So, the key questions for most Canadians are: “Do I need to care about this? Is my money safe?” The answers may be: “Probably not. As safe as the Canadian government can make it.”

The activities of SVB, regional banks in the U.S. and even Credit Suisse, are not likely to affect the average Canadian’s finances. There is some noise on the edges when it comes to Canadian banks that have some assets in America, but that’s pretty small potatoes. OFSI is watching closely to reassure everyone. And it’s stepped in to take control over SVB’s $864 million in Canadian assets, as noted above in the first section. It’s also worth looking at the Canadian Deposit Insurance Corporation (CDIC), as it has you covered up to $100,000 per account.

Personally, I feel quite confident in Canadian banks. Their earnings reports from two weeks ago were very solid. Each of the big six Canadian banks reported setting aside increasing amounts of money to cover off risk for situations just like what we’ve seen with SVB and Credit Suisse. There are some positive systemic reasons why Canada has not experienced a banking crisis in a long time. Given the negative headlines concerning all things banking at the moment, it might be an opportune time to get some widespread exposure to Canadian banks via an exchange-traded fund (ETF), like the Horizons Equal Weight Canada Banks Index ETF (HEWB/TSX).

Inflation in the U.S.: Where do we go from here?

Amid all this banking chaos, the U.S. Federal Reserve has a big decision to make next week, in regard to interest rates. More now, than at any other time in the past few decades, has the U.S. Fed been put between a rock and a hard place. If the central bank pauses on raising rates, it’s quite possible we could see a bull market in several assets and see inflation ramp its way back up. If it follows through on its hawkish warnings, we could see more structural problems such as bank runs continue.

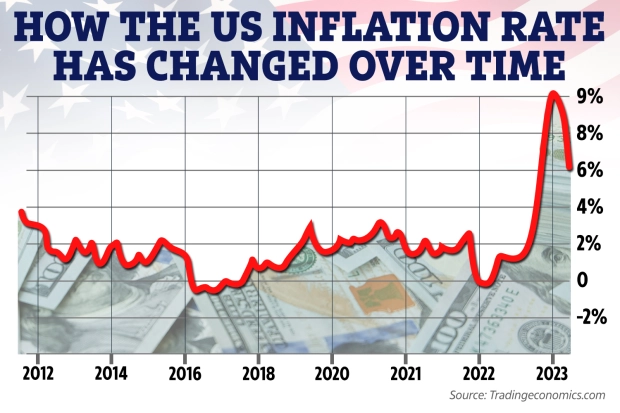

To complicate things more, the recently released U.S. inflation numbers don’t leave decision makers with an easy path. Prices in February were 6% higher than a year ago. That’s down a substantial chunk from January’s 6.4% inflation, and thankfully, way down from June’s 9.1% inflation–but it’s still far above the U.S. Fed’s 2% goal.

Month-to-month core inflation (which strips out volatile food and energy prices) actually ticked upward from January’s 0.4% to February’s 0.5%. The housing sector was responsible for this increase.

A week ago, CME economists suggested a 30%-plus chance that the U.S. Fed would be considering a 0.50% rate hike. Given the recent events, that’s quickly turned around. Now, not only is a 0.25% rate hike the favourited odds, but there is a 28% chance that there may be no rate hike at all!

At the first signs of the Fed reversing monetary direction, stock markets rallied, mortgage rates dropped, and bond markets decided pretty quickly that interest rates would not stay “higher for longer.” Hold on tight for where we are headed from here. For what it’s worth, I continue to believe that Canadian companies and broad Canadian equity index funds are an excellent place to be right now.

Kyle Prevost

Source link