[ad_1]

Sure, investing in these ETFs means you’ll forfeit 15% of your dividends to withholding tax. Yet, for many, it’s a worthwhile trade-off to gain access the most significant U.S. equity index—a benchmark that, according to the Standard & Poor’s Indices Versus Active (SPIVA) report, has outperformed 88% of all U.S. large-cap funds over the past 15 years.

But hold on, these aren’t your only choices. And here’s something you might not know: they aren’t even the cheapest around. Just like opting for no-name brands at the store can offer the same quality for a lower price, other ETF managers have been quietly rolling out competing U.S. equity index ETFs that come with even lower fees. Here’s what you need to know to make an informed choice.

Exploring cheaper alternatives to the well-known S&P 500 ETFs—like VFV, ZSP and XUS—leads us to a pair of lesser known but highly competitive options: the TD U.S. Equity Index ETF (TPU) and the Desjardins American Equity Index ETF (DMEU). Launched in March 2016 and April 2024, respectively, these ETFs track the Solactive US Large Cap CAD Index (CA NTR) and the Solactive GBS United States 500 CAD Index. The “CA NTR” stands for “net total return,” which means the index accounts for after-withholding tax returns, providing a more accurate measure of what Canadian investors might take home.

Essentially, these indices offer U.S. equity exposure without the licensing costs associated with the brand-name S&P 500 index, which is a significant advantage for keeping expenses low. You can think of Solactive as the RC Cola of the indexing industry, and S&P Global as Coca-Cola, and MSCI as Pepsi.

For TPU, the management fee is set at 0.06%, with a total MER of 0.07%. DMEU charges a management fee of just 0.05%. Since it hasn’t been trading for a full year yet, its MER is still to be determined but is expected to be competitively low.

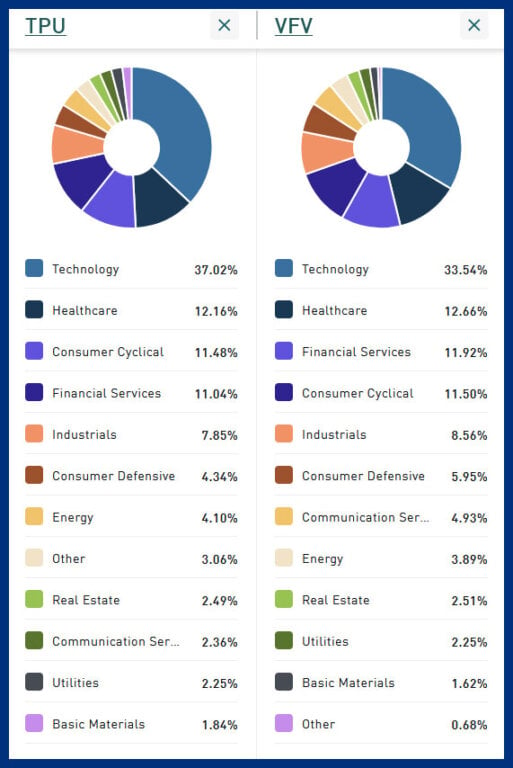

In terms of portfolio composition, there’s scant difference between the these ETFs: VFV, TPU and DMEU. Glance at the top 10 holdings, and you’ll see the weightings of these ETFs reveals very similar exposure, with only minor deviations. Similarly, when comparing sector allocations between TPU and VFV, they align closely, reflecting a consistent approach to capturing the broad U.S. equity market. However, look a bit deeper into the technical aspects, the indices that these ETFs track—the Solactive indices for TPU and DMEU versus the S&P 500 for VFV—exhibit some notable differences.

The S&P 500 is not as straightforward as it might seem, though. It doesn’t just track the 500 largest U.S. stocks. Instead, what is included is at the discretion of a committee, subject to eligibility criteria including market capitalization, liquidity, public float and positive earnings. This makes it more stringent and somewhat more active than you might have thought.

In contrast, the Solactive indices used by TPU and DMEU are more passive. They simply track the largest 500 U.S. stocks by market cap, with minimal additional screening criteria. This straightforward approach lends a more passive characteristic to these indices compared to the S&P 500.

[ad_2]

Tony Dong

Source link