Want more stock market and economic analysis from Phil Rosen directly in your inbox? Subscribe to Opening Bell Daily’s newsletter.

The AI trade isn’t running out of juice just because stock prices are falling.

One day after touching a record high, the Dow tumbled more than 600 points. Meanwhile, AI heavyweights like Nvidia, Alphabet, Broadcom and AMD all closed lower on Thursday.

These moves track with the volatility of the last several weeks. But as Opening Bell Daily readers know, bubble fears have picked up in November even as the demand story underpinning the AI boom becomes more robust.

Indeed, the fact asset prices haven’t climbed despite strengthening fundamentals suggests the recent chop is a near-term reaction that could reflect any number of things — the lack of economic data during the government shutdown, hawkish Fed rhetoric, corporate layoffs, bearish positions from “Big Short” investor Michael Burry.

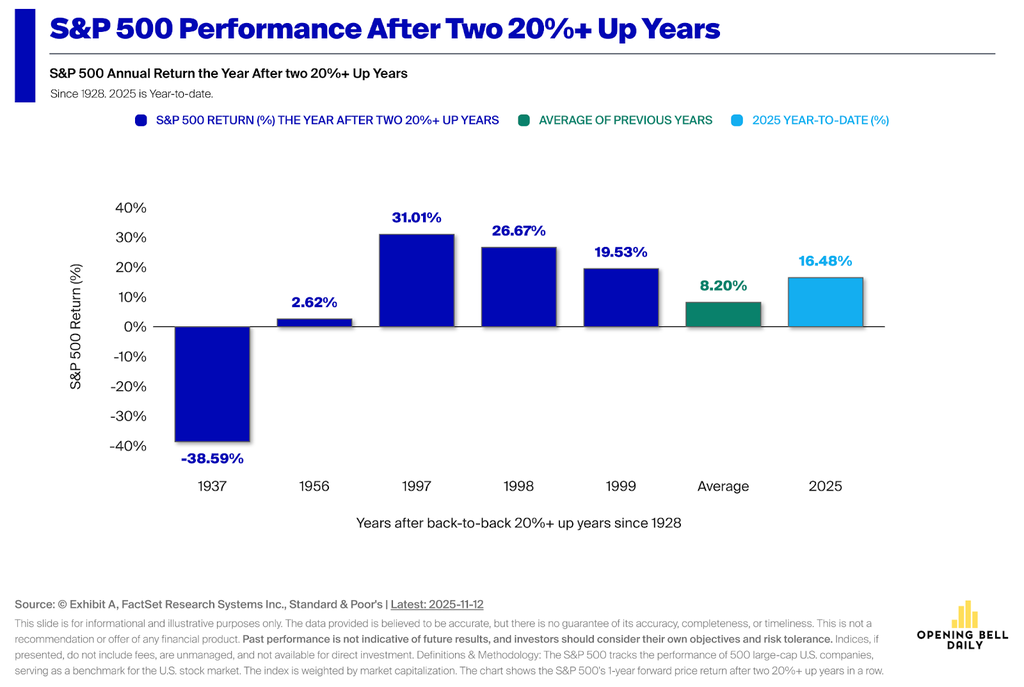

Yet, the money managers and strategists I’ve hosted on my show Full Signal over the last week have remained optimistic for the year ahead.

Todd Sohn, an ETF strategist with Strategas, pointed to narrow credit spreads, historic ETF inflows and falling yields in money market funds as evidence the bull market still has room to run.

Sonali Basak, chief investment strategist at iCapital, said the AI theme remains far from late-cycle, and that the chatter about a “rotation” out of Big Tech is overstated. After all, Big Tech spending looks set to reach $1 trillion annually soon.

“People have been saying ‘rotation’ all year,” she told me. “[But] markets are still near record highs. How much rotation are you really getting?”

Ryan Detrick, chief market strategist at Carson Group, made a similar case, dismissing dot-com parallels and highlighting earnings strength.

“We don’t think this is a bubble,” Detrick told me. “Those big AI and Mag 7 names are actually making a you-know-what amount of money.”

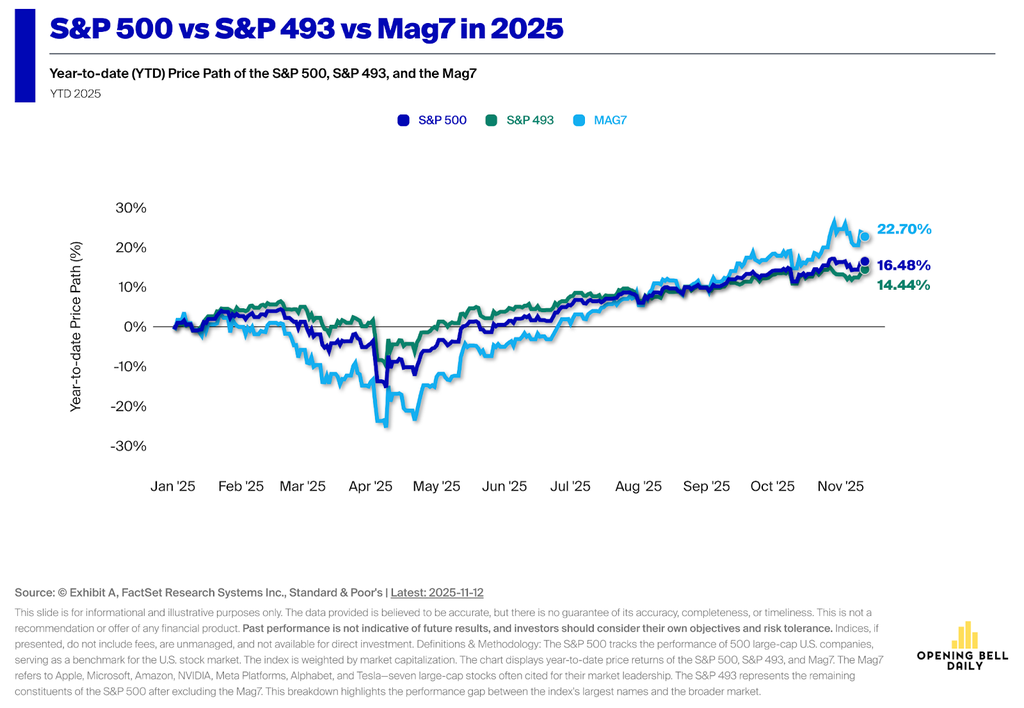

It is true that the largest technology stocks now account for nearly 40 percent of the S&P 500, that Big Tech’s capex plans sound absurd in scale, and that OpenAI’s finances and deal-making remain opaque. But concentration and ambiguity alone don’t constitute a bubble — particularly when earnings and cash flow continue to grow faster than Wall Street expects.

Still, these are reasonable points of unease.

That said, they can coexist with extraordinary and real demand for AI infrastructure. And in what looks like the early innings of the AI economy, the risks appear tied more to short-term volatility and positioning than any kind of systemic collapse.

The early-rate deadline for the 2026 Inc. Regionals Awards is Friday, November 14, at 11:59 p.m. PT. Apply now.

Phil Rosen

Source link