A pair of e-commerce entrepreneurs who bought a number of well-known retail brands — including RadioShack, Modell’s Sporting Goods and Pier 1 Imports — out of bankruptcy are accused of running a Ponzi scheme.

The Securities and Exchange Commission on Monday accused Alex Mehr and Tai Lopez, founders of the Miami-based Retail Ecommerce Ventures (REV), of defrauding investors out of approximately $112 million.

Through their holding company, Mehr and Lopez acquired distressed brick-and-mortar companies in order to turn them into successful, online-only brands. Dress Barn and Linens ‘n Things were also among their acquisitions.

REV acquired RadioShack in 2020, three years after the nearly century-old electronics chain filed for its second bankruptcy. RadioShack first filed for Chapter 11 protection in 2015.

Modell’s Sporting Goods filed for bankruptcy in March 2020, during which time it also announced it would be closing all of its stores. REV bought the Modell’s brand name and assets in August 2020. Pier 1 Imports — which still exists as an online store — declared bankruptcy in early 2020. REV acquired its trademark name and assets later that same year.

The SEC’s suit alleges that between 2020 and 2022, Mehr and Lopez, “made material misrepresentations” to hundreds of investors about the bankrupt retailers they had acquired. For example, to entice individuals to invest in their acquisitions, they said their portfolio companies were “on fire” and that “cash flow is strong.” They also told prospective backers that money raised for a company would only be used for that specific firm. That proved not to be the case, according to the SEC’s lawsuit, which was filed Monday in the U.S. District Court for the Southern District of Florida.

“Contrary to these representations, while some of the REV Retailer Brands generated revenue, none generated any profits,” the suit states. “Consequently, in order to pay interest, dividends and maturing note payments, Defendants resorted to using a combination of loans from outside lenders, merchant cash advances, money raised from new and existing investors, and transfers from other portfolio companies to cover obligations.”

Neither Mehr nor Lopez immediately responded to CBS News’ request for comment.

The SEC alleges that at least $5.9 million of returns paid to investors were actually Ponzi-like payments funded by other investors, as opposed to companies’ profits.

Additionally, the federal regulatory agency claims that Mehr and Lopez allocated $16 million worth of investments for their own use, according to the filing.

Megan Cerullo is a New York-based reporter for CBS MoneyWatch covering small business, workplace, health care, consumer spending and personal finance topics. She regularly appears on CBS News 24/7 to discuss her reporting.

A Harvard Business School graduate was arrested Thursday on fraud charges alleging he swindled fellow alumni of the prestigious school out of over $4 million in a Ponzi scheme, even assuring one investor they would soon “brag” about their “crazy gains” at the school’s reunion.

NEW YORK (AP) — A Harvard Business School graduate was arrested Thursday on fraud charges alleging he swindled fellow alumni of the prestigious school out of over $4 million in a Ponzi scheme, even assuring one investor they would soon “brag” about their “crazy gains” at the school’s reunion.

Vladimir Artamonov, 46, was taken into custody in Elkridge, Maryland, where he lived, and was charged with securities, wire and investment adviser fraud for allegedly carrying out the scheme from September 2021 through February 2024.

An indictment unsealed in Manhattan federal court said Artamonov promised big returns and little risk to dupe former classmates and other alumni into investing with him, telling one investor: “It will be your best investment. The insight is air tight.”

Messages for comment left with Harvard and a lawyer for Artamonov were not immediately returned. Artamonov, appearing before a magistrate judge in federal court in Maryland, was released on $300,000 bail with instructions to have no contact with victims or potential trial witnesses.

The allegations against Artamonov were first revealed in late February 2024 by New York Attorney General Letitia James, who said in a news release then that her office learned about the fraud after one of several dozen investors ended his own life after learning he had lost $100,000.

“Even sophisticated investors can be conned by fraudsters, especially when personal relationships and networks are used to build a false sense of trust,” James said.

She said Artamonov “used his alumnus status from Harvard Business School to prey on his classmates and others while seeming legitimate and dependable.”

Artamonov, a 2003 Harvard graduate with a master’s in business administration, used the school’s alumni network to identify investors, authorities said.

The indictment said he promised investors that he could identify securities on the verge of making large gains by spotting public insurance company filings by affiliates of Berkshire Hathaway Inc. prior to public filings made to the Securities and Exchange Commission that are more closely followed by investors.

Instead of following that plan, Artamonov put investor money into risky short-term options, losing millions of dollars, often within days of receiving the money from investors, the indictment said.

It said he repeatedly assured investors that big profits were on the horizon and even promised one investor that it was “almost certain we will make a ton of money” soon and that they would “brag” about their “crazy gains” at the Harvard Business School reunion.

Investors eventually demanded their money back, causing Artamonov to return less than $400,000 by paying original investors with money from new investors or by declining to reimburse them at all, the indictment said.

It said Artamonov lost most of the money or spent tens of thousands of dollars on items such as lodging, food and alcohol, and transportation.

Christopher G. Raia, head of New York’s FBI office, said in a news release that Artamonov “exploited the prestige of a well-respected university and investment company to unlawfully rocure investments, which he used to pay for personal expenses.”

U.S. Attorney Jay Clayton said Artamonov “betrayed investors, including friends and former Ivy League classmates.”

FBI agents swooped into the homes of two AB Capital executives in Newport Beach and Laguna Beach to find evidence of an alleged Ponzi scheme that cost investors tens of millions of dollars.

Armed with search warrants, the federal agents seized documents as part of an ongoing criminal investigation into Joshua Pukini and Ryan Young, co-owners of the Newport Beach-based real estate finance firm, the Los Angeles Daily News reported.

The FBI also searched AB Capital’s former Newport Beach headquarters at 15 Corporate Plaza Drive, investors say.

In a broadcast on KCal News, the FBI agents were seen hefting boxes and bags of evidence from one of the homes.

The raids lasted hours, with FBI agents first barking on a bullhorn to those inside the homes, said Brian Werlemman, a wealth manager who alleges he was fleeced out of $2.7 million in 2018 during an elaborate Ponzi scheme involving the company.

He claims around 100 others, many from Orange County, were duped into investing with the company.

“There was approximately upwards of $100 million involved,” Werlemman, who says he was the largest investor, told KCal News. “These are first and second trust deeds, where we started noticing bizarre things were happening — and money was missing, literally missing.”

Laura Eimiller, spokeswoman for the FBI in Los Angeles, confirmed the raids, saying they’re connected to an ongoing criminal investigation. She declined to provide further details.

Neither of AB Capital’s two principals could be reached for comment by the Daily News. Information wasn’t available on whether they face criminal charges.

Werlemman said he has cooperated with the FBI and the U.S. Internal Revenue Service.

The investigation follows an involuntary bankruptcy foisted upon AB Capital by disgruntled investors in 2022, he said. A civil lawsuit tied to the bankruptcy names Pukini and Young, alleging breach of fiduciary duty, conversion and other offenses.

It seeks $50 million or more in damages.

AB Capital is described in the suit as a real estate investment company that provides loans, then syndicates and sells fractional interest in those loans to investors.

“Prior to bankruptcy, debtor and its principals breached their fiduciary duties by looting and fraudulently transferring debtor’s assets, misappropriating debtor’s business opportunities, and defrauding creditors, the complaint says.

Werlemman, commenting on the alleged Ponzi scheme, said the defendants took real estate properties and liquidated them to return funds to investors.

“It looks like there are going to be cents on the dollar when everything is done,” he told the Daily News. “The civil suit is trying to unwind the tangled mess.”

The complaint alleges Pukin and Young refused to turn over AB Capital’s accounting records and destroyed documents, to the “shock and utter amazement” of a court-appointed bankruptcy trustee.

The trustee’s examination of AB Capital’s electronic and hard files on Oct. 7, 2022, revealed there were no files of any kind left on computers other than 80 files found in the computer’s “trash,” the complaint alleges. Additionally, large filing cabinets in a conference room at AB Capital’s headquarters were allegedly empty.

It is also alleged that Pukini lied about the disposition of AB Capital funds and misappropriated or fraudulently transferred proceeds, according to the Daily News.

AB Capital, founded in 2016, claims the firm makes “disciplined investments in targeted markets,” according to its website, with its founders having completed more than $1 billion in real estate deals.

Fifteen years to the day after the arrest of Bernie Madoff for the largest Ponzi scheme in history, nearly 25,000 of the disgraced financier’s victims will receive $158.9 million, bringing their total recoveries to 91% of their lost money, the Department of Justice announced on Monday.

The Madoff Victim Fund has distributed nine payments totaling over $4.22 billion to 40,843 of Madoff’s victims, as compensation for losses they suffered from the collapse of his investment securities business.

Bernard L. Madoff outside federal court in Manhattan in January of 2009.

Hiroko Masuike / Getty Images

“Among Madoff’s many victims were not only wealthy and institutional investors, but charities and pension funds alike — some of which invested money with Madoff on behalf of individuals working paycheck-to-paycheck who were relying on their pension accounts for their retirements,” said U.S. Attorney Damian Williams for the Southern District of New York, adding that “the financial toll on those who entrusted their money with Madoff was devastating.”

Bernard L. Madoff, the once-chairman of the NASDAQ, was arrested on Dec. 11, 2008, for defrauding investors out of $64 billion. He pleaded guilty in March 2009 to securities fraud and other charges, saying he was “deeply sorry and ashamed,” and was sentenced to 150 years in prison. Additionally, Madoff was ordered to pay $170 billion in restitution to his victims.

The DOJ says the fund has “exceeded expectations” in the level of recovery it has been able to successfully provide to victims.

Madoff died as a result of ongoing health issues while incarcerated in 2021 at age 82.

DappBay, a web3 dApp store for users on the BNB Chain, has flagged over 100 risky decentralized applications (dapps) in its recent update.

BNB Chain shared the findings on X (formerly Twitter). See below.

BNB Chain launched DappBay in July 2022, allowing users to discover new web3 projects while being kept abreast of their risk levels in real-time.

At the heart of DappBay is its Red Alarm component, a risk screening tool that can help identify possible rug pulls and scam projects by checking logic flaws or fraud risks in smart contracts.

This tool regularly updates its list with dapps and smart contracts that have been assessed as scams or deemed to carry an extraordinarily high level of risk.

Risky dapps

One of the prominent names on DappBay’s list of risky dapps is Genesis Universe, a non-fungible token (NFT) card exploration game built on the BNB Smart Chain. In this game, players explore and fight in a new world, following the increasingly popular play-to-earn approach.

However, its presence on the Red Alarm list points to possible risks in its operation, therefore advising caution for both users and investors.

Another notable addition to DappBay’s Red Alarm list is DeXe DAO Studio, categorized under tools and utilities and marked with a “significant risk” level.

This dapp reportedly supports the development of decentralized autonomous organizations (DAOs), highlighting the importance of active, valuable member involvement and expertise. However, despite its ambitious goals, the assigned risk level indicates possible drawbacks or issues that users need to consider.

Web3 Pilot, a first-in-first-out defi investment platform, was identified as a high-risk dapp. Per Red Alarm’s indication, the platform’s main risk revolves around it being a possible Ponzi scheme, misleadingly enticing investors with the allure of unusually high returns.

Other decentralized applications highlighted in Red Alarm’s list include QuickPay, Silo, and Defi Ujm. The first two are categorized as Ponzi schemes, while the third is suspected to be a phishing website.

A Beverly Hills luxury watch dealer accused of stealing people’s pricey timepieces was arrested by the FBI following a report in The Times detailing the allegations of theft against the dealer.

Anthony Farrer, 35, was charged with mail fraud and wire fraud over his alleged consignment scheme. The businessman, who ran a watch company called The Timepiece Gentleman, told potential clients that he would sell their watches and take a commission but often kept all the money, prosecutors announced Wednesday.

“Rather than selling the watches and remitting the funds back to the watch owners, Farrer appears to instead sell the watches and keep the proceeds for himself,” wrote Justin Palmerton, an FBI agent, in an affidavit filed Monday in U.S. District Court in the Central District of California.

If convicted, Farrer faces up to 20 years in prison and is currently being held at the Metropolitan Detention Center in Los Angeles. His next court date is Dec. 14.

Farrer stole about $3 million from at least 20 victims, according to Palmerton. Numerous victims of Farrer spoke with The Times for the October article, including one man who said he lost his life savings to Farrer.

All the while, Farrer lived a life of luxury, buying high-end cars, spending tens of thousands of dollars on a single meal and renting one of the most expensive apartments in Los Angeles — all of which he flaunted on social media sites such as TikTok. He posted about his exploits and eventually admitted to using people’s watches to pay off other debts.

“He confessed to running a Ponzi scheme and he almost does not seem to understand it,” said Chad Plebo, who helped put victims of in touch with the FBI in the case. “It’s such a bizarre, weird story.”

Farrer posted on social media about his debts in August, admitting that what he did was wrong.

“Spending people’s money, living above my means. … I’ve been digging myself this hole and it’s a five-million dollar hole,” he said in the Aug. 2 video. “About three million of that debt is to two big clients of mine. One who acted as an investor and I used his money to fund my lifestyle.”

In The Times story detailing the allegations, seven people said they had given Farrer watches worth between $10,000 and well over $100,000, only to have the timepieces disappear. One of the seven alleged victims has a pending lawsuit against Farrer over the issue; an eighth person who also sued did not speak with The Times.

When asked whether he was worried about going to prison for his alleged actions, Farrer said he could not focus on that.

“If I do, I do. If I don’t, I don’t,” he said.

Farrer was raised in Texas and started his company there in 2017 before moving to downtown Los Angeles, where he produced his own reality show about his life called “South Hill,” which he self-published on YouTube.

“People trusted him in this space because he had a social media following,” said John Buckley, a luxury watch dealer who runs a business called Tuscany Rose.

Opinions expressed by Entrepreneur contributors are their own.

If you’ve recently received an email from a Nigerian Prince asking for a small sum of money now to help him out of a financial bind, don’t bother. I have already paid it and should be receiving an expeditious reward in the form of gold bricks. It’s a great feeling.

Thank goodness I didn’t fall for any scams. You’re probably familiar with them; The Ponzi scheme, for example, whereby current investors are paid only by new investors until the jig is up and the new investors dry up. Without naming names, one very famous financial advisor used this ruse and Madoff with millions.

It looks like 81-year-old Carl Ruderman, the former CEO of short-term business loan company 1 Global Capital, might be saying goodbye to a luxurious retirement.

Ruderman has been indicted on charges of wire fraud, conspiracy to commit wire and mail fraud, and conspiracy to commit securities fraud — making him the fifth senior citizen in the Miami-Fort-Lauderdale-Palm Beach metropolitan area to face the consequences of a $250 million 1 Global Capital fraud scheme, The Miami Herald reported.

Hallandale Beach-based 1 Global Capital would make short-term, high-interest loans to small businesses while, unbeknownst to investors, the company paid large commissions to brokers (including unregistered ones) and otherwise misappropriated funds, per the outlet.

Prosecutors allege Ruderman used investors’ cash to finance travel, insurance payments for his art collection, drivers, housekeepers, mortgage payments and a luxury car for his wife, Miami New Times reported.

Other key players in the scam, which spanned dozens of states and racked up a $50 million cash deficit, include 65-year-old Alan Heide, 1 Global Capital’s former CFO; 78-year-old Steven Schwartz, the company’s former chief operating officer; 81-year-old attorney Andrew Ledbetter; and 78-year-old attorney Jan Atlas.

Those involved in the sprawling senior citizen crime ring received sentences ranging from eight months to five years in prison and were ordered to pay restitution between $29 million and $148 million, and the two attorneys agreed to disciplinary revocation from the Florida Bar, per The Miami Herald.

Disgraced “Crypto Queen” Ruja Ignatova’stime on the run may be coming to an end.

Cryptoqueen via Facebook

Ignatova,42, a German citizen born in Bulgaria, is a former crypto pioneer who vanished in October 2017 after over-promising high returns on her OneCoin crypto token in a $4 billion Ponzi Scheme. She’s now facing several charges of fraud and has been on the run from the FBI for five years.

Although she hasn’t been seen since her disappearance, a new London apartment listing suggests she’s alive and evading arrest.

Ignatova, the only woman on the FBI’s most wanted list, was recently found to be connected to an £11 million [$13.6 million] penthouse apartment for sale in Kensington, England, thanks to a new rule change by the UK’s Companies House, which acts similarly to the U.S’s Public Company Accounting Oversight Board.

The rule now requires properties purchased by companies to also list a beneficiary, and while it is believed Ignatova originally purchased the home under a shell company, a new court filing to the UK’s financial regulators lists Ignatova as the “beneficial owner” of the property – inadvertently exposing her whereabouts.

Ignatova’s connection to the home was first spotted by the host of “The Missing Cryptoqueen” podcast, Jamie Bartlett.

“[The document] suggests she is still alive, and there are documents out there somewhere which contain vital clues as to her recent whereabouts,” Bartlett told iNews.

Since Ignatova’s link to the home, which was listed on Knight Frank real estate website, was confirmed, the listing has been removed.

Here’s what to know about the disgraced “Crypto Queen.”

Before Ruja Ignatova become one of 11 women to be on the FBI’s most wanted list in its 72-year history, she was regarded as a rising star in the crypto industry.

Ignatova was known for liking glitz and glamour, per CNN,and was revered for growing from her humble beginnings in Germany to success as a consultant and then a crypto entrepreneur.

Together with her business partner Sebastian Greenwood, the pair convinced investors to back their OneCoin crypto token which they said would be more valuable than Bitcoin. However, authorities found that OneCoin defrauded investors out of $4 billion in one of the largest international fraud schemes of all time.

“OneCoins were entirely worthless … (Their) lies were designed with one goal, to get everyday people all over the world to part with their hard-earned money,” U.S. prosecutors said, according to court documents.

Furthermore, the court documents reveal that Ignatova and Greenwood intended to deceive their clients from the get-go, calling their own token a “trashy coin” and discussing an exit strategy in private emails.

Their scheme imploded in 2016 when investors struggled to sell their OneCoins to recoup their investments, alerting the media and investigators to look into the business.

Then in October 2017, the U.S. Department of Justice charged Ignatova with one count of wire fraud, conspiracy to commit wire fraud, securities fraud, conspiracy to commit securities fraud, and conspiracy to commit money laundering, with a federal judge issuing a warrant for her arrest, court documents state.

But Ignatova fled on a flight from Sofia, Bulgaria, to Athens, Greece, just two weeks after the warrant was issued and she hasn’t been seen since.

The FBI has offered a $100,000 reward for information leading to her arrest. Additionally, they said: “Ignatova is believed to travel with armed guards and/or associates. Ignatova may have had plastic surgery or otherwise altered her appearance.”

The #FBI has named Ruja Ignatova to its Ten Most Wanted Fugitives List. She is wanted for her alleged participation in a large-scale fraud scheme involving cryptocurrency. Up to $100,000 reward offered for info leading to her arrest: https://t.co/oU7EKYqaCipic.twitter.com/tJ8co8aqx0

Ruja Ignatova and her cofounder lured people to their OneCoin scheme beginning in 2014 by promising investors around the world a fivefold or tenfold return on their investments.

Taking advantage of the crypto frenzy at the time, investors gave them $4 billion between 2014 and 2016. However, OneCoin’s value was manipulated by the company and it was never mined like other cryptocurrencies, despite telling investors otherwise, according to CNN.

Once regulators uncovered the scheme and Ignatova vanished, she left her partners to deal with the fallout.

Cofounder Sebastian Greenwood was arrested in July 2018. He’s currently in jail after pleading guilty to wire fraud, conspiracy to commit wire fraud, and conspiracy to launder money. He is set to be sentenced in April.

Ignatova’s brother, Konstantin Ignatov, who was also a part of the business scheme, was arrested in March 2019 and is set to be sentenced in February after pleading guilty to wire fraud conspiracy, money laundering, and fraud charges.

Since the scandal unraveled, OneCoin has been shut down and its website is no longer active.

A lawsuit filed by the victims against OneCoin revealed that Ignatova had $500 million in Dubai bank accounts as of 2021, per a report by Financial Finds. It’s unknown how much crypto she holds, but the outlet found that shewas paid 230,000 Bitcoins by a member of the Emirati royal family in 2015.

Disgraced financier Bernie Madoff will go down in infamy for orchestrating the largest Ponzi Scheme in history, conning investors out of $65 billion over several decades.

TIMOTHY A. CLARY/AFP via Getty Images

Madoff pleaded guilty to 11 felony charges including securities fraud and money laundering in 2009. He was sentenced to 150 years in prison and died 12 years into his sentence at the age of 82 in April 2021.

“He stole from the rich. He stole from the poor. He stole from the in-between. He had no values,” said former investor Tom Fitzmaurice at Madoff’s sentencing, per AP News. “He cheated his victims out of their money so he and his wife … could live a life of luxury beyond belief.”

Netflix is set to revisit the con that rocked the 2008 financial crisis and unpack how Madoff used his status as a respected money manager to perpetrate the ruse in a new four-part docuseries “Madoff: The Monster of Wall Street” hitting the streamer on January 4.

The series chronicles Madoff’s rise to power and the poor oversight that allowed the scam to flourish. So far, only $14 billion in recovered funds has been distributed to victims so far, per ABC News, and the fallout of Madoff’s fraud is still felt today.

Here’s everything you need to know about Madoff and his infamous Ponzi scheme.

Who Was Bernie Madoff?

Before Bernie Madoff became a Wall Street powerhouse, the New York native came from humble beginnings. After growing up in Queens and attending Hofstra University, he started Bernard L. Madoff Investment Securities with just a few thousand dollars.

The firm traded penny stocks in the 1960s until Madoff convinced family and friends to invest with him, using an investing strategy called a split-strike conversion. He promised big returns to his clients and he delivered, however, he was keeping all the funds in a single Chase bank account. After decades in business, he became one of Wall Street’s biggest and most respected players.

Madoff was also instrumental in launching the Nasdaq, the first electronic stock exchange, in the 1970s and he even worked with the Securities and Exchange Commission (SEC) on the project, per The Guardian.

He later became chair of the Nasdaq in the 1990s. That, coupled with big returns on investments gave him the credibility investors needed to trust him with their assets. Some of his most notable investors included Steven Spielberg, Kevin Bacon, and Holocaust survivor Elie Wiesel.

What Did Bernie Madoff Do?

Bernie Madoff’s legitimate business endeavors and his status distracted from a $65 billion Ponzi Scheme that was hidden behind the scenes. A Ponzi Scheme is when investors are told their funds would be used for investment opportunities but were actually given as compensation to earlier investors, in other words, Madoff was robbing Peter to pay Paul.

The dark side of his business was hidden on an entirely different floor of his office that had very limited access, even Madoff’s sons who worked at the company were allegedly out of the loop.

To keep his ruse going, he printed false monthly statements that showed steady double-digit returns.

Despite several alarms made to the SEC about the too-good-to-be-true nature of Madoff’s business, his power in the industry and the billions of dollars involved allowed the scheme to prosper for years.

What Happened to Bernie Madoff?

The woes of the 2008 financial crisis left Madoff unable to continue his Ponzi Scheme with investors who were scrambling to gather back their assets. He knew the game was over when he only had $300 million left of investor money in his account, so he came clean to his sons, telling them the family business was “all just one big lie,” per AP News.

His sons, Andrew and Mark Madoff, then turned him in to the FBI, and Madoff was arrested the next day. He pleaded guilty to several counts of fraud in March 2009 and was released on a $10 million bond. Months later he was sentenced to 150 years in prison.

After being slapped with the maximum possible sentence, U.S. District Judge Denny Chin said: “Here, the message must be sent that Mr. Madoff’s crimes were extraordinarily evil and that this kind of irresponsible manipulation of the system is not merely a bloodless financial crime that takes place just on paper, but it is instead … one that takes a staggering human toll.”

Twelve years into Madoff’s sentence, he died behind bars due to “natural causes related to his failing health,” according to the outlet. He was 82 years old.

“No one sees this as a great loss,” said Jerry Reisman at the time, an attorney who represented a number of Madoff’s victims. “No one is going to mourn Bernie Madoff. They are happy they have survived him.”

Madoff’s son Mark died by suicide on the second anniversary of his father’s arrest in 2010, and his other son Andrew died from cancer in 2014. His wife, Ruth, is still alive today.

What Was Bernie Madoff’s Net Worth?

Before Madoff’s empire came crashing down, ABC News reported that Madoff and his wife, Ruth, had a total net worth of $823 million by the end of 2008.

According to the outlet, the assets consisted of $22 million worth of homes in Manhattan, The Hamptons, Palm Beach, and France, plus $17 million in cash, $45 million in securities, and his investment business valued at $700 million.

After Madoff was sentenced in 2009, a judge ordered him to forfeit all of his property, real estate, and investments, in addition to $80 million of Ruth’s personal assets, leaving her with $2.5 million, according to AP News.

The below is an excerpt from the Bitcoin Magazine Pro report on the rise and fall of FTX. To read and download the entire 30-page report, follow this link.

The Beginnings

Where did it all start for Sam Bankman-Fried? As the story goes, Bankman-Fried, a former international ETF trader at Jane Street Capital, stumbled upon the nascent bitcoin/cryptocurrency markets in 2017 and was shocked at the amount of “risk-free” arbitrage opportunity that existed.

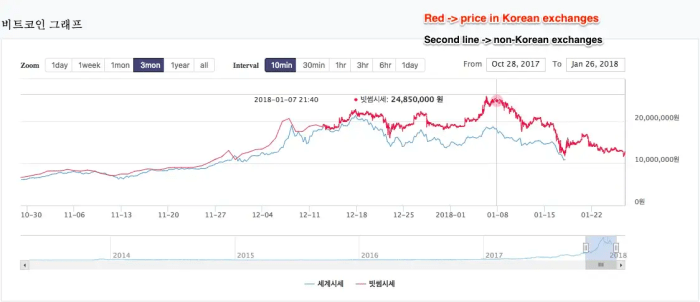

In particular, Bankman-Fried said the infamous Kimchi Premium, which is the large difference between the price of bitcoin in South Korea versus other global markets (due to capital controls), was a particular opportunity that he took advantage of to first start making his millions, and eventually billions …

The real story, while possibly similar to what SBF liked to tell to explain the meteoric rise of Alameda and subsequently FTX, looks to have been one riddled with deception and fraud, as the “smartest guy in the room” narrative, one that saw Bankman-Fried on the cover of Forbes and touted as the “modern day JP Morgan,” quickly changed to one of massive scandal in what looks to be the largest financial fraud in modern history.

The Start Of The Alameda Ponzi

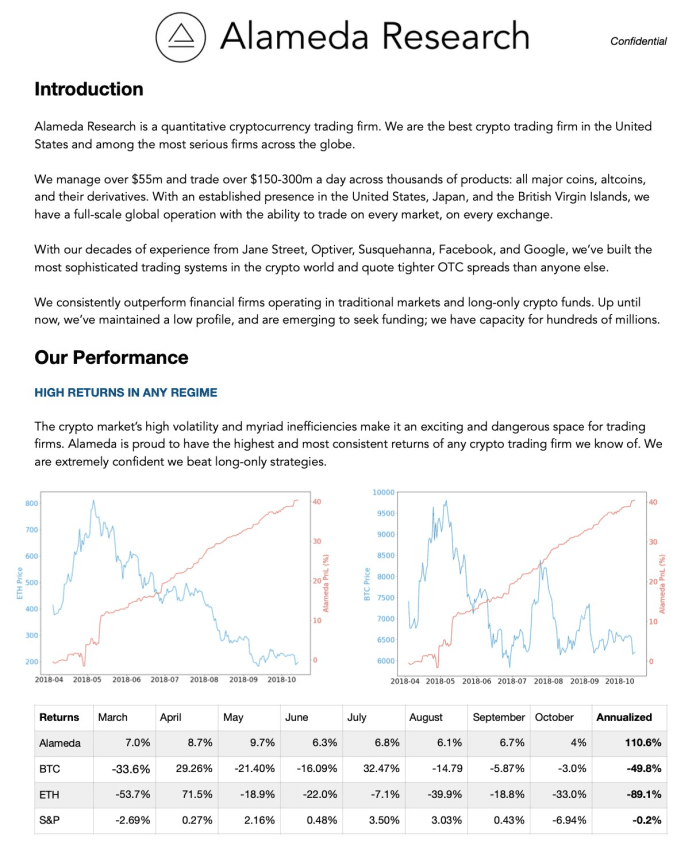

As the story goes, Alameda Research was a high-flying proprietary trading fund that used quantitative strategies to achieve outsized returns in the cryptocurrency market. While the story was believable on the surface, due to the seemingly inefficient nature of the cryptocurrency market/industry, the red flags for Alameda were glaring from the start.

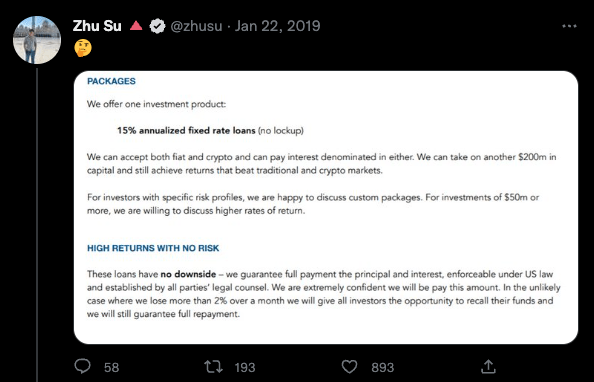

As the fallout of FTX unfolded, previous Alameda Research pitch decks from 2019 began to circulate, and for many the content was quite shocking. We will include the full deck below before diving into our analysis.

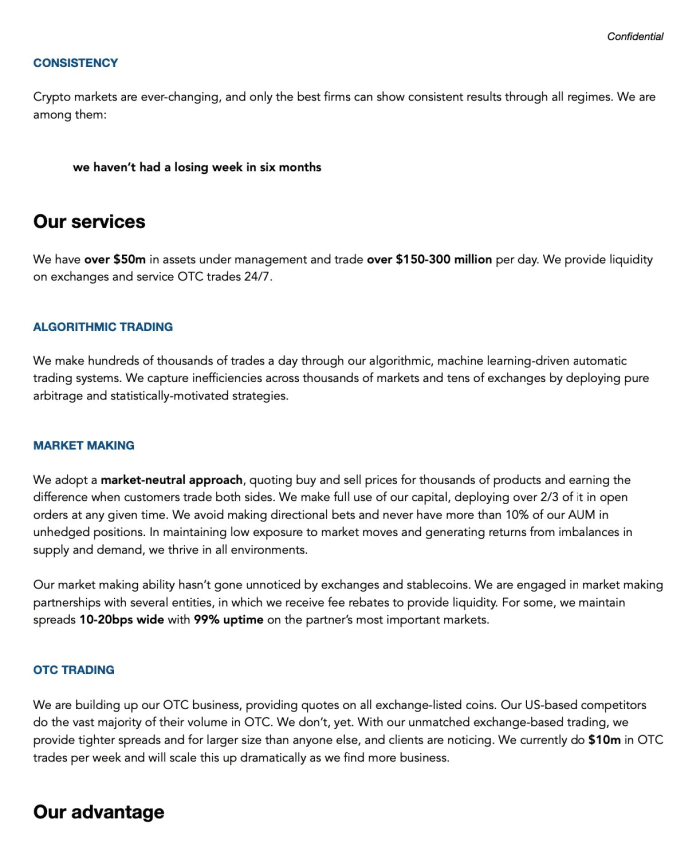

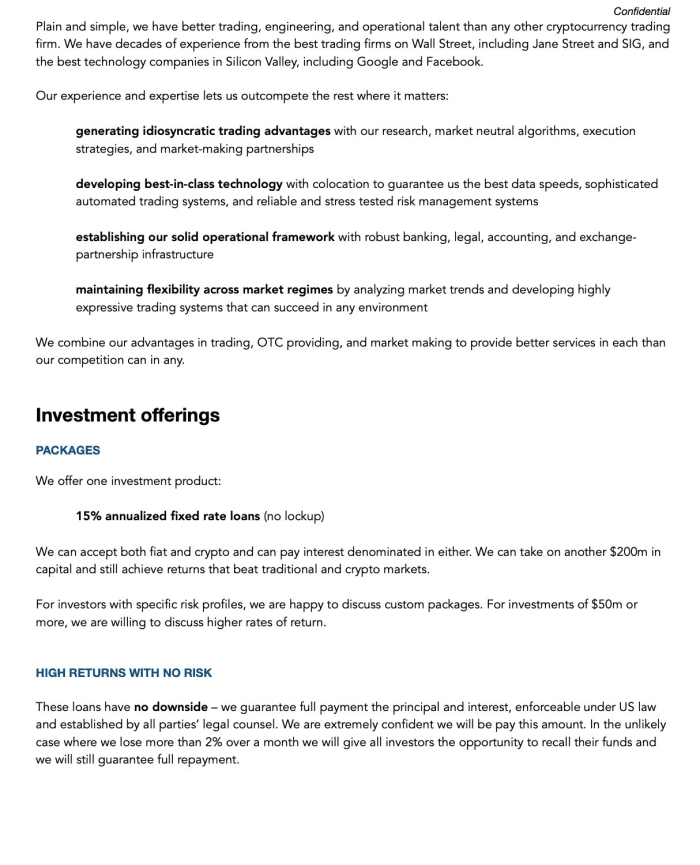

The deck contains many glaring red flags, including multiple grammatical errors, including the offering of only one investment product of “15% annualized fixed rate loans” that promise to have “no downside.”

All glaring red flags.

Similarly, the shape of the advertised Alameda equity curve (visualized in red), which seemingly was up and to the right with minimal volatility, while the broader cryptocurrency markets were in the midst of a violent bear market with vicious bear market rallies. While it is 100% possible for a firm to perform well in a bear market on the short side, the ability to generate consistent returns with near infinitesimal portfolio drawdowns is not a naturally occurring reality in financial markets. Actually, it is a tell-tale sign of a Ponzi scheme, of which we have seen before, throughout history.

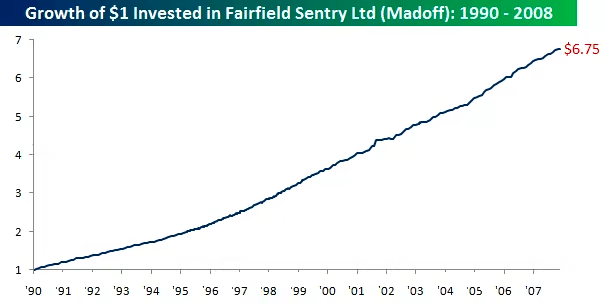

The performance of Bernie Madoff’s Fairfield Sentry Ltd for nearly two decades operated quite similarly to what Alameda was promoting via their pitch deck in 2019:

Up-only returns regardless of broader market regime

Minimal volatility/drawdowns

Guaranteeing the payout of returns while fraudulently paying out early investors with the capital of new investors

Stated returns by Bernie Madoff’s fund

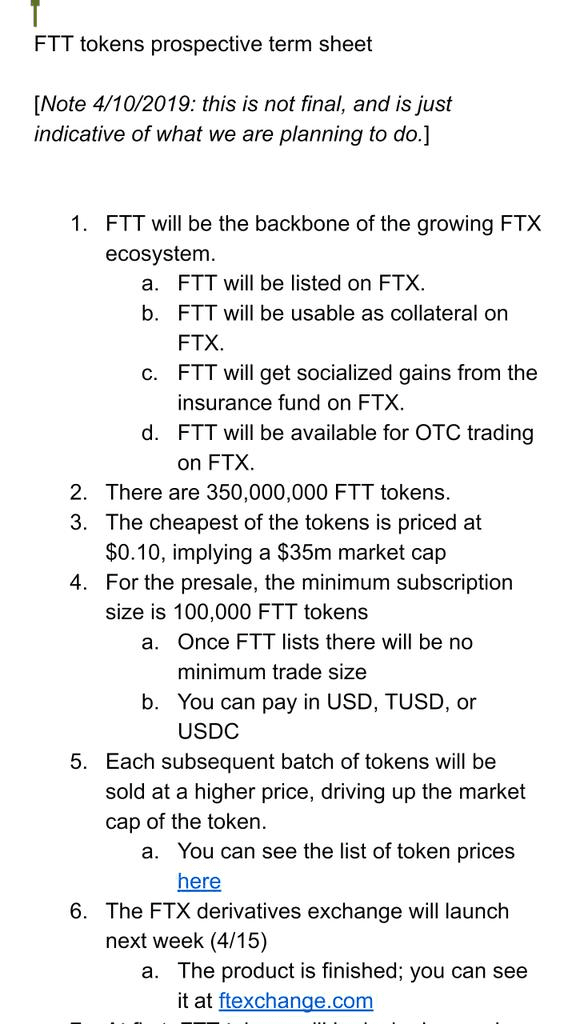

It appears that Alameda’s scheme began to run out of steam in 2019, which is when the firm pivoted to creating an exchange with an ICO (initial coin offering) in the form of FTT to continue to source capital. Zhu Su, the co-founder of now-defunct hedge fund Three Arrows Capital, seemed skeptical.

Approximately three months later, Zhu took to Twitter again to express his skepticism about Alameda’s next venture, the launch of an ICO and a new crypto derivatives exchange.

“These same guys are now trying to launch a “bitmex competitor” and do an ICO for it. 🤔” – Tweet, 4/13/19

Beneath this tweet, Zhu said the following while posting a screenshot of the FTT white paper:

“Last time they pressured my biz partner to get me to delete the tweet. They started doing this ICO after they couldn’t find any more greater fools to borrow from even at 20%+. I get why nobody calls out scams early enough. Risk of exclusion higher than return from exposing.” – Tweet, 4/13/19

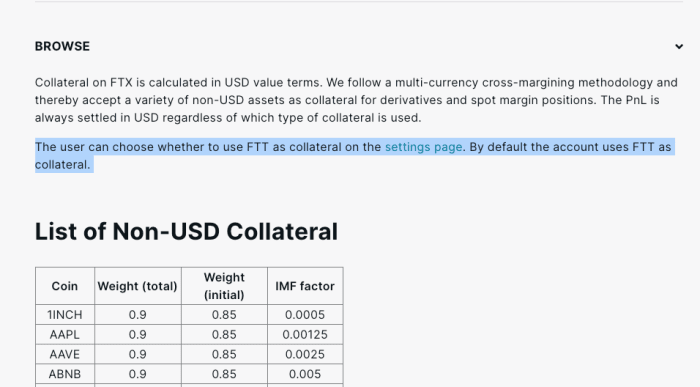

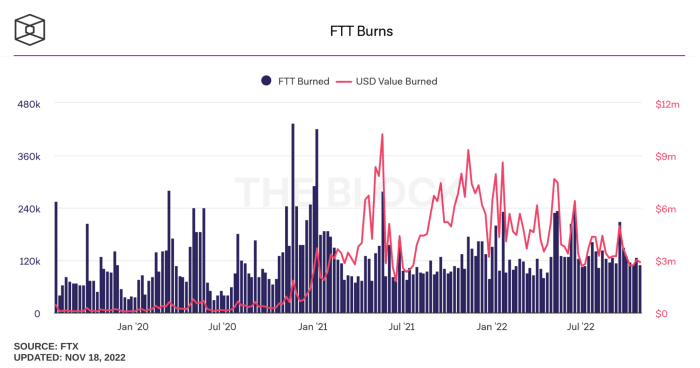

Additionally, FTT could be used as collateral in the FTX cross-collateralized liquidation engine. FTT received a collateral weighting of 0.95, whereas USDT & BTC received 0.975 and USD & USDC received a weighting of 1.00. This was true until the collapse of the exchange.

The FTT token was described as the “backbone” of the FTX exchange and was issued on Ethereum as a ERC20 token. In reality, it was mostly a rewards based marketing scheme to attract more users to the FTX platform and to prop up balance sheets. Most of the FTT supply was held by FTX and Alameda Research and Alameda was even in the initial seed round to fund the token. Out of the 350 million total supply of FTT, 280 million (80%) of it was controlled by FTX and 27.5 million made their way to an Alameda wallet.

FTT holders benefited from additional FTX perks such as lower trading fees, discounts, rebates and the ability to use FTT as collateral to trade derivatives. To support FTT’s value, FTX routinely purchased FTT tokens using a percentage of trading fee revenue generated on the platform. Tokens were purchased and then burned weekly to continue driving up the value of FTT.

FTX repurchased burned FTT tokens based on 33% of fees generated on FTX markets, 10% of net additions to a backstop liquidity fund and 5% of fees earned from other uses of the FTX platform. The FTT token does not entitle its holders to FTX revenue, shares in FTX nor governance decisions over FTX’s treasury.

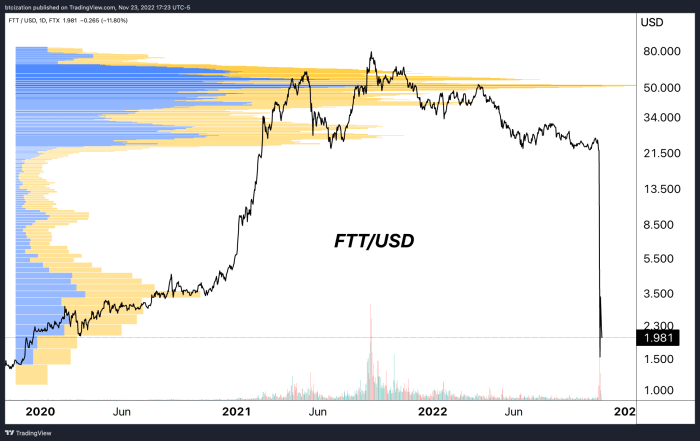

Alameda’s balance sheet was first mentioned in this Coindesk article showing that the fund held $3.66 billion in FTT tokens while $2.16 billion of that was used as collateral. The game was to drive up the perceived market value of FTT then use the token as collateral to borrow against it. The rise of Alameda’s balance sheet rose with the value of FTT. As long as the market didn’t rush to sell and collapse the price of FTT then the game could continue on.

FTT rode on the backs of the FTX marketing push, rising to a peak market cap of $9.6 billion back in September 2021 (not including locked allocations, all the while Alameda leveraged against it behind the scenes. The Alameda assets of $3.66b FTT & $2.16b “FTT collateral” in June of this year, along with its OXY, MAPs, and SRM allocations, were combined worth tens of billions of dollars at the top of the market in 2021.

The price of FTT with a side profile showing FTT trading volume on FTX (logarithmic scale)

FTT Market Cap (logarithmic scale) – Source:CoinMarketCap

CZ Chooses Blood

In one decision and tweet, CEO of Binance, CZ, kicked off the toppling of a house of cards that in hindsight, seems inevitable. Concerned that Binance would be left holding a worthless FTT token, the company aimed to sell $580 million of FTT at the time. That was bombshell news since Binance’s FTT holdings accounted for over 17% of the market cap value. This is the double edged sword of having the majority of FTT supply in the hands of a few and an illiquid FTT market that was used to drive and manipulate the price higher. When someone goes to sell something big, value collapses.

As a response to CZ’s announcement, Caroline of Alameda Research, made a critical mistake to announce their plans to buy all of Binance’s FTT at the current market price of $22. Doing that publicly sparked a wave of market open interest to place their bets on where FTT would go next. Short sellers piled in to drive the token price to zero with the thesis that something was off and the risk of insolvency was in play.

Ultimately, this scenario has been brewing since the Three Arrows Capital and Luna collapsed this past summer. It’s likely that Alameda had significant losses and exposure but were able to survive based on FTT token loans and leveraging FTX customer funds. It also makes sense now why FTX had an interest in bailing out companies like Voyager and BlockFi in the initial fallout. Those firms may have had large FTT holdings and it was necessary to keep them afloat to sustain the FTT market value. In the latest bankruptcy documents, it was revealed that $250 million in FTT was loaned to BlockFi.

With hindsight, now we know why Sam was buying up all of the FTT tokens he could get his hands on every week. No marginal buyers, lack of use cases and high risk loans with the FTT token were a ticking time bomb waiting to blow up.

How It All Ends

After pulling back the curtain, we now know that all of this led FTX and Alameda straight into bankruptcy with the firms disclosing that their top 50 creditors are owed $3.1 billion with only a $1.24 cash balance to pay it. The company likely has over a million creditors that are due money.

The original bankruptcy document is riddled with glaring gaps, balance sheet holes and a lack of financial controls and structures that were worse than Enron. All it took was one tweet about selling a large amount of FTT tokens and a rush for customers to start withdrawing their funds overnight to expose the asset and liability mismatch FTX was facing. Customer deposits weren’t even listed as liabilities in the balance sheet documents provided in the bankruptcy court filing despite what we know to be around $8.9 billion now. Now we can see that FTX never had really backed or properly accounted for the bitcoin and other crypto assets that customers were holding on their platform.

It was all a web of misallocated capital, leverage and the moving of customer funds around to try and keep the confidence game going and the two entities afloat.

.

.

.

This concludes an excerpt from “The FTX Ponzi: Uncovering The Largest Fraud In Crypto History.” To read and download the full 30-page report, follow this link.