Fear, uncertainty and doubt around Ripple’s cross-border payments token has increased, according to blockchain analytics.

XRP is seeing its “highest level of retail FUD” since US President Donald Trump announced trade tariffs six months ago, reported blockchain analytics firm Santiment using a bullish-to-bearish sentiment ratio on Tuesday.

Trump’s global tariff bombshell in April triggered a massive 20% XRP price drop to below $1.80 within days in line with a broader crypto market sell-off.

However, it is not all bad news. There have been more bearish comments than bullish for two of the past three days, it stated before adding that this is “generally a promising buy signal” because markets move opposite to small trader expectations.

😮 XRP is seeing it’s highest level of retail FUD since Trump’s tariffs were announced 6 months ago. There have been more bearish comments than bullish for 2 of the past 3 days, which is generally a promising buy signal. Markets move opposite to small trader expectations. pic.twitter.com/flO7jjlo9m

The negative sentiment arises as XRP has failed to perform, while others in its vicinity, such as Bitcoin, Ether, and BNB, have reached new all-time highs or come close to previous ones. Additionally, BNB flipped XRP in terms of market capitalization this week.

“Nothing to do with FUD, but just pure reality with XRP value accrual that is literally zero and doesn’t benefit holders at all,” said one respondent.

Historical sentiment analysis shows extreme retail FUD often precedes XRP rallies, as seen in July’s run-up to an all-time high of $3.65. However, the token has tanked more than 21% since then and has failed to break resistance above $3 multiple times since mid-August.

In reality, things are looking very bullish for Ripple and XRP, with legal and regulatory clarity expected to arrive in 2025 and an expansion of partnerships and integrations within the global TradFi ecosystem.

You may also like:

The Ripple DeFi ecosystem has also gone through recent expansion, as reported by CryptoPotato.

The CEO of agricultural investment firm Teucrium, Sal Gilbertie, said XRP was “a coin that will have the most utility out there,” and XRP has “a true use case.”

🗣️When the CEO of Teucrium says $XRP has real utility and calls it the coin with the most use case…

Nevertheless, retail traders and investors remain unconvinced, as the asset has fallen 3.8% on the day to $2.87 at the time of writing.

XRP touched $3.10 late last week, but resistance proved too strong again, causing the retreat. The asset has traded sideways since its surge in mid-July but is up 38% since the beginning of the year and a whopping 440% since the same time last year.

Chart guru Peter Brandt painted a gloomier picture, identifying a “classic descending triangle” developing, adding that there is a danger of a fall to $2.22 if XRP closes below $2.68.

SPECIAL OFFER (Sponsored)

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

Ethereum has become the default settlement layer engine of decentralized finance, and Tom Lee, the co-founder of Fundstrat Global Advisors, has recently expressed a bullish stance on ETH that was far from a random call. This dominant position explains why Lee’s confidence in ETH is rooted in speculation and the backbone of digital finance.

How Ethereum Powers The Largest Share Of Decentralized Finance

In an X post, analyst AdrianoFeria has highlighted that Tom Lee, the co-founder of Fundstrat Global Advisors, has chosen ETH because it is the default choice for stablecoins, tokenization, and DeFi, and the very rails on which the future of finance is being built. Ethereum is the internet of finance, and Wall Street is finally waking up to the reality.

Tom Lee and more high-profile figures of institutional finance are entering the ETH race and quietly building positions. The analyst noted that Ethereum treasuries are not just decentralized asset trackers (DATs). Rather, they are the perfect vehicle for influential billionaires who are late to ETH to gain leveraged exposure, while gifting early investors an entire army of mainstream ETH bulls who will defend their allocation in the media and beyond.

He has also stated that the representation of these treasuries and the capital flowing in is not just retail noise anymore, but is big money with a megaphone. The people backing Ethereum are changing the story at the highest levels of finance, and ETH is getting closer to cementing its role as the backbone of global markets.

However, this isn’t Bitcoin’s game anymore. It’s Ethereum’s internet of finance, and the smart money knows it. For those still clinging to the tired argument that ETH isn’t a store of value, the market has been slapping that narrative down for a decade. Despite endless FUD from no-coiners and even insiders, ETH has been the best-performing asset in the world over the last ten years.

Why ETH’s Volume Momentum Could Matter For Bulls

Following its recent upward trend to a new all-time high, AdrianoFeria also revealed that the ETH momentum over the past three months has been more than just price appreciation. It has been a showcase of growing market dominance. Unlike most altcoins, ETH has consistently brought higher trading volume on exchanges compared to any other crypto asset, including Bitcoin.

ETH’s volume has been trending upward steadily, while signaling sustained investor interest and market activity. The widening gap between ETH and BTC trading volumes underscores a shift in market attention, and as ETH/BTC continues to climb, more traders and institutions are prioritizing Ethereum.

This is an opinion editorial by Joakim Book, a research fellow at the American Institute for Economic Research and contributor to Bitcoin Magazine, HumanProgress.org and the Mises Institute.

Finding fault with Bitcoin and Bitcoiners is easy. Every schmuck, stick, know-it-all pundit, wiseass and establishment elite has a handful of complaints readily available. Bitcoin uses too much electricity; its fixed money supply schedule makes interventions from a benevolent central bank impossible; it doesn’t have enough inflation for a growing economy; it is used by pesky criminals; and its mean, technobabbling users hurt my brittle feelings.

The objections get tiresome about as quickly as they get recycled.

One fantastic example is the doomspeaker economist Nouriel Roubini, known for his bombastic and bearish declarations — frequently nicknamed “Dr. Doom” by the financial press. In his own mind, he is merely “realistic,” which every madman would say about himself when queried. In his latest book, “Megathreats: The Ten Trends That Imperil Our Future, And How To Survive Them,” he insists that most people overlook something about this infamous nickname:

“Those who label me Dr. Doom fail to see that I examine the upside with as much rigor as the downside. Optimists and pessimists both call me contrarian. If I could choose my nickname, Dr. Realist sounds right.”

The Bitcoin obituaries site 99bitcoins.com lists our beloved economist hater 12 times, but Googling finds plenty more Bitcoin denouncements from this outspoken character — in every outlet that’ll have him, it seems, from Twitter to the Financial Times.

To Roubini, bitcoin was a bubble in 2013, a “Ponzi game” and “not a currency” in 2014, a “gigantic speculative bubble” in 2017, almost all transactions were fake in 2019 and, most tastefully, in 2020 a little bit of everything:

What his new book does so well is outline the world’s many macroeconomic troubles. For five mesmerizing chapters, he describes the debt problems, the demographic impossibility that is the bankrupt Ponzi (sorry, “pension”) schemes of Western nations, the easy money disaster and the boom-bust cycle that it gives rise to. Stagflation in the 2020s did not come as a surprise to him, and he locates the blame precisely where it should be: “We poured massive amounts of money and fiscal stimulus into a financial and economic system already awash in cash and credit.” With a short-term view and politically-captured central banks, we get disastrously easy money because “that is what voters want and leveraged markets need to avoid crashing.”

He even comes down on the correct side of the 2022 blunder to use the dollar payment rails to sanction a G8 economy: “This sort of weaponizing of currency for the pursuit of national security goals is the latest frontier of the mission creep of central banks, starting with the Fed” (ignoring that the Federal Reserve doesn’t make sanction decisions).

As a rule, whatever Bitcoin’s flaws are — as a money, as a protocol, as a usable tool, as a community — it gets better, relatively speaking, when the incumbent monetary system gets worse. Whatever your position on Bitcoin was three, five or 10 years ago, you must look at it more favorably today: the monetary system in place has gotten so much worse, with inflation, anti-money-laundering bureaucracy, clown-world behavior and frozen accounts being just the worst offenders. All is not well in the world of money; that makes Bitcoin a more tempting prospect, all things equal.

So, is Roubini a Bitcoiner now? Has the ultimate Bitcoin bear, diligently at it for a decade, finally come around? Seeing clearly the monetary madness of the world, it wouldn’t be the strangest thing for Dr. Doom to at last tone down his criticism of Bitcoin.

Instead, we got Groundhog Day.

The single chapter dedicated to financial instability spends a dozen or so pages on Bitcoin, unbelievably dedicating most of them to “crypto,” “DeFi,” “stablecoins” and central bank digital currencies. Sigh.

Still, even here we had potential: The rise of crypto, explains Roubini, “exposes our collective wilting faith in the ability of governments to back the money they issue.” Hear, hear.

Queen Taylor Called

“Ugh, so he calls me up and he’s like ‘I still love youuu’, and I’m like ‘I just… I mean, this is exhausting, you know? Like, we are never getting back together. Like, ever.’”

If you are to critique Bitcoin — something youcertainly, certainly can do — here are some things you should do:

First, get your monetary attributes in order.

There are three — store of value, unit of account, medium of exchange — not five. You can’t invent new ones and duplicating previous ones isn’t useful. Roubini introduces “single numeraire,” which is exactly the same thing as a unit of account, and splits store of value into stable value against “market value” and against “an index of the price of goods and services.” Try carving out a difference. This is silly word play.

Second, make sure your criticism is levied against Bitcoin, not “crypto.”

Most people think of bitcoin as merely the first “cryptocurrency,” the most famous among tens of thousands of scammy shitcoins. It’s not. What holds and happens in the la-la land of vaporware tokens rarely has anything to do with Bitcoin: Sam Bankman-Fried’s shenanigans, Terra’s implosion or the Cryptoqueen scam do in no way detract from Bitcoin’s core, its principles or operations. When Roubini cites “BaconCoin,” quotes LoanSnap’s founder or reports negative comments by DogeCoin’s creator, he does not undermine Bitcoin’s promise.

Bitcoin is a one-off monetary invention, separated from every other money or “crypto” by a Great Wall of categories and concepts: it doesn’t have a company or founder running it, like every other shitcoin does; it doesn’t have counterparty risk nor is it subject to censorship like every other fiat currency. Bitcoin has no CEO and no marketing department; it has the strongest Lindy and the highest hash rate.

Third — and this is a hard one — make sure your points haven’t already been debunked, answered and relegated to the dustbin of unimpressive, erroneous jabs at Bitcoin.

Repeating an outdated accusation makes you look stupid, not Bitcoin. Roubini goes for the vast wealth inequality in Bitcoinland, believing it to be “worse than that of North Korea.” It’s not, and as flawed as these investigations are, UTXO ownership seems to become less and less unequal over time — as you’d expect for an emerging money that gets distributed in use.

Unsurprisingly, it uses too much energy, as much as a small country and therefore “will blunt urgent climate initiatives to slow down global warming.” It doesn’t and it won’t: if anything, Bitcoin unlocks stranded energy, contributes to balancing the grid and miners are more renewable than most major economies.

Fourth, make sure that the property of Bitcoin that you’re attacking isn’t worse in the legacy system.

Warren Buffet often makes this error, thinking that hacks, fees or the fact that bitcoin doesn’t generate “yield” dooms it to failure. Nevermind that paper money doesn’t either (unless you count seigniorage to the central bank); nevermind that his ridiculing of bitcoin as a Ponzi applies equally well to apartments or Uncle Sam’s pension schemes.

The most absurd accusation arrives with Roubini’s silly soda shitcoins: If you need Coke coins to buy Coke and Pepsi coins to buy Pepsi, how could you ever establish (relative) value?! How could you ever know what either of them are worth?

Makes you wonder how Americans could ever buy things when they’re abroad, how pound-based customers (i.e., British residents) can ever acquire anything sold in euros or spend their melting currency on Fifth Avenue. There’s a publicly-displayed market price for you to “convert” value into the monetary system that you’re familiar with; and there’s a publicly-traded market that the banks on either side of your and your vendor’s transaction can trade and settle such that international trade works.

Fascinating.

His currency risk examples are illustrative — and disingenuous. Apparently vendors can’t “price” goods in bitcoin since “an overnight fall in value might wipe out the [seller’s] profit margins.” That’s true as far as it goes, but holds equally so for any cross-currency transaction in the legacy world: imports or export or any supply chain more complicated than your local currency area. Besides, if you worry about the currency exposure in your sales, there is a liquid market that provides hedges for you. Many stores that accept bitcoin through various third-party solutions instantly exchange them for dollars, thus mitigating the risk.

In the very next sentence, Roubini considers the downside of the opposite risk:

“Were someone to write a mortgage with principal and interest in bitcoin, a spike in the value of bitcoin would cause the real value of the mortgage to skyrocket. If default then likely occurs, the lender loses money, and the borrower loses her house.”

I suppose no American therefore owns property in New Zealand or Mexico, no European has debt contracts in USD-dollars. These are not novel risks, but ordinary financial risks that firms and households deal with already.

What’s so fascinating is Roubini’s lack of symmetry: If margins can get obliterated by an overnight drop, then margins can also be doubled by an equal overnight rise. Symmetric risk. If bitcoin’s exchange rate for dollars falls — which Roubini is so certain it will — a bitcoin-denominated mortgage will wipe out itself by becoming easily repayable with appreciating dollars. This isn’t to say that he’s wrong to point out these risks, but that they’re reduced to what economists call “risk aversion.” Unhedged bitcoin transactions or debt contracts are bad if households worry about the downside more than the upside — which, in the real world, seems to be true only to some extent.

The honest conclusion isn’t Roubini’s “bitcoin is incapable of being money,” since many established currencies with volatile values between one another can serve that function, but that an emerging bitcoin economy would have this added, minor layer of business risk.

It’s like Roubini went out of his way to be up to date on all his other macro worries, only to lay forth criticism of Bitcoin that was outdated by the time he first voiced it in the mid-2010s.

Most devastatingly of all: Can anyone really be taken seriously when they slap a plural “s” on the uncountable noun “bitcoin”?

The better you understand the faults of the current way of doing monetary things, the better Bitcoin looks.

When you look at the many macro ills that Bitcoiners are so well attuned to, the pit of your stomach should churn in anxiety. When you look at the debts (public and private) that rampage the system, you should be feeling nauseous. All of this Roubini captures expertly, and much of his writing could even have been featured on these pages. Our beloved economist hater gets the problem, better and more vocally than most. Still, no dice.

It’s unfathomable that someone so attuned to the world’s catastrophic macro problems as Roubini cannot see the master-key solution that is Bitcoin.

This is a guest post by Joakim Book. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

This is an opinion editorial by Level39, a researcher focused on Bitcoin, technology, history, ethics and energy.

On December 14, the U.S. Senate Committee on Banking, Housing & Urban Affairs received inaccurate testimony regarding Bitcoin from actor Ben McKenzie and Professor Hillary J. Allen. The hearing, entitled “Crypto Crash: Why the FTX Bubble Burst and Harm to Consumers,” had all the markings of political theater and provided a stage to misinform senators and the public. It coincided with Elizabeth Warren’s new financial surveillance bill, which is a disaster for privacy and civil liberties. On December 18, the Senate Banking Committee Chair Senator Sherrod Brown divulged on “Meet The Press” that the hearing was intended to “educate the public” on the dangers of cryptocurrencies and floated the idea of banning them altogether.

Mr. McKenzie Goes To Washington

Actor Ben McKenzie, who has starred in “The O.C.,” “Gotham” and “Southland,” lacks the qualifications and expertise one would expect for being called before the U.S. Senate Banking Committee to testify on the inner workings of financial technology. It should therefore come as no surprise that he made basic errors in his testimony, and could have been avoided altogether had witnesses with actual expertise been called. According to Mr. McKenzie:

“Bitcoin cannot work as a medium of exchange because it cannot scale. The Bitcoin network can only process 5 to 7 transactions a second. By comparison, Visa can handle tens of thousands. To facilitate that relatively trivial amount of transactions, Bitcoin uses an enormous amount of energy. In 2021, Bitcoin consumed 134 TWh in total, comparable to the electrical energy consumed by the country of Argentina. Bitcoin simply cannot ever work at scale as a medium of exchange.

McKenzie’s testimony leaves one with the impression that he intentionally sought out the most biased and unreliable sources to confirm his own predetermined conclusions. Unfortunately, it was false information.

In technical terms, McKenzie conflated Visa’s transaction network with Bitcoin’s final settlement network, to make the illogical claim that Bitcoin cannot scale. This is a novice mistake. One could use the same faulty logic to make the erroneous claim that millions of retail payments within the banking system should be impossible because banks typically wait until the end of the business day to settle funds with each other. That, of course, is not true, as gross settlement is precisely how high-volume retail payments are batched between banks.

Visa is a credit-based transaction network. It’s not a financial institution, so it does not actually transfer money and cannot perform final settlement like Bitcoin can. Visa is effectively an IT company that informs its member banks how to clear and perform gross settlement with each other during business hours. If you’ve ever waited a few days for a check to clear, you know that payments between two bank accounts are not instantaneous. Credit card transactions take one to three days to post. And 90 to120 days to settle.

The Visa system works well and offers services such as risk assessment, fraud prevention and clawbacks, but can incur high fees from the banks and intermediaries along the way. Member banks aren’t actually sending each other tens of thousands of payments every second. Instead, they batch millions of transactions together into a small number of final settlement payments. The settlements are typically routed through lower-volume real-time gross settlement (RTGS) networks operated by central banks, such as Fedwire in the U.S. or TARGET2 in the EU.

Bitcoin and Fedwire can perform about the same number of transactions per year. In December of 2020, Bitcoin performed 26 million transfers (counting multiple outputs) across 9.6 million transactions, while Fedwire settled 18 million transactions during the same time period. Just as Visa operates on transactional layers that batch transactions into gross settlement layers, Bitcoin is designed to scale in a similar manner.

Bitcoin’s Lightning Network was formally theorized as a scaling solution at MIT in 2016 and today is a burgeoning Layer 2 open payments protocol, layered on top of Bitcoin. The Lightning Network enables instant payments, and micropayments down to a fraction of a penny, and can scale up to the entire world. Micropayments alone could change e-commerce and the internet itself as we know it. Imagine machines or people streaming fractions of pennies for content or APIs and you can already begin to see a new future for the internet emerging. Traditional finance simply cannot achieve this.

The Lightning Network allows high throughput Layer 3 retail payment apps and services such as Cash App, Strike and many other apps to efficiently batch transactions into Bitcoin’s “blocks” for final settlement. Services on Layer 3 can offer the same protections we are used to in the legacy financial system, but anyone can freely access Bitcoin’s Layer 2 or Layer 1 whenever they want.

“While it would require time and investment, Visa’s payment network could sit on top of the bitcoin network to fulfill payments much the same way it sits on top of the existing banking system.”

There is no doubt that the larger cryptocurrency industry has become rife with fraud, scams and deception and it’s commendable that McKenzie makes an effort to warn the public about those dangers. However, in his haste to condemn the entire industry, he failed to fundamentally understand what sets Bitcoin apart from the seemingly endless “crypto” scams and fraud that have sprung up around Satoshi Nakamoto’s invention.

Bitcoin’s Lightning Network has a theoretical throughput of 40 million transactions per second. Just as the internet took more than a generation to achieve today’s levels of connectivity and reach, the Lightning Network would need time to grow its liquidity for it to achieve this theoretical maximum throughput. The performance of the Lightning Network is already astounding and is faster than traditional contactless payments. Thus, the testimony McKenzie provided to the U.S. Senate Banking Committee that, “Bitcoin simply cannot ever work at scale as a medium of exchange” was not only misleading, it was false.

McKenzie, who after getting high one evening decided to write a book on the rampant fraud in the crypto industry, has since begun a collaboration with journalist Jacob Silverman on the endeavor. McKenzie earned his bachelor of arts degree from the University of Virginia in 2001, majoring in foreign affairs and economics. That the U.S. Senate Banking Committee felt that an actor with an atrophied undergraduate degree in economics would somehow make an expert witness for a particularly complicated financial innovation suggests that the hearing was solely intended as political theater.

Senators Regurgitate Ben McKenzie’s Fallacious Testimony

When it was Senator Mark Warner’s turn to ask questions, he remarked:

“I do think it’s curious that China made the decision to basically take that kind of risk, to ban crypto, because of their, at least, risk/reward analysis… The clunkiness of the technology behind Bitcoin, it could never go to scale no matter what! If you can only do 5 or 6 transactions per second, that is not a scalable tool and obviously a technology at a power and environmental cost. It just doesn’t make sense to me.”

Ignoring for a moment that Senator Warner thought it was “curious” that an authoritarian country made the risk/reward calculation to ban free speech of code and software — which is protected under the First Amendment — McKenzie’s false testimony had misinformed the senator into thinking that Bitcoin cannot scale when it is in fact already rapidly scaling.

SMITH: As I understand it, crypto mining is built on a process that becomes more and more energy intensive, over time. Is that correct?

MCKENZIE: Yes.

SMITH: So, it’s inherently inefficient. Is that correct?

MCKENZIE: The technology is bad.

SMITH: And so, where is the benefit of this kind of innovation? How should we think about the impacts when it comes to the climate and energy impacts? Because when crypto mines are located in communities, those communities often see their energy prices go up — their energy rates go up — is that correct?

MCKENZIE: That’s right. I visited the largest crypto mine in the country, Whinstone, which is in Rockdale, Texas, just outside of my hometown of Austin, Texas. Local citizens are upset. It raises the cost of electricity for all citizens. And it also uses an enormous amount of energy. It took over a former Alcoa aluminum smelting plant that had been abandoned and now we are using it to mine ephemeral digital assets of no productive value.

While it’s convenient that McKenzie just happened to have visited a mining operation and could provide Smith with the exact answers that confirmed her biases, unfortunately he has zero expertise on energy markets, demand response programs, power engineering or mining and has no qualifications to inform congress or policy on the matter.

The idea that Bitcoin mining is an “inefficient” technology and therefore needs the government to reign it in is nonsensical. If it were as inefficient as claimed, there would be no need to stop it, since more efficient technologies would be able to outcompete it and easily replace it. This is precisely the reason we have markets — to let the most efficient and cheapest technologies win over the inefficient and expensive technologies that will fail. Those who are willing to take the risk on those technologies are either rewarded or bear the consequences.

McKenzie doesn’t divulge that ERCOT, the Texas grid, is isolated and therefore is required to have excess dispatchable energy for extreme weather events. That excess energy needs to be consumed by large scale flexible customers who are willing to pay for it is an open market when it’s not needed. Buying energy that would otherwise go wasted, for computation, keeps dispatchable energy profitable and officially classifies Bitcoin miners as beneficial large flexible loads (LFLs) by the ERCOT grid. A recent ERCOT study showed miners are essential to its demand response strategy.

As demand response consumers, miners purchase wholesale energy in advance and buy private insurance products that incentivize them to turn off their machines when prices rise during periods of increased consumer demand — thus balancing the grid and its prices, while increasing grid reliability. The idea that McKenzie or any critic could isolate escalating power prices to a single consumer in a deregulated wholesale market is extremely dubious. Such a claim ignores the recent tripling in natural gas prices, as well as the recent build out of over 10 gigawatts of solar power and Texas load growth from non-mining customers, such as the Tesla Gigafactory.

Senator Smith and McKenzie’s suggestion that mining becomes “more and more energy intensive over time” is highly misleading and shows a lack of understanding of the technology. Like any publicly-traded commodity such as bitcoin, the energy required is economically linked to the public’s demand for its declining issuance, and unfolds in a highly-competitive open energy market. There is nothing about the technology that requires the consumption of more and more energy over time. Bitcoin’s four-year “halving” cycle reduces the rewards that miners receive to purchase energy. In fact, Bitcoin’s critics claim that miners may not be able to afford to buy as much energy, decades from now — a topic which is hotly debated. Eventually, critics will need to get their stories straight. Either miners will have the money to purchase energy in the future or they won’t, however, both outcomes cannot be true.

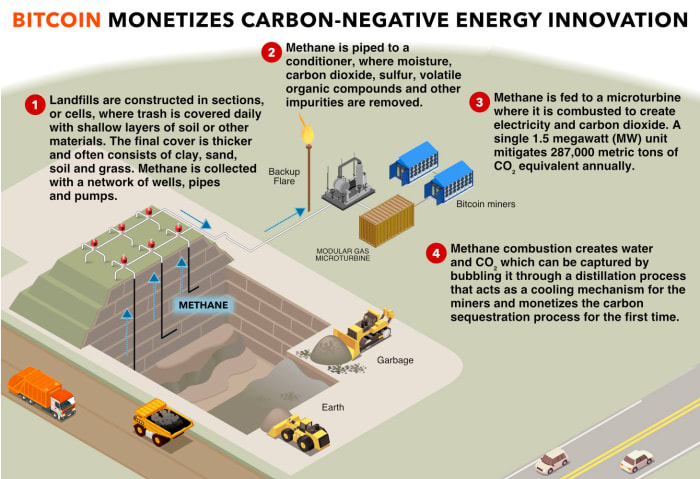

The Senate’s thespians don’t care that Bitcoin mitigates waste methane emissions from oil and natural gas exploration where there is no other use for waste CH₄, which would otherwise be vented into the atmosphere and would heavily contribute to warming forces. To them, Bitcoin is “bad” simply because people having the voluntaryoption for a digital sound money, without counterparty risk, threatens their politics.

“It’s not decentralized… Bitcoin is controlled by a few core software developers — fewer than 10. And they can make changes to the software and that software is implemented by mining pools and there’s just a few of them.”

Allen’s assertion is factually incorrect and shows a fundamentally flawed understanding of how Bitcoin works and why it is valued for being extremely difficult to change. Even if you believe that the project’s maintainers, who have the elevated commit and publishing privileges, could persuade the largest mining pools to support their own whims, they would still need to persuade a majority of the world’s independent miners to stay loyal to existing mining pools. Creating new competing pools is trivial and any software update supported by pools that miners disagreed with could easily be avoided by creating new pools for defectors to join.

And what if miners unanimously supported a software update that users didn’t want? In 2017, 83% of the global hash rate attempted to force an update to increase Bitcoin’s block size and failed because the users, who are actually responsible for propagating and interacting with the Bitcoin network through their own full nodes, refused to install the new software. The Bitcoin network simply doesn’t exist or propagate without the user nodes, so miners defecting to their own network is pointless unless they convince users to come with them. The history of this critical test for Bitcoin was carefully documented by Jonathan Bier in his book, “The Blocksize War: The Battle Over Who Controls Bitcoin’s Protocol Rules.”

Running a full node is fairly easy. At minimum, all it takes is a hard drive, a Raspberry Pi and an internet connection. Since Bitcoin updates with soft forks (backwards-compatible software updates), users who find themselves in the minority always have the right to dissent and oppose contentious updates by just continuing to run the software with the rules they signed up for. Additionally, even if the entire Bitcoin Core team went rogue, users would be able to install alternative competing clients in their nodes, without forking the blockchain.

Other so-called innovative “crypto” projects use coercive techniques to force updates while they try to rapidly innovate like software companies. No other project offers the kind of user rights that Bitcoin offers. As such, there is no incentive for Bitcoin users to run a fork that fundamentally changes Bitcoin’s properties — its resistance to change is the core value proposition that its users are drawn to and demand.

Is it plausible that Bitcoin could be tested again and fail the same test in the future? Of course. But for Professor Allen to ignore the fact that users ultimately decide Bitcoin’s fate — as well as its well-documented history proving its resilience to unwanted changes from miners and developers — shows Allen was either woefully unprepared to be discussing such technical aspects of Bitcoin or is intentionally misleading senators and the public with her testimony.

A Performance Of Misinformation

If anything was evident from the hearing, it was that there was zero effort to ascertain nuance or truth — the hearing was political theater. Unfortunately, having an undergraduate degree in economics, or reaching the higher echelons of Bitcoin-resenting academia, does not automatically qualify one to have the expertise to inform the Senate on how Bitcoin works. If only it were that easy. Understanding Bitcoin requires an open, multidisciplinary mind and hours upon hours of research just to begin scratching the surface. Perhaps Kanye West’s recent public statement on Bitcoin could have gone a long way for McKenzie and Allen.

“As far as Bitcoin, I’m just not knowledgeable enough to speak on that subject.”

Warren’s rapid-fire question and answer session with Allen showed Allen nervously reading, verbatim, pre-scripted answers to Warren’s questions. McKenzie on the other hand had the discipline to memorize and perform his lines with poise and confidence. If only they each had the expertise required to address the U.S Senate Banking Committee on Bitcoin — a technology that quite literally enables self custody and solves the breaches of trust that the hearing was ostensibly concerned with.

Whether the hearings participants realized they were being manipulated by politicians or not, participating in political theater means they are normalizing the loss of privacy rights as they lobby for legislation to limit the right to self custody digital property and one’s identity. Such action not only empowers governments to enact greater monitoring controls, install social credit systems and strip personal freedoms, but it also exposes consumers to the prying eyes of corporations and any hackers that can infiltrate highly-centralized data. Ironically, such restrictions will empower their political opponents when our political pendulums invariably swing in the other direction.

Meanwhile, Warren is headed in the opposite direction. She recently introduced a bipartisan bill with Senator Roger Marshall to aggressively close crypto money laundering loopholes by imposing Orwellian controls on all users. The bill seeks to make self-custody technology illegal — a dangerous policy that would expose Americans to mandated government surveillance and only increase the chances of the fraud that FTX committed against its users when funds were rehypothecated and stolen through their custodial platform. Stopping this kind of fraud was what the hearing was supposed to be about and is exactly the kind of protection that Bitcoin already empowers through self custody.

“Regardless, the good news is two-fold: Cryptocurrency-related crime is falling, and it still remains a small part of the overall cryptocurrency economy.”

However, this is not to say that crypto doesn’t have a problem with fraud. To Allen and McKenzie’s credit, 99.99% of the “crypto” market is indeed scams, and they should be commended for calling them out. Yet, to blindly call Satoshi Nakamoto’s invention a scam shows a lack of critical thinking and expertise. To attack Bitcoin — an open, global and neutral economic protocol layer for the internet with no issuer and no central control — simply because one does not like it or understand it, shows a lack of humility and unwillingness to recognize real-world benefits with an open mind.

If the U.S. Senate Banking Committee has any desire to preserve freedoms and keep the United States from falling behind other nations, it would do well to seek out actual experts who work in Bitcoin mining, energy markets and those who are using its layered payments architecture to build the next generation of commerce. Political theater will only cause the U.S. to fall further behind the rest of the world in all of these areas.