Editor’s note: This is a recurring post, regularly updated with new information.

When it comes to your financial persona, there are few metrics more important than your credit score. This number can influence not only your ability to get approved for top travel credit cards, but also the interest rate you pay on a mortgage, your ability to obtain an auto loan, and a host of other aspects of your life.

If you’ve made a New Year’s resolution to improve your credit score in 2023, here are some strategies to successfully do just that.

Understand credit score basics

Before getting into these tips, let’s start with a quick overview of just what constitutes your credit score. Right off the bat, it’s important to note that there are two main credit scoring models: VantageScore and FICO.

While there are a few minor differences between the two, they both attempt to numerically measure the same thing: your trustworthiness as a borrower.

A lower score indicates that you have a higher risk of defaulting on a loan, thus lowering the amount of money or credit a financial institution is willing to lend you (or lowering the chances of you being approved for a loan at all). A higher score, on the other hand, indicates that you’re less likely to default and thus able to handle larger loan amounts and smaller fees.

Both scores fall on the same scale (300-850) and use the same general criteria:

- Payment history: This looks at how many payments you’ve missed or made late across your credit history.

- Amounts owed: This is frequently referred to as your credit utilization ratio, a measure of how much of your available credit is currently being used.

- Length of credit history: This looks at the average age of your accounts across lenders.

- New credit: This looks at how much new credit to which you’ve recently gained access, including the number of hard inquiries.

- Credit mix: This looks at the different types of accounts you’ve had (credit cards, auto loans, mortgages, etc.).

By paying close attention to these five items — especially the first two — you can be well on your way to improving your credit score.

Related: Your next credit card approval is in the hands of these three agencies

Sign up for our daily newsletter

Review your credit report for inaccuracies

One of the most important things you should do is review your credit report for inaccurate information.

According to a study conducted by Consumer Reports, about a third of consumers found an error on their credit reports. In many cases, these errors aren’t malicious (e.g., identity theft), but rather an inaccuracy related to similar names or other simple mix-ups.

Fortunately, there’s a federally documented process for removing these errors. This article from the Federal Trade Commission provides full details of these steps, including how to request your free credit report every 12 months.

Once you’ve identified an error, submit a dispute letter directly with the credit reporting company; you can use the FTC’s sample for inspiration. The bureau must investigate the complaint, which typically includes going to the organization that provided the disputed information.

If this doesn’t get you anywhere, the next step is to contact the information provider directly with your complaint; again, the FTC provides a sample dispute letter for this purpose. Be detailed but concise, and include copies of any and all documentation that supports your dispute.

While this process can be time-consuming, cleaning up your credit report to be clear of all inaccuracies is an important step you can take to immediately improve your score — or at the very least prevent any future drops in your score related to errors.

Related: How to check your credit score for free

Extend your available credit

Another way to boost your credit score in the new year is to expand the credit line to which you have access. This may seem counterintuitive: surely more credit means more money to spend and therefore more risk, right?

While that’s true on the surface, remember that your credit utilization ratio makes up almost a third of your FICO score (and is also a key part of your VantageScore). That’s why gaining access to additional credit can improve your credit score.

There are two different ways to accomplish this:

- Request credit line increases on existing accounts: Some issuers make it very easy to request increases online, and this generally won’t result in a hard inquiry on your credit report.

- Apply for a new credit card: Even though this will result in a hard inquiry and will temporarily drop your score, it can still give you a new line of credit (not to mention unlock a potentially valuable sign-up bonus). This may outweigh the temporary drop in the short run and will almost certainly help in the long run.

Here’s an example of how this would work. Let’s say you have a single credit card with a limit of $5,000. Even though you pay it off in full every month, the card still has an average balance of roughly $2,500, as you use it as your primary credit card and will continue charging purchases to it as your payment due date approaches. The general rule of thumb is to keep your utilization under 30%, so in this example, you’re well above that (50%).

Now let’s say you request —and are granted — an increase of $5,000. Or maybe you apply for a new card and are given a $5,000 line. With this one action, you’ve just boosted your available credit to $10,000. As long as your balance remains in the $2,500 range, your utilization drops to 25%, which should result in a noticeable increase in your score over time.

However, this only works if you do not use the new credit line to spend beyond your means. As long as your spending remains consistent, you’re simply spreading that amount out over a larger credit limit, dropping your utilization and increasing your score. Credit cards are not necessarily a surefire way to get into debt; make sure you keep your purchases in line with your income.

Related: What is the difference between a hard and soft pull on your credit report?

Set up automatic payments

If you’re the type of person who’s prone to missing a deadline here or there, you should at least have calendar reminders for your credit card payment due dates, and at best have automatic payments enabled on your accounts. As noted above, your payment history is the most important factor in determining your credit score, and even a single late payment can dramatically reduce your score, as it indicates that you may be struggling to pay off your balance.

By setting up reminders or enabling automatic payments from your bank account, you’re ensuring that every payment will be processed on or before your statement due date.

Of course, this comes with the caveat that you must maintain enough money in your bank account to cover the balance that will be paid automatically. Otherwise, the overdraft fee could eat away at your earnings and still result in a late payment.

Related: How to set up autopay for all your credit cards

Budget to pay down outstanding balances

Our No. 1 commandment for travel rewards credit cards here at TPG is as follows: Thou shalt pay thy balance in full.

If you carry a credit card balance from month to month, the interest charges that accrue will easily cancel out the value of the points or miles you’re earning on the card — and then some.

However, you may have an old debt from your freewheeling days as a college student, or maybe you elected to finance a large purchase with an introductory 0% annual percentage rate credit card or deferred-interest offer on a store credit card. Do not let these balances go unpaid. If you haven’t already done so, sit down and put together a budget for how you’ll pay these balances off to avoid (or minimize) your interest exposure.

Related: 4 credit cards that will help you manage your finances better

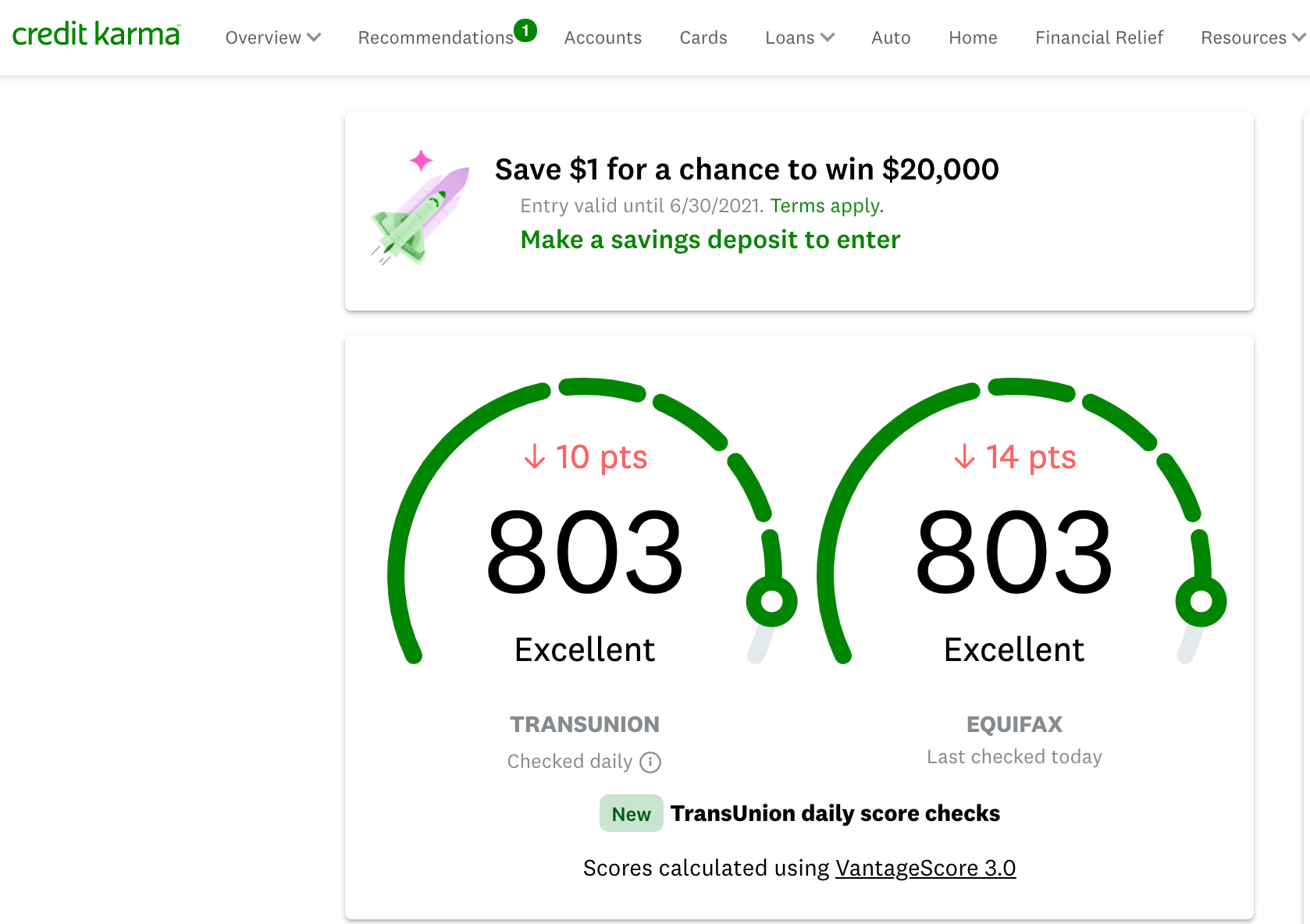

Sign up for credit monitoring

This final suggestion won’t necessarily result in an immediate increase in your credit score. Still, it’s a best practice to keep tabs on your score and to quickly identify any issues that may come up: Sign up for a service that monitors your credit profile and notifies you of any changes.

We like to use Credit Karma, a free service that tracks your TransUnion and Equifax scores and allows you to view your credit report any time you want. You can also set alerts for various things, such as changes to your report.

Bottom line

Whether you’re new to the points and miles hobby or have been around for a while, keeping your credit score high is one of the most important things you can do. Not only will this increase your approval odds for top travel rewards credit cards, but it can also expand your access to installment loans and even lower the interest rates and fees that you’d pay to lenders.

If you’ve made a resolution to boost your scores in 2023, we hope this guide has given you some concrete steps to improve your credit health in the weeks and months to come.

Additional reporting by Emily Thompson, Stella Shon and Benét J. Wilson.