[ad_1]

Why investors are no longer rewarding earnings beats, according to Goldman Sachs

[ad_2]

[ad_1]

Why investors are no longer rewarding earnings beats, according to Goldman Sachs

[ad_2]

[ad_1]

Broadcom Gets a Stock-Target Increase. Analyst Thinks Anthropic Is a Big, New Customer.

[ad_2]

[ad_1]

As Intel Corp.’s stock plunged to its biggest one-day drop in about three and a half years, analysts had some harsh words for the chip maker.

“How many times can you push the reset button?” Bernstein’s Stacy Rasgon asked in a note to clients.

While he thought many investors were bracing for the company to miss on its first-quarter forecast, the outlook came in “extremely weak and clearly worse than feared.” Intel

INTC,

expects $12.7 billion in revenue at the midpoint, while analysts had been looking for $14.3 billion.

See more: Intel seen struggling to ‘find its footing’ as guidance miss sends stock tanking

“After yet another major reset this story probably just shifted to 2026 at the earliest for the bulls, and there is a lot of meat for the bears to sink their teeth into in the meantime,” Rasgon wrote, while sticking with his market-perform rating and $42 target price.

Baird’s Tristan Gerra highlighted challenges for Intel’s data-center and artificial-intelligence unit, which is “on track for a third consecutive year of revenue declines,” while his own revenue forecast implies a 14-year low.

Gaudi, the company’s accelerator chip for artificial-intelligence applications, “does not seem enough to lift [data-center] revenue, while gross margin will be impacted by higher depreciation inclusive of an expected U.S. Chip Act credit,” Gerra continued.

He also expressed some concerns about the company’s broader road ahead.

“Can top-line growth in future years be sufficient to fund continued node migration?” Gerra said. “Many hurdles remain, notably ramping units from this year’s small base (small baseline for Intel 4 makes it more challenging to yield at the next node), while [the Intel Foundry Service] revenue ramp entirely depends on future node execution including yield and performance.”

Gerra has a neutral rating and $40 target price on Intel’s stock.

Shares fell 11.9% in Friday trading, making for their worst single-day percentage decline since July 24, 2020, when they fell 16.2%, according to Dow Jones Market Data.

Needham’s N. Quinn Bolton, meanwhile, downgraded the stock to hold from buy in the wake of Thursday afternoon’s report, calling the earnings reset “unexpected.”

“In addition to an overall worsening risk-reward, Intel’s core [data-center] business is challenged by a shift to accelerated computing architectures and direct competition from AMD and ARM,” he wrote. “We expect AI to remain the spending priority in the data center for the next several quarters. To that end, dollars will continue moving away from Intel’s core competency.”

Read: Missed the boat on AMD’s stock surge? Why this analyst says you’re not too late.

Rosenblatt’s Hans Mosesmann took a similar view as he argued that Intel’s sales outlook is “contrary to the uber bullish messaging to the Street and is consistent with share losses to AMD, a lack of any perceivable AI growth vector that moves any dial, and points to another, yes another, transitional year.”

Artificial intelligence “seems like everywhere except at Intel,” he continued, noting that his stance on the stock “has not changed for many years.” Mosesmann continues to rate it at sell.

Opinion: Intel’s stock plunge shows that Wall Street still hasn’t learned its lesson on AI hype

Raymond James analyst Srini Pajjuri, however, was more upbeat about Intel’s ability to capitalize on AI. “While Intel won’t likely get much credit for AI in the near term, we are encouraged by the growing pipeline for Gaudi accelerators ($2b+) and expect meaningful revenue contribution” in the second half of 2024, he wrote, while sticking with his outperform call but cutting his target price to $52 from $54.

[ad_2]

Source link

[ad_1]

Spirit Airlines stock was falling again Thursday as the ultra-low-cost carrier’s predicament worsened.

Continue reading this article with a Barron’s subscription.

View Options

[ad_1]

Alaska Airlines, United Airlines and Turkish Airlines have all grounded their Boeing 737 Max 9 airplanes after part of one such jet tore away during an Alaska Airlines flight on Friday. But despite the potential safety risks for travelers and further damage to Boeing’s

BA,

reputation, some Wall Street analysts, for now, have downplayed the financial impact for the jet maker.

In part, they pointed to the company’s status as one of two major players in aircraft production — the other being Airbus

EADSY,

They also cited a tighter supply of available aircraft and limited near-term impact, at least while investigators try to figure out the cause of the incident.

Those airlines and others took the action over the weekend after a panel on a jet blew out about 10 minutes into Alaska Airlines Flight 1282 at an altitude of about 16,000 feet.

No one died in the incident. But the Federal Aviation Administration ordered the temporary grounding of certain Boeing 737 Max 9 aircraft. The order covered 171 planes.

Shares of Boeing fell 8.2% as the stock weighed on the Dow Jones Industrial Average

DJIA.

Still, some Wall Street analysts on Monday said to buy the stock anyway. They said the latest difficulties with the aircraft — which follow the 2019 grounding of Max jets by many nations following two fatal crashes — were unlikely to have a big near-term financial impact.

BofA analysts, in a research note dated Sunday, said that “at this point in time, due to the duopoly nature of the industry, we do not see this impacting orders for any of the 737 MAX variants. However, if the hits to the program do keep coming … at some point, the flying public may lose confidence in the 737 MAX which could ultimately impact sales.”

The analysts said it wasn’t clear yet whether the blowout on Friday was due to an assembly mistake at Boeing, an improper installation from fuselage maker Spirit AeroSystems or oversight issues elsewhere. But they noted that the aircraft was relatively new, having been delivered on Oct. 31. And they said that “some scrutiny must be saved for regulators as well, as the FAA is ultimately responsible for certificating these aircraft before delivery.”

Spirit AeroSystems’ stock

SPR,

was down 11%.

Analysts at William Blair also said they didn’t expect a big hit to Boeing’s financials.

“While the Alaska Airlines door plug accident was terrifying, we do not believe that it will have a major financial impact, unless another incident occurs after the aircraft returns to service,” they said in a note on Monday.

Analysts there estimated that over the past two months, the Max 9 made up less than one-fifth of Boeing’s total deliveries. They said those deliveries would only be “modestly impacted over the first quarter as it could take some time to determine the cause.”

Of the 23 analyst ratings on Boeing’s stock tracked by FactSet, 18 are buy ratings or the equivalent.

Read more: How Boeing’s latest 737 Max problem is hurting the Dow

However, Morgan Stanley analyst Ravi Shanker said the 737 Max 9 issues will likely disrupt first-quarter results for United Airlines

UAL,

and Alaska Air

ALK,

“This will hopefully be a situation resolved in days/weeks rather than months, but it will also serve as a reminder of how fragile airline capacity can be despite the overhang of capacity,” Shanker said in a Monday research note.

United Airlines’ stock rose 2.4% on Monday, while Alaska Air’s dipped by 0.3%.

Along with United Airlines, Alaska Airlines and Turkish Airlines, Copa Airlines and Aeromexico grounded about 40 Boeing 737 Max 9 planes, according to reports.

According to Deutsche Bank analysts, the affected fleet accounts for 16.1% of Alaska Airlines flights and 6.6% of United flights, although United has more 737 Max 9 aircraft than Alaska.

Other airlines with the plane in their fleet include Jet Airways of India with one plane, Jin Air of Korea with three, KLM Royal Dutch Airlines

KLMR,

with five and Korean Air Lines

003490,

with nine, according to Planespotter.net.

European regulators also grounded the 737 Max 9 for inspection.

Some major airlines do not have any 737 Max 9s in their fleets, including American Airlines

AAL,

Southwest Airlines

LUV,

and Air Canada

AC,

according to reports.

Also read: Shares in Boeing slump, supplier Spirit AeroSystems tanks, after panel blows out

[ad_2]

[ad_1]

Shares of Apple Inc. are starting 2024 with a selloff, after Barclays analyst Tim Long said it was “time for a breather,” citing weak hardware sales as iPhone 15 demand disappoints.

“We are still picking up weakness on iPhone volumes and mix, as well as a lack of bounce-back in Macs, iPads and wearables,” Long wrote in a note to clients. “The biggest takeaway from the latest checks is incrementally worse [iPhone] 15 data points out of China, together with developed markets remaining soft.”

He cut his rating on the stock

AAPL,

to underweight from neutral, and trimmed his price target to $160 from $161. The new target implies about 17% downside from Friday’s closing price of $192.53.

The stock slumped 1.8% in premarket trading Tuesday, putting it on track to open at a seven-week low.

Long said iPhone 15 sales have been “lackluster” and believes Phone 16 sales will be the same, as he expects other hardware categories to remain weak. He said it’s time for investors to take a “breather” on the stock, as he doesn’t think it can keep rallying in the face of downbeat demand data, like it did in 2023.

“We expect reversion after a year when most quarters were missed and the stock outperformed,” Long wrote.

He expects Apple to report “in-line” fiscal first-quarter results, which runs through December, but he trimmed his second-quarter to further below consensus expectations.

He now expects earnings per share and revenue for the quarter through March to be down in the low-single-digit percentage range, while the FactSet consensus calls for EPS to be up 2.6% at $1.57 and revenue to rise 1.1% to $95.8 billion.

Apple’s stock surged 48.2% in 2023, or almost double the S&P 500 index’s

SPX

gain of 24.2%, even as revenue for each quarter of fiscal 2023 through September was below that of a year ago.

Long is now one of just four of the 44 analysts surveyed by FactSet who are bearish on Apple’s stock, while 27 (61%) are bullish and 13 are neutral. His $160 price target is 19.2% below the average target of $197.92.

[ad_2]

[ad_1]

U.S. stocks capped off a wild 2023 with a two-month sprint that has carried the Dow to record highs and the S&P 500 index to within a whisker of a similar milestone.

But after such a powerful advance, some portfolio managers and strategists are concerned that the market could suffer its own post-New Year’s Eve hangover once the calendar turns to January 2024.

Instead of providing a tailwind for the market, several who spoke with MarketWatch worried that the “January effect” might work in reverse as investors scramble to lock in gains after the S&P 500 rose 24% in 2023, according to FactSet data.

“Any time you have a big burst like that, I think you’re vulnerable to some profit-taking,” said James St. Aubin, chief investment strategist at Sierra Investment Management, during an interview with MarketWatch. “It wouldn’t surprise anybody to see the market cool off a bit after a strong run.”

From high valuations, to bullish sentiment indicators, to economic data, to geopolitics and beyond, here are a few things that could trip up the market in January.

A technical gauge that’s widely followed by Wall Street portfolio managers and technical analysts has been screaming that U.S. stocks are overbought for a month.

The 14-day relative strength index on the S&P 500, a momentum indicator that’s supposed to help put the magnitude of the index’s latest moves into context, climbed as high as 82.4 on Dec. 19, its highest since 2020, according to FactSet data.

Although the RSI has since pulled back, it continues to hover around 70, seen by analysts as the threshold for when something can be considered “overbought.”

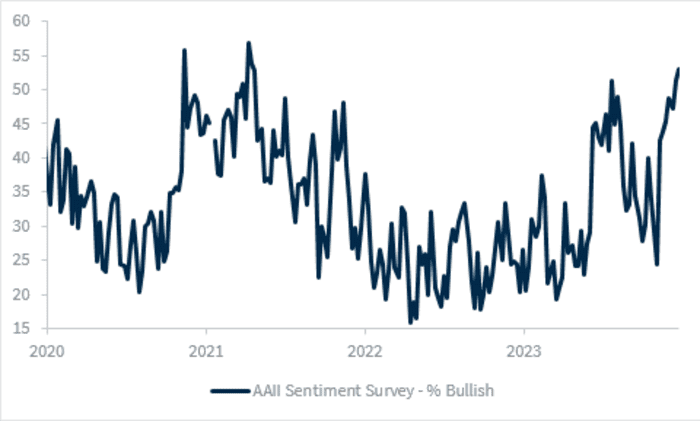

In the span of just two months, investors have gone from incredibly bearish to incredibly bullish, according to the American Association of Individual Investors’ weekly sentiment survey.

That should give investors pause, since the gauge is seen as a reliable counter-indicator. When sentiment becomes stretched in either direction, it can signal that the market is about to turn. Investors say that is what happened back in July, and also in October after the S&P 500 touched its 2022 bear-market nadir.

According to the AAII survey published ahead of the Christmas holiday, nearly 53% of respondents said they were bullish, the highest since April 2021. That number came down a bit this week, but it remains high relative to levels from October.

Wall Street’s favorite “fear gauge” is giving the all-clear. To some, that’s reason enough to worry.

The Cboe Volatility Index

VIX,

better known as the Vix, measures implied volatility, or how volatile traders’ expect the S&P 500 to be over the coming month based on trading activity in options contracts tied to the index.

In December, the Vix dropped below 12 for the first time since before the advent of the COVID-19 pandemic.

Nancy Tengler, CEO and CIO of Laffer Tengler Investments, said in emailed commentary that she is keeping a close eye on the Vix. Once volatility starts to climb, investors should consider taking some chips off the table.

Some investors are already anxious about the next U.S. inflation report, due Jan. 11.

The Cleveland Fed’s inflation nowcast has core CPI rising more than 0.3% in December. If this proves accurate, it would be the hottest inflation reading since May.

And even if core inflation comes in slightly cooler, stocks might not greet it with the same enthusiasm they have shown in the past.

“U.S. CPI for December will hopefully continue to show a disinflationary trend, although the question is: can we keep rallying on this same dynamic?” said Larry Adam, chief investment officer at Raymond James, in emailed comments.

For three straight quarters beginning with the final three months of 2022, the largest U.S. companies saw their earnings shrink on a year-over-year basis.

This “earnings recession” finally came to an end in the third quarter, but the conundrum that investors now face is whether companies can manage to satisfy Wall Street’s lofty expectations for 2024.

The artificial-intelligence software boom and the fact that the U.S. economy avoided a recession in 2023 has helped boost analysts’ confidence about earnings, strategists said.

According to the bottom-up consensus estimate from FactSet, analysts expect S&P 500 aggregate earnings to increase by 11.7% for the calendar year 2024.

“Markets have been baking in this 11.7% earnings growth figure for a while now. That’s a lot of optimism,” Goldman said during an interview with MarketWatch.

To be sure, this list is hardly comprehensive.

Politics and geopolitics also came up a lot in discussions with analysts. Investing professionals cited Taiwan’s upcoming presidential election, another looming federal debt-ceiling showdown in the U.S., the beginning of the 2024 Republican presidential primaries, the ongoing conflicts in Gaza and Ukraine, and more as potential threats to market calm.

Some expressed concern that the Treasury could spark a selloff in bonds and stocks with its next quarterly refunding announcement in early 2024.

But in the view of Cetera’s Goldman, a dynamic that Wall Street traders call it “buy the rumor, sell the news” could represent a bigger threat.

The thinking works like this: investors have already front-run aggressive Federal Reserve interest rate cuts. So, if the Fed delivers, the rush to take profits could drive stocks lower instead of propelling the main U.S. indexes to new highs. Put another way, many strategists believe investors have already priced in pretty aggressive Fed rate cuts.

So unless the central bank finds a way to deliver something even greater than what Wall Street is expecting, the main U.S. equity indexes could struggle to continue their advance.

“Markets are already buying the rumor that we’re going to have a better 2024, that the Fed is going to cut rates, that breadth is going to widen,” Goldman said.

“Maybe we’re already seeing that priced in.”

[ad_2]

[ad_1]

Nike beat expectations for second-quarter profit and announced a $2 billion cost-cutting plan, as it sees sales softening for the second half of its fiscal year.

Continue reading this article with a Barron’s subscription.

View Options

[ad_1]

When it comes to the baby boomers’ run of investing luck, timing has been on their side.

Decades of stellar stock-market returns produced by a series of bull markets that began in 1982 coincided with boomers’ prime working years and made their nest eggs grow.

Copyright ©2023 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

[ad_2]

[ad_1]

While Advanced Micro Devices Inc. shares didn’t enjoy a Wednesday bump during the company’s artificial-intelligence event, they were rallying sharply Thursday as analysts reflected on the chip maker’s presentation.

Chief Executive Lisa Su and her team “put together one of the most impressive new product event/launches by our reckoning in the last decade, perhaps ever,” Rosenblatt Securities analyst Hans Mosesmann wrote in a note to clients.

The launch of AMD’s

AMD,

MI300X AI/graphics-processing-unit accelerator “was not just a speeds and feeds geek fest (it was that for sure, with AMD claiming superiority in AI inferencing), but an industry movement coalescing around the concept of ‘open’ sourced technologies are preferred (demanded really), to address the insanely fast/accelerating life-changing thing that AI has become,” Mosesmann continued.

Opinion: AMD’s new products represent the first real threat to Nvidia’s AI dominance

He was also impressed by the company’s talk of its software platform ROCm, which he thinks is catching up to Nvidia Corp.’s

NVDA,

CUDA.

“Of course, Nvidia is not going away, and we are quite sure will remain the dominant AI player for years to come but AMD we feel made the case yesterday that they will be an important AI innovator on a secular basis,” Mosesmann noted, as he kept his outperform rating and $200 target price on the stock.

AMD shares were up 6% in Thursday morning trading.

Baird’s Tristan Gerra was also impressed.

“Rapidly unfolding hyperscaler engagements, highly competitive AI architecture specs, along with accelerated new product roadmap, bode well for share gains and continued acceleration in AI-related revenue for AMD beyond 2024, while faster-than-expected rate of adoption so far could potentially drive upside in the AI revenue outlook for 2024, in our view,” he wrote.

Gerra also sees the potential for “high-volume deployments,” thanks to the “significant software milestones” AMD is showing. He rates the stock at outperform with a $125 target price.

TD Cowen’s Matthew Ramsay said that AMD’s event reinforced his belief that the company “is well positioned to meaningfully participate” in the large total addressable market for AI accelerators.

The company called out Microsoft Corp.

MSFT,

Meta Platforms Inc.

META,

and Oracle Corp.

ORCL,

as customers, announcements that were “strong” but not “surprising,” in Ramsay’s view.

“We remain encouraged that AMD is making an impressive case (and is getting customer support) to provide adaptive computing solutions for both training and inference in increasingly large [generative-AI] infrastructure builds,” he wrote. “We believe this signifies a strong AI strategy of delivering a broad portfolio of [central processing unit], GPU, and [field-programmable gate array] assets, with open software that enables easily deployed AI workloads while leveraging the company’s existing partnerships to accelerate its AI ramps at-scale.”

Ramsay has an outperform rating and $130 target price on AMD shares.

[ad_2]

[ad_1]

MongoDB Inc. easily cleared expectations with its latest results and outlook, but shares of the database company were declining 5% in Tuesday’s extended session.

The database-management company posted a fiscal third-quarter net loss of $29.3 million, or 41 cents a share, compared with a net loss of $84.9 million, or $1.23 a share, in the year-prior quarter. On an adjusted basis, MongoDB

MDB,

posted earnings per share of 96 cents, while analysts were expecting 51 cents a share.

MongoDB’s revenue came in at $433 million, up 30% from a year before, while the FactSet consensus was for $406 million.

“MongoDB has clearly established itself as an indispensable part of the tech stack of any organization focused on building durable competitive differentiation through software development,” Chief Executive Dev Ittycheria said in a release. He noted that the company was having success “in winning new workloads from both new and existing customers across verticals, geographies and customer segments.”

For the fiscal fourth quarter, MongoDB anticipates $429 million to $433 million in revenue, along with 44 cents to 46 cents in adjusted EPS. The FactSet consensus was for $418 million in revenue and 37 cents in adjusted EPS.

[ad_2]

[ad_1]

Zscaler Inc. topped expectations with its results for the latest quarter and its outlook for the ongoing one, but shares of the cybersecurity company were moving lower in Monday’s extended session as Zscaler declined to up its full-year billings forecast.

Calculated billings for the fiscal first quarter came in at $457 million, up from $340 million a year prior, whereas analysts had been looking for $443 million. Despite showing upside in the latest quarter, Zscaler ZS kept its full-year forecast at $2.52 billion to $2.56…

Already a subscriber?

Log In

[ad_2]

[ad_1]

Fisker Inc. shares plunged around 10% in the after-hours session Monday after the electric-vehicle maker widened its quarterly loss and reported sales that missed the mark, underscoring the difficulties of turning a profit in the EV world.

Fisker

FSR,

lost $91 million, or 27 cents a share, in the third quarter, compared with a loss of $149.3 million, or 49 cents a share, in the year-ago period.

Revenue rose to $71.8 million, from $14,000 a year ago and $825,000 in the second quarter.

Analysts polled by FactSet expected Fisker to report a loss of 23 cents a share on sales of $143.1 million.

Fisker kept its guidance for 2023 operating expenses and capital expenditures unchanged, between $565 million and $640 million, but removed language about gross margins.

See also: Tesla’s Cybertruck contract restricts reselling vehicle within the first year

In August, the company said it expected gross margins between 8% and 12% for the year, “provided input costs do not change dramatically.”

The EV maker said the third quarter was its first quarter “with meaningful automotive sales revenue.”

Fisker is often dubbed the “Apple of autos,” and is focused on design and consumer interfaces while contracting out the manufacturing of cars.

The company said it produced 4,725 vehicles and sold 1,097 in the quarter. Deliveries “have accelerated as Fisker begins optimizing last-mile logistics and expanding its delivery infrastructure to achieve further scale effects in Q4 and beyond,” the company said in a statement.

“Over 3,000 vehicles delivered globally to date and hundreds more en route to consumers,” the company said.

On Monday, Fisker said it lowered its Fisker Ocean prices in the U.S. for the first time since it introduced the trim pricing in 2020 and 2021. Fisker also adjusted pricing in Europe and Canada, narrowing the gap between two trims.

Don’t miss: Plug Power’s stock extends losses as investors seek ‘clarity’ about going-concern warning

[ad_2]

[ad_1]

In less than a year, Chevron has gone from being Wall Street’s favorite Big Energy company to a show-me story. Investors who buy the stock now should end up liking what they see.

Chevron stock (ticker: CVX) has fallen 17% in 2023, making it the worst performer by far among the half-dozen global super majors this year. Exxon Mobil (XOM), by comparison, is down just 2% this year, and the Energy Select Sector SPDR exchange-traded fund (XLE) is about flat.

Most of the drop has come during the past few weeks after a disappointing earnings report that included news of a surprise delay in the development of a key oil field in Kazakhstan, while Chevron’s $60 billion deal to buy Hess (HES), an independent energy producer, not only failed to excite investors but was seen as a sign of weakness by some.

Continue reading this article with a Barron’s subscription.

[ad_2]

[ad_1]

JetBlue Airways Corp.’s stock fell 7% in premarket trades on Tuesday after the carrier warned it would post a wider-than-expected fourth-quarter loss, while it missed analyst estimates for its third-quarter loss and revenue.

“While we have been able to offset some of the costs associated with the challenging operational backdrop, the sheer magnitude of the air traffic control and weather-related delays has been staggering,” the carrier said.

JetBlue

JBLU,

said it lost $153 million, or 46 cents a share in the third quarter. In the year-ago quarter, JetBlue reported net income of $57 million, or 18 cents a share.

Adjusted loss in the latest quarter was 39 cents a share, wider than the FactSet consensus estimate for a loss of 25 cents a share.

JetBlue’s revenue fell 8% to $2.35 billion, below the analyst estimate of $2.38 billion.

For the fourth quarter, JetBlue expects to report an adjusted loss of 55 cents to 35 cents a share against an analyst estimate of a loss of 15 cents a share.

Also read: Airline stocks rocked as Israel-Hamas war fuels profit concerns

[ad_2]

[ad_1]

Intel Corp. shares were popping nearly 8% in Thursday’s extended session after the chip maker delivered a rosy forecast, while talking up new customers for its foundry business and traction related to artificial intelligence.

For the fourth quarter, Intel

INTC,

anticipates $14.6 billion to $15.6 billion in revenue, whereas analysts were looking for $14.4 billion. The company is also modeling 44 cents in adjusted earnings per share, while the FactSet consensus was for 33 cents.

“While the industry has seen some wallet share shifts between CPU and accelerators over the last several quarters, as well as some inventory burn in the server market, we see signs of normalization as we enter Q4,” Chief Executive Pat Gelsinger said on the earnings call.

Gelsinger expressed confidence about Intel’s positioning — and the future of central processing units — as AI becomes more dominant in the technology world.

“Training of these large models is interesting, but the deployment of those models, the inferencing use of those models is what we believe is truly spectacular for the future,” he said. “And…some of that will run on the accelerators, but a huge amount of that is going to run, right, on Xeons.”

He also shared that Intel now has three customers for its 18A foundry process technology that have made commitments. The company previously disclosed one customer made prepayments, but Gelsinger added Thursday that Intel has two other customers.

“The other thing that we saw this quarter, which was a little bit unexpected, was this huge surge in interest for AI customers and Intel’s advanced packaging technology,” he said.

Intel is in the midst of a big push to build a foundry business through which it would manufacture chips for other companies, though not all on Wall Street are sold yet on the move.

The company also delivered an upbeat third-quarter report, easily clearing Wall Street’s bar on profit and topping expectations on revenue as well.

The company reported net income of $297 million, or 7 cents a share, compared with $1.0 billion, or 25 cents a share, in the year-earlier period. On an adjusted basis, Intel earned 41 cents a share, down from 59 cents a share a year prior, while analysts were looking for 22 cents a share.

Revenue dropped to $14.2 billion from $15.3 billion, while the FactSet consensus called for $13.6 billion.

The company saw revenue from its personal-computer segment, known as client-computing, drop 3% to $7.9 billion, whereas analysts were looking for $7.3 billion. Data-center and AI revenue fell 10% to $3.8 billion, narrowly missing the FactSet consensus, which was $3.9 billion.

Intel recorded a 45.8% adjusted gross margin, compared with 39.8% in the second quarter. The company’s forecast had been for about 43%.

Intel shares have climbed 24% so far this year, as the Dow Jones Industrial Average

DJIA

has lost about 1%.

[ad_2]

[ad_1]

Morgan Stanley on Wednesday said its third-quarter profit fell 10% amid weakness in its investment banking business, but its trading and asset-management revenue rose.

Morgan Stanley

MS,

said profit for the three months ended Sept. 30 fell to $2.26 billion, or $1.38 a share, from $2.49 billion, or $1.47 a share, in the year-ago period.

Analysts tracked by FactSet expect Morgan Stanley to earn $1.28 a share.

At the start of the quarter, analysts were expecting earnings of $1.58 a share.

Revenue fell 1% to $13.27 billion, ahead of the FactSet consensus estimate of $13.22 billion.

Morgan Stanley’s stock fell 2.8% in premarket trading on Wednesday.

Chief Executive James Gorman said the market environment was mixed.

“Our equity and fixed income businesses navigated markets well, and both wealth management and investment management producer higher revenues and profits year-over-year,” Gorman said.

Morgan Stanley’s stock fell 4.4% in the third quarter in a choppy period for bank stocks overall. Prior to Wednesday’s trades, the stock was down just under 10% in the past month, compared with 1.9% drop by the S&P 500

SPX.

For the third quarter, trading revenue rose 10% in the quarter to $3.68 billion.

Asset-management revenue increased by 6% to $5.03 billion, while investment-banking revenue dropped 24% to $1.05 billion.

During the past month, 11 analysts cut their profit estimates for Morgan Stanley and only one increased their view.

UBS analyst Brennan Hawken downgraded Morgan Stanley to neutral from buy last week, cutting his price target to $84 from $110.

“Despite its successful transformation into a wealth-management-focused firm with a solid, wire house peer leading growth profile, MS is confronted with obstacles such as deposit sorting/yield seeking, intense competition for talent, and a challenging revenue environment,” Hawken said.

The average rating among 26 analysts that cover Morgan Stanley is overweight.

The bank is in the midst of a leadership transition, with Chief Executive James Gorman planning to step down by next May. Three potential successors at the bank include Andy Saperstein, who heads up wealth management; Ted Pick, who runs capital markets; and Dan Simkowitz, head of investment management.

Also read: Bank of America’s profit climbs 10%, boosted by interest rates and loans

[ad_2]

[ad_1]

If anyone wanted evidence that the market feels skittish just look at stocks related to electric vehicles. They are getting hammered on capital raising activity that, frankly, should surprise no one.