[ad_1]

[ad_2]

[ad_1]

Health policy changes in Washington will ripple through the country, resulting in millions of Americans losing their Medicaid or Affordable Care Act coverage. But there are still ways to find care.

Over the next decade, the GOP’s One Big Beautiful Bill Act is expected to slash nearly $1 trillion in spending from Medicaid, the state-federal program for people with low incomes and disabilities. The implementation of new work rules will cause some beneficiaries to lose their Medicaid coverage.

Millions of Americans are facing enormous increases in their out-of-pocket costs for ACA coverage. So far, 1.2 million fewer people have signed up for Obamacare plans compared with last year, and health policy analysts estimate more will lose coverage as they fail to pay their premiums.

Health costs are a top concern for Americans. Two-thirds of the public say they are somewhat or very worried about affording health care, more than express the same worries about utilities, food, housing, or gas, according to a January poll from KFF, a health information nonprofit that includes KFF Health News.

“All of this pain just doesn’t have to be there,” said Cheryl Fish-Parcham, director of private coverage at the health consumer group Families USA.

Doctors and health policy researchers say health coverage, of any kind, is the best protection against major medical debt.

Caitlin Donovan, a senior director at the Patient Advocate Foundation, recommends exhausting every available option for health coverage before going uninsured.

Even a high-deductible plan can protect patients from medical bankruptcy “if the absolute worst-case scenario happens,” she said.

Here are five ways that the uninsured can find affordable care.

Patients can be hesitant to tell their doctors they’re uninsured or be wary of expressing concern about being able to afford care.

But some hospitals, physicians, and other providers offer cheaper cash pay options, said Cynthia Cox, a senior vice president and the director of the Program on the ACA at KFF.

Often prices are negotiable. “Always ask,” she said.

Health care providers can make adjustments if they know patients are worried about money, said Ateev Mehrotra, a doctor and researcher at Brown University.

“If my patient tells me, ‘Doc, I’m gonna have to pay for this out-of-pocket,’ I’m gonna make a different risk calculus,” Mehrotra said.

That doesn’t mean a patient won’t get the care they need, he said. A doctor, for instance, might order an ultrasound instead of an MRI, which is more expensive.

If your usual provider won’t budge on prices, then search for providers that cater to patients without insurance.

Federally qualified health centers, or FQHCs, and other community clinics offer routine and non-emergency care, such as treatment for flu or infection, for low-income residents and the uninsured. Community health centers charge based on a sliding scale and see 52 million patients annually in some of the country’s most underserved areas, according to the National Association of Community Health Centers.

The Trump administration has made funding cuts that might lead some of the country’s approximately 1,500 FQHCs to close or cut services. But the administration still maintains a site to find a local center.

Planned Parenthood also accepts uninsured patients. Its centers test for sexually transmitted diseases, provide birth control options, and offer postpartum and gender-affirming care and other services.

And the National Association of Free & Charitable Clinics also offers a tool to help people find free or low-cost care.

Most community clinics don’t offer specialty care, but they can usually refer patients who need more intensive services to providers willing to work with uninsured patients.

And academic medical centers tend to have more charity care programs that help uninsured patients lower their bills.

“If you’re uninsured or even underinsured, you might be able to qualify for a significant discount on the cost of your care,” Cox said.

Still, be wary of heading to the emergency room, which is the most expensive place to get care. While ERs are federally required to stabilize all patients regardless of their ability to pay, they can still leave you with a big bill — and often do.

Health services vary widely from county to county, but many offer free vaccinations, family planning services, and testing for sexually transmitted infections, as well as for flu, covid, and tuberculosis.

Some county health departments also offer more advanced care, such as dental services and mental health or substance abuse programs. And some states have consumer assistance programs that can guide residents in finding care, Fish-Parcham said.

In addition, the Centers for Disease Control and Prevention’s National Breast and Cervical Cancer Early Detection Program makes free or low-cost breast and cervical cancer screenings available to low-income women in all states and territories. And some states cover screenings for other types of cancer as well.

Don’t just fill your prescription at the closest pharmacy. Instead, research generic drug options and look around for the best price on brand names.

A handful of sites such as GoodRx and WellRx offer comparison shopping tools and information on other ways to get drug discounts.

And some retailers offer low-cost access to common prescription drugs — at prices cheaper than you would find if you had insurance. Walmart, for instance, sells 90-day prescriptions of dozens of generic versions of drugs for $10. As does Target, Costco, and a new site called the Cost Plus Drug Company.

Many drugmakers also offer patient assistance programs, coupons, and rebates on some medications. Check their websites for details on how to apply.

States also offer drug assistance programs. The steps to qualify and types of drugs vary, but this tool has a list of programs and how they work.

Joining a clinical trial is another way to access treatment. The National Institutes of Health and its National Cancer Institute have lists, but patients must first meet the criteria. Clinical trials aren’t necessarily free, even with insurance, Donovan said, so be sure to ask about any associated costs.

Patients with a specific diagnosis might have additional options for specialty treatment.

For example, someone with breast cancer should check with the American Cancer Society and the nonprofit Susan G. Komen organization, Cox said.

The Patient Advocate Foundation hosts a list of vetted foundations that can help offset the cost of medical bills and provide other resources such as transportation and lodging, Donovan said. Just type in basic information such as age, location, and diagnosis to see what is available.

Disease-specific foundations such as those for lupus or irritable bowel syndrome can also steer patients to free or low-cost resources or cover some costs of care, Donovan said.

“Everything is out there,” she said.

As you research affordable care options, don’t be tricked by plans that look like health insurance but don’t offer guaranteed protection against big bills.

Some short-term plans and health care sharing ministries might seem like good deals, but read the fine print. Some red flags to look for: too-good-to-be-true monthly payments; no coverage for preexisting conditions; morality clauses such as those prohibiting the use of alcohol or drugs; or a lack of coverage for benefits such as mental health counseling that are required in ACA plans.

KFF Health News correspondent Sam Whitehead contributed to this report.

Are you struggling to afford your health insurance? Or have you decided to forgo coverage? Click here to contact KFF Health News and share your story.

KFF Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at KFF — the independent source for health policy research, polling, and journalism.

[ad_2]

[ad_1]

When Kassidy Hooter learned in December how much her health insurance costs were going to rise this year, she went into panic mode.

The Shreveport, Louisiana, resident and mother of three knew she urgently needed care — Hooter is in the final trimester of a high-risk pregnancy. But the family could no longer afford their Affordable Care Act plan coverage now that a federal tax subsidy was lapsing on Dec. 31, 2025, meaning they would face thousands of dollars in additional out-of-pocket costs.

“We heavily considered that it might just be cheaper to give birth at home,” Hooter, 24, told CBS News. “Just because that’s an insane amount of debt to take on.”

In the end, Hooter decided to forgo insurance altogether.

Courtesy of Kassidy Hooter

A local medical center offered three months of financial aid that will carry her through her due date in February and into late March. After that, she will have to bear any medical expenses on her own. Her plan now is to get her newborn on Medicaid, a government health plan for low-income Americans, as quickly as possible.

“I’m just hoping for the best,” she told CBS News.

Since its introduction in 2010, the ACA has been instrumental in cutting the share of uninsured Americans from approximately 15% to 8%, according to Nima Sheth, vice president of health justice at the National Partnership for Women and Families, a nonprofit advocacy group.

However, the number of people without health insurance is likely to surge if Congress fails to come up with a solution for the 22 million Americans who received an ACA tax credit, experts warn. The number of uninsured will rise by an average of 3.8 million each year from 2026 to 2034 without an extension of the credits, the Congressional Budget Office estimated in 2024.

Americans in most states have until Jan. 15 to enroll in an ACA marketplace plan, according to healthinsurance.org.

Without the tax credits, premiums for ACA enrollees who previously relied on the subsidies will increase by an average of 114%, estimates KFF, a nonprofit provider of health policy news and research.

“What we’re seeing here is a policy choice — is, in effect, turning insurance into a luxury item and medical debt into the default,” Michelle Sternthal, interim senior director of policy and strategy at health care advocacy group Community Catalyst, told CBS News.

The House of Representatives on Thursday approved a three-year extension of the expired ACA tax credits. The legislation faces an uphill climb in the Republican-led Senate, although lawmakers think it could provide a starting point for a compromise that would keep the credits alive in some form.

Plantation, Florida, resident Stacy Kanas, whose family also received an ACA tax credit, is now considering going without health insurance after realizing that her monthly premium to cover her and her husband would rise to $2,500 — more than double what she was paying last year to cover both of them plus her 20-year-old daughter.

“It’s weighing extraordinarily heavily on me,” Kanas, 59, told CBS News. “My husband had a major surgery about five years ago, and we don’t want to be uninsured.”

Although in decent health, the small business owner worries about what could happen if someone in her family falls seriously ill. “You’re one catastrophic event away from perhaps having a financial disaster,” she said.

Even people who keep their ACA coverage could end up skipping out on care to avoid out-of-pocket expenses, experts said.

“If you’re underinsured and you have high deductibles, the coverage that you’re getting is designed to dissuade getting care, including preventative care, so you’re going to delay your care until there are emergencies,” Sternthal said.

Robert Myers, a consultant based outside of St. Louis, Missouri, was on a silver ACA plan last year, but switched to a bronze plan after learning his premiums would rise to $400 a month, up from $17 in 2025.

Under his new plan, the 31-year-old does not have a monthly premium. However, Myers could owe much more in out-of-pocket costs due to $80 co-pays and an $8,000 deductible. As a result, he’s planning on scaling back on doctor’s visits, a trend experts say ends up driving more people to the emergency room for care.

“They’ll kind of go to the ER and get what they need fixed with a band aid, and then not get long-term care,” Sheth said.

This can have wider ripple effects because an increase in uncompensated hospital care can drive up costs for other patients, as facilities seek to recoup the costs, according to Sternthal, who supports an extension of the ACA tax credits.

“Every delay locks families into decisions that harm their health and their financial stability, but then also reverberates out into the business community, the local community,” she said.

[ad_2]

[ad_1]

It’s the first week of a new year for Congress, and each chamber is considering legislation with votes to watch on Thursday.Enhanced Health Care SubsidiesThe House of Representatives is voting on a bill to reinstate tax credits that expired last year and were central to the government shutdown.The bill aims to extend these subsidies for three years, helping those without insurance through their employers pay for coverage. Four Republicans: Rep. Brian Fitzpatrick (PA-1st), Rep. Ryan McKenzie (PA-7th), Rep. Rob Bresnahan (PA-8th), and Rep. Mike Lawler (NY-17th) joined Democrats to push the vote, which is expected to pass. Five more Republicans joined Democrats during a test vote on Wednesday.However, the Senate is not expected to consider this bill, as they are working on their own Affordable Care Act reform measure designed to pass both chambers.Venezuela War Powers ResolutionThe Senate is revisiting a war powers resolution that would prevent the president from using military force in Venezuela without congressional approval. This follows a recent military operation in Venezuela’s capital, which led to the arrest of President Nicolás Maduro and his wife, who are now in New York facing narcoterrorism charges. President Donald Trump has stated that the U.S. is running Venezuela and may deploy the military again if the remaining Maduro regime does not comply with U.S. demands.The same resolution failed a previous vote, as well as a measure to stop the Trump administration from bombing alleged drug boats in the Caribbean and Pacific that the White House says were connected to Venezuela. Past administrations arrested and charged such suspects. The Trump administration’s campaign has killed more than 100 people.Reactions To Greenland RhetoricThe White House’s suggestion to use military force to take over Greenland has been met with criticism on Capitol Hill. Democrats have long opposed this idea, and several Republicans have recently spoken out against it.Rep. Mike Johnson, House Speaker, said, “All this stuff about military action and all that, I don’t even think that’s a possibility.” Sen. Thom Tillis of North Carolina criticized the notion, saying, “Making insane comments about how it is our right to have territory owned by the kingdom of Denmark, folks, amateur hour is over.” Rep. Ryan Zinke of Montana noted, “In the case of Greenland, you have two things: one, not a present threat, and so they have a duly elected president. So, he doesn’t have the authority without Congress.”Rep. Don Bacon of Nebraska added, “It’s very… amateurish. I feel like we’ve got high school kids playing Risk.”Secretary of State Marco Rubio has also stated that the president wants to buy Greenland.Earlier this week, the White House Press Secretary Karoline Leavitt told Hearst Television: “President Trump has made it well known that acquiring Greenland is a national security priority of the United States, and it’s vital to deter our adversaries in the Arctic region. The President and his team are discussing a range of options to pursue this important foreign policy goal, and of course, utilizing the U.S. Military is always an option at the Commander in Chief’s disposal.”Keep watching for the latest from the Washington News Bureau:

It’s the first week of a new year for Congress, and each chamber is considering legislation with votes to watch on Thursday.

Enhanced Health Care Subsidies

The House of Representatives is voting on a bill to reinstate tax credits that expired last year and were central to the government shutdown.

The bill aims to extend these subsidies for three years, helping those without insurance through their employers pay for coverage. Four Republicans: Rep. Brian Fitzpatrick (PA-1st), Rep. Ryan McKenzie (PA-7th), Rep. Rob Bresnahan (PA-8th), and Rep. Mike Lawler (NY-17th) joined Democrats to push the vote, which is expected to pass. Five more Republicans joined Democrats during a test vote on Wednesday.

However, the Senate is not expected to consider this bill, as they are working on their own Affordable Care Act reform measure designed to pass both chambers.

Venezuela War Powers Resolution

The Senate is revisiting a war powers resolution that would prevent the president from using military force in Venezuela without congressional approval. This follows a recent military operation in Venezuela’s capital, which led to the arrest of President Nicolás Maduro and his wife, who are now in New York facing narcoterrorism charges.

President Donald Trump has stated that the U.S. is running Venezuela and may deploy the military again if the remaining Maduro regime does not comply with U.S. demands.

The same resolution failed a previous vote, as well as a measure to stop the Trump administration from bombing alleged drug boats in the Caribbean and Pacific that the White House says were connected to Venezuela. Past administrations arrested and charged such suspects. The Trump administration’s campaign has killed more than 100 people.

Reactions To Greenland Rhetoric

The White House’s suggestion to use military force to take over Greenland has been met with criticism on Capitol Hill. Democrats have long opposed this idea, and several Republicans have recently spoken out against it.

Rep. Mike Johnson, House Speaker, said, “All this stuff about military action and all that, I don’t even think that’s a possibility.”

Sen. Thom Tillis of North Carolina criticized the notion, saying, “Making insane comments about how it is our right to have territory owned by the kingdom of Denmark, folks, amateur hour is over.”

Rep. Ryan Zinke of Montana noted, “In the case of Greenland, you have two things: one, not a present threat, and so they have a duly elected president. So, he doesn’t have the authority without Congress.”

Rep. Don Bacon of Nebraska added, “It’s very… amateurish. I feel like we’ve got high school kids playing Risk.”

Secretary of State Marco Rubio has also stated that the president wants to buy Greenland.

Earlier this week, the White House Press Secretary Karoline Leavitt told Hearst Television: “President Trump has made it well known that acquiring Greenland is a national security priority of the United States, and it’s vital to deter our adversaries in the Arctic region. The President and his team are discussing a range of options to pursue this important foreign policy goal, and of course, utilizing the U.S. Military is always an option at the Commander in Chief’s disposal.”

Keep watching for the latest from the Washington News Bureau:

[ad_2]

[ad_1]

NEW YORK CITY, New York: Millions of Americans are beginning 2026 facing sharply higher health insurance bills after enhanced Affordable Care Act subsidies expired, locking in premium increases that could force some households to drop coverage altogether.

The tax credits, first introduced during the COVID-19 pandemic and later extended by Democrats, had lowered insurance costs for most people who buy coverage on the Affordable Care Act marketplaces. Their expiration comes after months of political deadlock in Washington, despite warnings from both parties that the issue could carry significant electoral consequences.

Democrats pushed unsuccessfully to extend the subsidies, even triggering a 43-day government shutdown over the issue. Some moderate Republicans urged action, while President Donald Trump floated — then abandoned — a potential compromise after opposition from conservative allies. With no agreement reached before the deadline, the credits expired at the start of the new year.

A House vote expected later in January could reopen the debate, but there is no guarantee that lawmakers will succeed in restoring the subsidies.

The lapse affects millions of Americans who do not receive health insurance through an employer and are ineligible for Medicaid or Medicare — including self-employed workers, small business owners, farmers, and ranchers. The timing also coincides with a midterm election year in which affordability, particularly healthcare costs, ranks among voters’ top concerns.

“It really bothers me that the middle class has moved from a squeeze to a full suffocation, and they continue just to pile on and leave it up to us,” said Katelin Provost, a 37-year-old single mother whose premiums are set to soar. “I’m incredibly disappointed that there hasn’t been more action.”

Costs Jump Sharply for Many Households

The expanded subsidies, introduced in 2021, allowed some lower-income enrollees to obtain coverage with no monthly premium, capped costs for higher earners at 8.5 percent of income, and broadened eligibility for middle-class households. Democrats later extended the program through the end of 2025.

With those credits gone, the impact is substantial. On average, more than 20 million subsidized Affordable Care Act enrollees are seeing premium increases of 114 percent in 2026, according to an analysis by KFF.

The higher premiums come amid broader increases in U.S. healthcare costs, which are also pushing up deductibles and other out-of-pocket expenses.

Some enrollees are absorbing the added burden. Stan Clawson, a 49-year-old freelance filmmaker and adjunct professor in Salt Lake City, said his monthly premium will rise from just under US$350 to nearly $500. Clawson, who lives with paralysis from a spinal cord injury, said the increase is painful but unavoidable.

Others face far steeper hikes. The Provost said her premium is jumping from $85 a month to nearly $750.

Enrollment Fallout Still Uncertain

Health policy experts warn that higher premiums could lead many people — particularly younger and healthier enrollees — to abandon coverage, raising costs further for those who remain insured.

An analysis by the Urban Institute and the Commonwealth Fund last September projected that about 4.8 million Americans could lose coverage in 2026 due to the expiration of subsidies.

However, enrollment effects remain uncertain, as the deadline to select or change plans runs through Jan. 15 in most states.

Provost said she is hoping Congress revives the subsidies early this year. If not, she plans to drop her own coverage and keep insurance only for her four-year-old daughter.

Political Stalemate Continues

In December, the Senate rejected competing partisan proposals — a Democratic plan to extend the subsidies for three years and a Republican alternative centered on health savings accounts. In the House, four centrist Republicans joined Democrats to push for a vote on a three-year extension, though prospects for passage remain unclear.

For many Americans, the impasse feels detached from everyday realities.

“Both Republicans and Democrats have been saying for years, oh, we need to fix it. Then do it,” said Chad Bruns, a 58-year-old Affordable Care Act enrollee in Wisconsin. “They need to get to the root cause, and no political party ever does that.”

[ad_2]

[ad_1]

From the passage of a massive bill that reduced federal funds for Medicaid to a comprehensive overhaul of a federal vaccine advisory panel, Congress and the Trump administration delivered major changes to America’s public health system in 2025.

Many of those changes are poised to reshape coverage, care delivery and public health policy in the new year as provisions take effect, healthcare premiums more than double, and new requirements begin to kick in.

Here’s a look at the biggest policy shifts set in motion last year that should be felt in the new year:

Premium tax credits meant to further reduce the price of healthcare plans bought on the Affordable Care Act marketplace expired on Dec. 31 after Congress declined to address a looming “subsidy cliff.”

The credits increased financial assistance and expanded it to those with incomes above 400% of the federal poverty lines. Since the credits were first introduced in 2021, enrollment in the ACA marketplace increased to more than 24 million.

The Center on Budget and Policy Priorities projected that almost 22 million people would see their healthcare costs “dramatically rise” or would lose their coverage altogether without the extension. The Urban Institute estimated that 7.3 million fewer Americans would receive subsidized coverage in 2026 and that 4.8 million more would be uninsured in 2026.

The American Rescue Plan Act of 2021 offered a temporary financial incentive to encourage states to expand Medicaid coverage to more low-income Americans. The act used the 138% poverty level listed in the Affordable Care Act to offer states a two-year, 5% match to the Federal Medical Assistance Percentage, the amount the federal government shoulders, for Medicaid expansion expenditures.

But the incentive will largely end as it currently exists due to the legislation known as the “big, beautiful bill.” States wishing to qualify for the enhanced funding must have completely expanded their Medicaid programs by Jan. 1. States that have already expanded their programs will retain their existing FMAP levels, and those receiving the two-year bonus will continue to receive it until the period ends.

For ACA marketplace enrollees, their premium tax credits are determined based on what they estimate their income will be at the beginning of the year. If the prediction is incorrect and the income is higher than expected, they are expected to repay. The process of repayment to the IRS is known as reconciliation and was expected to be undertaken when enrollees filed their federal income tax returns.

Now, under a provision of the “big, beautiful bill,” marketplace enrollees will be expected to repay the full amount they owe. Also, the continuous special enrollment period for people whose incomes are below 150% of the federal poverty line will end. In addition, those enrolling in coverage during a special enrollment period based on their income and not tied to a qualifying life event will not be eligible for the credits beginning this year.

The “big, beautiful bill” also included changes to the eligibility requirements for people who are not citizens who wish to receive ACA marketplace premium credits.

Credits will be limited to green-card holders, Cuban or Haitian entrants, or Compact of Free Association migrants or citizens of the Marshall Islands, Palau or Micronesia. Previously eligible categories, like refugees, asylum-seekers and those granted temporary protected status, will no longer qualify.

The bill also ends a special rule known as the Medicaid waiting list loophole. The rule allowed people who are not citizens whose incomes are below 100% of the federal poverty line and who are ineligible for Medicaid coverage due to their status to receive the premium credits.

The changes are expected to take effect Jan. 1.

The “big, beautiful bill” also caps the amount medical students can receive in Federal Direct Stafford Loans and Federal Direct PLUS Loans.

The changes will take effect on July 1.

Sign Up for U.S. News Healthcare of Tomorrow Bulletin

Your trusted source for critical insights and solutions-focused analysis.

Sign up to receive the latest updates from U.S. News & World Report and our trusted partners and sponsors. By clicking submit, you are agreeing to our Terms and Conditions & Privacy Policy.

The Department of Health and Human Services is expected to continue its overhaul of vaccine recommendations in the new year, starting with the schedule of recommended vaccines for children. The proposed new schedule will recommend fewer shots to mimic those from other developed countries, specifically Denmark. CNN reported that the plan has not been finalized but was expected in late December before it was pushed to 2026.In addition, the Centers for Disease Control and Prevention’s vaccine advisory panel is set to meet three times in the new year: Feb. 25-26, June 24-25 and Oct. 21-22.

[ad_2]

Aneeta Mathur-Ashton

Source link

[ad_1]

Maryland Rep. Glenn Ivey believes that Republicans will have to address the elimination of the Affordable Care Act tax subsidies with health care premiums rising.

Millions of Americans are entering the new year with far more expensive health insurance premiums. WTOP’s Sarah Jacobs reports Maryland Rep. Glenn Ivey predicts a health care fix early in the new year.

With the expiration of the Affordable Care Act tax subsidies, millions of Americans are entering the new year with far more expensive health insurance premiums.

Maryland Rep. Glenn Ivey said he believes this issue has fractured the Republican coalition in Congress.

“The health care fight that came out of the government shutdown has been a real sign,” said Ivey, a Democrat who represents Maryland’s 4th District. “I think there’s a lot of cracks, not only in the Trump administration, but the Republican caucuses in the Senate and the House”

In December, four Republicans broke from House Speaker Mike Johnson and signed a petition, led by Democrats, that would force a House vote on extending an enhanced pandemic-era subsidy for three years that lowers health insurance.

It came in the aftermath of House Republican leaders rushing to pass a health care bill that didn’t address the rising monthly premiums.

“I think that Republicans have dug a very deep hole for themselves with the way they’ve mishandled Americans health care, especially with respect to their refusal to extend the tax credits for the Affordable Care Act so that people can afford to continue to have insurance,” Ivey said.

Ivey expects that Democrats will force Republicans to address the elimination of the Affordable Care Act tax subsidies in the next 30 days.

“I think we’re going to force them to do something to address the elimination of the Obamacare tax credits so that people don’t see their premiums double and triple,” Ivey said.

Ivey is also predicting Democrats will retake the House in 2026 and possibly the Senate.

“Because he can’t be counted on to do it himself, the only way to keep him in check is to have counterweights to him and Republicans in Congress are not willing to do it,” he said. “It’s got to be Democrats that do it.”

WTOP’s Tadiwos Abedje contributed to this report.

[ad_2]

Sarah Jacobs

Source link

[ad_1]

Enhanced tax credits that have helped reduce the cost of health insurance for the vast majority of Affordable Care Act enrollees expired overnight as 2026 arrived, cementing higher health costs for millions of Americans at the start of the new year.

Democrats forced a 43-day government shutdown over the issue. Moderate Republicans called for a solution to save their 2026 political aspirations. President Trump floated a way out, only to back off after conservative backlash.

In the end, no one’s efforts were enough to save the subsidies before their expiration date. A House vote expected in January could offer another chance, but success is far from guaranteed.

The change affects a diverse cross-section of Americans who don’t get their health insurance from an employer and don’t qualify for Medicaid or Medicare — a group that includes many self-employed workers, small business owners, farmers and ranchers.

It comes at the start of a high-stakes midterm election year, with affordability — including the cost of health care — topping the list of voters’ concerns.

“It really bothers me that the middle class has moved from a squeeze to a full suffocation, and they continue to just pile on and leave it up to us,” said 37-year-old single mom Katelin Provost, whose health care costs are set to jump. “I’m incredibly disappointed that there hasn’t been more action.”

The expired subsidies were first given to Affordable Care Act enrollees in 2021 as a temporary measure to help Americans get through the COVID-19 pandemic. Democrats in power at the time extended them, moving the expiration date to the start of 2026.

With the expanded subsidies, some lower-income enrollees received health care with no premiums, and high earners paid no more than 8.5% of their income. Eligibility for middle-class earners was also expanded.

On average, the more than 20 million subsidized enrollees in the Affordable Care Act program are seeing their premium costs rise by 114% in 2026, according to an analysis by the health care research nonprofit KFF.

Those surging prices come alongside an overall increase in health costs in the U.S., which are further driving up out-of-pocket costs in many plans.

Some enrollees, like Salt Lake City freelance filmmaker and adjunct professor Stan Clawson, have absorbed the extra expense. Clawson said he was paying just under $350 a month for his premiums last year, a number that will jump to nearly $500 a month this year. It’s a strain for the 49-year-old but one he’s willing to take on because he needs health insurance as someone who lives with paralysis from a spinal cord injury.

Others, like Provost, are dealing with steeper hikes. The social worker’s monthly premium payment is increasing from $85 a month to nearly $750.

Lori Hunt of Des Moines, Iowa, spoke with CBS News during the congressional stalemate in October and said she “couldn’t afford” health insurance without the subsidies.

“I’d have to cancel my insurance,” Hunt said, joking that her insurance would consist of “thoughts and prayers.”

Hunt survived breast cancer three years ago and was laid off from her job in 2025. Without the subsidies, she expected her ACA premium would jump to about $700 per month. “It would be more than my mortgage payment,” Hunt said.

Health analysts have predicted the expiration of the subsidies will drive many of the 24 million total Affordable Care Act enrollees — especially younger and healthier Americans — to forgo health insurance coverage altogether.

Over time, that could make the program more expensive for the older, sicker population that remains.

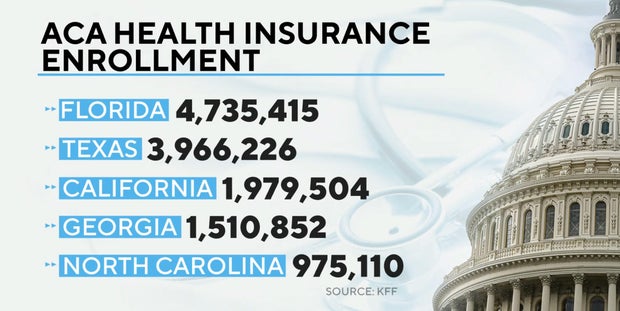

An analysis conducted last September by the Urban Institute and Commonwealth Fund projected the higher premiums from expiring subsidies would prompt some 4.8 million Americans to drop coverage in 2026.

The impact could be greatest in Florida, which has the largest number of ACA enrollees of any state — more than 4.7 million, according to KFF data. Texas is next, with more than 3.9 million, followed by California, Georgia and North Carolina.

KFF Data/CBS News

Kylie Barrios, a 30-year-old Florida resident, said she expected to be among those losing coverage.

“Our health insurance premium is effectively tripling from 2025 to 2026,” she told CBS News in December, saying it would rise from about $900 to $2,500.

Provost, the single mother, said she is holding out hope that Congress finds a way to revive the subsidies early in the year — but if not, she’ll drop herself off the insurance and keep it only for her 4-year-old daughter. She can’t afford to pay for both of their coverage at the current price.

But with the window to select and change plans still ongoing until Jan. 15 in most states, the final effect on enrollment is yet to be determined.

Last year, after Republicans cut more than $1 trillion in federal health care and food assistance with Mr. Trump’s big tax and spending cuts bill, Democrats repeatedly called for the subsidies to be extended. But while some Republicans in power acknowledged the issue needed to be addressed, they refused to put it to a vote until late in the year.

In December, the Senate rejected two partisan health care bills — a Democratic pitch to extend the subsidies for three more years and a Republican alternative that would instead provide Americans with health savings accounts.

In the House, four centrist Republicans broke with GOP leadership and joined forces with Democrats to force a vote that could come as soon as January on a three-year extension of the tax credits. But with the Senate already having rejected such a plan, it’s unclear whether it could get enough momentum to pass.

Meanwhile, Americans whose premiums are skyrocketing say lawmakers don’t understand what it’s really like to struggle to get by as health costs ratchet up with no relief.

Many say they want the subsidies restored alongside broader reforms to make health care more affordable for all Americans.

“Both Republicans and Democrats have been saying for years, oh, we need to fix it. Then do it,” said Chad Bruns, a 58-year-old Affordable Care Act enrollee in Wisconsin. “They need to get to the root cause, and no political party ever does that.”

Barrios, who said she has generally voted Republican, said she would like politicians to “act on those values that they … claim to protect.”

“The whole system feels as though it’s failed and isn’t advocating for me as a small business owner, as somebody who wants to become a mom and have a family,” she said.

[ad_2]

[ad_1]

The cost of health insurance is set to surge for millions of Americans under the Affordable Care Act at the start of the new year without the extension of expanded tax credits.The expanded subsidies were at the center of the 42-day government shutdown that ended in November. Now just days away from the new year, premiums are set to increase without an extension or resolution from Congress.The Get the Facts Data Team analyzed and aggregated statistics to know ahead of the rise in premiums in the new year.Premiums could rise on average 114%Premiums would more than double if the tax subsidies were to expire, according to an analysis from KFF. In addition to the potential ending of the subsidies, insurance rates are projected to rise across marketplace plans and employer-provided insurance.A one-person household with an annual income of $25,000 – a little more than 1.5 times the federal poverty level – is estimated to go from paying a maximum $100 out of pocket annually to $1,168.They would pay a maximum of less than $98 a month — 10 times more than the previous payment of less than $9 a month.The interactive below shows how the maximum out-of-pocket rates for benchmark plans may change if expanded subsidies expire for one, two and four-person households at various incomes. Estimates were calculated using maximum out-of-pocket rates from KFF published by the IRS, along with 2025 federal poverty level data from the U.S. Department of Health and Human Services for the 48 contiguous states plus D.C.The tool is not intended to calculate an individual’s actual payments. Healthcare.gov and other state marketplaces are the best source for specific premium costs.People closer to retirement age or with higher incomes could see the largest impactOnce the expanded tax credits expire at the end of this year, the out-of-pocket maximums will increase across the board, and people making above four times the poverty level will become ineligible for any tax credits.More than 6.7% of those who were enrolled in ACA plans earned more than 400% of the federal poverty level, accounting for 1.6 million people. Once the subsidies expire, these enrollees would no longer qualify for the subsidies under the ACA.Also heavily impacted are people approaching retirement age. The age group with the highest enrollment in marketplace plans is ages 55 to 64, data shows.KFF estimated in March that about half the enrollees who would lose the tax credit upon expiration are between 50 and 64.Premiums for individuals closer to retirement age and making more than 400% of the federal poverty level would also increase more compared to younger enrollees. Take a 30-year-old, a 45-year-old, and a 60-year-old earning $62,756 in a single household – 401% of the poverty level.Without the tax credits, the 30-year-old would see a $110 jump in the monthly premium for a silver plan, according to KFF’s ACA Enhanced Premium Tax Credit calculator. The 60-year-old would see an $881-per-month increase without the enhanced subsidies.24 million people are enrolled in plans under the Affordable Care ActThe subsidies are utilized by about 92% of the 24 million people enrolled in marketplace plans under the ACA, according to data from the Centers for Medicare & Medicaid Services.These expanded credits allow households of different sizes and income levels to be capped with maximum out-of-pocket costs.From 2020 to 2025, enrollment more than doubled as a result of expanded tax credits in the American Rescue Plan Act in 2021, which increased the subsidies and lifted a cap that disqualified people making four times the poverty level or more from being eligible for the subsidies.Under 2025 guidelines for the 48 contiguous states and Washington, D.C., the federal poverty level is $15,650 for a one-person household. At 400%, it’s $62,600.Six states have more than tripled in ACA enrollees since 2020There was a widespread increase in enrollment across states in the past five years.The six states that have more than tripled in enrollees since 2020 are Georgia, Louisiana, Mississippi, Tennessee, Texas and West Virginia. There were 14 states that more than doubled in enrollment. Just three places — including Washington, D.C. — declined in enrollment, according to data from the Centers for Medicare and Medicaid Services.Expired subsidies take effect Jan. 1Even though new insurance premiums would take effect in the new year, a retroactive extension could be passed in 2026.However, it would be complicated and would continue to grow more complicated over time, according to KFF. More enrollees may drop insurance in the meantime. In a KFF survey, a quarter of enrollees indicated they would go without health insurance if the cost of current coverage doubled. About a third said they’d look for a lower premium plan.PHNjcmlwdCB0eXBlPSJ0ZXh0L2phdmFzY3JpcHQiPiFmdW5jdGlvbigpeyJ1c2Ugc3RyaWN0Ijt3aW5kb3cuYWRkRXZlbnRMaXN0ZW5lcigibWVzc2FnZSIsKGZ1bmN0aW9uKGUpe2lmKHZvaWQgMCE9PWUuZGF0YVsiZGF0YXdyYXBwZXItaGVpZ2h0Il0pe3ZhciB0PWRvY3VtZW50LnF1ZXJ5U2VsZWN0b3JBbGwoImlmcmFtZSIpO2Zvcih2YXIgYSBpbiBlLmRhdGFbImRhdGF3cmFwcGVyLWhlaWdodCJdKWZvcih2YXIgcj0wO3I8dC5sZW5ndGg7cisrKXtpZih0W3JdLmNvbnRlbnRXaW5kb3c9PT1lLnNvdXJjZSl0W3JdLnN0eWxlLmhlaWdodD1lLmRhdGFbImRhdGF3cmFwcGVyLWhlaWdodCJdW2FdKyJweCJ9fX0pKX0oKTs8L3NjcmlwdD4=

The cost of health insurance is set to surge for millions of Americans under the Affordable Care Act at the start of the new year without the extension of expanded tax credits.

The expanded subsidies were at the center of the 42-day government shutdown that ended in November. Now just days away from the new year, premiums are set to increase without an extension or resolution from Congress.

The Get the Facts Data Team analyzed and aggregated statistics to know ahead of the rise in premiums in the new year.

Premiums would more than double if the tax subsidies were to expire, according to an analysis from KFF.

In addition to the potential ending of the subsidies, insurance rates are projected to rise across marketplace plans and employer-provided insurance.

A one-person household with an annual income of $25,000 – a little more than 1.5 times the federal poverty level – is estimated to go from paying a maximum $100 out of pocket annually to $1,168.

They would pay a maximum of less than $98 a month — 10 times more than the previous payment of less than $9 a month.

The interactive below shows how the maximum out-of-pocket rates for benchmark plans may change if expanded subsidies expire for one, two and four-person households at various incomes. Estimates were calculated using maximum out-of-pocket rates from KFF published by the IRS, along with 2025 federal poverty level data from the U.S. Department of Health and Human Services for the 48 contiguous states plus D.C.

The tool is not intended to calculate an individual’s actual payments. Healthcare.gov and other state marketplaces are the best source for specific premium costs.

Once the expanded tax credits expire at the end of this year, the out-of-pocket maximums will increase across the board, and people making above four times the poverty level will become ineligible for any tax credits.

More than 6.7% of those who were enrolled in ACA plans earned more than 400% of the federal poverty level, accounting for 1.6 million people. Once the subsidies expire, these enrollees would no longer qualify for the subsidies under the ACA.

Also heavily impacted are people approaching retirement age. The age group with the highest enrollment in marketplace plans is ages 55 to 64, data shows.

KFF estimated in March that about half the enrollees who would lose the tax credit upon expiration are between 50 and 64.

Premiums for individuals closer to retirement age and making more than 400% of the federal poverty level would also increase more compared to younger enrollees. Take a 30-year-old, a 45-year-old, and a 60-year-old earning $62,756 in a single household – 401% of the poverty level.

Without the tax credits, the 30-year-old would see a $110 jump in the monthly premium for a silver plan, according to KFF’s ACA Enhanced Premium Tax Credit calculator.

The 60-year-old would see an $881-per-month increase without the enhanced subsidies.

The subsidies are utilized by about 92% of the 24 million people enrolled in marketplace plans under the ACA, according to data from the Centers for Medicare & Medicaid Services.

These expanded credits allow households of different sizes and income levels to be capped with maximum out-of-pocket costs.

From 2020 to 2025, enrollment more than doubled as a result of expanded tax credits in the American Rescue Plan Act in 2021, which increased the subsidies and lifted a cap that disqualified people making four times the poverty level or more from being eligible for the subsidies.

Under 2025 guidelines for the 48 contiguous states and Washington, D.C., the federal poverty level is $15,650 for a one-person household. At 400%, it’s $62,600.

There was a widespread increase in enrollment across states in the past five years.

The six states that have more than tripled in enrollees since 2020 are Georgia, Louisiana, Mississippi, Tennessee, Texas and West Virginia. There were 14 states that more than doubled in enrollment.

Just three places — including Washington, D.C. — declined in enrollment, according to data from the Centers for Medicare and Medicaid Services.

Even though new insurance premiums would take effect in the new year, a retroactive extension could be passed in 2026.

However, it would be complicated and would continue to grow more complicated over time, according to KFF.

More enrollees may drop insurance in the meantime. In a KFF survey, a quarter of enrollees indicated they would go without health insurance if the cost of current coverage doubled. About a third said they’d look for a lower premium plan.

[ad_2]

[ad_1]

(CNN) — When patients come to Eric Frankenfeld’s chiropractic practice with insurance woes, his wife, Lisa, the office manager, tells them not to worry because she’ll work with them to keep care affordable.

But starting in January, the Frankenfelds might need to ask for the same treatment from their own doctors, since they will become uninsured. The Point Pleasant, New Jersey, couple will no longer be able to afford their Obamacare plan after the enhanced premiums subsidies lapse at year’s end. They decided to forgo coverage after learning that their plan’s premium will skyrocket to $1,928 a month, up from $340 this year.

Though they are both healthy, the idea of losing coverage keeps Lisa Frankenfeld, 62, up at night — worrying one of them might be diagnosed with cancer, suffer a stroke or heart attack or get into a serious accident.

“We are health care providers who cannot afford benefits. Oh, the irony,” she told CNN. “Purchasing a plan doesn’t make financial sense. We’re just going to cross our fingers and hope for the best.”

The Frankenfelds are among the millions of Affordable Care Act enrollees who are facing tough decisions this open enrollment season, which ends January 15 in most states. More than 90% of ACA policyholders — or about 22 million people — receive the enhanced subsidies, which spurred record sign-ups for Obamacare coverage this year.

A sizeable share of those enrollees are self-employed or own or work at small businesses. Nearly half of adults in the individual health insurance market — the vast majority of which is purchased through Obamacare exchanges — are affiliated with a small business, according to KFF, a nonpartisan health policy research group.

Employer policies are often too pricey for small businesses and for those who work for themselves, leading many to turn to the Affordable Care Act exchanges. And even though several told CNN their Obamacare coverage requires they spend a lot out of pocket for care, they say it’s still better than being uninsured.

However, without the enhanced subsidies, which were enacted by the Biden administration as part of a 2021 Covid-19 relief package, enrollees’ premium payments are expected to jump 114%, on average, next year. The provision’s lapse also means that consumers who make more than 400% of the federal poverty level — about $62,600 for an individual and $84,600 for a couple — will no longer qualify for any federal aid.

The House is set to vote in January on extending the beefed-up assistance for three years after four Republicans bucked their caucus and supported a Democratic proposal. But the measure faces a difficult path in the Senate, which voted down a similar Democratic bill earlier this month.

Increasingly squeezed by the rising cost of electricity, groceries, personal and business insurance and supplies for their garage door installation and repair company, Kathy and Jeffrey Many of Brandon, Vermont, decided not to renew their Affordable Care Act coverage for 2026. The premium for their plan is shooting up to nearly $2,670 a month, from $625 this year. The cheapest one they could find is nearly $1,870 a month.

Although the couple had high out-of-pocket costs for care, their Obamacare policy gave them peace of mind in case one of them had to deal with a major illness or accident, Kathy Many told CNN. Being uninsured next year will be “very nerve-wracking,” she said.

“Every time Jeffrey leaves to go out on a job, I’m going to be like ‘Jesus Christ, I hope nothing happens to him today,’” said Many, 61, her voice breaking, “because everything that I’ve worked my whole life for could be lost to bankruptcy.”

Instead of having health insurance, Many plans to sock away the $625 a month they were paying this year and “pray” that it will cover their health care expenses until her husband enrolls in Medicare in the fall and she qualifies in 2029.

A lot of enrollees have been waiting to explore their Obamacare options because they didn’t want to learn how much they would have to pay for coverage come January.

Jeff , a freelance musician from New York City who earns so little that he did not have to pay a premium this year and last year, waited until mid-December to sign onto his state’s exchange. When he saw the cheapest plan for 2026 would cost him $275 a month, he closed his laptop since he knew he couldn’t afford it and would become uninsured. Instead, he went back to searching for a gig to replace one he just lost.

The fact that Republicans in Congress are not renewing the enhanced subsidies infuriates Jeff, 50, a registered Democrat who asked that his last name not be used to protect his privacy.

“We can find money to build an arch and a ballroom that are completely unnecessary and tax cuts for billionaires,” he said, referencing President Donald Trump’s construction plans and the GOP domestic agenda package that passed this summer. “But we can’t insure people medically in this country. It’s unconscionable.”

Some small-business owners, however, can’t afford to go without health insurance because they have medical conditions and need care. The spike in premiums is forcing them to consider big decisions.

Sonja, who owns several real estate businesses with her husband, said they are looking into joining with another company in the hope that they can obtain group health insurance with lower premiums if they have a larger workforce. She asked not to include her last name to protect her and her business’ privacy.

The Minnesota couple will have to shell out more than $2,150 a month next year to cover themselves and their daughter, up from roughly $1,000 this year. Sonja, 49, is not willing to go without insurance, especially after her husband had to have surgery this year, though the higher premiums might force them to sell part of their holdings or stop saving for retirement.

“In the event that we would have a major health issue, paying for insurance would be a much better spend than being uncovered and opening ourselves to the potential of losing way more,” she said.

[ad_2]

Tami Luhby and CNN

Source link

[ad_1]

Millions of Americans are bracing for higher health costs in 2026, as subsidies that help them pay for health insurance under the Affordable Care Act are set to expire on December 31.

Experts warn that a failure in Congress to extend the tax credits could be financially devastating for individual policyholders, while also raising health care costs as a whole. Roughly 22 million Americans receive the ACA subsidies, which were created in 2021 to lower households’ monthly premiums.

New data from investment adviser SmartAsset projects how much people around the U.S. with an ACA plan would have paid on average for coverage in 2025 if they hadn’t received the enhanced subsidies. As the analysis shows, monthly premiums for the government health insurance would’ve been hundreds of dollars higher.

In Mississippi, where around 11% of residents are enrolled in an ACA plan, participants would have seen their average monthly premiums jump from $41 to $605, a 1,376% increase, SmartAsset found. In West Virginia, enrollees’ premiums would have risen an average of 1,058%.

A spokesperson for SmartAsset said the analysis captures 2025 costs, but noted the data amounts to a “close approximation” of how much more people with ACA coverage could expect to pay next year without the tax credits.

SmartAsset used public records from the Centers for Medicare and Medicaid Services’ 2025 Marketplace Open Enrollment Period to calculate the average cost of ACA plans.

The exact price hikes people could see next will depend on a range of factors, including their insurance plan, age, household income, health status and where they live, according to a spokesperson from KFF. The health policy group estimates that annual out-of-pocket premium costs will increase 114% on average for the 22 million ACA enrollees who rely on the subsidies.

The tax credits are set to lapse at the end of the year. Democratic lawmakers have pushed for an extension but lack enough support in the Republican-led Congress. And while the House passed a health care bill this week that includes several policies favored by Republicans, it excludes an extension of the tax credits and faces hurdles in the Senate.

Both chambers of Congress have left Washington until early next year, making it all but certain that the tax credits will expire on December 31. But four GOP members this week signed a Democratic measure to force a vote on extending the subsidies for three years, teeing up a final vote early next year.

If Congress fails to solve the tax credit issue, some enrollees will qualify for a smaller subsidy, while others could lose eligibility completely, according to KFF.

With sharply higher ACA costs on the horizon, the Congressional Budget Office estimates that about 4 million people could drop their health insurance altogether. Experts say that could lead to higher costs for people with other types of health insurance because hospitals will have to provide more uncompensated care for those lacking coverage.

“Hospitals can only reconcile that by raising their prices for everybody,” Emma Wager, a senior policy analyst at KFF, told CBS News last week.

[ad_2]

[ad_1]

Folks, who was supposed to be watching grandpa last night? Because he got out, got on TV and … It. Was. Not. Good.

For 18 long minutes Wednesday evening, we were subjected to a rant by President Trump that predictably careened from immigrants (bad) to jobs (good), rarely slowing down for reality. But jumbled between the vitriol and venom was a vision of American healthcare that would have horror villainess M3GAN shaking in her Mary Janes — a vision that we all should be afraid of because it would take us back to a dark era when insurance couldn’t be counted on.

Trump’s remarks offered only a sketchy outline, per usual, in which the costs of health insurance premiums may be lower — but it will be because the coverage is terrible. Yes, you’ll save money. But so what? A cheap car without wheels is not a deal.

“The money should go to the people,” Trump said of his sort-of plan.

The money he vaguely was alluding to is the government subsidies that make insurance under the Affordable Care Act affordable. After antics and a mini-rebellion by four Republicans also on Wednesday, Congress basically failed to do anything meaningful on healthcare — pretty much ensuring those subsidies will disappear with the New Year.

Starting in January, premiums for too many people are going to leap skyward without the subsidies, jumping by an average of $1,016 according to the health policy research group KFF.

That’s bad enough. But Trump would like to make it worse.

The Affordable Care Act is about much more than those subsidies. Before it took effect in 2014, insurance companies in many states could deny coverage for preexisting conditions. This didn’t have to be big-ticket stuff like cancer. A kid with asthma? A mom with colitis? Those were the kind of routine but chronic problems that prevented millions from obtaining insurance — and therefore care.

Obamacare required that policies sold on its exchange did not discriminate. In addition, the ACA required plans to limit out-of-pocket costs and end lifetime dollar caps, and provide a baseline of coverage that included essentials such as maternity care. Those standards put pressure on all plans to include more, even those offered through large employers.

Trump would like to undo much of that. He instead wants to fall back on the stunt he loves the most — send a check!

What he is suggesting by sending subsidy money directly to consumers also most likely would open the market to plans without the regulation of the ACA. So yes, small businesses or even groups of individuals might be able to band together to buy insurance, but there likely would be fewer rules about what — or whom — it has to cover.

Most people aren’t savvy or careful enough to understand the limitations of their insurance before it matters. So it has a $2-million lifetime cap? That sounds like a lot until your kid needs a treatment that eats through that in a couple of months. Then what?

Trump suggested people pay for it themselves, out of health savings accounts funded by that subsidy check sent directly to taxpayers. Because that definitely will work, and people won’t spend the money on groceries or rent, and what they do save certainly will cover any medical expenses.

“You’ll get much better healthcare at a much lower price,” Trump claimed Wednesday. “The only losers will be insurance companies that have gotten rich, and the Democrat Party, which is totally controlled by those same insurance companies. They will not be happy, but that’s OK with me because you, the people, are finally going to be getting great healthcare at a lower cost.”

He then bizarrely tried to blame the expiring subsidies on Democrats.

Democrats “are demanding those increases and it’s their fault,” he said. “It is not the Republicans’ fault. It’s the Democrats’ fault. It’s the Unaffordable Care Act, and everybody knew it.”

It seems like Trump just wants to lower costs at the expense of quality. Here’s where I take issue with the Democrats. I am not here to defend insurance companies or our healthcare system. Both clearly need reform.

But why are the Democrats failing to explain what “The money should go to the people” will mean?

I get that affordability is the message, and as someone who bought both a steak and a carton of milk this week, I understand just how powerful that issue is.

Still, everyone, Democrat or Republican, wants decent healthcare they can afford, and the peace of mind of knowing if something terrible happens, they will have access to help. There is no American who gladly would pay for insurance each month, no matter how low the premium, that is going to leave them without care when they or their loved ones need it most.

Grandpa Trump doesn’t have this worry, since he has the best healthcare our tax dollars can buy.

But when he promises to send a check instead of providing governance and regulation of one of the most critical purchases in our lives, the message is sickening: My victory in exchange for your well-being.

[ad_2]

Anita Chabria

Source link

[ad_1]

Submit your letter to the editor via this form. Read more Letters to the Editor.

Re: “Judge closes case for former officer” (Page A1, Dec. 13).

The appointed Alameda County District Attorney, Ursula Jones Dickson, was the endorsed candidate of the Pamela Price recall committee, which promised to end the alleged coddling of criminals. Indeed, Jones Dickson promises justice by prosecuting more children as adults and sending them to adult prisons.

Now, though, she has finally found a judge to drop manslaughter charges against the killer of Steven Taylor, former San Leandro cop Jason Fletcher. This despite then-District Attorney Nancy O’Malley’s Probable Cause Declaration that when he was shot after being tased twice, “Mr. Taylor was struggling to remain standing as he pointed the bat at the ground …” and “posed no threat of imminent deadly force or serious bodily injury to defendant Fletcher or anyone else.” Jones Dickson considers dropping the charges justice.

I would like a district attorney who has only one standard of justice.

Bob Britton

Castro Valley

Re: “Oakland surrenders in ‘coal war’ battle” (Page A1, Dec. 11).

Anyone who truly cares about future generations and acknowledges the impacts of climate change and the health risks of coal-related particulate pollution can’t in their right mind want to locally handle, ship and ultimately facilitate the burning of several million tons of coal annually.

If Oakland Bulk & Oversized Terminal LLC and its partners intend to develop their export terminal for coal, then they should build the specialized, enclosed, dome-shaped terminal they had said they would build to address coal dust health concerns — dust that could harm port workers and nearby residents.

The best outcome would be building a bulk terminal to export hundreds of commodities, excluding coal. If there’s still an option to stop coal as an export commodity here by gathering additional environmental health information, then that pathway should be pursued.

Dan Kalb

Oakland

As your family gathers for the holidays, ask about your family’s health history. Knowing your family’s health history can be key to a longer, healthier life. And it can help your health care provider identify traits that may put you at risk for certain health conditions or diseases.

Talk to immediate family members. Include three generations. Grandparents, parents, siblings, aunts, uncles, nieces and nephews may all have helpful information. Gather information about major medical conditions, age of onset, and for deceased relatives, causes of death. If you have a family history of a condition, it’s important to know this. While you can’t change your genetic makeup, there may be steps you can take now that could help you stay healthy.

Felicia Ziomek

Livermore

Our Congress wants health care for all Americans. We all want health care for all Americans. But let’s do it the right way. The current Obamacare program is not sustainable. Replete with the fraud, waste and corruption that has been uncovered — finally — it is obvious that it is costing far more than it should. Extending the existing subsidies without improving the program and its controls is simply throwing good money after bad.

Let’s get control of the current program, drive out the fraud, waste and corruption, so we can see what the existing program would cost if managed properly. Then we can determine how much we can afford to spend and design a well-controlled program that meets our needs. Extending the current payouts without controlling whether the money is spent appropriately, although easier, is simply irresponsible.

John Griggs

Danville

Why has Secretary of Defense Pete Hegseth ordered our largest, most lethal aircraft carrier with supporting destroyers and guided missile ships to sail near Venezuela? Donald Trump says it’s to stop drug traffickers, yet, at the same time, he released from prison the Honduran ex-president, who was convicted of massive cocaine trafficking into our country.

The aircraft carrier was moved from the eastern Mediterranean, near the Ukraine conflict. Trump seems to be abandoning our allies in Europe, giving Russia the opportunity to expand its war-stolen territory in Ukraine, while at the same time, he’s picking a fight in our hemisphere with fishermen in small boats.

Is the “emperor” crazy? Are his true loyalties toward aggressive dictators like Vladimir Putin? Americans need to know.

China is watching us closely and assessing whether we would defend Taiwan, Japan and Korea if they pulled a “Putin” in the western Pacific.

Bruce Joffe

Piedmont

[ad_2]

Letters To The Editor

Source link

[ad_1]

BOSTON — Democratic Gov. Maura Healey is renewing calls for Congress to extend Obamacare tax credits, warning that health care premiums for tens of thousands of Bay Staters will skyrocket without legislative action.

The U.S. Senate was expected to vote earlier this week on a Democratic proposal to extend the premium tax credits implemented during the COVID-19 pandemic and Healey is urging congressional Republicans and President Donald Trump to support the plan.

kAm“q642FD6 :7 E96J 5@?’E[ A6@A=6 2C6 8@:?8 E@ DF776C[” w62=6J E@=5 C6A@CE6CD 2E 2 3C:67:?8 %F6D52J] “!6@A=6 2C6 8@:?8 E@ 8@ H:E9@FE 42C6] xE’D E@E2==J F?277@C523=6[ :E’D E@E2==J F?2446AE23=6[ 2?5 :E ;FDE 5@6D?’E ?665 E@ 36]”k^Am

kAmw62=E9 :?DFC2?46 AC6>:F>D 7@C 2? 6DE:>2E65 ac >:==:@? p>6C:42?D H9@ C646:G6 E96:C 4@G6C286 E9C@F89 E96 p77@C523=6 r2C6 p4E[ 2=D@ 242C6[ 2C6 5F6 E@ C:D6 3J 5@F3=6 5:8:ED ?6IE J62C 23D6?E 4@?8C6DD:@?2= 24E:@? E@ 6IE6?5 E96 DF3D:5:6D]k^Am

kAm$6?2E6 s6>@4C2ED 92G6 7:=65 2 AC@A@D2= E92E H@F=5 6IE6?5 E96 E2I 4C65:ED 7@C E96 ?6IE E9C66 J62CD H:E9@FE >2;@C 492?86D] p G@E6 H2D 6IA64E65 %9FCD52J] qFE #6AF3=:42?D H9@ 4@?EC@= E96 492>36C C6;64E65 E96 AC@A@D2=]k^Am

kAm%96 $6?2E6 😀 E@ 2=D@ 4@?D:56C 2 v~! AC@A@D2= E@ C6A=246 962=E9 DF3D:5:6D F?56C E96 prp H:E9 D2G:?8D 244@F?ED E92E H@F=5 C646:G6 7656C2= 4@?EC:3FE:@?D E@ A2J @FE@7A@4<6E 6IA6?D6D] qFE >2?J s6>@4C2ED[ :?4=F5:?8 |2DD249FD6EED $6?D] t=:K236E9 (2CC6? 2?5 t5 |2C<6J[ 92G6 4C:E:4:K65 E96 #6AF3=:42? A=2?]k^Am

kAm|@C6 E92? bag[___ |2DD249FD6EED C6D:56?ED H9@ C646:G6 E96:C 962=E9 :?DFC2?46 E9C@F89 E96 7656C2= 6I492?86 92G6 C646:G65 ?@E:46D 23@FE E96:C AC6>:F>D 5@F3=:?8 – 😕 D@>6 42D6D EC:A=:?8 – ?6IE J62C 3642FD6 E96 E2I 4C65:ED 2C6 6IA:C:?8[ E96 w62=6J 25>:?:DEC2E:@? D2:5]k^Am

kAmpF5C6J v2DE6:6C[ 6I64FE:G6 5:C64E@C @7 E96 DE2E6 w62=E9 r@??64E@C[ D2:5 E96 DE2E6 42??@E 277@C5 E@ 7:== E96 82A 4C62E65 3J E96 6IA:C:?8 4C65:ED[ H9:49 H:== >62? 2 =@DD @7 >@C6 E92? Scad >:==:@? 😕 7656C2= 2DD:DE2?46 7@C A6@A=6 😕 |2DD249FD6EED E@ 96=A A2J 7@C E96:C 962=E9 42C6 4@G6C286]k^Am

kAm$@>6 72>:=:6D 4@F=5 D66 E96:C 4@G6C286 :?4C62D6 3J 2D >F49 2D S`_[___ 2 J62C[ D96 D2:5]k^Am

kAm#6?6H:?8 E96 6IA:C:?8 E2I 4C65:ED C6>2:?D 2 <6J 56>2?5 7C@> s6>@4C2ED[ H9@D6 AFD9 7@C 2 562= @? E96 DF3D:5:6D =6E E96> E@ 3=@4< 2 v~! DA6?5:?8 A=2? E@ <66A E96 8@G6C?>6?E CF??:?8[ C6DF=E:?8 😕 2 cb52J D9FE5@H?]k^Am

kAm%96 ?F>36C @7 prp 6?C@==66D 92D >@C6 E92? 5@F3=65 D:?46 a_a`[ =2C86=J 😕 A2CE 5F6 E@ DF3D:5:6D >256 2G2:=23=6 E9C@F89 E96 p>6C:42? #6D4F6 !=2? 2?5 E96 x?7=2E:@? #65F4E:@? p4E[ 3@E9 @7 H9:49 2C6 D6E E@ 6IA:C6 2E E96 6?5 @7 a_ad]k^Am

kAm#6AF3=:42?D 2C8F6 E92E E96 A2?56>:4 😀 @G6C 2?5 E92E E96 4@?E:?F65 7656C2= 962=E9 42C6 DF3D:5:6D 2C6 5C:G:?8 FA 4@DED 7@C E96 7656C2= 8@G6C?>6?E] %96J H2?E E@ E:89E6? prp DF3D:5J CF=6D 2D A2CE @7 3C@256C C67@C>D @7 7656C2= 962=E9 DA6?5:?8]k^Am

kAmk6>mr9C:DE:2? |] (256 4@G6CD E96 |2DD249FD6EED $E2E69@FD6 7@C }@CE9 @7 q@DE@? |65:2 vC@FAUCDBF@jD ?6HDA2A6CD 2?5 H63D:E6D] t>2:= 9:> 2E k2 9C67lQ>2:=E@i4H256o4?9:?6HD]4@>Qm4H256o4?9:?6HD]4@>k^2m]k^6>mk^Am

[ad_2]

By Christian M. Wade | Statehouse Reporter

Source link

[ad_1]

Washington — House Republican leaders unveiled a plan Friday to address health care costs ahead of a year-end lapse to tax credits that will result in skyrocketing premiums for more than 20 million Americans.

But the plan does not include an extension to the Affordable Care Act subsidies. Instead, Republican leaders will allow a vote on an amendment to the plan that would include an extension to those expiring tax credits, according to a GOP leadership aide.

The move is aimed at appeasing moderate Republicans who are trying to force votes, through what is known as a discharge petition, on separate pieces of legislation to extend the tax credits for one to two years with reforms.

An extension has split the party, with those opposed saying the subsidies are ripe with fraud and high-income households shouldn’t qualify.

Democrats have pushed a three-year extension without reforms — a nonstarter with Republicans.

The Republican plan released Friday includes a provision to expand association health plans, in which multiple employers band together to purchase coverage and lower the costs of benefits. Another provision would provide funding for cost-sharing reduction payments meant to lower premiums for some Affordable Care Act enrollees. The proposal would also require more transparency from pharmacy benefit managers in an effort to lower drug costs.

“While Democrats demand that taxpayers write bigger checks to insurance companies to hide the cost of their failed law, House Republicans are tackling the real drivers of health care costs to provide affordable care, increase access and choice, and restore integrity to our nation’s health care system for all Americans,” House Speaker Mike Johnson, a Louisiana Republican, said in a statement.

Johnson has been meeting with leaders of several factions of the conference this week to try to build a consensus on a plan.

The House Rules Committee is set to take up the package on Tuesday afternoon, teeing it up for a potential floor vote as soon as Tuesday evening or Wednesday.

It’s unclear whether it has enough support to survive a floor vote.

In a statement Friday night, House Minority Leader Hakeem Jeffries, a New York Democrat, called the GOP proposal an “11th hour measure” and said he would oppose it if the bill reaches the House floor.

“House Democrats will continue our fight to protect the healthcare of the American people. We are ready to work with anyone in good faith on the other side of the aisle who wants to prevent the Affordable Care Act tax credits from expiring at the end of the month,” Jeffries said. “Unfortunately, House Republicans have introduced toxic legislation that is completely unserious, hurts hardworking America taxpayers and is not designed to secure bipartisan support.”

[ad_2]

[ad_1]

Mahwah, New Jersey, resident Tina Jump recently learned that the premium for her Affordable Care Act health insurance is set to surge from about $400 a month to more than $1,100 starting in January — a nearly threefold increase that she said left her in a state of panic.

Jump, who earns about $72,000 a year as a real estate title officer, already feels financially stretched by the need to cover both her Blue Cross Blue Shield plan and the roughly $415 a month she pays for a prescription drug for type 2 diabetes.

“I don’t know how I’m going to pay for this,” Jump, 59, told CBS News. Her boss has offered to chip in, but she said the higher premium would still be a major strain on her budget.

“I’m just going to have to cut back on whatever else I can,” she added. “It’s just insane. What’s going to happen in the next couple of years? Is it going to continue to go up?”

With two health care bills failing to advance in the Senate on Thursday, the ACA’s enhanced premium tax credits — which 90% of enrollees in the government health program rely on to ease the cost of affording health insurance — are almost certain to expire on Dec. 31. That will leave Jump and the roughly 22 million other Americans who now qualify for the tax credits facing some tough financial decisions.

Out-of-pocket premium costs will increase 114% on average for ACA participants who currently receive the subsidies, hiking their annual costs for medical insurance by $1,016, according to health policy group KFF.

“That’s a huge financial burden for most families,” Emma Wager, a senior policy analyst at KFF, told CBS News. “There’s not a lot of people who can afford that.”

Some households could see even larger spikes. A family of four earning $75,000 per year is likely to see their insurance premiums rise by an additional $3,368 without the tax credits, the group estimated.

Such a drastic increase in ACA costs would arrive as Americans are already struggling to afford groceries, rent, utilities and other essentials, leaving many financially pinched.

Some ACA participants told CBS News they are considering going without health insurance next year if their monthly premiums spike. Others are opting for cheaper plans with less coverage, potentially exposing them to higher costs and medical debt, Michelle Sternthal, director of government affairs at health care advocacy group Community Catalyst, told CBS News.

“We are going to see a tsunami of health costs increasing” on January 1, Sternthal said. “Right now, we’re hearing about families facing shocking increases.”

About 4 million people could drop their health insurance due to the higher ACA premiums, the Congressional Budget Office has estimated.

The rising costs could hit some Americans harder than others, with small business owners and self-employed workers particularly vulnerable, Sternthal noted. Many such workers have turned to the ACA for health coverage because they lack employer-based insurance. About half of adults enrolled in the ACA are small business owners, employed by a company with fewer than 25 workers or are self-employed, according to KFF.

That group includes Aaron Lehman, an Iowa farmer who grows corn, soybeans and other crops on his family’s farm. In testimony before a Dec. 10 Senate hearing, he said the enhanced premium tax credits have allowed him to work full-time on his farm.

“But unfortunately, my wife and I have learned that in order to keep a similar policy for 2026, our health insurance costs will more than double,” Lehman told the committee.

The ACA tax credits were established in 2021, as the U.S. was reeling from the pandemic, to lower households’ monthly health plan costs; the subsidies were later extended under the Biden-era Inflation Reduction Act. With the credits set to expire this year, Democratic lawmakers this fall pushed for an extension, a congressional fight that became the main sticking point in the 43-day government shutdown that ended in November.

As part of the deal to end the funding impasse, Republicans vowed to hold a vote on whether to extend the ACA credits by mid-December. The GOP also introduced its own measure to address health care costs, which involved sending funds directly to consumers rather than extending the ACA subsidies.

However, votes on both health care proposals failed in the Senate on Thursday. Some lawmakers remain optimistic they can strike a bipartisan deal. But any agreement would likely involve reforms to the ACA to address income caps and fraud, along with a gradual phasing out of the enhanced subsidies.

Sternthal of Community Catalyst thinks Congress will face political pressure to address the expired tax credits once once millions of families face sticker shock in January.

In the meantime, Americans who get their health insurance through an employer-based plan could also be impacted by the higher ACA costs, she added.

The reason: If millions drop coverage, as the CBO has predicted, it would likely destabilize the health care market because more people would need to rely on emergency rooms for treatment. Because hospitals, by law, must treat uninsured patients, they typically recoup the costs by hiking treatment costs for others.

“If you have fewer people covered, that means there will be more uncompensated care, and people will go to the ER — and that will trickle down into providers and insurance companies,” Sternthal said. “It’s an economy-wide problem.”

[ad_2]

[ad_1]