U.S. inflation rose 3% in September compared to a year ago, according to the Bureau of Labor Statistics’ latest data. The report shows food items like instant coffee and beef are getting pricier. Instant coffee prices in September were about 22% higher than last year. Prices went up by 0.5% from August to September. Roasted coffee drinkers, however, saw slight relief as prices dropped 0.6%. The Consumer Price Index, released by the BLS, is a common measure of inflation, as it shows the change over time in the prices consumers pay for goods and services. Inflation increased slightly by 0.3% from August to September, coming in lower than economists had predicted.Overall, meat prices saw a monthly increase of 1.6%. The average price for ground beef reached $6.32 per pound, up 12.9% from the year before.The release of the September report was delayed due to the government shutdown and would normally have been released on Oct. 15. It is the only economic data the BLS has released amid the shutdown and is used by the Social Security Administration to calculate next year’s annual cost-of-living adjustment for benefits.The White House on Friday said it’s unlikely the BLS will release October’s CPI because of the shutdown. Some grocery items, like eggs and lettuce, saw a decrease in prices. Click on the grocery items below to add them to your cart and see whether the total cost of your list has gone up or down. The total cost is based on the average CPI prices from September 2024 to September 2025. PHNjcmlwdCB0eXBlPSJ0ZXh0L2phdmFzY3JpcHQiPiFmdW5jdGlvbigpeyJ1c2Ugc3RyaWN0Ijt3aW5kb3cuYWRkRXZlbnRMaXN0ZW5lcigibWVzc2FnZSIsKGZ1bmN0aW9uKGUpe2lmKHZvaWQgMCE9PWUuZGF0YVsiZGF0YXdyYXBwZXItaGVpZ2h0Il0pe3ZhciB0PWRvY3VtZW50LnF1ZXJ5U2VsZWN0b3JBbGwoImlmcmFtZSIpO2Zvcih2YXIgYSBpbiBlLmRhdGFbImRhdGF3cmFwcGVyLWhlaWdodCJdKWZvcih2YXIgcj0wO3I8dC5sZW5ndGg7cisrKXtpZih0W3JdLmNvbnRlbnRXaW5kb3c9PT1lLnNvdXJjZSl0W3JdLnN0eWxlLmhlaWdodD1lLmRhdGFbImRhdGF3cmFwcGVyLWhlaWdodCJdW2FdKyJweCJ9fX0pKX0oKTs8L3NjcmlwdD4=

The report shows food items like instant coffee and beef are getting pricier. Instant coffee prices in September were about 22% higher than last year. Prices went up by 0.5% from August to September. Roasted coffee drinkers, however, saw slight relief as prices dropped 0.6%.

The Consumer Price Index, released by the BLS, is a common measure of inflation, as it shows the change over time in the prices consumers pay for goods and services. Inflation increased slightly by 0.3% from August to September, coming in lower than economists had predicted.

Overall, meat prices saw a monthly increase of 1.6%. The average price for ground beef reached $6.32 per pound, up 12.9% from the year before.

The release of the September report was delayed due to the government shutdown and would normally have been released on Oct. 15. It is the only economic data the BLS has released amid the shutdown and is used by the Social Security Administration to calculate next year’s annual cost-of-living adjustment for benefits.

The White House on Friday said it’s unlikely the BLS will release October’s CPI because of the shutdown.

Some grocery items, like eggs and lettuce, saw a decrease in prices.

Click on the grocery items below to add them to your cart and see whether the total cost of your list has gone up or down. The total cost is based on the average CPI prices from September 2024 to September 2025.

Deciding when to take Social Security benefits is one of the most important questions to answer in planning your retirement strategy. Second to that is understanding what might increase—or reduce—your benefit amount. Does retirement income count as income for Social Security? No, but working while claiming benefits could shrink the amount that you’re able to collect. Talking to a financial advisor can help you to maximize Social Security benefits in retirement.

Understanding Social Security Benefits

Social Security retirement benefits are designed to provide a supplement source of income to eligible seniors. You can begin taking Social Security retirement benefits as early as 62, though doing so can reduce the amount you receive. Waiting until age 70 to begin taking benefits, meanwhile, can increase your benefit amount.

Benefits are calculated based on your earnings history. Specifically, Social Security considers earned income, wages and net income from self-employment. If any money is withheld from your wages for Social Security or FICA taxes, then your wages are covered by Social Security since you’re paying into the system.

When you apply for benefits, Social Security uses your average indexed monthly earnings to decide how much you qualify for. This average is based on up to 35 years of your indexed earnings and it’s used to calculate your primary insurance amount (PIA). The PIA determines the benefits that are paid out to you once you retire.

Does Retirement Income Count as Income for Social Security?

Retirement income does not count as income for Social Security and won’t affect your benefit amount. Specifically, the Social Security Administration excludes the following from income:

None of these are considered earnings for Social Security purposes. Again, Social Security only looks at money that you actually earn from working a job or being self-employed. That means that you could collect Social Security benefits while also taking withdrawals from a 401(k) or individual retirement account (IRA) or receiving payments from an annuity. Reverse mortgages won’t affect your Social Security benefits or eligibility for Medicare either.

With a reverse mortgage, you tap into your home equity but instead of making payments to a lender, the lender makes payments to you. You don’t have to pay anything back towards the reverse mortgage as long as you’re living in the home. Many retirees choose to supplement Social Security benefits with a reverse mortgage.

Does Working in Retirement Reduce Social Security Benefits?

Financial advisor explaining someone’s retirement social security tax obligation

Under Social Security rules, you’re considered to be retired once you begin receiving benefits. If you’re below full retirement age but still working, Social Security can deduct $1 from your benefit payments for every $2 you earn above the annual limit. For 2023, the limit is $21,240.

In the year you reach your full retirement age (FRA), the deduction changes to $1 for every $3 earned above a different annual limit. For 2023, the limit is $56,520. Once you reach your full retirement age, your benefits are no longer reduced regardless of how much you earn. Social Security will also recalculate your benefit amount so that you get credit for any months that your benefits were reduced because of your earnings.

Coordinating Retirement Withdrawals and Social Security

Deciding when to take Social Security benefits starts with considering your other sources of retirement income. For example, that might include:

You could also add a health savings account (HSA) here, though it’s technically not a retirement account. An HSA lets you save money on a tax-advantaged basis for healthcare expenses but once you turn 65, you can withdraw money from it for any reason without a tax penalty. You would, however, pay ordinary income tax on the distribution.

From a tax perspective, it usually makes sense to start with taxable accounts first, then tax-advantaged accounts for withdrawals, leaving Roth and Roth-designated accounts last. In doing so, you allow your Roth investments to continue growing tax-free until you need them.

In terms of when to take Social Security benefits, delaying usually makes sense if you’re hoping to get a larger payout or you have other sources of income to rely on. You might also consider putting off taking benefits if you plan to continue working up until your full retirement age, as that could allow you to claim a larger benefit amount.

Creating Multiple Streams of Income for Retirement Without Affecting Social Security

Since retirement income doesn’t count as income for Social Security, it could be to your advantage to have more than one source that you can rely on. You might already be contributing to your 401(k) at work but you could add an IRA into the mix for additional savings.

Whether it makes sense to choose a traditional or Roth IRA can depend on where you expect to be tax-wise once you retire. You might choose a traditional IRA if you expect to be in a lower tax bracket down the line but could benefit from claiming deductible contributions now. On the other hand, a Roth IRA might be preferable if you’d like to be able to withdraw money tax-free in retirement.

An annuity is another option if you’d like to invest money now to generate guaranteed income later. When considering an annuity, it’s important to learn how different types of annuities work and what they can cost.

Real estate might be another possibility if you’re looking for a passive income option that won’t affect your Social Security benefits. You could purchase a rental property or become a flipper, but owning property directly isn’t a requirement. You can also create passive investment income through real estate investment trusts (REITs), real estate crowdfunding platforms or real estate mutual funds.

Talking to a financial advisor can give you a better idea of how to create multiple streams of income for retirement, without affecting your Social Security benefits. An advisor should also be able to help you formulate a strategy for getting the most benefits possible for yourself and your spouse if you’re married.

Bottom Line

Man confused with his social security

Retirement income won’t affect your Social Security benefits, but income earned from working could. If you plan to draw Social Security while working, it’s helpful to know what that might mean for your benefits payout. Getting an early start with saving and investing for retirement could allow you to delay taking Social Security so that you’re able to claim a larger benefit.

Retirement Planning Tips

Working with a financial advisor can help you to fine-tune your retirement plan. Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three vetted financial advisors who serve your area, and you can have a free introductory call with your advisor matches to decide which one you feel is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

Social Security benefits are taxable for retirees who have substantial income from wages, self-employment, interest and dividends. If you’re working while claiming benefits or earning interest and dividend income, you may have to pay taxes on some of your benefits, depending on how much income you have.

Check out our free retirement calculator for a quick estimate on what you can expect based on your age, expected retirement and sources of income.

Keep an emergency fund on hand in case you run into unexpected expenses. An emergency fund should be liquid — in an account that isn’t at risk of significant fluctuation like the stock market. The tradeoff is that the value of liquid cash can be eroded by inflation. But a high-interest account allows you to earn compound interest. Compare savings accounts from these banks.

Social Security has been one of the most important social programs in the U.S. for decades. For retirement specifically, it provides vital income to millions of Americans across the country. After years of paying Social Security taxes, beneficiaries reap the rewards with a financial safety net of sorts.

However, these benefits aren’t restricted only to people who worked and paid taxes over the years. For example, Social Security allows spousal benefits to support non-working or low-earning spouses in retirement. For any couple that is nearing or in retirement and putting financial plans in place, here are three things they should know about Social Security spousal benefits.

Image source: Getty Images.

1. How Social Security spousal benefits work

Social Security typically calculates a recipient’s monthly benefits using a formula that factors in their 35 highest-earning years of income. But a spouse can receive Social Security benefits based on their partner’s earning record if they’re at least 62 years old or caring for a child under 16 or with a disability.

Assuming the person claiming spousal benefits is at full retirement age, they’re eligible to receive 50% of their spouse’s primary insurance amount too.

For example, if spouse A’s earnings record gives them a monthly benefit of $2,000 at their full retirement age, spouse B could receive up to $1,000 monthly as well. The exact amount will depend on the age at which spouse B claims benefits.

2. The impact of claiming benefits early or late

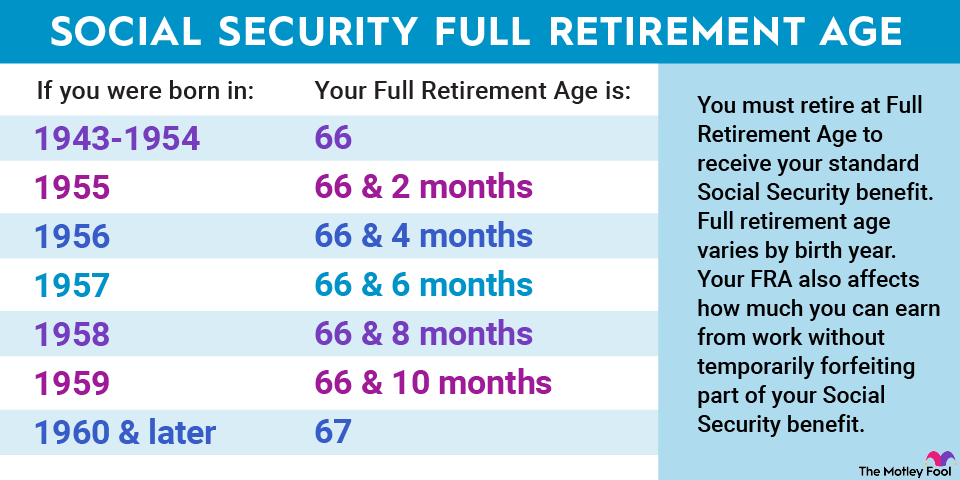

Chart showing Social Security full retirement ages by birth year.

Your full retirement age is one of the most important numbers related to Social Security because it tells you when you’re eligible to receive your primary insurance amount. However, you don’t have to claim benefits at your full retirement age; you can claim them early (which reduces your payout) or delay (which increases your payout).

Claiming Social Security benefits early affects a spouse and their partner receiving spousal benefits in different ways.

Looking first at the person claiming based on their work record, their benefits are reduced by 5/9 of 1% each month before their full retirement age, up to 36 months. Each month after that further reduces benefits by 5/12 of 1%. Here’s an example: Someone with a full retirement age of 67 who claims benefits at 62 will see their monthly benefit reduced 30% from their primary insurance amount.

For the person receiving spousal benefits, benefits are reduced by 25/36 of 1% each month before their full retirement age, up to 36 months, and then they go down 5/12 of 1% each month thereafter. So a person with the same full retirement age (67) claiming spousal benefits at 62 would see their checks reduced 35%.

Although benefits typically increase if you wait beyond your full retirement age, these delayed retirement credits don’t apply to spousal benefits.

3. What happens if a spouse passes away

Social Security spousal and survivors benefits can be closely linked as the latter extends critical financial assistance after a partner has passed away.

If you’re claiming spousal benefits when your partner passes away, Social Security will convert your spousal benefits to survivors benefits. Survivors benefits make you eligible to receive up to 100% of your deceased spouse’s benefit, including any delayed retirement credits they earned prior to their passing. A widow or widower can begin receiving survivors benefits at age 60 (50 if dealing with a disability), but as in the case with spousal benefits, they’ll be reduced if claimed before full retirement age.

You can’t simultaneously receive spousal and survivors benefits, only whichever is higher. Since spousal benefits max out at 50% of the partner’s primary insurance amount, survivors benefits are typically the higher-paying option.

The $21,756 Social Security bonus most retirees completely overlook If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $21,756 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

Among retirement rules of thumb, saving 10 times your salary by 67 reigns supreme. But workers should also have another way by planning for their savings to provide 45% of their pretax, preretirement income.

Financial services giant Fidelity has a rule for retirement savings you may have heard of: Have 10 times your annual salary saved for retirement by age 67. This oft-cited guideline can help you identify a retirement savings goal, but it doesn’t fully account for how much of those savings will cover in retirement.

Enter Fidelity’s 45% rule, which states that your retirement savings should generate about 45% of your pretax, pre-retirement income each year, with Social Security benefits covering the rest of your spending needs.

A financial advisor can analyze your income needs and help you plan for retirement. Find an advisor today.

The financial services firm analyzed spending data for working people between 50 and 65 years old and found that most retirees need to replace between 55% and 80% of their pre-retirement income in order to preserve their current lifestyle. Because retirees have lower day-to-day expenses and don’t typically contribute to retirement accounts, their income requirements are lower than people who are still working.

As a result, a retiree who was earning $100,000 a year would need between $55,000 and $80,000 per year in Social Security benefits and savings withdrawals (including pension benefits) to continue their current lifestyle.

Fidelity’s 45% guideline dictates that a retiree’s nest egg should be large enough to replace 45% of their pre-retirement, pretax income each year. Following this rule, the same retiree who was earning $100,000 per year would need enough saved up to spend $45,000 a year, in addition to his Social Security benefits, to fund his lifestyle. Assuming the person lives another 25 years after reaching retirement age, this person would need $1.125 million in savings.

If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

Pre-Retirement Income Plays an Important Role

Among retirement rules of thumb, saving 10 times your salary by 67 reigns supreme. But workers should also have another way by planning for their savings to provide 45% of their pretax, preretirement income.

But all retirement spending plans aren’t equal. Those who earned less money during their careers will have less saved than high earners, and as a result, will need to replace a larger proportion of their pre-retirement income.

“Your salary plays a big role in determining what percentage of your income you will need to replace in retirement,” Fidelity wrote in its most recent Viewpoints. “People with higher incomes tend to spend a small portion of their income during their working years, and that means a lower income replacement goal in percentage terms to maintain their lifestyle in retirement.”

According to Fidelity, a person who makes $50,000 per year would need savings and Social Security to replace approximately 80% of his income in retirement. An individual earning $200,000, however, could get by in retirement by replacing just 60%.

Social Security plays a less significant role in the retirement plans of higher-earning workers. Consider the table below:

Replacing Income Using Fidelity’s 45% Rule Pre-Retirement Income Replacement Rate From Savings Replacement Rate From Social Security Total Replacement Rate $50,000 45% 35% 80% $100,000 45% 27% 72% $200,000 45% 16% 61% $300,000 44% 11% 55%

According to Fidelity, a retiree who made $50,000 per year would receive 35% of that income via Social Security. But a high-earning individual who made $300,000 per year would only see 11% of his income replaced by Social Security benefits. While higher-earning individuals don’t need to replace as much of their pre-retirement income, retirement savings plays a more important role for these types of retirees.

Bottom Line

Among retirement rules of thumb, saving 10 times your salary by 67 reigns supreme. But workers should also have another way of figuring: planning for their savings to provide 45% of their pretax, preretirement income.

Fidelity’s 10x rule of thumb is a nifty guideline to follow as you save for retirement over the course of many decades. But when retirement arrives, Fidelity recommends that your savings should cover 45% of your income needs, with Social Security covering the rest. As a result, the average retiree will need to replace between 55% and 80% of his pre-retirement, pretax income to maintain his current lifestyle.

Tips for Retirement Planning

A financial advisor can be an invaluable resource when it comes to planning for retirement. Whether it’s saving in tax-advantaged accounts or mapping out your income needs, an advisor can help you with your retirement planning needs.

Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

While people can start collecting Social Security benefits at age 62, delaying collection will result in higher benefits. SmartAsset’s Social Security calculator can help you develop a collection plan that enables you to maximize your benefits and enjoy retirement.

At 67, you’re presumably at or near retirement. If you have $1 million in IRAs, it may be attractive to converting to a Roth because it can provide tax-free income in retirement.

It’s not too late from legal or regulatory perspectives. The IRS does not restrict Roth conversions on the basis of age or income. If you have existing traditional IRA assets, you can convert them. However, when making this decision at a later stage of life, noteworthy financial tradeoffs around taxes, healthcare costs, estate planning and more come into play. Ask a financial advisor if Roth IRA conversion makes sense for you.

Understanding Roth IRA Conversions

A Roth conversion involves moving retirement savings from a traditional IRA account into a Roth IRA account. Traditional IRA contributions provide tax deductions, lowering your taxable income each year you contribute. But traditional IRA withdrawals taken during retirement get taxed as ordinary income based on whatever tax bracket you fall into at that time.

Roth IRAs work in the opposite manner. Contributions are made using after-tax dollars, so you don’t lower your current taxable income with contributions. However, qualified withdrawals later in retirement are completely tax-free. The conversion catch is that when you do one you have to pay any taxes due now on the funds you convert. This is not an insignificant concern.

A 67-year-old couple converting their entire $1 million traditional IRA into a Roth version in a single year would owe income tax immediately on the entire converted balance. This lump of income would also put them into the highest income tax bracket. Tax rates could be as high as 37% federally, plus applicable state taxes of 5% to 13% depending on your location. Naturally, few people are eager to write a six-figure check to the IRS, although there are ways to make this less painful.

Let’s walk through what could happen if a retired 67-year old couple with $1 million in a traditional IRA and average combined annual Social Security benefits of about $44,000 decides to convert to a Roth IRA. There are two main ways of doing this, including all at once and over time.

If they opted to convert the entire $1 million IRA balance to a Roth IRA in a single tax year, they would incur federal and state income taxes that year on the full $1 million converted amount, placing them in the highest income tax bracket. Total ordinary tax rates could approach 40% to 45%, or $400,000 to $450,000 on a $1-million conversion.

That’s the all-at-once approach. By taking their time and spreading the $1 million conversion over 10 years at $100,000 converted per year, they would only owe income tax each year on $100,000. Assuming for this example that Social Security benefits and income tax brackets stay unchanged, they would be in the 22% federal tax bracket. They would owe $22,000 federal tax on each $100,000 conversion, a much more manageable bill. Plus, total tax over 10 years comes to $220,000 or about half as much as the all-at-once approach.

They would still owe taxes on their Social Security benefits as well in each of those 10 years. But diverting some savings into the Roth IRA provides some future tax-free income capacity that can be drawn on to balance out taxes owed later on traditional 401(k) or IRA withdrawals. Conversion diversification lets them prudently minimize their overall lifetime tax liability. It also creates a pool of tax-free legacy money if they eventually gift a portion of the Roth account to children or grandchildren.

You can review your options for minimizing taxes and maximizing retirement income with a financial advisor.

Additional Roth IRA Conversion Considerations

Other factors also may weigh on a sizable Roth IRA conversion decision. For instance, realizing the conversion income could impact taxation of Social Security benefits, Medicare premiums and eligibility for certain tax credits like the Premium Tax Credit. Any Required Minimum Distributions (RMDs) already taking place on the existing traditional IRA would need to be accounted for in multi-year projections also.

Estate plans should also be taken into account. For instance, if you plan to leave all your wealth to a charity, it likely makes sense to leave funds in the traditional IRA rather than converting to a Roth because the charity won’t owe taxes on the bequest. You’ll also need to ensure beneficiaries on the Roth are named correctly and evaluate the conversion’s impact on any trusts you have set up.

If you’re thinking about doing a large Roth conversion, consider this process:

First, clarify what should happen to the IRA assets upon death – if the goal is leaving an inheritance to heirs entirely tax-free, then doing calculated Roth conversions can guarantee that continued tax-free growth.

Next, assess current marginal and future effective tax rates in retirement. If rates seem likely to rise substantially due to tax code changes, paying taxes now through a conversion could save money later.

Finally, analyze existing income streams, multi-year tax scenarios, healthcare budget and estate plans.

In most cases, you’ll wind up choosing not to convert all at once. For those with large traditional IRAs, strategic partial conversions tailored to your needs often makes the most financial sense. A financial advisor can help you weigh your options.

Bottom Line

In summary, once you reach 67 years old and beyond, you still can convert all or part of your traditional IRA assets over to a Roth IRA. That doesn’t mean you should, however. To decide if this aligns with your, assess your multi-year tax picture, compare current and future tax brackets, understand total costs and implications involved, and pick a Roth conversion approach that works your particular financial situation. Converting everything in one year often won’t make as much sense as spreading conversions over time.

Tips

A financial advisor can explain how a Roth IRA conversion would impact tax bills, estate planning, healthcare costs and more. SmartAsset’s free tool matches you with up to three financial advisors in your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

The simplest answer is yes: Social Security income is generally taxable at the federal level, though whether or not you have to pay taxes on your Social Security benefits depends on your income level. If you have other sources of retirement income, such as a 401(k) or a part-time job, then you should expect to pay income taxes on your Social Security benefits. If you rely exclusively on your Social Security checks, though, you probably won’t pay taxes on your benefits. State laws vary on taxing Social Security. Regardless, it’s a good idea to work with a financial advisor to help you understand how different sources of retirement income are taxed.

Is My Social Security Income Taxable?

According to the IRS, the quick way to see if you will pay taxes on your Social Security income is to take one half of your Social Security benefits and add that amount to all your other income, including tax-exempt interest. This number is known as your combined income (combined income = adjusted gross income (AGI) + nontaxable interest + half of your Social Security benefits).

If your combined income is above a certain limit (the IRS calls this limit the base amount), you will need to pay at least some tax.

The limit is $25,000 if you are a single filer, head of household or qualifying widow or widower with a dependent child. The limit for joint filers is $32,000. If you are married filing separately, you will likely have to pay taxes on your Social Security income.

Calculating Your Social Security Income Tax

If your Social Security income is taxable, the amount you pay in tax will depend on your total combined retirement income. However, you will never pay taxes on more than 85% of your Social Security income. If you file as an individual with a total income that’s less than $25,000, you won’t have to pay taxes on your Social Security benefits in 2021, according to the Social Security Administration.

For the 2021 tax year (which you will file in 2022), single filers with a combined income of $25,000 to $34,000 must pay income taxes on up to 50% of their Social Security benefits. If your combined income was more than $34,000, you will pay taxes on up to 85% of your Social Security benefits.

For married couples filing jointly, you will pay taxes on up to 50% of your Social Security income if you have a combined income of $32,000 to $44,000. If you have a combined income of more than $44,000, you can expect to pay taxes on up to 85% of your Social Security benefits.

If 50% of your benefits are subject to tax, the exact amount you include in your taxable income (meaning on your Form 1040) will be the lesser of either a) half of your annual Social Security benefits or b) half of the difference between your combined income and the IRS base amount.

Let’s look at an example. Say you’re a single filer who receives a monthly benefit of $1,543, which is the average benefit after the cost of living increase in January 2021. Your total annual benefits would be $18,516. Half of that would be $9,258. Then let’s say you have a combined income of $30,000. The difference between your combined income and your base amount (which is $25,000 for single filers) is $5,000. So the taxable amount that you would enter on your federal income tax form is $5,000, because it is lower than half of your annual Social Security benefit.

The example above is for someone who is paying taxes on 50% of his or her Social Security benefits. Things get more complicated if you’re paying taxes on 85% of your benefits. However, the IRS helps taxpayers by offering software and a worksheet to calculate Social Security tax liability.

If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

How to File Social Security Income on Your Federal Taxes

Once you calculate the amount of your taxable Social Security income, you will need to enter that amount on your income tax form. Luckily, this part is easy. First, find the total amount of your benefits. This will be in box 3 of your Form SSA-1099. Then, on Form 1040, you will write the total amount of your Social Security benefits on line 5a and the taxable amount on line 5b.

Note that if you are filing or amending a tax return for the 2017 tax year or earlier, you will need to file with either Form 1040-A or 1040. The 2017 1040-EZ did not allow you to report Social Security income.

Simplifying Your Social Security Taxes

During your working years, your employer probably withheld payroll taxes from your paycheck. If you make enough in retirement that you need to pay federal income tax, then you will also need to withhold taxes from your monthly income.

To withhold taxes from your Social Security benefits, you will need to fill out Form W-4V (Voluntary Withholding Request). The form only has only seven lines. You will need to enter your personal information and then choose how much to withhold from your benefits. The only withholding options are 7%, 10%, 12% or 22% of your monthly benefit. After you fill out the form, mail it to your closest Social Security Administration (SSA) office or drop it off in person.

If you prefer to pay more exact withholding payments, you can choose to file estimated tax payments instead of having the SSA withhold taxes. Estimated payments are tax payments that you make each quarter on income that an employer is not required to withhold tax from. So if you ever earned income from self-employment, you may already be familiar with estimated payments.

In general, it’s easier for retirees to have the SSA withhold taxes. Estimated taxes are a bit more complicated and will simply require you to do more work throughout the year. However, you should make the decision based on your personal situation. At any time you can also switch strategies by asking the the SSA to stop withholding taxes.

The Impact of Roth IRAs

If you’re concerned about your income tax burden in retirement, consider saving in a Roth IRA. With a Roth IRA, you save after-tax dollars. Because you pay taxes on the money before contributing it to your Roth IRA, you will not pay any taxes when you withdraw your contributions. You also do not have to withdraw the funds on any specific schedule after you retire. This differs from traditional IRAs and 401(k) plans, which require you to begin withdrawing money once you reach 72 years old, or 70.5 if you were born before July 1, 1949.

So, when you calculate your combined income for Social Security tax purposes, your withdrawals from a Roth IRA won’t count as part of that income. That could make a Roth IRA a great way to increase your retirement income without increasing your taxes in retirement.

Another thing to note is that many retirement plans allow individuals, aged 50 years or older, to make annual catch-up contributions. You can make catch-up contributions up to $1,000. These must be made by the due date of your tax return. You have until April 15, 2022 to make the $1,000 catch-up contribution apply to your 2021 Roth IRA contribution total.

State Taxes on Social Security Benefits

Everything we’ve discussed above is about your federal income taxes. Depending on where you live, you may also have to pay state income taxes.

There are 12 states that collect taxes on at least some Social Security income. Two of those states (Minnesota and Utah) follow the same taxation rules as the federal government. So if you live in one of those two states then you will pay the state’s regular income tax rates on all of your taxable benefits (that is, up to 85% of your benefits).

The other states also follow the federal rules but offer deductions or exemptions based on your age or income. So in those nine states, you likely won’t pay tax on the full taxable amount.

The other 38 states (plus Washington, D.C.) do not tax Social Security income.

State Taxes on Social Security Benefits

Taxed According to Federal Rules: Minnesota, Utah

Partially Taxed (Exemptions for Income and Age): Colorado, Connecticut, Kansas, Missouri, Montana, Nebraska, New Mexico, Rhode Island, Vermont, West Virginia

No State Tax on Social Security Benefits: Alabama, Alaska, Arizona, Arkansas, California, Delaware, District of Columbia, Florida, Georgia, Hawaii, Idaho, Illinois, Indiana, Iowa, Kentucky, Louisiana, Maine, Maryland, Massachusetts, Michigan, Mississippi, Nevada, New Hampshire, New Jersey, New York, North Carolina, North Dakota, Ohio, Oklahoma, Oregon, Pennsylvania, South Carolina, South Dakota, Tennessee, Texas, Virginia, Washington, Wisconsin, Wyoming

Don’t miss out on news that could impact your finances. Get news and tips to make smarter financial decisions with SmartAsset’s semi-weekly email. It’s 100% free and you can unsubscribe at any time. Sign up today.

Bottom Line

We all want to pay as little in taxes as possible. That’s especially true in retirement, when most of us have a set amount of savings. But consider that if you have enough retirement income that you’re paying taxes on Social Security benefits, you’re probably in decent shape financially. It means you have income from other sources and you’re not entirely dependent on Social Security to meet living expenses.

You can also save on your taxes in retirement simply by having a plan. Help yourself get ready for retirement by working with a financial advisor to create a financial plan.

Tips for Saving on Taxes in Retirement

Financial advisors can offer valuable guidance and insight into retiree taxes. Finding a qualified financial advisor doesn’t have to be hard. Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

What you pay in taxes during your retirement will depend on how retirement friendly your state is. So if you want to decrease tax bite, consider moving to a state with fewer taxes that affect retirees.

Another way to save in retirement is to downsize your home. Moving into a smaller home could lower your property taxes and it could also lower your other housing costs.

Experts at Social Security Solutions discuss why teachers with non-covered pensions might be missing out on their Social Security benefits.

Press Release –

Oct 26, 2016

Leawood, KS, October 26, 2016 (Newswire.com)

– All too often, teachers with non-covered pensions are told that they don’t qualify for Social Security benefits. In many cases, this is not accurate because most teachers have worked some number of years in “covered” jobs where Social Security taxes were either withheld or paid on their behalf.

“There is a great deal of misinformation around non-covered pensions and Social Security for teachers that leads to many teachers not claiming all the Social Security to which they are entitled,” said Robin Brewton, COO, Social Security Solutions, Inc. “We want to close the knowledge gap.”

By not claiming Social Security benefits, many teachers could be losing tens of thousands of dollars in retirement income to which they are entitled. Teachers can learn more about non-covered pensions and Social Security by viewing this complimentary webinar.

About Social Security Solutions, Inc.

Headquartered in Leawood, KS, Social Security Solutions, Inc. (www.SocialSecuritySolutions.com) delivers advice and education about Social Security benefit claiming strategies to consumers and financial professionals. Social Security Solutions, Inc. leverages its expertise, research and technology to help individuals determine the best strategy for collecting benefits in line with their overall retirement goals.