they pressured my biz partner to get me to delete the tweet. They started doing this ICO after they couldn’t find any more greater fools to borrow from even at 20%+. I get why nobody calls out scams early enough. Risk of exclusion higher than return from exposing.” – Tweet, 4/13/19

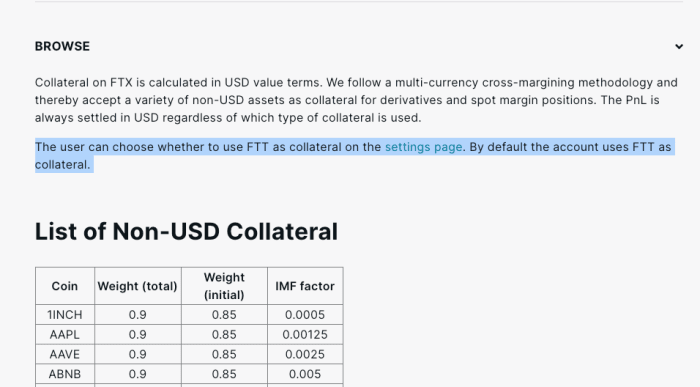

Additionally, FTT could be used as collateral in the FTX cross-collateralized liquidation engine. FTT received a collateral weighting of 0.95, whereas USDT & BTC received 0.975 and USD & USDC received a weighting of 1.00. This was true until the collapse of the exchange.

The FTT token was described as the “backbone” of the FTX exchange and was issued on Ethereum as a ERC20 token. In reality, it was mostly a rewards based marketing scheme to attract more users to the FTX platform and to prop up balance sheets. Most of the FTT supply was held by FTX and Alameda Research and Alameda was even in the initial seed round to fund the token. Out of the 350 million total supply of FTT, 280 million (80%) of it was controlled by FTX and 27.5 million made their way to an Alameda wallet.

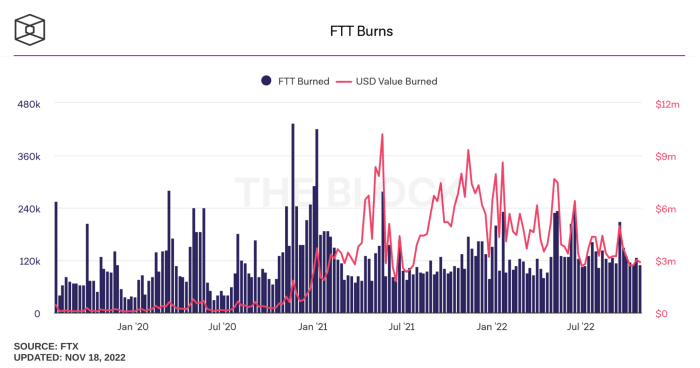

FTT holders benefited from additional FTX perks such as lower trading fees, discounts, rebates and the ability to use FTT as collateral to trade derivatives. To support FTT’s value, FTX routinely purchased FTT tokens using a percentage of trading fee revenue generated on the platform. Tokens were purchased and then burned weekly to continue driving up the value of FTT.

FTX repurchased burned FTT tokens based on 33% of fees generated on FTX markets, 10% of net additions to a backstop liquidity fund and 5% of fees earned from other uses of the FTX platform. The FTT token does not entitle its holders to FTX revenue, shares in FTX nor governance decisions over FTX’s treasury.

Alameda’s balance sheet was first mentioned in this Coindesk article showing that the fund held $3.66 billion in FTT tokens while $2.16 billion of that was used as collateral. The game was to drive up the perceived market value of FTT then use the token as collateral to borrow against it. The rise of Alameda’s balance sheet rose with the value of FTT. As long as the market didn’t rush to sell and collapse the price of FTT then the game could continue on.

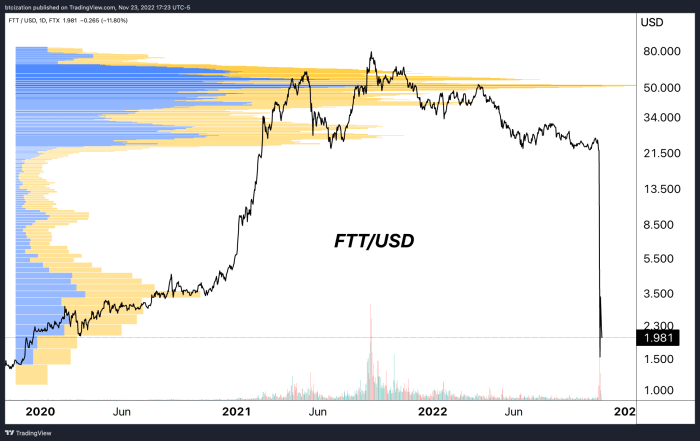

FTT rode on the backs of the FTX marketing push, rising to a peak market cap of $9.6 billion back in September 2021 (not including locked allocations, all the while Alameda leveraged against it behind the scenes. The Alameda assets of $3.66b FTT & $2.16b “FTT collateral” in June of this year, along with its OXY, MAPs, and SRM allocations, were combined worth tens of billions of dollars at the top of the market in 2021.

The price of FTT with a side profile showing FTT trading volume on FTX (logarithmic scale)

FTT Market Cap (logarithmic scale) – Source:CoinMarketCap

CZ Chooses Blood

In one decision and tweet, CEO of Binance, CZ, kicked off the toppling of a house of cards that in hindsight, seems inevitable. Concerned that Binance would be left holding a worthless FTT token, the company aimed to sell $580 million of FTT at the time. That was bombshell news since Binance’s FTT holdings accounted for over 17% of the market cap value. This is the double edged sword of having the majority of FTT supply in the hands of a few and an illiquid FTT market that was used to drive and manipulate the price higher. When someone goes to sell something big, value collapses.

As a response to CZ’s announcement, Caroline of Alameda Research, made a critical mistake to announce their plans to buy all of Binance’s FTT at the current market price of $22. Doing that publicly sparked a wave of market open interest to place their bets on where FTT would go next. Short sellers piled in to drive the token price to zero with the thesis that something was off and the risk of insolvency was in play.

Ultimately, this scenario has been brewing since the Three Arrows Capital and Luna collapsed this past summer. It’s likely that Alameda had significant losses and exposure but were able to survive based on FTT token loans and leveraging FTX customer funds. It also makes sense now why FTX had an interest in bailing out companies like Voyager and BlockFi in the initial fallout. Those firms may have had large FTT holdings and it was necessary to keep them afloat to sustain the FTT market value. In the latest bankruptcy documents, it was revealed that $250 million in FTT was loaned to BlockFi.

With hindsight, now we know why Sam was buying up all of the FTT tokens he could get his hands on every week. No marginal buyers, lack of use cases and high risk loans with the FTT token were a ticking time bomb waiting to blow up.

How It All Ends

After pulling back the curtain, we now know that all of this led FTX and Alameda straight into bankruptcy with the firms disclosing that their top 50 creditors are owed $3.1 billion with only a $1.24 cash balance to pay it. The company likely has over a million creditors that are due money.

The original bankruptcy document is riddled with glaring gaps, balance sheet holes and a lack of financial controls and structures that were worse than Enron. All it took was one tweet about selling a large amount of FTT tokens and a rush for customers to start withdrawing their funds overnight to expose the asset and liability mismatch FTX was facing. Customer deposits weren’t even listed as liabilities in the balance sheet documents provided in the bankruptcy court filing despite what we know to be around $8.9 billion now. Now we can see that FTX never had really backed or properly accounted for the bitcoin and other crypto assets that customers were holding on their platform.

It was all a web of misallocated capital, leverage and the moving of customer funds around to try and keep the confidence game going and the two entities afloat.

.

.

.

This concludes an excerpt from “The FTX Ponzi: Uncovering The Largest Fraud In Crypto History.” To read and download the full 30-page report, follow this link.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Speculation And Yields

This cycle has been super charged by speculation and yield, leading all the way back to the initial Grayscale Bitcoin Trust premium arbitrage opportunity. That opportunity in the market incentivized hedge funds and trading shops from all over the world to lever up in order to capture the premium spread. It was a ripe time for making money, especially back in early 2021 before the trade collapsed and switched to the significant discount we see today.

The same story existed in the perpetual futures market where we saw 7-day average annualized funding rates reach up to 120% at peak. This is the implied annual yield that long positions were paying in the market to short positions. There were an abundance of opportunities in the GBTC and futures markets alone for yield and quick returns to be had — without even mentioning the bucket of DeFi, staking tokens, failed projects and Ponzi schemes that were generating even higher yield opportunities in 2020 and 2021.

There’s an ongoing, vicious feedback loop where higher prices drive more speculation and leverage, which, in turn, drive higher yields. Now, we’re dealing with this cycle in reverse. Lower prices wipe out more speculation and leverage while washing out any “yield” opportunities. As a result, yields everywhere have collapsed.

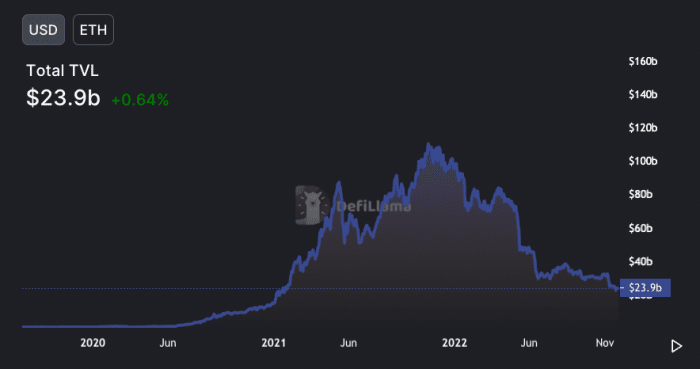

“Total value locked” in the Ethereum DeFi ecosystem surpassed over $100 billion in 2021 during the speculative mania, and is now a mere $23.9 billion today. This leverage-fueled mania in the crypto ecosystem fueled the growth of the “yield” products offered by the market, most of which have all collapsed now that the figurative tide has drawn out.

The total value locked in Ethereum DeFi ecosystem has mostly disappeared

This dynamic brought about the rise of bitcoin and cryptocurrency yield-generating products, from Celsius to BlockFi to FTX and many more. Funds and traders capture a juicy spread while kicking back some of those profits to the retail users who keep their coins on exchanges to get a small amount of interest and yield. Retail users know little about where the yield comes from or the risks involved. Now, all of those short-term opportunities in the market seem to have evaporated.

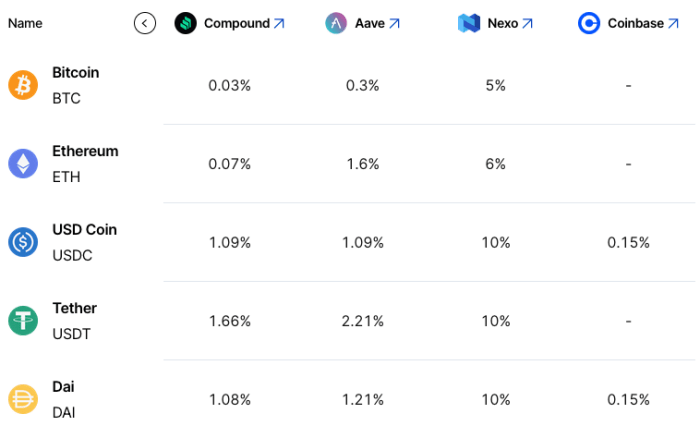

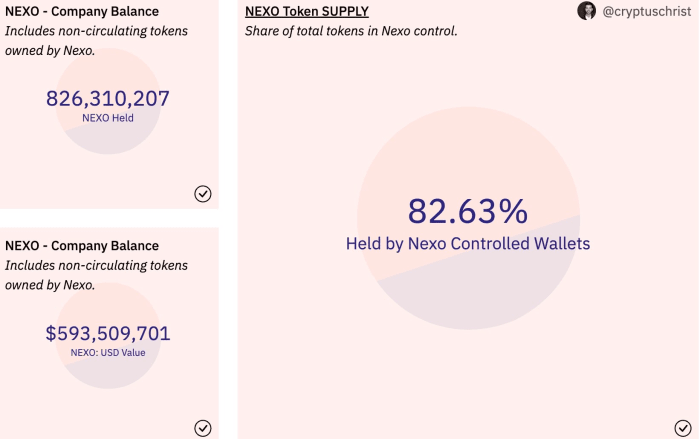

With all of the speculative trades and yield gone, how can companies still offer such high-yielding rates that are well above traditional “risk-free” rates in the market? Where does the yield come from? Not to single out or FUD any specific companies, but take Nexo for example. Rates for USDC and USDT are still at 10% versus 1% on other DeFi platforms. The same goes for bitcoin and ethereum rates, 5% and 6% respectively, while other rates are largely nonexistent elsewhere.

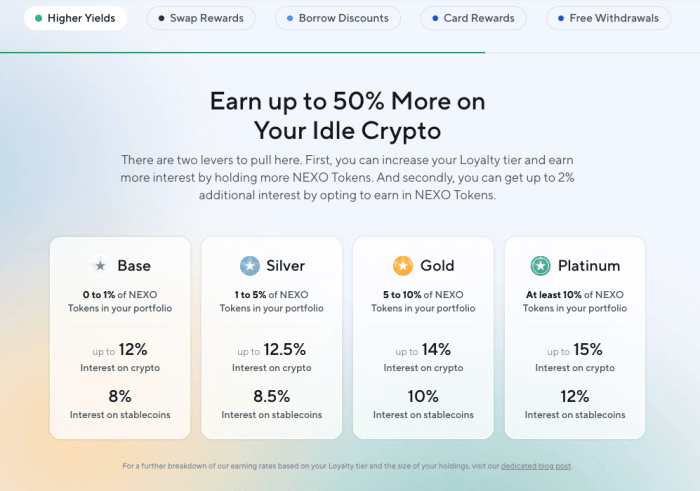

These high borrow rates are collateralized with bitcoin and ether offering a 50% LTV (loan-to-value ratio) while a number of other speculative tokens can be used as collateral as well at a much lower LTV. Nexo shared a detailed thread on their business operations and model. As we’ve found out time and time again, we can never know for sure which institutions to trust or not to trust as this industry de-leveraging continues. However, the main questions to ask are:

Will a 13.9% loan demand be a sustainable business model going forward into this bear market? Won’t rates have to come down further?

Regardless of Nexo’s risk management practices, are there heightened counterparty risks currently for holding customer balances on numerous exchanges and DeFi protocols?

Rates on different DeFi lending platforms

Current rates on Nexo’s yield-generating offerings

Statistics for Nexo’s company holdings

Here is what we know:

The crypto-native credit impulse — a metric that is not perfectly quantifiable but imperfectly observable via a variety of datasets and market metrics — has plunged from its 2021 euphoric highs and now looks to be extremely negative. This means that any remaining product that is offering you crypto-native “yield” is likely to be under extreme duress, as the arbitrage strategies that fueled the explosion in yield products throughout the bull market cycle have all disappeared.

What remains, and what will emerge from the depths of this bear market will be the assets/projects built on the strongest of foundations. In our view, there is bitcoin, and there is everything else.

Readers should evaluate counterparty risk in all forms, and stay away from any of the remaining yield products that exist in the market.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Genesis Looks For Liquidity Injection

If you don’t know about Genesis Trading perhaps you should. They represent the backbone infrastructure of the institutional investor base in the bitcoin and broader crypto markets. For lending, trading, hedging, exchange yields and more, Genesis Trading was the brokerage to facilitate all of this activity in the space. Remember those juicy yields from the BlockFi and Gemini Earn products in the space? Genesis is the middleman between those platforms and hedge funds to generate that yield.

Genesis held a short client call to announce the suspension of redemptions, withdrawals and new loan originations. With exposure to FTX and Alameda Research, the company now needs another liquidity injection after having nearly $175 million locked in a trading account with FTX. As an initial response, parent company Digital Currency Group (DCG, the parent company of Grayscale), injected $140 million into the business to keep operations running smoothly. Yet, Genesis is now scrambling to find more capital. It’s the reason Gemini Earn had to halt withdrawals.

Although Gemini has been vocal that the rest of their operations are working normally, limiting the Gemini Earn product and having service outages across the platform seem to have sparked a small rush to get bitcoin off the exchange: 13% of the total bitcoin balance has left over the last 24 hours. As we’ve highlighted before, exchanges are not the place for your bitcoin, especially when there’s a high probability that there is another exchange (or even multiple) left to fall.

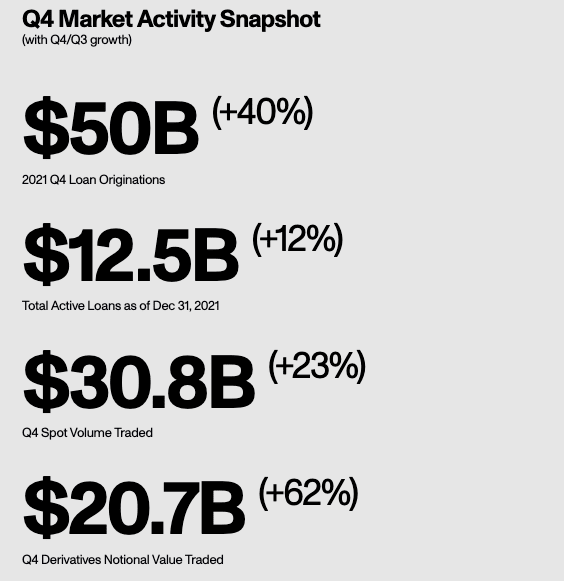

To give you an idea of size, Genesis had $50 billion in loan originations in one quarter and a $12.5 billion active loan book at the peak of the market back in 2021. Yet, loan originations and the active loan book both took a hefty haircut, falling to $8.4 billion and $2.8 billion respectively, as of the third quarter of this year. Back in July, Genesis filed a $1.2 billion claim against Three Arrows Capital that was picked up by DCG to keep the hit off Genesis’ books. Loans were partially collateralized with shares of GBTC, ETHE, AVAX and NEAR tokens.

We know from on-chain activity that Genesis had tons of interactions with Alameda, Gemini and BlockFi through their OTC trading desk; FTT was also a top token received and sent in that activity. Without Genesis sharing more details, we don’t know the extent of the exposure and capital needed to make customers whole. Yet, the fact that the parent company DCG hasn’t already stepped in to provide another liquidity injection is a warning sign on where this might end up. News surfaced that Genesis is seeking a $1 billion credit facility immediately. Not good.

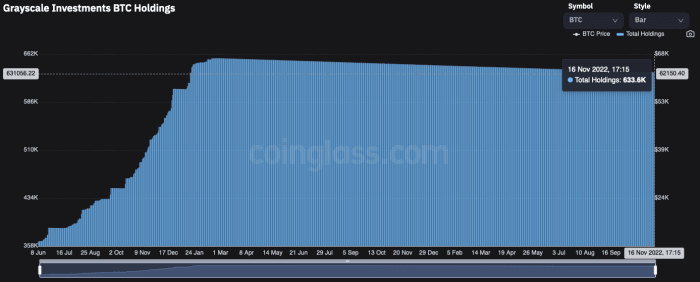

In the worst-case scenario, the lack of funding supplied by DCG could spark questions around accessible liquid assets. DCG and Grayscale have dissolved trusts before and that option is not off the table. It’s an unlikely path but certainly one to highlight since Grayscale is the largest holder of bitcoin via the Grayscale Bitcoin Trust, holding nearly 633,600 bitcoin. Easily, this could be a regulatory issue or another limitation (that we don’t know about) where DCG cannot supply the capital to Genesis.

Circle, the issuer of the stablecoin USDC, also has ties to Genesis. Yet, they highlight that their Circle Yield product only accounts for $2.6 million in collateralized loans outstanding which, if true, is fairly insignificant.

We will likely hear more about the state of Genesis in the coming days since they want/need the capital injection by Monday. This would be a massive hit to a laundry list of institutions in the industry if withdrawals remain suspended and funds tied up. Genesis reflects the exact reason why the overall contagion of the FTX and Alameda Research collapse has yet to play out. Defaults and insolvencies come in waves, not all at once. It takes weeks and months to see where the biggest holes are and who is having liquidity, counterparty and/or insolvency troubles.

On top of that, nearly every major player and market maker has pulled their cash from exchanges to shore up their own balance sheets and decrease counterparty risk. Liquidity in the market is thin and the time is ripe for volatility to ensue. Although the market has seemed to find a temporary bottom amid all of the negative news headlines over the last week, the unknown downside risk still far outweighs the upside potential in the short term.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

We’re currently in the middle of the industry contagion and market panic taking shape. Although FTX and Alameda have fallen, many more players across funds, market makers, exchanges, miners and other businesses will follow suit. This is a similar playbook to what we’ve seen before in the previous crash sparked by Luna, except that this one will be more impactful to the market. This is the proper cleansing and washout from the misallocation of capital, speculation and excessive leverage that come with the global economic liquidity tide going back out.

That said, everyone is quick to jump on the next domino to fall. It’s natural. Most information surrounding balance sheets and hidden leverage in the system is unknown while new information and developments in real time are flowing out every half hour, it seems. Exchanges are under the spotlight right now and the market is watching their every move and transaction. There’s likely no exchange that is going to be as egregious with client funds as FTX and Alameda were, but we don’t know which exchanges can or cannot survive a bank run.

As shown by the market’s reaction, Crypto.com’s Cronos token (CRO), fell 55% in a week before getting some relief over the last day. There’s been a parabolic trend of withdrawals — a bank run — on the exchange over the last two days with the CEO doing the media rounds to assure everyone that withdrawals are processing fine and that they will survive.

Huobi token (HT) follows the same path, down nearly 60% in the last two weeks. Huobi recently provided their list of assets on the platform, showing around $900 million in HT owned by both Huobi Global and Huobi users. It’s not clear what percentage of that $900 million is owned by Huobi Global, but it’s quite the haircut. Exchanges everywhere have been scrambling to provide some version of proof of reserves in attempting to calm the market.

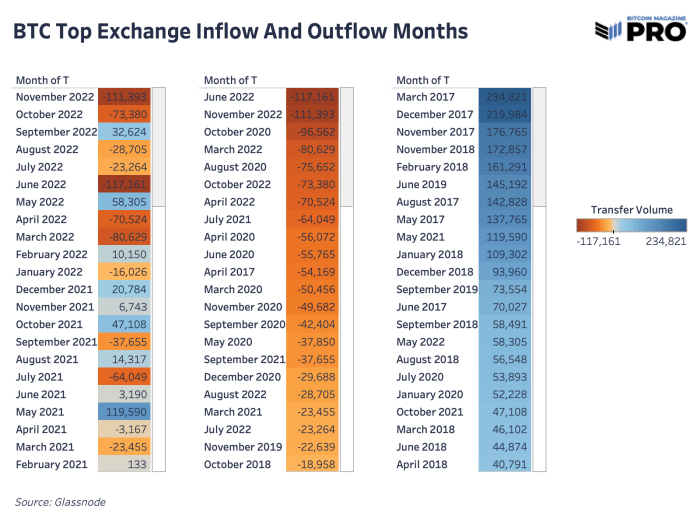

In terms of bitcoin leaving exchanges, it’s been a similar trend for the last three major market panic events: the March 2020 COVID crash, the Luna crash and now the FTX and Alameda crash. Bitcoin flies off exchanges as exchange and counterparty risk becomes priority No. 1 to mitigate. Overall, this is a welcome trend with over 122,000 bitcoin flowing out of exchanges over the last 30 days. It’s the lack of transparency, trust and excessive leverage in centralized institutions that have fueled the latest fall.

Having more of the bitcoin supply in self-custody is the way to counter this risk in the future. That said, assuming all of this bitcoin is going to self-custody and is intended to not come back to the market is a broad, unlikely assumption. Likely, market participants are taking whatever precaution they can regardless if their intent is to store this bitcoin long-term versus sending it back to an exchange later on.

In previous times, bitcoin flowing in and out of exchanges was more of a signal for price, but as more paper bitcoin, wrapped bitcoin on other chains and bitcoin financial products have grown, bitcoin exchange flows are more reflective of current user trends despite the last two major exchange outflows marking local price bottoms. Just 12.02% of bitcoin supply lives on exchanges today, down from its 2020 high of 17.29%. Although we’re only halfway through the month, November 2022 is shaping up to be the largest outflow month in history.

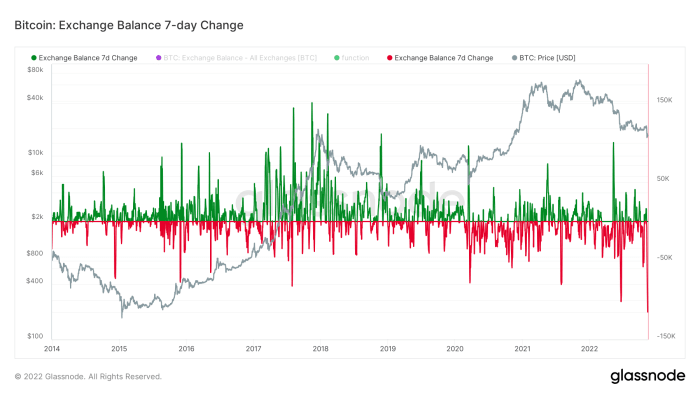

Bitcoin balances on exchanges continues to trend down since March 2020.

Bitcoin is leaving exchanges at a record pace.

The silver lining of the industry’s largest-ever exchange collapse is that a broad sense of distrust in counterparties and self-sovereign practices are set to increase among buyers of bitcoin going forward. While many have been speaking for over a decade on the importance of personal custody for the world’s first decentralized digital bearer asset, it often fell on deaf ears, as financial institutions like FTX seemed credible and trustworthy. Fraud assuredly can change that.

This dynamic, and the potential for greater amounts of contagion among the crypto space, has users fleeing to personal custody, with this past week bringing in the largest week-over-week decline in bitcoin on exchanges at -115,200 BTC.

This past week was the largest week-over-week decline in bitcoin on exchanges.

Interestingly enough, this sell-off was unique in the sense that unlike previous sell-offs in recent years, it wasn’t triggered by a flood of bitcoin being sent to exchanges, instead moreso by an implosion of illiquid crypto collateral without many (or in the case of FTT, any) natural buyers.

Given our immense focus on the risks of crypto-native contagion over the previous six months, we highly recommend our readers learn about and look into the prospects of self-custody; if nothing else, for the ease of mind.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Latest Public Miner Developments