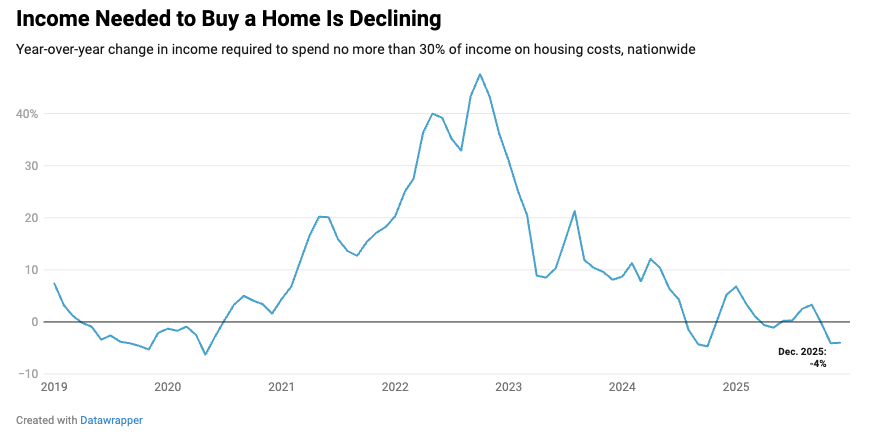

The amount Americans needed to earn declined 4% year over year in December, from $115,870 to $111,252, marking the second month in a row of declines after rising in nearly every month for five years in a row. Income needed to buy a home peaked at $122,000 in June.

Redfin attributed the improvement to lower mortgage rates and slowing home-price growth. The median home sale price in December was $426,747, up slightly from December 2024, but mortgage rates have fallen from 7% last year to about 6.1% now. Those factors brought the median monthly mortgage payment down from $2,800 to $2,675.

“The housing affordability crisis is showing signs of easing as costs come down slightly but meaningfully, opening the door for more Americans to make the jump to homeownership,” said Chen Zhao, Redfin’s head of economics research. “While housing remains historically expensive, the trajectory is finally starting to reverse, with the door to buying a home opening a bit wider rather than closing tighter. But while affordability is improving, Americans are contending with other obstacles on the road to buying a home, like nerves about layoffs and economic uncertainty.”

Redfin considers a home affordable if a buyer taking out a mortgage spends no more than 30% of their income on monthly housing payments. Redfin based its analysis on median home sale prices, prevailing mortgage rates and property tax payments.

Courtesy of Redfin.

While affordability is improving, the typical U.S. household does not earn enough to afford the median-priced home. The typical American household earns just $86,185, about $25,000 less than needed, according to the report.

On a local level, affordability is improving in 37 of the 50 largest U.S. cities, led by Dallas, where required earnings fell 7.4%, and followed by Sacramento, California, and Jacksonville, Florida, where the amount needed was down 6.8% and 5.9%, respectively.

On the flip side, the amount homebuyers needed to earn actually increased in some cities, led by Detroit (up 3.6%) and followed by Chicago (3.5%) and St. Louis (3%)

The typical household could actually afford to buy a median-priced home in only 12 metros, led by Pittsburgh, where buyers needed to earn $66,168, and the typical household earned $82,188, followed by St. Louis, where $73,984 is needed, and the typical household earned $87,471, and Cleveland, where $66,725 was needed, and the typical income was $76,912.

After a year of big moves for Compass, Chairman and CEO Robert Reffkin retained his position as the No. 1 most powerful person in real estate, according to the annual Swanepoel Power 200 from T3 Sixty.

Jeremy Wacksman, CEO of Zillow Group, ranked No. 2, following a profitable year for the real estate portal. T3 Sixty also noted Wacksman’s ongoing battle with Compass over exclusive listings.

No. 3 on the list was Rocket Companies CEO Varun Krishna, who oversaw the group’s acquisition of Redfin in July; followed by eXp World Holdings Founder and CEO Glenn Sanford at No. 4 and Anywhere Real Estate President and CEO Ryan Schneider at No. 5.

Also in the top 10 were Andy Florance, founder and CEO of CoStar Group at No. 6; Chris Kelly, president and CEO of HomeServices of America at No. 7; Howard “Hoby” Hanna IV, CEO of Hanna Holdings at No. 8; Nykia Wright, CEO of the National Association of REALTORS® at No. 9; and Leo Pareja, CEO of eXp Realty at No. 10.

Redfin CEO Glenn Kelman is leaving the company after 20 years, effective Jan. 16.

In an email to employees with the subject line, “Unemployed, In Greenland,” Kelman said the time had come for him to leave after the company completed its integration with Rocket Companies, which acquired the online brokerage for $1.75 billion last year.

“We’ll start the second, much-longer phase at next week’s all-company meeting, which is much-greater scale. Approaching that, I had to decide whether to be at Rocket for years,” Kelman wrote. “Instead, I want to try finding another mission-driven enterprise outside of real estate.”

After Kelman’s departure, Rocket CEO Varun Krishna will take over running Redfin until a successor is found. Kelman said he would remain in an advisory capacity through April 1.

The Federal Trade Commission (FTC) is suing home-search website Zillow, alleging that it paid rival Redfin $100 million to eliminate competition in the online listing business. The suit refers to a deal inked back in February between the two companies in which Redfin allegedly agreed to become “an exclusive syndicator of Zillow listings.”

The allegations suggest that Redfin began copying over listings from Zillow instead of creating its own listings, which gave Zillow much more control over the space. The suit also accuses Redfin of agreeing to end contracts with advertising customers in an alleged attempt to cede more ground to Zillow.

The FTC went on to suggest that this anti-competitive practice would lead to higher prices and worsening terms for both renters and advertisers. “This agreement is nothing more than an end run around competition that insulates Zillow from head-to-head competition on the merits with Redfin for customers advertising multifamily buildings,” the lawsuit said.

Zillow released a statement on the suit, which was published by CNN. The statement called the previous deal with Redfin “pro-competitive and pro-consumer” and noted that “our listing syndication with Redfin benefits both renters and property managers and has expanded renters’ access to multifamily listings across multiple platforms.”

Redfin also disagrees with the allegations from the FTC, saying that “by the end of 2024, it was clear that the existing number of Redfin advertising customers couldn’t justify the cost of maintaining our rentals sales force.” The company went on to suggest that “partnering with Zillow cut those costs and enabled us to invest more in rental-search innovations on Redfin, directly benefiting apartment seekers.”

The FTC further alleges that Redfin laid off hundreds of workers as part of the deal, going on to help Zillow hire some of these employees. Basically, the agency is accusing Zillow of acquiring a large part of Redfin’s business, all while hiding behind the idea of a partnership to avoid scrutiny. The FTC has asked the court to end the agreement and consider a divestiture of assets.

This isn’t the only current legal dispute that Zillow finds itself in. A real estate brokerage company called Compass issued its own lawsuit back in June, accusing Zillow of engaging in anticompetitive practices.

Federal regulators are accusing online real estate firm Zillow of paying rival Redfin $100 million to discourage competition in home rental advertising, harming both renters and property managers.

In a lawsuit filed Tuesday in the U.S. District Court for the Eastern District of Virginia, the Federal Trade Commission alleged the companies struck an “unlawful agreement that eliminates Redfin as a competitor” in the market for placing home rental ads on so-called internet listing services, which the agency notes are widely used by consumers.

Zillow and Redfin, which both operate large real estate listing networks, in February agreed that Redfin would stop competing in the ad market for multifamily properties for nine years and help transition its customers to Zillow, the FTC alleged.

“Paying off a competitor to stop competing against you is a violation of federal antitrust laws,” Daniel Guarnera, director of the FTC’s Bureau of Competition, said in a statement. “Zillow paid millions of dollars to eliminate Redfin as an independent competitor in an already concentrated advertising market — one that’s critical for renters, property managers and the health of the overall U.S. housing market.”

In a statement to CBS news, a Zillow spokesperson said the company’s listing agreement with Redfin “benefits both renters and property managers and has expanded renters’ access to multifamily listings across multiple platforms.”

“It is pro-competitive and pro-consumer by connecting property managers to more high-intent renters so they can fill their vacancies and more renters can get home,” the spokesperson added.

A spokesperson for Redfin said the company “strongly disagrees” with the government’s allegations. “Our partnership with Zillow has given Redfin.com visitors access to more rental listings and our advertising customers access to more renters,” the spokesperson said in a statement.

Mary Cunningham is a reporter for CBS MoneyWatch. Before joining the business and finance vertical, she worked at “60 Minutes,” CBSNews.com and CBS News 24/7 as part of the CBS News Associate Program.

Residential real estate investors bought 18% of all homes that sold in the fourth quarter, and, with elevated home prices and sluggish rents, they’re increasingly attracted to lower-priced homes, according to Redfin.

Residential real estate investors bought 18% of all homes that sold in the fourth quarter, and, with elevated home prices and sluggish rents, they’re increasingly attracted to lower-priced homes, according to Redfin.

Last quarter, investors accounted for 26.1% of sales of homes Redfin considers low-priced, in the bottom third of the market, and that’s a record share of low-priced homes investors purchased.

Redfin defines investor buyers as any institution or business that purchases residential real estate, including corporations, LLCs and real estate investment trusts.

In the D.C. market, the overall share of investment buyers was considerably less, accounting for 10.9% of home sales in the fourth quarter, according to Redfin. That’s partly because D.C. is an expensive market — but that may not be the only reason for lower investor appetite for area homes.

“D.C. is a very expensive market, so it is harder for investors to finance those purchases, or to diversify in expensive markets,” said Daryl Fairweather, chief economist at Redfin. “Also, D.C. has strong renter protections, and investors might find those unappealing, because they are ultimately going to be the landlords.”

The impact on the market for first-time homebuyers is significant. Investor-buyers have more resources, may be less sensitive to borrowing costs and have deeper market knowledge, increasing pressure on an already competitive market for first-time buyers.

Fairweather said investment buyers also tend to have a positive impact on the overall housing market.

“These real estate investment trusts are buying properties and renting them out. The people they are renting them out to are typically lower-income, or have less wealth than a first time homebuyer. So, yes the investor purchaser of the home may be boxing out a first-time homebuyer, and that may seem bad from an equity perspective, but the person who is actually renting the home probably has fewer resources than a first-time homebuyer,”

Pointing the finger at investor-buyers, she said, is not the solution.

“If all we did was ban investors from buying homes, it would actually make it harder for renters to find place to live, but it would make it easier for first-time homebuyers,” Fairweather said. “What we really need to do is increase the overall supply of housing so everyone can find a place to live, regardless of how they are going about it, whether they are buying or renting.”

Last summer, Democratic senators Elizabeth Warren and Sherrod Brown, who chairs the Senate Banking Committee, introduced the Stop Predatory Investing Act to restrict tax breaks for large corporate investors that buy local homes, arguing it drives up costs. It would prohibit investors who acquire 50 or more single-family rental homes from deducting interest and depreciation on them.

A research paper published in March disputed claims that single-family real estate investment trusts are increasing home prices. That paper was authorized in part by the Marshall School of Business, Arizona State University’s W.P. Carey School of Business and the Federal Reserve Bank of Philadelphia.

Regardless, more buyers for fewer properties continues to put upward pressure on home prices. In December, the total supply of homes for sale was 5.1% lower than a year earlier, and far below pre-pandemic levels.

Get breaking news and daily headlines delivered to your email inbox by signing up here.

You don’t have to be a millionaire to buy a home, but earning six figures would help.

The typical American household needs an annual income of $115,000 to afford the median priced home, which is $40,000 more than what the average household makes, according to Redfin chief economist Daryl Fairweather.

“Even places that historically have been affordable now need six figures,” she told CBS MoneyWatch.

In pricey San Francisco, it may not be surprising to learn a household income of in excess of $400,000 is needed to afford the median home. But what about Boise City, Idaho, where the figure $127,000. In fact, a six-figure income is required to buy a median priced home in at least 50 U.S. cities, according to data from Redfin.

Unless you’re a white-collar worker employed remotely who can move to the middle of the country, now may not be the best of time to buy a home. As Greg McBride, chief financial analyst at Bankrate.com, says to those looking to buy a home: “You’re not getting a bargain. In most major markets, particularly east of the continental divide, home prices are at record highs, and the cost of financing the purchase is the highest in more than 20 years.”

Escalating home prices are largely due mortgage rates now at 7.5%, making rent a more affordable option than buying a home in all but four U.S. cities: Detroit, Cleveland Philadelphia and Houston, Fairweather noted.

Also underlying rising home values is the limited supply of existing homes, with owners unwilling or reluctant to sell in an environment where they are carrying a low mortgage rate.

“Mortgage rates may move lower at some point, but we’re not going back to 3% — the 2020 levels are not going to go back,” McBride said.

“It would take a recession, and we don’t want that,” said Fairweather.

Would-be home buyers are getting at least a sliver of relief in the form of the second consecutive weekly drop in the average rate on a typical 30-year mortgage, which last week fell 25 basis points to 7.61%, the Mortgage Bankers Association said Wednesday. The biggest weekly rate drop since June of 2022 fueled a 2.5% weekly hike in mortgage applications, the MBA stated.

The opposite can be said of the rental market, which is seeing increased supply amid new construction and migration slowing, McBride noted. “The rent picture is better of late,” he said. “Supply and demand is not as out of whack as it was coming out of the pandemic. Asking prices are no higher than a year ago.”

Frustrated, aspiring homeowners could benefit, McBride said.

“Rather than stretch to buy a place now, you’re better off taking 18 months to pay down debt, boost savings and see another promotion at work,” he advised. “Homeownership will be much more tenable than it is today. You can do a lot worse than renting in the interim.”

While there are now fewer home purchases than since the Great Recession, more inventory will eventually become available as people move on, whether marrying, divorcing, having a baby or relocating for work, Fairweather said. People should focus on their personal circumstances and “not worry about the timing of the market, because the market is really hard to time.”

Residential real estate tends to go through spurts, McBride added.

“Home prices go up rapidly for two or three years, then they don’t change a lot for six to 10 years,” he said. “There’s some reassurance in that for the aspiring homeowner that has seen prices go up dramatically that it’s not into perpetuity.”

Affluent Americans who can afford to pay cash are more apt to buy homes in such an expensive housing market, when the income necessary to buy a home is higher than ever before, and higher mortgage rates make buying a home in cash and avoiding interest altogether more attractive.

In dollar terms, the median down payment was $60,980 in September, according to Redfin. That’s up roughly 15% from a year earlier, the biggest increase since June 2022.

Many people with the means and desire to buy a second home have already done so.

getty

During the onset of the pandemic, the flexibility to work remotely coupled with record-low interest rates had many home buyers toying with the idea of moving to vacation home markets as shifting priorities and preferences altered where and how people wanted to live.

Vacation home sales skyrocketed during the second half of 2020 and through 2021. Page views of for-sale listings soared in metro areas typically considered vacation destinations, such as the Jersey Shore area; Myrtle Beach, South Carolina; Key West, Florida; Lake Tahoe, Nevada; Cape Cod, Massachusetts; and Park City, Utah.

Today, it’s a different story. A scarcity of new listings, elevated mortgage rates, still-high home prices and persistent inflation, among other economic woes, are holding back demand for both primary and second homes, according to a new report from Redfin.

A variety of factors are causing the huge drop in second-home demand:

Many potential second-home buyers are priced out because it’s frequently more expensive to buy a vacation home than a primary home. The typical second home was worth $465,000 in 2022, versus $375,000 for a primary home. Additionally, the federal government increased loan fees for second homes in April 2022.

Vacation-home buyers are quicker to pull back from the market than primary-home buyers because second homes aren’t a necessity.

Workers are returning to the office. Second homes are less attractive when there’s less time to spend in them. While working from home is more common than it was before the pandemic, the share of job openings that allow remote work has shrunk since early 2022.

Buying a vacation home to rent it out is nowhere near as attractive as it was during the pandemic home buying and investing boom. Owners of short-term rentals are reporting a steep decline in business. That’s because many people became vacation-rental hosts during the pandemic, which led to oversupply. Many local governments are also instituting new short-term-rental regulations, like new taxes and stricter permitting. The long-term rental market is also cooling.

Bank accounts are shrinking as stock markets decline, so would-be buyers have less cash on hand for down payments and monthly payments.

Many people with the means and desire to buy a second home have already done so, during the pandemic home-buying boom of 2020 and 2021.

“With housing payments near their all-time high; a lot of people can’t afford to buy one home right now, let alone a second,” said Redfin deputy chief economist Taylor Marr. “Add the recent increase in loan fees, inflation, shaky financial markets, the end of pandemic-related financial stimulus and many companies calling workers back to the office and it’s simply a challenging time for most Americans to buy a vacation home.”

Jacob Channel, senior economist for LendingTree, agrees.He said,“Ultimately, it’s not surprising that demand for vacation homes has fallen so far from pre-pandemic levels. After all, with mortgage rates as high as they are and with home prices still relatively steep in many parts of the country, buying a vacation home is unlikely to be an affordable endeavor for most. This, combined with the fact that the economy is slowing and a recession appears increasingly likely in the near future, mean that most people probably aren’t going to be particularly keen to stretch their budgets in order to buy a second house.”

Channel added, “Buying a home in today’s market, be it a first or a second house, is going to be tough for most people. And, given that a second home is far from necessity, it makes sense for people to cut back on buying them.”

But there are still some second-home buyers out there, especially in popular vacation destinations. Phoenix Redfin agent Van Welborn said some buyers are looking for vacation condos, especially in desirable neighborhoods.

“It’s mostly affluent cash buyers who don’t have to worry about high rates,” Welborn said. “They’re motivated to buy now because they think they can get a vacation home for under asking price–and in some cases, they’re right. There are fewer buyers looking to buy properties to be used as short-term rentals, though, as they’re finding that the market is saturated.”

Austin, Texas cooled the fastest over the last year as the housing market descended from its … [+] pandemic-era boom.

getty

The tide has turned as housing markets in tech hubs and pandemic migration hot spots are cooling more rapidly than other parts of the country as the tech sector falters and mortgage rates remain elevated, according to a recent survey.

The Redfin analysis found that Austin, Texas cooled the fastest over the last year as the housing market descended from its pandemic-era boom. The Fed started hiking interest rates to combat inflation, leading to an increase in mortgage rates a year ago. Austin is followed by Seattle; Phoenix; Tacoma, Washington; and Denver. Las Vegas, Stockton, California; San Jose, California; Sacramento and Oakland, California round out the top 10.

Seattle had the third-biggest drop off in home buying demand.

getty

When push comes to shove, high rates, low supply and tech layoffs dampen demand in West Coast hubs

Measures of home buying demand and competition dropped off quickly in tech centers, including Seattle, San Jose and Oakland. The typical San Jose home sold for just 0.6% above its asking price in February, compared with 12% aboveasking price a year earlier—the biggest percentage-point drop off in the country. Seattle had the third-biggest drop off, going from 8% above asking price to 1% below during the last year. Pending home sales declined 40% year over year in Seattle, and they were down 38% in San Jose.

Redfin asked its agents to share how big a role the surge in tech layoffs, the shaky stock market and banking turmoil are playing in the cooldown, and found that coastal hubs are cooling quickly for a combination of reasons. Some reported that layoffs and precarious tech stocks are deterring buyers. Others attribute the slowdown mainly to other factors, including super-low inventory. San Jose and Oakland are among the five U.S. metros where new listings are dropping off fastest.

Home prices in Silicon Valley rose quickly for many years, especially during the pandemic, pricing … [+] out residents who didn’t work at Google, Meta, Amazon, Microsoft or any other tech company.

getty

Housing markets in tech hubs are cooling quickly for several reasons

Topsy-turvy tech stocks. Tech stocks fell more than 30% in 2022, though they have ticked up a bit since then. Shaky tech stocks hit the Bay Area and Seattle hard because buyers employed in the tech industry often use stock proceeds for down payments.

Tech layoffs. Layoffs in the tech industry, concentrated largely in the Bay Area and Seattle area, are widespread. Shelley Rocha, a Redfin manager in the Bay Area, said some buyers have bowed out of their search or canceled contracts because they have lost their jobs or are worried about losing them. Other agents say layoffs and dwindling tech job prospects are preventing some first-time buyers from entering the market at all.

Low inventory. There are plenty of Bay Area and Seattle residents who aren’t put off by the prospect of layoffs and a rocky stock market. But the limited number of homes coming on the market is tamping down demand from them, too.

Pandemic home price increases are unsustainable. Home prices in tech hubs rose quickly for many years, especially during the pandemic, pricing out residents who didn’t work at Google, Meta, Amazon, Microsoft or any other tech company. Now that tech is struggling and mortgage rates are high, an even bigger portion of local residents are unable to afford homes.

High mortgage rates. Mortgage rates are sitting around 6.4%. Is this a good thing? No, because it’s more than double the record low of 3% that was common in late 2020 and early 2021. That has driven up monthly housing payments substantially in expensive markets. The typical Seattle home buyer pays $4,210 per month with today’s 6.4% rate, versus around $3,200 a year ago at a 3.5% rate.

Still-high home prices. Home prices are falling in the Bay Area and Seattle, but they’re still high, largely because of limited inventory. The typical San Jose and Seattle homes sell for $1,250,000 and $710,000, respectively, compared with the $386,000 national median. High mortgage rates are exacerbating the expense, pushing out many would-be buyers.

It’s worth noting that while these markets cooled quickly from February 2022 to February 2023, some agents are now noticing competition on fairly priced homes as mortgage rates decline from their peak and supply remains low.

“I’m seeing bidding wars on homes that are priced fairly and accurately, and the overall market looks strong this week,” said San Jose Redfin agent Laxmi Penupothula. “Overpriced listings are the ones sitting on the market.”

The collapse of Silicon Valley Bank, which lent money to a lot of Bay Area startups, is having a mixed impact on the local housing market (the bank collapsed in March, after the time frame of the data in this report). Redfin agents report that uncertainty around the stability of the banking and tech industries is exacerbating nerves in some buyers and sellers. But the bank’s failure—along with turmoil surrounding other banks—caused the Fed to raise interest rates only modestly last week, which has already brought mortgage rates down and could help bring some buyers back.

The New York metro area (ranked #66 in terms of markets cooling fastest) is also likely to feel the impact of banking turmoil because so many of its residents work in the financial sector. Nearly one in five finance jobs in the U.S. are in New York, and finance is the highest-paying industry in the city. Banking instability could dampen home buying demand in the area as finance workers worry about their industry.

Pandemic boomtowns go from hot spots to not-so-hot spots

Austin soared in popularity in 2021 and early 2022 as an influx of out-of-town remote workers moved in from expensive coastal areas, taking advantage of historically low mortgage rates..

But now, measures of home buying competition and demand in Austin are dropping off fast. Its total supply of for-sale homes rose 140% year over year in February, the second-biggest increase in the U.S. (only North Port, Florida had a bigger increase). Pending sales dropped 40%, and just 16% of homes went under contract within two weeks of hitting the market in February, down from 38% a year earlier.

The surge of affluent home buyers pushed up local home prices, and the subsequent rise in mortgage rates priced out even more local residents. Even though Austin’s median price per square foot fell 13% year over year in February, the biggest drop of any major U.S. metro, it’s still higher than it was two years ago and the income needed to buy a home there remains far higher than what the typical local earns.

The story is similar in Phoenix, Las Vegas and Sacramento, also magnets for remote workers leaving expensive areas for more affordable homes and sunnier weather. Phoenix, Las Vegas and Sacramento are all mainstays on Redfin’s list of most popular migration destinations and quickly went from relatively affordable to not-so-affordable—at least for existing residents—during the pandemic.

Now housing markets in those boomtowns are doing an about-face as rates rise. Tech troubles are also contributing to dampened demand in these areas because many remote workers are struggling with layoffs and the prospect of them. The Bay Area and/or Seattle are among the top origins for homebuyers moving to Austin, Phoenix, Las Vegas and Sacramento.

The increasing portion of home sellers dropping their asking price illustrates just how much some of these markets have cooled. In Phoenix, 70% of for-sale homes had a price drop in February, compared with 21% a year earlier—the second-biggest uptick in the U.S. It’s followed closely by Denver, where 37% of homes had a price drop in February, compared with 13% a year earlier.

Las Vegas and Phoenix are also among the places that have seen the biggest upticks in sellers offering concessions to woo buyers over the last year.

Parts of Connecticut, upstate New York and the Midwest are holding up best amid a shaky housing market

Among the homes that are selling in Hartford, Connecticut, more are going under contract within two … [+] weeks

getty

Hartford, Connecticut is holding up best, according to the analysis. The housing market there isn’t necessarily hot—pending sales dropped 16% year over year in February and new listings also dropped by double digits—but other metrics show that there’s still competition for homes. Among the homes that are selling, more are going under contract within two weeks than a year earlier and the median price per square foot is up 8%.

Next comes Milwaukee, followed by two other Connecticut metros and two upstate New York metros: New Haven, Bridgeport, Albany and Rochester. Lake County, Illinois; McAllen, Texas; Wilmington, Delaware; and Chicago round out the top 10.

Homes in all those places are relatively affordable; nine of the 10 have a median sale price below the national median (Bridgeport is the exception). That means the uptick in mortgage rates doesn’t make as big of a dollar difference in monthly housing payments as it does in expensive areas.

The labor market has held up better than anticipated, which has helped prop up demand for … [+] apartments.

getty

Renters are finally getting a break on their rent as prices drop.The median asking rent rose 1.7% year over year to $1,937 in February—the smallest increase in nearly two years and the lowest level in a year, according to a new report from Redfin. Rents were up nearly 10 times that much (16.5%) a year earlier.

February was the ninth straight month where rent growth slowed on a year-over-year basis. Rents fell 0.3% from a month earlier. Still, the median asking rent remained 21.4% higher than it was in February 2020, the month before the coronavirus was declared a pandemic.

Rent growth has cooled as persistently high housing costs, inflation, recession fears and a slowdown in household formation have made people less likely to move, putting a damper on demand for new leases. A jump in supply due to a boom in apartment construction has also contributed to the slowdown in rent growth. The number of apartments under construction is up 24.9% year over year to 943,000, the highest level since 1974, according to a recent report from the National Association of Home Builders.

“Landlords are slowing their roll on rent increases because they’re grappling with a rise in vacancies as an influx of new apartments hits the market and demand slows from its peak,” said Redfin deputy chief economist Taylor Marr. “Rents are likely close to hitting a floor, though. That’s because stubbornly high inflation is boosting expenses for landlords, so instead of dropping rents they may seek to lure renters with other concessions, like free parking or a discounted security deposit.”

Marr added, “While rent growth has slowed, it hasn’t slowed quite as much as expected—in part because the labor market has held up better than anticipated, which has helped prop up demand. This is likely a reason overall inflation remains stubbornly high, as rent growth is a major contributor to inflation.”

Rents declined in 11 major metro areas

Austin, Texas (-6.5%)

New Orleans (-6.4%)

Phoenix (-4%)

Minneapolis (-3.5%)

Dallas (-2.6%)

Baltimore (-2.2%)

Houston (-1.9%)

Birmingham, Alabama (-0.5%)

Chicago (-0.5%)

Denver (-0.3%)

Virginia Beach, Virginia (-0.2%)

Charlotte, North Carolina and Columbus, Ohio saw the largest rent increases

Charlotte, North Carolina (14.3%)

Columbus, Ohio (12.6%)

Milwaukee (9.5%)

Nashville (9.0%)

Indianapolis (8.5%)

Kansas City, Missouri (8.3%)

Hartford, Connecticut (6%)

Buffalo, New York and Providence, Rhode Island (5.9%)

Cincinnati, Memphis and Louisville, Kentucky (5.5%)

The cost of buying a home is drifting further out of financial reach for the average American, according to a report from Redfin.

The real estate website analyzed homes that went on sale last year and found that only 21% of them were affordable, meaning that nearly 80% of homes were outside the typical buyer’s budget. By comparison, about 60% of homes were considered affordable in 2021, the report released Friday found.

Redfin Deputy Chief Economist Taylor Marr said those stats boil down to one truth: housing affordability is at its lowest point in history.

“Many millennials were able to buy their first home before or during the pandemic homebuying boom, but many others were priced out of homeownership and forced to keep renting,” he said in the report. “That means a lot of young adults missed out on a major wealth-building opportunity: the value of homes owned by millennials has risen nearly 30% in the past year.”

Redfin defined an “affordable” home as one whose mortgage payment would equal 30% or less of the average monthly income of residents in the county where the home sits. Redfin found that the highest percentage of affordable homes were in Akron, Cleveland and Dayton in Ohio, Pittsburgh and St. Louis, Missouri. Five California cities — Anaheim, Los Angeles, Oxnard, San Diego and San Francisco — had the lowest percentage of affordable homes.

The Redfin report dovetails with a recent Bloomberg analysis that shows Americans will need a higher income to land their first home. First-time buyers in 2022 had a typical household income of as much as $90,000 compared to just $70,000 in 2019, Bloomberg reported Friday.

The housing market is expected to pick up steam in the coming weeks as the historically hectic spring buying season kicks into gear. House hunters today face mortgage rates of around 6.6%, up from 3.75% a year ago. The median home price hit $415,000 last month, up from $406,000 in January, according to National Association of Realtors data.

Why are prices rising?

Home prices are climbing for a couple of reasons, Redfin said. The Federal Reserve’s monthslong battle with soaring inflation has helped push mortgage rates skyward, thus increasing borrowing costs for buyers. Also, demand for homes soared in 2022 and builders couldn’t keep up with the pace, driving prices for existing homes even higher.

The next few months will be tough sledding for buyers and sellers alike. Many homeowners are leery of selling because they might have to buy another house at a much higher mortgage rate, while buyers are still seeing far elevated prices, Daryl Fairweather, chief economist at Redfin, told CBS News on Thursday.

“The one silver lining is that if you manage to be able to afford a home, if you can get that mortgage, you’re going to face a lot less competition,” Fairweather said.

Khristopher J. Brooks is a reporter for CBS MoneyWatch covering business, consumer and financial stories that range from economic inequality and housing issues to bankruptcies and the business of sports.

Homes that sold were on the market for a median of 50 days. That’s up from 34 days a year earlier.

getty

Home buyer demand continues to increase from its fall low point despite mortgage rates ticking up this week, according to a new report from Redfin, a technology-powered real estate brokerage. Seller activity is also picking up.

Pending home sales posted their smallest decline since September during the four weeks ending February 5, falling 20% from a year earlier, and mortgage-purchase applications rose 3% from a week earlier. Redfin’s Homebuyer Demand Index—a measure of requests for tours and other services from Redfin agents—hit its highest level since September.

More homes are hitting the market to meet increasing demand; new listings dropped 17% from a year earlier, but that’s the smallest decline in over four months.

Although mortgage rates increased this week, they’re still down roughly a full percentage point from the peak they reached at the end of 2022. Rates coming down from their peak—along with home prices coming down from theirs—is the main reason buyers and sellers have started coming off the sidelines.

“By Super Bowl weekend, we usually have a good idea how a given year’s housing market will play out. But this year is anything but typical,” said Chen Zhao, Redfin’s economics research lead. “This year is more uncertain than most because the effects of last year’s rapid rate hikes are still flowing through the economy, and we’re not sure how much more the Fed will raise rates this year. So even after the Super Bowl comes and goes, we’ll be closely monitoring the Fed’s words and actions, along with inflation rates and indicators about the health of the labor market for signals that could affect home buyer demand.”

Leading indicators of home buying activity:

For the week ending February 9, the average 30-year fixed mortgage rate was 6.12%, up slightly from 6.09% the prior week, but down from the 2022 peak of 7.08% in November. The daily average was 6.32% on February 9, up from 5.99% a week earlier.

Mortgage purchase applications during the week ending February 3 increased 3% from a week earlier, seasonally adjusted. Purchase applications were down 37% from a year earlier.

The seasonally adjusted Redfin Homebuyer Demand Index hit its highest level since September during the week ending February 5. It was up 21% from its October trough but down 25% from a year earlier.

Google searches for “homes for sale” were up about 38% from their November low during the week ending February 4, but down about 23% from a year earlier.

Key housing market takeaways for 400+ metro areas:

Unless otherwise noted, this data covers the four-week period ending February 5. Redfin’s weekly housing market data goes back through 2015.

The median home sale price was $346,769, up 0.9% year over year.

Median sale prices fell in 18 of the 50 most populous metros, with the biggest drops in Oakland, California (-9.7% YoY); Austin, Texas (-6.5%); Sacramento (-5.8%); San Francisco (-4.9%) and Phoenix (-4.6%). Prices increased most in Milwaukee (12.8%), West Palm Beach, Florida (12.3%), Indianapolis (10.1%), Fort Lauderdale, Florida (9.8%) and Miami (8.4%).

The median asking price of newly listed homes was $376,160, up 1.7% year over year.

The monthly mortgage payment on the median-asking-price home was $2,376 at a 6.12% mortgage rate, the current weekly average. That’s down $131 (-5.2%) from the October peak. Monthly mortgage payments are up 25.1% ($477) from a year ago.

Pending home sales were down 19.5% year over year, the smallest decline since September.

Among the 50 most populous metros, pending sales fell most in Las Vegas (-58.7% YoY), Nashville (-50.6%), Phoenix (-50.1%), San Jose (-49.7%) and Austin (-48.9%). Pending sales rose in two metros: Cincinnati (31.5%) and Chicago (31.4%).

New listings of homes for sale fell 16.5% year over year. That’s the smallest decline since September.

New listings fell in all 50 of the most populous metros. They declined most in Oakland (-40.5%), Sacramento (-39%), San Jose (-38.1%), San Diego (-38%) and Las Vegas (-37.6%). They fell by less than 1% in Nashville, Dallas and Austin.

Active listings (the number of homes listed for sale at any point during the period) were up 22.6% from a year earlier.

Months of supply—a measure of the balance between supply and demand, calculated by the number of months it would take for the current inventory to sell at the current sales pace—was 4.1 months, up from 2.2 months a year earlier.

42% of homes that went under contract had an accepted offer within the first two weeks on the market, the highest level since July, but down from 50% a year earlier.

Homes that sold were on the market for a median of 50 days. That’s up from 34 days a year earlier and the record low of 18 days set in May.

20% of homes sold above their final list price, down from 39% a year earlier and the lowest level since March 2020.

On average, 5.4% of homes for sale each week had a price drop, up from 2.1% a year earlier.

The average sale-to-list price ratio, which measures how close homes are selling to their final asking prices, fell to 97.7% from 100% a year earlier. That’s the lowest level since March 2020.

More demand from buyers and less supply from homeowners is holding prices steady.

getty

The housing market is showing early signs of recovery with pending sales of homes climbing for the first time in a year. Pending home sales fell 26% year over year during the four weeks ending January 22 as mortgage rates ticked down. It was the smallest drop in more than three months, according to a new report from Redfin, a technology-powered real estate brokerage.

Pending sales began rising on a month-over-month basis in December as buyers started returning to the market, encouraged by their increased negotiating power and mortgage rates that have declined to 6.1% from their 7% peak. That signals the recent increase in early-stage home buyer demand—mortgage-purchase applications are up 28% since November and Redfin home tour requests are on the rise—is starting to translate into sales.

More demand from buyers and less supply from homeowners is holding prices steady. New listings of homes for sale are down 18% from a year ago, though that’s a smaller drop than recent weeks. The median home-sale price rose 1.1% year over year to $350,000, the biggest increase in over a month. On a local level, the number of metros where prices are falling from a year earlier is shrinking. Home prices declined in 17 of the 50 most populous U.S. metros, with the biggest drops in the Bay Area, down from 20 at the beginning of January.

Redfin agents are reporting that mortgage rates dipping nearly a full percentage point over the last two months is bringing back some sidelined buyers and attracting new ones. They are noticing an increase in interest from clients, including requests for tours, and reporting that some homes that have been on the market for months are finally going under contract.

“Home buyers are starting to feel more confident as mortgage rates tick down closer to 6% than 7% and the overall economy chugs along with surprising resilience, especially in the labor market. Steadily cooling inflation is likely to prevent mortgage rates from jumping back up,” said Chen Zhao, Redfin’s economics research lead. “When rates were seesawing up and down in the fall, many buyers dropped out because they could wake up the day after finding their dream home to a three-digit increase in their potential monthly payment. Now they have a better sense of how far their budget will go in which neighborhoods and which homes they can afford.”

Leading indicators of home buying activity:

For the week ending January 26, 30-year mortgage rates dropped to 6.13%, hitting their lowest level since September. The daily average was 6.18% on January 25.

Mortgage purchase applications during the week ending January 20 increased 3% from a week earlier and 28% from their early-November trough, seasonally adjusted. Purchase applications were down 39% from a year earlier.

The seasonally adjusted Redfin Homebuyer Demand Index—a measure of requests for home tours and other home buying services from Redfin agents—was up 6% from a month earlier during the four weeks ending January 22. It was down 29% from a year earlier.

Google searches for “homes for sale” were up about 40% from their November low during the week ending January 21, but down about 21% from a year earlier.

Key housing market takeaways for 400+ U.S. metro areas:

This data covers the four-week period ending January 22. Redfin’s weekly housing market data goes back through 2015.

The median home sale price was $349,950, up 1.1% year over year, the biggest gain in over a month.

The median asking price of newly listed homes was $367,450, up 3.8% year over year.

Among the 50 most populous metros, sale prices fell in 17, with the biggest drops in San Francisco (-9.3% year over year), Oakland, California (-6.5%), Austin (-6.3%), Detroit (-5.5%) and San Jose, California (-5.4%). Prices increased the most in West Palm Beach, Florida (13.5%), Nashville (9.6%), Milwaukee (9.2%), Indianapolis (7.8%) and Montgomery County, Pennsylvania (7.7%).

The monthly mortgage payment on the median asking-price home was $2,323 at the current 6.13% mortgage rate. That’s down nearly $200 from the October peak. Monthly mortgage payments are up 29% from a year ago.

Pending home sales were down 26.2% year over year, the smallest decline in over three months.

Among the 50 most populous metros, pending sales fell the most in Las Vegas (-63.2% year over year), Phoenix (-56%), Nashville (-52.5%), Jacksonville, Florida (-52.1%) and Austin (-50.7%). Pending sales rose in one metro: Cincinnati (+11.7%).

New listings of homes for sale fell 18.3% year over year, the smallest decline in nearly three months.

Active listings (the number of homes listed for sale at any point during the period) were up 23.6% from a year earlier.

Months of supply—a measure of the balance between supply and demand, calculated by dividing the number of active listings by closed sales—was 4.4 months, up from four months a week earlier and 2.1 months a year earlier.

33% of homes that went under contract had an accepted offer within the first two weeks on the market, up from 29% during the prior four-week period but down from 40% a year earlier.

Homes that sold were on the market for a median of 47 days. That’s up from 32 days a year earlier and the record low of 18 days set in May.

21% of homes sold above their final list price, down from 40% a year earlier and the lowest level since March 2020.

On average, 5% of homes for sale each week had a price drop, up from 2.1% a year earlier.

The average sale-to-list price ratio, which measures how close homes are selling to their final asking prices, fell to 97.8% from 100.1% a year earlier. That’s the lowest level since March 2020.

Some buyers are likely coming in from the sidelines because mortgage rates have dropped.

getty

Homes are selling at their slowest pace since the housing market nearly ground to a halt at the beginning of the pandemic, according to a new report from Redfin, a technology-powered real estate brokerage.

The typical home that sold during the four weeks ending January 8 was on the market for 44 days, the longest time span since April 2020, contributing to the biggest annual inventory increase on record. Pending home sales dropped 32% year over year to their lowest level on record and mortgage-purchase applications dropped to their lowest level since 2014.

High mortgage rates and extreme winter weather at the start of the year deterred would-be home buyers, exacerbating the typical holiday slowdown. But there are signs that early-stage demand is up. Redfin’s Homebuyer Demand Index–a measure of tour requests and other buying services from Redfin agents–posted a 6% increase over the last month, and Google searches for “homes for sale” are on the rise. Some buyers are likely coming in from the sidelines because mortgage rates have dropped to 6.33% from their November peak of over 7%, saving the typical buyer roughly $250 on monthly housing payments.

Buyers may also be encouraged by signs of improvement in the economy, with inflation easing in December for the sixth month in a row as wage growth softens. “We’re entering 2023 with positive economic news,” said Redfin deputy chief economist Taylor Marr. “The latest consumer price index report confirms that the worst of inflation is behind us. That means the Fed is likely to continue easing its interest rate increases, which should cause mortgage rates to continue gradually declining. This could bring back some home buyers in the coming months. We’ve already seen an uptick in people initiating home searches. Although those house hunters haven’t yet turned into buyers, they may soon given that monthly mortgage payments are notably down from their peak and the latest inflation and employment data lower the chances of a recession.”

Home prices fell from a year earlier in 20 of the 50 most populous metros

The typical home sold for $351,250 during the four weeks ending January 8. That’s up 0.8% from a year earlier, but down about 10% from the June peak. Prices fell year over year in 20 of the 50 most populous metros. By comparison, 11 metros saw price declines a month earlier.

Prices fell 10.6% year over year in San Francisco; 5% in Seattle; 4.9% in San Jose; 4% in Austin; 3.8% in Detroit; 3.7% in Phoenix; 3.4% in Oakland, California; 3% in Boston; 3% in Los Angeles; 3% in Sacramento; 2.6% in San Diego; and 2.5% in Chicago. They fell 2% or less in Portland, Oregon; Anaheim, California; Riverside, California; Newark, New Jersey; New York; Pittsburgh; Las Vegas; and Washington, D.C.

This marks the first time Las Vegas prices have dropped year over year since at least 2015. It’s the biggest year-over-year price drop in San Francisco, Seattle, Phoenix, Chicago, Boston, Portland and San Diego since at least 2015.

Leading indicators of home buying activity:

For the week ending January 12, 30-year mortgage rates declined from the week before to 6.33%. The daily average was 6.15% on January 11.

Mortgage-purchase applications during the week ending January 6 declined 1% from a week earlier, seasonally adjusted, hitting their lowest level since 2014. Purchase applications were down 44% from a year earlier.

The seasonally adjusted Redfin Homebuyer Demand Index–a measure of requests for home tours and other home buying services from Redfin agents–was essentially flat from a week earlier and up 6% from a month earlier during the four weeks ending January 8. It was down 29% from a year earlier.

Google searches for “homes for sale” were up nearly 50% from their November low during the week ending January 7, but down about 17% from a year earlier.

Key housing market takeaways for 400+ U.S. metro areas

This data covers the four-week period ending January 8. Redfin’s weekly housing market data goes back through 2015.

The median home sale price was $351,250, up 0.8% year over year.

The median asking price of newly listed homes was $352,150, up 3.9% year over year.

The monthly mortgage payment on the median asking-price home was $2,263 at the current 6.33% mortgage rate. That’s roughly flat from a week earlier and down $244 from the October peak. Monthly mortgage payments are up 32.7% from a year ago.

Pending home sales were down 31.7% year over year to the lowest level on record, the 12th straight period of pending sales declining more than 30%.

Among the 50 most populous metros, pending sales fell the most in Las Vegas (-61.9% year-over-year), Jacksonville, Florida (-57.4%), Phoenix (-56.9%), Austin, Texas (-55.3%) and Nashville (-50.8%).

New listings of homes for sale fell 21.9% year over year.

Active listings (the number of homes listed for sale at any point during the period) were up 20.7% from a year earlier, the biggest annual increase since at least 2015.

Months of supply—a measure of the balance between supply and demand, calculated by dividing the number of active listings by closed sales—was 3.8 months, up from 3.4 months a week earlier and 1.9 months a year earlier.

27% of homes that went under contract had an accepted offer within the first two weeks on the market, down from 34% a year earlier.

Homes that sold were on the market for a median of 44 days, the longest time period since April 2020. That’s up nearly two weeks from 31 days a year earlier and the record low of 18 days set in May.

22% of homes sold above their final list price, down from 40% a year earlier and the lowest level since March 2020.

On average, 4% of homes for sale each week had a price drop, down sharply from 5.7% a month earlier.

The average sale-to-list price ratio, which measures how close homes are selling to their final asking prices, fell to 97.9% from 100.1% a year earlier. That’s the lowest level since March 2020.

Buyers are feeling more empowered during negotiations as their offer is often the only one on the … [+] table.

getty

In a key sign that the tide is turning in favor of home buyers, sellers gave concessions to buyers in 41.9% of home sales in the fourth quarter—the highest share of any three-month period in Redfin’s records, according to a new report from the technology-powered real estate brokerage.

That’s up from just over 30% in both the previous quarter and the fourth quarter of 2021, and outpaces the prior 40.8% high from the three months ending July 2020, when the housing market nearly ground to a halt due to the onset of the pandemic. Redfin’s concessions records date back to July 2020 and are based on data submitted by Redfin buyers’ agents.

Concessions have made a comeback as rising mortgage rates, inflation and economic uncertainty have dampened home-buying demand, giving the buyers who remain in the market increased negotiating power.

That’s a stark shift from the pandemic home-buying frenzy of late 2020 and 2021, when record-low mortgage rates fueled fierce competition, forcing most buyers to bid over the asking price and waive every contingency just to have their offers taken seriously.

“Buyers are asking sellers for things that were unheard of during the past few years,” said Van Welborn, a Redfin real estate agent in Phoenix. “They’re feeling empowered, partly because their offer is often the only one, and partly because they know sellers have built up so much equity during the pandemic that they can afford to dole out sizable concessions.”

Welborn added, “I recently helped one of my buyers negotiate a $10,000 credit for a new roof and a handful of other repairs. We originally asked for $15,000, but were happy with $10,000 because the homeowner also agreed to sell for less than their asking price.”

Homeowners are increasingly selling for below their desired price as the housing market slows. A record 22% of home sales recorded by Redfin buyers’ agents in the fourth quarter included both a concession and a final sale price below the listing price, while a record 19% included both a concession and a listing-price cut that occurred while the home was on the market. A record 11% included all three.

Phoenix saw the biggest jump in concessions

In Phoenix, sellers gave concessions to buyers in 62.9% of home sales in the fourth quarter, up from 33.2% a year earlier. That 29.7-percentage-point increase is the largest among the 25 metropolitan areas for which data was available. Next came Seattle (25.6 percentage-points), Las Vegas (22.2 percentage-points), San Diego (20.7 percentage-points) and Detroit (20.4 percentage-points).

Phoenix and Las Vegas are among the fastest cooling markets after they soared in popularity during the pandemic as scores of remote workers moved in, searching for relative affordability and warm weather.

“It took a while, but seller expectations are coming back down to earth,” said Welborn. “Concessions were common before the pandemic, and we may be returning to that norm. Sellers realize they’re not going to get $80,000 over the asking price like their neighbor did last year.”

Welborn said he has recently seen sellers offer credits of as much as $25,000 to cover repairs and closing costs, and that they’re also offering to pay for 2-1 mortgage-rate buydowns and warranties on household appliances.

There were four metros in which concessions were less common compared with a year ago. In Austin, sellers gave concessions to buyers in 33.3% of home sales, down from 38.1% a year earlier (-4.8 percentage points). Next came Philadelphia (-2.7 percentage points), New York (-2.4 percentage points) and Chicago (-1.6 percentage points).

Concessions are most common in San Diego

In San Diego, sellers gave concessions to buyers in 73% of home sales in the fourth quarter—the highest share among the metros Redfin analyzed (San Diego also had the highest share a year ago). Next came Phoenix (62.9%), Portland, Oregon (61.6%), Las Vegas (61.3%) and Denver (58.4%).

In New York, sellers gave concessions to buyers in 13.4% of home sales—the lowest share among the metros Redfin analyzed. It was followed by San Jose, California (14.4%), Boston (17.5%), Philadelphia (22%) and Austin (33.3%).

Luxury homes are often among the first to get cut from budgets during times of economic stress.

getty

Sales of luxury homes fell 38.1% year over year during the three months ending November 30, 2022, the biggest decline on record, according to a new report from Redfin, a technology-powered real estate brokerage. That outpaced the record 31.4% decline in sales of non-luxury homes. Redfin’s data goes back to 2012.

The luxury market and the overall housing market lost momentum in 2022 due to many of the same factors: inflation, relatively high interest rates, a sagging stock market and recession fears. But the high-end market has slowed at a sharper clip for a handful of reasons, including:

Luxury homes are often among the first to get cut from budgets during times of economic stress.

Luxury properties are frequently used as investment properties, and with home values and rents poised to fall in 2023, investment prospects are lackluster.

High-end home sales saw outsized growth during the pandemic, so they have more room to fall.

Affluent buyers often have significant funds stored in the stock market, which has been losing value.

Expensive coastal markets led the decline in high-end home sales. In Nassau County, New York (Long Island), luxury-home sales plummeted 65.6% year over year during the three months ending November 30, the largest decline among the most populous metropolitan areas. Next came four California metros: San Diego (-60.4%), San Jose (-58.7%), Riverside (-55.6%) and Anaheim (-55.5%). These markets are prohibitively expensive for most buyers even when the economy is thriving, so it’s not surprising more buyers would back off during a downturn.

There are early signs that overall home buyer demand is starting to creep back as interest rates decline, which may ultimately cause the decline in luxury sales to ease. Mortgage applications and Redfin’s Homebuyer Demand Index—a measure of requests for tours and other buying services—have both been on the rise, and Redfin real estate agents say they are seeing more buyers move off of the sidelines.

“There has been a small shift in the market that’s not fully showing up in the data yet. With mortgage rates falling, a lot of house hunters see this as their moment to come back and compete,” said Seattle Redfin agent Shoshana Godwin. “Many of my buyers are taking out jumbo loans—mortgages typically used for purchases of high-end homes. While some data shows jumbo mortgage rates above 6%, some of my buyers are getting rates in the low 5% range.”

Luxury home supply rises most in six years

The number of luxury homes for sale rose 5.2% year over year to roughly 163,000 during the three months ending November 30, the largest increase since 2016. By comparison, the supply of non-luxury homes declined 5.7% to about 552,000.

The large decline in luxury home sales is contributing to the rise in supply, but new listings are also a factor. New listings of luxury homes fell just 2.9% year over year during the three months ending November 30, compared with a 19.8% drop in listings of non-luxury homes.

Home price growth slows across the board

Home price growth has slowed across the housing market due to ebbing demand. Prices of both luxury and non-luxury homes rose 10% year over year during the three months ending November 30, compared with 17% growth one year earlier. The median sale price was $1.1 million for luxury homes and $325,000 for non-luxury homes.

Metro-level highlights: three months ending November 30

Home sales: Luxury home sales fell in every metro. The biggest declines were in Nassau County (-65.6% YoY), San Diego (-60.4%), San Jose (-58.7%), Riverside (-55.6%) and Anaheim, California (-55.5%). The smallest decreases were in Kansas City, Missouri (-20.2%), Cleveland (-21.5%), Virginia Beach, Virginia (-26.2%) Milwaukee (-26.4%) and Charlotte, North Carolina (-28.3%).

Supply: Active listings of luxury homes rose in 21 metros, with the biggest increases in Austin, Texas (51% YoY), Denver (50.1%), Nashville (35.7%), Warren, Michigan (29.8%) and Atlanta (25.9%). The largest declines were in San Jose (-32.2%), Anaheim (-22.5%), Los Angeles (-19.4%), St. Louis (-18.5%) and Miami (-16.6%).

New listings: New listings of luxury homes fell in 39 metros. The biggest declines were in San Jose (-39.2% YoY), Oakland, California (-37.1%), Anaheim (-29.8%), San Diego (-26.2%) and Orlando, Florida (-25.9%) The largest gains were in Denver (44%), Warren, Michigan (32.4%), Austin, Texas (20.2%), Detroit (16.3%) and Atlanta (15%).

Prices: The median sale price of luxury homes rose in all but one metro—San Jose (-0.3% YoY). The biggest jumps were in Miami (28.1%), Tampa (27.7%), Charlotte, North Carolina (25%), West Palm Beach, Florida (25%) and Orlando (23.7%). The smallest increases were in San Francisco (0.1%), Nassau County (2.1%), Oakland (3.1%) and Portland, Oregon (5.8%).

Positive inflation news could lead to mortgage rates declining further and a gradual home-sale … [+] recovery early next year.

getty

Redfin’s Homebuyer Demand Index—a measure of home-tour requests and other services from Redfin agents—is up 10% and mortgage-purchase applications are up 14% from the end of October, when both hit their 2022 troughs, according to a new report from Redfin, a technology-powered real estate brokerage. That’s largely because mortgage rates continue to steadily decline.

According to a new report from Redfin, mortgage-purchase applications and the Homebuyer Demand Index have increased significantly since hitting a low point at the end of October, but demand is still much lower than it was a year ago. This week’s positive inflation news could lead to mortgage rates declining further and a gradual home-sale recovery early next year, even with the Fed signaling continued rate hikes.

Measures of early-stage buyer demand are up by double digits since hitting a low point at the end of October. Redfin’s Homebuyer Demand Index–a measure of home-tour requests and other services from Redfin agents–is up 10% and mortgage-purchase applications are up 14% from the end of October, when both hit their 2022 troughs. That’s largely because mortgage rates continue to steadily decline. The weekly average came in at 6.31% this week, down from a peak of 7.08% during the last week of October, saving the typical home buyer more than $200 on a monthly payment.

But while they’ve risen from the trenches, demand and purchase applications are still down sharply from a year ago. Additionally, pending home sales are down more than 30% year over year and homes are selling at their slowest pace in nearly two years–though it takes time for early indicators of demand to translate into pending sales. The nation’s median home-sale price rose just 1.4% year over year, the slowest growth rate since the start of the pandemic, reflecting still-cool homebuyer demand.

“Slowing inflation and the hope of the Fed easing rate hikes in the new year are likely to bring mortgage rates down further and thereby improve home buying demand,” said Redfin Deputy chief economist Taylor Marr. “But don’t call it a comeback or even a recovery yet; demand is still way down from its peak. We’re keeping a close eye on the labor market for confirmation that inflation will continue slowing. A strong job market like the one we have now contributes to inflation because it pushes up wages and leads to higher prices. Though it seems counterintuitive, a slight uptick in unemployment and/or slower economic growth would likely help bring mortgage rates down further. If that happens, the increase we’re seeing in early-stage demand could translate to an uptick in pending sales in early 2023.”

Home prices fell from a year earlier in 15 of the 50 most populous metros

The number of metros with declining sale prices is piling up. Home-sale prices fell year over year in 15 of the 50 most populous U.S. metros, many of them in California, compared with declines in 11 of the 50 a week earlier.

Prices fell 7.3% year over year in San Francisco, 5.8% in San Jose, California, 3.3% in Los Angeles, 3% in Austin, 2.6% in Pittsburgh, 2% in Oakland, 1.9% in Detroit and 1.8% in Sacramento. They declined 1% or less in Anaheim, California, Chicago, Philadelphia, Seattle, Riverside, California, Phoenix and Las Vegas. The Los Angeles and Austin price declines are the biggest since at least 2015, as far back as this data goes. Although the declines were small, this marks the first time that Las Vegas and Riverside home prices have fallen on a year-over-year basis since at least 2015.

Leading indicators of home buying activity

For the week ending December 15, 30-year mortgage rates ticked down slightly to 6.31%, the fifth straight weekly decrease. The daily average was 6.13% on December 15.

Mortgage purchase applications during the week ending December 14 increased 4% from a week earlier and 7.6% from a month earlier, seasonally adjusted. They’re up 13.8% from late October, when purchase applications fell to their trough. Still, purchase applications were down 38% from a year earlier.

The seasonally adjusted Redfin Homebuyer Demand Index–a measure of requests for home tours and other home buying services from Redfin agents–was essentially flat from a week earlier, but up 5% from a month earlier during the four weeks ending December 11. It was down 27% from a year earlier.

Fewer people searched for “homes for sale” on Google than this time in 2021. Searches during the week ending December 10 were down about 34% from a year earlier, and flat from the week before.

Touring activity as of December 11 was down 40% from the start of the year, compared to a 16% decrease at the same time last year, according to home tour technology company ShowingTime.

Key housing market takeaways for 400+ U.S. metro areas

The median home sale price was $353,750, up 1.4% year over year, the slowest growth rate since the start of the pandemic.

The median asking price of newly listed homes was $354,779, up 3.9% year over year, the slowest growth rate since the start of the pandemic.

The monthly mortgage payment on the median-asking-price home was $2,276 at the current 6.31% mortgage rate. That’s down slightly from a week earlier and down more than $200 from a month earlier, when mortgage rates were around 7%. Still, monthly mortgage payments are up 36.5% from a year ago.

Pending home sales were down 33.3% year over year, one of the largest declines since at least January 2015, as far back as this data goes.

Among the 50 most populous U.S. metros, pending sales fell the most from a year earlier in Las Vegas (-64%), Austin (-58.3%), Phoenix (-57.1%), Portland, OR (-53.6%) and Jacksonville, FL (-52%).

New listings of homes for sale were down 21.5% from a year earlier, the largest decline since the start of the pandemic.

Active listings (the number of homes listed for sale at any point during the period) were up 15.9% from a year earlier, the biggest annual increase since at least 2015.

Months of supply—a measure of the balance between supply and demand, calculated by dividing the number of active listings by closed sales—was 3.7 months, down from a week earlier and up from 2 months a year earlier.

29% of homes that went under contract had an accepted offer within the first two weeks on the market, down from 37% a year earlier and the lowest share since January 2020.

Homes that sold were on the market for a median of 38 days, up more than a week from 29 days a year earlier and up from the record low of 17 days set in May and early June.

25% of homes sold above their final list price, down from 41% a year earlier and the lowest level since June 2020.

On average, 5.6% of homes for sale each week had a price drop, down sharply from 7.2% a month earlier. It’s up from 2.6% a year earlier.

The average sale-to-list price ratio, which measures how close homes are selling to their final asking prices, fell to 98.3% from 100.3% a year earlier. That’s the lowest level since March 2020.