Analysts continue to raise their revenue and stock price targets for Shopify, Inc. (SHOP). Its new target price is 20% higher. This article will demonstrate how to achieve a 3.0% yield by shorting one-month away SHOP puts at a 4% out-of-the-money strike price.

SHOP closed at $146.82 on Friday, Sept. 5, with a $191.274 billion market cap. That is well over my prior target price of $137 at a 178 billion market valuation.

SHOP stock – last 3 months – Barchart – As of Sept. 5, 2025

This can be seen in my July 13 Barchart article, just after its Q2 earnings release (“Shopify Stock is a Bargain – How to Make a 3.2% One-Month Yield with SHOP“).

Since then, Shopify delivered strong Q2 results on Aug. 6. This article will update our prior target price based on its strong free cash flow (FCF) and FCF margins.

Shopify, which competes more and more with Amazon (AMZN) in the third-party online seller space, said its Q2 revenue rose 31% to $2.68 billion from $2.045 billion a year ago.

Moreover, its free cash flow (FCF), which is what is left over after all cash expenses, net working capital changes, and even capex spending, rose by +$26.7% to $422 million.

That means that, as a percent of revenue, its FCF represented 15.75% of sales (which Shopify rounds up to 16%) compared to 15.38% last quarter and 16.3% last year.

Shopify Q2 FCF and FCF margins page 6 of Q2 earnings release

That implies that the company is continuing to squeeze out good amounts of cash from its operations, even as sales keep rising.

Keep in mind that during Q4, Shopify tends to make significantly higher FCF margins during the Christmas season.

For example, last Q4, its FCF margin was 21.73%, according to Stock Analysis. As a result, its look-back trailing 12 months (TTM) FCF margin as of Q2 was 18.14%, based on Stock Analysis data. In Q1, its TTM FCF margin was slightly higher at 18.42%.

As a result, assuming the next Q4 margin will rise, we can use an 18.5% FCF margin to forecast its next 12 months (NTM) free cash flow.

Analysts now project 2025 sales will be $11.26 billion (up from $10.88 billion in my prior Barchart article). Moreover, the 2026 sales forecast is now $13.75 billion, up from $13.11 billion.

That implies that Shopify’s next 12 months (NTM) revenue will be on a run rate of $12.505 billion (up from $12.0 billion in my prior article).

That is 4.2% higher than my prior estimate of $2.22 billion.

We can use that FCF estimate to forecast its target price.

If we assume that Shopify will eventually pay out 100% of its FCF to shareholders, and that the market will give the stock a 1.0% FCF yield, here is its valuation:

$2.3134 billion / 0.01 = $231.34 billion market value

Today, Shopify’s market cap is $191.274 billion, according to Yahoo! Finance:

In other words, SHOP stock could be worth almost 21% more over the next 12 months:

$146.82 x 1.2095 = $177.58 per share

The point is that if the company makes an 18.5% FCF margin and the market gives the stock a 1.0% FCF yield valuation, the stock could rise 21% to $177.58.

Analysts tend to agree with this. For example, AnaChart.com now shows that 34 analysts have a price target of $155.33.

One way to play this is to set a lower buy-in target price by shorting out-of-the-money (OTM) puts. That way an investor can make a good yield while waiting for the stock to fall.

For example, look at the Oct. 10 expiration period, one month away (i.e., 33 days to expiration or DTE). It shows that the $141.00 put option contract, which is 4% below Friday’s close, has a midpoint premium of $4.35 per put contract.

That implies that a short-seller of these puts can make an immediate yield of 3.085% (i.e., $4.35/$141.00 = 0.03085).

SHOP puts expiring Oct. 10, 2025 – Barchart – As of Sept. 5, 2025

To do this, an investor first secures $14,100 with their brokerage firm in cash or buying power. That acts as collateral to buy 100 shares of SHOP stock, in case it falls 4% to $141.00 (each contract has 100 shares).

Then, after entering an order to “Sell to Open” 1 put contract at $141.00, the account will immediately receive $435.00. That is why this play has a 3.085% yield (i.e., $435/$14,100).

Note that the investor who does this play has a lower potential break-even buy-in point:

$131.00- $4.35.00 = $136.65 breakeven

That is -6.92% below Friday’s closing price, so it provides a good downside protection.

However, this only applies if SHOP falls to $141.00 and the account is assigned to buy 100 shares using the collateral already posted.

The point, however, is that an investor has a good upside this way. On the one hand, they can make an immediate yield of 3.085%. If this is repeated for three months, the expected return (ER) could be +9.255%.

That is the same as holding shares and seeing SHOP stock rise to $160.81 over the next 3 months. Moreover, an investor could also buy deep in-the-money (ITM) calls for a further out period and use these short-put plays to help pay for the cost. That way, they may have some upside if SHOP keeps rising from here.

However, if SHOP falls below the breakeven point over the next month, an investor could end up with an unrealized capital loss. Investors can study the downside risks by going to Barchart’s Option Education Center.

The bottom line is SHOP stock looks cheap here. Shorting OTM puts and/or buying ITM calls is one way to play it.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

The CAPE Ratio assesses a stock’s price compared to its average earnings over the past 10 years, adjusted for inflation. A high CAPE Ratio suggests that stocks might be overvalued relative to historical earnings, indicating potential downside risks.

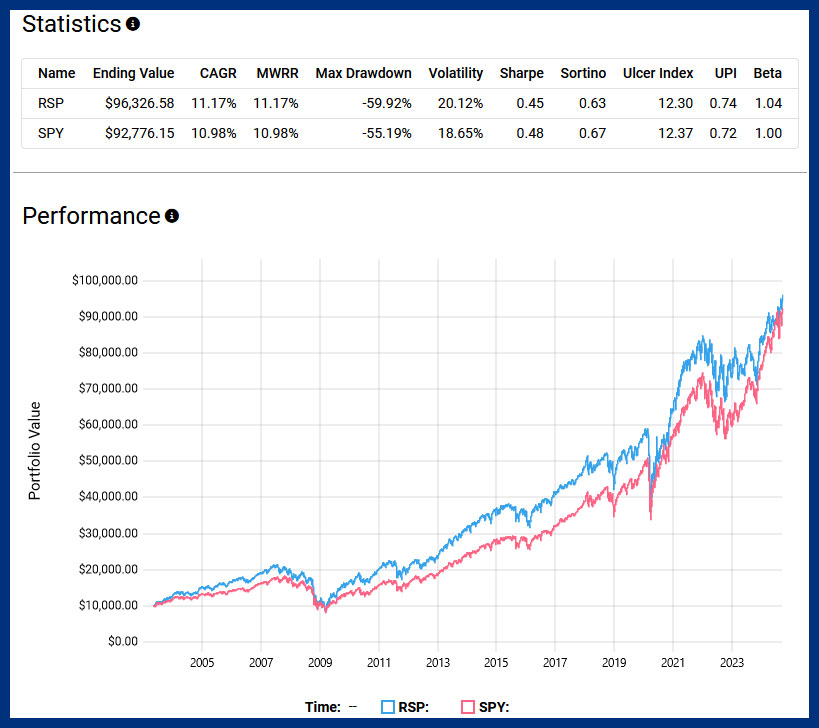

The picture isn’t as clear-cut as it seems, however. One of the primary drawbacks of equal weighting, as critics point out, is the additional drag on performance from its methodology.

Take the Invesco S&P 500 Equal Weight ETF (RSP) as an example. It has a 21% turnover and a 0.20% expense ratio. The Canadian-listed version is the Invesco S&P 500 Equal Weight Index ETF (EQL, EQL.F). In contrast, SPY maintains a mere 2% turnover and a lower expense ratio of 0.0945%.

While it’s true that RSP outperformed SPY in total returns since its inception in April 2003, the victory isn’t as clear-cut as it might seem. The risk-adjusted return of RSP, indicated by a Sharpe ratio of 0.45, is slightly lower than SPY’s 0.48. What does that mean? It could suggest that RSP took on higher volatility for only marginally better returns. Moreover, RSP experienced a deeper maximum drawdown than SPY. A maximum drawdown measures the largest single drop from peak to trough during a specified period, indicating a higher historical risk of losses for investors.

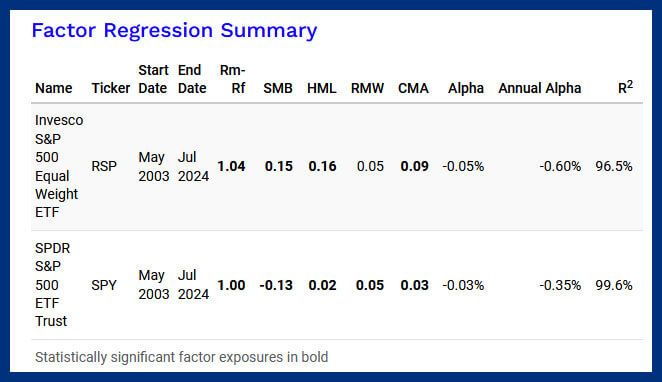

Further analysis via factor regression reveals that most of RSP’s outperformance can be attributed to the size. Essentially, RSP’s equal-weighted methodology has inadvertently skewed its exposure towards smaller and more undervalued companies, which historically have contributed to outperformance.

This raises a critical point: If the goal is to invest in these kinds of companies, wouldn’t it be more straightforward and efficient to target them directly based on fundamental metrics rather than adopting a blanket equal-weighting approach to the entire S&P 500?

I find myself siding with cap weighting now. The primary appeal is simplicity. Market-cap strategies require fewer decisions regarding rebalancing or reconstitution, which in turn keeps sources of friction like turnover and fees considerably lower—resulting in fewer headwinds to performance.

In an ideal frictionless world, the appeal of equal weighting is clear. However, the reality of quarterly rebalancing and higher fees associated with equal-weight ETFs has not historically yielded better risk-adjusted returns over the last two decades.

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Analyzing On-Chain Bottom Indicators

In this week’s dashboard release, we highlighted some key on-chain metrics we like to track. In this article, we want to walk through more of those in detail. Across bitcoin’s short history, many on-chain cyclical indicators are currently pointing to what looks to be a classic bottom in bitcoin price. Market extremes — potential tops and bottoms — are where these indicators have proven to be the most useful.

On-chain indicators overlaid with previous bitcoin price bottoms.

However, these indicators need to be considered alongside many other macroeconomic factors and readers should consider the possibility that this could be another bear market rally — as we still sit below the 200-week moving average price of around $24,600. That being said, if price can sustain above $20,000 in the short-term, the bullish metrics paint a compelling sign for more long-term accumulation here.

A major tail risk is a possible market-wide selloff in risk assets that are currently pricing a “soft landing” style scenario along with the potentially incorrect expectations of a Federal Reserve policy pivot in the second half of this year. Many economic indicators and data still point to the likelihood that we’re in the midst of a bear market similar to 2000-2002 or 2007-2008 and the worst has yet to unfold. This secular bear market is what’s different about this bitcoin cycle compared to any other in the past and what makes it that much harder to use historical bitcoin cycles after 2012 as perfect analogues for today.

All that being said, from a bitcoin-native perspective, the story is clear: Capitulation has clearly unfolded, and HODLers held the line.

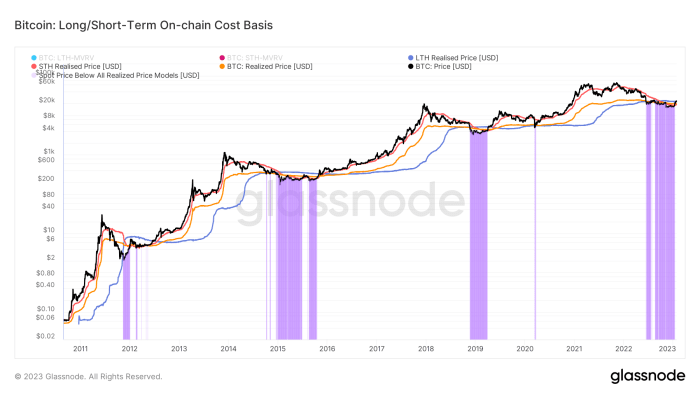

Given the transparent nature of bitcoin ownership, we can view various cohorts of bitcoin holders with extreme clarity. In this case, we are viewing the realized price for the average bitcoin holder as well as the same metric for both long-term holders (LTH) and short-term holders (STH).

The realized price, STH realized price and LTH realized price can give us an understanding of where various cohorts of the market are in profit or underwater.

A look at realized price for short- and long-term holders.

On a monthly basis, realized losses have flipped to realized profits for the first time since last April.

Capitulation and loss taking has flipped to profit realization across the network, which is a very healthy sign of thorough capitulation.

There is a strong case to be made that given the current elasticity of bitcoin’s supply — as evidenced by the historically small number of short-term holders or rather the large number of long-term holders — it will be challenging to shake out current market participants. Especially considering the gauntlet endured over the previous 12 months.

Statistically, long-term bitcoin holders are usually unfazed in the face of bitcoin price volatility. The data shows a healthy amount of accumulation throughout 2022, despite a massive risk-off event in both the bitcoin and legacy market.

While liquidity dynamics in legacy markets should be noted, the supply-side dynamics for bitcoin look to be as strong as ever. All it will take for a significant price appreciation will be a small influx of newfound demand.

Like this content? Subscribe now to receive PRO articles directly in your inbox.

The below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

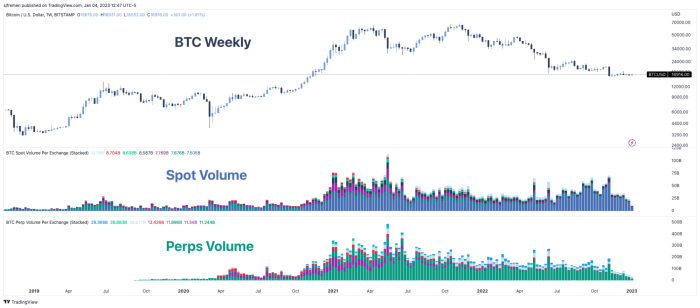

As we head into 2023, we want to highlight the latest state of bitcoin’s volume and volatility after a recent wave of capitulation. Last time we touched on these dynamics was in “The Bitcoin Ghost Town” in October, where we highlighted that an extremely low volume and low volatility period in bitcoin price, GBTC and the options market was a concerning sign for the next leg lower. This played out in early November.

Fast forward and the trends of declining volume and low volatility are back once again. Although this could be indicative of another leg lower to come in the market, it’s more likely indicative of a complacent and decimated market that few participants want to touch.

Even during the November 2021 capitulation period, there was a historically low period of volatility. Sometimes the most market pain can be felt when having to wait for a clear change in trends. The bitcoin price is providing that pain as we’ve yet to see the type of explosion in market volatility that has defined market pivots and major directional moves in the past.

SPX Bottoms

While there are many different ways to define, classify and estimate bitcoin volume in the market, they all show the same thing: September and November 2021 were the peak months of action. Since then, volume in both the spot and perpetual futures markets have been in steady decline.

Bitcoin volume across spot and perpetual futures markets

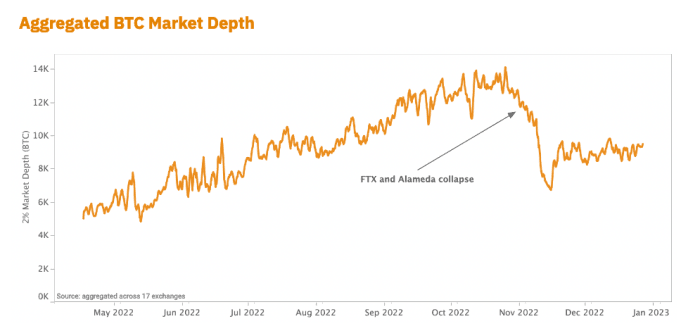

Overall market depth and liquidity has also taken a major hit after the collapse of FTX and Alameda. Their destruction has led to a large liquidity hole, which is yet to be filled due to the lack of market makers currently in the space.

By far, bitcoin is still the most liquid market of any other cryptocurrency or “token,” but it’s still relatively illiquid compared to other capital markets since the whole industry has been crushed over the last few months. Lower market depth and liquidity means assets are prone to more volatile shocks as single, relatively large orders can have a greater impact on market price.

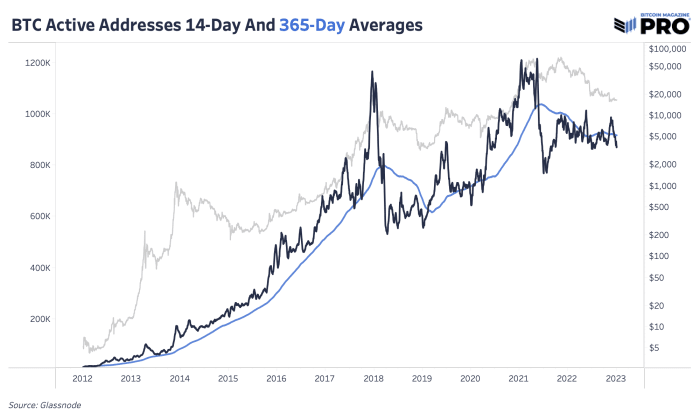

As expected in the current environment, we’re also seeing more market complacency when looking at on-chain data. Although continuing to rise over time, the number of active addresses — unique addresses active as either a sender or receiver — remain fairly stagnant over the last few months. The chart below highlights the 14-day moving average of active addresses falling below the running average over the last year. In previous bull market conditions, we’ve seen growth in active addresses outpace the existing trend fairly significantly.

Moving averages of active bitcoin adresseses

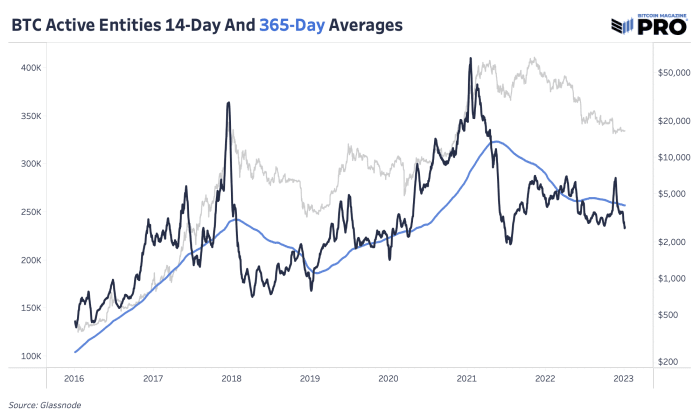

Since address data has its flaws, looking at Glassnode’s data for active entities shows us the same trend. Overall, bear markets reversing are the result of many factors, including growth in new users and an increase in on-chain activity.

Moving averages of active bitcoin entities

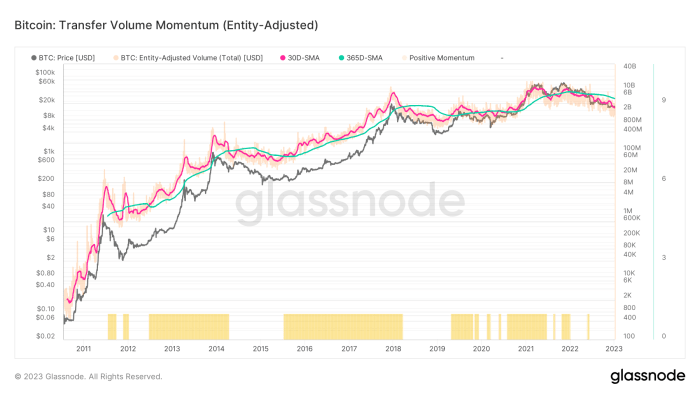

Bitcoin transfer volume momentum

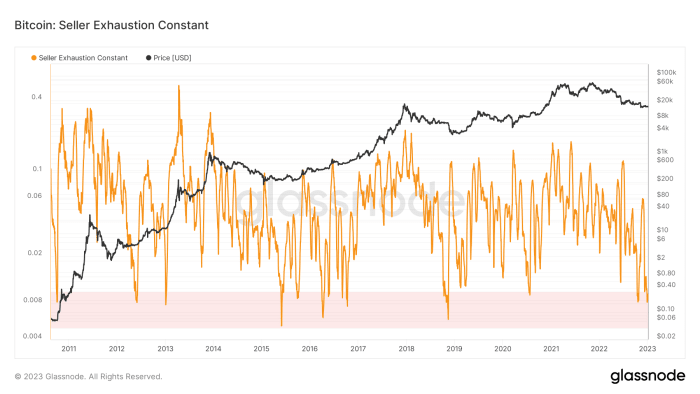

Bitcoin seller exhaustion levels

In our July 11 release “When Will The Bear Market End?”, we made the case that the brunt of the price-based capitulation had already been felt, while the real pain ahead was in the form of a time-based capitulation.

“A look at previous bitcoin bear market cycles shows two distinct phases of capitulation:

“The first is a price-based capitulation, through a series of sharp selloffs and liquidations, as the asset draws down anywhere from 70 to 90% below previous all-time-high levels.

“The second phase, and the one that is spoken of far less often, is the time-based capitulation, where the market finally begins to find an equilibrium of supply and demand in a deep trough.” — Bitcoin Magazine PRO

We believe time-based capitulation is where we stand today. While exchange rate pressures can certainly intensify over the short term — given the macroeconomic headwinds that remain — the conditions that look likely to persist over the short and medium term look to be a sustained period of chop with extremely low levels of volatility that leave both traders and HODLers questioning when volatility and exchange rate appreciation will return.

Like this content? Subscribe now to receive PRO articles directly in your inbox.