[ad_1]

U.S. Steel Stock Soars on $14.9 Billion Acquisition by Nippon Steel

[ad_2]

[ad_1]

Streaming customers are likely to see more familiar faces and less megabudget content in the coming year.

Shifting consumer tastes and corporate strategies portend changes in programming, with artificial intelligence looming in the background, as major streaming services consider how to use technology and new forms of programming without escalating annual multibillion-dollar content budgets.

“The big quandary is, how do we make [services] profitable? Things have shifted so dramatically and so quickly in how people consume,” Cole Strain, head of research and development at Samba TV, which tracks viewership of shows, said in an interview. “The streamers that find out what consumers truly want — they win.”

Streaming services are facing some big choices, noted Jacqueline Corbelli, CEO of software company BrightLine. “The cost of the content and the length of the content war will force them to make some major decisions. They are trying to figure it out,” she said in an interview.

“Great content has to be paid for, and investors want to see an increasingly efficient and profitable business,” she said, adding: “Right now the economics of these are at odds with one another.”

This year’s prolonged Hollywood strikes, the prevalence of up-close-and-personal sports documentaries and the increased licensing of older cable-TV shows are the most tangible evidence so far of how content is evolving. Throw in cost-cutting, and customers of services like Netflix Inc.

NFLX,

Walt Disney Co.’s

DIS,

Disney+ and Hulu, and Amazon.com Inc.’s

AMZN,

Prime Video are looking at a vastly different content landscape.

What’s at stake? Streaming’s big guns continue to spend lavishly in the pursuit of engagement, which is the single most important metric in media. During its third-quarter earnings calls, Netflix said it would spend $17 billion on content in 2024, while Disney pledged $25 billion, including sports rights.

“‘I think when it comes to creativity, quality is critical, of course, and quantity in many ways can destroy quality.’”

Complicating matters and raising the urgency is the pressure, particularly at Disney, to cut costs. The very future of blockbuster movies is also in doubt in the wake of box-office misfires such as “Wish,” “Indiana Jones and the Dial of Destiny” and the latest Marvel entries, “Ant-Man and the Wasp: Quantumania” and “The Marvels.”

“One of the reasons I believe it’s fallen off a bit is that we were making too much,” Disney CEO Bob Iger said at a recent employee town hall meeting in New York City. “I think when it comes to creativity, quality is critical, of course, and quantity in many ways can destroy quality. Storytelling, obviously, is the core of what we do as a company.”

Also read: Disney CEO Bob Iger walks back comments about asset sales

Speaking at the New York Times DealBook Summit last week, Iger acknowledged that “the movie business is changing. Box office is about 75% of what it was pre-COVID.” Noting the $7 monthly fee for a Disney+ subscription, he said the experience of viewing content from home on large TV screens is both more convenient and less expensive than going to the movie theater.

Iger’s task is significantly more fraught than those faced by his rivals. He is in the midst of a turnaround at Disney aimed at making streaming profitable and is simultaneously fending off yet another proxy fight from activist investor Nelson Peltz.

Part of Iger’s plan is to slash costs. Of the $7.5 billion Disney intends to save in 2024, $4.5 billion will come out of the content budget. Previously, the company was aiming at a $3 billion content cut out of a total annual reduction of $5.5 billion. Disney plans to spend $25 billion on content in 2024, down from $27.2 billion in 2023 and a record $29.9 billion in 2022.

Read more: Bob Iger: ‘I was not seeking to return’ as Disney CEO

What streamers have done so far hews closely to the classic TV model of producing original movies and series, broadcasting live sporting events and throwing in licensed content, or syndication. They’ve also displayed a willingness to place ads on their services after vowing not to (in the case of Netflix) and have managed to mitigate spending on pricey sports rights with behind-the-scenes content.

Most prominently, Netflix has licensed older shows like USA Networks’ “Suits,” reintroducing the cast, including a then-unknown Meghan Markle, to solid viewership. “As the competitive environment evolves, we may have increased opportunities to license more hit titles to complement our original programming,” Netflix said in its third-quarter earnings statement.

During the company’s earnings call in October, Netflix co-CEO Ted Sarandos pointed to the historic streaming success of “Suits.” “This continues to be important for us to add a lot of breadth of storytelling,” he said. “Our consumers have a wide range of tastes, and we can’t make everything, but we can help you find just about anything. That’s really the strength.”

The success of “Suits” and of original sports programming, among several tweaks, indicates that consumers like what they see so far. Streaming additions at Netflix and Disney were significant — 8.76 million and nearly 7 million, respectively — during the recently completed third calendar quarter.

Read more: Netflix’s stock jumps more than 10% on huge spike in subscribers, price hikes

“There exist a lot of popular, good shows that people hadn’t seen before. HBO Max has licensed ‘Band of Brothers.’ ‘Yellowstone’ is on the CBS network after performing well on Paramount Global

PARA,

and Comcast Corp.’s

CMCSA,

Peacock,” Jon Giegengack, founder and principal of Hub Entertainment Research, said in an interview. “Consumers increasingly don’t care if a show is new, if they haven’t seen it before.”

On the sports front, Netflix and Amazon Prime Video have sidestepped expensive rights to live sporting events and instead produced docuseries such as Netflix’s “Quarterback” and “Formula 1: Drive to Survive” and Amazon’s “Coach Prime” and “Redefined: J.R. Smith.” Amazon also continues to air “NFL Thursday Night Football.”

Competition for eyeballs is tight with so many suitors — from Alphabet Inc.’s

GOOGL,

GOOG,

YouTube to TikTok, both of which are developing long-form content — and viewers face “too many streaming options,” said Brittany Slattery, chief marketing officer at OpenAP, an advertising platform founded by the owners of most of the large TV networks.

“There is a high churn rate, because consumers keep popping in and out of services because they can’t afford all these services,” Slattery said in an interview.

Also see: Here’s what’s worth streaming in December 2023: Not much new, yet still a lot to watch

Mark Vena, CEO and principal analyst at SmarTech Research, sums up the typical customer experience: “There are too many services for streaming. I will buy service for a month, watch a movie and then cancel.”

Major streamers are pinning many of their hopes on technology as a way to entice viewers and expand beyond the traditional TV model they’ve adopted. Strategies include mobile gaming (Netflix), gambling (Disney’s ESPN Bet) and shoppable media (Amazon).

The biggest near-term change would bring ESPN exclusively to streaming, perhaps as early as 2025, although big games would probably be simulcast on network TV to retain older viewers.

“Technology will be a major impetus for being in the winning circle,” said Hunter Terry, head of connected TV at global data company Lotame, pointing to Amazon’s shoppable-media strategy during Prime Video’s broadcast of an NFL game on Black Friday.

The NFL game, the first ever on a Friday, featured QR codes of Amazon ads for direct purchases via mobile devices and PCs, contributing greatly to what the e-commerce giant said was its best-ever sales day — 7.5% higher than Black Friday 2022. The game drew between 9.6 million and 10.8 million viewers, according to Nielsen and Amazon, making it the highest-rated show on Black Friday for young adults (18-34) and adults (18-49).

And what of generative AI, a major flashpoint in the writers and actors strikes that roiled Hollywood for months earlier this year? Creators feared generative AI would be used to produce low- and middle-brow entertainment without the need for writers, actors or production crew.

The technology is as intriguing to streamers as it is vexing. Full-blown adoption would rankle creators as well as customers. There are also limitations: AI-created content is lacking in humor and original thought, said David Parekh, CEO of SRI International, a leading research and development organization serving government and industry.

“The pressing question is, who goes first among the streamers and risks getting blowback from studios and consumers?” said Rick Munarriz, a contributing analyst at the Motley Fool who covers streaming-service stocks. “You don’t want to offend people, but there are tools to create ideas” at little cost.

AI and machine learning are already being used to mine data to find out what resonates with viewers.

“It is very hard to produce successful content,” said Ron Gutman, CEO of Wurl, which helps streamers and publishers monetize and distribute content, and which was recently acquired by AppLovin Corp.

APP,

for $430 million. “The market is so fragmented. The problem is connecting people to content.”

Big-budget busts present another potential source of content, by salvaging unreleased movies, according to experts.

The so-called dust-bin option is the natural successor to straight-to-video and straight-to-pay-per-view movies. There has been some precedent, with the release of Disney’s superhero hit “Black Widow” simultaneously on streaming and in theaters in May 2021.

Will streaming services end up as the first stop for movies abruptly canceled before release? Candidates include “Batgirl,” which cost $90 million to make and was in post-production when Warner Bros. Discovery Inc.

WBD,

pulled the plug.

The same fate could also await two other shelved Warner Bros. movies, “Scoob! Holiday Haunt” and the completed “Coyote vs. Acme.”

While the $90 million “Batgirl” is a tax write-off, there could be upside to “Coyote” and “Scoob!” if they went to streaming without a costly marketing campaign, said SmarTech Research’s Vena.

Still, the long-term plans of streaming giants to meld tech to TV remains a ticklish task, said Wurl’s Gutman. “TV is a lean-back experience, not a lean-into technology medium,” he said. “People are looking at their phones while watching TV. It is a passive experience.”

Tracy Swedlow, founder and co-producer of the TV of Tomorrow Show conference, said: “They’ve been burning a candle at both ends, investing in original content as well as licensing long-tail content such as ‘Suits’ and ‘Breaking Bad.’ Something has to give.”

[ad_2]

[ad_1]

A rally in the U.S. stock and bond markets in the past week defied the bears and fueled hopes for more gains to come by year-end and in 2024 as Wall Street bought into the idea that the economy will pull off a “soft landing” after a run of interest-rate hikes by the Federal Reserve.

But market skeptics are putting investors on alert that the “soft-landing” scenario is still at risk with consumer spending and job growth slowing, along with corporate earnings.

“The equity market is misguided,” said Josh Schachter, senior portfolio manager at Easterly Investment Partners, in a phone interview with MarketWatch. “The markets are behaving in almost a bipolar fashion — some asset classes such as bonds

BX:TMUBMUSD10Y,

oil

BRN00,

and dollar

DXY,

are being priced for a recession, while other assets such as equities and bitcoin

BTCUSD,

are priced risk-on.”

U.S. stocks built on their November gains in the past week, with the S&P 500 index

SPX

ending at new 2023 high on Friday and the Dow Jones Industrial Average

DJIA

logging its fifth week in the green. The rebound in stocks was due in part to bond investors starting to believe the Fed is done raising interest rates and is likely to begin cutting them by the first quarter of 2024.

Meanwhile, the narrative that a resilient labor market and steadier-than-expected economic growth should keep a recession at bay has gained traction, bolstering the “goldilocks” scenario for the financial markets.

However, signs are emerging that consumer spending, which accounts for about 70% of the U.S. economic output and has boosted the economy this year, has likely run its course following the post-pandemic recovery. Credit card and car loan delinquency rates are rising, student loan payments have resumed, consumer spending is cooling, and there are warnings from top retailers.

Joseph Quinlan, head of CIO market strategy for Merrill and Bank of America Private Bank, said the “softness” in the U.S. consumer sector is visible but not huge, referring to that as “a canary in a coal mine,” he told MarketWatch via phone on Thursday.

The pullback in consumer spending is welcome news for Fed officials, who have increased interest rates 11 times since March 2022 to get inflation back to its preferred target of 2%. However, some analysts are worried that high interest rates and a decline in pandemic savings could eventually translate to weaker consumers in 2024, potentially another sign of a long-predicted slowdown in the U.S. economy.

“One of the things I’m most concerned about is consumers’ ability to continue to pace the economy — you’ve got several headwinds that haven’t really borne completely out yet,” said Jason Heller, senior executive vice president at Coastal Wealth. “Does the consumer continue to behave the way they behaved the last 36 months? I think you will eventually see a slowdown in consumer spending which is going to mandate a slowdown in the labor market.”

Lauren Goodwin, economist and portfolio strategist at New York Life Investments, acknowledged that a modest slowdown in inflation and employment growth means that a “Fed relief rally” in stocks can be sustained, but her concern is this late-cycle limbo is no different than those of the past, which is a moment of “goldilocks” before the very reason that inflation is moderating — slowing economic growth and employment — becomes clear in the data.

See: ‘We Are Still Headed for a Pretty Hard Landing,’ Ex-Treasury Secretary Larry Summers Says

That’s why the November employment report, which will be released by the Bureau of Labor Statistics next Friday at 8:30 a.m. Eastern, will be key for investors to watch. The U.S is expected to add 172,500 jobs in November after a 150,000 increase in the prior month, according to economists polled by Dow Jones. The percentage of jobless Americans seeking work is forecast to stay the same at 3.9%, leaving it at the highest level since the beginning of 2022.

See: U.S. job growth pick up on the radar this coming week

In fact, nonfarm payroll report publication days have been among the most volatile for stocks in 2023, compared with the release of monthly consumer-price index readings, which sparked some of the biggest daily up and down moves for the S&P 500 and other major indexes in 2022.

See also: Do CPI days still rock the stock market? How 2023 stacks up to 2022

This year, the S&P 500 saw an absolute average percentage change of 1.12% on employment situation release dates, compared with an average percentage move of 0.64% on CPI days, according to figures compiled by Dow Jones Market Data.

That said, analysts are skeptical if the employment data is able to tell “a radically different story” but suggest the labor market will remain relatively tight into 2024, said Quinlan and Lauren Sanfilippo at Merrill and Bank of America Private Bank, in a phone interview.

See: What 2024 S&P 500 forecasts really say about the stock market

Corporate America and their shares are telling investors a different story about next year.

With an estimated average S&P 500 earnings growth of 11.7% next year, the U.S. stock market is nowhere near recessionary concerns, said Heller. “We’ve [the stocks] priced in pretty significant growth in 2024.”

Strategists at Merrill and Bank of America Private Bank are in the camp of expecting a “mid-single digit” earnings growth for the S&P 500 in 2024, as earnings have troughed and the economy will fall back to the 2%-level of real growth after high rates confine consumer spending and corporate profits, cooling a red-hot economy.

To be sure, Wall Street analysts tend to overestimate the earnings-per-share (EPS) for the S&P 500, said John Butters, senior earnings analyst at FactSet.

The current bottom-up EPS estimate for the S&P 500 in 2024 is $246.30. If that holds true, that would be the highest EPS number reported by the large-cap index since FactSet began tracking this metric in 1996.

However, over the past 25 years, the average difference between the EPS estimate at the beginning of the year and the actual EPS number has been 6.9%, meaning analysts on average have overestimated the earnings one year in advance, said Butters in a Friday note (see chart below).

[ad_2]

[ad_1]

Gold futures ended Friday at their highest on record, with prices on the cusp if a so-called golden cross — signaling the potential for further upside in the precious metal.

Gold prices surged as the market reacted to the escalating tensions in the Middle East, said Bas Kooijman, CEO and asset manager of DHF Capital, in market commentary. The end of the truce in the region could “continue to fuel risk aversion and investors’ concerns.”

The escalation has “helped extend gold’s uptrend of the last two months as traders take into account changing expectations regarding monetary policy,” he said. “Traders have been betting on an end to the interest rate hiking cycle and possible rate cuts in the first half of next year, which could continue to support gold’s rise over the medium term.”

On Friday, gold for February delivery

GC00,

GCG24,

climbed by $32.50, or 1.6%, to settle at $2,089.70 an ounce on Comex. Prices based on the most-active contracts, settled at an all-time high, surpassing the Aug. 6, 2020 record-high finish of $2,069.40, according to Dow Jones Market Data.

Prices traded as high as $2,095.70 on an intraday basis on Friday, surpassing the previous record intraday high of $2,089.20 from Aug. 7, 2020.

Gold’s rally started after the release of the October consumer-price index, Edmund Moy, senior IRA strategist for U.S. Money Reserve and a former director of the U.S. Mint, told MarketWatch. The data released Nov. 14 showed that the U.S. cost of living was unchanged in October.

The market viewed that reading as saying the Fed has “tamed inflation and is probably finished raising rates and will, in all probability, start reducing rates sooner and faster than previously predicted,” said Moy.

Lower Fed rates mean lower Treasury yields, and since Treasurys are purchased in dollars, falling demand for Treasurys means falling demand for the dollar, he said, which can boost the price for dollar-denominated gold.

“While gold’s current rally is a bit overheated, both the golden cross and the proximity of an all-time high acting like a magnet for the price means that we’re likely to see further gains in the very immediate term,” Brien Lundin, editor of Gold Newsletter, told MarketWatch.

Most-active gold futures on Friday were close to reaching a bullish indicator known as a golden cross, when an asset’s short-term moving average moves above its long-term moving average. The 50-day moving average was at $1,955.44, pennies below the 200-day moving average of $1,955.51 Friday.

Gold prices around the globe had already rallied to fresh record price highs in other currencies and with the U.S. dollar gold price joining the party, “you can expect another wave of buying momentum to come into the market now,” said Peter Spina, president of GoldSeek.com.

““The end of the stealth phase move of the gold bull market is over. It will finally be acknowledged and recognized by the mainstream.””

“I fully expect significantly higher gold prices in the months ahead,” he told MarketWatch. “The end of the stealth phase move of the gold bull market is over. It will finally be acknowledged and recognized by the mainstream.”

Read: Gold rallies toward ‘golden cross’ after defying bearish signal

Spina said it’s important to note that gold prices are “not hitting record highs, but rather the U.S. dollar is hitting record lows against superior money.”

That says the U.S. dollar’s purchasing power is “being eroded even further, more aggressively now,” he said. The ICE U.S. Dollar Index

DXY,

a measure of the currency against a basket of six major rivals, is down 0.3% for the year to date after a November pullback.

The precious metal remains supported by Federal Reserve interest-rate cut bets even after Fed Chairman Jerome Powell signaled that it was too soon for the Fed to claim victory over the inflation beast, said Lukman Otunuga, manager, market analysis at FXTM.

Read: Powell won’t endorse market expectations for quick rate cuts

The Fed’s ability to cut interest rates in March is likely to be influenced by key data including CPI and jobs data, among others,” said Otunuga. “Given how the Relative Strength Index (RSI) on the daily charts remains in overbought regions, gold could experience a technical throwback before pushing higher.”

Lundin, meanwhile, also warned that the all-time high for gold may mark a “quadruple top” unless gold is able to decisively break through a new plateau, probably somewhere over $2,100 an ounce.

[ad_2]

[ad_1]

JOHANNESBURG (AP) — An elevator suddenly dropped around 200 meters (656 feet) while carrying workers to the surface in a platinum mine in South Africa, killing 11 and injuring 75, the mine operator said Tuesday.

It happened Monday evening at the end of the workers’ shift at a mine in the northern city of Rustenburg. The injured workers were hospitalized.

Impala…

Already a subscriber?

Log In

[ad_2]

[ad_1]

BERLIN—Bayer Chief Executive Bill Anderson said the company would bounce back quickly from a recent spate of bad news, and warned that a breakup of the pharmaceutical and agricultural company was no universal cure for its ailments.

A stream of negative news has rekindled calls from investors for Bayer to unlock value by spinning off its units into separate businesses. But in an interview with The Wall Street Journal this week, Anderson said the company couldn’t be distracted from the tough restructuring to fix the businesses.

Copyright ©2023 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

[ad_2]

[ad_1]

Gold futures fell on Friday, as hawkish comments from Federal Reserve Chairman Jerome Powell on Thursday and weaker investor appetite for the haven metal prompted prices to post their first weekly decline since early October.

“The tailwind in gold has gone silent,” said Adam Koos, president at Libertas Wealth Management Group. The yellow metal was formerly supported, in part, by the thought that the U.S. would be hitting a ceiling on interest rates and dissipating inflation, but “none of that seems to matter under the shadow of the Fed.”

On Friday, gold for December delivery fell $32.10, or 1.6%, to settle at $1,937.70 an ounce on Comex, down 3.1% for the week, according to Dow Jones Market Data. Prices based on the most-active contract marked the biggest daily decline since mid-April and first weekly loss in five weeks.

In remarks on a panel at the International Monetary Fund Thursday, Powell said Fed officials are “gratified” with the progress made so far to bring down U.S. inflation but weren’t yet confident that interest rates are high enough to bring inflation down to their 2% target over time.

“Gold is an inmate within the confines of overhead resistance, and the door to freedom resides at $2,060,” Koos told MarketWatch. “Just when an exit plan seems near — when a break-out with parole seems promising — Jerome Powell came in like the warden on Thursday, saying that he’s unconvinced that monetary policy has been sufficient thus far, and that inflation could still warrant future rate hikes.”

Read: Powell says Fed is wary of ‘head fakes’ from inflation

Gold prices have also been influenced by a fall in investor appetite, as fears that Middle East tensions will spill over to wider regions have eased, said Lukman Otunuga, manager, market analysis, at FXTM.

If concerns over the spread of the Middle East conflict continue to ease, that may “pave the way for further downside” in gold prices, he told MarketWatch.

However, should fears return and intensify over a potential spillover of the Israel-Hamas conflict, there may be a “fresh wave of risk aversion” that would send investors towards “safe-haven destinations” like gold, said Otunuga.

“It’s not only the developments in the Middle East, but also Russia’s invasion of Ukraine that could fan fears about a global recession,” he said.

For now, gold has the potential to extend its losses, said Otunuga.

Ahead of Friday’s gold-price settlement, he warned that a “solid breakdown and daily close” below $1,945 would open the doors toward a fall to the 200-day simple moving average at $1,934, before the U.S. October consumer price index report on Nov. 14.

Koos, meanwhile, said gold is likely to remain in “price prison, staring at the ceiling of $2,060” an ounce, until the Fed decides to slow its role in fighting inflation.

A move beyond that price level represents “freedom and new all-time-highs,” he said. “Until then, patience will be a requirement, at the very least.”

[ad_2]

[ad_1]

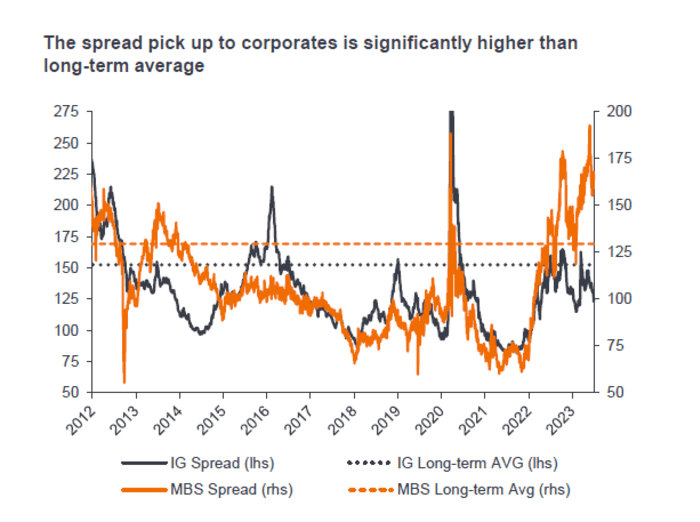

U.S. homes may be wildly unaffordable for first-time buyers, but mortgage bonds backed by those same properties could be dirt cheap.

Shocks from the Federal Reserve’s dramatic rate increases have walloped the $8.9 trillion agency mortgage-bond market, the main artery of U.S. housing finance for almost the past two decades.

Spreads, or compensation for investors, have hit historically wide levels, even through the sector is underpinned by home loans that adhere to the stricter government standards set in the wake of the subprime-mortgage crisis.

Bond prices also have tumbled, sinking from a peak above 106 cents on the dollar to below 98, despite guarantees that mean investors will be fully repaid at 100 cents on the dollar.

Bloomberg, Goldman Sachs Global Investment Research

“It’s really, really struggled,” Nick Childs, portfolio manager at Janus Henderson Investors, said of the agency mortgage-bond market during a Thursday talk on the firm’s fixed-income outlook.

Yet Childs and other investors also see big opportunities brewing. While mortgage bonds have gotten cheaper with the sector’s two anchor investors on the sidelines, the stalled housing market should breed scarcity in the bonds, which could help lift the sector out of a roughly two-year slump.

Prices have tumbled since rate shocks hit, but also since the Fed continued winding down its large footprint in the sector by letting bonds it accumulated to help shore up the economy roll off its balance sheet.

Banks awash in underwater securities have pulled back too. The repricing of similar bonds helped hasten the collapse of Silicon Valley Bank in March.

“Banks have been not only absent, but selling,” said Childs, who helps oversee the Janus Henderson Mortgage-Backed Securities exchange-traded fund

JMBS,

an actively managed $2 billion fund focused on highly rated securities with minimal credit risk.

“But we’re moving into an environment where supply continues to dwindle,” he said, given anemic refinancing activity and the dearth of new home loans being originated since 30-year fixed mortgage rates topped 7%.

The bulk of all U.S. mortgage bonds created in the past two decades have come from housing giants Freddie Mac

FMCC,

Fannie Mae

FNMA,

and Ginnie Mae, with government guarantees, making the sector akin to the $25 trillion Treasury market. But unlike investors in Treasurys, investors in mortgage bonds also earn a spread, or extra compensation above the risk-free rate, to help offset its biggest risk: early repayments.

While homeowners typically take out 30-year loans, most also refinanced during the pandemic rush to lock in ultralow rates, instead of continuing to make three decades of payments on more expensive mortgages. If someone refinances, sells or defaults on a home, it leads to repayment uncertainty for bond investors.

“To put this another way, the biggest risk to mortgages is now off the table, yet spreads are at or near historic wides,” said Sam Dunlap, chief investment officer, Angel Oak Capital Advisors, in a new client note.

That spread is now far above the long-term average, topping levels offered by relatively low-risk investment-grade corporate bonds.

Janus Henderson Investors

Agency mortgage bonds typically are included in low-risk bond funds and can be found in exchange-traded funds. While they have been hard hit by the sharp selloff in long-dated Treasury bonds

BX:TMUBMUSD10Y

BX:TMUBMUSD30Y,

there has also been hope that the worst of the storm could be nearly over.

Goldman Sachs credit analysts recently said they favored the sector but warned in a weekly client note that it still faces “high rate volatility and a dearth of institutional demand.”

As evidence of the U.S. bond selloff, the popular iShares 20+ Year Treasury Bond ETF

TLT

recently sank to its lowest level in more than a decade. It also was on pace for a negative 10% total return on the year so far, according to FactSet. Janus Henderson’s JMBS ETF was on pace for a negative 2.7% total return on the year through Friday.

“Frankly, why they fit portfolios so well is that because the government backs agency mortgages, there is no credit risk,” Childs said. “So if a borrower defaults, you get par back on that. It just comes through as a typical payment.”

[ad_2]

[ad_1]

Uranium prices have reached their highest level in more than a decade as a global supply shortage persists, with the bull market for uranium investments still in its “earliest days.”

The market is “definitely in a structural deficit as demand is growing at a 5% annual rate and the current (2023) gap between global production and consumption remains at over 50 million pounds,” Scott Melbye, executive vice president at mining company Uranium Energy Corp.

UEC,

told MarketWatch.

Weekly spot uranium prices stood at $72.75 a pound as of Oct. 2, the highest since February 2011, according to data from nuclear-fuel consulting firm UxC, and were last at $69 as of Oct. 9. Weekly prices have climbed nearly 45% since the end of last year.

UxC

In late August, Jonathan Hinze, president at UxC, told MarketWatch that the market was seeing the “best set up for nuclear power expansion” that he’d ever seen. That observation still holds, he said.

It is clear that the uranium supply/demand balance remains “extremely tight, and it will likely only get tighter” in the coming 12 to 24 months as demand continues to rise, “while new supplies are taking more time to materialize, and inventories keep getting drawn down,” he said.

Since late August, financial players, including hedge and publicly traded funds active in uranium, have been quite active buying additional uranium off the spot market, said Hinze. These funds “clearly believe that prices are set to rise further, and investors are therefore adding money to their coffers to allow them to buy physical uranium.”

This is demand that isn’t fully anticipated in the market and this has added to the overall positive demand picture, he said.

Still, Melbye pointed out that uranium prices have pulled back a bit more recently as some traders took some “very handsome profits on their accumulated long positions.”

That pullback may have also come as an “overreaction,” he said, to news from Kazakhstan, which produced the world’s largest share of uranium from mines in 2022, according to the World Nuclear Association. Kazatomprom, Kazakhstan’s national operator for the export and import of uranium, announced in late September a return to full production in 2025 to meet global nuclear energy demand.

Melbye believes there was an overreaction in uranium prices because “this will ultimately have little impact on Western supply and demand as most analysts had them producing close to those levels by that time in their forecasts.”

Even with that production assumption, the market is “still dramatically undersupplied,” and based on Melbye’s estimation, requires eight to 10 new mines starting up globally by 2030, he said.

And while uranium has been among the best performing commodities year to date, it has only recently reached the level which “incentivizes the world’s best mines,” he said.

This bull market in uranium investments is “still in its earliest days,” said Melbye.

Among the exchange-traded funds, the Global X Uranium ETF

URA

has gained more than 25% on the year through Friday afternoon, while the Sprott Uranium Miners ETF

URNM

has added almost 36%. The Sprott Physical Uranium Trust

SRUUF,

a closed-end fund, trades nearly 39% higher.

Broader new mine developments with significant capital investments in an inflationary environment require higher prices to move ahead, Melbye said. “Even at those levels, the long lead times needed to achieve these necessary start ups could leave the market in a short squeeze for several years.”

The recent spot market move lower in prices marks a “temporary pause, and not a peak,” he said. “Buyers should be active on this welcome dip.”

Contributing to supply concerns, a July coup has disrupted mining operations in the country of Niger in West Africa. Niger produced just over 4% of the world’s uranium in 2022, according to World Nuclear News.

The coup caused borders to close, and major uranium mine and mill operation called Somair has been halted, said UxC’s Hinze. The mine, operated by the French company Orano, sells most of uranium to customers in Europe, he said.

Meanwhile, Cameco Corp.

CCJ,

one of the world’s largest providers of uranium, said it’s encountered challenges at its mine and milling operation in Canada. The company now expects to produce nearly 3 million pounds of uranium concentrate less this year than previously anticipated, said Hinze.

“These production challenges add to the overall view that the supply/demand balance is very tight and will get even tighter,” he said.

[ad_2]

[ad_1]

Exxon Mobil Corp. said in a filing late Wednesday that its third-quarter profit is likely to get a bump of around $1 billion from rising crude prices.

Exxon

XOM,

estimated between $900 million and $1.3 billion more than second-quarter profit due to crude-price changes, and between $200 million and $400 million in gas-price changes.

The energy giant is expecting $600 million to $400 million less as a result of thinner margins for its chemicals, however.

Exxon shares dropped 0.5% in the extended session after ending the regular trading day down 3.7%. The stock late last month ended at a record, according to data going back to November 1972.

Oil futures prices on Wednesday ended at their lowest in about five weeks, but had been inching closer to $100 a barrel recently.

Exxon is slated to report third-quarter earnings in early November, with FactSet consensus calling for adjusted earnings of $2.35 a share on sales of $85.6 billion. That would compare with adjusted EPS of $4.45 on sales of $112 billion in the third quarter of 2022.

So far this year, Exxon shares have gained nearly 2%, compared to an advance of around 10% for the S&P 500 index

SPX.

[ad_2]

[ad_1]

Two things investors can be sure about: Nothing lasts forever and the stock market always overreacts. The spiking of yields on long-term U.S. Treasury securities has been breathtaking, and it has led to remarkable declines for some sectors and possible bargains for contrarian investors who can commit for the long term.

First we will show how the sectors of the S&P 500

have performed. Then we will look at price-to-earnings valuations for the sectors and compare them to long-term averages. Then we will screen the entire index for companies trading below their long-term forward P/E valuation averages and narrow the list to companies most favored by analysts.

Here are total returns, with dividends reinvested, for the 11 sectors of the S&P 500, with broad indexes below. The sectors are sorted by ascending total returns this year through Monday.

| Sector or index | 2023 return | 2022 return | Return since end of 2021 | 1 week return | 1 month return |

| Utilities | -18.4% | 1.6% | -17.2% | -11.1% | -9.6% |

| Real Estate | -7.1% | -26.1% | -31.4% | -3.0% | -8.8% |

| Consumer Staples | -5.4% | -0.6% | -6.0% | -2.2% | -4.4% |

| Healthcare | -4.2% | -2.0% | -6.1% | -1.7% | -3.3% |

| Financials | -2.5% | -10.5% | -12.7% | -2.5% | -4.7% |

| Materials | 1.3% | -12.3% | -11.2% | -1.9% | -7.0% |

| Industrials | 3.5% | -5.5% | -2.1% | -1.8% | -7.3% |

| Energy | 4.0% | 65.7% | 72.4% | -1.9% | -1.4% |

| Consumer Discretionary | 27.0% | -37.0% | -20.0% | -0.6% | -5.2% |

| Information Technology | 36.5% | -28.2% | -2.0% | 0.8% | -5.9% |

| Communication Services | 42.5% | -39.9% | -14.3% | 1.1% | -1.3% |

|

S&P 500 |

13.1% | -18.1% | -7.4% | -1.1% | -4.9% |

|

DJ Industrial Average |

2.5% | -6.9% | -4.5% | -1.7% | -4.0% |

|

Nasdaq Composite Index COMP |

28.0% | -32.5% | -13.7% | 0.3% | -5.1% |

|

Nasdaq-100 Index |

36.5% | -32.4% | -7.7% | 0.5% | -4.2% |

| Source: FactSet | |||||

Returns for 2022 are also included, along with those since the end of 2021. Last year’s weakest sector, communications services, has been this year’s strongest performer. This sector includes Alphabet Inc.

GOOGL

and Meta Platforms Inc.

META,

which have returned 52% and 155% this year, respectively, but are still down since the end of 2021. To the right are returns for the past week and month through Monday.

On Monday, the S&P 500 Utilities sector had its worst one-day performance since 2020, with a 4.7% decline. Investors were reacting to the jump in long-term interest rates.

Here is a link to the U.S. Treasury Department’s summary of the daily yield curve across maturities for Treasury securities.

The yield on 10-year U.S. Treasury notes

jumped 10 basis points in only one day to 4.69% on Monday. A month earlier the 10-year yield was only 4.27%. Also on Monday, the yield on 20-year Treasury bonds

rose to 5.00% from 4.92% on Friday. It was up from 4.56% a month earlier.

Market Extra: Bond investors feel the heat as popular fixed-income ETF suffers lowest close since 2007

The Treasury yield curve is still inverted, with 3-month T-bills

yielding 5.62% on Monday, but that was up only slightly from a month earlier. An inverted yield curve has traditionally signaled that bond investors expect a recession within a year and a lowering of interest rates by the Federal Reserve. Demand for bonds pushes their prices down. But the reverse has happened over recent days, with the selling of longer-term Treasury securities pushing yields up rapidly.

Another way to illustrate the phenomenon is to look at how the Federal Reserve has shifted the U.S. money supply. Odeon Capital analyst Dick Bove wrote in a note to clients on Friday that “the Federal Reserve has not deviated from its policy to defeat inflation by tightening monetary policy,” as it has shrunk its balance sheet (mostly Treasury securities) to $8.1 trillion from $9 trillion in March 2022. He added: “The M2 money supply was $21.8 trillion in March 2022; today it is $20.8 trillion. You cannot get tighter than these numbers indicate.”

Then on Tuesday, Bove illustrated the Fed’s tightening and the movement of the 10-year yield with two charts:

Bove said he believes the bond market has gotten it wrong, with the inverted yield curve reflecting expectations of rate cuts next year. If he is correct, investors can expect longer-term yields to keep shooting up and a normalization of the yield curve.

This has set up a brutal environment for utility stocks, which are typically desired by investors who are seeking dividend income. In a market in which you can receive a yield of 5.5% with little risk over the short term, and in which you can lock in a long-term yield of about 5%, why take a risk in the stock market? And if you believe that the core inflation rate of 3.7% makes a 5% yield seem paltry, keep in mind that not all investors think the same way. Many worry less about the inflation rate because large components of official inflation calculations, such as home prices and car prices, don’t affect everyone every year.

We cannot know when this current selloff of longer-term bonds will end, or how much of an effect it will have on the stock market. But sharp declines in the stock market can set up attractive price points for investors looking to go in for the long haul.

A combination of rising earnings estimates and price declines could shed light on potential buying opportunities, based on forward price-to-earnings ratios.

Let’s look at the sectors again, in the same order, this time to show their forward P/E ratios, based on weighted rolling 12-month consensus estimates for earnings per share among analysts polled by FactSet:

There is a limit to how many columns we can show in the table. The S&P 500’s forward P/E ratio is now 17.94, compared with 16.79 at the end of 2022 and 21.53 at the end of 2021. The benchmark index’s P/E is above its 10- and 15-year average levels but below the five-year average.

If we compare the current sector P/E numbers to 5-, 10- and 15-year averages, we can see that the current levels are below all three averages for four sectors: utilities, real estate, financials and communications services. The first three face obvious difficulties as they adjust to the rising-rate environment, while the real-estate sector reels from continuing low usage rates for office buildings, from the change in behavior brought about by the COVID-19 pandemic.

Your own opinions, along with the pricing for some sectors, might drive some investment choices.

A broader screen of the S&P 500 might point to companies for you to research further.

We narrowed the S&P 500 as follows:

Here are the 20 companies that passed the screen, for which analysts’ price targets imply the highest upside potential over the next 12 months.

There is too much data for one table, so first we will show the P/E information:

| Company | Ticker | Current P/E to 5-year average | Current P/E to 10-year average | Current P/E to 15-year average |

| SolarEdge Technologies Inc. | SEDG | 89% | N/A | N/A |

| AES Corp. | AES | 66% | 75% | 90% |

| Insulet Corp. | PODD | 18% | N/A | N/A |

| United Airlines Holdings Inc. | UAL | 42% | 50% | N/A |

| Alaska Air Group Inc. | ALK | 51% | 57% | N/A |

| Tapestry Inc. | TPR | 39% | 49% | 70% |

| Albemarle Corp. | ALB | 39% | 50% | 73% |

| Delta Air Lines Inc. | DAL | 60% | 63% | 21% |

| Alexandria Real Estate Equities Inc. | ARE | 59% | 68% | N/A |

| Las Vegas Sands Corp. | LVS | 96% | 78% | 53% |

| Paycom Software Inc. | PAYC | 61% | N/A | N/A |

| PayPal Holdings Inc. | PYPL | 33% | N/A | N/A |

| SBA Communications Corp. Class A | SBAC | 27% | N/A | N/A |

| Advanced Micro Devices Inc. | AMD | 58% | 39% | N/A |

| LKQ Corp. | LKQ | 92% | 44% | 78% |

| Charles Schwab Corp. | SCHW | 75% | 54% | 73% |

| PulteGroup Inc. | PHM | 94% | 47% | N/A |

| Lamb Weston Holdings Inc. | LW | 71% | N/A | N/A |

| News Corp Class A | NWSA | 93% | 73% | N/A |

| CVS Health Corp. | CVS | 75% | 61% | 67% |

| Source: FactSet | ||||

Click on the tickers for more about each company or index.

News Corp

NWSA

is on the list. The company owns Dow Jones, which in turn owns MarketWatch.

Here’s the list again, with ratings and consensus price-target information:

| Company | Ticker | Share “buy” ratings | Oct. 2 price | Consensus price target | Implied 12-month upside potential |

| SolarEdge Technologies Inc. | SEDG | 74% | $122.56 | $268.77 | 119% |

| AES Corp. | AES | 79% | $14.16 | $25.60 | 81% |

| Insulet Corp. | PODD | 68% | $165.04 | $279.00 | 69% |

| United Airlines Holdings Inc. | UAL | 71% | $41.62 | $69.52 | 67% |

| Alaska Air Group Inc. | ALK | 87% | $36.83 | $61.31 | 66% |

| Tapestry Inc. | TPR | 75% | $28.58 | $46.21 | 62% |

| Albemarle Corp. | ALB | 81% | $162.41 | $259.95 | 60% |

| Delta Air Lines Inc. | DAL | 95% | $36.45 | $58.11 | 59% |

| Alexandria Real Estate Equities Inc. | ARE | 100% | $98.18 | $149.45 | 52% |

| Las Vegas Sands Corp. | LVS | 72% | $45.70 | $68.15 | 49% |

| Paycom Software Inc. | PAYC | 77% | $260.04 | $384.89 | 48% |

| PayPal Holdings Inc. | PYPL | 69% | $58.56 | $86.38 | 48% |

| SBA Communications Corp. Class A | SBAC | 68% | $198.24 | $276.69 | 40% |

| Advanced Micro Devices Inc. | AMD | 74% | $103.27 | $143.07 | 39% |

| LKQ Corp. | LKQ | 82% | $49.13 | $67.13 | 37% |

| Charles Schwab Corp. | SCHW | 77% | $53.55 | $72.67 | 36% |

| PulteGroup Inc. | PHM | 81% | $73.22 | $98.60 | 35% |

| Lamb Weston Holdings Inc. | LW | 100% | $92.23 | $123.50 | 34% |

| News Corp Class A | NWSA | 78% | $20.00 | $26.42 | 32% |

| CVS Health Corp. | CVS | 77% | $69.69 | $90.88 | 30% |

| Source: FactSet | |||||

A year may actually be a short period for a long-term investor, but 12-month price targets are the norm for analysts working for brokerage companies.

Don’t miss: This fund shows that industry expertise can help you make a lot of money in the stock market

[ad_2]

[ad_1]

U.S. stocks have risen sharply in 2023, with a small number of technology companies driving an ever-increasing share of the stock-market gains.

While the 11.7% year-to-date gains for the large-cap benchmark S&P 500 index

SPX

show 2023 has been a “good year” for stocks, that hardly tells the whole story, said Jonathan Krinsky, the technical strategist at BTIG.

The U.S. stock market has seen the median return for shares in the S&P 500 index rise merely 1.1% in 2023, which is “a different planet” compared with their median gain of 16.2% in 2014, when the benchmark index recorded a yearly advance of 11.4%, Krinsky said in a Sunday note (see chart below).

The Russell 3000

RUA

— a barometer that represents approximately 98% of the American equities — had a median return of negative 2.2% this year, but the index has gained 11.3% year to date, wrote Krinsky, citing BTIG and Bloomberg data. In 2014, the median return for the Russell 3000 was 6.9%, and it recorded a yearly gain of 10.4%.

Meanwhile, the median year-to-date return for stocks in the S&P 1500, which includes all shares in the S&P 500, S&P 400

MID

and S&P 600

SML

and covers approximately 90% of U.S. stocks, rose a merely 0.1% versus the index’s 11.2% advance this year, said Krinsky. The S&P 1500 recorded a median return of 8.8% in 2014 and was up 10.9%.

So far in 2023, investors have struggled to brush off a rise in Treasury yields primarily triggered by the Federal Reserve bumping up interest rates and the risk of recession, with hope that the stock-market rally hasn’t run out of steam yet.

However, the S&P 500 and the Nasdaq Composite

COMP

Friday locked in their worst month of the year, down 4.9% and 5.8%, respectively, according to FactSet data.

Treasury yields continued to rise on Monday with the yield on the 2-year

BX:TMUBMUSD02Y

up 6.4 basis points to 5.110%, while the yield on the 10-year Treasury

BX:TMUBMUSD10Y

jumped 11 basis points to 4.682%. The 10-year rate ended at its highest level since Oct. 12, 2007, according to Dow Jones Market Data.

As a result, investors were hoping October and the last quarter of 2023 could bring some relief to the scorching summer selloff they had to endure in markets. Historically, the fourth quarter has been the best quarter for the U.S. stock market, with the S&P 500 index up nearly 80% dating back to 1950 and gaining more than 4% on average, according to data compiled by Carson Group.

“It seems to us that a rally [in the fourth quarter] is the consensus view based on the fact that seasonals tend to work that way,” Krinsky said. “While October is a strong month on ‘average’, it has been down ten of the last 30 years, with eight of those years losing 1.77% or more.”

In other words, when October is good it tends to be really good, but when it’s bad it tends to be quite bad, Krinsky added.

U.S. stocks finished mostly higher on Monday with the Dow Jones Industrial Average

DJIA

down 0.2%, while the S&P 500 ended flat and the Nasdaq edged up 0.7%, according to FactSet data.

[ad_2]

[ad_1]

Shares of Alcoa Corp. slumped to a multiyear low Monday as the aluminum company said that Roy Harvey had been replaced as chief executive officer after seven years in the role.

The company named William Oplinger as president and CEO, effective Sunday. Oplinger had served as Alcoa’s chief operations officer since February and before that as chief financial officer since November 2016.

Alcoa’s stock

AA,

dropped 5.1% in morning trading. That put it on track for the lowest close since March 1, 2021. It has tumbled 18% over the past three months and plunged 40.8% year to date, while the S&P 500

SPX

has rallied 12.8% this year.

“In our opinion, investors have expressed concern around cash flow and the company’s medium to long-term outlook,” B. Riley analyst Lucas Pipes wrote in a note to clients. “While the timing of the transition is somewhat unexpected, we believe Mr. Oplinger is the most well-positioned candidate for the CEO role.”

Harvey had been CEO since the company completed its separation from Arconic Inc. in November 2016. Arconic was acquired by Apollo Global Management Inc.

APO,

in a deal that was completed in August 2023.

“The transition of the president and CEO roles reflects the company’s succession planning process,” Alcoa said in a statement.

“Our board believes Bill’s extensive experience with Alcoa makes him well-positioned to carry the company forward,” said Steven Williams, Alcoa’s board chair.

B. Riley’s Pipes said that as Alcoa has faced challenging aluminum markets in recent quarters, and given the troubles associated with approvals of mine plans in Australia, he believes the change in leadership reflects the company’s desire to reposition its asset base for stronger cash-flow generation.

“While Mr. Harvey has successfully transformed Alcoa in recent years, particularly as [Alcoa] has aggressively deleveraged, we believe the transition will be viewed favorably by investors,” Pipes wrote.

[ad_2]

[ad_1]

Text size

Michael Nagle/Bloomberg

Can a guppie swallow a whale? Investors may find out.

Bloomberg reported Thursday that Canadian steel maker

Stelco

(STLC. Canada) was weighing a bid for

United States Steel

(X).

Stelco and U.S. Steel didn’t immediately respond to a request for comment

A bid, if it happened, would be surprising. U.S. Steel is much larger than Stelco. The Canadian steel maker shipped about 2.6 million tons of steel in 2022, while U.S. Steel shipped about 15 million. Stelco’s enterprise value, including stock and debt, is about $1 billion. U.S. Steel’s is about $9 billion.

“That makes it an upstart and we suppose the key to handicapping its chances is knowing who it is partnered with. If that partner is an investor with deep pockets, we won’t be so quick to dismiss Stelco’s chances,” wrote Gordon Haskett analyst Don Bilson in a report Friday. “For now, however, we’re going to view it as a long shot.”

Stelco likely would need a partner to complete a merger.

The possible bid is surprising in another way, too. Stelco was actually once owned by U.S. Steel. The American firm bought it 2007 after Stelco filed for bankruptcy protection. Stelco filed for bankruptcy again in 2014 and was purchased by Bedrock Industries in 2017 before listing as a public company again later that year.

“Recent history has not been kind to companies that have tried to recombine with a former partner,” added Bilson, citing

Altria

(MO) and

Philip Morris International’s

(PM) attempt to re-merge in 2019 that “went nowhere” and

CBS

and Viacom’s combination.

Paramount

(PARA) shares are down about 70% since the merger plan was announced in August 2019.

That bids are emerging for U.S. Steel isn’t surprising, though. On Aug. 13, the company said it was exploring strategic options, which could include a sale of the company. Since then, steel maker

Cleveland-Cliffs

(CLF) and steel service center Esmark have announced bids.

Esmark processes and distributes steel, rather than producing it. The company didn’t announce financing with its bid and has dropped out of the process.

Global steelmaking giant

ArcelorMittal

(MT) was reportedly considering a bid. ArcelorMittal didn’t comment on a potential bid, which also would have been a little odd. Arcelor sold its U.S. operations to Cliffs in 2020.

U.S. Steel stock was about $23 a share before its announcement and bids started to emerge. The Cliffs bid, which is a mix of cash and stock, and is the only current bid with hard numbers attached to it, is currently worth $32.21 a share.

U.S. Steel stock was at $31.80 on Friday, up 1.8%. The

S&P 500

and

Dow Jones Industrial Average

were up about 0.3% and 0.1%, respectively. Stelco stock is unchanged. Its shares are listed in Canada.

Write to Al Root at allen.root@dowjones.com

[ad_2]

[ad_1]

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

https://www.barrons.com/articles/stock-market-movers-8c0c7b23

[ad_2]

[ad_1]

The U.S. stock market, as measured by the S&P 500 Index SPX, is trapped in a trading range, and volatility seems to be damping down considerably. The significant edges of the trading range are support at 4330 and resistance at 4540. Both of those levels were touched in the latter half of August. A breakout from this range should give the market some strong directional momentum.

Since Labor Day, prices have hunkered down into an even narrower range. Typically, the latter half of September through the early part of October…

[ad_2]

[ad_1]

Neuberger Berman, an asset manager with eight decades under its belt, is on the lookout for cracks in credit markets from the Federal Reserve’s rate-hiking campaign.

Erik Knutzen, chief investment officer of multi asset, worries that several factors could be a tipping point for the economy, from an economic slowdown in China to U.S. consumers finally becoming exhausted by higher rates.

Yet Knutzen expects the high-yield, or junk bond, market to serve as the “canary in the coal mine” for broader market volatility, acting as “perhaps the most visible threat, and therefore one we think could be priced in sooner than later.”

The Bloomberg U.S. High Yield Bond Index has returned 6.4% through the end of August, producing one of the year’s highest gains in fixed income, helped along by a “resilient U.S. economy coupled with still-available financial liquidity,” according to the Wells Fargo Investment Institute.

But Knutzen worries that as the high-yield maturity wall draws closer, “the first policy rate cuts get priced further and further out, raising the threat of expensive refinancings.”

The 10-year Treasury yield’s

BX: TMUBMUSD10Y

climb to a multidecade high in August of almost 4.4% left many major U.S. corporations in early September hesitant to borrow beyond 10 years.

Starting next year, some $700 billion of high-yield bonds are set to mature through the end of 2027, with a big slice of the refinancing need coming from companies with riskier credit ratings below the top BB ratings bracket.

Bloomberg, Wells Fargo Investment Institute, Moody’s Investors Service

The two big U.S. exchange-traded funds linked to junk bonds are the SPDR Bloomberg High Yield Bond ETF

JNK

and the iShares iBoxx $ High Yield Corporate Bond ETF

HYG,

both up 1.8% and 1.5% on the year through Monday, respectively, while offering dividend yields of more than 5.8%, according to FactSet.

Of note, fixed-income strategists at the Wells Fargo Investment Institute also said they see risks emerging in junk bonds for companies rated B and below, particularly with spread in the sector trading less than 400 basis points above the risk-free Treasury rate since July. Spreads are the premium that investors are paid on bonds to help compensate for default risks.

Top corporate executives appear hopeful that the Federal Reserve will cut rates sooner than later. Fed Chairman Jerome Powell said in Jackson Hole, Wyo., in August that the central bank is prepared to keep its policy rate restrictive for a while to get inflation down to its 2% target.

To that end, Neuberger Berman, which has roughly $443 billion in managed assets, sees several sources of volatility lurking through year’s end, and has a “defensive inclination” in equity and credit, favoring high-quality companies with plenty of free cash flow, high cash balances and less expensive long-term debt.

U.S. stocks booked gains on Monday after a week of losses, with the S&P 500 index

SPX

and Nasdaq Composite Index

COMP

scoring their best daily percentage gains in about two weeks. The Dow Jones Industrial Average

DJIA

advanced 0.3%.

[ad_2]

[ad_1]

Investors in index funds have been well rewarded by a high concentration in the largest technology companies over the past decade. But there are also continuing warnings about the risk of such heavy concentrations, even in index funds that track the S&P 500. Solutions are offered to limit this risk, but if you expect Big Tech to continue to drive the broad market returns over the coming years, why not make an even more focused bet?

Comparisons of three index-fund approaches highlight how successful concentration in the “Magnificent Seven” has been.

The Magnificent Seven are Apple Inc.

AAPL,

Microsoft Corp.

MSFT,

Nvidia Corp.

NVDA,

Amazon.com Inc.

AMZN,

Alphabet Inc.

GOOGL,

GOOG,

Tesla Inc.

TSLA,

and Meta Platforms Inc.

META,

We have listed them in the order of their concentration within the Invesco S&P 500 ETF Trust

SPY,

which tracks the S&P 500

SPX.

The U.S. benchmark index is weighted by market capitalization, as is the Nasdaq Composite Index

COMP

and the Russell indexes.

SPY is 27.6% concentrated in the Magnificent Seven. One way to play the same group of 500 stocks but eliminate concentration risk is to take an equal-weighted approach to the index, which has worked well for certain long periods. But here, we’re focusing on how well the concentrated strategy has worked.

Let’s take a look at the group’s concentration in three popular index approaches, then look at long-term performance and consider what happened in 2022 as rising interest rates helped crush the tech sector.

Here are the portfolio weightings for the Magnificent Seven in SPY, along with those of the Invesco QQQ Trust

QQQ,

which tracks the Nasdaq-100 Index

NDX

and the Invesco S&P 500 Top 50 ETF

XLG

:

| Company | Ticker | % of SPY | % of QQQ | % of XLG |

| Apple Inc. |

AAPL, |

7.05% | 10.85% | 12.46% |

| Microsoft Cor. |

MSFT, |

6.65% | 9.53% | 11.76% |

| Amazon.com Inc. |

AMZN, |

3.30% | 5.50% | 5.84% |

| Nvidia Corp. |

NVDA, |

3.02% | 4.44% | 5.33% |

| Alphabet Inc. Class A |

GOOGL, |

2.17% | 3.12% | 3.83% |

| Alphabet Inc. Class C |

GOOG, |

1.88% | 3.11% | 3.32% |

| Tesla Inc. |

TSLA, |

1.79% | 3.10% | 3.17% |

| Meta Platforms Inc. Class A |

META, |

1.77% | 3.60% | 3.12% |

| Totals | 27.63% | 43.25% | 48.83% | |

| Sources: Invesco Ltd., State Street Corp. | ||||

The same group of seven companies (eight stocks with two common share classes for Alphabet) is at the top of each exchange-traded fund’s portfolio, although the top seven for QQQ aren’t in the same order as those for SPY and XLG. QQQ’s weighting was changed recently as the underlying Nasdaq-100 underwent a “special rebalancing” last month.

Here’s a five-year chart comparing the performance of the three approaches. All returns in this article include reinvested dividends.

QQQ has been the clear winner for five years, but it is also worth noting how well XLG has performed when compared with SPY. This “top 50” approach to the S&P 500 incorporates many stocks that aren’t listed on the Nasdaq and therefore cannot be included in QQQ, which itself is made up of the largest 100 nonfinancial companies in the full Nasdaq Composite Index

COMP,

Examples of stocks held by XLG that aren’t held by QQQ include such non-tech stalwarts as Berkshire Hathaway Inc.

BRK.B,

Johnson & Johnson

JNJ,

Procter & Gamble Co.

PG,

Home Depot Inc.

HD,

and Nike Inc.

NKE,

Now let’s go deeper into long-term performance. First, here are the total returns for various time periods:

| ETF | 3 Years | 5 Years | 10 Years | 15 Years | 20 Years |

|

SPDR S&P 500 ETF Trust SPY |

40% | 69% | 223% | 370% | 531% |

|

Invesco QQQ Trust QQQ |

41% | 113% | 430% | 882% | 1,158% |

|

Invesco S&P 500 Top 50 ETF XLG |

41% | 85% | 262% | 404% | N/A |

| Source: FactSet | |||||

Click on the tickers for more about each ETF, company or index.

There is no 20-year return for XLG because this ETF was established in 2005.

For five years and longer, QQQ has been the runaway leader, but for 5, 10 and 15 years, XLG has also beaten SPY handily, with broader industry exposure.

Something else to consider is that during 2022, when SPY was down 18.2%, XLG fell 24.3% and QQQ dropped 32.6%.

For disciplined long-term investors, the tech pain of 2022 may not seem to have been a small price to pay for outperformance. And it may have been easier to take the pounding when holding SPY or even XLG that year.

Here’s a look at the average annual returns for the three ETFs:

| ETF | 3 years | 5 years | 10 years | 15 years | 20 years |

|

SPDR S&P 500 ETF Trust SPY |

11.8% | 11.0% | 12.4% | 10.9% | 9.6% |

|

Invesco QQQ Trust QQQ |

12.0% | 16.3% | 18.2% | 16.4% | 13.5% |

|

Invesco S&P 500 Top 50 ETF XLG |

12.2% | 13.1% | 13.7% | 11.4% | N/A |

| Source: FactSet | |||||

So the question remains — do you believe that the largest technology companies will continue to lead the stock market for the next decade at least? If so, a more concentrated index approach may be for you, provided you can withstand the urge to sell into a declining market, such as the one we experienced last year.

Here is something else to keep in mind. In a note to clients on Monday, Doug Peta, the chief U.S. investment strategist at BCA, made a fascinating point: “The only novel development is that all the heaviest hitters now hail from Tech and Tech-adjacent sectors and are therefore more prone to move together than they were at the end of 2004, when the seven largest stocks came from six different sectors. “

Nothing lasts forever. Peta continued by suggesting that investors who are tired of big tech taking all the glory “need only wait.”

“[I]f history is any guide, their time at the top of the capitalization scale will be short,” he wrote.

Don’t miss: These four Dow stocks take top prizes for dividend growth

[ad_2]

[ad_1]

This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com.

https://www.barrons.com/articles/stock-market-movers-3fac9192

[ad_2]

[ad_1]

By David Sachs and Joshua Kirby

Eramet shares fell Wednesday after the French miner said it was ceasing operations in Gabon, where the military has reportedly seized control of the government in a coup.

At 0811 GMT, shares in Eramet slumped 19% to EUR61.65.

The company said all operations have stopped and rail traffic has been suspended in the West African country, and that it has begun procedures to ensure the safety of staff and facilities of its two subsidiaries there, Comilog and Setrag.

The former operates the Moanda manganese mine–the world’s largest–and Setrag is a rail transport company.

“The group continues to monitor developments in real time,” Eramet said.

Write to David Sachs at david.sachs@wsj.com and to Joshua Kirby at joshua.kirby@wsj.com

[ad_2]