New updates have been made to Ripple’s XRP Ledger (XRPL) as the network looks to dominate and gain more traction. This is also a positive for XRP, which serves as the network’s bridge currency.

Ripple’s XRP Ledger Gets A New Update

In an X post, XRP validator Vet revealed that the credentials amendment on the XRP Ledger is now active. He explained that credentials can be applied to attest to compliance requirements, such as KYC and AML, for a user or institution and issued to their decentralized identity. This helps to further build trust in the network.

Related Reading

Vet also noted that the amendment has all been done natively on the XRP Ledger. Notably, this update is part of a larger move to enable compliance amendments on the network. With decentralized identities and credentials implemented, Vet indicated that their next focus is to work on the permissioned domains and permissioned DEX.

Ripple and other XRP Ledger stakeholders aim to utilize these compliance amendments to attract more institutions to the network, enabling them to adhere to traditional finance (TradFi) standards even on-chain. This also comes as the network aims to become the go-to for tokenization. Ripple recently stated that 10% of global assets will become tokenized by 2030, and is undoubtedly looking to tap into this trillion-dollar market.

Ripple Engineer Breaks Down Significance Of This Update

In an X post, Ripple engineer Kenny explained that the credentials update gives developers and businesses a way to handle identity checks and compliance requirements directly on the XRP Ledger. With these, they do not need to approve each account one by one manually. The Ripple engineer noted that traditionally, verifying user credentials like KYC requires multiple checks across different platforms.

Related Reading

Kenny remarked that this process isn’t only inefficient but also increases privacy risks because sensitive information has to be shared multiple times. As such, this makes the XRP Ledger credentials update vital. The Ripple engineer revealed that this feature enables credentials to be issued, stored, and verified natively on the XRPL.

He noted the benefits of how this allows users to prove a required criterion without undergoing repeated verification. Kenny also stated that this will improve the onboard process and enhance security, while maintaining privacy. The Ripple engineer further gave an example of what a typical flow will look like using this credentials feature.

A business will define the credentials it requires, such as the KYC, then a trusted issuer creates and signs that credential. The user then accepts and stores these credentials in their XRP Ledger account. That way, the credential is checked on-chain whenever the user interacts with the business.

At the time of writing, the XRP price is trading at around $2.83, up in the last 24 hours, according to data from CoinMarketCap.

XRP trading at $2.81 on the 1D chart | Source: XRPUSDT on Tradingview.com

Featured image from Adobe Stock, chart from Tradingview.com

JPMorgan Chase is reaping rewards in know-your-customer operations from deployment of AI. The bank processed 155,000 know-your-customer (KYC) files in 2022, using 3,000 people to accomplish the task. “By the end of next year, we will process 230,000 files with 20% less of the people. It’s an increase in productivity between 80% to 90%,” Chief […]

The automated clearing house payment system reaches all U.S. bank accounts and is an extremely cost-effective way to move money. This helps explain the ACH Network’s steady growth.

Shamir Karkal, co-founder and chief strategy officer, Sila

Nacha says the ACH Network processed 7.6 billion in payments worth $19.2 trillion in the third quarter of 2022. Meanwhile, ACH same-day payments reached 176.6 million, up 23.5% from the third quarter of 2021. And Forrester Research says that “2023 will be the year when at least one major global retailer begins accepting ACH-based payments on their site, as some challenger brands already have.”

As the volume and value of ACH transactions continues growing, ACH fraud has been surging.

Our real-time world, financial system complexity, the lack of an ACH dispute mediator and the fact that pandemic relief funds inadvertently provided fraudsters with the resources to launch more (and more sophisticated) attacks also contribute to the ACH fraud problem.

ACH has been around for more than 50 years. It was built in a 9-to-5, Monday-through-Friday banking world. But we now live in an on-demand world in which financial services occur at all hours and every day.

The rise of two-sided marketplaces, a plethora of new banks and bank-like organizations that connect to them, peer-to-peer transfers and other complicated payment flows created more entry points and opportunities for attack.

Also, unlike card networks, for which MasterCard and Visa mediate between card issuers, consumers and merchants, no one mediates and resolves disputes in the ACH arena. That’s why ACH is less expensive than card networks. It’s also why ACH has seen higher levels of fraud.

The U.S. government’s Paycheck Protection Program (PPP) and other Coronavirus Aid, Relief and Economic Security (CARES) Act programs also “have placed lenders and borrowers at significant risk for criminal and civil liability,” as law firm Arnold & Porter explains. The PPP inadvertently gave some mom-and-pop cyberattackers access to funding, which they invested in more people and technology. That, in turn, has made some of these smaller bad actors bolder and more ambitious.

So, what should fintech startups that are developing and promoting applications be aware of when they are suddenly hit with fraud? And how can they limit ACH returns so that they don’t face penalties from Nacha, regulators and their suppliers? Let’s take a look.

Architecture and data matter

Fraudsters can be extremely inventive. A two-sided marketplace company once saw a fraudster create a business, apply for money on one side of the marketplace and go to the other side of the marketplace to fund the loan. The fraudster then transferred it over, moved the money to a separate bank account and then did an unauthorized return — and the money vanished.

Be aware that ACH fraud is almost unavoidable. ACH is batch-based. It’s a technology that was created in the 1970s. And there is no authentication or authorization baked into ACH.

How best to address ACH fraud varies by organization. But if you have any kind of fraud controls, you’re going to decline some people because you’re concerned their requests are not legitimate. However, you really won’t know whether those requests actually are fraudulent. So, collect data both from the people that you approve and from those that you decline over concerns of fraud. Learn from that data and be willing to rethink your fraud controls over time.

Understand fraud prevention is not a one-and-done endeavor

A customer might have a good first or second transaction. But 18 months later, that same customer might want to do a $10,000 transaction, which would be a signal in itself.

Small transactions can also signal a fraudster has overtaken an account. If account transfers are typically $5,000 and you see a $5 transaction, it may indicate a fraudster is testing the waters.

Stay vigilant. Implement fraud controls up front. And continue to fine tune those controls.

Review Nacha’s Risk Management Framework, which helps those who use the ACH Network and other payment systems using credit-push payments with guidance on how to address new and persistent fraud. Nacha says, “The most significant fraud threats to bank account holders involve fraud and scams that result in money being sent out of their accounts using credit payments, including ACH credits, wires, cards and other instant and digital payments.”

Get to know the Office of Foreign Assets Control (OFAC) guidelines and ACH fraud mitigation guidelines under National Institute of Standards and Technology cybersecurity maturity levels. And wait 48 hours to process ACH return codes.

Implement good, old-fashioned velocity controls

When a new customer comes in, sometimes that customer is clearly a fraudster.

But there’s also a lot of gray area, where you see some signals of fraud, but you’re not entirely sure that they’re fraudulent. For example, folks who usually do transactions from home might just be on vacation. You don’t necessarily want to decline all people due to their locations.

Implement velocity controls that look at how the user’s 10th transaction is different from their sixth, second or first transactions. Consider what other parameters are different among those transactions. And, above all, take steps to ensure customers are who they say they are.

Leverage biometric verification. You might not need it on Day One, but you may find it extremely useful as you scale. Employ technologies that allow you to add security easily, because if it takes six months to get biometric verification in place, you’re going to lose a lot of money. Without velocity controls and biometric verification, you will have to rely exclusively on know-your-customer data, and your business will suffer mightily from fraud.

Most organizations experience fraud somewhere between their 50th friend-and-family user and their 5 millionth customer. So, if you think about it, you can look at fraud as a badge of success. It means that your business has achieved enough scale to draw fraudsters’ attention.

But leaving fraud unchecked will have serious implications for your organization. So, take the steps above to control ACH fraud. And adopt a payments-as-a-service solution and trusted partner that arm you with the technology and know-how that you need to combat fraud.

Shamir Karkal is a co-founder and chief strategy officer of Sila, a fintech software platform that provides payment infrastructure as a service.

Financial institutions today are teetering into a Nash Equilibrium.

Mike Butler, CEO, Grasshopper

A Nash Equilibrium, named for mathematician John Nash, occurs when players in a game can fully anticipate the choices of other players. When all players’ actions are considered, everyone is able to achieve their objectives. Every player wins.

The concept was a groundbreaking contribution to game theory study and continues to be widely used by economists — but it also has practical applications. In the banking industry, financial institutions can benefit from Nash’s work by adopting a holistic approach to personalization, better understanding individual customer needs in order to make business decisions based on real market demand. This strategy is proving to be an effective way to connect with customers and win business.

Creating a tailored platform

The expansion and adoption of digital banking has unlocked the opportunity to create a highly individualized customer experience known as “hyperpersonalization.”

Deloitte defines this as “using real-time data to generate insights by using behavioral science and data science to deliver services, products and pricing that are context-specific and relevant to customers’ manifest and latent needs.”

Personalization powered by real-time data and analytics to serve each distinct customer has quickly become an expectation. A Salesforcesurvey found that 56% of customers expect banks to anticipate customer needs and make appropriate recommendations even before initial contact.

Banks are using automation to serve individual clients by tracking transactional activity and extracting unique data. They use the information to provide services that best fit specific customers’ needs. Based on customer expectations, banks are aggressively pursuing these strategies. HSBC executives expect hyperpersonalization will become a new standard of service, and JPMorgan Chase is investing $12 billion in cloud and AI technologies to strengthen the customer experience.

Leveraging partnerships to meet goals

Financial institutions understand that technology is the gateway to achieving hyperpersonalization.

In a survey conducted by information technology services company Wipro, industry leaders listed “improving the user experience with greater personalization” as the most valuable use of AI technology. However, most financial institutions are not equipped with the infrastructure to collect and process data, conduct pertinent market research and retain qualitative feedback from customers.

To bridge the technology gap and advance the integration of hyperpersonalization, banks are partnering with fintech companies like Plaid, MX and Alloy, which provide the mature and future-ready technology that banks need to foster a custom experience and better connect with customers.

With access to the right technology, the potential for hyperpersonalization is infinite. Leveraging automation and machine learning technologies gives banks an opportunity to connect with potential customers, solidify existing customers and serve as a differentiator in an increasingly diverse marketplace.

Knowing your customers inside and out

At its core, this strategy is simply a means of better understanding customers and the market. Technology can reveal subtle insights into customer patterns and behaviors and the trends shaping the market to deliver individualized solutions. Banks are able to use data to assess the risks and rewards, and make a decision that is best for the organization’s goals.

The strategy should also include an analysis of competitor activity, including niche submarkets and emerging specializations. Information about other industry players will reveal market gaps or unmet needs as well as overserved demographic groups or areas of the market with the potential to become overheated. Digital banks can use this information to decide which market areas to pursue and where the company’s product lines and expertise best fit within the existing market dynamics.

Building loyalty

Banks are not the only beneficiary of a hyperpersonalized strategy. SMBs will benefit from individualized analysis, intelligent insights and personal communication. The strategy will not only win customers but establish a meaningful connection that will evolve into a trusted and loyal relationship. According to research from Deloitte on hyperpersonalization in banking, “emotionally connected customers are more than twice as valuable as even highly satisfied customers.”

To achieve a human connection, a personalization strategy should include progress reports for customers tracking financial performance, support and consultation, and education about how a company’s financial objectives are linked to broader economic, social and environmental trends. This is where customers will see the qualitative benefits of a bespoke platform.

With hyperpersonalization, the digital banking industry is playing a positive sum game, one where both banking customers and financial institutions win. The trend is redefining competition in the financial services industry and delivering better banking to small businesses. That truly is a victory.

Mike Butler is the chief executive of digital bank Grasshopper which offers small businesses products and services for specific industries such as commercial real estate lending and yacht financing.

This is an opinion editorial by Robert Hall, a content creator and small business owner.

What is the most likely path to hyperbitcoinization? This is a question that has come up in my mind time and time again. Will it be a top-down implementation like we saw in El Salvador last year? Regarding world leaders, Nayib Bukele is the rare exception to the rule. Most world leaders think within a predefined box of fiat options.

Bitcoin adoption in Nigeria has continued to grow despite their central bank banning legacy financial institutions in Nigeria from interacting with Bitcoin at all. Bitcoin P2P trading in Nigeria is up 27 percent despite the ban.

Bitcoin adoption in Nigeria and El Salvador are two examples of opposite sides of the adoption spectrum. Both are working despite legal hurdles and educating more people about Bitcoin.

What will widespread adoption look like in developed countries such as the United States, Europe and developed countries? The dynamics in the West differ significantly from that of developing countries. Western countries have the rule of law, regulated markets, a population that has access to bank accounts and a currency that doesn’t debase as rapidly as other currencies.

Bitcoin adoption in the West is going to take a fundamentally different path than the path other parts of the world are going to take. This should be acknowledged and inform how Bitcoiners talk about adoption in the western world.

If you live in the West, you live in an economic and political panopticon. Your government knows who you are, where you live and how much money you earn. They also can gather your phone records, transaction history and online activity with impunity via third-party providers.

If you have money in a bank account, Western governments can call your bank, tell them you are a terrorist, and seize your bank account. Don’t think it can happen to you? It happened in Canada to regular everyday citizens protesting against government policies they disagreed with and were agitating for change. The Canadian truckers were not violent thugs with weapons; they used well-established protest tactics to have their voices heard.

Think this is an isolated incident? Authorities in the Netherlands opened fire on a farmer protesting against government plans that would have them cut nitrogen oxide and ammonia emissions by 70 percent in seven years. The state could give two sh*ts about your life if it gets in the way of their plan, plain and simple. You know it, and I know it. There is no need to sugarcoat anything here.

The idea that we are free is folly. Bitcoin is our best hope to change our current circumstances, but it starts with people purchasing and owning Bitcoin.

Where Do People In The West Buy Bitcoin?

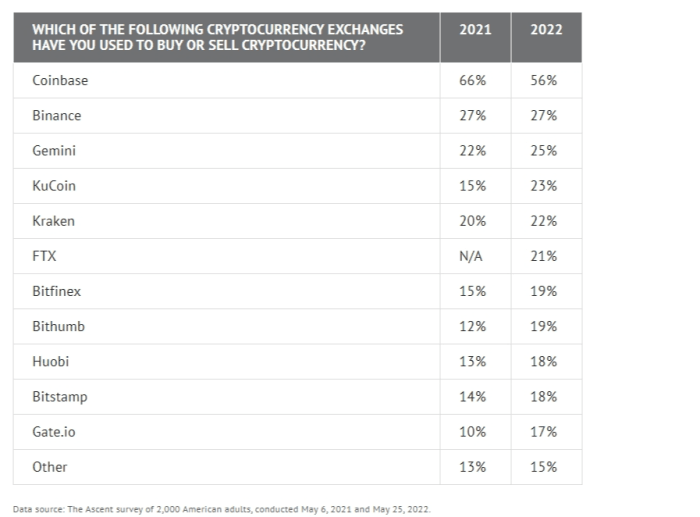

For a large majority of people new to Bitcoin, their first interaction with bitcoin will be through exchanges such as Coinbase, Kraken, Binance and OkCoin. Not ideal, but these are the facts.

When someone new to Bitcoin searches “how to buy bitcoin,” the first page results will show you where you can buy bitcoin from exchanges.

These entities comply with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations set forth by their jurisdictions.

The people new to Bitcoin will have no problem handing over their personal information to these companies because they see it as normal and is something they have done their whole lives. This is a fact of life that isn’t going away anytime soon.

This is an unpopular opinion, but I will say it anyway. Mass adoption of Bitcoin in the Western world will be with KYC’d Bitcoin. I wish it weren’t the case, but I don’t see how it won’t be. There is even an implicit realization of this fact on Bitcoin Twitter.

The new people coming into Bitcoin won’t be your anarcho-capitalist types that want nothing to do with the state. The next wave of people coming into the space will be the mom-and-pop shop owners down the street, your truck driver, mailman or a teacher looking to save their hard-earned money in money that the government can’t debase.

Many people see the government and the laws and regulations they promulgate as a form of safety. They might see KYC as a good thing. Currently, KYC is a fact of life, and this creates honeypots of information for hackers to target. We’ve dealt with this problem in the fiat world; we’ll also have to deal with it on a bitcoin standard. I didn’t make rules; I’m just looking at the facts as they are now. That doesn’t mean any of this can’t change.

Still, I believe advising newcomers about different privacy methods is the way to go. There are many great articles here on how to make your Bitcoin more private.

In addition to teaching newcomers about privacy methods, we should all work on creating a bitcoin-powered parallel economy where we don’t need fiat offramps. This is the ultimate goal.

El Zonte in El Salvador and other communities have shown us how we can follow in their footsteps.

The future of bitcoin is bright if we can get enough people on the bitcoin lifeboat. We shouldn’t quarrel about what path they took to get there, but educate them on the most private ways to do so.

Stay focused on the mission. Educate others. Stack sats.

This is a guest post by Robert Hall. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.