This is an opinion editorial by Hannah Wolfman-Jones, author of “System Override: How Bitcoin, Blockchain, Free Speech, & Free Tech Can Change Everything” and founder of We The Web.

Capitalism is controversialthesedays. Many look at societal problems today and lay the blame squarely at the feet of capitalism. What these crusaders who proudly label themselves as “anti-capitalists” fail to realize is the global fiat system we have today is not really capitalism.

Under capitalism in its pure form, people with capital invest in businesses and ventures that they believe have merit and thus are likely to generate returns. Investors need to make difficult prudent judgments and take on the risk of losing big. Their capital — when invested in a successful business — allows for the creation of services, goods and jobs that are desired by people, making the profits awarded to successful investors just. Through investors in a free market, worthy ventures can get the capital they need to launch or expand a successful business, increasing prosperity across society in a meritocratic manner.

Unfortunately, this system has been greatly disrupted as the decentralized judgements by millions of independent actors in a free marketplace have been supplanted by the unilateral judgements of a few bureaucrats. Under the fiat monetary system, money itself is controlled by a small cabal of unelected economists and bankers. Capitalism is all about free markets. When it comes to our money itself, the currencies used, their supply and interest rates are not market-determined but rather calibrated by bureaucrats. This is not capitalism.

So, instead of spending all their considerable analytical efforts looking at possible business ventures and market needs, savvy capital allocators must follow and predict the actions of central banks, whose edicts can tip entire economies into bear or bull runs. “Don’t fight the Fed,” is an old mantra on Wall Street referring to the idea that investments must align with the current monetary policies of the Federal Reserve to be successful. Investors thus have to follow and theorize around the actions of unelected, unaccountable, powerful centralized actors such as the Chair of the Federal Reserve Jerome Powell. This creates wasted effort and a huge misallocation of resources as the capital available to value-generating businesses fluctuates hugely on the words of one man — Powell — whose actions these businesses do not control. For example, Powell’s speech on August 26, 2022 precipitated a drop in the Dow Jones Industrial Average, the S&P 500, and the Nasdaq Composite of 3.03%, 3.37%, and 3.94% respectively — a staggering fall for just one day. This greatly hinders the meritocratic value creation of capitalism: Savvy investors must make decisions based on Powell’s words rather than a business’s value.

Moreover, under the fiat system, designated legal tenders such as the U.S. dollar are in a perpetual state of inflation. This inflation forces ordinary people looking to save money to risk their capital on investments or else watch their purchasing power be steadily eaten away. Thus, people who are not investors, who lack the skill and desire to risk their capital on business ventures, are forced to do so. Without a venture they believe in for investment, hard-working normal people put their money in indexes and mutual funds. “Zombie companies,” — economically unviable companies that survive through investments while failing to deliver sufficient products and services to the market to cover their costs — can persist for many years due to their inclusion in these indexes and funds. These “zombie companies” receive passive investments from ordinary people who do not know company fundamentals but are forced to invest in indexes and mutual funds to preserve their savings in the face of constant fiat inflation.

If Bitcoin were adopted globally, it would provide hard money that does not depreciate in value long-term. Thus, ordinary people could save in Bitcoin rather than risk their retirements on companies they themselves have not evaluated through mutual funds and indexes. Moreover, the monetary policy of Bitcoin is transparently baked into its code rather than being controlled by powerful central bankers. In a world where Bitcoin dominated over fiat, investors could once again turn all their attention to finding ventures of merit rather than hanging on every word of the Fed. This would largely restore the prosperity-creating engine of capitalism — the least terrible economic system we have.

This is a guest post by Hannah Wolfman-Jones. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Dusk approaches in Yangon, Myanmar. Credit: Unsplash/Alexander Schimmeck

Opinion by Noeleen Heyzer (united nations)

Inter Press Service

UNITED NATIONS, Oct 27 (IPS) – The political, human rights and humanitarian crisis in Myanmar continues to take a catastrophic toll on the people, with serious regional implications.

More than 13.2 million people are food insecure, about 40 percent of the population is living below the poverty line and 1.3 million are internally displaced. Military operations continue with disproportionate use of force including aerial bombings, burning of civilian structures, and the killing of civilians including children.

I condemn the indiscriminate airstrikes on a celebration in Kachin State that killed large numbers of civilians days ago. The People’s Defence Forces are also accused of targeting civilians.

The plight of the Rohingya people, along with other forcefully displaced communities, remains desperate, with many seeking refuge through dangerous land and sea journeys. The price of impunity is a grave reminder that accountability remains essential.

Since the release of the Report of the Secretary-General on the situation in Myanmar, violence between the Arakan Army and the military in Rakhine has escalated to levels not seen since late 2020, with significant cross-border incursions, endangering all communities, harming conditions for durable return, and prolonging the burden on Bangladesh as host of about 1 million Rohingya refugees.

As the Myanmar crisis deepens, I continue to promote a coordinated international strategy, in line with my mandate, engaging all stakeholders for an inclusive Myanmar-led process to return to the democratic transition.

A child looks after his younger sibling in Myanmar. Credit: World Bank/Tom Cheatham

My first visit to Myanmar as Special Envoy in August to meet the military’s Commander-in-Chief was part of broader efforts by the UN to urgently support a return to civilian rule based on the will and needs of the people.

I made six requests during the visit: ending aerial bombing and burning of civilian infrastructure; delivery of humanitarian assistance without discrimination; the release of all children and political prisoners; a moratorium on executions; the well-being of and engagement with State Counsellor Aung San Suu Kyi.

I also highlighted Myanmar’s responsibility for creating conducive conditions for the voluntary, safe, dignified and sustainable return of Rohingya refugees. Soon after, I visited Dhaka and Cox’s Bazar on the five-year anniversary of the Rohingya’s mass displacement, where I expressed the United Nations’ appreciation for Bangladesh’s generosity and heeded Prime Minister Sheikh Hasina’s statements that the current situation is unsustainable.

A highlight of the visit was my discussions with women and youth in the refugee camps. They made it clear that they need to be engaged directly in discussions and decisions about their future.

Their rights and protection, in particular their citizenship, freedom of movement and security, must be guaranteed, guided by the recommendations of the Advisory Commission on Rakhine State. Going forward, I will continue to strengthen co-operation with ASEAN and engagement with all stakeholders.

While there is little room for the de-escalation of violence or for “talks about talks” in the present zero-sum situation, there are some concrete ways to reducing the suffering of the people. Recognizing that many more people will be forced to flee the violence,

I will continue to urge ASEAN to develop a regional protection framework for refugees and forcefully displaced persons. The recent forced return of Myanmar nationals, some of whom were detained on arrival, underlines the urgency of a coordinated ASEAN response to address shared regional challenges caused by the conflict.

Education and skills development are powerful tools to prepare Rohingya refugees for their return to Myanmar, which I continue to advocate, working closely with leaders of ASEAN and neighbouring countries as well as the Organisation of Islamic Cooperation (OIC).

Key Ethnic Armed Organizations and the National Unity Government have together appealed for me to convene an Inclusive Forum for engagement to facilitate protection and humanitarian assistance to ALL people in need, in observance of International Humanitarian Law.

I have also initiated a women, peace and security (WPS) platform on Myanmar with the Foreign Minister of Indonesia to amplify the needs of women affected by the conflict, and their leadership as agents of change.

To conclude, there is a new political reality in Myanmar: a people demanding change, no longer willing to accept military rule. I will continue to appeal to all governments and other key stakeholders to listen to the people and be guided by their will to prevent deeper catastrophe in the heart of Asia.

Noeleen Heyzer, Special Envoy of the Secretary-General on Myanmar, in her address to the United Nations General Assembly’s Third Committee 25 October 2022

This is an opinion editorial by Stephan Livera, host of the “Stephan Livera Podcast” and managing director of Swan Bitcoin International.

Last weekend I had the pleasure of attending and speaking at Liberty In Our Lifetime, a conference organized by the Free Cities Foundation in Prague, Czechia. And it dawned on me that we’re now seeing the rise of an adjacent and relevant movement for Bitcoiners interested in citadels, and what they might even look like in the real world.

The Free Cities Movement is made up of a combination of Libertarians, Bitcoiners, free private city operators and investors, seasteaders, those seeking to create intentional communities and those attempting to create parallel institutions and structures within the existing statist world of today. What lessons are there in this movement and how can more Bitcoiners get involved?

At a high level, there is a strong crossover between the cause of many Bitcoiners and those pursuing free cities. They have a broadly Libertarian ethos, and they’re interested in financial freedom and creating parallel structures. For people unfamiliar with the free cities movement or the free private city concept, I recommend listening to my podcast episodes with Titus Gebel (SLP161, SLP417) or, of course, reading the free private cities white paper as ways of learning more.

As a leader in the free private cities movement, Gebel opened the conference up with a reminder on why there is a fundamental need for this parallel approach. He noted that modern day states are being driven by the “bolshe-woke” progressives. Many institutions of society have effectively been captured, bloated and/or corrupt. Progressives simply go where their ideas do not have to work in the real world, such as universities or in media. Over time, the social and cultural degeneration has worsened, such that even a moderate or center-left person in decades gone by is now considered a “far right wing” person.

For this reason, there is a need to create alternatives. But it is only through trial and error that we can understand which approaches work, and which ones don’t. Of course, there will be many states that resist this kind of thing, but there may be some that can be brought on board if the approach is “win-win” in terms of creating jobs and opportunities for people locally, or perhaps to attract foreign investment.

Overall, I sensed a bias toward action rather than merely speaking about the philosophy of freedom and Libertarianism, which is one I appreciate.

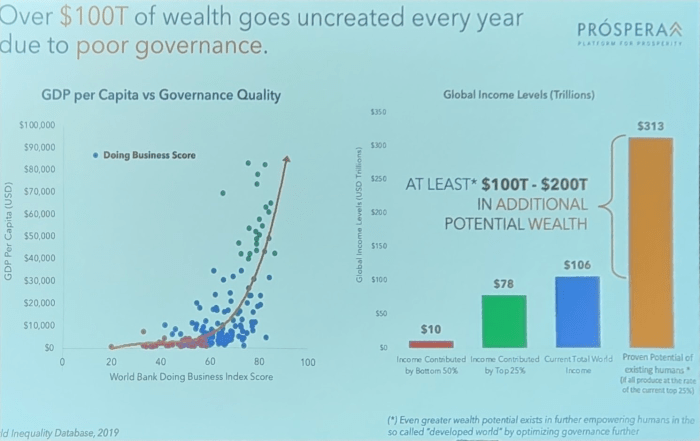

ZEDEs: Próspera Morazán And Ciudad Morazán

Some of the most prominent projects within the free cities community are based on the idea of using Honduran Zones For Employment And Economic Development (ZEDEs) to create the conditions for good, private governance.

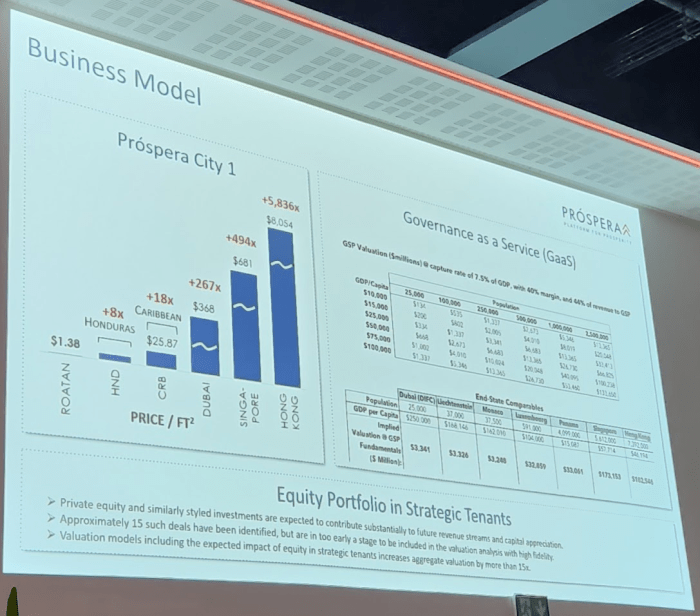

Now, there’s good and bad. The good is that the projects are carrying forward with building, and given a set up that promises favorable regulation and lower taxes, this could be attractive for investors, entrepreneurs and even workers. The bad is that there are challenges on the way, and some states will resist as they could view free private cities as a challenge to their national sovereignty.

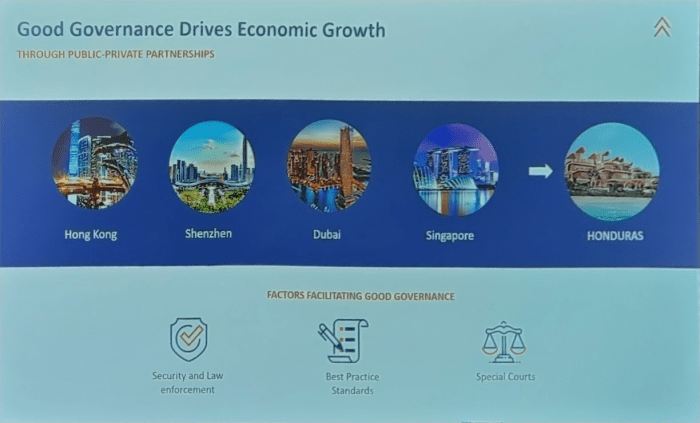

Trey Goff of Próspera spoke about the market for governance and how globally, there is a huge market here in additional potential wealth. How much extra wealth could be created if people all around the world had access to high-quality governance?

Could these free private cities replicate the successes of other economically free zones such as Shenzhen, Hong Kong, Singapore or Dubai?

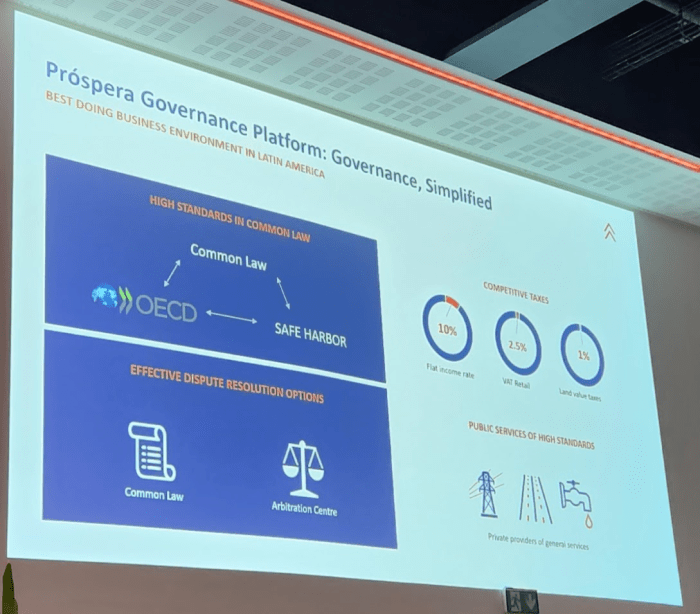

The Próspera governance platform was laid out like so:

Goff also noted that by providing the right circumstances, such as competitive taxes (such as a 10% flat income tax, 2.5% value-added tax (VAT) and 1% land value), along with high-quality infrastructure and dispute resolution, they might hypothetically achieve the following growth:

And it’s not all about rich businessmen and expats. There will be job opportunities for, say, local Hondurans who could come and work for a company inside the ZEDE/free city. There are some projects that intend to provide work opportunities for blue-collar workers, and have housing that is low cost and accessible. Some speakers mentioned how the ZEDEs are looking to hire Hondurans and provide well paid jobs, paying above what they would otherwise be earning.

The Elephant In The Honduran Room

To be clear, there is one elephant in the room: the recent Honduran election and change in president, and the Honduran congress repealing the so-called ZEDE law to undo the ZEDE framework. There is technically a 50-year protection in place, according to the presentations, as the government is supposed to respect the “acquired right,” but as noted by one free city project speaker, the government still controls the men with guns. So, it’s still unclear what happens with these particular ZEDEs/free private city projects as there is expected to be a ratification process taking place next year.

I have sympathy for the people operating, investing and promoting the ZEDEs as they are likely subject to unfair mainstream media treatment. Bitcoiners know this feeling well, as they are subject to being told that “Bitcoin is dead” (for the thousandth time) or that “Bitcoin boils the oceans” (while the mainstream cites a statist central bank blogger with an ax to grind). ZEDE operators seem to want to provide liberty, choice and improved prosperity, from what I could tell.

ZEDEs From A Bitcoin Perspective

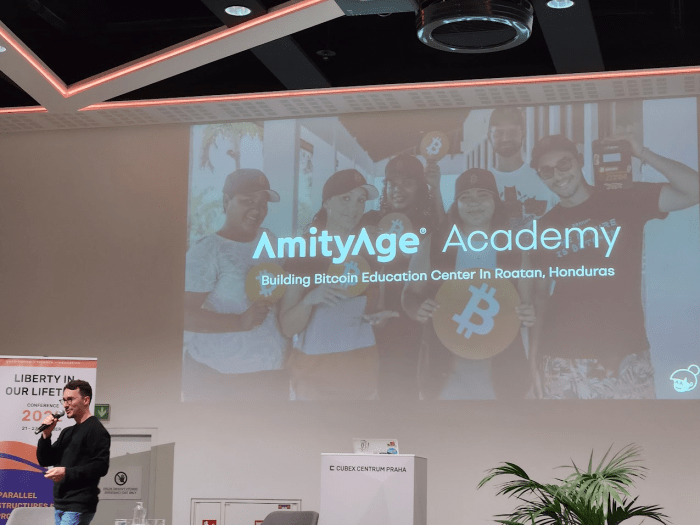

Interestingly for Bitcoiners, Próspera is open in terms of legal tender and there is no capital-gains tax, permitting free spending of bitcoin without accounting and record keeping headaches. Also of note is that the island of Roatán (Próspera is located on this island) also has focused Bitcoiner education.

Dusan Matuska spoke at the conference about his educational efforts with AmityAge Academy, the first Bitcoin education center in Honduras. There are Bitcoin workshops, and restaurants and pubs on the island accepting bitcoin, and even bitcoin education projects and events planned, such as the bitcoin hill run.

Seasteaders

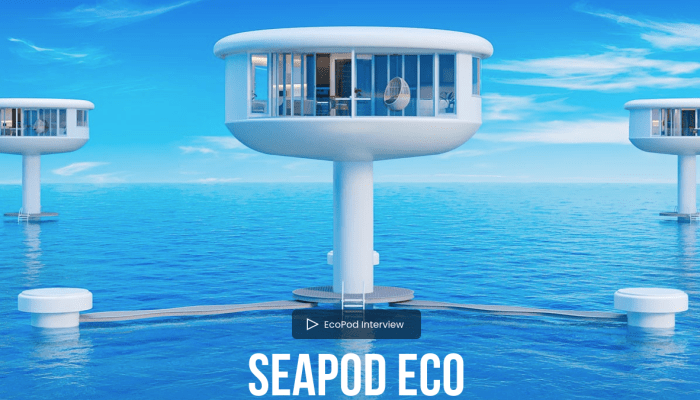

There were some influential people from the seasteading movement presenting as well, such as Patri Friedman, Joe Quirk and others. The tagline I noticed was, “stop arguing. Start seasteading,” which I can understand given the attitude of many statists around the world who proactively stop Libertarians and other free-minded people from having freedom.

If all (or most) of the land on earth is claimed and ruled by statists, is the answer really to go and set up shop on the seas? I saw various approaches and ideas being shared in this way, such as the creation of a SeaPod (or perhaps to be stylized as a “SeaBNB”), which could be set up such that the visitors/inhabitants get a full 360-degree view of the sea.

There were various technological and almost sci-fi ideas shared too, such as the use of drone delivery, helipads and intelligent voice assistants (that don’t “phone home” to Apple, Google, Amazon, etc.).

Separate from the SeaPod, there were also ideas presented on how to gradually create a community of like-minded seasteaders who would first get together in their boats in marinas around the world, and then slowly and gradually shift out in stages, the idea being to form connected floating platforms that permit freer markets out at sea, and to have the ability for people to join, leave or to reconfigure their components of the joint floating platform, all within a free market voluntary context.

Flag theorists

Of course, from the Libertarian world there is “flag theory” and we saw some consultancy services such as Katie The Russian’sPlan B Passport and Staatenlos’ talk about playing the geo-arbitrage game.

This could mean using various kinds of “flags”: citizenships, residencies, business structures, bank accounts, phone service, insurance and various other components to select from choices around the world — instead of being locked into one country. This crowd is, of course, very familiar with using Bitcoin as part of an overall strategy to gain freedom and generally they are comfortable transacting using bitcoin.

Bitcoiners

Of course there were bitcoiners present, too. I gave a talk about some practical tools and examples of people or organizations using Bitcoin as a parallel system.

We also saw some well-known Bitcoiners present and hosting a panel discussion on Madeira, an autonomous region of Portugal. Daniel Prince, Knut Svanholm, Andre Lojas, Jeff Booth (virtually), Greg Foss (virtually) and Lawrence Lepard (virtually) presented on the Free Madeira initiative.

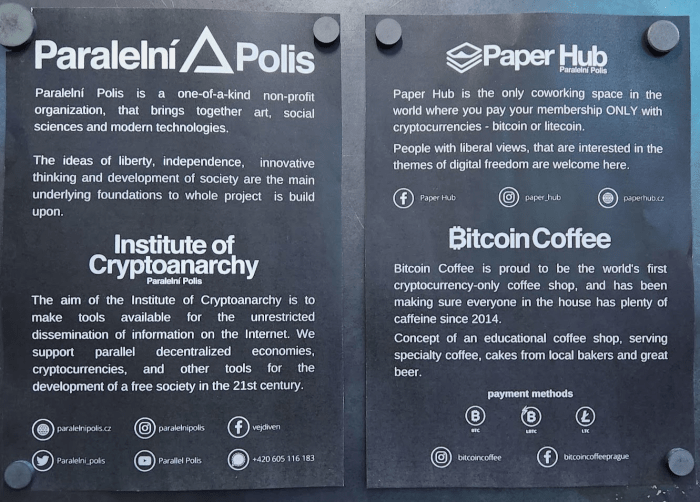

And of course, while in town in Prague, the Bitcoiner crew visited Paralelní Polis, a unique organization known for promoting liberty, and crypto anarchy. There you can pay with bitcoin on chain or through Lightning!

Summing Up

These various projects and methods are additive and helping the overall cause of freedom. For example, the flag theorists are out there encouraging individuals to acquire additional residencies or passports and to play the jurisdictional arbitrage game, this helps reinforce the idea that countries or states have to compete with each other to attract talented individuals or businesses. The creation of new free cities projects also helps provide new opportunities. The seasteading efforts (though perhaps not my cup of tea), are still additive in providing new opportunities for people to express their desire for freedom and to choose a different jurisdiction.

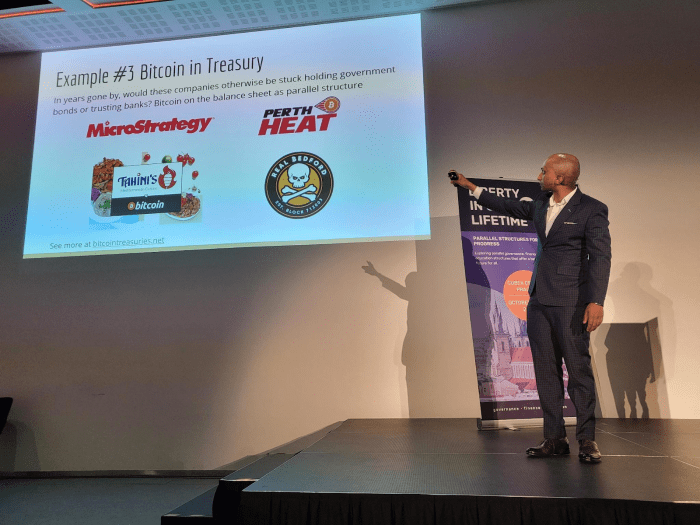

Of course, most powerfully, Bitcoin has a big role to play in enabling these other projects and initiatives to operate, even in spite of fiat banking system resistance. We should all look to ways that we can act more freely, and grow our parallel financial system: Bitcoin.

This is a guest post by Stephan Livera. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Achieving the temperature goals of the Paris Agreement requires not only slowing new construction, but also retiring existing coal power plants early, worldwide. Credit: Wikimedia Commons

Opinion by Philippe Benoit (paris)

Inter Press Service

PARIS, Oct 26 (IPS) – With COP 27 approaching, pressure is mounting on wealthy countries to increase their support to poorer ones in the face of climate change. The recent floods in Pakistan have amplified this issue. China, as the world’s second largest economy, will similarly face increasing pressure to help other developing countries on climate.

At last year’s COP, the Asian Development Bank (ADB) unveiled an innovative program to fund the early retirement of coal power plants by mobilizing capital to buy-out the investors in these plants. This approach has an interesting, and potentially even easier, application to the coal plants financed by China in Pakistan and elsewhere overseas under its Belt and Road Initiative (“BRI”). The key to unlocking this, somewhat surprisingly, lies in the dominance of China’s state-owned companies in BRI transactions.

In response to this challenge, the ADB announced the Energy Transition Mechanism which includes an initiative to buy out existing coal investors to shutter their plants early and thereby avoid the attendant future emissions. Typically, this would involve mobilizing international financing from multilateral development banks, climate funds, etc. to compensate the private sector investors in these plants.

Interestingly, the dominance in the BRI’s overseas projects of China’s state-owned companies creates the opportunity for the Chinese Government to apply the ADB mechanism in a streamlined manner — under what could be called the “BRI Clean Energy Transition Mechanism”. How might this work? Some initial ideas follow.

As noted above, Chinese state-owned financial institutions are the major lenders to the BRI coal power projects in Pakistan. Similarly, Chinese government-owned energy firms are the dominant coal plant owners. It is the financial interests of these various Chinese state-owned lenders and other enterprises (SOEs) that would be affected adversely by any early retirement.

Consequently, under the proposed mechanism, China would be compensating its own SOEs for the revenues they would lose in the future from the early plant retirements in Pakistan. In essence, China would pay itself. This is a unique feature of this BRI coal retirement program that flows from China’s reliance on its own SOEs … and it presents several operational and financial advantages.

The financial arrangements for early retirement should be easier to negotiate and execute since the parties are all affiliated — i.e., the Chinese government, its state-owned banks and other SOEs. This should also reduce transaction costs.

In the ADB’s early retirement context, private sector investors would typically insist on some compensation being paid today for the loss of projected future revenues. In contrast, because the BRI context would involve compensation from the Chinese Government to its own SOEs, the Government could reasonably delay payments till the point at which the SOEs would actually be foregoing revenues. So, for example, if we assume early retirement in 2030 — an interval that would give Pakistan the time to replace the retired coal electricity generation with renewables in an orderly manner (see discussion below) – then the payments by the Chinese Government to its SOE lenders and energy firms could similarly be deferred till that time.

The Government would also, as a practical matter, enjoy significant discretion regarding the level of compensation to be paid to its SOE lenders and energy firms in 2030 and beyond. Notably, the Government could impose a discount on these future payments — especially if it has implemented by that time financial disincentives targeting coal generation (e.g., a carbon price) to support its own carbon peaking and neutrality goals.

The proposed BRI mechanism would resemble in various ways a debt-for-nature swap, notably from the perspective of China as a creditor/donor country. In this BRI “debt-for-coal” swap, China would forego the payments due its SOEs in the future from the operation of these Pakistan coal plants in exchange for the reduced emissions generated by their early retirement. Significantly, this mechanism would produce emissions avoidance benefits without China providing any new overseas funding.

What are some possible motivations for Beijing to launch this type of initiative?

Second, the ability to launch an international climate program that does not require China to disburse funds for the next several years — and, when it does so, to pay its own SOEs — may appeal to the Government, particularly given the current domestic economic stress. This is consistent with other debt-for-nature swap programs advanced by other donor countries where the financial cost to the donor is from foregone revenues, not new funding.

Moreover, the loss in revenues for China and its SOEs from the early BRI coal plant retirements would only take place in 2030 when China’s economy should be markedly larger and more capable of absorbing the expense.

Importantly, Pakistan and other BRI developing countries will need even more electricity to power their economic development. Consequently, the BRI Clean Energy Transition Mechanism needs to include additional funding for new renewables power generation capacity (as is the case under the ADB’s approach).

The extreme climate events of 2022 have increased awareness regarding the vulnerability of poorer countries to climate change and the consequent importance of reducing future emissions. This article sets out a proposal for how China could retire BRI coal plants early in Pakistan and elsewhere that capitalizes on its use of state-owned companies, while supporting more renewables in these countries to reduce the climate change threat and promote sustainable economic growth.

Philippe Benoit has over 20 years working on international energy, climate and development issues, including management positions at the World Bank and the International Energy Agency. He is currently research director at Global Infrastructure Analytics and Sustainability 2050.

My boyfriend owns a house with a 30-year mortgage balance of $150,000 on a 4% interest rate. He has $275,000 in cash and retirement accounts. He is retired.

My house is paid off. I have $50,000 in cash and retirement accounts. I would like to retire within one to two years.

We wish to cohabitate but have not been able to agree on a fair “rent” to pay. He is not willing to live in my house because it has fewer amenities.

“‘He believes I should pay half of his monthly cost at his nicer, more expensive house. He could pay off his mortgage and save $600 a month, but he likes to have cash. ‘”

He believes I should pay half of his monthly cost at his nicer, more expensive house. He could pay off his mortgage and save $600 a month, but he likes to have cash.

I have forgone that luxury and paid off my mortgage. I am now working on building my savings. I don’t feel it is fair for me to pay half of the mortgage interest expense.

I don’t know what repair and maintenance costs should be expected from me, if I have no equity in his house. There are many points of view, none of which feels fair.

These are the options he set forth:

· I live in his house and thus get to rent mine out. Pay him half of what I net from that rental.

· Pay half of the actual costs of living expenses and upkeep on his house while I live there.

· Pay him what I pay to live in my current home for taxes, insurance, and utilities: $800/month.

What say you, Moneyist?

House Owner & Girlfriend

Dear House Owner,

I’m sure your house is just as nice. And just because he believes you should pay half his costs, does not make it so. If you are paying no mortgage on your own home, I don’t believe you should pay one red cent more to live in his home.

That is to say, you should not come out of this arrangement paying more, just because (a) he would like you to live in his home and (b) he would like you to help him pay off his mortgage, or his tax and maintenance.

You both made different choices: Yours was to have a home that’s free-and-clear of a mortgage, so you can spend this time building up your savings for retirement and/or a rainy day.

You have worked hard to pay off your mortgage, and you have $50,000 in savings, less than 20% of your boyfriend’s savings. He has $150,000 left on his mortgage, and that’s his choice.

“If his aim is to find help to pay off half of his mortgage, he can find a tenant to do that for him. ”

You are not the answer to his long-term financial plans, you are his partner in life. If his aim is to find help to pay off half of his mortgage, he can find a tenant to do that for him. What do you expect of you? Forget what he expects.

By the way he is approaching this arrangement, it seems like he wants the equivalent of a detergent and a fabric softener — a girlfriend and a tenant in one handy bottle to keep his financial plans smooth and clean.

Bottom line: You should not compromise any plans to build your nest egg. The lady’s not for turning. Only acquiesce to his plan if — with the help of an actual tenant in your home — it helps you too.

In other words, the desired outcome for you is more important than the suggestions he has put forward. He could save $600 a month! That’s his business. Not yours. What do you want to have in your pocket every month?

Figure out what you want, and then work your way backwards based on that goal. For instance, if you can pay him $800 a month, charge $1,600 rent for your home, and put $800 towards your savings, do that.

You’ve come a long way. Don’t let these negotiations scupper that.

Check out the Moneyist private Facebookgroup, where we look for answers to life’s thorniest money issues. Readers write in to me with all sorts of dilemmas. Post your questions, tell me what you want to know more about, or weigh in on the latest Moneyist columns.

The Moneyist regrets he cannot reply to questions individually.

By emailing your questions, you agree to having them published anonymously on MarketWatch. By submitting your story to Dow Jones & Co., the publisher of MarketWatch, you understand and agree that we may use your story, or versions of it, in all media and platforms, including via third parties.

STOCKHOLM, Oct 26 (IPS) – In his treatise On War, the Prussian general Carl von Clausewitz (1780–1831) stated that war is “merely a continuation of policy with other means”. With his experience from the Napoleonic Wars von Clausewitz knew that totalitarian regimes could end up conducting huge and ruthless military campaigns. Furthermore, he assumed that to win a war it is necessary to mobilize and indoctrinate the inhabitants of an entire nation. Such an endeavour is called total war, a term that actually can be applied to Putin’s war in Ukraine.

Putin came to power during the turbulent times following the collapse of the Soviet Empire. His image as a forceful personality convinced many that Putin could make Russia “safe for democracy and business”. In June 2000, Bill Clinton proclaimed that Putin was “fully capable of building a prosperous, strong Russia, while preserving freedom and pluralism and the rule of law.”

Soon business flourished, satisfying foreign investors eager to enjoy Russia’s vast deposits of natural riches. At the same time, fear of terrorism was boosted by explosions in heavily populated residential areas. Putin’s answer to these assumed terrorist threats was in accordance with von Clausewitz´s advice to use “force unsparingly, without reference to the quantity of bloodshed.” The pursuing escalation of the war in Chechnya, pinpointed as the origin of terrorism in Russia, made Putin a nationalist hero, while his characteristics as teetotaler, capable administrator, quick learner and talented actor made him assume the role of a Hollywood-inspired saviour/hero. He single-highhandedly flew planes and rode bare-chested through the wilderness surrounding Siberian rivers. Media lionised him as a rough and strong judo/black-belt champion capable of leading an entire, long suffering nation onto a straight path to prosperity.

Some worrisome signs were nevertheless written on the wall. In 2004, Putin declared the collapse of the Soviet Union as” the greatest geopolitical catastrophe of the twentieth century.” Meanwhile, his acolytes were amassing the spoils from the collapsed Soviet Empire. Putin supported and protected those oligarchs who backed him, while bankrolling his inner circle.

In Munich 2007, Putin bared his teeth and claws in a speech given at an international Security Conference. He declared that the US was a predatory nation prone to apply an ”almost unconstrained hyper-use of force – military force – in international relations plunging the world into an abyss of conflicts.” This revelation was in 2008 followed by Russia´s military assault on neighbouring Georgia.

General elections were rigged, while some political opponents ended up dead, like Boris Nemtsov, who in 2015 was killed on a bridge close to the Kremlin. Alex Navalny, Putin’s most prominent and fearless opponent, was arrested and imprisoned for thirteen years. Out of jail, he was in 2020 poisoned on a flight to Siberia. Close to dying, he was brought to Germany for expert treatment. After recovering, Navalny went back to Russia, where he was immediately put on trial and imprisoned.

Non-compliant oligarchs were and are routinely harassed. First to be rounded up were those who controlled independent media, like Vladimir Gusinsky and Boris Berezovsky. Both fled the country. In 2013, Berezovsky died ”in suspicious circumstances”. Another oligarch, Mikhail Khodorkovsky, who had funded independent media, was already in October 2003 arrested on board his private jet and imprisoned for ten years.

Putin can now unopposed claim that the belligerent attack on Ukraine was necessary for protecting the Motherland. Subdued Russian media affirm that ruthless Ukrainian leaders have transformed their nation into a pawn in the cynical game of a Superpower intending to subjugate, or even annihilate, the Russian Federation.

It appears as if Putin is not only dedicated to make “Russia great again”. Another goal of his seems to be to enrich himself and his cronies. As a means to cover up his greed, Putin poses as upholder of “strict” morals, based on “pro-life” and traditional “family” values, as well as heroic patriotism and religious fundamentalism. Twenty years after coming to power Putin could declare: “The liberal idea has become obsolete. Liberals cannot simply dictate anything to anyone just like they have been attempting to do over recent decades.”

In spite of the Ukrainian war and his disrespect for human rights, Putin remains an icon for right-wing nationalists. A symbol of defiance to Western Liberal Establishment’s alleged encouragement of mass immigration and affinity to ”multiculturalism”, conceived as attempts to undermine morals and national identities.

As a counterweight to such assumed measures, backward looking politicians around the world pay homage to nostalgic notions, like a lost Great Chinese Tradition, a Russian Empire, Hindu pride before the arrival of Islam, a Global Britain, the Ottoman Empire, etc. This trend is occasionally joined with a global system where ruling elites consider themselves to be unrestrained by international norms, traditional modes of state governance, and democratic decision processes. Some world leaders try to pull the wool over the eyes of their followers by packaging their intents within populist opinions, like despise for political correctness, globalism, investigative journalism, LBTQ rights, feminism and environmental NGOs. A dangerous trend that, if unchecked, might as in the case of Putin´s Russia lead to socioeconomic conflicts degenerating into total war.

In the US, a strengthened adherence to illiberalism was fostered by Donald Trump. Under his watch US politics began to shift from rule-based order to one where might and wealth make right, a message boosted by media like Fox – and Breitbart News. Trump behaved like a wannabe despot, trying to apply authoritarian tactics at home, while paying homage to thugs and dictators abroad. Before him, US presidents had pledged their adherence to human rights, democracy, and freedom of speech. Nevertheless, their governments occasionally supported despots and dictators, not linking concerns for human rights to security, economy and financial affairs. A Realpolitik, which to “friendly” despots indicated that the US did not care so much about repression and corruption within the fiefdoms of their friends. Such behaviour was based on strategic reasons, while Donald Trump appeared to embrace authoritarians because he actually admired them – Dutete, Xi Jinping, Orbán, Erdo?an, Kim Jung-un, and not the least, Putin.

The former US president´s homage to ideas similar to those of Putin and his pose as a nationalistic superman might be connected with his obvious narcissism and appeal to nationalistic extremists. However, his senseless bragging is also combined with greed. A wealth of investigating reporting has demonstrated links between organized crime and corrupt rulers/oligarchs with the Trump Organization’s overseas business connections.

Money is also part of Russian foreign relations. Populist, chauvinistic parties like Italian Lega Nord (currently known as the Lega) and the French Front National (currently Rassemblement National) have received intellectual and economic support from Russia. This support to European political parties may be considered as a Russian effort to secure support for Putin’s policies abroad, as well as locally.

Germany’s former chancellor, Angela Merkel, a fluent Russian speaker far from being a friend of Putin, dismissed him as a leader using nineteenth-century means to solve twenty-first century problems. For sure, Putin’s attack on Ukraine mirrors age-old use of devastating warfare as a radical solution to complicated sociopolitical problems. It seems to be a stalwart application of the two-hundred-years-old advice provided by von Clausewitz:

Philanthropists may easily imagine there is a skillful method of disarming and overcoming an enemy without causing great bloodshed, and that this is the proper tendency of the Art of War. However plausible this may appear, still it is an error which must be extirpated; for in such dangerous things as war, the errors which proceed from a spirit of benevolence are just the worst. As the use of physical power to the utmost extent by no means excludes the co-operation of the intelligence, it follows that he who uses force unsparingly, without reference to the quantity of bloodshed, must obtain a superiority if his adversary does not act likewise. By such means the former dictates the law to the latter, and both proceed to extremities, to which the only limitations are those imposed by the amount of counteracting force on each side.

Putin´s Ukrainian war neglects human suffering and has now disintegrated into a bloody power struggle, where Russia “to the utmost extent” makes use of its military strength, while being supported by “the co-operation” of a propaganda striving to engage the entire Russian population in the war effort.

The Ukrainian war not only concerns the protection of Mother Russia from a “predatory West”, its ultimate goal is to control a hitherto sovereign nation’s politics and natural resources. Putin’s declared support to an allegedly discriminated Russian minority in Luhansk and Donetsk seems to be a subterfuge for grabbing an essential part of Ukraine’s economic resources.

During early 2000s, privatization of state industries yielded a so called Donbas Clan control of the economic and political power in the Donbas region. These oligarchs were supported by Kremlin and a rampant corruption soon took hold of an area dominated by heavy industry, such as coal mining (60 billion tonnes of coal are waiting to be extracted) and metallurgy.

Before Russia in 2014 backed separatist forces in a ferocious civil war, this particular area produced about 30 percent of Ukraine’s exports and a huge amount of gas reserves in the Dnieper-Donets basin was beginning to be extracted. In those days, the most prominent oligarchs in the Luhansk and Donetsk regions were Putin proteges – Rinat Akhmetov and Viktor Yanukovych, the latter had become Ukraine’s President, though his attachment to Russia and conspicuous corruption led to his fall through the Maidan Uprising in 2013, starting point for Ukraine’s transformation into a prosperous nation.

The Maidan Revolution caused a wave of insecurity sweeping through the former Soviet Empire, shaking up corrupt “counterfeit” democracies/dictatorships like Belarus, Azerbaijan, Kazakhstan, Tajikistan, and Uzbekistan. Small wonder that the authoritarian leaders of these nations are stout supporters of Putin’s war in Ukraine.

While reading von Clausewitz’s On War it is quite easy to relate it to Putin’s politics that undeniably have resulted in war as a “continuation of policy with other means.” It is not the first time in history that authoritarian regimes have plunged entire nations into a blood-drained pit of war. All of us have to be be aware that support of authoritarian regimes might lead us all down into Hell.

Main Sources: Klaas, Brian (2018) The Despot´s Accomplice: How the West is Aiding and Abetting the Decline of Democracy. London. Hurst & Company. von Clausewitz, Carl (1982) On War. London: Penguin Classics.

NEW YORK, Oct 26 (IPS) – Held in-person for the first time in three years, the annual meetings of the International Monetary Fund and World Bank last week in Washington, D.C. failed to offer solutions to the dozens of developing countries in debt distress or on the forewarned global recession instigated by monetary tightening.

Meanwhile, austerity measures are reinforced through a repeated emphasis on fiscal tightening, underpinned by a monetarism upheld by the IMF and rich country central banks.

The scenario of a dual tightening in both monetary and fiscal policy is only exacerbated by the absence of political will among creditors to cooperate in debt restructuring, bolstered by narratives of losing market access to financial flows.

New loan programs are created by the IMF to boost concessional financing for food price shocks, climate transitions and liquidity shortfalls. However, these very loans create new debt and reinscribe the very austerity measures that worsen the challenges of inflation and climate.

Within these asymmetries of power and access in the world economy, and the foreclosing of developmental policy tools for developing countries, what then is the fate of the vast majority of people and nations in the world?

The IMF’s World Economic Outlook warned of an imminent recession amidst a shift of financial regime from cheap and easy money to an aggressive synchronization of global monetary tightening.

“In short, the worst is yet to come, and for many people 2023 will feel like a recession,” said IMF Chief Economist Pierre-Olivier Gourinchas. Convening the world’s finance ministers, central bank governors, and financial market leaders, the IMF announced a slowdown in global growth by 2.7%, down from the 3.2% growth projected for this year.

On the heels of a global pandemic followed by the war in Ukraine, the US Federal Reserve’s interest rate hikes, aimed toward domestic price stability, is creating a global push toward more expensive money.

A stronger dollar, higher international and domestic interest rates, coupled with depreciating currencies and sell-offs in many developing country assets, is generating protracted economic and social pain across the globe.

The spillover impacts are seen in soaring food and fuel prices, increases in dollar-denominated debt and imports costs, volatile commodity markets and debt distress intensifying into a 50-year record across the developing world.

The UN’s 2022 Trade and Development Report warns that the most vulnerable countries and communities are being hit the hardest. Warnings of another ‘lost decade’ abound, in that the current interest rate hikes resemble those of 1979-82, which triggered debt crises in over 40 developing countries where ‘structural adjustment programs’ through IMF loans contributed to a decade of lost growth and development across the Global South.

The tightrope global central banks are walking is acknowledged by IMF Managing Director, Kristalina Georgieva, who says, “Not tightening enough would cause inflation to become de-anchored and entrenched — which would require future interest rates to be much higher and more sustained, causing massive harm on growth and massive harm on people.

On the other hand, tightening monetary policy too much and too fast — and doing so in a synchronized manner across countries — could push many economies into prolonged recession.”

Meanwhile, the topline recommendation of the IMF’s Global Financial and Stability Report is that “central banks must act resolutely to bring inflation back to target.” Doing otherwise would risk credibility and market volatility, or in other words, create difficulties in market access to financial and investment flows and/or worsen borrowing terms.

One of the central tenets of neoclassical economic consensus among global central banks is that of maintaining price stability through a low inflation target of 2%. Financial rulemakers have for decades deemed inflation a threat to economic growth by way of the specter of hyperinflation. However, empirical evidence points to the contrary.

Collating data from 31 countries from 1961-94, World Bank chief economist Michael Bruno and William Easterly concluded that the inflation does not lead to lower growth, even when the significant oil price increase of 1974-75 is included.

The US Federal Reserve’s own historical archives demonstrate that the so-called ‘Great Inflation’ of 1965-82 did not harm growth either. In light of these studies by neoclassical economists and central bank institutions, economists Anis Chowdhury and Jomo Kwame Sundaram argue that “there is no empirical basis for setting a particular threshold, such as the now standard 2% inflation target – long acknowledged as ‘plucked from the air.’”

From press conferences to panel speeches, the IMF leadership repeats that the danger of “entrenched” inflation requires a global commitment to tackle it head on through global to domestic monetary tightening.

This stems in large part from a belief that once inflation begins, it has an inherent tendency to accelerate. Consequently, IMF loans and surveillance recommend central bank independence (from the executive) as a means to ensure unbiased financial policymaking, while critics contend that it has only enhanced the influence and power of big banks and financial actors, largely at the expense of the real economy.

However, history again demonstrates that inflation does not accelerate easily, even when workers have more bargaining power, or wages are indexed to consumer prices – as in some countries.

Lost decade redux?

The IMF’s Fiscal Monitor, published on October 12, called upon all policymakers to “maintain a tight fiscal stance, so that fiscal policy does not work at cross-purposes with monetary policy.” In essence, fiscal policy must serve monetary policy in its “fight against inflation,” by retrenching public spending for the singular objective of sending “a powerful signal that policymakers are aligned in the fight against inflation.”

The rationale is straightforward: “In a time of high inflation, policies to address high food and energy prices should not add to aggregate demand.” Increased demand is anathema, as it “forces central banks to raise interest rates even higher.”

The fiscal tightening is not new. In 2021, 131 governments started scaling back public spending. The geographic and population scale of austerity cuts is expected to intensify up to 2025.

Governments are implementing, or discussing, a range of fiscal adjustment policies, such as targeting social protection, regressive taxation, reducing public expenditure in social sectors, eliminating subsidies, privatizing public services or State-Owned Enterprises, pension reforms, labor flexibilization.

All have long histories of negative social impacts on economic and social rights, such as the right to food, water, health, housing, education, and livelihoods. The human impact will reach over 6 billion people, or 85% of humanity, in 2023.

In a time of poly-crisis, retrenching public spending and imposing regressive taxes that disproportionately hurt the poor, especially women, not only extinguishes the hope of achieving the Sustainable Development Goals by 2030, but more fundamentally, regresses decades of fighting poverty.

Meanwhile, the IMF’s Board has approved the creation of two new loan facilities, the new Food Shock Window, available for a year to countries reeling from the global food price crisis, and the Resilience and Sustainability Trust (RST), through which many rich countries may re-channel their unused Special Drawing Rights if the funds are used to address “external shocks, including climate change and pandemics” by rules set out by the Fund.

While both loans address urgent threats, they also create new debt. The RST is also conditional upon an IMF loan program hinged on fiscal consolidation.

The severity of the food crisis warrants aid in the form of grants not loans. Based on prior research done by the World Bank and Center for Global Development on food price spikes, Oxfam estimates that another 65 million people could be pushed below the $1.90 extreme poverty line as a consequence of food price increases.

Debt crises nearing point of no return

Despite the imminent threat of a debt crises imploding across many developing countries, sovereign debt solutions, the Group of 20, IMF, World Bank as well as the Institute of International Finance, the consortium of private financial actors, have to date failed to create viable solutions.

The G20’s Debt Service Suspension Initiative, which suspended debt payments for 73 low-income countries, was terminated at the end of 2021. And two years after the Common Framework was established in 2020, it’s multiple flaws have led even the World Bank to call it a ‘slow-motion debt tragedy.’

One key dilemma is the lack of political will to enforce a comparability of treatment, where all creditors, including private, participate on equivalent terms or restructuring and in the principle of burden sharing. Another challenge is the glacial pace of restructuring is not only protracted but also riddled with uncertainty.

Middle-income countries, where the vast majority of the world’s poor reside and where serious debt defaults are taking place, are not included. Low-income countries fear that access to commercial financing will be cut off if they apply to the Common Framework, as evidenced by Fitch and S&P slashed Ethiopia’s sovereign rating when the nation applied to the Common Framework in 2021.

Out of the three countries that have so far asked for their debt to be treated – Chad, Ethiopia and Zambia – only Zambia has seen some forward movement.

The narratives coming from within the IMF reiterate a subservience to market access and creditor interests. Across panels and webinars, senior level IMF staff remarked that a large debt restructuring is a serious event, which may result in a decrease of future multilateral and private financing, in amounts that outweigh the financing gained in relief or restructuring.

Some warned that private creditors will not participate in debt restructuring where national fiscal instability reigns. To secure market access, countries have to tighten fiscal belts even more. The logic here is that financial stability imperative for accessing private credit requires fiscal consolidation that generates social devastation.

The lack of official creditor participation and the dilemma of transparency, referring in large part to China, was repeatedly stressed as a key problem. At the same time, an old and wholly condescending trope of the need to increase debtor discipline in light of its financial mismanagement and irresponsibility repeatedly emerged.

Meanwhile, there is no mention of the often-legalized corruption of private actors, such as tax evasion and avoidance, speculative and/or rigged trading. Amidst the talk, actual debt solutions are in omission. While political will is already in short supply, the lack of cooperation toward problem-solving is exacerbated by the finger-pointing between the creditor groups of bilateral, private, and multilateral.

History has repeatedly illustrated the way forward on debt, and the waves of austerity that it generates. For decades, advocates and policymakers alike have called for a transparent and binding debt workout mechanism within a multilateral framework for debt crisis resolution, in a process convening all creditors.

The UN General Assembly has adopted multiple resolutions calling for such a mechanism over the years. Debt justice movements from across the developing world have urged for the cancellation of all unsustainable and illegitimate debts in a manner that is ambitious, unconditional, and without repercussions for future market access.

Past cases show how reducing debt stock and payments allow for countries to increase their public financing for urgent domestic needs.

The principle of burden-sharing ensures genuine debt relief, as does the commitment to include all creditors in an automatic or orderly way. Recognizing that multilateral institutions account for around one-third of the outstanding debt of low- and lower-middle-income countries, the World Bank and IMF must participate in such efforts.

They should both cancel debt payments owed, and the IMF should eliminate surcharges. Protection needs to be provided to debtor states against holdouts and lawsuits by non-participating creditors, while laws and procedures for responsible borrowing and lending need to be ensured to protect citizens and communities against corrupt, predatory and odious debts.

Last but not least, an automatic mechanism for a debt standstill in the wake of an extreme exogenous shock should be created. As proposed by the G77 group of developing countries in the UN General Assembly in response to the global financial crisis of 2007-8, such a mechanism must “be established for a determined period in response to external catastrophe events, as climate and natural disasters, health pandemic, military conflict and inflation.” The prescience of the G77 group in 2009 offers a salient message.

While the developing world has little recourse but to ‘dance to the tune of the Federal Reserve,’ the devastating toll of the human, social and economic crisis must be addressed through tools and choices that can be generated.

The question is how to muster political will, be it from the moral pressure of global justice movement to analysis of the effects that soaring poverty and intensifying climate change will have on the very survival of our planet and species.

Bhumika Muchhala is development economist and senior advocate on economic governance at Third World Network. She works on research, analysis, advocacy and public education on the international political economy of development, feminist economics and decolonial theory and approaches.

This is an opinion editorial by Kelly Slaughter, an associate professor of professional practice at the Neeley School of Business at Texas Christian University.

With elections coming up next month, it’s almost impossible to find common ground between liberals and conservatives. But there’s one subject that should unite red and blue voters: keeping bitcoin free from government regulation.

To make this case, compare bitcoin to a potential central bank digital currency (CBDC), currently being explored per a recommendation from a recent White House report. A CBDC fails to provide all the benefits of bitcoin while introducing new risks.

The attraction of bitcoin and other cryptocurrencies is that they are not subject to central decision-making. With a CBDC, the government could freeze digital accounts. As a replicated system, transactions between bitcoin holders cannot be restricted. Inspired by the same fear of having the accessibility of your assets at the whim of whichever party is in power, red and blue should agree to the benefits of a platform without a selective “off” button.

The White House report states a CBDC could promote financial inclusion and equity by enabling access for a broad set of consumers. Bitcoin is better positioned to do this. Roughly 5% of U.S. households are “unbanked,” which is to say they have no savings or checking accounts. The top two reasons for being unbanked are the inability to meet minimum requirements and a lack of trust in banks. Bitcoin requires no minimum balance and does not require trust in a governing institution.

Indeed, bitcoin’s most significant adoption is in poorer countries with high rates of unbanked households and high institutional distrust. The social good possibilities such as direct transfers are immense. Liberals and conservatives may come at this subject from different perspectives but both see the value in providing a financial infrastructure for those without.

Bitcoin is the most transparent financial system ever introduced and no central authority decides what is transparent and what is not made public. Anyone can access historical and current Bitcoin data. Even the code running Bitcoin is open for public review, including what changes were made and when.

The opportunities for leveraging this transparency are immense. What if you paid your taxes to a government bitcoin address? What if vendors were paid in bitcoin? What if the government and vendors had to share their addresses publicly? We would have the most financially transparent government ever conducted, answerable to both blue and red sides of the aisle.

There are a number of legitimate criticisms directed towards bitcoin. Regarding energy use, proponents and critics agree that a reduction in energy use is a worthwhile pursuit. We can then recognize the progress being made in transitioning to green mining.

What of the grift and illegal activities? Bitcoin proponents are keen to wrest this type of activity out of the system (though to be fair, what is the standard for an honest system? Are we asking more of Bitcoin than other systems?). While transparency alone can work against dishonest activity as seen in the legalseizure of cryptocurrency, many Bitcoin proponents want to work with the government to introduce reasonable regulations.

Bitcoin experiences significant volatility and speculation. This is not behavior we want in a currency and an issue recognized by all bitcoin advocates. But we analyze bitcoin from a 2022-based perspective as if the nature of money is static. In our country’s history, we have accepted foreign currency for official spending and allowed banks to print their own currency. The idea of what money does and how it behaves evolves. Bitcoin is a bit over a decade old and, if allowed, will also evolve based on our technical, economic and social preferences.

Bitcoin is not a replacement for the U.S. dollar, it is an alternative. We accept that USD is an alternative currency, officially and by custom, across the globe. Barter without a currency at all is still legal. We recognize a number of ways for people to transact. Both red and blue parties recognize the value of having financial options — bitcoin is another option with unique benefits.

Bitcoin opponents argue that bitcoin has no intrinsic value, unlike a fiat currency that is backed by the government. But what is our government but an agreement among citizens? Accordingly, citizens have the power of agreement in recognizing bitcoin as a means of transacting. With supporters on the right and the left, let’s agree to let bitcoin continue to evolve as a voluntary way for parties to choose to conduct business.

This is a guest post by Kelly Slaughter. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Opinion by Jomo Kwame Sundaram, Anis Chowdhury (sydney and kuala lumpur)

Inter Press Service

SYDNEY and KUALA LUMPUR, Oct 25 (IPS) – Widespread adverse reactions to the UK government’s recent ‘mini-budget’ forced new Prime Minister Liz Truss to resign. The episode highlighted problems of macroeconomic policy coordination and the interests involved.

Macro-policy coordination

But macroeconomic, specifically fiscal-monetary policy coordination almost became “taboo” as central bank independence (CBI) became the new orthodoxy. It has been accused of enabling CBs to finance government deficits. Critics claim inflation, even hyperinflation, becomes inevitable.

Anis ChowdhuryGovernment finance ministries and CBs are the two main macroeconomic policy protagonists. Poor ‘macro-policy’ coordination has generated problems, including contradictory policy responses. This has meant more macroeconomic and financial instability, worrying markets and investors.

Fiscal policy – notably variations in government tax and spending – mainly aims to influence long-term growth and distribution. CB monetary policy – e.g., variations in short-term interest rates and credit growth – claims to prioritize price and exchange rate stability.

By the early 1990s, the ‘Washington consensus’ implied the two macro-policy actors should work independently due to their different time horizons. After all, governments are subject to short-term political considerations inimical to monetary stability needed for long-term growth.

Claiming to be “technocratic”, CBs have increasingly set their own goals or targets. CBI has involved both ‘goal’ and ‘instrument’ independence, instead of ‘goal dependence’ with ‘instrument independence’.

CBI was ostensibly to avoid ‘fiscal dominance’ of monetary policy. Meanwhile, government fiscal policy became subordinated to CB inflation targets. For former Reserve Bank of Australia Deputy Governor Guy Debelle, monetary policy became “the only game in town for demand management”.

Debelle noted that except for rare and brief coordinated fiscal stimuli in early 2009, after the onset of the global financial crisis, “demand management continued to be the sole purview of central banks. Fiscal policy was not much in the mix”.

Jomo Kwame SundaramSub-optimal outcomes

But more than three decades of “divorce” between independent CBs and fiscal authorities have failed to deliver its promised benefits. Instead, monetary policy dominance has worsened financial instability.

Adam Posen found the costs of disinflation, or keeping inflation low, higher in OECD countries with CBI. Carl Walsh found likewise in the European Community.

For Guy Debelle and Stanley Fischer, CBs have sought to enhance their credibility by being tougher on inflation, even at the expense of output and employment losses.

Committed to arbitrary targets, independent CBs have sought credit for keeping inflation low. They deny other contributory factors, e.g., labour’s diminished bargaining power and globalization, particularly cheaper supplies.

John Taylor, author of the ‘Taylor rule’ CB mantra, concluded CB “performance was not associated with de jure central bank independence”. De jure CB independence has not prevented them from “deviating from policies that lead to both price and output stability”.

The de facto independent US Fed has also taken “actions that have led to high unemployment and/or high inflation”. As single-minded independent CBs pursued low inflation, they neglected their responsibility for financial stability.

CBs’ indiscriminate monetary expansion during the 2000s’ Great Moderation enabled asset price bubbles and dangerous speculation, culminating in the global financial crisis (GFC).

Since the GFC, “the financial sector has become dependent on easy liquidity… To compensate for quantitative easing (QE)-induced low return…, increased the risk profile of their other assets, taking on more leverage, and hedging interest rate risk with derivatives”.

Independent CBs also never acknowledge the adverse distributional consequences of their policies. This has been true of both conventional policies, involving interest rate adjustments, and unconventional ones, with bond buying, or QE. All have enabled speculation, credit provision and other financial investments.

They have also helped inefficient and uncompetitive ‘zombie’ enterprises survive. Instead of reversing declining long-term productivity growth, the slowdown since the GFC “has been steep and prolonged”.

Dire consequences

The pandemic has seen unprecedented fiscal and monetary responses. But there has been little coordination between fiscal and monetary authorities. Unsurprisingly, greater pandemic-induced fiscal deficits and monetary expansion have raised inflationary pressures, especially with supply disruptions.

This could have been avoided if policymakers had better coordinated fiscal and monetary measures to unlock key supply bottlenecks. War and economic sanctions have made the supply situation even more dire.

Government debt has been rising since the GFC, reaching record levels due to pandemic measures. CBs hiking interest rates to contain inflation have thus worsened public debt burdens, inviting austerity measures.

Thus, countries go through cycles of debt accumulation and output contraction. Supposed to contain inflation, they adversely impact livelihoods. Many more developing countries face debt crises, further setting back progress.

Needed reforms

Sixty years ago, Milton Friedman asserted, “money is too important to be left to the central bankers”. He elaborated, “One economic defect of an independent central bank … is that it almost invariably involves dispersal of responsibility… Another defect … is the extent to which policy is … made highly dependent on personalities… third … defect is that an independent central bank will almost invariably give undue emphasis to the point of view of bankers”.

Thus, government-sceptic Friedman recommended, “either to make the Federal Reserve a bureau in the Treasury under the secretary of the Treasury, or to put the Federal Reserve under direct congressional control.

“Either involves terminating the so-called independence of the system… either would establish a strong incentive for the Fed to produce a stabler monetary environment than we have had”.

Undoubtedly, this is an extreme solution. Friedman also suggested replacing CB discretion with monetary policy rules to resolve the problem of lack of coordination. But, as Alan Blinder has observed, such rules are “unlikely to score highly”.

Effective fiscal-monetary policy coordination requires appropriate supporting institutions and operating arrangements. As IMF research has shown, “neither legal independence of central bank nor a balanced budget clause or a rule-based monetary policy framework … are enough to ensure effective monetary and fiscal policy coordination”.

Although rules-based policies may enhance transparency and strengthen discipline, they cannot create “credibility”, which depends on policy content, not policy frameworks.

For Debelle, a combination of “goal dependence” and “instrument or operational independence” of CBs under strong democratic or parliamentary oversight may be appropriate for developed countries.

There is also a need to broaden membership of CB governing boards to avoid dominance by financial interests and to represent broader national interests.

But macro-policy coordination should involve more than merely an appropriate fiscal-monetary policy mix. A more coherent approach should also incorporate sectoral strategies, e.g., public investment in renewable energy, education & training, healthcare. Such policy coordination should enable sustainable development and reverse declining productivity growth.

As Buiter urges, it is up to governments “to make appropriate use of … fiscal space” created by fiscal-monetary coordination. Democratic checks and balances are needed to prevent “pork-barrelling” and other fiscal abuses and to protect fiscal decision-making from corruption.

This is an opinion editorial by Kevin Murcko, CEO and founder of Coinmetro.

On October 12, 2022, I was honored to speak at Bitcoin Amsterdam’s panel session titled “FATF And The Threat To Bitcoin Privacy.” With my fellow speakers, we dove into the evolving role of the Financial Action Task Force (FATF), and its relationship to Bitcoin. It’s so important that we understand both sides of the argument if we are to create a world where both the ideological and the practical implementation of Bitcoin will match the original intentions outlined in Satoshi Nakamoto’s now-famous white paper.

As an overview, the FATF was created in 1989 by the G7 to gather data on money laundering, almost 20 years prior to the birth of Bitcoin. As time went on, the FATF evolved into a policing body tackling all illicit money movements. During this time frame, Bitcoin came into creation and moved into the mainstream with the launch of regulated exchanges and wallets. The co-existence of the FATF and Bitcoin throws up one of the most recurrent and contentious debates around cryptocurrencies: Whether they should be regulated.

The conference brought together less-than-popular arguments for working with legislators and regulators, with those of a technologist detailing the solutions evolving to solve regulatory issues, and welcomed insights from ideologues, arguing that the regulation of cryptocurrency service providers goes against its core concept of sovereign currency and privacy.

Seeing such diversity of opinions in one room made me reflect on the evolution of Bitcoin conferences themselves. I myself have been on stages and at meetups since the beginning of Bitcoin, and I notice how the dialogue within the sector has expanded. In their nascent days, conferences were all about ideology. Bitcoin was far less monetarily valuable and had very few use cases. So, discussions had to be led by the ideology of the change-makers looking to better financial markets and give people back their sovereignty when it comes to their money. That’s an amazing ideology, and it’s an ideology that hasn’t been lost.

But beyond ideology, to get where we are today, bitcoin and the Bitcoin network have matured and taken on more use cases. They have become full-fledged platforms and businesses with loyal consumer bases. And with this, comes an increased duty to the customer and the financial landscape in which they exist.

Hosting Bitcoin Amsterdam today, at a time when Bitcoin prices are not at an all-time high, is an important reminder of the average Bitcoin user’s conviction. If Bitcoin was at record value, we’d have unanimous support for the self-sovereignty ideology. Many of the people speaking at Bitcoin Amsterdam have not experienced losses recently — they have been in the game far longer and therefore are still in profit. But, most users are not in this position and the average consumer is still acutely aware of the volatility that comes with the currency. The “crypto winter” ushered in a consideration of what is preventing the mass global adoption of bitcoin, and how this can be overcome to attract a new wave of bitcoin users. This dip has prompted discussions of the business, regulatory and technological side of the digital currency, looking at practical ways to improve these facets.

However, given ideology is so central to Bitcoin, conversations are rarely had without reverting to its key tenets.

Sitting on the panel at Bitcoin Amsterdam, I sat in the middle of these diverse speakers, literally and figuratively. To me, all stakeholders want the same outcome. We all believe there should be a choice between using government-controlled currency and centralized payment vehicles and opting for channels that are run by a consensus model, in which users have self-sovereignty and are able to operate outside of the traditional powerhouses that run the world. In this world, there still needs to be oversight, because at the end of the day, nobody wants to see funds move into the hands of illicit, violent actors.

My own perspective is that change must start from the inside not from the outside. Many players, in the larger cryptocurrency space and in traditional finance, may see the regulator as an obstacle. But, we live in a world that requires law and order. And while the regulatory system is flawed, the only way to fix it is from within, having experienced its pain points firsthand.

In order to make a convincing case that commands the respect of traditional global finance, the Bitcoin community has to prioritize unity. All market players, be it exchanges, wallet providers or DeFi products, big or small, need to make their voices heard by engaging with regulators and legislators to educate them directly. Having our common end goal in mind, it is far easier to fight from the inside by sitting in one room with a dozen of regulators than trying to educate every single person on the planet about the virtues of Bitcoin and drive mass adoption that way.

Overall, the panel was a great opportunity to share my thoughts and views on the industry as it stands today. Yes, the Financial Action Task Force will continue to do everything it can to combat money laundering and illicit transactions, but if it continues to dictate the rules without the Bitcoin community at the table, the end result will not be what any of us want, ideologically or otherwise.

This is a guest post by Kevin Murcko. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.

Might the bear market’s losses at its recent low have gotten so bad that it was actually good news?

Some eager stock bulls I monitor are advancing this convoluted rationale. The outline of their argument is that when things get bad enough, good times must be just around the corner.

But their argument tells us more about market sentiment than its prospects.

At the market’s recent closing low, the S&P 500 SPX, +1.19%

had dropped to 25% below its early-January high. According to one version of this “so-bad-it’s-good” argument, the stock market in the past was a good buy whenever bear markets fell to that threshold. Following those prior occasions, they contend, the market was almost always higher in a year’s time.

This is not an argument you’d normally expect to see if the recent low represented the final low of the bear market. On the contrary, it fits squarely within the third of the five-stage progression of bear market grief, about which I have written before: denial, anger, bargaining, depression and acceptance.

With their argument, the bulls are trying to convince themselves that they can survive the bear market, rationalizing that the market will be higher in a year’s time. As Swiss-American psychiatrist Elisabeth Kübler-Ross put it when creating this five-stage scheme, the key feature of the bargaining stage is that it is a defense against feeling pain. It is far different than the depression and eventual acceptance that typically come later in a bear market.

Though not all bear markets progress through these five stages, most do, as I’ve written before. Odds are that we have two more stages to go through. That suggests that the market’s rally over the past couple of weeks does not represent the beginning of a major new bull market.

Numbers don’t add up

Further support for this bearish assessment comes from the discovery that the bulls’ argument is not supported historically. Only in relatively recent decades was the market reliably higher in a year’s time following occasions in which a bear market had reached the 25% pain threshold. It’s not a good sign that the bulls are basing their optimism on such a flimsy foundation.

Consider what I found upon analyzing the 21 bear markets since 1900 in the Ned Davis Research calendar in which the Dow Jones Industrial Average DJIA, +1.34%

fell at least 25%. I measured the market’s one-year return subsequent to the day on which each of these 21 bear markets first fell to that loss threshold. In seven of the 21 cases, or 33%, the market was lower in a year’s time.

That’s the identical percentage that applies to all days in the stock market over the past century, regardless of whether those days came during bull or bear markets. So, based on the magnitude of the bear market’s losses to date, there’s no reason to believe that the market’s odds of rising are any higher now than at any other time.

This doesn’t mean that there aren’t good arguments for why the market might rise. But the 25%-loss concept isn’t one of them.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com.

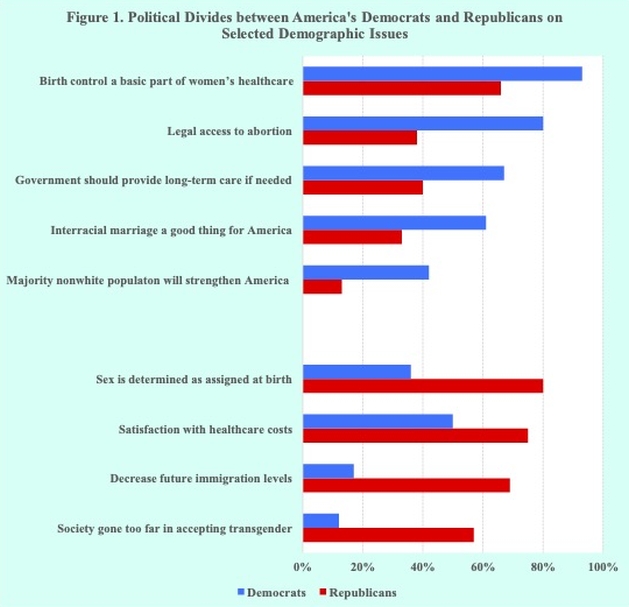

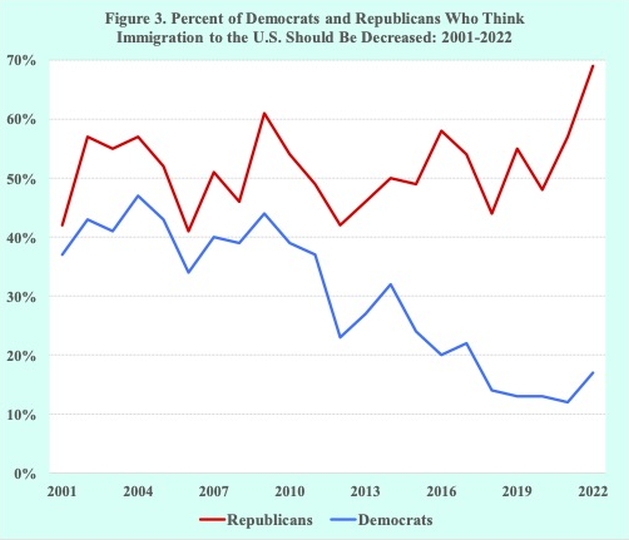

Republicans in general favor less immigration than Democrats. For example, a national Gallup poll in July 2022 found that the proportion saying immigration to America should be decreased was 69 percent among Republicans versus 17 percent among Democrats. Credit: Guillermo Arias / IPS

Opinion by Joseph Chamie (portland, usa)

Inter Press Service

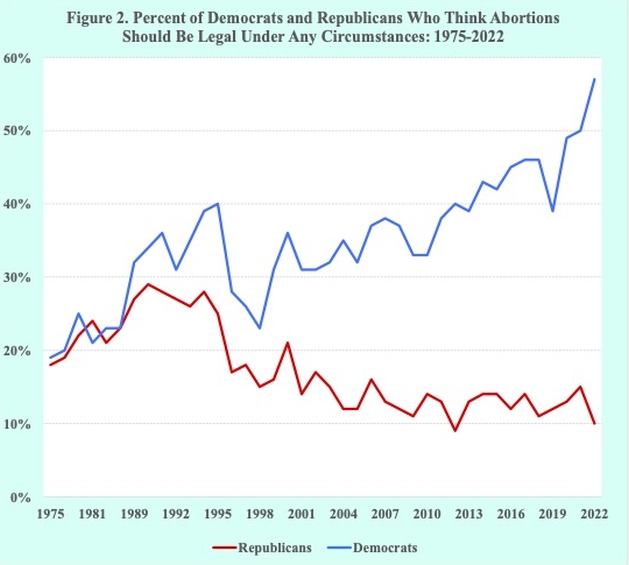

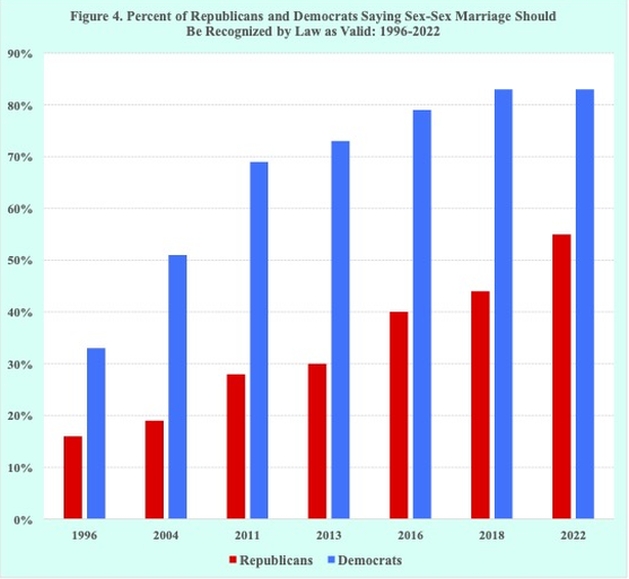

PORTLAND, USA, Oct 24 (IPS) – Given the upcoming midterm elections in the United States and the consequences of the outcome for domestic legislation and programs as well as the country’s foreign policy, it’s useful and fitting to review fundamental differences between America’s two major political parties on vital demographic issues.

On virtually every major demographic issue, including reproduction, mortality, immigration, ethnic composition, gender, marriage and population ageing, significant divides exist between the Democrats and Republicans (Figure 1). Those divides have significant consequences and implications for current and future government policies and programs.

Source: Various U.S. public opinion surveys.

Those divides on vital demographic matters, which have become increasingly politicized by the two major parties, are reinforcing political polarization and partisan antipathy across the country and hindering the economic, social and cultural development of the United States.