Dan Ives, the popular tech analyst at Wedbush Securities, is quite gung-ho about the AI revolution. Quite often heard saying that “It is still 10 PM in the AI party, and the party goes on till 4 AM,” Ives certainly has his party favorites, chief among them being chip giant Nvidia (NVDA) and AI-driven data analysis company, Palantir (PLTR).

However, his other bets in the AI race do not garner as much limelight as the aforementioned duo. Thus, its recent note on SoundHound AI (SOUN) is worth, well, listening to.

Founded in 2005, SoundHound builds voice, sound and natural-language AI technologies involving speech recognition, natural language understanding, sound recognition, voice interfaces, and conversational agents. Its applications span multiple verticals, including automotive (voice assistants in cars), smart devices & IoT, enterprise customer service, restaurant/delivery voice ordering, and other conversational-AI use cases.

Valued at a market cap of $5.8 billion, the SOUN stock is down 27% on a year-to-date (YTD) basis. Yet, Ives and his associates remain bullish about the company, stating, “SOUN slightly raised its FY25 guidance to $165.0 million to $180.0 million (prior guidance of $160.0 million to $178.0 million) which we believe is conservative as demand remains strong across all vertical as it continues to see slight improvements in automotive along with strong growth in other verticals.”

So, should investors also tune in to SoundHound? Let’s analyze.

www.barchart.com

SoundHound AI’s latest results for Q3 2025 saw the company reporting record revenues. Yet, its losses came in wider than expected when compared to Street estimates, as profitability remains elusive for the company.

In Q3, the company’s revenues came in at $42 million, up 68% from the previous year as the company secured several deals across industries such as automotive, financial services, healthcare, and insurance, among others. Conversely, losses widened significantly to $0.27 per share from $0.06 per share as the company struggles to deal with scale. Estimates were for a loss of $0.09 per share.

Notably, net cash used in operating activities also increased for the nine months ended September 30, 2025, to $76.3 million from $75.8 million in the year-ago period. Despite the widening in the cash outflow from operating activities, SoundHound closed the quarter with a cash balance of $268.9 million, which was much higher than its short-term debt levels of $2.3 million.

So, the financials do not really inspire that much confidence in the SOUN stock as an investment. What does is its growth potential, and there are certainly some solid drivers for it, underpinned by AI.

SoundHound AI’s leadership in the AI-driven conversational tech market is commendable, which acts as a solid base for the company to capture the rapidly growing agentic AI market. Notably, the company’s expansive data repository stands as a pivotal asset in advancing these objectives. The management has previously highlighted that its platforms now handle in excess of 1 billion queries monthly, a metric that underscores robust operational expansion and a pronounced edge in data accumulation. Going forward, as platform usage intensifies, the resultant insights sharpen the efficacy of machine learning and AI-driven enhancements, facilitating accelerated innovation in product development. This dynamic establishes SoundHound’s inaugural point of distinction relative to industry peers.

SoundHound further sets itself apart from established voice assistants, including Amazon’s (AMZN) Alexa and Google’s (GOOG) (GOOG) Home devices, by fusing its proprietary machine learning frameworks, CaiNET and CaiLAN, with generative AI and large language models to yield more fluid and precise conversational interactions. This integration empowers clients to preserve their distinctive branding, retain ownership over their information, and shape the end-user journey on their terms.

Moreover, strategic buyouts, including those of Amelia and SYNQ3, are poised to deliver meaningful accretive value. The Amelia acquisition fortifies SoundHound’s foothold in financial services, insurance, and medical sectors, whereas SYNQ3 brings expertise in voice-enabled solutions tailored for hospitality, backed by a prospective base exceeding 100,000 restaurant sites and commitments from over 10,000 to date.

Lastly, recent alliances have additionally reinforced SoundHound’s stature as a frontrunner in agentic AI applications. One such arrangement involves the casual dining operator Red Lobster, which plans to implement a novel agentic AI solution for managing inbound telephone orders across its network of more than 500 outlets. This deployment aims to refine order processing workflows, thereby elevating service quality. For SoundHound, the initiative offers a compelling showcase of deployment at scale, potentially enticing additional participants within the fast-casual dining segment.

Equally significant is the expanded collaboration with Apivia Courtage, a prominent French intermediary in commercial insurance. The broker intends to integrate SoundHound’s Amelia 7 agentic AI system across its call center infrastructure to address diverse client engagements. This builds upon an established relationship dating to 2023, during which prior SoundHound implementations yielded a 20% improvement in contact center performance. The current phase advances those foundations by incorporating autonomous agents adept at deliberation, strategy formulation, and fulfillment of intricate, multifaceted requests, eliminating the need for human intervention. At the same time, the partnership extends SoundHound’s international profile well beyond its primary domestic stronghold of the United States.

SoundHound is a pure play on voice-enabled by AI, which separates it from other larger players, for whom it is just one of their products. Although this differentiates it from them, the company does not have the deep pockets that they possess. Yet, the company is not ceding ground and remains a credible choice for enterprises, as evidenced by the recent partnerships. Now, the primary goal of the company should be to do this profitably.

Overall, analysts have rated SOUN stock a “Moderate Buy”, with a mean target price of $16.50. This implies an upside potential of about 17% from current levels. Out of nine analysts covering the stock, five have a “Strong Buy” rating, and four have a “Hold” rating.

www.barchart.com

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

The adoption of artificial intelligence (AI) is continuing at a brisk pace, but some are waiting for the other shoe to drop. A strengthening U.S. economy and robust quarterly results from several AI-related companies helped push the Nasdaq Composite to a new record high last week. Yet these same factors have some investors wondering if the bull market has gone too far, too fast.

Nvidia(NASDAQ: NVDA) has become the de facto standard bearer for the generative AI industry. The company is scheduled to report its fiscal 2025 third-quarter results in less than three weeks, and it’s not an exaggeration to suggest that Wall Street is on pins and needles waiting for the clues that report will offer about the state of AI adoption. Nvidia’s sales have surged since the start of last year, driving the stock up 833% (as of this writing). It’s also less than 5% off the all-time high it touched late last month.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

There’s a lot riding on Nvidia’s upcoming financial report, and many shareholders are wondering whether the stock can possibly continue its breathtaking run. Is it worth picking up shares ahead of its financial report on Nov. 20? Fortunately for investors, data has begun to pile up that could help answer that question.

Image source: Getty Images.

The key to Nvidia’s astounding successes of the past couple of years has been the performance of its graphics processing units (GPUs), which are the best chips for supplying the specific type of computational horsepower necessary for generative AI, as well as other types of cloud computing needs. The necessary resources and the sheer magnitude of data involved limit the top-tier AI models to the world’s largest technology companies and cloud providers — most of which are Nvidia customers. Comments made in conjunction with those tech giants’ recent quarterly results provide some insights about the state of the AI revolution — and the evidence is clear.

For example, Microsoft(NASDAQ: MSFT) said it spent heavily to advance its AI agenda in its fiscal 2025 first quarter (which ended Sept. 30). The company had capital expenditures (capex) of $20 billion, which primarily went to support “cloud and AI-related” demand. CFO Amy Hood expects Microsoft’s spending spree to continue: “We expect capital expenditures to increase on a sequential basis given our cloud and AI demand signals,” she said.

During Alphabet‘s (NASDAQ: GOOGL)(NASDAQ: GOOG) third-quarter earnings call, CEO Sundar Pichai said, “Realizing [the opportunity] of AI requires … meaningful capital investment.” The company revealed capex of $13 billion during the quarter and suggested there would be “substantial increases in capital investment … going into 2025.”

Rounding out the big three cloud providers is Amazon(NASDAQ: AMZN). During its Q3 earnings call, CEO Andy Jassy called generative a “maybe once-in-a-lifetime type of opportunity … we’re aggressively pursuing it.” CFO Brian Olsavsky put that in context, saying Amazon’s capex would amount to roughly $75 billion this year, with much of that going toward cloud computing and AI infrastructure. The company also said it would unveil “100 new cloud infrastructure and AI capabilities” at AWS re:Invent later this month.

Finally, there’s Meta Platforms(NASDAQ: META). While it isn’t a cloud provider, the company’s social media sites attract 3.29 billion people every day, giving Meta vast volumes of user data. The company increased its full-year capex outlook to roughly $39 billion, and CFO Susan Li said, “We continue to expect significant capital expenditures growth in 2025.” She previously noted this was “to support our AI research and product development efforts.”

The trend of accelerating capex to support the growing demand for AI is clear. Additionally, a large fraction of that money will be spent on the data centers and servers needed for cloud computing — where the majority of generative AI software lives. As such, Nvidia will likely be the recipient of a good deal of this spending.

Nvidia has historically kept mum about its biggest customers, but that hasn’t stopped Wall Street from doing some digging. Analysts with Bloomberg and Barclays Research have run the numbers and come to the conclusion that Nvidia’s four biggest customers — generating a total of 40% of its sales — are:

Microsoft: 15%

Meta Platforms: 13%

Amazon: 6.2%

Alphabet: 5.8%

Each of these companies has left no question about their plans to spend heavily on capital expenditures, and in particular to spend heavily on infrastructure to support their cloud computing and AI aspirations. As the leading provider of data center GPUs, Nvidia will likely continue to top the list of beneficiaries of that spending.

Nvidia will deliver its next set of quarterly results on Nov. 20. After achieving triple-digit-percentage year-over-year growth for five consecutive quarters, the company has tried to rein in the market’s expectations, suggesting that its revenue growth this time will only clock in at about 79%. While that would be a deceleration, it would also still be remarkable growth by any stretch of the imagination.

Investors looking to make money over the coming three weeks might be disappointed. No one can say for sure how Nvidia stock will react to the report — even if the company exceeds expectations.

For a reminder of the difficulties involved in short-term prognostication, investors need only look back to this summer, when, starting in mid-June, Nvidia stock lost as much as 27% of its value on fears that its next-generation Blackwell AI processors would be delayed — only to come roaring back. It was an illustration that with this stock, volatility is part of the cost of admission. That said, both the comments made by its big tech customers and their historical spending patterns suggest that Nvidia has further strong growth ahead.

For investors looking for stocks to hold for years and decades rather than weeks and months, Nvidia is a clear choice to benefit from the AI revolution. And trading at roughly 32 times next year’s earnings, it’s still attractively priced. I can’t say for sure what the stock will do between now and Nov. 20. What I can say — with a fair degree of confidence — is that investors who buy Nvidia stock soon and hold it for three to five years or more will be very glad they did.

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $829,746!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Danny Vena has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

One of the biggest themes in the markets for the last two years has been artificial intelligence (AI).

Naturally, famed entrepreneur Elon Musk has found himself at the center of the AI revolution — and he just gave investors a big reason to seriously consider both Dell Technologies(NYSE: DELL) and Super Micro Computer(NASDAQ: SMCI).

Let’s explore how Musk is working with these AI leaders, and assess if these stocks are good buys right now.

What did Elon Musk just say?

In addition to running Tesla and social media platform X (formerly Twitter), Musk is also managing an AI start-up, called xAI.

xAI is building a chatbot called Grok, and is aiming to compete with the likes of OpenAI. Musk is a co-founder of OpenAI but abandoned the project back in 2018. Since his departure, Musk has gotten into many publicized tiffs with OpenAI’s CEO, Sam Altman, over safety concerns and how AI should be used in society.

Namely, Musk took to X to tell investors and AI enthusiasts that xAI will be partnering with Dell and Supermicro to build its AI infrastructure such as server rack solutions and factory architecture.

How Dell and Supermicro stand to benefit

AI has many different components. One of the biggest bellwethers for AI at the moment are specialized chips known as graphics processing units (GPUs). These chips are used to train large language models and other computing functions to develop generative AI applications.

Right now, Nvidia is the undisputed leader of AI chips — owning an estimated 80% share of the market.

However, deploying chips into machine learning models and other use cases is only part of the broader equation. Companies such as Dell and Supermicro specialize in a different area within the chip realm.

Both Dell and Supermicro are major players in AI infrastructure solutions. Essentially, both companies specialize in designing integrated systems architecture, server racks, and storage clusters for data centers.

Considering xAI just raised $6 billion in funding back in May, Dell and Supermicro appear well positioned to benefit from AI tailwinds as xAI moves swiftly to catch up with the competition.

Image source: Getty Images.

Dell, Supermicro, both, or neither?

On the surface, owning different businesses across the semiconductor landscape might be a good idea. AI is still in its infancy, and there are many different applications among chip companies that are playing a role in the technology’s development.

With that said, a close look at valuation should shed some light on investing in Dell and Supermicro in particular.

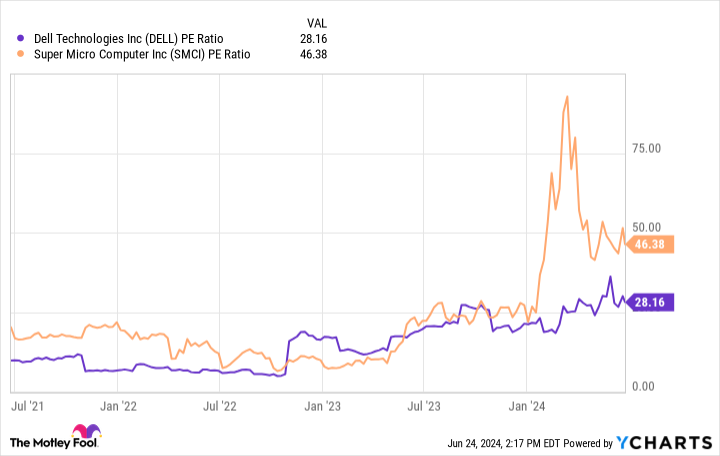

DELL PE Ratio Chart

The chart above illustrates the price-to-earnings (P/E) multiple for Dell and Supermicro over the last few years. While neither stock looks cheap, Dell is clearly trading at a noticeable discount to Supermicro. With that said, Supermicro’s premium is arguably warranted considering how fast the company is growing.

Moreover, one of my biggest knocks against Supermicro has been that the company relies heavily on business from Nvidia — a dynamic that could hurt the company in the long run as more companies design competing chips.

Now, with a nod of approval from Musk and xAI, I’m more optimistic about Supermicro’s prospects of branching out and earning meaningful business from new customers in the AI space.

At the end of the day, allocating a portion of your AI holdings to both Dell and Supermicro could be a good idea for long-term investors. If I had to just choose one company, I think Dell is the better value compared to Supermicro based on its lower P/E and diversified business. Considering Supermicro is still relatively small, I think its valuation needs to continue normalizing before it looks like a bargain opportunity.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $759,759!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

Adam Spatacco has positions in Nvidia and Tesla. The Motley Fool has positions in and recommends Nvidia and Tesla. The Motley Fool has a disclosure policy.

The Nasdaq hit a new record high recently, and the good times may be far from over. History shows us that over the past 10 periods of annual market declines — dating back to the early 1970s — the index always has climbed for at least two consecutive years afterward. And on all but one occasion, the index posted a double-digit increase during its second year of gains. If this trend continues, the Nasdaq, heading for a 7.4% increase so far, is set to climb higher in 2024.

And the stocks that have led the gains and could continue leading the movement are artificial intelligence (AI) players. Investors are excited about this high-growth, high-potential technology. AI may make game-changing moves — like bringing lifesaving drugs to patients more quickly — and could save companies and individuals money and time as it completes tasks and solves problems.

That’s why right now is the perfect time to get in on potential AI powerhouses. Let’s check out two AI stocks to buy hand over fist before the Nasdaq soars higher.

Image source: Getty Images.

1. Amazon

Amazon(NASDAQ: AMZN) is benefiting from AI in two ways. The company uses AI across its e-commerce business to streamline operations and improve the customer experience. And Amazon sells AI solutions to customers through Amazon Web Services (AWS), its cloud computing business.

In e-commerce, Amazon’s AI will help you choose a product based on your buying history, and AI is helping the company choose the best delivery routes for packages. These and other AI efforts should keep customers coming back and boost Amazon’s profitability.

As for AWS, the service offers everything from chips for customers to train their own AI models to a fully managed service that allows customers to customize the most popular large language models (LLMs) to suit their needs. AWS customers can access the company’s own lower-cost chips, as well as the fastest, highest-performing chips and services from AI chip market leader Nvidia(NASDAQ: NVDA).

All of this could make Amazon one of the winners of a potential AI revolution. And Amazon already has a solid earnings track record — so the company has the resources to invest in this hot area and continue to grow. In the most recent quarter, Amazon’s net sales rose in the double digits, and operating income more than quadrupled to surpass $13 billion.

Today, the stock trades for 42x times forward earnings estimates, a fair price for an already solid business with top AI prospects.

2. Nvidia

Nvidia holds 80% of the AI chip market, and though it faces competitors in the space, it’s unlikely to lose its lead any time soon for two reasons. First, the company’s first-to-market advantage and brand strength should keep at least some customers loyal. Second, Nvidia is pouring investment into research and development to stay ahead.

Investors expect the launch of Nvidia’s H200 chip in the second quarter and then potentially the launch of the Blackwell architecture along with the B100 chip later in the year. These newer products are improvements on the company’s already fastest-on-the-market chip.

But Nvidia doesn’t only design chips. The company also offers a full portfolio of products and services for the AI client, including a software platform that serves as an “operating system” for AI. Nvidia products are offered on AWS, as mentioned, but also through all other major cloud providers. So it’s easy for customers to access Nvidia’s offerings directly through their cloud service.

Nvidia’s earnings have soared, but growth may be far from over considering the company’s market leadership — and likelihood of remaining on top. Today, Nvidia trades for 35x times forward earnings estimates, which seems reasonable for such a solid growth stock. That’s why Nvidia makes a no-brainer addition to any AI portfolio.

Should you invest $1,000 in Amazon right now?

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adria Cimino has positions in Amazon. The Motley Fool has positions in and recommends Amazon and Nvidia. The Motley Fool has a disclosure policy.

Semiconductor stocks have been on fire ever since ChatGPT was launched in late 2022. Since then, a slew of new generative artificial intelligence (AI) applications have made cutting-edge graphics processing units that can handle accelerated applications a hot commodity. As Nvidia(NASDAQ: NVDA) is the leader in that subset of the chip market, its sales and stock price have been rocketing higher.

After watching Nvidia’s share price rise by 222% during the 12-month period that ended Wednesday, some investors are justifiably nervous that the stock has gotten too far ahead of itself.

Nvidia will report its fiscal fourth-quarter results on Feb 21. During its fiscal third quarter, which ended Oct. 29, total revenue surged 206% year over year.

Its valuation of about 97 times trailing earnings isn’t unreasonable if you assume continued growth at its present rate. However, the semiconductor industry is famously cyclical. Demand for chips that can power generative AI applications will eventually crash. We just don’t know when that crash will come. If you buy Nvidia at this inflated valuation and the bottom falls out next year, you could suffer heavy losses.

For most folks who missed the boat on Nvidia, climbing aboard now entails more risk than they can tolerate. If you want to hitch your portfolio to a major player in the AI revolution with significantly less risk, consider buying shares of Alphabet(NASDAQ: GOOG)(NASDAQ: GOOGL) now to hold for the long run.

Alphabet’s AI prowess is better than you think

The AI gold rush started when OpenAI launched ChatGPT about a year and a half ago. By that time, though, Alphabet had already been an AI-first company for several years. In a 2016 blog post, Alphabet CEO Sundar Pichai told everyone that “in the next 10 years, we will shift to a world that is AI-first, a world where computing becomes universally available.”

If it didn’t have an army of engineers skilled in the arts of machine learning, Google wouldn’t be able to recognize poor spelling in search queries or rank search results properly. With AI working behind the scenes to provide better results, Google has captured a 91.5% share of the global search market, according to Statcounter. Microsoft, a tech giant currently worth over $3 trillion, launched Bing nearly 15 years ago, but it still has just 3.4% of the global market for search.

Google Maps has over a billion monthly users, and millions of businesses eagerly use the platform to attract new customers. Maps is another AI-heavy application — it wouldn’t be able to forecast traffic or recommend improved routes without the contributions of some of the AI industry’s most valuable talent.

Why Alphabet is well positioned for AI’s next chapter

In addition to a search business that dominates its competitors, Alphabet is a leading provider of cloud computing services. Late last year, its cloud offering became a lot more valuable with the addition of Gemini.

OpenAI caught Alphabet flatfooted when it launched ChatGPT in late 2022. In a nutshell, Gemini offers a similar generative AI experience for consumers with the chatbot formerly known as Bard. Gemini also gives enterprise-sized Google Cloud customers a chance to build AI applications of their own.

With several applications that boast over a billion active users per month, Google can offer enterprise-level cloud customers access to reams of real-world data they won’t find anywhere else.

Image source: Getty Images.

A fair price

Google Cloud sales rose 26% year over year in the third quarter. With a large addressable market and an advantage over competitors who don’t dominate the markets for search and location data, investors can reasonably expect strong growth from its cloud business for another decade.

The vast majority of Alphabet’s revenues and profits still come from Google Services. This segment is growing more slowly than its cloud business, but it’s still a long way from stagnation. Google Services revenue rose 12.5% year over year in the fourth quarter. Over the same time frame, operating income from the services segment jumped 32%.

With advantages over the competition, and its two main operating segments growing by double-digit percentages, Alphabet should be valued at a high earnings multiple — but it isn’t. You can buy the stock for around 21 times forward earnings expectations.

There’s no such thing as a risk-free growth stock. With reliable earnings from advertising and cloud services, though, buying Alphabet at a reasonable valuation gives you an excellent chance to come out ahead over the long run. With its firm toehold in the rapidly evolving AI space, it also has a chance to become a top performer. Buying some shares now to hold for the long run looks like a smart move.

Should you invest $1,000 in Alphabet right now?

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Cory Renauer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Investors can’t get enough of Nvidia (NVDA). Now, the company is spreading that love to other stocks.

On Wednesday night, an SEC filing revealed the chipmaking giant held investments in the stocks Arm Holdings (ARM), SoundHound AI (SOUN), and biotech company Recursion Pharmaceuticals (RXRX) as of Dec. 31, 2023.

All three of the AI-related stocks popped on the news. Arm, whose stock was already up more than 80% in the last month after the company attributed its better-than-expected revenue expectations to AI initiatives, saw a modest 1% gain on the news. Recursion’s stock rose nearly 10%.

Meanwhile,SoundHound, a smaller player that specializes in voice AI and speech recognition, saw a huge gain. The stock was on track for its best day ever at the open, popping about 80% before paring gains to nearly 50% on Thursday morning.

Still, the massive price move in SoundHound, which had been down more than 40% over the last year, reaffirms market enthusiasm for Nvidia and other names associated with the stock.

Nvidia shares areup nearly 50% since the start of 2024 and more than 220% in the past year. The company’s market cap — which stood at $1.8 trillion as of Thursday midday — recently surpassed that of Amazon (AMZN) and Alphabet (GOOG, GOOGL). Only Microsoft (MSFT) and Apple (AAPL) now have a higher valuation than Nvidia.

The company’s revenue has increased significantly over the past year as demand for its AI-powered chips has soared. In the third quarter, Nvidia reported revenue of $18.12 billion, up 206% from a year ago. The company is set to report quarterly results on Feb. 21.

Wedbush Securities senior equity analyst Dan Ives said that Nvidia’s investments signal a stamp of approval from the “Godfather of AI,” CEO Jensen Huang —and that can go a long way with investors.

“We view this as a positive indicator for [SoundHound] as this investment now further solidifies the company’s brand within the AI Revolution,” Ives wrote in a note on Thursday morning.

As of Dec. 31, Nvidia had a nearly $3.67 million stake in SoundHound. Meanwhile, its stakes in Arm and Recursion totaled just over $147 million and $75.9 million, respectively.

Nvidia’s logo is seen displayed on a mobile phone screen with AI written in the background. (Idrees Abbas/SOPA Images/LightRocket via Getty Images) (SOPA Images via Getty Images)

Josh Schafer is a reporter for Yahoo Finance. Follow him on X @_joshschafer.