Hugh Carney is EVP for financial institutions policy and regulatory affairs at ABA.

The Trump administration has made clear that lowering the cost of living for American households is a top economic priority. That focus creates an important opportunity for the federal banking agencies as they consider how to move forward with mitigating the regulatory burden banks face and specifically the Basel III “endgame,” or B3E, proposal. Capital rules are not abstract regulatory exercises. They directly influence the price and availability of credit that families, businesses, and communities rely on every day.

Banks are the primary drivers of economic growth in the economy. When capital requirements are set too high or calibrated without regard to how they will impact borrowers and the overall economy, the result is predictable and straightforward: credit becomes more expensive and less available. The costs of miscalibrated and overzealous capital requirements are ultimately borne by borrowers — including farmers buying seed and equipment, small businesses and startups seeking working capital, families purchasing their first homes and communities financing infrastructure and utilities — creating an economic drag.

That dynamic has real world impact. A wide range of commenters warned that the misguided 2023 B3E proposal would have raised costs and limited access to credit across the economy. Agricultural organizations cautioned that higher costs and reduced availability of clearing and credit services would disproportionately harm farmers, grain elevators, and rural communities, with higher costs flowing through the food supply chain. Small business advocates similarly warned that increased capital requirements would make lending more expensive and restrict access to affordable credit.

Housing and household affordability concerns were also a central theme. Civil rights, housing, and consumer groups warned that the proposal would undermine efforts to expand homeownership, particularly for first-time, first-generation, Black and Hispanic homebuyers who lack access to generational wealth. Independent analysis suggested that the proposed capital levels exceed what would be needed even under severe economic stress and would disproportionately disadvantage low-to-moderate-income borrowers and communities.

The impacts would extend well beyond farmers and households. Utility companies warned that higher financing and hedging costs would be passed directly on to customers in the form of higher monthly bills. State and local government finance officials cautioned that increased capital requirements would raise borrowing costs for municipal issuers and reduce liquidity in municipal debt markets. Manufacturers and infrastructure advocates warned that higher bank regulatory costs would limit access to funding for major projects, undermine U.S. competitiveness, and slow investment. Clean energy groups raised concerns that higher capital charges would make tax equity and other financing prohibitively expensive, putting billions of dollars in energy investments at risk. Public pension funds and insurers also warned of higher costs that would ultimately be borne by retirees and policyholders.

Taken together, these comments reinforce a simple point: Capital policy is economic policy. As the banking agencies consider next steps on the B3E, they have the opportunity to align prudential objectives with the nation’s cost of living goals. That means carefully calibrating capital requirements to actual risk, avoiding unnecessary increases that constrain lending, and recognizing that a strong, well-functioning banking system is essential to making credit affordable and widely available.

Lowering the cost of living does not stop at grocery prices or energy bills. It depends on ensuring that credit remains accessible and reasonably priced for the millions of Americans who rely on banks to finance homes, businesses, infrastructure and retirement.

ABA Viewpoint is the source for analysis, commentary and perspective from the American Bankers Association on the policy issues shaping banking today and into the future. Click here to view all posts in this series.

The FDIC announced today that it will push back the deadline for comment on its proposal to create a process through which banks can seek agency approval to issue stablecoins through a subsidiary.

The FDIC issued proposed rulemaking in December to begin implementing the Genius Act. The agency originally set a comment deadline of Feb. 17, but in a statement, it pushed that deadline back to May 18.

Last month, the American Bankers Association joined four associations in urging the FDIC to extend the comment period. Among other things, they noted the agency has yet to issue a separate proposal to implement the law’s capital, liquidity, risk management and other prudential requirements.

Proposed legislation would provide “a strong framework” to improve social media companies’ urgency in removing fraudulent advertising, “stopping countless scams before they start,” American Bankers Association President and CEO Rob Nichols said today in a letter to the bill’s sponsors.

The Safeguarding Consumers from Advertising Misconduct, or SCAM, Act by Sens. Bernie Moreno (R-Ohio) and Ruben Gallego (D-Ariz.) would require social media platforms to take additional steps to prevent scam ads from appearing on their platforms. Nichols noted that no other sector invests more to protect customers from fraud than the banking sector. However, banks cannot solve the problem alone.

“When social media companies perform minimal, if any, vetting of the advertisements placed on their networks, criminals can exploit these platforms to impersonate banks and other legitimate companies and gain consumers’ trust,” he said. “As long as fraudulent ads can continue to drive revenue for platforms without consequence, more must be done to protect consumers.

The SCAM Act would require social media companies to verify advertisers’ identity, implement systems to detect fraudulent advertisements, and investigate and remove fake ads, Nichols said. The bill also limits immunity under Section 230 of the Communications Act, which shields social media companies from the legal consequences of what is posted on their platforms.

“For too long, the social media scam ecosystem has been generating profits for social media platforms,” Nichols said. “Under the SCAM Act, a greater volume of scams will no longer mean greater revenue.”

Mirae Asset Global Investments Co. Ltd. lessened its holdings in ATI Inc. (NYSE:ATI – Free Report) by 53.2% during the 3rd quarter, Holdings Channel.com reports. The firm owned 5,361 shares of the basic materials company’s stock after selling 6,082 shares during the period. Mirae Asset Global Investments Co. Ltd.’s holdings in ATI were worth $436,000 as of its most recent filing with the Securities & Exchange Commission.

A number of other institutional investors and hedge funds also recently made changes to their positions in the business. Meeder Asset Management Inc. increased its holdings in ATI by 2,010.0% during the third quarter. Meeder Asset Management Inc. now owns 422 shares of the basic materials company’s stock valued at $34,000 after buying an additional 402 shares during the last quarter. Nomura Asset Management Co. Ltd. boosted its stake in shares of ATI by 56.5% during the 2nd quarter. Nomura Asset Management Co. Ltd. now owns 720 shares of the basic materials company’s stock worth $62,000 after acquiring an additional 260 shares during the last quarter. MAI Capital Management grew its position in shares of ATI by 38.6% during the 2nd quarter. MAI Capital Management now owns 869 shares of the basic materials company’s stock valued at $75,000 after acquiring an additional 242 shares during the period. NewEdge Advisors LLC purchased a new stake in shares of ATI in the 2nd quarter worth $75,000. Finally, Pilgrim Partners Asia Pte Ltd purchased a new stake in shares of ATI in the 3rd quarter worth $91,000.

Analyst Upgrades and Downgrades

Several equities analysts recently weighed in on the company. JPMorgan Chase & Co. lifted their target price on ATI from $135.00 to $150.00 and gave the company an “overweight” rating in a research report on Wednesday. BTIG Research lifted their price objective on ATI from $120.00 to $165.00 and gave the company a “buy” rating in a research report on Wednesday. Weiss Ratings reiterated a “buy (b-)” rating on shares of ATI in a research note on Monday, December 29th. Deutsche Bank Aktiengesellschaft restated a “buy” rating and set a $150.00 target price on shares of ATI in a research note on Wednesday. Finally, Susquehanna set a $155.00 price objective on shares of ATI in a research note on Wednesday. Ten equities research analysts have rated the stock with a Buy rating and one has assigned a Hold rating to the company. Based on data from MarketBeat.com, the company presently has an average rating of “Moderate Buy” and a consensus target price of $133.00.

In other ATI news, Chairman Robert S. Wetherbee sold 60,000 shares of the stock in a transaction on Tuesday, November 18th. The shares were sold at an average price of $98.34, for a total transaction of $5,900,400.00. Following the completion of the transaction, the chairman owned 246,538 shares in the company, valued at $24,244,546.92. This trade represents a 19.57% decrease in their ownership of the stock. The transaction was disclosed in a document filed with the Securities & Exchange Commission, which is available through this link. Also, VP Timothy J. Harris sold 10,543 shares of ATI stock in a transaction on Tuesday, November 11th. The stock was sold at an average price of $97.69, for a total transaction of $1,029,945.67. Following the completion of the transaction, the vice president directly owned 119,394 shares of the company’s stock, valued at $11,663,599.86. The trade was a 8.11% decrease in their ownership of the stock. Additional details regarding this sale are available in the official SEC disclosure. In the last ninety days, insiders sold 148,087 shares of company stock worth $15,131,989. 1.10% of the stock is currently owned by insiders.

ATI Trading Up 1.1%

Shares of ATI stock opened at $128.88 on Friday. The company has a current ratio of 2.66, a quick ratio of 1.18 and a debt-to-equity ratio of 0.90. The stock has a market capitalization of $17.51 billion, a price-to-earnings ratio of 45.38, a price-to-earnings-growth ratio of 1.18 and a beta of 1.02. ATI Inc. has a 12-month low of $39.23 and a 12-month high of $137.00. The stock’s 50-day moving average price is $115.83 and its 200-day moving average price is $95.54.

ATI (NYSE:ATI – Get Free Report) last announced its quarterly earnings results on Tuesday, February 3rd. The basic materials company reported $0.93 EPS for the quarter, beating analysts’ consensus estimates of $0.89 by $0.04. ATI had a return on equity of 24.26% and a net margin of 8.81%.The company had revenue of $1.18 billion during the quarter, compared to analyst estimates of $1.18 billion. During the same period in the prior year, the company earned $0.79 earnings per share. The firm’s revenue was up .4% on a year-over-year basis. ATI has set its FY 2026 guidance at 3.990-4.270 EPS and its Q1 2026 guidance at 0.830-0.890 EPS. Equities research analysts predict that ATI Inc. will post 2.89 EPS for the current fiscal year.

ATI News Roundup

Here are the key news stories impacting ATI this week:

Allegheny Technologies Incorporated (ATI) is a global manufacturer of specialty materials and complex components, serving aerospace, defense, oil and gas, chemical processing, medical and other industrial end markets. The company operates through two main segments: High Performance Materials & Components, which produces titanium and nickel-based alloys, stainless and specialty steels, and precision forgings; and Flat-Rolled Products, which supplies stainless steel, nickel and specialty alloy sheet, strip and precision-rolled plate.

Receive News & Ratings for ATI Daily – Enter your email address below to receive a concise daily summary of the latest news and analysts’ ratings for ATI and related companies with MarketBeat.com’s FREE daily email newsletter.

With its home in London, it is no surprise that FinvoateEurope often showcases the highest number of demoing companies headquartered outside of the United States. What’s especially interesting about this year’s cohort of FinovateEurope demoing companies, however, is the percentage of non-US companies compared to the total: more than 77% of this year’s demoers hail from countries other than the US. Check them out below and then join us next week for FinovateEurope 2026!

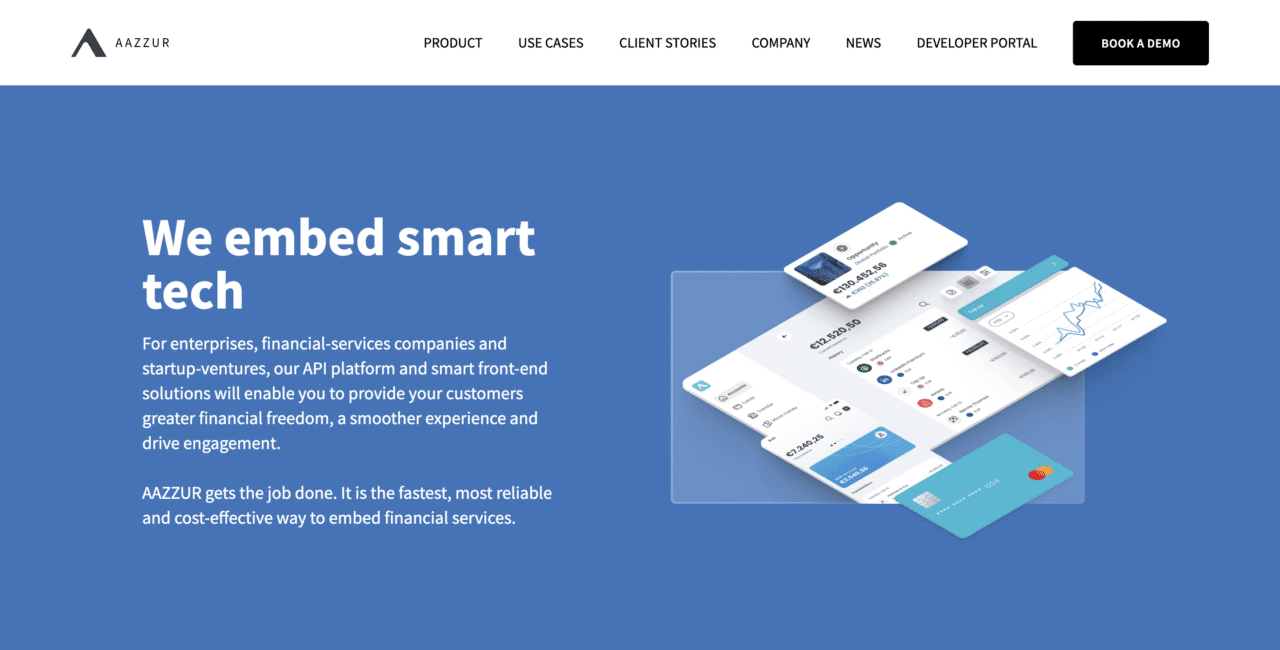

Founded in 2019, AAZZUR empowers brands to launch embedded finance solutions with a single integration, unlocking new revenue streams and enhancing customer engagement.

Founded in 2021, Candour Identity boosts onboarding conversions, reduces fraud losses, enables daily biometric use, and supports regulatory complaince to help instituions scale their digital offerings.

Founded in 2024, FINTRAC automates workflows to deliver stronger controls, richer analytics, and lower costs across the model lifecycle. The company’s Model Ops platform helps banks and other financial institutions manage their most complex models and calculations.

Founded in 2025, Francis empowers financial institutions and fintechs to make the most of open finance by leveraging AI. The company’s technology turns fragmented financial data into actionable wealth insights.

From simple workflows to complex cases such as commercial loans and mortgages, Intuitech delivers AI agents capable of automating over 90% of manual tasks, shortening approval times and lowering costs. The company was founded in 2018.

Keyless replaces outdated multi-factor authentication (MFA) with biometrics, improving the user experience and saving millions. Founded in 2019, Keyless was acquired by fellow Finovate alum Ping Identity.

Maisa boosts business efficiency by automating end-to-end processes with traceability, hallucination-resistance, and governance, in regulated industries such as banking and financial services. Maisa was founded in 2024.

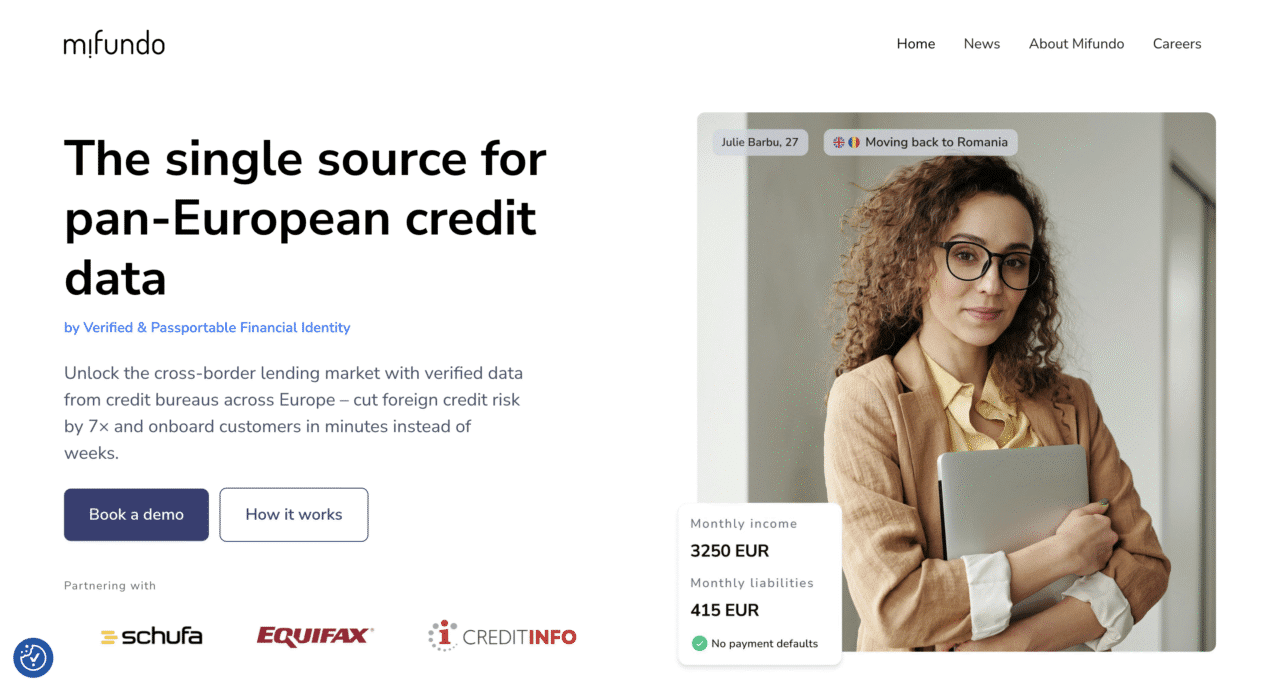

Mifundo enables banks and other financial institutions to grow their business volume by up to 15% by enabling them to better serve foreign and cross-border customers throughout Europe. The company was founded in 2022.

Founded in 2020, MyPocketSkill is a digital technology company at the nexus of fintech and edtech that offers solutions to help Gen Z to save, invest, and become more money savvy.

Founded in 2024, Neuralk AI makes predictive capability a viable option at every point where tabular data is available. The company’s technology delivers superior performance compared to traditional machine learning and large-language models.

Founded in 2023, Opentech partners with banks and card issuers, supporting digital transformation with secure, compliant, and scalable payment solutions. The company combines UX design with software engineering via a co-design model that accelerates delivery while ensuring equality and reliability.

Founded in 2019, R34DY offers an automated system, ABLEMENTS, that enables rapid AI transformation for banks, enabling them to deliver new products faster, lower IT costs, and differentiate themselves via context-aware modernization.

Sea.dev provides embeddable AI for business lending. The company’s technology automates underwriting workflows, to enable credit analysts to focus on higher-value analysis, faster decision-making, and growth. Sea.dev was founded in 2024.

Founded in 2023, Serene combines behavioral insights, predictive intelligence, and financial data to enable institutions to identify and understand early signs of fraud, vulnerability, and financial stress.

Founded in 2025, Skill Studio AI transforms training documents into engaging, AI-powered learning experiences. The company’s platform reduces training costs, accelerates compliance readiness, and scales globally.

Tweezr—Tel Avi, Israel and Amsterdam, the Netherlands

Tweezr empowers institutions to transform and grow by accelerating time-to-market and boosting developer productivity for both maintaining legacy systems as well as for modernization initiatives. The company was founded in 2024.

Nearly nine in 10 U.S. adults reported feeling some kind of financial stress at the start of 2026, with more than three in four saying they experienced a financial setback last year, according to a new survey by the National Endowment for Financial Education.

NEFE, in conjunction with the market research firm Verasight, polled U.S. adults on their overall financial well-being at the end of 2025 and their expectations for 2026. Among the findings:

Eighty-eight percent felt some form of financial stress as they began the new year and 77% said they experienced a financial setback in 2025.

The largest anticipated expenses in 2026, excluding mortgage and rent, are “paying down debt” (40%), “home-related expenses” (36%) and “transportation expenses” (32%).

When asked about their confidence in handling an unexpected $2,000 expense, 36% are “certain they could,” 19% “probably could,” 13% “probably could not” and 26% are “certain they could not.”

If faced with an unexpected expense, most respondents would use some combination of “credit cards” (35%), “emergency savings” (25%) or “cash” (24%), followed by “borrowing money from family or friends” (20%), “selling something they own” (18%) and “using a ‘Buy Now, Pay Later’ offer to free up funds” (17%).

Respondents were most likely to view the quality of their current financial life as “about what they expected” (41%), followed by “worse than they expected” (38%) and then “better than they expected” (16%).

Respondents said the frequency they had a month-end surplus of money is “every month” (20%), “most months” (19%), “only some months” (22%), “rarely” (24%) and “never” (14%).

“While these findings are startling, there is growing momentum to address these challenges through youth financial education graduation requirements,” said Billy Hensley, president and CEO of NEFE. “Many of the issues highlighted in this poll are already among the core topics states are considering for their curricula. Financial topics and the choices surrounding them shouldn’t be a mystery. By normalizing conversations about money and strengthening young people’s confidence, we increase the likelihood that they can align their financial lives with their personal values and decisions.”

Imagine the power of an entire bank right in your pocket. In 2026, digital banking has evolved from a simple convenience into a personalized command center for your financial life. At OneUnited Bank, we’ve spent more than 20 years pioneering technology that puts you in control, giving you the visibility and flexibility to build wealth on your own schedule.

The relationship between inflation and real economic activity has long been central to debates in macroeconomics and monetary policy. At the core of this debate is the Phillips curve (PC), which measures how strongly inflation reacts to movements in economic conditions. The steepness of this curve matters enormously for monetary policy: if the PC is steeper, inflation rises faster during booms and falls faster in recessions, which entails central banks having to act more forcefully if they want to stabilize inflation around their target. Prior analysis found astonishingly small estimates of the slope of the PC, which suggests that the curve is “flat” (or even dead). In this post, I present evidence from coauthored research showing that, contrary to the conventional view, the Phillips curve is alive and steep, and it captures inflation volatility remarkably well once real marginal cost is used instead of standard real economic activity measures.

The Conventional Formulation of the Phillips Curve

The Phillips curve links inflation to expectations of future inflation and a measure of economic slack. In the conventional formulation of the PC, economic slack is typically proxied by the output or unemployment gaps—the deviation of output or employment from its natural level:

In this view, inflation rises when the economy overheats and falls during slowdowns. The slope of the Phillips curve,Kin the equation above, captures how sensitive inflation is to these fluctuations. A large body of research finds that the PC is quite flat—the slope is very small—implying that inflation hardly moves in response to shifts in output or employment gaps. These findings have long puzzled economists and fueled debate about how active monetary policy should be to steer inflation.

The Primitive (Cost-Based) Formulation of the Phillips Curve

There is another way to think about inflation dynamics and its drivers. At its foundation, the Phillips curve emerges from the aggregation of firms’ pricing decisions in response to changes in production costs. In the primitive formulation of the PC, the variable influencing inflation is real marginal cost in percentage deviation from trend, rather than the output or unemployment gap:

In this view, inflation rises when economic forces increase firms’ production costs. The slope of the curve reflects how strongly (and quickly) these costs are passed through into output prices.

The Slope of the Cost-Based Phillips Curve

The cost-based formulation makes it easier to understand the key forces that determine the slope of the PC. In theory, if markets were perfectly competitive and frictionless, prices would move one-for-one with costs: any increase in wages or input prices would be instantly reflected in consumer prices. That is, the slope would be one.

Reality is very different. Firms typically adjust prices infrequently, since doing so involves both direct costs (such as relabeling or updating systems) and indirect costs (such as confusing customers or losing goodwill). In addition, firms often set prices strategically, choosing to delay changes until they are sure cost pressures will last, or timing revisions to match competitors. Thus, frictions that lead to infrequent price changes and strategic considerations in price setting weaken the transmission of cost shocks into prices. The more firms deviate from the ideal of flexible, competitive markets, the flatter the Phillips curve becomes.

Estimating the Slope of the Cost-Based Phillips Curve Using Microdata

How steep is the cost-based PC in the data? Answering this question is notoriously difficult, particularly when the estimation is solely based on aggregate data in which many shocks influence inflation and real activity at the same time. To address this problem, we turn to firm-level evidence. In a recent paper coauthored with Mark Gertler (New York University), Luca Gagliardone (Yale University), and Joris Tielens (National Bank of Belgium), we use detailed microdata on prices and costs to study how individual firms adjust their prices in response to changes in production costs. This approach allows us to quantify how nominal rigidities (infrequent price changes) and real rigidities (strategic interactions among firms) dampen the response of prices to cost shocks. With these estimates we recover the slope of the primitive form of the Phillips curve.

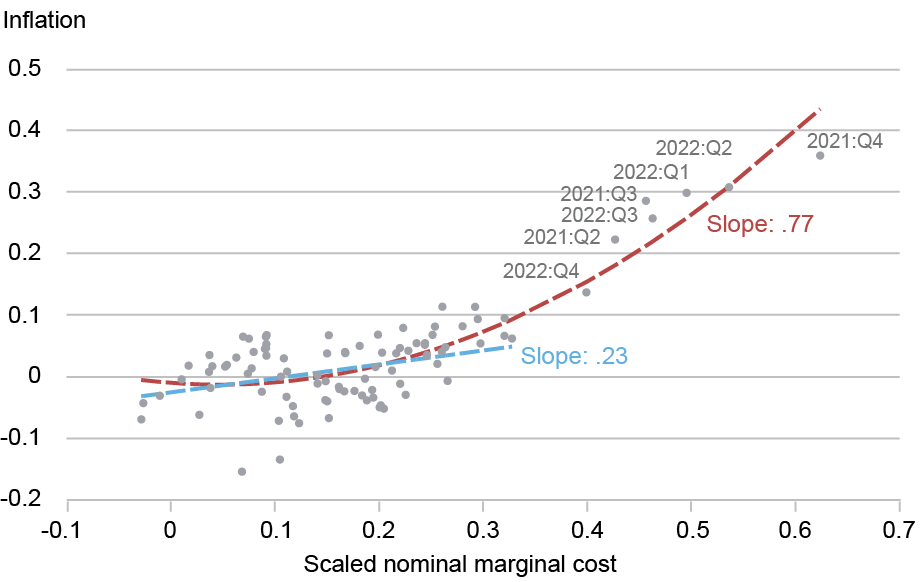

Our analysis suggests a strong link between inflation and real economic conditions, as captured by producers’ costs. On average, firms keep prices fixed for three to four quarters, confirming a substantial degree of nominal rigidity. We also find strong evidence of strategic complementarities: firms adjust less aggressively because they prefer to move in step with competitors, which cuts the pass-through of cost shocks roughly in half. Taking these frictions into account, we estimate the slope of the cost-based Phillips curve to be three to ten times larger than the estimates for the output- or unemployment-based PC formulation. This implies that the Phillips curve is steep, not flat, even in normal times.

Accounting for Aggregate Inflation Dynamics

Cost pass-through plays a dominant role in shaping aggregate inflation. To illustrate this, we build a cost index by combining firm-level changes in labor and input costs and then feed it into the cost-based Phillips curve. Using the Belgian manufacturing sector as a case study, we construct a model-generated inflation series by feeding data on costs into the Phillips curve. The results, shown in the chart below, show that the predicted inflation aligns very closely with actual producer price inflation (PPI) in Belgium. The two series are highly correlated, with a correlation coefficient above 80 percent; quantitatively, movements in production costs alone account for about 70 percent of observed inflation fluctuations, highlighting the central role of costs in driving inflation dynamics.

Through the Lens of the Cost-Based Phillips Curve, Fluctuations in Production Costs Account Well for Inflation Volatility

Source: Gagliardone, Gertler, Lenzu, and Tielens (2025). Notes: The blue line represents the time series of manufacturing PPI in Belgium. The red line is the model-implied manufacturing PPI obtained feeding an aggregate cost index to a cost-based PC.

Reconciling the Steep Cost-Based Phillips Curve with the Flat Output-Based Phillips Curve

These results raise a natural question: Why does the cost-based Phillips curve slope steeply while the output-based one appears flat? And are these findings at odds with previous research?

Our research shows that the “flatness” of the conventional Phillips curve reflects a weak link between output gaps and marginal costs. In other words, while production costs feed directly into firms’ pricing decisions, movements in output (or unemployment) bear only a loose relationship to inflation.

From a conceptual standpoint, the conventional PC holds only if marginal cost and the output gap move proportionally—an assumption that requires, among other things, perfectly flexible wages. When these conditions fail, the output gap may be a poor proxy for real marginal cost, biasing estimates of PC downward. Moreover, even if proportionality roughly holds, the output-based slope equals the cost-based slope scaled by the elasticity of marginal cost with respect to output. If this elasticity is low, the slope of output-based PC will be low as well, even if the slope of the cost-based PC is sizable.

These results are confirmed in the data. Focusing on the pre-pandemic period (1999–2019), we estimate a very low elasticity of marginal cost with respect to output. This finding helps explain why the cost-based PC is steep while the conventional PC looks flat.

Lessons for the Post-Pandemic Inflation Surge

Our findings show a strong pass-through from marginal costs to prices, which explains why the cost-based Phillips curve matches inflation dynamics so well. The weak link between output and marginal cost, on the other hand, helps explain why the conventional output-gap version of the PC looks “flat.” In normal times, two factors drive this low elasticity: firms’ cost schedules tend to display nearly constant short-run returns to scale, so marginal costs barely move with output; and wage rigidity further dampens any feedback from demand to costs.

The pandemic and its aftermath revealed how quickly these relationships can change under stress. Severe shocks—whether from labor market tightness or supply chain bottlenecks—pushed firms against capacity limits, sending marginal costs sharply higher and fueling inflation. At the same time, the slope of the Phillips curve itself can shift. Pre-pandemic data showed stable adjustment frequencies and an approximate linear relationship between inflation and (percentage) changes in real marginal costs. More recently, however, firms have been adjusting prices much more often, raising the elasticity of inflation with respect to costs and generating nonlinear inflation dynamics. I will talk about nonlinear inflation dynamics—what it means, how it works, and what it implies—in a companion post on Liberty Street Economics.

Simone Lenzu is a financial research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post: Simone Lenzu, “Anatomy (not Autopsy) of the Phillips Curve,” Federal Reserve Bank of New York Liberty Street Economics, February 4, 2026, https://doi.org/10.59576/lse.20260204 BibTeX: View |

@article{

Lenzu2026,

author={Lenzu, Simone},

title={Anatomy (not Autopsy) of the Phillips Curve},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={February 4},

year={2026},

url={https://doi.org/10.59576/lse.20260204}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

Inflation does not always respond to cost and demand pressures in the same way. When shocks are small, the mapping from costs to prices is roughly proportional—double the shock, double the inflation response. But when the economy is hit by large shocks, this proportionality breaks down. As the recent surge and subsequent decline of global inflation showed, price growth can accelerate—or decelerate—by more than one-for-one relative to the size of the disturbance. Economists refer to this pattern as nonlinear inflation dynamics. In this post, I discuss what these nonlinearities mean, how they relate to the slope of the Phillips curve discussed in a companion post, and how firm-level data can help us understand the mechanisms behind them.

Evidence of Nonlinearities in the Data

The chart below illustrates nonlinear inflation dynamics taken from a recent working paper. It plots a measure of real cost changes for the Belgian manufacturing sector against producer price inflation (PPI) over the period 1999–2023.

The Nonlinear Relation Between Inflation Cost Shocks and Inflation

Source: Gagliardone, Gertler, Lenzu, and Tielens (2025). Notes: Each dot represents the joint realization of year-over-year change in a production-cost index (x-axis) against year-over-year PPI inflation (y-axis) for Belgian manufacturing in the same quarter. The data cover the period 2000:Q1 through 2023:Q4.

For small and medium-sized cost shocks, inflation rises roughly one-for-one with costs: the dots align along a straight line. When the economy is under stress, however, this proportionality breaks down. Once cost shocks exceed a threshold—around a 20 percent annual increase in our data—the slope steepens sharply. Double the size of the shock and inflation rises by much more than twofold. That is, inflation becomes more sensitive to shocks when disturbances are sufficiently large. This pattern is exactly what we observe in recent years, when the energy shocks and supply-chain disruptions associated with the COVID-19 pandemic and the war in Ukraine drove exceptionally large increases in producers’ costs.

The State-Dependent Nature of Pricing

Nonlinear inflation dynamics reflect the microeconomics of firms’ pricing decisions—and, in particular, the state-dependent way firms respond to shocks. Simply put, firms do not react uniformly: when shocks are small, many wait; when shocks are large, more firms adjust, and by larger amounts.

To see the intuition, consider a world where firms can adjust prices only at random and with a fixed probability—like in a lottery. In this world, the firms that reprice are not necessarily those facing the largest shocks (those whose prices deviate most from their optimal level). Yet when they do reprice, they update their prices to reflect current economic conditions. These ideas underlie the Calvo model, the workhorse model used in academic and policy analysis. In this framework, the average frequency of price changes does not vary with economic conditions, implying that inflation scales linearly with the size of the shock (a linear Phillips curve). Strict as they may seem, the assumptions behind the Calvo model—particularly the fixed probability of price adjustment—are remarkably consistent with the data in normal times.

Things look different when shocks are large. If adjusting prices is costly—because, for example, it involves updating menus or risks alienating customers—firms reprice only when the benefits outweigh those costs, much as a restaurant rewrites its menu only when prices are far out of date. When pressures are modest, few firms find it worthwhile; when shocks surge, many do. These shifts show up clearly in the data: large jumps in the average frequency of price changes occurred, more recently, during the recent pandemic inflation surge.

Such spikes are inconsistent with the Calvo model, but they are exactly what state-dependent pricing models—such as menu-cost models or models with information frictions—predict. These models capture the idea that when the economy is hit by large shocks, the entire price-setting process speeds up.

Three Facts About Pricing

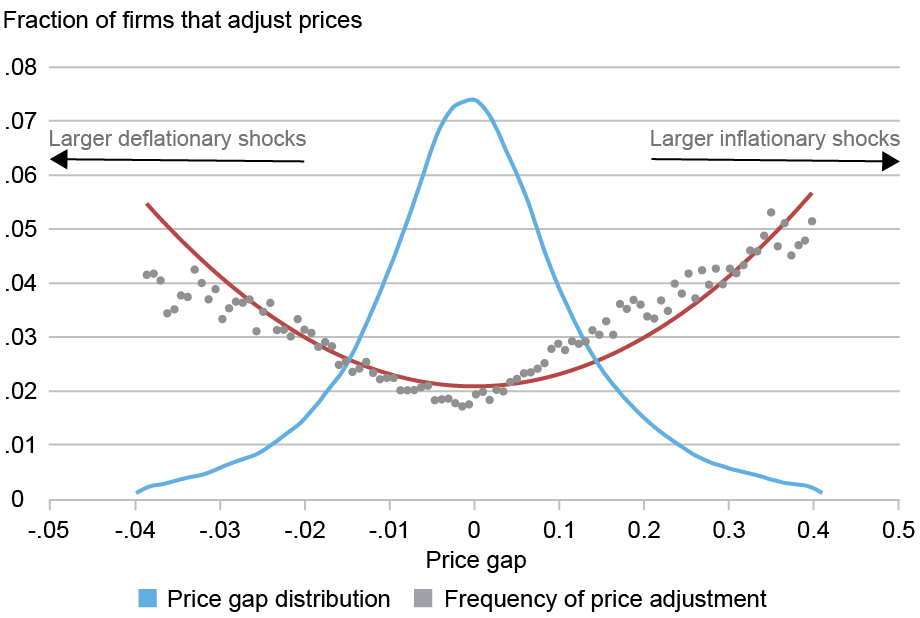

Using detailed administrative data on thousands of Belgian manufacturing firms, we construct an empirical measure of each firm’s price gap—the percentage difference (in percentage terms) between the price it currently charges and the price it would set if it could adjust freely (its “desired price”). The larger the gap—whether positive or negative—the greater the changes in costs or competitive pressures the firm faces, and the further its current price drifts from the desired one. We thus provide a natural way to study how often and by how much firms adjust in response to shocks of different sizes.

Fact 1: Firms adjust more frequently when their prices drift far from optimal

The chart below shows the relationship between firms’ price gaps and the frequency of price adjustment. The blue line represents the probability density function of price gaps and the red line the fraction of firms that adjust their prices (y-axis) at each point of the price gap distribution. Firms in the tails—those with prices far above or below their desired price level—change prices much more often. The relationship is U-shaped: the further a firm’s price is from its target, the more likely it is to adjust. This is exactly what state-dependent pricing models predict. By contrast, in the Calvo model the probability of adjustment is unrelated to the price gap—its predicted curve would be flat.

The Probability of Price Adjustment Rises with the Size of the Price Gap

Source: Gagliardone, Gertler, Lenzu, and Tielens (2025). Notes: The blue line represents the probability density function of the distribution of price gaps; the red line shows the measured frequency of price adjustment along the price gap distribution.

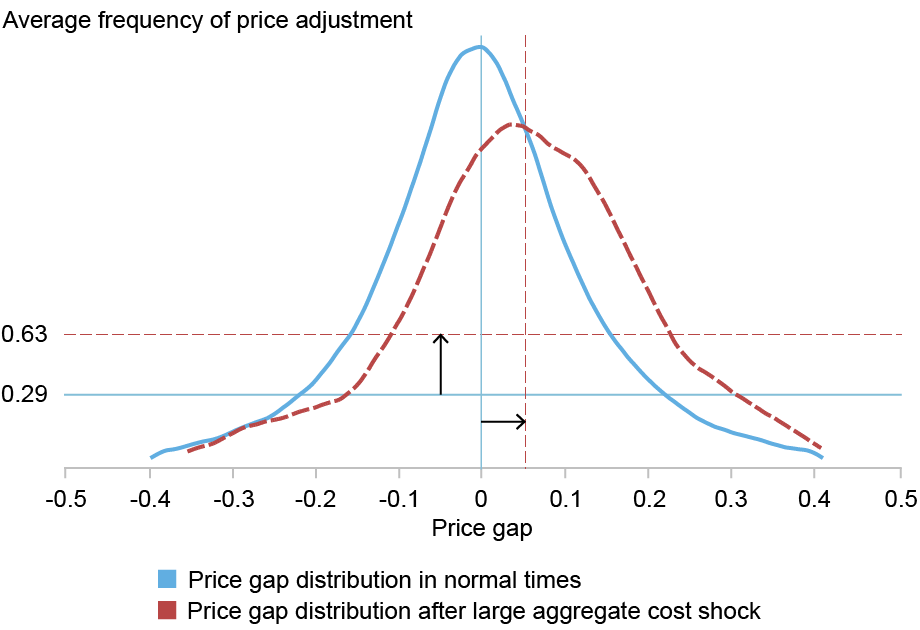

Fact 2: Large aggregate shocks shift the entire distribution of price gaps, prompting more frequent price changes

The chart below shows how aggregate shocks reshape firms’ incentives to reprice. Before the pandemic, the distribution of price gaps was centered around zero (blue line). In 2022:Q2—the quarter with the largest jump in firms’ production costs—the entire curve shifts rightward (red dashed line) as producers grappled with surging energy prices and widespread supply chain disruptions, and, as predicted by state-dependent pricing, the share of firms changing prices nearly doubled, leading to a marked acceleration in inflation.

Large Aggregate Shocks Shift the Entire Distribution of Price Gaps, Prompting More Frequent Price Changes

Source: Gagliardone, Gertler, Lenzu, and Tielens (2025). Notes: The blue curve is the pre-pandemic (1999–2019) density of price gaps; the red dashed curve is the 2022:Q2 density. Vertical lines mark the average gaps in the pre-pandemic period and in 2022:Q2. Horizontal lines show average adjustment probabilities in each period.

Fact 3: Inflation grows disproportionately larger when large shockshit

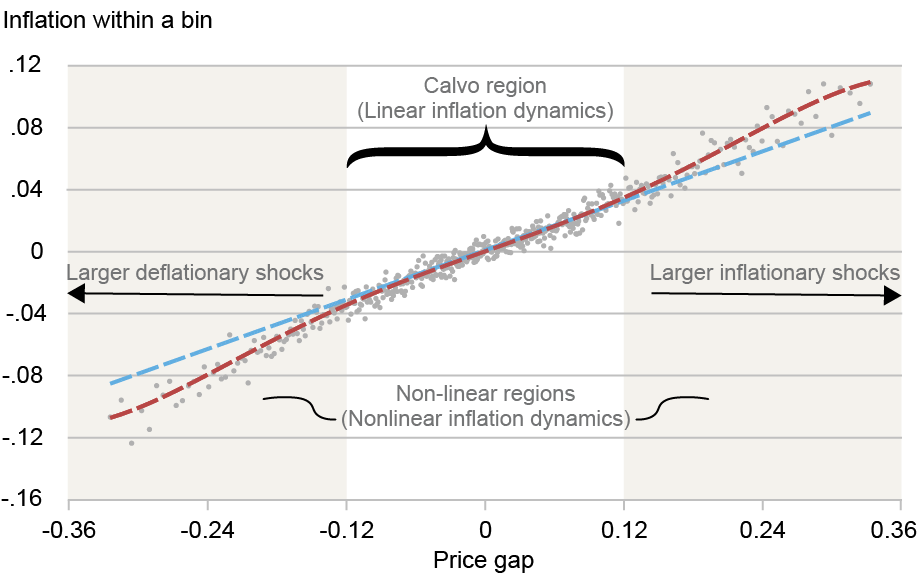

In the chart below, we again group firms by the size of their price gap. Each dot represents the average price gap for a group of firms (x-axis) plotted against their average price change (y-axis). The red dashed line shows a nonlinear fit through this cloud of points.

Inflation Responds Nonlinearly with the Size of the Shocks to Firms’ Desired Prices

Source: Gagliardone, Gertler, Lenzu, and Tielens (2025). Notes: The blue dashed line represents a linear fit of price changes (inflation) on price gaps, estimated on the subsample of bins covering firms between the 25th and 75th percentiles of the price gap distribution, with the estimated slope reported in black. The red dashed line represents the fit of a third-order polynomial in price gaps, estimated using bins across the entire price gap distribution.

At any point along this curve, its slope measures how strongly cost shocks are passed through into prices—the steeper the slope, the stronger the pass-through, and the steeper the Phillips curve. This exercise reveals that the mapping between expected price changes and price gaps is not constant. In fact, we can identify two distinct regions.

The Calvo region. When price gaps are small (roughly +/- 10 percent), pricing behavior looks linear: adjustment frequencies are stable, pass-through is proportional, and the elasticity of price changes with respect to gaps matches the average adjustment frequency. This pattern helps explain why the Calvo model works well in low-inflation environments.

The nonlinear regions. At the tails of the price gap distribution, pricing becomes far more reactive. Firms hit by large shocks exhibit nearly double the usual pass-through due to the significant rise in the frequency of price adjustment. The behavior of these firms mirrors what happens to the broader economy during major disturbances—such as those triggered by the COVID-19 pandemic. During these episodes, the economy is pushed into regions where the slope of the Phillips curve rises, and inflation reacts much more strongly and quickly to cost pressures.

Recognizing when the economy shifts between these regimes is important for decision makers who rely on timely signals about changing inflation conditions. Accounting for these transitions is key to understanding how inflation builds and eventually unwinds.

Simone Lenzu is a financial research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post: Simone Lenzu, “Does the Phillips Curve Steepen When Costs Surge?,” Federal Reserve Bank of New York Liberty Street Economics, February 5, 2026, https://doi.org/10.59576/lse.20260205 BibTeX: View |

@article{

Lenzu2026,

author={Lenzu, Simone},

title={Does the Phillips Curve Steepen When Costs Surge?},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={February 5},

year={2026},

url={https://doi.org/10.59576/lse.20260205}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

Oracle (NYSE:ORCL – Get Free Report) had its price objective cut by equities researchers at Scotiabank from $260.00 to $220.00 in a report issued on Tuesday, MarketBeat.com reports. The firm presently has a “sector outperform” rating on the enterprise software provider’s stock. Scotiabank’s price target indicates a potential upside of 49.91% from the company’s previous close.

Other equities analysts have also issued reports about the stock. DA Davidson lowered their target price on shares of Oracle from $200.00 to $180.00 and set a “neutral” rating for the company in a report on Thursday, December 11th. Citigroup reaffirmed a “market outperform” rating on shares of Oracle in a research report on Wednesday, December 17th. Erste Group Bank downgraded Oracle from a “buy” rating to a “hold” rating in a report on Monday, November 10th. Evercore ISI raised their price target on Oracle from $350.00 to $385.00 and gave the company an “outperform” rating in a report on Friday, October 17th. Finally, Mizuho set a $400.00 price target on Oracle in a research report on Monday, December 15th. Three analysts have rated the stock with a Strong Buy rating, twenty-five have assigned a Buy rating, eleven have assigned a Hold rating and two have assigned a Sell rating to the stock. Based on data from MarketBeat, the company has an average rating of “Moderate Buy” and a consensus target price of $296.03.

Shares of Oracle stock opened at $146.75 on Tuesday. Oracle has a 12 month low of $118.86 and a 12 month high of $345.72. The firm has a market capitalization of $421.63 billion, a P/E ratio of 27.58, a P/E/G ratio of 1.35 and a beta of 1.64. The company has a current ratio of 0.91, a quick ratio of 0.91 and a debt-to-equity ratio of 3.28. The business has a fifty day simple moving average of $191.31 and a two-hundred day simple moving average of $235.52.

Oracle (NYSE:ORCL – Get Free Report) last released its earnings results on Wednesday, December 10th. The enterprise software provider reported $2.26 earnings per share for the quarter, topping analysts’ consensus estimates of $1.64 by $0.62. Oracle had a net margin of 25.28% and a return on equity of 70.60%. The firm had revenue of $16.06 billion for the quarter, compared to the consensus estimate of $16.19 billion. During the same period in the prior year, the firm earned $1.47 EPS. The company’s revenue was up 14.2% compared to the same quarter last year. On average, equities analysts forecast that Oracle will post 5 earnings per share for the current fiscal year.

Insider Activity at Oracle

In other Oracle news, CEO Clayton M. Magouyrk sold 10,000 shares of the business’s stock in a transaction on Friday, December 19th. The shares were sold at an average price of $192.52, for a total transaction of $1,925,200.00. Following the completion of the sale, the chief executive officer directly owned 144,030 shares in the company, valued at approximately $27,728,655.60. The trade was a 6.49% decrease in their position. The sale was disclosed in a filing with the Securities & Exchange Commission, which is accessible through this hyperlink. Also, insider Mark Hura sold 15,000 shares of the stock in a transaction on Wednesday, December 24th. The shares were sold at an average price of $196.89, for a total value of $2,953,350.00. Following the transaction, the insider directly owned 234,077 shares in the company, valued at $46,087,420.53. The trade was a 6.02% decrease in their ownership of the stock. The SEC filing for this sale provides additional information. Insiders sold 62,223 shares of company stock valued at $12,136,764 over the last ninety days. Company insiders own 40.90% of the company’s stock.

Institutional Trading of Oracle

A number of hedge funds have recently bought and sold shares of ORCL. Winnow Wealth LLC purchased a new position in shares of Oracle in the second quarter worth approximately $28,000. FSA Wealth Management LLC purchased a new stake in Oracle during the third quarter valued at approximately $28,000. Joseph Group Capital Management bought a new position in Oracle in the fourth quarter worth approximately $29,000. Kilter Group LLC bought a new position in Oracle in the second quarter worth approximately $30,000. Finally, Darwin Wealth Management LLC boosted its stake in shares of Oracle by 130.0% during the 3rd quarter. Darwin Wealth Management LLC now owns 115 shares of the enterprise software provider’s stock worth $32,000 after acquiring an additional 65 shares during the last quarter. Hedge funds and other institutional investors own 42.44% of the company’s stock.

More Oracle News

Here are the key news stories impacting Oracle this week:

Positive Sentiment: Some sell-side firms (e.g., Barclays) have reiterated bullish ratings and high price targets, implying analysts still see upside if Oracle executes its AI/data-center strategy. Barclays Reiterates Overweight on Oracle

Neutral Sentiment: Oracle announced an equity distribution agreement and senior notes issuance to fund its plans — this provides capital but increases near-term financing activity and complexity. Oracle Bolsters Financing with Major Senior Notes Issuance

Neutral Sentiment: Oracle continues product and go-to-market pushes (AI banking platform, enterprise AI agents) that could drive long-term growth but require heavy near-term capex. Oracle Reimagines Banking for the AI Era

Neutral Sentiment: Strategic commentary ties Oracle’s massive data-center and power plans to a structural shift (e.g., MarketBeat piece on companies funding power and SMRs); long-term strategic rationale exists but is execution- and timeline-dependent. The Atomic Pivot: AI’s $50 Billion Power Move

Negative Sentiment: Multiple law firms have filed or are soliciting clients for securities class actions tied to Oracle’s disclosures (senior notes/offering documents and the June–Dec 2025 class period), adding legal risk and headline pressure. Kessler Topaz Files Securities Fraud Class Action Against Oracle

Negative Sentiment: Analysts have trimmed price targets (BMO, Scotiabank among them) and commentary highlights investor anxiety about the size/timing of the capital raise and AI execution — contributing to the stock’s decline. Oracle Price Target Lowered at BMO

Oracle Corporation is a multinational technology company that develops and sells database software, cloud engineered systems, enterprise software applications and related services. The company is widely known for its flagship Oracle Database and a portfolio of enterprise-grade software products that support data management, application development, analytics and middleware. Over recent years Oracle has expanded its focus to include cloud infrastructure and cloud applications, positioning itself as a provider of both platform and software-as-a-service solutions for large organizations.

Oracle’s product and service offerings include Oracle Database and the Autonomous Database, Oracle Cloud Infrastructure (OCI), enterprise resource planning (ERP), human capital management (HCM) and supply chain management (SCM) cloud applications (often grouped under Oracle Fusion Cloud Applications), middleware such as WebLogic, and developer technologies including Java and MySQL.

Further Reading

Receive News & Ratings for Oracle Daily – Enter your email address below to receive a concise daily summary of the latest news and analysts’ ratings for Oracle and related companies with MarketBeat.com’s FREE daily email newsletter.

The relationship between inflation and real economic activity has long been central to debates in macroeconomics and monetary policy. At the core of this debate is the Phillips curve (PC), which measures how strongly inflation reacts to movements in economic conditions. The steepness of this curve matters enormously for monetary policy: if the PC is steeper, inflation rises faster during booms and falls faster in recessions, which entails central banks having to act more forcefully if they want to stabilize inflation around their target. Prior analysis found astonishingly small estimates of the slope of the PC, which suggests that the curve is “flat” (or even dead). In this post, I present evidence from coauthored research showing that, contrary to the conventional view, the Phillips curve is alive and steep, and it captures inflation volatility remarkably well once real marginal cost is used instead of standard real economic activity measures.

The Conventional Formulation of the Phillips Curve

The Phillips curve links inflation to expectations of future inflation and a measure of economic slack. In the conventional formulation of the PC, economic slack is typically proxied by the output or unemployment gaps—the deviation of output or employment from its natural level:

In this view, inflation rises when the economy overheats and falls during slowdowns. The slope of the Phillips curve,Kin the equation above, captures how sensitive inflation is to these fluctuations. A large body of research finds that the PC is quite flat—the slope is very small—implying that inflation hardly moves in response to shifts in output or employment gaps. These findings have long puzzled economists and fueled debate about how active monetary policy should be to steer inflation.

The Primitive (Cost-Based) Formulation of the Phillips Curve

There is another way to think about inflation dynamics and its drivers. At its foundation, the Phillips curve emerges from the aggregation of firms’ pricing decisions in response to changes in production costs. In the primitive formulation of the PC, the variable influencing inflation is real marginal cost in percentage deviation from trend, rather than the output or unemployment gap:

In this view, inflation rises when economic forces increase firms’ production costs. The slope of the curve reflects how strongly (and quickly) these costs are passed through into output prices.

The Slope of the Cost-Based Phillips Curve

The cost-based formulation makes it easier to understand the key forces that determine the slope of the PC. In theory, if markets were perfectly competitive and frictionless, prices would move one-for-one with costs: any increase in wages or input prices would be instantly reflected in consumer prices. That is, the slope would be one.

Reality is very different. Firms typically adjust prices infrequently, since doing so involves both direct costs (such as relabeling or updating systems) and indirect costs (such as confusing customers or losing goodwill). In addition, firms often set prices strategically, choosing to delay changes until they are sure cost pressures will last, or timing revisions to match competitors. Thus, frictions that lead to infrequent price changes and strategic considerations in price setting weaken the transmission of cost shocks into prices. The more firms deviate from the ideal of flexible, competitive markets, the flatter the Phillips curve becomes.

Estimating the Slope of the Cost-Based Phillips Curve Using Microdata

How steep is the cost-based PC in the data? Answering this question is notoriously difficult, particularly when the estimation is solely based on aggregate data in which many shocks influence inflation and real activity at the same time. To address this problem, we turn to firm-level evidence. In a recent paper coauthored with Mark Gertler (New York University), Luca Gagliardone (Yale University), and Joris Tielens (National Bank of Belgium), we use detailed microdata on prices and costs to study how individual firms adjust their prices in response to changes in production costs. This approach allows us to quantify how nominal rigidities (infrequent price changes) and real rigidities (strategic interactions among firms) dampen the response of prices to cost shocks. With these estimates we recover the slope of the primitive form of the Phillips curve.

Our analysis suggests a strong link between inflation and real economic conditions, as captured by producers’ costs. On average, firms keep prices fixed for three to four quarters, confirming a substantial degree of nominal rigidity. We also find strong evidence of strategic complementarities: firms adjust less aggressively because they prefer to move in step with competitors, which cuts the pass-through of cost shocks roughly in half. Taking these frictions into account, we estimate the slope of the cost-based Phillips curve to be three to ten times larger than the estimates for the output- or unemployment-based PC formulation. This implies that the Phillips curve is steep, not flat, even in normal times.

Accounting for Aggregate Inflation Dynamics

Cost pass-through plays a dominant role in shaping aggregate inflation. To illustrate this, we build a cost index by combining firm-level changes in labor and input costs and then feed it into the cost-based Phillips curve. Using the Belgian manufacturing sector as a case study, we construct a model-generated inflation series by feeding data on costs into the Phillips curve. The results, shown in the chart below, show that the predicted inflation aligns very closely with actual producer price inflation (PPI) in Belgium. The two series are highly correlated, with a correlation coefficient above 80 percent; quantitatively, movements in production costs alone account for about 70 percent of observed inflation fluctuations, highlighting the central role of costs in driving inflation dynamics.

Through the Lens of the Cost-Based Phillips Curve, Fluctuations in Production Costs Account Well for Inflation Volatility

Source: Gagliardone, Gertler, Lenzu, and Tielens (2025). Notes: The blue line represents the time series of manufacturing PPI in Belgium. The red line is the model-implied manufacturing PPI obtained feeding an aggregate cost index to a cost-based PC.

Reconciling the Steep Cost-Based Phillips Curve with the Flat Output-Based Phillips Curve

These results raise a natural question: Why does the cost-based Phillips curve slope steeply while the output-based one appears flat? And are these findings at odds with previous research?

Our research shows that the “flatness” of the conventional Phillips curve reflects a weak link between output gaps and marginal costs. In other words, while production costs feed directly into firms’ pricing decisions, movements in output (or unemployment) bear only a loose relationship to inflation.

From a conceptual standpoint, the conventional PC holds only if marginal cost and the output gap move proportionally—an assumption that requires, among other things, perfectly flexible wages. When these conditions fail, the output gap may be a poor proxy for real marginal cost, biasing estimates of PC downward. Moreover, even if proportionality roughly holds, the output-based slope equals the cost-based slope scaled by the elasticity of marginal cost with respect to output. If this elasticity is low, the slope of output-based PC will be low as well, even if the slope of the cost-based PC is sizable.

These results are confirmed in the data. Focusing on the pre-pandemic period (1999–2019), we estimate a very low elasticity of marginal cost with respect to output. This finding helps explain why the cost-based PC is steep while the conventional PC looks flat.

Lessons for the Post-Pandemic Inflation Surge

Our findings show a strong pass-through from marginal costs to prices, which explains why the cost-based Phillips curve matches inflation dynamics so well. The weak link between output and marginal cost, on the other hand, helps explain why the conventional output-gap version of the PC looks “flat.” In normal times, two factors drive this low elasticity: firms’ cost schedules tend to display nearly constant short-run returns to scale, so marginal costs barely move with output; and wage rigidity further dampens any feedback from demand to costs.

The pandemic and its aftermath revealed how quickly these relationships can change under stress. Severe shocks—whether from labor market tightness or supply chain bottlenecks—pushed firms against capacity limits, sending marginal costs sharply higher and fueling inflation. At the same time, the slope of the Phillips curve itself can shift. Pre-pandemic data showed stable adjustment frequencies and an approximate linear relationship between inflation and (percentage) changes in real marginal costs. More recently, however, firms have been adjusting prices much more often, raising the elasticity of inflation with respect to costs and generating nonlinear inflation dynamics. I will talk about nonlinear inflation dynamics—what it means, how it works, and what it implies—in a companion post on Liberty Street Economics.

Simone Lenzu is a financial research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post: Simone Lenzu, “Anatomy (not Autopsy) of the Phillips Curve,” Federal Reserve Bank of New York Liberty Street Economics, February 4, 2026, https://doi.org/10.59576/lse.20260204 BibTeX: View |

@article{

Lenzu2026,

author={Lenzu, Simone},

title={Anatomy (not Autopsy) of the Phillips Curve},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={February 4},

year={2026},

url={https://doi.org/10.59576/lse.20260204}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

Treasury Secretary Scott Bessent today reiterated the Trump administration’s push for regulatory tailoring during a sometimes contentious congressional hearing that touched on several issues, from stablecoin regulation to community development financial institutions.

Bessent appeared before the House Financial Services Committee to give the annual report of the Financial Stability Oversight Council. He often sparred with committee Democrats over administration policy. But he also emphasized the administration’s deregulatory push, which he argued would help community banks by easing the compliance burden on the institutions.

“Under the regulatory straitjacket that emerged, that pushed lending outside the traditional banking system, small banks became too small to succeed,” Bessent said. “I think that we have to tailor to the risk for people who know their communities, who are concentrated geographically.”

As for other issues, Bessent was asked by Rep. Joyce Beatty (D-Ohio) about why the Community Development Financial Institution Fund had yet to allocate most of the 2025 program funds. Bessent declined to answer after Beatty sought a yes or no response to her question, but the Treasury Department in December announced increased oversight of CDFI Fund awards.

Bessent said regulators are moving with “deliberate speed” to implement a regulatory framework for stablecoins, as required by passage of the Genius Act. He was also asked by Rep. Jim Hines (D-Conn.) about President Trump’s endorsement of a one-year, 10% cap on credit card interest rates, specifically whether a cap would harm subprime borrowers.

“That would be very important to examine as it is being put in,” Bessent said about the cap.

As banks digitize their lending processes and seek to expand credit access across borders, it is becoming increasingly difficult to make fast, accurate credit decisions. To mitigate risk, lenders need real-time insights into spending habits, automated functionality, and visibility into a broader set of data, especially as they seek to improve speed, enhance the customer experience, and maintain compliance.

At FinovateEurope 2026, a new group of fintechs will showcase how they are addressing these challenges by bringing intelligence and automation directly into the lending process. From sourcing alternative credit data to deploying AI-driven lending agents, the companies below are helping banks and lenders modernize credit decisioning while keeping risk in check.

FinovateEurope 2026 will take place at London’s InterContinental O2 on February 10 and 11. Tickets are available now. Visit our FinovateEurope hub today and save your spot!

Intuitech brings live AI agents into lending workflows to automate manual, time-consuming processes across origination and servicing. The company helps lenders streamline tasks including data collection, validation, and borrower interactions. This automation helps reduce operational burden while improving speed and consistency.

By embedding AI agents directly into clients’ lending operations, Intuitech enables them to scale their lending activity without requiring additional talent in-house. The automated approach helps bring modern credit delivery to lenders of all sizes.

Mifundo’s technology enables customers to assess cross-border credit risk by sourcing and standardizing credit data from across European markets. The company helps lenders better evaluate borrowers with international financial histories by assess creditworthiness for mobile, expatriate, and cross-border customers. Mifundo enables banks to reach more borrowers, as many are underserved by traditional credit systems and therefore are overlooked.

With remote work becoming more popular and the potential for cross-border lending increasing, firms are realizing that there is a gap in data for European credit markets. Mifundo closes this gap by expanding access to reliable credit information, ultimately helping lenders minimize risk while unlocking new lending opportunities across borders.

sea.dev provides real-time risk insights designed to help lending teams make better credit decisions across the loan lifecycle. The company’s platform aggregates and analyzes borrower, portfolio, and market-level data to offer lenders clearer visibility into risk exposure, ultimately supporting faster approvals.

sea.dev enables lending teams to continuously monitor risk and adapt decisions as inputs change. The company’s more dynamic, insight-driven approach helps lenders explore more products and serve new borrower segments.

Why banks should care

With more consumer data available than ever before, lenders can now underwrite loans more effectively, especially for customers who were once considered risky or had limited credit histories. This abundance of data also introduces new challenges, including inaccurate, unclean, or cross-border information that can complicate analysis and require specialized expertise. Fortunately, new tools are emerging to help automate data collection, filtering, and validation. These tools have the potential to enable lenders of all sizes to expand their reach and better serve a broader customer base.

The relationship between inflation and real economic activity has long been central to debates in macroeconomics and monetary policy. At the core of this debate is the Phillips curve (PC), which measures how strongly inflation reacts to movements in economic conditions. The steepness of this curve matters enormously for monetary policy: if the PC is steeper, inflation rises faster during booms and falls faster in recessions, which entails central banks having to act more forcefully if they want to stabilize inflation around their target. Prior analysis found astonishingly small estimates of the slope of the PC, which suggests that the curve is “flat” (or even dead). In this post, I present evidence from coauthored research showing that, contrary to the conventional view, the Phillips curve is alive and steep, and it captures inflation volatility remarkably well once real marginal cost is used instead of standard real economic activity measures.

The Conventional Formulation of the Phillips Curve

The Phillips curve links inflation to expectations of future inflation and a measure of economic slack. In the conventional formulation of the PC, economic slack is typically proxied by the output or unemployment gaps—the deviation of output or employment from its natural level:

In this view, inflation rises when the economy overheats and falls during slowdowns. The slope of the Phillips curve,Kin the equation above, captures how sensitive inflation is to these fluctuations. A large body of research finds that the PC is quite flat—the slope is very small—implying that inflation hardly moves in response to shifts in output or employment gaps. These findings have long puzzled economists and fueled debate about how active monetary policy should be to steer inflation.

The Primitive (Cost-Based) Formulation of the Phillips Curve

There is another way to think about inflation dynamics and its drivers. At its foundation, the Phillips curve emerges from the aggregation of firms’ pricing decisions in response to changes in production costs. In the primitive formulation of the PC, the variable influencing inflation is real marginal cost in percentage deviation from trend, rather than the output or unemployment gap:

In this view, inflation rises when economic forces increase firms’ production costs. The slope of the curve reflects how strongly (and quickly) these costs are passed through into output prices.

The Slope of the Cost-Based Phillips Curve

The cost-based formulation makes it easier to understand the key forces that determine the slope of the PC. In theory, if markets were perfectly competitive and frictionless, prices would move one-for-one with costs: any increase in wages or input prices would be instantly reflected in consumer prices. That is, the slope would be one.

Reality is very different. Firms typically adjust prices infrequently, since doing so involves both direct costs (such as relabeling or updating systems) and indirect costs (such as confusing customers or losing goodwill). In addition, firms often set prices strategically, choosing to delay changes until they are sure cost pressures will last, or timing revisions to match competitors. Thus, frictions that lead to infrequent price changes and strategic considerations in price setting weaken the transmission of cost shocks into prices. The more firms deviate from the ideal of flexible, competitive markets, the flatter the Phillips curve becomes.

Estimating the Slope of the Cost-Based Phillips Curve Using Microdata

How steep is the cost-based PC in the data? Answering this question is notoriously difficult, particularly when the estimation is solely based on aggregate data in which many shocks influence inflation and real activity at the same time. To address this problem, we turn to firm-level evidence. In a recent paper coauthored with Mark Gertler (New York University), Luca Gagliardone (Yale University), and Joris Tielens (National Bank of Belgium), we use detailed microdata on prices and costs to study how individual firms adjust their prices in response to changes in production costs. This approach allows us to quantify how nominal rigidities (infrequent price changes) and real rigidities (strategic interactions among firms) dampen the response of prices to cost shocks. With these estimates we recover the slope of the primitive form of the Phillips curve.

Our analysis suggests a strong link between inflation and real economic conditions, as captured by producers’ costs. On average, firms keep prices fixed for three to four quarters, confirming a substantial degree of nominal rigidity. We also find strong evidence of strategic complementarities: firms adjust less aggressively because they prefer to move in step with competitors, which cuts the pass-through of cost shocks roughly in half. Taking these frictions into account, we estimate the slope of the cost-based Phillips curve to be three to ten times larger than the estimates for the output- or unemployment-based PC formulation. This implies that the Phillips curve is steep, not flat, even in normal times.

Accounting for Aggregate Inflation Dynamics

Cost pass-through plays a dominant role in shaping aggregate inflation. To illustrate this, we build a cost index by combining firm-level changes in labor and input costs and then feed it into the cost-based Phillips curve. Using the Belgian manufacturing sector as a case study, we construct a model-generated inflation series by feeding data on costs into the Phillips curve. The results, shown in the chart below, show that the predicted inflation aligns very closely with actual producer price inflation (PPI) in Belgium. The two series are highly correlated, with a correlation coefficient above 80 percent; quantitatively, movements in production costs alone account for about 70 percent of observed inflation fluctuations, highlighting the central role of costs in driving inflation dynamics.

Through the Lens of the Cost-Based Phillips Curve, Fluctuations in Production Costs Account Well for Inflation Volatility

Source: Gagliardone, Gertler, Lenzu, and Tielens (2025). Notes: The blue line represents the time series of manufacturing PPI in Belgium. The red line is the model-implied manufacturing PPI obtained feeding an aggregate cost index to a cost-based PC.

Reconciling the Steep Cost-Based Phillips Curve with the Flat Output-Based Phillips Curve

These results raise a natural question: Why does the cost-based Phillips curve slope steeply while the output-based one appears flat? And are these findings at odds with previous research?

Our research shows that the “flatness” of the conventional Phillips curve reflects a weak link between output gaps and marginal costs. In other words, while production costs feed directly into firms’ pricing decisions, movements in output (or unemployment) bear only a loose relationship to inflation.

From a conceptual standpoint, the conventional PC holds only if marginal cost and the output gap move proportionally—an assumption that requires, among other things, perfectly flexible wages. When these conditions fail, the output gap may be a poor proxy for real marginal cost, biasing estimates of PC downward. Moreover, even if proportionality roughly holds, the output-based slope equals the cost-based slope scaled by the elasticity of marginal cost with respect to output. If this elasticity is low, the slope of output-based PC will be low as well, even if the slope of the cost-based PC is sizable.

These results are confirmed in the data. Focusing on the pre-pandemic period (1999–2019), we estimate a very low elasticity of marginal cost with respect to output. This finding helps explain why the cost-based PC is steep while the conventional PC looks flat.

Lessons for the Post-Pandemic Inflation Surge

Our findings show a strong pass-through from marginal costs to prices, which explains why the cost-based Phillips curve matches inflation dynamics so well. The weak link between output and marginal cost, on the other hand, helps explain why the conventional output-gap version of the PC looks “flat.” In normal times, two factors drive this low elasticity: firms’ cost schedules tend to display nearly constant short-run returns to scale, so marginal costs barely move with output; and wage rigidity further dampens any feedback from demand to costs.

The pandemic and its aftermath revealed how quickly these relationships can change under stress. Severe shocks—whether from labor market tightness or supply chain bottlenecks—pushed firms against capacity limits, sending marginal costs sharply higher and fueling inflation. At the same time, the slope of the Phillips curve itself can shift. Pre-pandemic data showed stable adjustment frequencies and an approximate linear relationship between inflation and (percentage) changes in real marginal costs. More recently, however, firms have been adjusting prices much more often, raising the elasticity of inflation with respect to costs and generating nonlinear inflation dynamics. I will talk about nonlinear inflation dynamics—what it means, how it works, and what it implies—in a companion post on Liberty Street Economics.

Simone Lenzu is a financial research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post: Simone Lenzu, “Anatomy (not Autopsy) of the Phillips Curve,” Federal Reserve Bank of New York Liberty Street Economics, February 4, 2026, https://doi.org/10.59576/lse.20260204 BibTeX: View |

@article{

Lenzu2026,

author={Lenzu, Simone},

title={Anatomy (not Autopsy) of the Phillips Curve},

journal={Liberty Street Economics},

note={Liberty Street Economics Blog},

number={February 4},

year={2026},

url={https://doi.org/10.59576/lse.20260204}

}

Disclaimer The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

Sandoz Group (OTCMKTS:SDZNY – Get Free Report) and CERo Therapeutics (NASDAQ:CERO – Get Free Report) are both medical companies, but which is the better business? We will compare the two businesses based on the strength of their dividends, valuation, analyst recommendations, institutional ownership, profitability, risk and earnings.

Insider & Institutional Ownership

0.1% of Sandoz Group shares are owned by institutional investors. Comparatively, 29.6% of CERo Therapeutics shares are owned by institutional investors. 0.4% of CERo Therapeutics shares are owned by company insiders. Strong institutional ownership is an indication that hedge funds, endowments and large money managers believe a stock is poised for long-term growth.

Analyst Ratings

This is a summary of recent ratings and target prices for Sandoz Group and CERo Therapeutics, as reported by MarketBeat.

Sell Ratings

Hold Ratings

Buy Ratings

Strong Buy Ratings

Rating Score

Sandoz Group

0

1

0

1

3.00

CERo Therapeutics

1

3

0

0

1.75

CERo Therapeutics has a consensus price target of $45.00, indicating a potential upside of 92,683.51%. Given CERo Therapeutics’ higher possible upside, analysts plainly believe CERo Therapeutics is more favorable than Sandoz Group.

Profitability

This table compares Sandoz Group and CERo Therapeutics’ net margins, return on equity and return on assets.

Net Margins

Return on Equity

Return on Assets

Sandoz Group

N/A

N/A

N/A

CERo Therapeutics

N/A

N/A

-209.40%

Volatility and Risk

Sandoz Group has a beta of 0.52, suggesting that its share price is 48% less volatile than the S&P 500. Comparatively, CERo Therapeutics has a beta of 0.27, suggesting that its share price is 73% less volatile than the S&P 500.

Earnings & Valuation

This table compares Sandoz Group and CERo Therapeutics”s top-line revenue, earnings per share and valuation.

Gross Revenue

Price/Sales Ratio

Net Income

Earnings Per Share

Price/Earnings Ratio

Sandoz Group

$10.36 billion

3.31

$1.00 million

N/A

N/A

CERo Therapeutics

N/A

N/A

-$8.30 million

($102.61)

0.00

Sandoz Group has higher revenue and earnings than CERo Therapeutics.

Summary

Sandoz Group beats CERo Therapeutics on 6 of the 9 factors compared between the two stocks.

Sandoz Group AG develops, manufactures, and markets generic pharmaceuticals and biosimilars worldwide. The company covers therapeutic areas, including cardiovascular, central nervous system, oncology, infectious diseases, pain and respiratory, diabetes, immunology, endocrinology, hematology, and ophthalmology, as well as bone disease. It also provides a portfolio of active pharmaceutical ingredients and finished dosage forms. The company was founded in 1886 and is headquartered in Basel, Switzerland.

CERo Therapeutics Holdings, Inc., an immunotherapy company, focuses on advancing the development of engineered T cell therapeutics for the treatment of cancer. Its lead program in hematologic malignancies targets an Eat Me signal upregulated on B cell and myeloid tumors. The company is based in South San Francisco, California.

Receive News & Ratings for Sandoz Group Daily – Enter your email address below to receive a concise daily summary of the latest news and analysts’ ratings for Sandoz Group and related companies with MarketBeat.com’s FREE daily email newsletter.

Compliance and fraud prevention platform Sumsub has teamed up with digital asset infrastructure solutions provider Fireblocks to provide Travel Rule compliance.

The Travel Rule is a regulation mandated by the Financial Action Task Force (FATF) designed to fight money laundering and terrorist financing. The rule requires financial institutions and Virtual Asset Service Providers (VASPs) to share specific information about the sender and receiver of funds during certain transactions. Enacted to defend traditional financial transactions from money laundering and terrorist financing, the rule has been extended to cover cryptocurrencies and digital assets.

Courtesy of the partnership, Sumsub’s Travel Rule solution will be natively integrated into the Fireblocks platform. This will provide both financial institutions and VASPs with real-time, automated, and dynamic verification for virtual asset transactions. Fireblocks users will benefit from complete control over compliance workflows, enabling them to customize these workflows to fit their preferred risk profiles. The integration features automated and encrypted Travel Rule data exchange between VASPs, supporting faster and more secure stablecoin payments.

“We’re excited to partner with Fireblocks to bring native Travel Rule compliance directly into one of the world’s leading digital asset infrastructure platforms,” the company noted on its X page. “Together we’re setting a new standard for Travel Rule compliance—secure, automated, and designed for scale—helping businesses power faster, safer, and fully compliant stablecoin payments.”

The Sumsub/Fireblocks partnership comes at a time of increased interest in stablecoins, with stablecoin volumes nearing $1 trillion per month in 2025, twice the levels of the previous year. The rise of stablecoins has put pressure on the fragmented settlement rails and compliance workflows of VASPs and other financial institutions. Further, evolving regulations—from MiCA in the European Union to the latest moves from the FATF—are driving firms to improve their ability to manage financial risks associated with virtual assets, including both implementation and operationalization of the Travel Rule.

“As digital asset payments and stablecoin adoption accelerate, our customers need compliance solutions that are robust and operationally seamless,” Fireblocks SVP of Corporate Development & Partnerships Adam Levine said. “By integrating Sumsub’s Travel Rule solution directly into the Fireblocks platform, we’re giving institutions the flexibility to meet global regulatory requirements while maintaining efficient, streamlined transaction workflows.”