[ad_1]

CNBC’s Leslie Picker joins ‘Squawk Box’ to report on Morgan Stanley’s quarterly earnings results.

[ad_2]

[ad_1]

CNBC’s Leslie Picker joins ‘Squawk Box’ to report on Morgan Stanley’s quarterly earnings results.

[ad_2]

[ad_1]

Morgan Stanley on Tuesday posted results that topped analysts’ estimates for profit and revenue as wealth management, trading and investment banking exceeded expectations.

Here’s what the company reported:

The bank said first-quarter profit rose 14% from a year earlier to $3.41 billion, or $2.02 a share, helped by rising results at each of its three main divisions. Revenue climbed 4% to $15.14 billion.

Shares of the bank jumped about 2.5%.

Wealth management revenue rose 4.9% to $6.88 billion, topping the StreetAccount estimate by $230 million, as rising markets helped boost fee revenue and offset a decline in interest income.

Equities trading revenue increased 4.1% to $2.84 billion, $160 million more than expected, fueled by derivatives volumes. Fixed income trading revenue slipped 3.5% to $2.49 billion, but that still topped expectations by $120 million.

Investment banking revenue jumped 16% to $1.45 billion, edging out the $1.40 billion estimate, as increases in debt and equity issuance offset lower fees from acquisitions.

The firm’s smallest division, investment management, was the only major business to underperform expectations. While revenue climbed 6.8% to $1.38 billion, it was below the $1.43 billion StreetAccount estimate.

CEO Ted Pick’s tenure had kicked off on a rocky note, as high interest rates have incentivized the bank’s wealth management customers to move cash into higher-yielding securities. The bank’s shares have declined nearly 7% this year before Tuesday.

But like rivals including Goldman Sachs and JPMorgan Chase, Morgan Stanley was helped by strong trading and investment banking results in the quarter.

Last week, JPMorgan, Wells Fargo and Citigroup each topped expectations for revenue and profit, a streak continued by Goldman on Monday and Bank of America on Tuesday.

Analysts questioned Pick about reports that multiple U.S. regulators are investigating Morgan Stanley for potential shortfalls in how it screens clients for its wealth management division.

“We’ve been focused on our client on-boarding and monitoring processes for a good while,” Pick said Tuesday. “We have been spending time, effort and money for multiple years, and it is ongoing. We’ve been on it and the costs associated with this are largely in the expense run rate.”

[ad_2]

[ad_1]

Bank of America on Tuesday reported first-quarter earnings that topped analysts’ estimates for profit and revenue on better-than-expected interest income and investment banking.

Here’s what the company reported:

The bank said profit fell 18% to $6.67 billion, or 76 cents a share; excluding a $700 million FDIC assessment, profit was 83 cents a share. Revenue slipped 1.6% to $25.98 billion as net interest income declined from a year earlier.

Net interest income, or the difference between what the company earns from loans and investments and what it pays customers for their deposits, was $14.19 billion, topping the $13.93 billion StreetAccount estimate.

The bank’s interest income was a “slight positive surprise,” though it’s unclear if this means the metric will improve earlier than expected, Wells Fargo analyst Mike Mayo said Tuesday in a research note.

The bank’s total deposits of $1.95 trillion climbed roughly 1% from the fourth quarter, while loans were essentially unchanged at $1.05 trillion.

“I was unimpressed with deposits and loans being flat,” David Wagner, portfolio manager at Aptus Capital Advisors, said in an email. “The only areas that BAC did well was where other banks have shown strength.”

Bank of America CFO Alastair Borthwick told analysts Tuesday in a conference call that NII will likely dip in the second quarter to about $14 billion on drops in wealth management and markets interest income. Though it could grow in the second half of the year, he said.

NII has been declining in recent quarters as funding costs have climbed along with the rise in interest rates.

Shares of the bank fell more than 3%.

Bank of America’s share decline Tuesday has more to do with the rise in the 10 year Treasury yield than first quarter results, according to KBW analyst David Konrad. Shares of many banks have been yoked to yields in the past year, as rising yields means some bond and loan holdings decline in value.

Investment banking revenue jumped 35% to $1.57 billion, exceeding the $1.36 billion estimate and following a similar rise at rivals including Goldman Sachs and JPMorgan Chase.

It’s also considerably higher than the guidance given by Borthwick, who told analysts last month to expect investment banking revenue to rise by 10% to 15% from a year earlier.

The bank’s trading operations also edged out expectations. Fixed income revenue fell 3.6% to $3.31 billion, slightly beating the $3.24 billion estimate, and equities revenue rose 15% to $1.87 billion, compared with the $1.84 billion estimate.

[ad_2]

[ad_1]

Harsh Modi of the investment bank discusses the opportunities in India's banking sector.

[ad_2]

[ad_1]

David Solomon, Chairman & CEO Goldman Sachs, speaking on CNBC’s Squawk Box at the World Economic Forum Annual Meeting in Davos, Switzerland on Jan. 17th, 2024.

Adam Galici | CNBC

Goldman Sachs is scheduled to report first-quarter earnings before the opening bell Monday.

Here’s what Wall Street expects:

Goldman Sachs CEO David Solomon has taken his lumps in the past year, but hope is building for a turnaround.

Dormant capital markets and missteps tied to Solomon’s ill-fated push into retail banking should give way to stronger results this year.

Rivals JPMorgan Chase and Citigroup posted better-than-expected trading results and a rebound in investment banking fees in the first quarter; investors will be disappointed if Goldman doesn’t show similar gains.

Unlike more diversified rivals, Goldman gets most of its revenue from Wall Street activities. That can lead to outsized returns during boom times and underperformance when markets don’t cooperate.

After pivoting away from retail banking, Goldman’s new emphasis for growth has centered on its asset and wealth management division. The business could see gains from buoyant markets at the start of the year, though it also has taken write-downs tied to commercial real estate in the past.

Solomon may also field questions about the latest examples of an exodus in senior managers, including his global treasurer Philip Berlinski and Beth Hammack, co-head of the bank’s global financing group.

On Friday, JPMorgan, Citigroup and Wells Fargo each posted quarterly results that topped estimates.

This story is developing. Please check back for updates.

[ad_2]

[ad_1]

The pandemic accelerated changes at big banks, where Chase and Wells Fargo already have branches that look more like lounges than banks. But it’s not just Wall Street-sized banks where AI is disrupting the way things works.

Small, independent branches are also following, and experts and executives say they’ll use their small size and agility to their advantage. The local bank branch, with its traditional teller windows and long lines, will transform into an AI-infused, customer-centric financial services center, aiming to beat the big banks on the service that AI will allow them to provide customers.

“As a small bank, your only value proposition is service. Nothing is proprietary anymore,” said Christopher Naghibi, executive vice president and CEO of Irvine, California-based First Foundation Bank, which has 43 branches in five states. With just over $10 billion in assets, Naghibi helped shepherd First Foundation from a single branch in 2007 to its size today.

Naghibi envisions community bank branches with fewer employees and more AI. The employees would be freed to help customers reach their financial goals and not be stuck answering basic questions about recent transactions and account information.

“The teller line, as we see it today, will eventually die,” he said.

Naghibi isn’t alone among bank CEOs contemplating the AI future for financial workers and customer interactions.

Jamie Dimon, the veteran chairman and CEO of JPMorgan Chase, has written about artificial intelligence in his annual shareholder letters dating back to 2017. But his latest letter, released on Monday, was notable not only for his AI predictions — he wrote it could be as transformational as the printing press, the steam engine, electricity, computing and the internet — but also how he thinks the technology could impact the jobs of the bank’s more than 310,000 employees.

“Over time, we anticipate that our use of AI has the potential to augment virtually every job, as well as impact our workforce composition,” Dimon wrote. “It may reduce certain job categories or roles, but it may create others as well.”

Many of JPMorgan’s AI ambitions are taking place behind the scenes rather than at the teller window — it now has more than 2,000 AI and machine learning employees and data scientists working on 400 applications including fraud detection, marketing and risk controls, Dimon said. The bank is also exploring the use of generative AI in software engineering, customer service and ways to boost employee productivity.

For smaller banks, the customer interaction may be the critical application, with AI freeing a bank’s resources from answering routine questions..

“This will be at the forefront of how we engage in service,” Naghibi said. “You can ask AI, ‘Hey, did this happen? Did this check clear? How many payments have I made to this person?’ You’ll get answers directly from AI.”

Customers will be able to go in 24/7 with a special access technology and pay bills by touchscreens, send a wire at midnight, and see transactions updated in real-time. “Effectively, a small bank’s branch will be a wall of screens,” he said.

Security will improve at transformed branches as paper money becomes less plentiful and more locked into machines. The AI will bring a lot more security to branches also, with plenty of cameras, biometrics used for access, and PIN codes a thing of the past. It will also help in more extreme scenarios. “If someone has a weapon, AI can automatically see that it is a weapon, sense it, and prevent a problem,” Naghibi said.

Jackie Verkuyl, chief administrative officer of the eight-branch BAC Community Bank in Stockton, California, a commercial and consumer bank with over $800 million deposits, says implementation of generative AI is already well underway and transforming the small bank. “The AI is getting smarter every day,” she said.

But while the corner bank will become an AI-infused financial services center, Verkuyl says generative AI will bring the same services to phones, far beyond the capability of current apps. BAC uses an app called Smart Alac (an acronym for All Access Connection), developed by San Francisco-based Agent IQ, which answers customer questions and matches them with a BAC banker who becomes their assigned point of contact. “This allows community and regional banks to provide self-service AI and have a relationship-based banking experience; every customer has a primary point of contact,” said Slaven Bilac, CEO of Agent IQ, a AI-powered customer support platform.

AI distills all the questions that customers are asking Smart Alac and provides a report to Verkuyl, allowing her to tailor the experience more. “We get lots and lots of questions about debit cards, so we created a whole menu that customers can help themselves to,” she said.

“Chase and Wells Fargo’s advantage over BAC is the amount of data they have. We can provide AI benefits without large amounts of know-how from BAC’s team,” Bilac said.

Not everyone in the industry is convinced.

The way a bank controls and shares large amounts of data with AI will be critical to effective transformation, according to Ken Tumin, a senior analyst at LendingTree. Banks have to give AI access to enough data to be effective, from account disclosures to frequently asked questions. “Unless a bank is committed to generating and maintaining high quality and comprehensive data, the use of AI in customer service will likely result in more customers being aggravated than pleased,” he said.

The Independent Community Banking Association, a trade group for small banks, doesn’t think AI can outshine the human element in a relationship. While AI will be a significant factor, “it will never match the local knowledge and personal relationships that are crucial to helping a first-time homebuyer get a mortgage or helping a small business or farm finance its operations,” said ICBA assistant vice president and regulatory counsel Mickey Marshall.

But bankers like Naghibi believe AI will allow small banks to become more involved in their communities, and in effect, more human.

“Right now, getting branch managers to go out into the community and get business is tough. We are not a large, important bank; people are not going to come to us. You have to go out and build relationships,” Naghibi said. “If generative AI is in place, you as a branch manager should be going to get business.”

Multiple human and tech-centered connections serve as “touchpoints” to the consumer, Naghibi said, and “the more touchpoints the bank has in their financial lives, the more we can be involved in their lives. As a community bank, that is where the edge is.”

“Community banking needs to change; every single one of my clients has my mobile number,” he added. “People don’t want untouchable and unreachable. Making local bankers more accessible is the promise of AI.”

[ad_2]

[ad_1]

Wells Fargo customers use the ATM at a bank branch on August 08, 2023 in San Bruno, California.

Justin Sullivan | Getty Images

Wells Fargo reported better-than-expected earnings results on Friday, but some weakness under the hood is putting a lid on the bank’s stock. Stay the course: Shares should move higher as management continues to shake off regulatory punishments for past misdeeds.

[ad_2]

[ad_1]

JPMorgan Chase CEO and Chairman Jamie Dimon gestures as he speaks during the U.S. Senate Banking, Housing and Urban Affairs Committee oversight hearing on Wall Street firms, on Capitol Hill in Washington, U.S., December 6, 2023.

Evelyn Hockstein | Reuters

JPMorgan Chase CEO Jamie Dimon warned Friday that multiple challenges, primarily inflation and war, threaten an otherwise positive economic backdrop.

“Many economic indicators continue to be favorable,” the head of the largest U.S. bank by assets said in announcing first-quarter earnings results. “However, looking ahead, we remain alert to a number of significant uncertain forces.”

An “unsettling” global landscape, including “terrible wars and violence,” is one such factor introducing uncertainty into both JPMorgan’s business and the broader economy, Dimon said.

Additionally, he noted “persistent inflationary pressures, which may likely continue.”

Dimon also noted the Federal Reserve’s efforts to draw down the assets it is holding on its $7.5 trillion balance sheet.

“We have never truly experienced the full effect of quantitative tightening on this scale,” Dimon said.

The latter comment references the nickname given to a process the Fed is employing to reduce the level of Treasurys and mortgage-backed securities it is holding.

The central bank is allowing up to $95 billion in proceeds from maturing bonds to roll off each month rather than reinvesting them, resulting in a $1.5 trillion contraction in holdings since June 2022. The program is part of the Fed’s efforts to tighten financial conditions in hopes of alleviating inflationary pressures.

Though the Fed is expected to slow down the pace of quantitative tightening in the next few months, the balance sheet will continue to contract.

Taken together, Dimon said the three issues pose substantial unknowns ahead.

“We do not know how these factors will play out, but we must prepare the Firm for a wide range of potential environments to ensure that we can consistently be there for clients,” he said.

Dimon’s comments come amid renewed worries over inflation. Though the pace of price increases has come well off the boil from its June 2022 peak, data so far in 2024 has shown inflation consistently higher than expectations and well above the Fed’s 2% annual goal.

As a result, markets have had to dramatically shift their expectations for interest rate reductions. Whereas markets at the beginning of the year had been looking for up to seven cuts, or 1.75 percentage points, the expectation now is for only one or two that would total at most half a percentage point.

Higher rates are generally considered positive for banks as long as they don’t lead to a recession. JPMorgan on Friday reported an 8% boost in revenue in the first quarter, attributable to stronger interest income and higher loan balances. However, the bank warned net interest income for this year could be slightly below what Wall Street is expecting and shares were off nearly 2% in premarket trading.

[ad_2]

[ad_1]

Citigroup on Friday posted first-quarter revenue that topped analysts’ estimates, helped by better-than-expected results in the bank’s investment banking and trading operations.

Here’s how the company performed, compared with estimates from LSEG, formerly known as Refinitiv:

The bank said profit fell 27% from a year earlier to $3.37 billion, or $1.58 a share, on higher expenses and credit costs. Adjusting for the impact of FDIC charges as well as restructuring and other costs, Citi earned $1.86 per share, according to LSEG calculations.

Revenue slipped 2% to $21.10 billion, mostly driven by the impact of selling an overseas business in the year-earlier period.

Investment banking revenue jumped 35% to $903 million in the quarter, driven by rising debt and equity issuance, topping the $805 million StreetAccount estimate.

Fixed income trading revenue fell 10% to $4.2 billion, edging out the $4.14 billion estimate, and equities revenue rose 5% to $1.2 billion, topping the $1.12 billion estimate.

The bank also posted an 8% gain to $4.8 billion in revenue in its Services division, which includes businesses that cater to the banking needs of global corporations, thanks to rising deposits and fees.

Shares of the bank fell nearly 2% Friday.

Citigroup CEO Jane Fraser previously said that her sweeping corporate overhaul would be complete by March, and that the firm would give an update to severance expenses along with first-quarter results.

“Last month marked the end to the organizational simplification we announced in September,” Fraser said in the earnings release. “The result is a cleaner, simpler management structure that fully aligns to and facilitates our strategy.

Last year, Fraser announced plans to simplify the management structure and reduce costs at the third-biggest U.S. bank by assets. The bank on Friday reiterated its medium term targets for returns hitting at least 11% and generating at least $80 billion in revenue this year.

JPMorgan Chase reported results earlier Friday, and Goldman Sachs reports on Monday.

[ad_2]

[ad_1]

The exterior of the Bank of England in the City of London, United Kingdom.

Mike Kemp | In Pictures | Getty Images

LONDON — The Bank of England on Friday announced a “once in a generation” overhaul of its inflation forecasting following a long-awaited review by former Federal Reserve Chair Ben Bernanke.

The review — initiated after criticism of the central bank’s policymaking amid spiraling inflation — sets out 12 recommendations which BOE Governor Andrew Bailey said the bank was committed to implementing.

Bailey told CNBC it had been “invaluable” to compare and contrast the U.S. policy perspective with its own.

“This is a once in a generation opportunity to update our forecasting, and ensure it is fit for our more uncertain world,” Bailey said.

Bernanke’s recommendations are organized into three key areas: improving the bank’s forecasting infrastructure, supporting decision-making within the Monetary Policy Committee (MPC) and better communicating economic risks to the public.

The provisions include scrapping the bank’s long-held “fan chart” forecasting system and introducing a revamped forecast framework.

The fan chart — which shows a range of possible future data points — has long been used by the bank to present the probability distribution that forms the basis of its inflation forecasts. The model has faced heavy criticism over recent years for failing to accurately keep track of inflationary pressures, and the review concluded that fan charts had “outlived their usefulness” and “should be eliminated.”

Bernanke stopped short of recommending Fed-style “dot plot” forecasting, which was introduced in the U.S. after the global financial crisis to allow each member to chart their course of policy stance, inflation, real GDP and employment. But he suggested a new model which better reflects the differing views of committee members and how inflation expectations can become “de-anchored.”

He also noted that the BOE currently relies more heavily on a central forecast than do other central banks, and said that its analysis should be supplemented with a wider range of alternative scenarios that “help the public better understand the reasons for the policy choice.” Such scenarios may include the effects of different policy choices, or unexpected global shocks.

The suggestion came as part of a wider set of recommendations on how the bank can improve its communications with the public, simplify its policy statement and reduce repetitiveness. The review also said that the bank should move ahead with the current modernization of the software it uses to manage and manipulate data as a “high priority.”

The Bernanke review was launched last summer to assess the bank’s struggles to accurately project the huge global spike in inflation after Russia’s invasion of Ukraine.

The bank was widely criticized for being too slow to hike interest rates, meaning it subsequently had to raise its main bank rate to a 15-year high of 5.25%.

With inflation now falling faster than the MPC had anticipated, some economists have contended that the bank is committing the same mistake in the opposite direction, by cutting rates too slowly.

Bernanke added that his role chairing the Fed during the global financial crisis highlighted the critical role of monetary policy on the real economy, but added that the review made “no judgment” of the BOE’s recent decision-making.

“The effects of the financial sector on the economy go beyond interest rates. Credibility is important. Risk-taking is important,” he told CNBC.

He also said that the difficulties in forecasting were not unique to the BOE, but added that he hoped the bank would draw appropriate lessons from the experience.

The review recommended that the bank take a phased approach to implementing the new measures, starting with improving its forecasting infrastructure. It should then “cautiously” move on to adopting changes to its policymaking and communications, it said.

Incoming BOE Deputy Governor Clare Lombardelli has been charged with leading the implementation of these recommendations when she takes her seat in July. The bank said it will provide an update on the proposed changes by the end of the year.

— CNBC’s Elliott Smith contributed to this article.

[ad_2]

[ad_1]

Jamie Dimon, President and CEO of JPMorgan Chase, speaking on CNBC’s “Squawk Box” at the World Economic Forum Annual Meeting in Davos, Switzerland, on Jan. 17, 2024.

Adam Galici | CNBC

JPMorgan Chase is scheduled to report first-quarter earnings before the opening bell Friday.

Here’s what Wall Street expects:

JPMorgan will be watched closely for clues on how banks fared at the start of the year.

While the biggest U.S. bank by assets has navigated the rate environment well since the Federal Reserve began raising rates two years ago, smaller peers have seen their profits squeezed.

The industry has been forced to pay up for deposits as customers shift cash into higher-yielding instruments, squeezing margins. Concern is also mounting over rising losses from commercial loans, especially on office buildings and multifamily dwellings, and higher defaults on credit cards.

Still, large banks are expected to outperform smaller ones this quarter, and expectations for JPMorgan are high. Analysts believe the bank can boost guidance for 2024 net interest income as the Federal Reserve is forced to maintain interest rate levels amid stubborn inflation data.

Analysts will also want to hear what CEO Jamie Dimon has to say about the economy and the industry’s efforts to push back against efforts to cap credit card and overdraft fees.

Wall Street may provide some help this quarter, with investment banking fees for the industry up 11% from a year earlier, according to Dealogic.

Shares of JPMorgan have jumped 15% this year, outperforming the 3.9% gain of the KBW Bank Index.

Wells Fargo and Citigroup are scheduled to release results later Friday, while Goldman Sachs, Bank of America and Morgan Stanley report next week.

This story is developing. Please check back for updates.

[ad_2]

[ad_1]

A woman walks past Wells Fargo bank in New York City, U.S., March 17, 2020.

Jeenah Moon | Reuters

What a difference a year makes.

[ad_2]

[ad_1]

Traders work on the floor at the New York Stock Exchange (NYSE) in New York City, U.S., February 7, 2024.

Brendan Mcdermid | Reuters

The benefits of scale will never be more obvious than when banks begin reporting quarterly results on Friday.

Ever since the chaos of last year’s regional banking crisis that consumed three institutions, larger banks have mostly fared better than smaller ones. That trend is set to continue, especially as expectations for the magnitude of Federal Reserve interest rates cuts have fallen sharply since the start of the year.

The evolving picture on interest rates — dubbed “higher for longer” as expectations for rate cuts this year shift from six reductions to perhaps three – will boost revenue for big banks while squeezing many smaller ones, adding to concerns for the group, according to analysts and investors.

JPMorgan Chase, the nation’s largest lender, kicks off earnings for the industry on Friday, followed by Bank of America and Goldman Sachs next week. On Monday, M&T Bank posts results, one of the first regional lenders to report this period.

The focus for all of them will be how the shifting view on interest rates will impact funding costs and holdings of commercial real estate loans.

“There’s a handful of banks that have done a very good job managing the rate cycle, and there’s been a lot of banks that have mismanaged it,” said Christopher McGratty, head of U.S. bank research at KBW.

Take, for instance, Valley Bank, a regional lender based in Wayne, New Jersey. Guidance the bank gave in January included expectations for seven rate cuts this year, which would’ve allowed it to pay lower rates to depositors.

Instead, the bank might be forced to slash its outlook for net interest income as cuts don’t materialize, according to Morgan Stanley analyst Manan Gosalia, who has the equivalent of a sell rating on the firm.

Net interest income is the money generated by a bank’s loans and securities, minus what it pays for deposits.

Smaller banks have been forced to pay up for deposits more so than larger ones, which are perceived to be safer, in the aftermath of the Silicon Valley Bank failure last year. Rate cuts would’ve provided some relief for smaller banks, while also helping commercial real estate borrowers and their lenders.

Valley Bank faces “more deposit pricing pressure than peers if rates stay higher for longer” and has more commercial real estate exposure than other regionals, Gosalia said in an April 4 note.

Meanwhile, for large banks like JPMorgan, higher rates generally mean they can exploit their funding advantages for longer. They enjoy the benefits of reaping higher interest for things like credit card loans and investments made during a time of elevated rates, while generally paying low rates for deposits.

JPMorgan could raise its 2024 guidance for net interest income by an estimated $2 billion to $3 billion, to $93 billion, according to UBS analyst Erika Najarian.

Large U.S. banks also tend to have more diverse revenue streams than smaller ones from areas like wealth management and investment banking. Both should provide boosts to first-quarter results, thanks to buoyant markets and a rebound in Wall Street activity.

Furthermore, big banks tend to have much lower exposure to commercial real estate compared with smaller players, and have generally higher levels of provisions for loan losses, thanks to tougher regulations on the group.

That difference could prove critical this earnings season.

Concerns over commercial real estate, especially office buildings and multifamily dwellings, have dogged smaller banks since New York Community Bank stunned investors in January with its disclosures of drastically larger loan provisions and broader operational challenges. The bank needed a $1 billion-plus lifeline last month to help steady the firm.

NYCB will likely have to cut its net interest income guidance because of shrinking deposits and margins, according to JPMorgan analyst Steven Alexopoulos.

There is a record $929 billion in commercial real estate loans coming due this year, and roughly one-third of the loans are for more money than the underlying property values, according to advisory firm Newmark.

“I don’t think we’re out of the woods in terms of commercial real estate rearing its ugly head for bank earnings, especially if rates stay higher for longer,” said Matt Stucky, chief portfolio manager for equities at Northwestern Mutual.

“If there’s even a whiff of problems around the credit experience with your commercial lending operation, as was the case with NYCB, you’ve seen how quickly that can get away from you,” he said.

[ad_2]

[ad_1]

Two leading NBFCs -Bajaj Finance and Shriram Finance -have hiked rates on term deposits following a slew of deposit rate hikes by banks in Q4 FY24.

While traditionally NBFCs offer higher deposit rates than banks, intensified competition for deposit accretion has forced NBFCs to compete with smaller private banks and small finance banks which have turned more aggressive on rates.

Currently, medium and small private banks are offering FD rates up to 8.5 per cent for regular citizens and up to 9.0 per cent for senior citizens, whereas small finance banks are giving interest of up to 9.25 per cent.

Bajaj Finance has increased FD rates for most tenures by up to 60 bps, effective April 3. FD rates have been hiked by up to 45 bps for deposits with a tenure of 25-35-months, by 40 bps for 18 and 22-month deposits, and by 35 bps for FDs with a tenure of 30 and 33 months.

For senior citizens FD rates have been hiked by up to 60 bps in the 25-35-month tenure and by 40 bps in the 18-24-month tenure.

“Senior citizens can continue to avail FD rates of up to 8.85 perc ent and non-senior citizens can take benefit of rates of up to 8.60 per cent by booking digitally in the 42-month tenure,” the company said in a release.

Another NBFC Shriram Finance has raised FD rates by 5-20 bps across deposits maturing in 12 to 60 months. The rates effective April 9 go up to maturities that range between 12 and 60 months, effective April 9.

Deposits between 12 and 36 months will earn up to 7.85 per cent whereas those between 36 and 60 months will earn up to 8.8 per cent interest. Further, an additional 50 bps is being offered to senior citizens and 10 bps to women depositors. Effectively, senior citizen women investors can earn up to 9.4 per cent interest.

Like banks, NBFCs too are struggling to raise funds to support the sustained pace of credit growth. In addition to increased competition from banks for deposits, NBFCs have also seen normalisation in bank credit lines due to repeated warnings by the central bank on increasing inter-connectedness between the two sectors, making deposit accretion even more crucial.

While banks have been hiking rates through H2 FY24 on various maturity buckets, NBFCs have less flexibility in changing deposit rates. Further, a lot of these lenders were also waiting for the end of the quarter and the financial year to protect their margins for the reported period, analysts said.

Deposit growth for most private banks accelerated during Q4 to 14-26 per cent. Sequential deposit growth too was higher at 4-15 per cent compared with 2-8 per cent in the previous quarter, as per provisional numbers declared by banks. Small finance banks saw high growth of 24-50 per cent.

[ad_2]

[ad_1]

Carey Halio, Goldman Sachs’ head of strategy and investor relations, is getting promoted to global treasurer at the bank, according to people familiar with the matter.

Her new role, effective June 1, encompasses authority over the firm’s more than $1.6 trillion balance sheet, with responsibilities including overseeing the firm’s liquidity, funding and capital. She will report to Denis Coleman, Goldman Sachs’ chief financial officer.

Philip Berlinski, the previous global treasurer, is leaving the bank to become co-chief operating officer of Millennium Management, a $62 billion hedge fund, according to the Financial Times.

As part of her new role, Halio will oversee a team of about 900 people, the people familiar said. She will also serve on the management committee.

“As a tenured leader of the firm with experience working in several of our divisions and partnering with leaders across the organization to drive our strategic priorities forward, Carey will bring important expertise and perspectives to her new role,” Goldman Sachs CEO David Solomon said in a memo, obtained by CNBC. “Carey will continue to oversee our Firmwide Strategy team on an interim basis.”

Before running strategy and investor relations, Halio was the CEO of Goldman Sachs Bank USA and deputy treasurer of Goldman Sachs. She joined the firm in 1999 as a summer associate in credit risk and rejoined the following year, ultimately becoming the head of the Americas Financial Institutions team in credit risk.

Jehan Ilahi, who worked with Halio for years in strategy and investor relations, will become head of investor relations.

Goldman Sachs is slated to report first-quarter earnings Monday.

[ad_2]

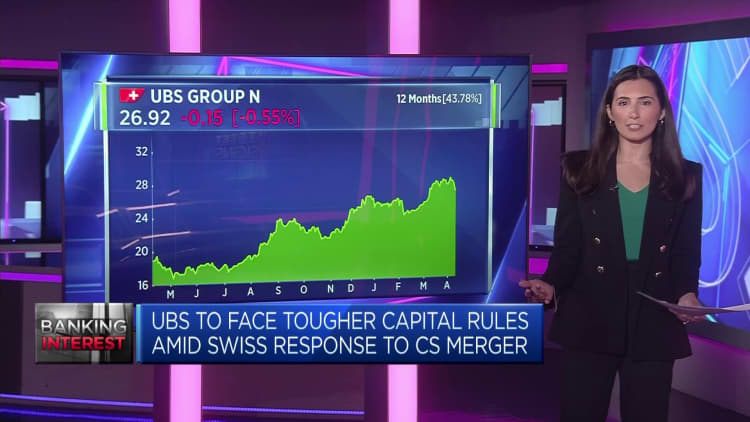

[ad_1]

Sergio Ermotti, CEO of Swiss banking giant UBS, during the group’s annual shareholders meeting in Zurich on May 2, 2013.

Fabrice Coffrini | Afp | Getty Images

Switzerland’s tough new banking regulations create a “lose-lose situation” for UBS and may limit its potential to challenge Wall Street giants, according to Beat Wittmann, partner at Zurich-based Porta Advisors.

In a 209-page plan published Wednesday, the Swiss government proposed 22 measures aimed at tightening its policing of banks deemed “too big to fail,” a year after authorities were forced to broker the emergency rescue of Credit Suisse by UBS.

The government-backed takeover was the biggest merger of two systemically important banks since the Global Financial Crisis.

At $1.7 trillion, the UBS balance sheet is now double the country’s annual GDP, prompting enhanced scrutiny of the protections surrounding the Swiss banking sector and the broader economy in the wake of the Credit Suisse collapse.

Speaking to CNBC’s “Squawk Box Europe” on Thursday, Wittmann said that the fall of Credit Suisse was “an entirely self-inflicted and predictable failure of government policy, central bank, regulator, and above all [of the] finance minister.”

“Then of course Credit Suisse had a failed, unsustainable business model and an incompetent leadership, and it was all indicated by an ever-falling share price and by the credit spreads throughout [20]22, [which was] completely ignored because there is no institutionalized know-how at the policymaker levels, really, to watch capital markets, which is essential in the case of the banking sector,” he added.

The Wednesday report floated giving additional powers to the Swiss Financial Market Supervisory Authority, applying capital surcharges and fortifying the financial position of subsidiaries — but stopped short of recommending a “blanket increase” in capital requirements.

Wittman suggested the report does nothing to assuage concerns about the ability of politicians and regulators to oversee banks while ensuring their global competitiveness, saying it “creates a lose-lose situation for Switzerland as a financial center and for UBS not to be able to develop its potential.”

He argued that regulatory reform should be prioritized over tightening the screws on the country’s largest banks, if UBS is to capitalize on its newfound scale and finally challenge the likes of Goldman Sachs, JPMorgan, Citigroup and Morgan Stanley — which have similarly sized balance sheets, but trade at s much higher valuation.

“It comes down to the regulatory level playing field. It’s about competences of course and then about the incentives and the regulatory framework, and the regulatory framework like capital requirements is a global level exercise,” Wittmann said.

“It cannot be that Switzerland or any other jurisdiction is imposing very, very different rules and levels there — that doesn’t make any sense, then you cannot really compete.”

In order for UBS to optimize its potential, Wittmann argued that the Swiss regulatory regime should come into line with that in Frankfurt, London and New York, but said that the Wednesday report showed “no will to engage in any relevant reforms” that would protect the Swiss economy and taxpayers, but enable UBS to “catch up to global players and U.S. valuations.”

“The track record of the policymakers in Switzerland is that we had three global systemically relevant banks, and we have now one left, and these cases were the direct result of insufficient regulation and the enforcement of the regulation,” he said.

“FINMA had all the legal backdrop, the instruments in place to address the situation but they didn’t apply it — that’s the point — and now we talk about fines, and that sounds like pennywise and pound foolish to me.”

[ad_2]

[ad_1]

Beat Wittman, partner at Porta Advisors, reviews new Swiss banking regulation and its potential impact on UBS in the wake of its absorption of Credit Suisse.

[ad_2]

[ad_1]

A New York Community Bank stands in Brooklyn on February 08, 2024 in New York City.

Spencer Platt | Getty Images

New York Community Bank, the regional lender that needed a $1 billion-plus lifeline last month, is offering the country’s highest interest rate for a savings account.

NYCB raised the annual percentage yield offered via its online arm, My Banking Direct, to 5.55%, higher than any other bank’s widely available account, according to Ken Tumin, an analyst who tracks rates for his website DepositAccounts.

The standout rate could be a sign that NYCB is facing funding pressure, Tumin said.

“It looks like they’re trying really hard to attract deposits,” Tumin said. “My Banking Direct has been around for a long time, more than 10 years, so them having an aggressive rate could be a sign of neediness” for funding.

NYCB’s woes began in January, when it said it was preparing for far greater losses on commercial real estate loans than analysts had expected. That set off a downward spiral in its stock price, downgrades from rating agencies and multiple management changes. The bank announced a capital injection from investors led by former Treasury Secretary Steven Mnuchin’s Liberty Strategic Capital on March 6.

In the month before the rescue was announced, NYCB shed 7% of its deposits, falling to $77.2 billion by March 5, the bank said in a presentation.

During a conference call held after the capital raise, analysts asked how NYCB managed to retain so much of its deposits during the tumultuous period.

“We didn’t do anything crazy relative to deposit pricing,” NYCB chairman Sandro DiNello replied. “We didn’t go out and offer 6% CDs or something like that in order to make the numbers look good, if that’s what you’re concerned with.”

NYCB didn’t return a call for comment on its funding strategy.

Joseph Otting, a former comptroller of the currency, took over as the bank’s CEO on April 1, about a week before the rate increase.

Despite the turnaround plan, shares of NYCB still trade for under $4 apiece and are off more than 68% year to date.

Other banks offering rates higher than 5% right now tend to be newer or smaller players than NYCB, according to Tumin.

Among established banks, the average high-yield savings rate is about 4.4%, and several of them (including American Express, Goldman Sachs and Ally) have dropped rates in the past month, he said. The NYCB rate also tops accounts listed on NerdWallet and Bankrate.

Customer deposits at My Banking Direct are insured by the FDIC up to the standard $250,000.

Over the past two years, savings account rates have broadly been on the rise.

Since the regional banking crisis consumed Silicon Valley Bank and First Republic last year, smaller players have been forced to pay higher rates for deposits compared to giants like JPMorgan Chase in order to compete, said Matt Stucky, chief portfolio manager for equities at Northwestern Mutual.

“When a bank has to go out and advertise a much higher rate, it’s typically because they have a deposit problem,” Stucky said. “It’s not hard for customers to switch banks anymore.”

[ad_2]

[ad_1]

There are credit cards designed to meet all kinds of financial situations and needs. Whether you’re a foodie, road warrior, traveler, student or someone looking to build credit, there are many card options to choose from.

To help narrow down the best credit card for your lifestyle, each month, CNBC Select publishes a list of the top credit cards available. It can change depending on limited-time sign-up bonuses, benefits and more.

However, some cards deserve extra recognition for consistently differentiating themselves from the competition and topping our rankings month after month. These cards offer extra generous rewards and perks and continuously evolve to meet changing needs.

Here, CNBC Select rounds up the best credit cards of 2024 for a variety of consumer habits based on rewards, fees, introductory and standard APRs, as well as other perks like annual statement credits, discounts at select retailers and built-in insurance. (See our methodology for more information on how we choose the best credit cards of 2024.)

Enjoy 4.5% cash back on drugstore purchases and dining at restaurants, including takeout and eligible delivery services, 6.5% cash back on travel purchased through Chase Travel, our premier rewards program that lets you redeem rewards for cash back, travel, gift cards and more; and 3% cash back on all other purchases (on up to $20,000 spent in the first year). After your first year or $20,000 spent, enjoy 5% cash back on travel purchased through Chase Travel, 3% cash back on drugstore purchases and dining at restaurants, including takeout and eligible delivery service, and unlimited 1.5% cash back on all other purchases.

INTRO OFFER: Earn an additional 1.5% cash back on everything you buy (on up to $20,000 spent in the first year) – worth up to $300 cash back!

0% for the first 15 months from account opening on purchases and balance transfers

Intro fee of either $5 or 3% of the amount of each transfer, whichever is greater, on transfers made within 60 days of account opening. After that, either $5 or 5% of the amount of each transfer, whichever is greater.

Member FDIC. Terms apply.

Who’s this for? The Chase Freedom Unlimited® Card is ideal for consumers who want a robust rewards card with no annual fee.

Cardholders earn 5% cash back on travel purchased through Chase Ultimate Rewards®, 3% on drugstores and dining at restaurants (including takeout) and 1.5% on all other purchases. Plus, there’s a generous welcome bonus.

This card has no annual fee, and you can benefit from an introductory APR offer. This card also offers 5% cash back on Lyft purchases through March 31, 2025 and complimentary three months of DashPass with 50% off for the next nine months. Simply activate by December 31, 2024.

4X Membership Rewards® points at Restaurants (plus takeout and delivery in the U.S.) and at U.S. supermarkets (on up to $25,000 per calendar year in purchases, then 1X), 3X points on flights booked directly with airlines or on amextravel.com, 1X points on all other purchases

Earn 60,000 Membership Rewards® points after you spend $6,000 on eligible purchases with your new Card within the first 6 months of Card Membership.

Who’s this for? If you love food and travel, the American Express® Gold Card could be the ideal card for you. Whether you dine out or cook at home, this card earns a competitive 4X points per dollar spent at restaurants and 4X points at U.S. supermarkets (on up to $25,000 per year in purchases, then 1X). Plus, travelers can benefit from the 3X points on flights booked directly with airlines or on amextravel.com.

The value of Membership Rewards points varies depending on how cardholders redeem them. You can use them in a variety of ways, from paying with points at checkout at sites like Amazon to redeeming for gift cards or a statement credit to booking travel. See more on how points are calculated.

Cardholders also receive an annual dining credit of up to $120 ($10 in statement credits a month) at participating partners, including Grubhub, The Cheesecake Factory, Goldbelly, Wine.com, Milk Bar and select Shake Shack locations. Terms apply. Enrollment required. There are also *no foreign transaction fees.

This card does have a *$250 annual fee, but it can be reduced to effectively $130 if you take advantage of the $120 dining credit each year. Then, the rewards you earn help further “pay” for the card.

Gold Card members can also participate in Amex Offers, where you can earn statement credits or bonus Membership Rewards® points at select retailers. For example, a recent offer for Wine.com states: “Spend $50 or more, get $10 back.” These limited-time offers are location-based and additional terms apply.

*See rates and fees.

Enjoy benefits such as 5x on travel purchased through Chase Ultimate Rewards®, 3x on dining, select streaming services and online groceries, 2x on all other travel purchases, 1x on all other purchases, and $50 annual Ultimate Rewards Hotel Credit, plus more.

Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That’s $750 when you redeem through Chase Ultimate Rewards®.

21.49% – 28.49% variable on purchases and balance transfers

Either $5 or 5% of the amount of each transfer, whichever is greater

Who’s this for? If you want to get a lot of value right out of the gate, consider the Chase Sapphire Preferred. The card is currently offering new cardholders the chance to earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That’s $750 when you redeem through Chase Travel℠. You can even potentially get more value if you transfer Chase points to Chase’s travel partners, like Hyatt hotels and United Airlines, and book business-class flights and luxury hotels.

The Sapphire Preferred is also a great travel rewards credit card and has strong earning categories for those who spend on travel and dining. It earns 5X on travel purchased through Chase Travel℠, 3X on dining, select streaming services and online groceries, 2X on all other travel purchases, 1x on all other purchases, $50 Annual Chase Travel Hotel Credit, plus more.

Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases. To earn cash back, pay at least the minimum due on time. Plus, for a limited time, earn 5% total cash back on hotel, car rentals and attractions booked on the Citi Travel℠ portal through 12/31/24

Earn $200 cash back after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

0% for the first 18 months on balance transfers; N/A for purchases

For balance transfers completed within 4 months of account opening, an intro balance transfer fee of 3% of each transfer ($5 minimum) applies; after that, a balance transfer fee of 5% of each transfer ($5 minimum) applies

See rates and fees. Terms apply.

Who’s this for? The Citi® Double Cash Card is a straightforward rewards card that continues to offer one of the best flat-rate cash-back programs since it launched in 2014. Cardholders earn 2% cash back on all purchases — 1% when you make a purchase and an additional 1% when you pay your credit card bill.

There is no limit to the amount of cash back you can earn and you don’t have to worry about activating bonus categories. Cashback can be redeemed for a statement credit or direct deposit.

This card is also a good choice for debt consolidation as it offers a useful introductory APR offer on balance transfers.

Automatically earn unlimited 1.5x Miles on every dollar of every purchase.

Discover will match all the Miles earned for all new cardmembers at the end of your first year.

0% Intro APR for 15 months on purchases.

17.24% to 28.24% Variable

3% intro balance transfer fee, up to 5% fee on future balance transfers (see terms)*

*See rates and fees, terms apply.

Who’s this for? The Discover it® Miles card comes with a generous rewards program — all for zero annual fee — that makes it a standout among travel cards.

The Discover it Miles card offers users unlimited 1.5X miles for every dollar spent on all purchases. But for higher spenders, Discover offers a welcome bonus that’s hard to beat: It will do a mile-for-mile match of all miles earned the first year (for new card members in their first year only). If you rack up 35,000 miles within the first 12 months, Discover will match you with 35,000 miles. That’s a total of 70,000 miles or $700 toward travel.

With this card, there are no blackout dates when you pay for travel purchases using your card. And, you can easily redeem miles as a statement credit for travel, restaurant or gas station purchases, as well as a deposit to your bank account. The best part is that miles earned never expire — even if your account is closed.

0% for 21 months on balance transfers; 0% for 12 months on purchases

There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

Who’s this for? The Citi Simplicity® Card offers one of the longest balance transfer intro periods at 0% for 21 months from the date of the first transfer (after, 18.49% – 29.24% variable APR). Balance transfers must be completed within four months of account opening. This is nearly two years to pay off debt, which can be helpful if you have a large balance or if your cash flow doesn’t allow you to pay off the debt within the 6-, 12- or 15-month time periods of other balance transfer cards.

This card has no annual fee and comes with an introductory balance transfer fee: either 3% ($5 minimum) for transfers completed within the first 4 months of account opening, then up to 5% ($5 minimum). This can be worthwhile if you’re paying high-interest charges.

New cardholders have four months to complete their balance transfer (longer than the typical 60 to 90 days). While you have more time to complete a transfer, the intro APR period starts at account opening — so try to make the transfer as soon as possible to get the most benefit of the interest-free period.

This card also never charges late fees (though we always recommend you pay your balance on time and in full). There isn’t a welcome bonus or a rewards program.

3X points on gas and grocery purchases and 1.5X points on all other purchases

Earn 10,000 points when you spend $1,500 within the first 90 days

N/A for purchases and balance transfers

13.74% to 18.00% variable on purchases; 13.74% to 17.99% on balance transfers.

Rewards totals incorporate the points earned from the welcome bonus

Who’s this for? The Titanium Rewards Visa® Signature Card from Andrews Federal Credit Union stands out for offering low interest rates, a strong rewards program and no foreign transaction fees — all at no annual fee.

This card offers a variable APR of 13.74% to 18.00% on purchases. If you carry a balance, you can benefit from low interest charges compared to other cards that have high interest rates. Balance transfers do incur a fee of $10.00 or 2.00% of the amount of each cash advance, whichever is greater.

Beyond interest rates, the Visa® Titanium Signature Rewards Card offers a generous rewards program: Earn 3X points on gas and grocery purchases and 1.5X points on all other purchases. Plus, there’s a welcome bonus of 10,000 points after you spend $1,500 within the first 90 days.

In order to open this card, you need to join Andrews Federal Credit Union, but anyone can join. If you don’t meet the qualification requirements, you can opt to join the American Consumer Council (ACC) for free with the promo code “Andrews.”

Earn 2% cash back at Gas Stations and Restaurants on up to $1,000 in combined purchases each quarter, automatically. Plus earn unlimited 1% cash back on all other purchases.

Discover will match all the cash back you’ve earned at the end of your first year

3% intro balance transfer fee, up to 5% fee on future balance transfers (see terms)*

*See rates and fees, terms apply.

Who’s this for? The Discover it® Secured Credit Card is a well-rounded secured card that offers many benefits that are typically found with unsecured cards. Cardholders can earn cash back, receive a generous welcome bonus, use the card overseas without incurring added fees and more — all for no annual fee.

Cardholders earn a competitive 2% cash back at gas stations and restaurants on up to $1,000 in combined purchases each quarter, then 1%. Plus, you can earn unlimited 1% cash back on all other purchases automatically. The welcome bonus is also unique: For new card members in the first year only, Discover will automatically match all the cash back you’ve earned at the end of your first year. So, if you earn $50 cash back at the end of the first year, Discover will give you an additional $50.

This card requires a minimum $200 security deposit, which is fairly standard for secured credit cards. It stands out from the crowd because it gives users a clear path to upgrading to an unsecured card (and getting their deposit back). Starting at seven months from account opening, Discover will automatically review your credit card account to see if they can transition you to an unsecured line of credit and return your deposit. This takes the guesswork out of wondering when you’ll qualify for an unsecured credit card.

1% cash back on eligible purchases right away and up to 1.5% cash back on eligible purchases after making 12 on-time monthly payments; 2% to 10% cash back at select merchants

18.24% – 32.24% variable

Who’s this for? The Petal 2 “Cash Back, No Fees” Visa Credit Card, issued by WebBank, is easier to get approved for because it takes a different approach to the credit card application process. Instead of judging your creditworthiness solely based on credit history, Petal may ask you to link bank accounts during the application process. Then, WebBank analyzes your bank statements and other data, such as bill payments and earnings, to determine your eligibility.

This is especially beneficial for applicants who may not have any credit history. However, if you do have a credit history, that does factor into the credit decision.

The Petal 2 Visa Credit Card is one of the few cards that charge zero fees*: no annual fee, no late payment fee and no foreign transaction fees. And it stands out for consumers trying to build credit because there’s no security deposit required.

It also offers a rewards program with 1% cash back on eligible purchases right away, which can increase up to 1.5% cash back after you make 12 on-time monthly payments. This is not only a nice perk, but a great way to encourage responsible behavior. Cardholders also earn 2% to 10% cash back from select merchants.

Earn 5% cash back on everyday purchases at different places you shop each quarter like grocery stores, restaurants, gas stations, and more, up to the quarterly maximum when you activate. Plus, earn unlimited 1% cash back on all other purchases-automatically.

Discover will match all the cash back earned for all new cardmembers at the end of your first year

0% for 6 months on purchases

18.24% – 27.24% Variable

3% intro balance transfer fee, up to 5% fee on future balance transfers (see terms)*

*See rates and fees, terms apply.

Who’s this for? The Discover it® Student Cash Back is a well-rounded card that offers college students enrolled in a two- or four-year college the chance to build credit while earning rewards. You must be over 18 and a U.S. citizen to apply.

Upon activation, cardholders can earn 5% cash back on rotating categories up to a $1,500 maximum each quarter (then 1%). All other purchases earn unlimited 1% cash back automatically.

There is also an introductory APR offer which can be perfect for financing dorm room essentials or textbooks. After you graduate, your Discover it student credit card becomes a regular credit card.

Earn 5X total points on flights and 10X total points on hotels and car rentals when you purchase travel through Chase Travel℠ immediately after the first $300 is spent on travel purchases annually. Earn 3X points on other travel and dining & 1 point per $1 spent on all other purchases plus, 10X points on Lyft rides through March 2025

Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That’s $900 toward travel when you redeem through Chase Travel℠.

Rewards totals incorporate the points earned from the welcome bonus

Who’s this for? The Chase Sapphire Reserve® is geared toward foodies and frequent travelers looking for luxurious perks, such as free airport lounge access and complimentary hotel room upgrades. Cardholders earn a competitive 3X points on dining and travel worldwide. Based on CNBC Select’s calculations, we found the average American using this card could earn an estimated $165 per year in rewards for dining purchases alone (assuming you redeem rewards for travel via Chase Ultimate Rewards®, receiving 50% more value).

The value of Chase rewards points varies depending on how you use them. If you redeem points for cash and gift cards, each point is worth $.01, which means that 100 points equals $1 in redemption value. (See more on how the value of points is calculated.)

This card has a unique benefit where all points are worth 50% more when redeemed for travel via Chase Ultimate Rewards®. For example, 60,000 points are worth $900 redeemed toward airfare, hotels, car rentals and cruises when you redeem through Chase Ultimate Rewards®. This perk is a great way to get the most value for your rewards.

While this card has a robust travel rewards program, it also comes with a steep $550 annual fee. All the card’s added credits and benefits provided by Chase can help offset the annual cost. The $300 annual travel credit effectively reduces the annual fee to $150. Cardholders can take advantage of a Priority Pass™ Select membership that has a value of about $429. They also get a Global Entry or TSA PreCheck application fee credit of up to $100 every four years.

5X points on gas purchases at the pump and electrical vehicle charging stations, 3X points on supermarket purchases, 1X point on all other purchases

15,000 points when you spend $1,500 in the first 3 months from account opening

0% introductory APR for 12 months on balance transfers made in the first 90 days after account opening.*

17.99% variable on purchases; 17.99% non-variable on balance transfers

Rewards totals incorporate the points earned from the welcome bonus.

*0% introductory APR for 12 months on balance transfers made in the first 90 days after account opening. After that, the APR for the unpaid balance and any new balance transfers will be a non-variable rate of 17.99%. 3% balance transfer fee per transaction. Subject to credit approval. If you take advantage of this balance transfer, you will immediately be charged interest on all purchases made with your credit card unless you pay the entire account balance, including balance transfers, in full each month by the payment due date.

Who’s this for? Among the cards we analyzed, the PenFed Platinum Rewards Visa Signature® Card currently offers the highest rewards rate at gas stations with 5X points per dollar spent for gas purchases at the pump.

This card has no annual fee, so road warriors can maximize their savings. In addition to earning high rewards at gas stations, cardholders also benefit from unlimited 3X points for supermarket purchases.

PenFed is a credit union, so membership is required to open the PenFed Platinum Rewards Visa Signature® Card. Anyone can join by completing a few extra steps: You need to apply, open a savings account with a $5 deposit and maintain a $5 account balance.

6% cash back at U.S. supermarkets on up to $6,000 per year in purchases (then 1%), 6% cash back on select U.S. streaming subscriptions, 3% cash back at U.S. gas stations, 3% cash back on transit (including taxis/rideshare, parking, tolls, trains, buses and more) and 1% cash back on other purchases. Cash Back is received in the form of Reward Dollars that can be redeemed as a statement credit or at Amazon.com checkout.

Earn a $250 statement credit after you spend $3,000 in purchases on your new card within the first 6 months.

$0 intro annual fee for the first year, then $95.

0% for 12 months on purchases from the date of account opening

19.24% – 29.99% variable. Variable APRs will not exceed 29.99%.

Either $5 or 3% of the amount of each transfer, whichever is greater.

See rates and fees, terms apply.

Rewards totals incorporate the cash back earned from the welcome bonus

Who’s this for? Frequent grocery shoppers will be happy to learn the Blue Cash Preferred® Card from American Express offers the highest cash-back rate at U.S. supermarkets at 6% (on up to $6,000 per year in purchases, then 1%). The average American can earn $310 in cash back each year when they do their shopping at qualifying supermarkets.

If you want to maximize cash back on groceries, this card is for you. In addition to high grocery rewards, there’s an unlimited 6% cash back on select streaming subscriptions, unlimited 3% cash back at U.S. gas stations, unlimited 3% cash back on transit including taxis/rideshare, parking, tolls, trains, buses and more and 1% cash back on all other purchases.

Cardmembers can also take advantage of Amex Offers, where users earn a statement credit or additional cash back at select retailers. For example, a recent offer gave you $25 back each month (up to three times), if you spent $70 or more a month on Sun Basket meal kit delivery. These limited-time offers are location-based and additional terms apply.

This card has $0 intro annual fee for the first year (then $95), but it can be offset by the cash back you earn and discounts you can get through the Amex Offers. (See rates and fees)

Earn Bilt Points when you make 5 transactions that post each statement period – up to 1x points on rent payments without the transaction fee (up to 100,000 points each calendar year), 3x points on dining, 2x points on travel, and 1x points on other purchases.

Introductory fee of either $5 or 3% of the amount of each balance transfer, whichever is greater, for 120 days from account opening. After that, up to 5% for each balance transfer ($5 minimum).

See rates/fees and rewards/benefits; terms apply.

Who’s this for? The Bilt Mastercard® is the only credit card that lets you earn travel rewards on rent payments with no fees.

So long as you make at least five card transactions per statement period, you’ll earn 3X points on dining, 2X points on travel 1X points on rent (on up to $50,000 in rent payments every year) and everything else. Thanks to a new partnership with Lyft, cardholders can now also earn up to 5X points on their rideshares.

Thanks to the BiltProtect feature, cardholders are protected from using up their entire credit limit or risk going into debt by charging their rent to their card every month. Other benefits include cell phone protection; Purchase Assurance Plus, which covers your purchases for 90 days; exclusive discounts with brands like Lyft, DoorDash and ShopRunner; and access to the Mastercard Luxury Hotels & Resorts portfolio, which offers amenities like upgrades, free breakfast and property credits.

Bilt Rewards points are extremely flexible. They can be redeemed for travel either by transferring them to airline and hotel partners or by booking through the Bilt Travel Portal at a fixed rate of 1.25 cents per point. Other redemption options include using them to shop online, book fitness classes, pay rent and even make a down payment on a home.

4% cash back on dining and entertainment, 4% on eligible streaming services, 3% at grocery stores and 1% on all other purchases

Earn a one-time $300 cash bonus once you spend $3,000 on purchases within the first three months from account opening

3% for promotional APR offers; none for balances transferred at regular APR

Who’s this for? Sports fans, movie buffs and adventure seekers will all find a common reason to like the Capital One Savor Cash Rewards Credit Card: unlimited 4% cash back on entertainment purchases. Compared to other rewards cards, this is the highest unlimited rewards rate on entertainment spending, whether you’re buying movie tickets, taking a family trip to the zoo or spending the evening bowling with friends.

Cardholders can also benefit from exclusive access to entertainment events, such as the iHeartRadio Music Festival and the Capital One JamFest.

Beyond entertainment perks, there’s also 10% cash back on Uber rides, 4% cash back on dining and popular streaming services, 3% at grocery stores and 1% on all other purchases. Plus, you can enjoy an Uber One membership through Nov. 14, 2024 and foodie-centric perks through Capital One Dining.

This card does come with a $95 annual fee, but can be offset by the cash back you earn.

5 Miles per dollar on hotel and rental cars booked through Capital One Travel, 2X miles per dollar on every other purchase

Earn 75,000 bonus miles once you spend $4,000 on purchases within 3 months from account opening

N/A for purchases and balance transfers

19.99% – 29.99% (Variable)

$0 at the Transfer APR, 4% of the amount of each transferred balance that posts to your account at a promotional APR that Capital One may offer to you

Who’s this for? The Capital One Venture Rewards Credit Card offers excellent rewards rates: Earn 5X miles on hotel and rental cars booked through Capital One Travel and 2X miles per dollar spent on all other spending. While Venture does come with a $95 annual fee, that’s low compared to some other rewards cards, with some annual fees of up to $550.

In addition to rewards, every four years cardholders receive a credit for a Global Entry or TSA PreCheck application, up to $100. Cardholders now also get two free visits to Capital One airport lounges per year. If you travel often, these are great perks that can save you time and money.

This card has no foreign transaction fees and comes with a bunch of additional travel perks, such as 24-hour travel assistance services and an auto rental collision damage waiver.

*Terms, conditions and exclusions apply. Refer to your Guide to Benefits for more details.

Earn 5X Membership Rewards® Points for flights booked directly with airlines or with American Express Travel up to $500,000 on these purchases per calendar year, 5X Membership Rewards® Points on prepaid hotels booked with American Express Travel, 1X points on all other eligible purchases

Earn 80,000 Membership Rewards® Points after you spend $8,000 on purchases on your new Card in your first 6 months of Card Membership. Apply and select your preferred metal Card design: classic Platinum Card®, Platinum x Kehinde Wiley, or Platinum x Julie Mehretu.

Who’s this for? The Platinum Card® from American Express is for those who want a luxury card with a lengthy list of benefits. Although best known for its travel perks, this card also offers a number of everyday benefits, including digital entertainment, shopping and wellness credits (enrollment required), so you don’t need to be a road warrior to benefit from it.

To start, cardholders earn a respectable 5X Membership Rewards® points on flights booked directly with airlines or with American Express Travel (on up to $500,000 per calendar year), 5X points on prepaid hotels booked with American Express Travel and 1X points on all other purchases.

In addition, cardholders can enjoy over a dozen premium travel and lifestyle benefits, including:

Its $695 annual fee (see rates and fees) is higher than any other card on this list, but you can definitely come out ahead if you take full advantage of the benefits. And that’s before factoring in the card’s welcome offer, which many rewards experts value at $2,000. (See more on how the value of points is calculated.)

10 Miles on hotels per dollar and rental cars, 5 Miles per dollar on flights when booked via Capital One Travel; unlimited 2X miles on all other eligible purchases

Earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening

19.99% – 29.99% (Variable)

$0 at the Transfer APR, 4% of the amount of each transferred balance that posts to your account at a promotional APR that Capital One may offer to you

See rates and fees, terms apply.

Who’s this for? If you value simplicity and want one, strong standalone credit card, it doesn’t get much better than the Capital One Venture X Rewards Credit Card. It offers a straightforward rewards structure, a myriad of valuable benefits and a lower annual fee than other high-end cards with similar features.

Cardholders earn 2X miles on everyday purchases, plus 5X miles on flights and a whopping 10X miles on hotels and cars booked through Capital One Travel. These miles can be transferred to airline and hotel partners, such as Accor Live Limitless, Air Canada Aeroplan and Etihad Guest. You can also redeem rewards toward travel through Capital One Travel, cash-back, gift cards, experiences and more.

On top of that, the Venture X card offers up to $100 in statement credit for either Global Entry or TSA PreCheck®, complimentary cell phone insurance, special perks on hotel stays book through the Premier Collection and access to Capital One Lounges as well as the extensive network of Priority Pass and Plaza Premium airport lounges worldwide. Every year, cardholders receive up to $300 back in statement credits each year for bookings made through Capital One Travel and a 10,000-mile bonus on each account anniversary (worth at least $100 for travel), making it easy to recoup the $395 the annual fee.

*Terms, conditions and exclusions apply. Refer to your Guide to Benefits for more details.

Having a credit card is an important piece of your financial profile, but with so many options available, it can be hard to find the best one for your needs. Here are some common questions to ask yourself so you can decide what’s the best credit card for you.

There are hundreds of rewards credit cards out there, where you can earn cash back, points or miles on every purchase you make.

Rewards credit cards come in all shapes and sizes. If you want to maximize rewards in specific categories, check out cards offering bonus rewards on gas, groceries, restaurants, entertainment, travel and more. Or keep it simple and opt for a flat-rate cash-back card.

If you’re carrying a balance on a high-interest credit card, consider transferring it to a balance transfer credit card offering no interest for up to 21 months. There are even cards with no balance transfer fees.

Experts agree the sooner you build credit, the better. Credit cards are a great way to do that. Check out secured cards for credit newbies or other cards for building or rebuilding credit.

A credit card with no foreign transaction fees is essential to save you the typical 3% fee per purchase made outside the U.S. Also, it can be a good idea to consider cards that waive Global Entry or TSA PreCheck application fees.

Find the best credit card for you by reviewing offers in our credit card marketplace or get personalized offers via CardMatch™.

When you apply for a credit card, the bank or lender will review your credit report from one or more of the three major credit bureaus. It will also typically check your FICO credit score, the top credit cards usually require a very good or excellent credit score.

This is how FICO credit scores are classified according to myFICO:

Building and maintaining a healthy credit score helps your personal finances in all sorts of ways outside of increasing your chances of getting approved for a great sign-up bonus. Your FICO score is calculated based on the following factors and each is weighted differently:

Many people have multiple credit cards, and there are benefits to this. It can help increase your credit score by giving you more available credit and therefore a better credit utilization ratio.

At its most basic, having access to more credit can help you finance more purchases if you don’t have enough cash to cover everything up front.

You can also earn more rewards by optimizing which card you use for certain spending categories. For instance, you may make all your dining purchases with a card that earns bonus rewards in that category, but another card with a bonus multiplier for grocery purchases.

Ultimately, it’s up to you to decide how many credit cards you need. Make sure to evaluate your spending habits and research what card would be best for you.

Applying for a credit card is easy, and you’ll often get an instant decision on whether you’re approved or denied. To apply for a credit card, you’ll generally need to provide the following:

Secured credit cards are generally the easiest credit cards to be approved for. They are similar to traditional cards (they extend credit, can incur interest charges and in some cases can even earn rewards) but require you to put down a security deposit to access a line of credit. The amount you deposit usually becomes your credit limit.

There are four major credit card issuers: American Express, Discover, Mastercard and Visa.

Visa and Mastercard are the most widely accepted credit card networks globally. That said, American Express and Discover still have 99% acceptance rates among U.S. merchants who take credit cards and are increasing their international footprints.

When it comes to credit cards, most billing cycles are one month or 28 to 31 days. After your billing cycle ends, you typically have what is known as a grace period where you can pay off your full balance without incurring any interest charges. However, if you pay off your card balance before the billing cycle ends, it will help to keep your credit utilization down, which boosts your credit score.

Keep in mind that the grace period may not apply to all charges. Balance transfers and cash advances are usually charged interest starting on the transaction date.

Having a separate credit card for your small business or side hustle is important so you can keep your personal and business activities separate. Business credit cards come in all shapes and sizes, there are business cards that offer cash-back rewards, travel rewards and everything in between.

The right business credit card for you should offer bonus rewards that align with your business spending. To keep it simple, you can start your business credit card search at the bank where you currently have your business bank accounts. If you bank with Wells Fargo, Bank of America or Chase, then it may be easiest to have all of your accounts with one institution.

Many of the banks that offer the best consumer cards also have top-notch business cards. For example, Chase has the Ink Business line of small business cards, which includes the Ink Business Unlimited® Credit Card and the Ink Business Cash® Credit Card. Both cards have no annual fee, hefty sign-up bonuses and generous bonus spending categories.

At CNBC Select, our mission is to provide our readers with high-quality service journalism and comprehensive consumer advice so they can make informed decisions with their money. Every credit card review is based on rigorous reporting by our team of expert writers and editors with extensive knowledge of credit card products. While CNBC Select earns a commission from affiliate partners on many offers and links, we create all our content without input from our commercial team or any outside third parties, and we pride ourselves on our journalistic standards and ethics. See our methodology for more information on how we choose the best credit cards.